How Pension Income and Retirement Account Withdrawals Can Impact Unemployment Benefits

How Pension Income and Retirement Account Withdrawals Can Impact Unemployment Benefits As the economy continues to slow, unemployment claims continue to rise at historic rates.

How Pension Income and Retirement Account Withdrawals Can Impact Unemployment Benefits

As the economy continues to slow, unemployment claims continue to rise at historic rates. Due to this expected increase in unemployment, the CARES Act included provisions for Coronavirus related distributions which give people access to retirement dollars with more favorable tax treatment. Details on these distributions can be found here. With retirement dollars becoming more accessible with the CARES Act, a common question we are receiving is “Will a retirement distribution impact my Unemployment Benefits?”.

Unemployment Benefits vary from state to state and therefore the answer to this question can be different depending on the state you reside in. This article will focus on New York State Unemployment Benefits, but a lot of the items discussed may be applied similarly in other states.

The answer to this question also depends on the type of retirement account you are receiving money from so we will touch on the most common.

Note: Typically, to qualify for unemployment insurance benefits, you must have been paid minimum wage during the “base period”. Base period is defined as the first four quarters of the last five calendar quarters prior to the calendar quarter which the claim is effective. “Base period employer” is any employer that paid the claimant during the base period.

Pension Reduction

Money received from a pension that a base period employer contributed to will result in a dollar for dollar reduction in your unemployment benefit. Even if you partially contributed to the pension, 100% of the amount received will result in an unemployment benefit reduction.

If you were the sole contributor to the pension, then the unemployment benefit should not be impacted.

Even if you are retired from a job and receiving a pension, you may still qualify for unemployment benefits if you are actively seeking employment.

Qualified Retirement Plans (examples; 401(k), 403(b))

If the account you are accessing is from a base period employer, a withdrawal from a qualified retirement plan could result in a reduction in your unemployment benefit. It is common for retirement plans to include some type of match or profit-sharing element which would qualify as an employer contribution. Accounts which include employer contributions may result in a reduction of your unemployment benefit.

We recommend you contact the unemployment claims center to determine how these distributions would impact your benefit amount before taking them.

IRA

No unemployment benefit rate reduction will occur if the distribution is from a qualified IRA.Knowing there is no reduction caused by qualified IRA withdrawals, a common practice is rolling money from a qualified retirement plan into an IRA and then accessing it as needed. Once you are no longer at the employer, you are often able to take a distribution from the plan. Rolling it into an IRA and accessing the money from that account rather than directly from the retirement plan could result in a higher unemployment benefit.

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

Should I Refinance My Mortgage Now?

With all the volatility going on in the market, it seems there is one certainty and that is the word “historical” will continue to be in the headlines. Over the past few months, we’ve seen the Dow Jones Average hit historical highs, the 10-year treasury hit historical lows, and historical daily point movements in the market.

Should I Refinance My Mortgage Now?

With all the volatility going on in the market, it seems there is one certainty and that is the word “historical” will continue to be in the headlines. Over the past few months, we’ve seen the Dow Jones Average hit historical highs, the 10-year treasury hit historical lows, and historical daily point movements in the market. Market volatility will always lead the headlines as it does impact anyone with an investment account. With that in mind, it is important to use these times to reassess your overall financial plan and take advantage of parts of the plan that are in your control.

For a lot of people, their home is their most significant asset and is held for a longer period than any stock or bond they may have. This brings us back to “historical” as mortgage rates continue to drop. Whenever this happens, our clients will call and ask if it makes sense to refinance. In this article, we will help you in making this decision.

3 Important Questions

How much will I be saving annually in interest with a lower rate?

What are the closing costs of refinancing?

How long do I plan on being in the home and how many more years do I have on the mortgage?

If you can answer these questions, then you should have a pretty good idea if it makes sense for you to refinance.

How Much Will I be Saving Annually in Interest with a Lower Rate?

With most financial decisions, dollars matter. So how do you determine how much you will be saving each year with a lower interest rate? Below, I walk through a very basic example, but it will show the possible advantage of the refinance.

One important note with this example is the fact that most loan payments you make will decrease the principal which should decrease the cost of interest. To make this simple, I assume a consistent mortgage balance throughout the year.

