Do I Have To Pay Tax On A House That I Inherited?

The tax rules are different depending on the type of assets that you inherit. If you inherit a house, you may or may not have a tax liability when you go to sell it. This will largely depend on whose name was on the deed when the house was passed to you. There are also special exceptions that come into play if the house is owned by a trust, or if it was gifted

Do I Have To Pay Tax On A House That I Inherited?

The tax rules are different depending on the type of assets that you inherit. If you inherit a house, you may or may not have a tax liability when you go to sell it. This will largely depend on whose name was on the deed when the house was passed to you. There are also special exceptions that come into play if the house is owned by a trust, or if it was gifted with the kids prior to their parents passing away. On the bright side, with some advanced planning, heirs can often times avoid having to pay tax on real estate assets when they pass to them as an inheritance.

Step-up In Basis

Many assets that are included in the decedent’s estate receive what’s called a step-up in basis. As with any asset that is not held in a retirement account, you must be able to identify the “cost basis”, or in other words, what you originally paid for it. Then when you eventually sell that asset, you don’t pay tax on the cost basis, but you pay tax on the gain.

Example: You buy a rental property for $200,000 and 10 years later you sell that rental property for $300,000. When you sell it, $200,000 is returned to you tax free and you pay long-term capital gains tax on the $100,000 gain.

Inheritance Example: Now let’s look at how the step-up works. Your parents bought their house 30 years ago for $100,000 and the house is now worth $300,000. When your parents pass away and you inherit the house, the house receives a step-up in basis to the fair market value of the house as of the date of death. This means that when you inherit the house, your cost basis will be $300,000 and not the $100,000 that they paid for it. Therefore, if you sell the house the next day for $300,000, you receive that money 100% tax-free due to the step-up in basis.

Appreciation After Date of Death

Let’s build on the example above. There are additional tax considerations if you inherit a house and continue to hold it as an investment and then sell it at a later date. While you receive the step-up in basis as of the date of death, the appreciation that occurs on that asset between the date of death and when you sell it is going to be taxable to you.

Example: Your parents passed away June 2019 and at that time their house is worth $300,000. The house receives the step-up in basis to $300,000. However, lets say this time you rent the house or don’t sell it until September 2020. When you sell the house in September 2020 for $350,000, you will receive the $300,000 tax-free due to the step-up in basis, but you’ll have to pay capital gains tax on the $50,000 gain that occurred between date of death and when you sold house.

Caution: Gifting The House To The Kids

In an effort to protect the house from the risk of a long-term event, sometimes individuals will gift their house to their kids while they are still alive. Some see this as a way to remove themselves from the ownership of their house to start the five-year Medicaid look back period, however, there is a tax disaster waiting for you with the strategy.

When you gift an asset to someone, they inherit your cost basis in that asset, so when you pass away, that asset does not receive a step-up in basis because you don’t own it and it’s not part of your estate.

Example: Your parents change the deed on the house to you and your siblings while they’re still alive to protect assets from a possible nursing home event. They bought the house 30 years ago for $100,000, and when they pass away it’s worth $300,000. Since they gifted the assets to the kids while they were still alive, the house does not receive a step-up in basis when they pass away, and the cost basis on the house when the kids sell it is $100,000; in other words, the kids will have to pay tax on the $200,000 gain in the property. Based on the long-term capital gains rates and possible state income tax, when the children sell the house, they may have a tax bill of $44,000 or more which could have been completely avoided with better advanced planning.

How To Avoid Paying Capital Gains Tax On Inherited Property

There are ways to both protect the house from a long-term event and still receive the step-up in basis when the current owners pass away. This process involves setting up an irrevocable trust to own the house which then protects the house from a long-term event as long as it’s held in the trust for at least five years.

Now, we do have to get technical for a second. When an asset is owned by an irrevocable trust, it is technically removed from your estate. Most assets that are not included in your estate when you pass do not receive a step-up in basis; however, if the estate attorney that drafts the trust document puts the correct language within the trust, it allows you to protect the assets from a long-term event and receive a step-up in basis when the owners of the house pass away.

For this reason, it’s very important to work with an attorney that is experienced in handling trusts and estates, not a generalist. It only takes a few missing sentences from that document that can make the difference between getting that asset tax free or having a huge tax bill when you go to sell the house.

Establishing this trust can sometimes cost between $3,000 and $6,000. But by paying this amount upfront and doing the advance planning, you could save your heirs 10 times that amount by avoiding a big tax bill when they inherit the house.

Making The House Your Primary

In the case that the house is gifted to the children prior to the parents passing away and the house is not awarded the step-up in basis, there is an advance tax planning strategy if the conditions are right to avoid the big tax bill. If one of the children would be interested in making their parent’s house their primary residence for two years, then they are then eligible for either the $250,000 or $500,000 capital gains exclusion.

According to current tax law, if the house you live in has been your primary residence for two of the previous five years, when you go to sell the house you are allowed to exclude $250,000 worth of gain for single filers and $500,000 worth of gain for married filing joint. This advanced tax strategy is more easily executed when there is a single heir and can get a little more complex when there are multiple heirs.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

How Much Should I Budget For Health Care Costs In Retirement?

The number is higher than you think. When you total up the deductibles and premiums for Medicare part A, B, and D, that alone can cost a married couple $7,000 per year. We look at that figure as the baseline number. That $7,000 does not account for the additional costs associated with co-insurance, co-pays, dental costs, or Medigap insurance

The number is higher than you think. When you total up the deductibles and premiums for Medicare part A, B, and D, that alone can cost a married couple $7,000 per year. We look at that figure as the baseline number. That $7,000 does not account for the additional costs associated with co-insurance, co-pays, dental costs, or Medigap insurance premiums which can quickly increase the overall cost to $10,000+ per year.

