Will Moving From New York to Florida In Retirement Save You Taxes?

Will moving from NY to FL For Retirement Save You In Taxes

I am getting the question much more frequently from clients - "When I retire, does it make sense from a tax standpoint to change my residency from New York to Florida?". When I explain how the taxes work between New York and Florida, most people are disappointed to find out that it either makes no difference tax wise, or it is less of a difference than they thought. I think too many people wrongly assume that changing your state domicile from New York to Florida is a no-brainer. Whether or not it will have a big impact for you depends on your personal financial situation for retirement. For some individuals, it will save them a lot of taxes, but for most, the tax impact may be minimal. You have to consider:

How Social Security is taxed in NY

The $20,000 NYS exemption on the distributions from retirement accounts

How state pensions are taxed

The property tax breaks in NY once you are over 65

Hidden Medicare cost if you leave New York

How much your NY tax liability would be in retirement

Cost of Living

Estate tax laws

It probably seems like a lot of factors to consider, but all of them should be factored in before you decide to pack up the car and move to Florida for retirement.

How Social Security Is Taxed In New York

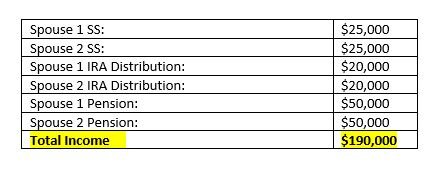

Many people do not realize that when you receive Social Security payments in retirement, it is considered taxable income at the federal level for most individuals. While most individuals will pay federal income tax on their Social Security benefits, you do not have to pay NYS income taxes on social security. If you are married, you and your spouse are each receiving $25,000 for social security, and you do not save any state income taxes on the $50,000 by moving to Florida, since New York does not tax your social security benefits.

NYS Tax Exemption On First $20,000 Distributed From Retirement Accounts

If you are NYS resident and over the age of 59½, New York does not make you pay state tax on the first $20,000 distributed from a corporate pension, IRA, 401(k) or other retirement plan. Married couples get to double that at $20,000 each for a total of $40,000.

If we build on the social security example above, assume you and your spouse are each getting $25,000 in Social Security, and you can withdraw $20,000 each out of your IRA account without having to pay NYS income tax:

Taxes on Retirement Accounts

So, now you are up to $90,000 in annual income without a dime in income tax paid to New York State.

Taxes on Public Pension

If you have a pension with New York State, local government, federal government, or certain public authorities, you do not have to pay state taxes on that pension income in retirement.

Given that we are based out of Albany, NY, we have a lot of financial planning clients that have pensions through New York State. Building again on the social security and IRA example above, now assume we have a married couple that both worked for New Year State and each have pensions for $50,000 each. They do not have to pay NYS income tax on the pension income, they have no NYS income tax on social security, and no state income tax on the first $20K each out of their NYS 457 Plan or IRA’s.

Taxes on Public Pension

We are now up to $190,000 in annual income with zero dollars paid in NYS income taxes.

Property Tax Credits

It is no secret that New York State has high property taxes compared to other states which can often be one of the larger expenses in retirement after the mortgage is paid off. Most New York residents are familiar with the STAR program which reduces the property taxes for homeowners that make less than $500,000 in income. What many retirees do not realize is that there is something called the “Enhanced STAR” credit once you reach age 65, which can further reduce your school taxes.

However, the income limitation for the Enhanced STAR credit is much lower than the regular STAR program. The extra exemption is limited to individuals age 65 and older making less than $86,000 per year in income. A special note: income from annuities and IRA’s do not count toward the $86,000 income limitation.

While Florida may have lower property taxes compared to New York State, if you can qualify for the Enhanced STAR program, the difference in property taxes may be closer than you think.

SNOW BIRDS: This Enhanced STAR program is a big deal for our clients that are snowbirds that go back and forth from New York to Florida. If you plan to maintain a residence in New York and the have a second house in Florida, if you formally change your state of domicile to Florida, your are no longer Eligible for the STAR program, because you are no longer a New York State resident. So, you think you might be saving property taxes by making this move, but your property taxes for your house in New York could actually go up by thousands of dollars since you are no longer eligible for the STAR credit.

Medicare Consideration

When you retire, what is often the largest expenses for retirees? The answer is healthcare. While New York is known for its higher property taxes and higher income taxes, not many people realize are lucrative health insurance benefits until after they have left the state. When you turn age 65, you typically have to enroll in Medicare, which provides you with your healthcare coverage. But Medicare does not pay for everything, so most individuals will enroll in either a Medicare Supplemental or Medicare Advantage Plan to fill on the cost gaps that Medicare does not cover. Unfortunately, most retirees do not understand the difference between a Medicare Supplemental Plan and a Medicare Advantage Plan.

If you do not know the difference, here is our YouTube Video on the topic: Medicare Supplemental Plans (Medigap) vs Medicare Advantage Plans

Here is a quick summary of the issue: Medicare advantage plans can carry a lower monthly cost but you sign up for a Medicare Advantage Plan, you are no longer covered by Medicare. With Medicare supplemental plans, you are covered by Medicare, and the insurance policy supplements your Medicare coverage. In New York, we have the luxury that each year you can decide whether you want to switch from a Medicare Advantage Plan to a Medicare Supplement Plan and visa versa if your health needs change. That is only allowed in two states right now, New York and Connecticut.

If you were to change your state of domicile from New York to Florida, as soon as you become a Florida resident, you no longer have that option available to you. If you are enrolled in a Medicare Advantage plan, you may not be able to change back to Medicare coverage with a Supplemental Plan in the future if your healthcare need change. That is a big deal in retirement, so you really to analyze what type of coverage you when you make the move to Florida.

What Is Your New Tax State Liability

It is a given that no one likes to pay taxes and we would all like to pay less, but before you go through all of these maneuvers to save taxes, you should quantify how much you are actually saving. For example, let us say we have a marriage couple, and their retirement expenses required them to withdraw $30,000 annually from their retirement accounts over and above the NYS $20K exemption amount. Ignoring for now any standard deduction for tax purposes, they would have a New York State tax liability of approximately $2,200. So you have to ask yourself the question, “Is moving to Florida worth saving $2,200 per year in taxes?”.

Cost of Living

There are a few other factors that should be considered in this decision. The first being the difference in the cost of living between New York and Florida. It is not uncommon for the cost of living to be lower in the southern states compared to the northeaster so your retirement dollar may go further.

Estate Planning

While it is kind of morbid to think about, estate laws vary state by state, meaning, depending on the size of your state, your state tax liability may vary depending on whether you're a resident of New York versus Florida. For individuals that have large estates, this could me a bigger factor in their decision of whether or not to make the move.

People That Save Taxes By Moving

All things considered, for some individuals, making the decision to change you state of domicile from New York to Florida, could save them a tremendous amount of tax dollars but it depends on what your income picture will look like in retirement. For individuals that plan to take larger distributions out of retirement accounts and may have earned income in retirement, it could give more weight did the decision to change your state of domicile but it is important to talk with a tax professional to fully evaluate all the moving pieces before making the decision.

Changing Your State of Residency

If you plan to maintain houses in both New York and Florida but plan to change your state of domicile to Florida for tax purposes make sure you know all of the rules. It is not as easy as just declaring that I am a Florida resident because I spent more than half of the year in Florida. Below is our video that details all of the items that need to be consider when changing your state of domicile from New York to Florida.

Video: How Do I Change My State Residency For Tax Purposes

Disclosure: This is for educational purposes only. It is not tax advice. For tax advice, please consult your financial professional.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.