Strategies to Save for Retirement with No Company Retirement Plan

The question, “How much do I need to retire?” has become a concern across generations rather than something that only those approaching retirement focus on. We wrote the article, How Much Money Do I Need To Save To Retire?, to help individuals answer this question. This article is meant to help create a strategy to reach that number. More specifically, for those who work at a company that does not offer a company sponsored plan.

Over the past 20 years, 401(k) plans have become the most well-known investment vehicle for individuals saving for retirement. This type of plan, along with other company sponsored plans, are excellent ways to save for people who are offered them. Company sponsored plans are set up by the company and money comes directly from the employees paycheck to fund their retirement. This means less effort on the side of the individual. It is up to the employee to be educated on how the plan operates and use the resources available to them to help in their savings strategy and goals but the vehicle is there for them to take advantage of.

We also wrote the article, Comparing Different Types of Employer Sponsored Retirement Plans, to help business owners choose a retirement plan that is most beneficial to them in their retirement savings.

Now back to our main focus on savings strategies for people that do not have access to an employer sponsored plan. We will discuss options based on a few different scenarios because matters such as marital status and how much you’d like to save may impact which strategy makes the most sense for you.

Married Filing Jointly - One Spouse Covered by Employer Sponsored Plan and is Not Maxing Out

A common strategy we use for clients when a covered spouse is not maxing out their deferrals is to increase the deferrals in the retirement plan and supplement income with the non-covered spouse’s salary. The limits for 401(k) deferrals in 2021 is $19,500 for individuals under 50 and $26,000 for individuals 50+. For example, if I am covered and only contribute $8,000 per year to my account and my spouse is not covered but has additional money to save for retirement, I could increase my deferrals up to the plan limits using the amount of additional money we have to save. This strategy is helpful as it allows for easier tracking of retirement accounts and the money is automatically deducted from payroll. Also, if you are contributing pre-tax dollars, this will decrease your tax liability.

Note: Payroll deferrals must be withheld from payroll by 12/31. If you owe money when you file your taxes in April, you would not be able to go back and increase your deferrals in your company plan for that tax year.

Married Filing Jointly - One Spouse Covered by Employer Sponsored Plan and is Maxing Out

If the covered spouse is maxing out at the high limits already, you may be able to save additional pre-tax dollars depending on your Adjusted Gross Income (AGI).

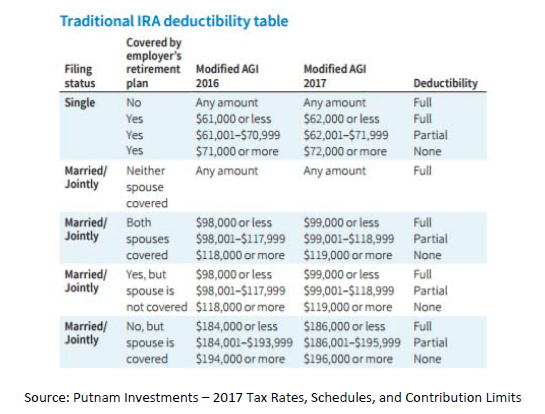

Below is the Traditional IRA Deductibility Table for 2021. This table shows how much individuals or married couples can earn and still deduct IRA contributions from their taxable income.

As shown in the chart, if you are married filing jointly and one spouse is covered, the couple can fully deduct IRA contributions to an account in the covered spouses name if AGI is less than $99,000 and can fully deduct IRA contributions to an account in the non-covered spouses name if AGI is less than $184,000. The Traditional IRA limits for 2017 are $5,500 if under 50 and $6,500 if 50+. These lower limits and income thresholds make contributing to company sponsor plans more attractive in most cases.

Single or Married Filing Jointly and Neither Spouse is Covered

If you (and your spouse if married filing joint) are not covered by an employer sponsored plan, you do not have an income threshold for contributing pre-tax dollars to a Traditional IRA. The only limitations you have relate to the amount you can contribute. These contribution limits for both Traditional and Roth IRA’s are $5,500 if under 50 and $6,500 if 50+. If married filing joint, each spouse can contribute up to these limits.

Unlike employer sponsored plans, your contributions to IRA’s can be made after 12/31 of that tax year as long as the contributions are in before you file your tax return.

Please feel free to e-mail or call with any questions on this article or any other financial planning questions you may have.

Below are related articles that may help answer additional questions you have after reading this.

Traditional vs. Roth IRA’s: Differences, Pros, and Cons

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally , professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, pleas feel free to join in on the discussion or contact me directly.