Tough to believe? Allow me to walk you through the numbers for a married couple.

Medicare Part A: $2,632 Per Year

Part A covers inpatient hospital stays, skilled nursing facility stays, some home health visits, and hospice care. While Part A does not have an annual premium, it does have an annual deductible for each spouse. That deductible for 2017 is $1,316 per person.

Medicare Part B: $3,582

Part B covers physician visits, outpatient services, preventive services, and some home health visits. The standard monthly premium is $134 per person but it could be higher depending on your income level in retirement. There is also a deductible of $183 per year for each spouse.

Medicare Part D: $816

Part D covers outpatient prescription drugs through private plans that contract with Medicare. Enrollment in Part D is voluntary. The benefit helps pay for enrollees’ drug costs after a deductible is met (where applicable), and offers catastrophic coverage for very high drug costs. Part D coverage is actually provided by private health insurance companies. The premium varies based on your income and the types of prescriptions that you are taking. The national average in 2017 for Part D premiums is $34 per person.

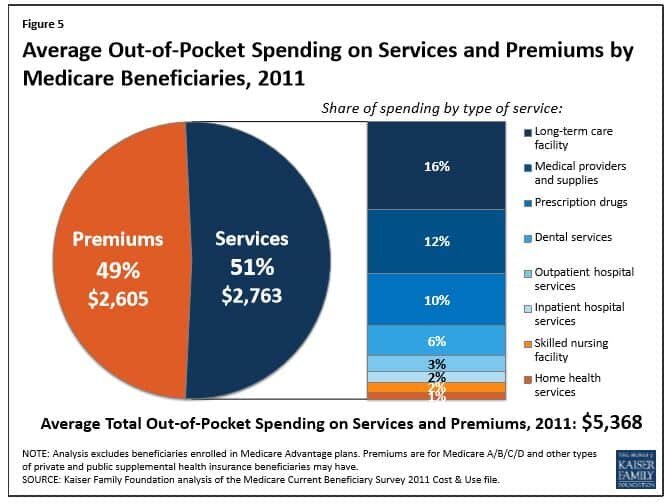

If you total up just these three items, you reach $7,030 in premiums and deductibles for the year. Then you start adding in dental cost, Medigap insurance premiums, co-insurance for Medicare benefits, and it quickly gets a married couple over that $10,000 threshold in health and dental cost each year. Medicare published a report that in 2011, Medicare beneficiaries spent $5,368 out of their own pockets for health care spending, on average. See the table below.

Start Planning Now

Fidelity Investments published a study that found that the average 65 year old will pay $240,000 in out-of-pocket costs for health care during retirement, not including potential long-term-care costs. While that seems like an extreme number, just take the $10,000 that we used above, multiply that by 20 year in retirement, and you get to $200,000 without taking into consideration inflation and other important variable that will add to the overall cost.

Bottom line, you have to make sure you are budgeting for these expenses in retirement. While most individuals focus on paying off the mortgage prior to retirement, very few are aware that the cost of health care in retirement may be equal to or greater than your mortgage payment. When we are create retirement projections for clients we typically included $10,000 to $15,000 in annual expenses to cover health care cost for a married couple and $5,000 – $7,500 for an individual.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Social Security Filing Strategies

Making the right decision of when to turn on your social security benefit is critical. The wrong decision could cost you tens of thousands of dollars over the long run. Given all the variables surrounding this decision, what might be the right decision for one person may be the wrong decision for another. This article will cover some of the key factors to

Making the right decision of when to turn on your social security benefit is critical. The wrong decision could cost you tens of thousands of dollars over the long run. Given all the variables surrounding this decision, what might be the right decision for one person may be the wrong decision for another. This article will cover some of the key factors to consider:

Normal Retirement Age

First, you have to determine your "Normal Retirement Age" (NRA). This is listed on your social security statement in the "Your Estimated Benefits" section. If you were born between 1955 – 1960, your NRA is between age 66 – 67. If you were born 1960 or later, your NRA is age 67. You can obtain a copy of your statement via the social security website.

Before Normal Retirement Age

You have the option to turn on social security prior to your normal retirement age. The earliest you can turn on social security is age 62. However, they reduce your social security benefit by approximately 7% per year for each year prior to your normal retirement age. See the chart below from USA Today which illustrates an individual with a normal retirement age of 66. If they turn on their social security benefit at age 62, they would only receive 75% of their full benefit. This reduction is a permanent reduction. It does not increase at a later date, outside of the small cost of living increases.

taking social security early

The big questions is: “If I start taking it age 62, at what age is the breakeven point?” Remember, if I turn on social security at 62 and my normal retirement age is 66, I have received 4 years of payments from social security. So at what age would I be kicking myself wishing that I had waited until normal retirement age to turn on my benefit. There are a few different ways to calculate this accounting for taxes, the rates of return on other retirement assets, inflations, etc. but in general it’s sometime between the ages of 78 and 82.

Since the breakeven point may be in your early 80’s, depending on your health, and the longevity in your family history, it may or may not make sense to turn on your benefit early. If we have a client that is in ok health but not great health and both of their parents passed way prior to age 85, then it may make sense to for them to turn on their social security benefit early. We also have clients that have pensions and turning on their social security benefit early makes the different between retiring now or have to work for 5+ more years. As long as the long-term projections work out ok, we may recommend that they turn on their social security benefit early so they can retire sooner.

