Should You Prepay Your Property Taxes?

If you live in New York or any other state with "higher" property taxes you should determine whether or not it makes sense to pay your 2018 property taxes prior to December 31, 2017. Why? Tax reform will be capping your state and local tax deductions at $10,000 beginning in 2018. Don't forget though, that it's important to make sure you keep on

If you live in New York or any other state with "higher" property taxes you should determine whether or not it makes sense to pay your 2018 property taxes prior to December 31, 2017. Why? Tax reform will be capping your state and local tax deductions at $10,000 beginning in 2018. Don't forget though, that it's important to make sure you keep on top of your taxes, as you don't want to cause an issue further down the line.

To prevent taxpayers from navigating around the $10,000 deduction cap that will take effect in 2018, Congress wrote right into the tax bill that taxpayers will not be able to prepay their 2018 state income taxes and take the tax deduction in 2017. However, they left the door open for prepaying your 2018 property taxes in 2017 and taking the deduction in 2017 before the cap goes into effect.

Should you do this? The answer depends on your expected income for the 2017 tax year.

Alternative Minimum Tax

Before you rush down to your town office in the last week of December to prepay your 2018 taxes, if you think your income level in 2017 is going to make you subject to AMT, I will save you the trip. Alternative Minimum Tax (AMT) is a special tax calculation that was implemented back in 1969 to make sure the "wealthy" pay their fair share of taxes. The AMT calculation allows fewer deductions and exemptions than the standard tax system. Taxpayers have to calculate their taxes the "normal way" and then calculate their taxes under the AMT method. Whichever method generates the higher tax liability is the one that you pay.

The problem with AMT is over time they did not index the exemption level adequately for wage inflation since its inception in 1969. Again it was supposed to stop the wealthy from taking advantage of tax deductions. In 2017, the exemptions amounts for AMT are as follows:

Single Filer: $54,300

Married Filing Joint: $84,500

Not exactly what many of us would considered wealthy. It gets better, that exemption begins to phase out at the following levels in 2017 making more of your income subject to the special AMT calculation.

Single Filers: $120,700

Married Filing Joint: $160,900

Why am I going into so much detail amount AMT? Remember, AMT adds back deductions that were previously allowed under the standard calculation. One of those add backs is property taxes. So if your AMT tax liability exceeds your tax liability calculated with the standard formula, there is no point in prepaying your 2018 property taxes because you won't be able to deduct them anyways. Those deductions get added back in as part of the AMT calculation.

Contact Your Accountant

The AMT calculation is complex. If you are not able to accurately estimate whether or not your AMT tax liability will be greater than the standard calculation, you should contact your accountant for guidance.

Those Not Subject To AMT

If you are not subject to AMT and you plan to itemize in 2017, it probably does makes sense to prepay your property taxes for 2018 by December 29, 2017. Otherwise you are just going to lose the deduction in 2018 because it will most likely be more advantageous at that income level to just take the larger standard deduction that will be available in 2018. You end up with the best of both worlds. You get to deduct your 2018 property taxes in 2017 which reduces your income and then capture the large standard deduction in 2018,

How Do You Prepay Your Property Taxes?

So how do you pay your property taxes early? It's most likely going to require your checkbook and a trip to your town office, First, call your town office to make sure the 2018 property tax invoices are available. Once you know that they are available, you should drive down to your town office prior to December 29, 2017 and pay the tax bill.

If you escrow taxes, which many homeowners do, there is a good chance that your mortgage company will not receive your property tax bill in time to issue a check from your escrow account prior to December 29th. For this reason, you should call your mortgage services company and determine what they need to prove that you paid your 2018 property taxes with a personal check. This will hopefully prevent them from issuing a check out of your escrow account for the property taxes that you already paid with your personal check for 2018.

About Michael.........