Higher Interest Lower Interest

Mortgage Balance: $300,000 Mortgage Balance: $300,000

Interest Rate: 4.5% Interest Rate: 3.5%

Annual Interest: $13,500 Annual Interest: $10,500

By refinancing at the lower rate, the dollar savings in one year was $3,000 in the example when the mortgage balance was $300,000.

Savings over the life of a mortgage at 3.5% compared to 4.5% on a $300,000, 30-year mortgage, should be over $60,000 in interest over that time period if you are making consistent monthly payments.

What are the Closing Costs of Refinancing?

After walking through the exercise above, most people will say “Of course it makes sense to refinance”. Before making the decision, you must consider the cost of refinancing which can vary from person to person and bank to bank. There are several closing costs to consider which could include title insurance, tax stamps, appraisal fee, application fees, etc.

If the cost of closing is $5,000, you will have to determine how long it will take you to make that back based on the annual interest savings. Using the example from before, if you save $3,000 in interest each year, it should take you 2 years to breakeven.

One tip we give clients is to start at your current lender. Banks are in competition with other banks and they usually do not want to lose business to a competitor. Knowing the current interest rate environment, a lot of institutions will offer a type of “rapid refinance” for existing customers which may make the process easier but also give you a break on the closing costs if you are staying with them. This should be taken into consideration along with the possibility of getting an even lower interest rate from a different institution which could save you more in the long run even if closing costs are higher.

How Long do I Plan on Being in the Home and How Many More Years do I have on the Mortgage?

This is important since there is a cost to refinancing your mortgage. If it will take you 10 years to “breakeven” between the closing costs and interest you are saving but only plan on being in the house for 5 more years, refinancing may not be the right choice. Also, if you only have a few years left to pay the mortgage you would have to weigh your options.

In summary, taking advantage of these historical low mortgage rates could save you a lot of dollars over the long term but you should consider all the costs associated with it. Taking the time to answer these questions and shop around to make sure you are getting a good deal should be worth the effort.

Public Service Announcement: Like the stock market, it is hard to say anyone has the capability of knowing for sure when interest rates will hit their lows. Make sure you are comfortable with the decision you are making and if you do refinance try not to have buyer’s remorse if the historical lows today turn into new historical lows next year.

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

When Do Higher Interest Rates Become Harmful To The Stock Market?

On Friday, the jobs report came out and it was a strong report. The consensus was expecting 180,000 new jobs in January and the actual number released on Friday ended up being 200,000. So why did the markets drop? The answer: wage growth. The jobs report not only contains how many new employees were hired but it also includes the amount

On Friday, the jobs report came out and it was a strong report. The consensus was expecting 180,000 new jobs in January and the actual number released on Friday ended up being 200,000. So why did the markets drop? The answer: wage growth. The jobs report not only contains how many new employees were hired but it also includes the amount that wages for the current workforce either increased or decreased on a year over year basis. The report on Friday indicated that wages went up by 2.9% year over year. That is the strongest wage growth number since 2009.

Double Edged Sword

Wage growth is a double edged sword. On the positive side, when wages are going up, people have more money in their paychecks which allows them to spend more and consumer spending makes up 70% of our GDP in the United States. I'm actually surprised the market did not see this coming. The whole premise behind tax reform was "if we give U.S. corporations a tax break, they will use that money to hire more employees and increase wages." The big question people had with the tax reform was "would the trickle down of the dollars saved by the corporations eventually make it to the employees pockets?" Many corporations in January, as a result of tax reform, announced employee bonuses and increases to the minimum wage paid within their organizations. The wage growth number on Friday would seem to imply that this is happening. So again, I'm actually surprised that the market was not ready for this and while the market reacted negatively I see this more as a positive long term trend, instead of a negative one. If instead the U.S. corporations decided not to give the bonuses or increase wages for employees and just use the money from the tax reform savings to increase dividends or share buybacks, then you probably would have seen only a moderate increase in the wage growth number. But that also would imply that there would be no "trickle down" effect to the middle class.

The Downside

This all sounds really positive but what is the downside to wage growth? While wage growth is good for employees, it's bad for corporate earnings. If I was paying Employee A $50,000 in 2017 but now I'm paying them $55,000 per year in 2018, assuming the output of that employee did not change, the expenses to the company just went up by $5,000 per year. Now multiply that over thousands of employees. It's a simple fact that higher expenses without higher output equals lower profits.