Are You Still Working?

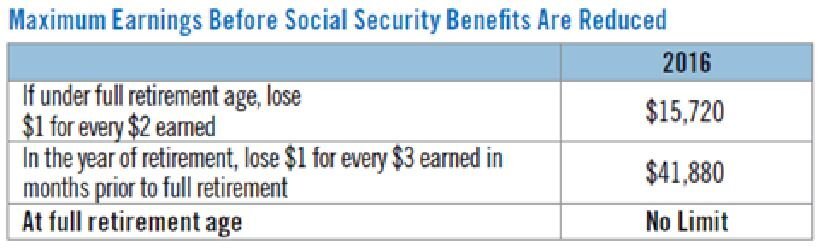

This is a critical question for anyone that is considering turning on their social security benefits early. Why? If you turn on your social security benefit prior to reaching normal retirement age, there is an “earned income” penalty if you earn over the threshold set by the IRS for that year. See the table listed below:

In 2016, for every $2 that you earned over the $15,720 threshold, your social security was reduced by $1. For example, let’s say I’m entitled to $1,000 per month ($12,000 per year) from social security at age 62 and in 2016 I had $25,000 in W2 income. That is $9,280 over the $15,720 threshold for 2016 so they would reduce my annual benefit by $4,640. Not only did I reduce my social security benefit permanently by taking my social security benefit prior to normal retirement age but now my $12,000 in annual social security payments they are going to reduce that by another $4,640 due to the earned income penalty. Ouch!!!

Once you reach your normal retirement age, this earned income penalty no longer applies and you can make as much as you want and they will not reduce your social security benefit.

Because of this, the general rule of thumb is if you are still working and your income is above the IRS earned income threshold for the year, you should hold off on turning on your social security benefits until you either reach your normal retirement age or your income drops below the threshold.

Should I Delay May Benefit Past Normal Retirement Age

As was illustrated in first table, if you delay your social security benefit past your normal retirement age, your benefit will increase by approximately 8% per year until you reach age 70. At age 70, your social security benefit is capped and you should elect to turn on your benefits.

So when does it make sense to wait? The most common situation is the one where you plan to continue working past your normal retirement age. It’s becoming more common that people are working until age 70. Not because they necessarily have too but because they want something to keep them busy and to keep their mind fresh. If you have enough income from employment to cover you expenses, in many cases, is does make sense to wait. Based on the current formula, your social security benefit will increase by 8% per year for each year you delay your benefit past normal retirement age. It’s almost like having an investment that is guaranteed to go up by 8% per year which does not exist.

Also, for high-income earners, a majority of their social security benefit will be taxable income. Why would you want to add more income to the picture during your highest tax years? It may very well make sense to delay the benefit and allow the social security benefit to increase.

Death Benefit

The social security death benefit also comes into play as well when trying to determine which strategy is the right one for you. For a married couple, when their spouse passes away they do not continue to receive both benefits. Instead, when the first spouse passes away, the surviving spouse will receive the “higher of the two” social security benefits for the rest of their life. Here is an example:

Spouse 1 SS Benefit: $2,000

Spouse 2 SS Benefit: $1,000

If Spouse 1 passes away first, Spouse 2 would bump up to the $2,000 monthly benefit and their $1,000 monthly benefit would end. Now let’s switch that around, let’s say Spouse 2 passes away first, Spouse 1 will continue to receive their $2,000 per month and the $1,000 benefit will end.

If social security is a large percentage of the income picture for a married couple, losing one of the social security payments could be detrimental to the surviving spouse. Due to this situation, it may make sense to have the spouse with the higher benefit delay receiving social security past normal retirement to further increase their permanent monthly benefit which in turn increases the death benefit for the surviving spouse.

Spousal Benefit

The “spousal benefit” can be a powerful filing strategy. If you are married, you have the option of turning on your benefit based on your earnings history or you are entitled to half of your spouse’s benefit, whichever benefit is higher. This situation is common when one spouse has a much higher income than the other spouse.

Here is an important note. To be eligible for the spousal benefit, you personally must have earned 40 social security “credits”. You receive 1 credit for each calendar quarter that you earn a specific amount. In 2016, the figure was $1,260. You can earn up to 4 credits each calendar year.

Another important note, under the new rules, you cannot elect your spousal benefit until your spouse has started receiving social security payments.

Here is where the timing of the social security benefits come into play. You can turn on your spousal benefit as early as 62 but similar to the benefit based on your own earnings history it will be reduce by approximately 7% per year for each year you start the benefit prior to normal retirement age. At your normal retirement age, you are entitled to receive your full spousal benefit.

What happens if you delay your spousal benefit past normal retirement age? Here is where the benefit calculation deviates from the norm. Typically when you delay benefits, you receive that 8% annual increase in the benefits up until age 70. The spousal benefit is based exclusively on the benefit amount due to your spouse at their normal retirement age. Even if your spouse delays their social security benefit past their normal retirement age, it does not increase the 50% spousal benefit.

Here is the strategy. If it’s determine that the spousal benefit will be elected as part of a married couple’s filing strategy, since delaying the start date of the benefits past normal retirement age will only increase the social security benefit for the higher income earning spouse and not the spousal benefit, in many cases, it does not make sense to delay the start date of the benefits past normal retirement age.

Divorce

For divorced couples, if you were married for at least 10 years, you can still elect the spousal benefit even though you are no longer married. But you must wait until your ex-spouse begins receiving their benefits before you can elect the spousal benefit.