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Tax Reform: Summary Of The Changes

The conference version of the tax bill was released on Friday. The House and the Senate will be voting to approve the updated tax bill this week with what seems to be wide spread support from the Republican party which is all they need to sign the bill into law before Christmas. Most of the changes will not take effect until 2018 with new tax rates for

The conference version of the tax bill was released on Friday. The House and the Senate will be voting to approve the updated tax bill this week with what seems to be wide spread support from the Republican party which is all they need to sign the bill into law before Christmas. Most of the changes will not take effect until 2018 with new tax rates for individuals set to expire in 2025. At which time the tax rates and brackets will return to their current state. Here is a run down of some of the main changes baked into the updated tax bill:

Individual Tax Rates

They are keeping 7 tax brackets with only minor changes to percentages in each bracket. The top tax bracket was reduced from 39.6% to 37%.

Capital Gains Rates

There were no changes to the capital gains rates and they threw out the controversial mandatory FIFO rule for calculating capital gains tax when selling securities.

Standard Deduction and Personal Exemptions

They did double the standard deduction limits. Single tax payers will receive a $12,000 standard deduction and married couples filing joint will receive a $24,000 standard deduction.The personal exemptions are eliminated.

Mortgage Interest Deduction

New mortgages would be capped at $750,000 for purposes of the home mortgage interest deduction.

State and Local Tax Deductions

State and local tax deduction will remain but will be capped at $10,000. An ouch for New York State. That $10,000 can be a combination of your property tax and either sales or income tax (whichever is larger or will get you to the cap of $10,000).Oh and you cannot prepay your 2018 state income taxes in 2017 to avoid the cap. They made it clear that if you prepay your 2018 state income taxes in 2017, you will not be able to deduct them in 2017.

Medical Expense Deductions

Medical expense deductions will remain for 2017 and 2018 and they lowered the AGI threshold to 7.5%. Beginning in 2019, the threshold will change back to the 10% threshold.

Miscellaneous Expense Deductions

Under the current rules, you are able to deduct miscellaneous expenses that exceed 2% of your AGI. That was eliminated. This includes unreimbursed business expenses and home office expenses.

A Few Quick Ones

Student Loan Interest: Still deductible

Teacher Out-of-Pocket Expenses: Still deductible

Tuition Waivers: Still not taxable

Fringe Benefits (including moving expenses): Will be taxable starting in 2018 (except for military)

Child Tax Credit: Doubled to $2,000 per child

Gain Exclusion On Sale Of Primary Residence: No Change

Obamacare Individual Mandate: Eliminated

Corporate AMT: Eliminated

Individual AMT: Remains but exemption is increased: Individuals: $70,300 Married: $109,400

Corporate Tax Rate: Drops to 21% in 2018

Federal Estate Tax: Remains but exemption limit doubles

Alimony

For divorce agreements signed after December 31, 2018, alimony will no longer be deducible. This only applies to divorce agreements executed or modified after December 31, 2018.

529 Plans

Under current tax law, you do not pay taxes on the earnings for distributions from 529 accounts for qualified college expenses. The new tax reform allows 529 account owners to distribute up to $10,000 per student for public, private and religious elementary and secondary schools, as well as home school students.

Pass-Through Income For Business

This is still a little cloudy but in general under the conference bill, owners of pass-through companies and sole proprietors will be taxed at their individual tax rates less a 20% deduction for business-related income, subject to certain wage limits and exceptions. The deduction would be disallowed for businesses offering "professional services" above a threshold amount; phase-ins begin at $157,500 for individual taxpayers and $315,000 for married taxpayers filing jointly.

About Michael.........

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

The House Passed The Tax Bill. What's The Next Step?

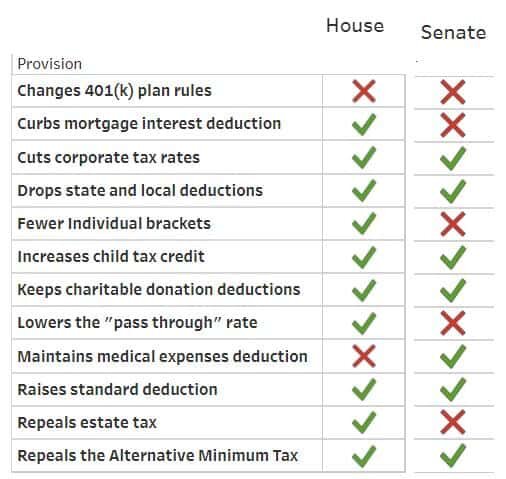

Last night the house passed the Tax Cut & Jobs Act Bill with ease. Next up is the Senate vote. It’s important to understand the House and the Senate are voting on two different tax reform bills. Below is a chart illustrating the main differences between the House version and the Senate version of the tax reform bill.