Wage Growth = Inflation

There is another downside to wage growth. Wage growth is the single largest contributor to inflation. Inflation is what we use to measure the increase in the price of goods and services in the U.S.. Why are these two measurements so closely related? If your salary just increased by $300 per month, when you go to the grocery store to buy milk, you may not notice that the price of milk went up by $0.15 over last week because you are making more in your paycheck. That is inflation. The price of everything starts going up because, in general, consumers have more take home pay and it gives the sellers of goods and services more pricing power. Visa versa, when the economy is in a recession, people are losing their jobs, and wages are decreasing. If you sell cars and you decided to raise the price of the cars that you sell, that may cause the consumer to not buy from you and look for a lower priced alternative. Companies have less pricing power when the economy is contracting and you typically have "deflation" not inflation.

When Does Inflation Become Harmful?

Some inflation is good. It means the economy is doing well. A rapid increase in inflation is bad because it forces the Fed to use monetary policy to slow down the economy so it does not over heat. The Fed uses the Federal Funds Rate as their primary tool to keep inflation in check. When inflation starts heating up, the Fed will often raise the Fed Funds Rate to increase the cost of lending which in turn reduces the demand for lending. It’s like tapping the brakes in your car to make sure you do not accelerate too quickly and then go flying off the road.

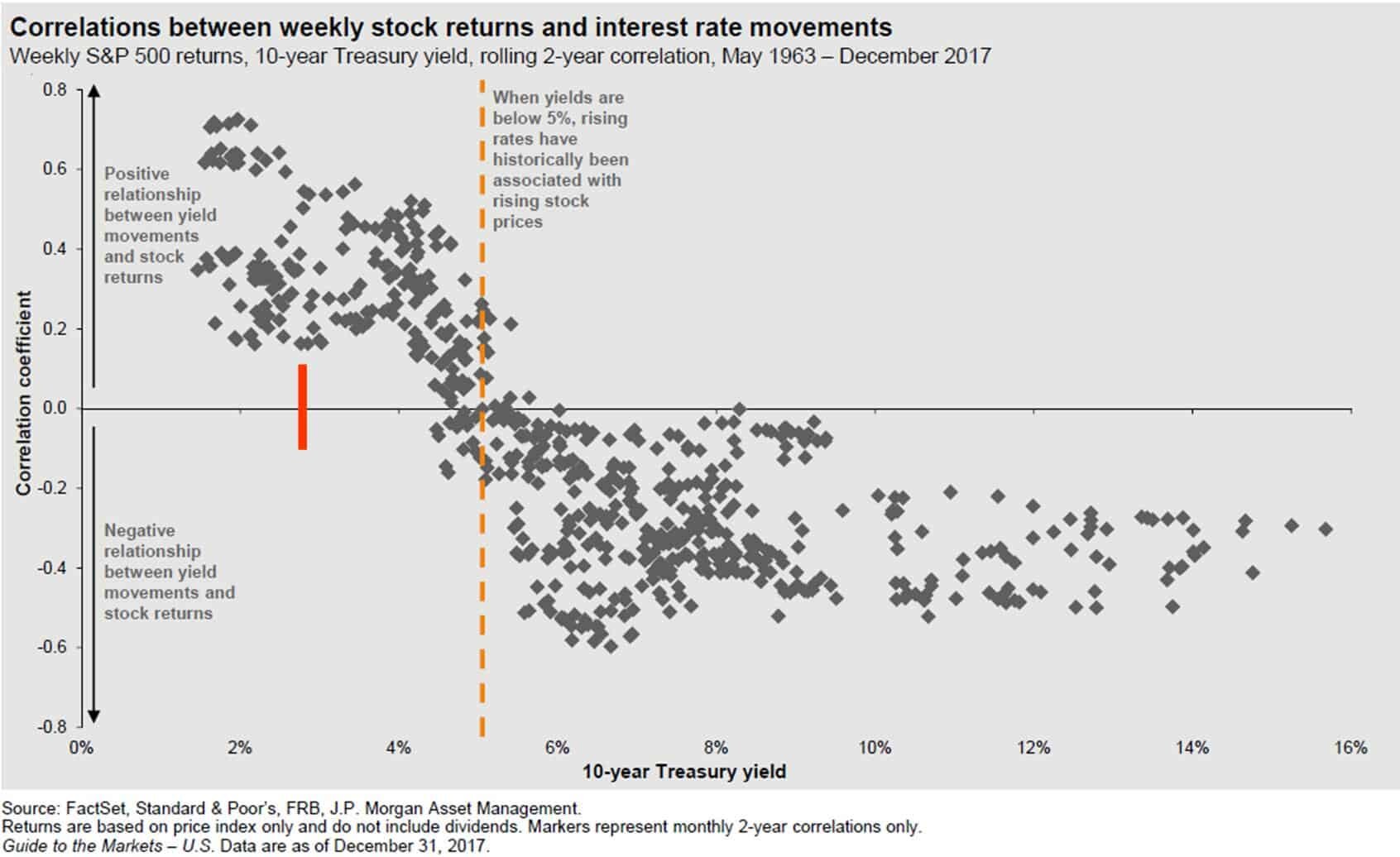

If some inflation is good but too much inflation is bad, the question is at what point do higher interest rates really jeopardize economic growth? The chart below provides us with guidance as to what has happened in the past when interest rates were on the rise.

correlation between interest rates and stocks

The chart compares every 2 year period in the stock market versus the level of the 10-Year Treasury yield between 1963 – 2017. For example, one dot would represent the time period 1963 – 1964. Another dot would represent 1964 – 1965 and so on. If the dot is above the “0.0” line, that means that there was a “positive correlation” between stock prices going up and the interest rate on the 10-Year Treasury yield going up during that same time period. Worded another way, when the dot is above the line that means the stock market was going up while interest rates were also increasing. In general, the dots above the line are good, when they are below the line, that’s bad.