Also, if you were married for at least 10 years, you are also entitled to the death benefit as their ex-spouse. When your ex-spouse passes away, you can notify the social security office, elect the death benefit, and you will receive their full social security benefit amount for the rest of your life instead of just 50% of their benefit resulting from the “spousal benefit” calculation.

Whether or not your ex-spouse remarries has no impact on your ability to elect the spousal benefit or death benefit based on their earnings history.

Consult A Financial Planner

Given all of the variables in the mix and the importance of this decision, we strongly recommend that you consult with a Certified Financial Planner® before making your social security benefit elections. While the interaction with a fee-based CFP® may cost you a few hundred dollars, making the wrong decision regarding your social security benefits could cost you thousands of dollars over your lifetime. You can also download a Financial Planner Budget Worksheet to give you that extra help when sorting out your finances and monthly budgeting.

About Michael.........

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Can I Negotiate A Car Lease Buyout?

The short answer is "yes", but the approach that you take will most likely determine whether or not you are successful at purchasing your vehicle for a lower price than the amount listed in the lease agreement. When you lease a car, the lease agreement typically includes an amount that you can purchase the car for at the end of the lease. That amount is

The short answer is "yes", but the approach that you take will most likely determine whether or not you are successful at purchasing your vehicle for a lower price than the amount listed in the lease agreement. When you lease a car, the lease agreement typically includes an amount that you can purchase the car for at the end of the lease. That amount is essentially a guess by the bank that is providing the financing for the lease as to what the future value of your vehicle will be at the end of the lease.

Lease Buyout Calculation

Step number one in the negotiation process is to determine what your vehicle is worth. Did the bank guess right or wrong? If the purchase amount in your lease agreement is $25,000 but you find that the vehicle, based on current market conditions, is only worth $18,000, you probably have room to negotiate the purchase price of your vehicle but you have to do your homework. Compare your vehicle's purchase price to the retail value of local auto dealers. If you can show the bank that there is a local auto dealer trying to sell the exact make and model of your leased car with similar mileage, the bank will be more likely to accept a lower purchase price realizing that they guessed wrong.

Deal Directly With The Bank

You may have noticed that I continue to reference the "bank" in the negotiation process and not the "dealer". This is intentional. Some leasing banks allow dealers to increase the cost of the lease buyout to make a profit. Dealers can also charge document fees, which are taxable in most states. It may also be advantageous to line up your own financing for the lease purchase amount before entering into the negotiation process. If the dealer arranges the financing for you, it can sometimes increase your interest rate to make more money on the purchase. By dealing directly with the leasing bank you can cut out these additional costs.

You Make The Offering Price

Start by making an offer to the leasing bank based on your market research. Also make sure you contact the leasing bank well in advance of the lease "turn-in date". The bank may not be able to provide you with an immediate response to your offer so give yourself plenty of time for the negotiation process to work.

About Michael.........

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog. I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Can I Use My 401K or IRA To Buy A House?

The most difficult part of buying a house is coming up with the down payment. This leads to the question, "Can I access cash in my retirement accounts to help toward the down payment on my house?". The short answer is in most cases, "Yes". The next important questions is "Is it a good idea to take a withdrawal from my retirement account for the down

The most difficult part of buying a house is coming up with the down payment. This leads to the question, "Can I access cash in my retirement accounts to help toward the down payment on my house?". The short answer is in most cases, "Yes". The next important questions is "Is it a good idea to take a withdrawal from my retirement account for the down payment given all of the taxes and penalties that I would have to pay?" This article aims to answer both of those questions and provide you with withdrawal strategies to help you avoid big tax consequences and early withdrawal penalties.

401(k) Withdrawal Options Are Not The Same As IRA's

First you have to acknowledge that different types of retirement accounts have different withdrawal options available. The withdrawal options for a down payment on a house from a 401(k) plan are not the same a the withdrawal options from a Traditional IRA. There is also a difference between Traditional IRA's and Roth IRA's.

401(k) Withdrawal Options

There may be loan or withdrawal options available through your employer sponsored retirement plan. I specifically say "may" because each company's retirement plan is different. You may have all or none of the options available to you that will be presented in this article. It all depends on how your company's 401(k) plan is designed. You can obtain information on your withdrawal options from the plan's Summary Plan Description also referred to as the "SPD".

Taking a 401(k) loan.............

The first option is a 401(k) loan. Some plans allow you to borrow 50% of your vested balance in the plan up to a maximum of $50,000 in a 12 month period. Taking a loan from your 401(k) does not trigger a taxable event and you are not hit with the 10% early withdrawal penalty for being under the age of 59.5. 401(k) loans, like other loans, change interest but you are paying that interest to your own account so it is essentially an interest free loan. Typically 401(k) loans have a maximum duration of 5 years but if the loan is being used toward the purchase of a primary residence, the duration of the loan amortization schedule can be extended beyond 5 years if the plan's loan specifications allow this feature.

Note of caution, when you take a 401(k) loan, loan payments begin immediately after the loan check is received. As a result, your take home pay will be reduced by the amount of the loan payments. Make sure you are able to afford both the 401(k) loan payment and the new mortgage payment before considering this option.

The other withdrawal option within a 401(k) plan, if the plan allows, is a hardship distribution. As financial planners, we strongly recommend against hardship distributions for purposes of accumulating the cash needed for a down payment on your new house. Even though a hardship distribution gives you access to your 401(k) balance while you are still working, you will get hit with taxes and penalties on the amount withdrawn from the plan. Unlike IRA's which waive the 10% early withdrawal penalty for first time homebuyers, this exception is not available in 401(k) plans. When you total up the tax bill and the 10% early withdrawal penalty, the cost of this withdrawal option far outweighs the benefits.