Last night the house passed the Tax Cut & Jobs Act Bill with ease. Next up is the Senate vote. It’s important to understand the House and the Senate are voting on two different tax reform bills. Below is a chart illustrating the main differences between the House version and the Senate version of the tax reform bill.

As you can see, there are a number of dramatic differences between the two bills. The easy part was getting the House to approve their version because the Republican Party own 239 of the 435 seats. In other words, they own 55% of the votes.

The Senate Vote

Next, the Senate will put their tax reform bill to a vote. The vote is expected to take place during the week of Thanksgiving. However, in the Senate , which the Republican have the majority, they only have 52 of the 100 seats. In this case, they would need at least 50 “Yes” votes to get the bill approved in the senate. It’s 50, not 51 votes, because in the event of a “tie”, the Vice President gets a vote to break the tie and he is likely to vote “Yes” to keep tax reform moving along.

Reconciliation Process

Once the House and Senate have approved their own separate tax bills, they will then have to begin the reconciliation process of blending the two bills together. This will be the difficult part. The two tax bills are dramatically different so there will be a fair amount of grappling between the House and the Senate committees as to which features stay and which features get tossed out or adjusted as part of the final tax bill. In the end, the final tax reform bill cannot add more than $1.5 Trillion to the national debt over the next 10 years. Otherwise, the bill would need to return to the Senate and would require “60” votes to approve the bill. There is a slim too no chance of that happening.

Tax Reform by Christmas

President Trump wants the bill on his desk to sign into law before Christmas. While it seems likely that the Senate will pass their tax bill next week, the battle will take place in the reconciliation process that will begin immediately after that vote. It’s a tall order to fill given that there are only six weeks left in the year and how different the two bills are in their current form. However, don’t underestimate how badly the Republican party wants to put a run on the scoreboard before the end of the year. If they get tax reform through in the last week of the year, it’s an understatement to say that it will be an intense final week of December for year-end tax planning. Stay tuned for more………

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Tax Reform: At What Cost?

The Republicans are in a tough situation. There is a tremendous amount of pressure on them to get tax reform done by the end of the year. This type of pressure can have ugly side effects. It’s similar to the Hail Mary play at the end of a football game. Everyone, including the quarterback, has their eyes fixed on the end zone but nobody realizes that no

The Republicans are in a tough situation. There is a tremendous amount of pressure on them to get tax reform done by the end of the year. This type of pressure can have ugly side effects. It’s similar to the Hail Mary play at the end of a football game. Everyone, including the quarterback, has their eyes fixed on the end zone but nobody realizes that no one is covering one of the defensive lineman and he’s just waiting for the ball to be hiked. The game ends without the ball leaving the quarterback’s hands.

The Big Play

Tax reform is the big play. If it works, it could lead to an extension of the current economic rally and more. I’m a supporter of tax reform for the purpose of accelerating job growth both now and in the future. It’s not just about U.S. companies keeping jobs in the U.S. That has been the game for the past two decades. The new game is about attracting foreign companies to set up shop in the U.S. and then hire U.S. workers to run their plants, companies, subsidiaries, etc. Right now we have the highest corporate tax rate in the world which has not only prevented foreign companies from coming here but it has also caused U.S. companies to move jobs outside of the United States. If everyone wants more pie, you have to focus on making the pie bigger, otherwise we are all just going to sit around and fight over who’s piece is bigger.

Easier Said Than Done

How do we make the pie bigger? We have to lower the corporate tax rate which will entice foreign companies to come here to produce the goods and services that they are already selling in the U.S. Which is easy to do if the government has a big piggy bank of money to help offset the tax revenue that will be lost in the short term from these tax cuts. But we don’t.

$1.5 Trillion In Debt Approved

Tax reform made some headway in mid-October when the Senate passed the budget. Within that budget was a provision that would allow the national debt to increase by approximately $1.5 trillion dollars to help offset the short-term revenue loss cause by tax reform. While $1.5 trillion sounds like a lot of money, and don’t get me wrong, it is, let’s put that number in context with some of the proposals that are baked into the proposed tax reform.