Right now the 10-Year Treasury Bond is at 2.85% which is the red line on the chart. What we can conclude from this is going all the way back to 1963, at this data point, there has never been a two year period where interest rates were rising and stock prices were falling. Could it be different this time? It could, but it’s a low probability if we use historical data as our guide. History would suggest that we do not run into trouble until the yield on the 10-Year Treasury Bond gets above 4%. Once the yield on our 10-Year Treasury Bond reaches that level and interest rates are rising, historically the correlation between rising interest rates and stock prices turns negative. Meaning interest rates are going up but stock prices are going down.

It makes sense. Even though interest rates are moving up right now, they are still at historically low levels. So lending is still “cheap” by historical standards which will continue to fuel growth in the economy.

A Gradual Rise In Interest Rates

Most fixed income managers that we speak with are expecting a gradual rise in interest rates throughout 2018. While we expect interest rates to move higher throughout the year due to an increase in wage growth as a result of a tighter labor market, in our opinion, it’s a stretch to make the case that the yield on the 10-year Treasury will be at 4% by the end of the year.

If the U.S. was the only country in the world, I would feel differently. Our economy is continuing to grow, wages are increasing, the labor markets are tight which requires companies to pay more for good employees, and all of these factors would warrant a dramatic increase in the rate of inflation. But we are not the only country in the world and the interest rate environment in the U.S. is impacted by global rates.

The chart below illustrates the yield on a 10 year government bonds for the U.S., Japan, Germany, UK, Italy, Spain, and total “Global Ex-U.S.”.

global interest rates

On December 31, 2017 the yield on a 10-Year Government Bond in the U.S. was 2.71%. The yield on a 10-Year government bond in Germany was only 0.46%. So, if you bought a 10-Year Government Bond from Germany, they are going to hand you back a measly 0.46% in interest each year for the next 10 years.

Why is this important? The argument can be made that while the changes in the Fed Funds Rate may have a meaningful impact on short-term rates, it may have less of an impact on intermediate to longer term interest rates. When the U.S. government needs more money to spend they conduct “treasury auctions”. The government announces that on a specified date that they are going to be selling “30 million worth of 10-year treasury bonds at a 2.8% rate”. As long as there is enough demand to sell all of the bonds at the 2.8% rate, the auction is a success. If there is not enough demand, then they may have to increase the interest rate from 2.8% to 3% to sell all $30 million worth of the bonds. While the U.S. 10-Year Treasury Bond only had a yield of 2.71%, it’s a lot higher than the other trusted government lenders around the world. As you can see in the chart above, the average 10-year government bond yield excluding the U.S. is 1.03%. This keeps the demand for U.S. debt high without the need to dramatically increase the interest rate on new government debt issuance to attract buyers of the debt.