If You Have A Roth IRA.......Read This.....

Roth IRA's can be one of the most advantageous retirement accounts to access for the down payment on a new house. With Roth IRA's, you make after tax contributions to the account, and as long as the account has been in existence for 5 years and you are over the age of 59� all of the earnings are withdrawn from the account 100% tax free. If you withdraw the investment earnings out of the Roth IRA before meeting this criteria, the earnings are taxed as ordinary income and a 10% early withdrawal penalty is assessed on the earnings portion of the account.

What very few people know is if you are under the age of 59� you have the option to withdraw just your after-tax contributions and leave the earnings in your Roth IRA. By doing so, you are able to access cash without taxation or penalty and the earnings portion of your Roth IRA will continue to grow and can be distributed tax free in retirement.

The $10,000 Exclusion From Traditional IRA's.......

Typically if you withdraw money out of your Traditional IRA prior to age 59� you have to pay ordinary income tax and a 10% early withdrawal penalty on the distribution. There are a few exceptions and one of them is the "first time homebuyer" exception. If you are purchasing your first house, you are allowed to withdrawal up to $10,000 from your Traditional IRA and avoid the 10% early withdrawal penalty. You will still have to pay ordinary income tax on the withdrawal but you will avoid the early withdrawal penalty. The $10,000 limit is an individual limit so if you and your spouse both have a traditional IRA, you could potentially withdrawal up to $20,000 penalty free.

Helping your child to buy a house..........

Here is a little known fact. You do not have to be the homebuyer. You can qualify for the early withdrawal exemption if you are helping your spouse, child, grandchild, or parent to buy their first house.

Be careful of the timing rules..........

There is a very important timing rule associated with this exception. The closing must take place within 120 day of the date that the withdrawal is taken from the IRA. If the closing happens after that 120 day window, the full 10% early withdrawal penalty will be assessed. There is also a special rollover rule for the first time homebuyer exemption which provides you with additional time to undo the withdrawal if need be. Typically with IRA's you are only allowed 60 days to put the money back into the IRA to avoid taxation and penalty on the IRA withdrawal. This is called a "60 Day Rollover". However, if you can prove that the money was distributed from the IRA with the intent to be used for a first time home purchase but a delay or cancellation of the closing brought you beyond the 60 day rollover window, the IRS provides first time homebuyers with a 120 window to complete the rollover to avoid tax and penalties on the withdrawal.

Don't Forget About The 60 Day Rollover Option

Another IRA withdrawal strategy that is used as a “bridge solution” is a “60 Day Rollover”. The 60 Day Rollover option is available to anyone with an IRA that has not completed a 60 day rollover within the past 12 months. If you are under the age of 59.5 and take a withdrawal from your IRA but you put the money back into the IRA within 60 days, it’s like the withdrawal never happened. We call it a “bridge solution” because you have to have the cash to put the money back into your IRA within 60 days to avoid the taxes and penalty. We frequently see this solution used when a client is simultaneously buying and selling a house. It’s often the intent that the seller plans to use the proceeds from the sale of their current house for the down payment on their new house. Unfortunately due to the complexity of the closing process, sometimes the closing on the new house will happen prior to the closing on the current house. This puts the homeowner in a cash strapped position because they don’t have the cash to close on the new house.

As long as the closing date on the house that you are selling happens within the 60 day window, you would be able to take a withdrawal from your IRA, use the cash from the IRA withdrawal for the closing on their new house, and then return the money to your IRA within the 60 day period from the house you sold. Unlike the “first time homebuyer” exemption which carries a $10,000 limit, the 60 day rollover does not have a dollar limit.

About Michael.........

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Should I Gift A Stock To My Kids Or Just Let Them Inherit It?

Many of our clients own individual stocks that they either bought a long time ago or inherited from a family member. If they do not need to liquidate the stock in retirement to supplement their income, the question comes up “should I just gift the stock to my kids while I’m still alive or should I just let them inherit it after I pass away?” The right answer is

Many of our clients own individual stocks that they either bought a long time ago or inherited from a family member. If they do not need to liquidate the stock in retirement to supplement their income, the question comes up “should I just gift the stock to my kids while I’m still alive or should I just let them inherit it after I pass away?” The right answer is largely influenced by the amount of appreciation or depreciation in the stock.

Gifting Stock

When you make a non-cash gift such as a stock, house, or even a business, the person receiving the gift assumes your cost basis in the assets. They do not receive a “step-up” in basis at the time the gift is made. Example, I buy XYZ Corp stock in 1995 for $10,000. In 2017, those shares of XYZ are now worth $100,000. If I gift them to my kids, no one owes tax on the gift at the time that the gift is made but my kids carry over my cost basis in the stock. If my kids hold the stock for 10 more years and sell it for $150,000, their basis in the stock is $10,000, and they owe capital gains tax on the $140,000 gain. Thus, creating an adverse tax consequence for my kids.

Inheriting Stock

Instead, let’s say I continue to hold XYZ stock and when I pass away my kids inherited the stock. If I pass away in 10 years and the stock is worth $150,000 then my kids receive a “step-up” in basis which means that their cost basis in the stock is the value of the stock as of the date of my death. They inherit the stock at $150,000 value, sell it the next day, and they owe $0 in taxes due to the step-up in basis upon my death.

In general, if you have assets that have low cost basis it is usually better for your heirs to inherit the assets as opposed to gifting it to them.

