Inherited IRA's: How Do They Work?

how do inherited ira's work

An Inherited IRA is a retirement account that is left to a beneficiary after the owner’s death. It is important to have a general knowledge of how Inherited IRA’s work because a minor error in how the account is set up could lead to major tax consequences.

Before going into the different kinds of Inherited IRA’s, if you are the sole beneficiary of your spouse’s IRA, you are able to transfer the assets to your own existing IRA or to a new IRA through what is called a “Spousal Transfer”. This account is not treated as an Inherited IRA and therefore is subject to all the rules a Traditional IRA would be subject to as if it was always held in your name. If the spouse needs to have access to the money before age 59 ½, it would probably make sense to set up an Inherited IRA because this would give the spouse options to access the money without incurring a 10% early withdrawal penalty.

Withdrawal Rules for Spouse & Non-Spouse Beneficiaries

The SECURE Act that passed in December 2019 dramatically changed the distribution options that are available to non-spouse beneficiaries. If you are spousal beneficiary please reference the following article:

10 Year Method

All the assets must be distributed by the 10th year after the year in which the account holder died. This option may make sense compared to the Lump Sum option explained next to spread out the tax liability over a longer period.

Lump Sum Distribution

You may take a lump sum distribution when the account is inherited. It is recommended that you consult your tax preparer to discuss the tax consequences of this method since you may move up into a different tax bracket.

Additional Takeaways

If the decedent was required to take a distribution in the year of death, it is important to determine whether or not the decedent took the distribution. If the decedent was required to take a RMD but did not do so in the year they passed, the inheritor must take the distribution based on the life expectancy of the decedent or the distribution will be subject to a 50% penalty. Distributions going forward will be based on the life expectancy of the inheritor.

It is important to be sure a beneficiary form is completed for the Inherited IRA. If there is no beneficiary and the account goes to an estate then the inheritor will have limited choices on which distribution method to choose among other tax consequences.

You are only able to combine Inherited IRA’s if they were inherited from the same individual. If you have multiple Inherited IRA’s from different individuals, you cannot commingle the assets because of the distributions that must be taken.

There is no 60 day rule with Inherited IRA’s like there is with other Traditional IRA’s. The 60 day rule allows someone to withdraw money from an IRA and as long as it’s replenished within 60 days there is no tax consequence. This is not available with Inherited IRA’s, all non-Roth distributions are taxable.

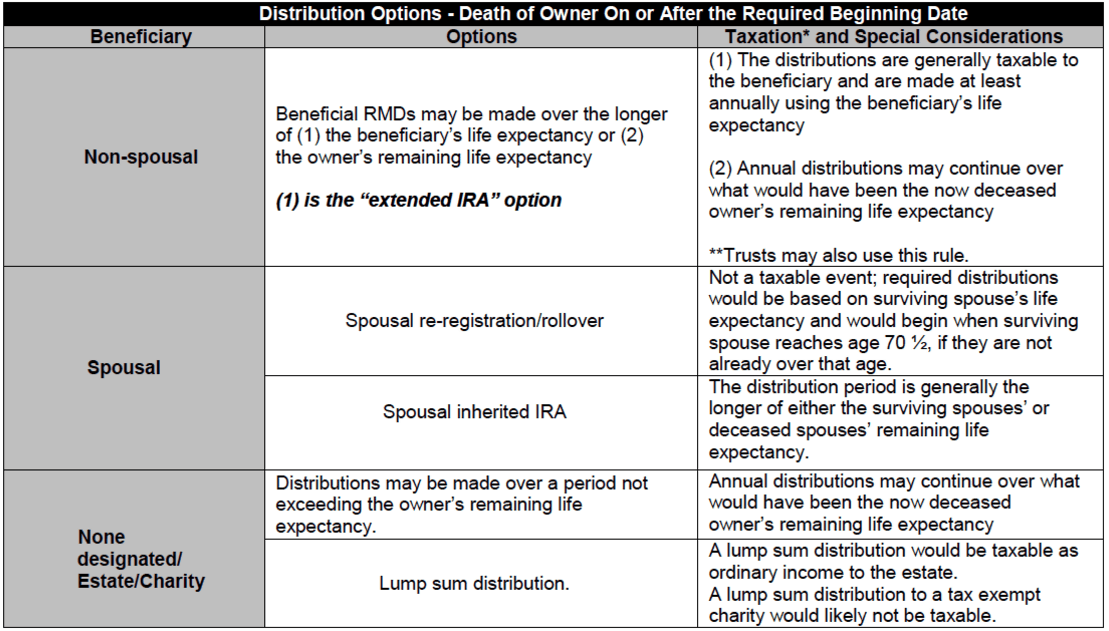

The charts below are from insurancenewsnet.com publication titled “Extended IRA Quick Reference Guide” give another look at the details of Inherited IRA’s.

inherited ira options

inherited ira distribution options

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally , professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, pleas feel free to join in on the discussion or contact me directly.