As for the trend in global interest rates, you will see in the chart that from September 30, 2017 to December 31, 2017, global 10-year government bond yields ex-U.S. decreased from 1.05% to 1.03%. While we are in the monetary tightening cycle in the U.S., there is still monetary easing happening around the world as a whole which should prevent our 10-year treasury yields from spiking over the next 12 months.

Impact on Investment Portfolios

The media will continue to pounce on this story about “the risk of rising interest rates and inflation” throughout 2018 but it’s important to keep it in context. If tax reform works the way that it’s supposed to, wage growth should continue but we may not see the positive impact of increased consumer spending due to the wage growth until corporate earnings are released for the first and second quarter of 2018. We just have to wait to see how the strength of consumer spending nets out against the pressure on corporate earnings from higher wages.

However, investors should be looking at the fixed income portion of their portfolio to make sure there is the right mix of bonds if inflation is expected to rise throughout the year. Bond duration and credit quality will play an important role in your fixed income portfolio in 2018.

About Michael.........

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

How Pass-Through Income Will Be Taxed For Small Business Owners

While one of the most significant changes incorporated in the new legislation was reducing the corporate tax rate from the current 35% rate to a 21% rate in 2018, the tax bill also contains a big tax break for small business owners. Unlike large corporations that are taxed at a flat rate, most small businesses, are "pass-through" entities, meaning that the

While one of the most significant changes incorporated in the new legislation was reducing the corporate tax rate from the current 35% rate to a 21% rate in 2018, the tax bill also contains a big tax break for small business owners. Unlike large corporations that are taxed at a flat rate, most small businesses, are "pass-through" entities, meaning that the profits from the business flow through to the business owner's personal tax return and then are taxed at ordinary income tax rates.While pass-through income will continue to be taxed at ordinary income tax rates, many small business owners will be eligible to deduct 20% of their "qualified business income" (QBI) starting in 2018. In other words, some pass-through entities will only be taxes on 80% of their pass-through income.

Pass-through entities include

Sole proprietorships

Partnerships

LLCs

S-Corps

Unanswered Questions

I wanted to write this article to give our readers the framework of what we know at this point about the treatment of the pass-through income in 2018. However, as many accountants will acknowledge, there seems to be more questions at this point then there are answers. The IRS will need to begin issuing guidance at the beginning of 2018 to clear up many of the unanswered questions as to who will be eligible and not eligible for the new 20% deduction.

Above or Below "The Line"

This 20% deduction will be a below-the-line deduction which is an important piece to understand. Tax lingo makes my head spin as well, so let's pause for a second to understand the difference between an "above-the-line deduction" and a "below-the-line deduction".The "line" refers to the AGI line on your tax return which is the bottom line on the first page of your Form 1040. While both above-the-line and below-the-line deductions reduce your taxable income, it's important to understand the difference between the two.

Above-The-Line Deductions

Above-the-line deductions happen on the first page of your tax return. These deductions reduce your gross income to eventually reach your AGI (adjusted gross income) for the year. Above-the-line deductions include:

Contributions to health savings accounts

Contributions to retirement plans

Deduction for one-half of the self-employment taxes

Health insurance premiums paid

Alimony paid, student loan interest, and a few others

The AGI is important because the AGI is used to determine your eligibility for certain tax credits and it will also have an impact on which below-the-line deductions you are eligible for. In general, the lower your AGI is, the more deductions and credits you are eligible to receive.

Below-The-Line Deductions

Below-the-line deductions are reported on lines that come after the AGI calculation. They are comprised mainly of your “standard deduction” or “itemized deductions” and “personal exemptions” (most of which will be gone starting in 2018). The 20% deduction for qualified business income will fall into this below-the-line category. It will lower the income of small business owners but it will not lower their AGI.