The concept is often times reversed for assets that have depreciated in value…..with an important twist. If I purchase XYZ Corp stock in 1995 for $10,000 but in 2017 it’s only worth $5,000, if I sold the stock myself I would capture the realized investment loss and could use it to offset investment gains or reduce my income by $3,000 for the IRS realized loss allowance.

Here is a very important rule......

In most cases, do not gift a depreciated asset to someone else. Why? When you gift an asset that has depreciated in value the carry over basis rules change. For an asset that has depreciated in value, the carry over basis for the person receiving the gift is the higher of the fair market value of the asset or the cost basis of the person making the gift. In other words, the loss evaporates when I gift the asset to someone else and no one gets the tax advantage of using the realized loss for tax purposes. It would be better if I sold the stock, captured the investment loss, and then gifted the cash.

If they inherit the stock that has lost value there is no value to the step-up in basis because the stock has not appreciated in value.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

How To Teach Your Kids About Investing

As kids enter their teenage years, as a parent, you begin to teach them more advanced life lessons that they will hopefully carry with them into adulthood. One of the life lessons that many parents teach their children early on is the value of saving money. By their teenage years many children have built up a small savings account from birthday gifts,

As kids enter their teenage years, as a parent, you begin to teach them more advanced life lessons that they will hopefully carry with them into adulthood. One of the life lessons that many parents teach their children early on is the value of saving money. By their teenage years many children have built up a small savings account from birthday gifts, holidays, and their part-time jobs. As parents you have most likely realized the benefit of compounding interest through working with a financial advisor, contributing to a 401(k) plan, or depositing money to a college savings account. As financial planners, we often get the question: “What is the best way to teach your children about the value of investing and compounding interest? "

The #1 rule.......

We have been down this road many times with our clients and their children. Here is the number one rule: Make it an engaging experience for your kids. Investments can be a very dull topic to talk about and it can be painfully dull from a child’s point of view. All they know is the $1,000 that was in their savings account is now with their parent’s investment guy.

Ignoring the life lessons for a moment, the primary investment vehicle for brokerage accounts with balances under $50,000 is typically a mutual fund. But let’s pause for a moment. We have a dual objective here. We of course want our children to make as much money as possible in their investment account but we also want to simultaneously teach them life long lessons about investing.

The issue with young investors

Explaining how a mutual fund operates can be a complex concept for a first time investor because you have all of these companies in one investment, expense ratios, different types of funds, and different fund families. It’s not exciting, it’s intimidating.

Consider this approach. Ask the child what their hobbies are? Do they have a cell phone? Have them take their cell phone out during the meeting and ask them how often they use it during the day and how many of their friends have cell phones. Then ask them, if you received $20 every time someone in this area bought a cell phone would you have a lot of money? Then explain that this scenario is very similar to owning stock in a cell phone company. The more they sell the more money the company makes. As a “shareholder” you own a piece of that company and you receive a piece of the profits if the company grows. If your child plays sports, do they wear a lot of Nike or Under Armour? Explain investing to them in a way that they can relate it to their everyday life. Now you have their attention because you attached the investment idea to something they love.

A word of caution....

If they are investing in stocks it is also important for them to understand the concept of risk. Not every investment goes up and you could start with $1,000 and end the year with $500, so they need to understand risk and time horizon.

While it’s not prudent in most scenarios to invest 100% of a portfolio in one stock, there may be some middle ground. Instead of investing their entire $1,000 in a mutual fund, consider investing $500 – $700 in a mutual fund but let them pick one to three stocks to hold in the account. It may make sense to have them review those stock picks with your investment advisor for two reasons. One, you want them to have a good experience out of the gates and that investment advisor can provide them with their option of their stock picks. Second, the investment advisor can tell them more about the companies that they have selected to further engage them.

Don't forget the last step......

Download an app on their smartphone so they can track the investments that they selected. You may be surprise how often they check the performance of their stock holdings and how they begin to pay attention to news and articles applicable to the companies that they own.At that point you have engaged them and as they hopefully see their investment holdings appreciate in value they will become even more excited about saving money in their investment account and making their next stock pick. In addition, they also learn valuable investment lessons early on like when one of their stocks loses value. How do they decide whether to sell it or continue to hold it? It’s a great system that teaches them about investing, decision making, risk, and the value of compounding investment returns.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Planning for Long Term Care

The number of conversations that we are having with our clients about planning for long term care is increasing exponentially. Whether it’s planning for their parents, planning for themselves, or planning for a relative, our clients are largely initiating these conversations as a result of their own personal experiences.

The number of conversations that we are having with our clients about planning for long term care is increasing exponentially. Whether it’s planning for their parents, planning for themselves, or planning for a relative, our clients are largely initiating these conversations as a result of their own personal experiences.

The baby-boomer generation is the first generation that on a large scale is seeing the ugly aftermath of not having a plan in place to address a long term care event because they are now caring for their aging parents that are in their 80’s and 90’s. Advances in healthcare have allowed us to live longer but the longer we live the more frail we become later in life.

Our clients typically present the following scenario to us: “I have been taking care of my parents for the past three years and we just had to move my dad into the nursing home. What an awful process. How can I make sure that my kids don’t have to go through that same awful experience when I’m my parents age?”

“Planning for long term care is not just about money…….it’s about having a plan”

If there are no plans, your kids or family members are now responsible for trying to figure out “what mom or dad would have wanted”. Now tough decisions need to be made that can poison a relationship between siblings or family members.

Some individuals never create a plan because it involves tough personal decisions. We have to face the reality that at some point in our lives we are going to get older and later in life we may reach a threshold that we may need help from someone else to care for ourselves or our spouse. It’s a tough reality to face but not facing this reality will most likely result in the worst possible outcome if it happens.