Pass-Through Entities

One of the provisions in the proposed tax reform is that income from “pass-through” businesses would be taxed at a flat rate of 25%.

A little background on pass-through business income: sole proprietorships, S corporations, limited liability companies (LLCs), and partnerships are known as pass-through businesses. These entities are called pass-throughs, because the profits of these firms are passed directly through the business to the owners and are taxed on the owners’ individual income tax returns.

How many businesses in the U.S. are pass-through entities? The Tax Foundation states on its website that pass-through entities “make up the vast majority of businesses and more than 60 percent of net business income in America. In addition, pass-through businesses account for more than half of the private sector workforce and 37 percent of total private sector payroll.”

At a conference in D.C., the American Society of Pension Professionals and Actuaries (ASPPA), estimated that the “pass through 25% flat tax rate” will cost the government $6 trillion - $7 trillion in tax revenue. That is a far cry from the $1.5 trillion that was approved in the budget and remember that is just one of the many proposed tax cuts in the tax reform package.

Are Democrats Needed To Pass Tax Reform?

Since $1.5 trillion was approved in the budget by the senate, if the proposed tax reform is able to prove that it will add $1.5 trillion or less to the national debt, the Republicans can get tax reform passed through a “reconciliation package” which does not require any Democrats to step across the aisle. If the tax reform forecasts exceed that $1.5 trillion threshold, then they would need support from a handful of Democrats to get the tax reformed passed which is unlikely.

Revenue Hunting

To stay below that $1.5 trillion threshold, the Republicans are “revenue hunting”. For example, if the proposed tax reform package is expected to cost $5 trillion, they would need to find $3.5 trillion in new sources of tax revenue to get the net cost below the $1.5 trillion debt limit.

State & Local Tax Deductions – Gone?

One for those new revenue sources that is included in the tax reform is taking away the ability to deduct state and local income taxes. This provision has created a divide among Republicans. Since many southern states do not have state income tax, many Republicans representing southern states support this provision. Visa versa, Republicans representing states from the northeast are generally opposed to this provision since many of their states have high state and local incomes taxes. There are other provisions within the proposed tax reform that create the same “it depends on where you live” battle ground within the Republican party.

Obamacare

One of the main reasons why the Trump administration pushed so hard for the Repeal and Replace of Obamacare was “revenue hunting”. They needed the tax savings from the repeal and replace of Obamacare to carrry over to fill the hole that will be created by the proposed tax reform. Since that did not happen, they are now looking high and low for other revenue sources.

Retirement Accounts At Risk?

If the Republicans fail to get tax reform through they run the risk of losing face with their supporters since they have yet to get any of the major reforms through that they campaigned on. Tax reform was supposed to be a layup, not a Hail Mary and this is where the hazard lies. Republicans, out of the desperation to get tax reform through, may start making cuts where they shouldn’t. There are rumors that the Republican Party may consider making cuts to the 401(k) contribution limits and employers sponsored retirement plan. Even though Trump tweeted on October 23, 2017 that he would not touch 401(k)’s as part of tax reform, they are running out of the options for other places that they can find new sources of tax revenue. If it comes down to the 1 yard line and they have the make the decision between making deep cuts to 401(k) plans or passing the tax reform, retirement plans may end up being the sacrificial lamb. There are other consequences that retirement plans may face if the proposed tax reform is passed but it’s too broad to get into in this article. We will write a separate article on that topic.

Tax Reform May Be Delayed

Given all the variables in the mix, passing tax reform before December 31st is starting to look like a tall order to fill. If the Republicans are looking for new sources of revenue, they should probably look for sources that are uniform across state lines otherwise they risk splintering the Republican Party like we saw during the attempt to Repeal and Replace Obamacare. We are encouraging everyone to pay attention to the details buried in the tax reform. While I support tax reform to secure the country’s place in the world both now and in the future, if provisions that make up the tax reform are rushed just to get something done, we run the risk of repeating the short lived glory that tax reform saw during the Reagan Era. They passed sweeping tax cuts, the deficits spiked, and they were forced to raise tax rates a few years later.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.