However, it was stated in the tax legislation that even though the 20% qualified business deduction will be a below –the-line deduction it will not be considered an “itemized deduction”. This is a huge win!!! Why? If it’s not an itemized deduction, then small business owners can claim the 20% qualified business income deduction and still claim the standard deduction. This is an important note because many small business owners may end up taking the standard deduction for the first time in 2018 due to all of the deductions and tax exemptions that were eliminated in the new tax bill. The tax bill took away a lot of big deductions:

Capped state and local taxes at $10,000 (this includes state income taxes and property taxes)

Eliminated personal exemptions ($4,050 for each individual) (Eliminated in 2018)

Family of 4 = $4,050 x 4 = $16,200 (Eliminated in 2018)

Miscellaneous itemized deductions subject to 2% of AGI floor (Eliminated in 2018)

Restrictions On The 20% Deduction

If life were easy, you could just assume that I'm a sole proprietor, I make $100,000 all in pass-through income, so I will get a $20,000 deduction and only have to pay tax on $80,000 of my income. For many small business owners it may be that easy but what's a tax law without a list of restrictions.The restriction were put in place to prevent business owners from reclassifying their W2 wages into 100% pass-through income to take advantage of the 20% deduction . They also wanted to restrict employees from leaving their company as a W2 employee, starting a sole proprietorship, and entering into a sub-contractor relationship with their old employer just to reclassify their W2 wages into 100% pass-through income.

S-Corps

Qualified business income will specifically exclude "reasonable compensation" paid to the owner-employee of an S-corp. While it would seem like an obvious reaction by S-corp owners to reduce their W2 wages in 2018 to create more pass through income, they will still have to adhere to the "reasonable compensation" restriction that exists today.

Partnerships & LLCs

Qualified business income will specifically exclude guaranteed payments associated with partnerships and LLCs. This creates a grey area for these entities. Partnerships do not have a “reasonable compensation” requirement like S-corps since companies taxed as partnerships are not allowed to pay W2 wages to the owners. Also the owners of partnerships are not required to take guaranteed payments. My guess is, and this is only a guess, that as we get further into 2018, the IRS may require partnerships to classify a percentage of a owners total compensation as a “guaranteed payment” similar to the “reasonable compensation” restriction that S-corps currently adhere too. Otherwise, partnerships can voluntarily eliminate guaranteed payments and take the 20% deduction on 100% of the pass-through income.

This may also prompt some S-corps to look at changing their structure to a partnership or LLC. For high income earners, S-corps have an advantage over the partnership structure in that the owners do not pay self-employment tax on the pass-through income that is distribution to the owner over and above their W2 wages. However, S-corp owners will have to weigh the self-employment tax benefit against the option of changing their corporate structure to a partnership and potentially receiving a 20% deduction on 100% of their income.

Sole Proprietors

Sole proprietors do not have "reasonable compensation" requirement or "guaranteed payments" so it would seem that 100% of the income generated by sole proprietors will count as qualified business income. Unless the IRS decides to enact a "reasonable compensation" requirement for sole proprietors in 2018, similar to S-corps. Before everyone runs from a single member LLC to a sole proprietorship, remember, a sole proprietorship offers no liability barrier between the owner and liabilities that could arise from the business.

Income Restrictions

There are limits that are imposed on the 20% deduction based on how much the owner makes in “taxable income”. The thresholds are set at the following amounts:

Individual: $157,500

Married: $315,000

The thresholds are based on each business owner’s income level, not on the total taxable income of the business. We need help from the IRS to better define what is considered “taxable income” for purposes of this phase out threshold. As of right now, it seems that “taxable income” will be defined as the taxpayer’s own taxable income (not AGI) less deductions.

If the owner’s taxable income is below this threshold, then the calculation is a simple 20% deduction of the pass-through income. If the owner’s taxable income exceeds the threshold, the qualified business deduction is calculated as follows:

The LESSER of:

20% of its business income OR 50% of the total wages paid by the business to its employees

Let’s look at this in a real life situation. A manufacturing company has a net profit of $2M in 2018 and pays $500,000 in wages to its employees during the year. That company would only be able to take the qualified business income deduction for $250,000 since 50% of the total employee wages ($500,000 x 50% = $250,000) are less than 20% of the net income of the business ($2M x 20% = $400,000).