Ask yourself this question: “You worked hard all of your life to buy a house, accumulate assets in retirement accounts, etc. If there are assets left over upon your death, would you prefer that those assets go to your kids or to the nursing home?” With some advance planning, you can make sure that your assets are preserved for your heirs.

The most common reason that causes individuals to avoid putting a plan in place is: “I have heard that long term care insurance is too expensive.” I have good news. First, there are other ways to plan for the cost of a long term care event besides using long term care insurance. Second, there are ways to significantly reduce the cost of these policies if designed correctly.

The most common solution is to buy a long term care insurance policy. The way these policies work is if you can no longer perform certain daily functions, the policy pays a set daily benefit. Now a big mistake many people make is when they hear “long term care” they think “nursing home”. In reality, about 80% of long term care is provided right in the home via home health aids and nurses. Most LTC policies cover both types of care. Buying a LTC policy is one of the most effective ways to address this risk but it’s not the only one.

Why does long term care insurance cost more than term life insurance or disability insurance? The answer, most insurance policies insure you against risks that have a low probability of happening but has a high financial impact. Similar to a life insurance policy. There is a very low probability that a 25 year old will die before the age of 60. However, the risk of long term care has a high probability of happening and a high financial impact. According to a study conducted by the U.S Department of Human Health and Services, “more than 70% of Americans over the age of 65 will need long-term care services at some point in their lives”. Meaning, there is a high probability that at some point that insurance policy is going to pay out and the dollars are large. The average daily rate of a nursing home in upstate New York is around $325 per day ($118,625 per year). The cost of home health care ranges greatly but is probably around half that amount.

So what are some of the alternatives besides using long term care insurance? The strategy here is to protect your assets from Medicaid. If you have a long term care event you will be required to spend down all of your assets until you reach the Medicaid asset allowance threshold (approx. $13,000 in assets) before Medicaid will start picking up the tab for your care. Often times we will advise clients to use trusts or gifting strategies to assist them in protecting their assets but this has to be done well in advance of the long term care event. Medicaid has a 5 year look back period which looks at your full 5 year financial history which includes tax returns, bank statements, retirement accounts, etc, to determine if any assets were “given away” within the last 5 years that would need to come back on the table before Medicaid will begin picking up the cost of an individuals long term care costs. A big myth is that Medicare covers the cost of long term care. False, Medicare only covers 100 days following a hospitalization. There are a lot of ins and outs associated with buildings a plan to address the risk of long term care outside of using insurance so it is strongly advised that individuals work with professionals that are well versed in this subject matter when drafting a plan.

An option that is rising in popularity is “semi self-insuring”. Instead of buying a long term care policy that has a $325 per day benefit, an individual can obtain a policy that covers $200 per day. This can dramatically reduce the cost of the LTC policy because it represents less financial risk to the insurance company. You have essentially self insured for a portion of that future risk. The policy will still payout $73,000 per year and the individual will be on the line for $45,625 out of pocket. Versus not having a policy at all and the individual is out of pocket $118,000 in a single year to cover that $325 per day cost.

As you can see there are a number of different options when it come to planning for long term care. It’s about understanding your options and determining which solution is right for your personal financial situation.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Financial Planning To Do's For A Family

My wife and I just added our first child to the family so this is a topic that has been weighing on my mind over the last 40 weeks. I will share just one non-financial takeaway from the entire experience. The global population may be much lower if men had to go through what women do. That being said, this article is meant to be a guideline for some of the important financial items to consider with children. Worrying about your children will never end and being comfortable with the financial aspects of parenthood may allow you to worry a little less and be able to enjoy the time you have with the

My wife and I just added our first child to the family so this is a topic that has been weighing on my mind over the last 40 weeks. I will share just one non-financial takeaway from the entire experience. The global population may be much lower if men had to go through what women do. That being said, this article is meant to be a guideline for some of the important financial items to consider with children. Worrying about your children will never end and being comfortable with the financial aspects of parenthood may allow you to worry a little less and be able to enjoy the time you have with them.

There is a lot of information to take into consideration when putting together a financial plan and the larger your family the more pieces to the puzzle. It is important to set goals and celebrate them when they are met. Everything cannot be done in a day, a week, or a month, so creating a task list to knock off one by one is usually an effective approach. Using relatives, friends, and professionals as resources is important to know what should be on that list for topics you aren’t familiar with.

Create a Budget

It may seem tedious but this is one of the most important pieces of a family’s financial plan. You don’t have to track every dollar coming in and out but having a detailed breakdown on where your money is being spent is necessary in putting together a plan. This simple Expense Planner can serve as a guideline in starting your budget. If you don’t have an accurate idea of where your money is being spent then you can’t know where you can cut back or afford to spend more if needed. Also, the budget is a great topic during a romantic dinner.

You will always want to have 4-6 months expenses saved up and accessible in case a job is lost or someone becomes disabled and cannot work. Having an accurate budget will help you determine how much money you should have liquid.

Insurance

You want to be sure you are sufficiently covered if anything ever happened. One terrible event could leave your family in a situation that may have been avoidable. Insurance is also something you want to take care of as soon as possible so you know the coverage is there if needed.

Health Insurance

Research the policies that are available to you and determine which option may be the most appropriate in your situation. It is important to know the medical needs of your family when making this decision.

Turning one spouse’s single coverage into family coverage is one of the more common ways people obtain coverage for a family. Insurance companies will usually only allow changes to policies through open enrollment or when a “qualifying event” occurs. Having a child is usually a qualifying event but this may only allow the child to be added to one’s coverage, not the spouse. If that is the case, the spouse will want to make sure they have their own coverage until they can be added to the family plan.

It is important to use the resources available to you and consult with your health insurance provider on the ins and outs. If neither spouse has coverage through work, the exchange can be a resource for information and an option to obtain coverage (https://www.healthcare.gov/).

Life Insurance

The majority of people will obtain Term Life Insurance as it is a cost effective way to cover the needs of your family. Life insurance policies have an extensive underwriting process so the sooner you start the sooner you will be covered if anything ever happened. How Much Life Insurance Do I Need?, is an article that may help answer the question regarding the amount of life insurance sufficient for you.

Disability Insurance

The probability of using disability insurance is likely more than that of life insurance. Like life insurance, there is usually a long underwriting process to obtain coverage. Disability insurance is important as it will provide income for your family if you were unable to work. Below are some terms that may be helpful when inquiring about these policies.

Own Occupation – means that insurance will turn on if you are unable to perform YOUR occupation. “Any Occupation” is usually cheaper but means that insurance will only turn on if you can prove you can’t do ANY job.

60% Monthly Income – this represents the amount of the benefit. In this example, you will receive 60% of your current income. It is likely not taxable so the net pay to you may be similar to your paycheck. You can obtain more or less but 60% monthly income is a common benefit amount.

90 Day Elimination Period – this means the benefit won’t start until 90 days of being disabled. This period can usually be longer or shorter.

Cost of Living or Inflation Rider – means the benefit amount will increase after a certain time period or as your salary increases.

Wills, POA’s, Health Proxies

These are important documents to have in place to avoid putting the weight of making difficult decisions on your loved ones. There are generic templates that will suffice for most people but it is starting the process that is usually the most difficult. “What Is The Process Of Setting Up A Will?, is an article that may help you start.

College Savings

The cost of higher education is increasing at a rapid rate and has become a financial burden on a lot of parents looking to pick up the tab for their kids. 529 accounts are a great way to start saving early. There are state tax benefits to parents in some states (including NYS) and if the money is spent on tuition, books, or room and board, the gain from the investments is tax free. Roth IRA’s are another investment vehicle that can be used for college but for someone to contribute to a Roth IRA they must have earned income. Therefore, a newborn wouldn’t be able to open a Roth IRA. Since the gain in 529’s is tax free if used for college, the earlier the dollars go into the account the longer they have to potentially earn income from the market.

529’s can also be opened by anyone, not just the parents. So if the child has a grandparent that likes buying savings bonds or a relative that keeps purchasing clothes the child will wear once, maybe have them contribute to a 529. The contribution would then be eligible for the tax deduction to the contributor if available in the state.

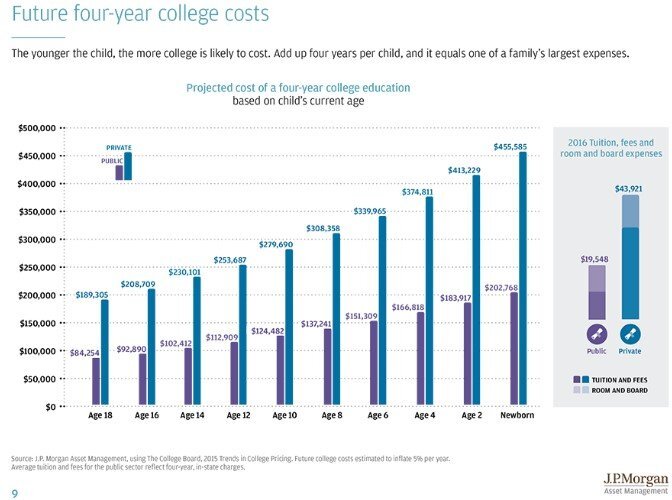

Below is a chart of the increasing college costs along with links to information on college planning.

About Rob……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Should I Buy Or Lease A Car?

This is one of the most common questions asked by our clients when they are looking for a new car. The answer depends on a number of factors:

How long do you typically keep your cars?

How many miles do you typically drive each year?

What do you want your down payment and monthly payment to be?

This is one of the most common questions asked by our clients when they are looking for a new car. The answer depends on a number of factors:

How long do you typically keep your cars?

How many miles do you typically drive each year?

What do you want your down payment and monthly payment to be?

We typically start off by asking how long clients usually keep their cars. If you are the type of person that trades in their car every 2 or 3 year for the new model, leasing a car is probably a better fit. If you typically keep your cars for 5 plus years, then buying a car outright is most likely the better option.

“How many miles do you drive each year?”

This is often times the trump card for deciding to buy instead of lease. Most leases allow you to drive about 12,000 miles per year but this varies from dealer to dealer. If you go over the mileage allowance there are typically sever penalties and it becomes very costly when you go to trade in the car at the end of the lease. We see younger individuals get caught in this trap because they tend to change jobs more frequently. They lease a car when they live 10 miles away from work but then they get a job offer from an employer that is 40 miles away from their house and the extra miles start piling on. When they go to trade in the car at the end of the lease they owe thousands of dollars due to the excess mileage.

We also ask clients how much they plan to put down on the car and what they want their monthly payments to be. If you think you can stay within the mileage allowance, a lease will more often require a lower down payment and have a lower monthly payment. Why? Because you are not “buying” the car. You are simply “borrowing” it from the dealership and your payments are based on the amount that the dealership expects the car to depreciate in value during the duration of the lease. When you buy a car……you own it……and at the end of the car loan you can sell it or continue to drive the car with no car payments.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.