This creates another grey area because it seems that the additional calculation is triggered by the taxable income of each individual owner but the calculation is based on the total profitability and wages paid by the company. For the owners that required this special calculation for exceeding the threshold, how is their portion of the lower deduction amount allocated? Multiplying the lower total deduction amount by the percent of their ownership? Just more unanswered questions.:

Restrictions For "Service Business"

There will be restrictions on the 20% deduction for pass-through entities that are considered a "service business" under IRC Section 1202(e)(3)(A). The businesses specifically included in this definition as a services business are:

Health

Law

Accounting

Actuarial Sciences

Performing Arts

Consulting

Athletics

Financial Services

Any other trade or business where the principal asset of the business is the reputation or skill of 1 or more of its employees

In a last minute change to the regulations, to their favor, engineers and architects were excluded from the definition of “service businesses”.

This is another grey area. Many small businesses that fall outside of the categories listed above will undoubtedly be asking the question: “Am I considered a service business or not?” Outside of the industries specifically listed in the tax bill, we really need more guidance from the IRS.

If you are a “services business”, when the tax reform was being negotiated it looked like service businesses were going to be completely excluded from the 20% deduction. However, the final regulations were more kind and instead implemented a phase out of the 20% deduction for owners of service businesses over a specified income threshold. The restriction will only apply to those whose “taxable income” exceeds the following thresholds:

Individual: $157,500

Married: $315,000

If you are a consultant or owner of a services business and your taxable income is below these thresholds, it would seem at this point that you will be able to capture the 20% deduction for your pass-through income. As mentioned above, we need help from the IRS to clarify the definition of “taxable income”.

Phase Out For Service Businesses

The amounts listed above: $157,500 for individual and $315,000 for a married couple filing joint, are where the thresholds for the phase out begins. The service business owners whose income rises above those thresholds will phase out of the 20% deduction over the next $50,000 of taxable income for individual filers and $100,000 of taxable income for married filing joint. This means that the 20% pass-through deduction is completely gone by the following income levels:

Individual: $207,500

Married: $415,000

Any taxpayer’s falling in between the threshold and the phase out limit will receive a portion of the 20% deduction.

Since the thresholds are assessed based on the taxpayer’s own taxable income and not the total income of the business, a service business could be in a situation, like in an accounting firm, where the partners with the largest ownership percentage may not qualify for 20% deduction but the younger partners may qualify for the deduction because their income is lower.

Tax Planning For 2018

It's an understatement to say that most small business owners will need to spend a lot of time with their accountant in the first quarter of 2018 to determine the best of course of action for their company and their personal tax situation.While we are still waiting for clarification on a number of very important items associated with the 20% deduction for qualified business income, hopefully this article has provided our small business owners with a preview of things to come in 2018.

Disclosure: I'm a Certified Financial Planner® but not an accountant. The information contained in this article was generated from hours and hours of personal research on the topic. I advise each of our readers to consult with your personal tax advisor for tax advice.

About Michael.........

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Tax Reform: Your Company May Voluntarily Terminate Your Retirement Plan

Make no mistake, your company retirement plan is at risk if the proposed tax reform is passed. But wait…..didn’t Trump tweet on October 23, 2017 that “there will be NO change to your 401(k)”? He did tweet that, however, while the tax reform might not directly alter the contribution limits to employer sponsored retirement plans, the new tax rates

Make no mistake, your company retirement plan is at risk if the proposed tax reform is passed. But wait…..didn’t Trump tweet on October 23, 2017 that “there will be NO change to your 401(k)”? He did tweet that, however, while the tax reform might not directly alter the contribution limits to employer sponsored retirement plans, the new tax rates will produce a “disincentive” for companies to sponsor and make employer contributions to their plans.

What Are Pre-Tax Contributions Worth?

Remember, the main incentive of making contributions to employer sponsored retirement plans is moving income that would have been taxed now at a higher tax rate into the retirement years, when for most individuals, their income will be lower and that income will be taxed at a lower rate. If you have a business owner or executive that is paying 45% in taxes on the upper end of the income, there is a large incentive for that business owner to sponsor a retirement plan. They can take that income off of the table now and then realize that income in retirement at a lower rate.

This situation also benefits the employees of these companies. Due to non-discrimination rules, if the owner or executives are receiving contributions from the company to their retirement accounts, the company is required to make employer contributions to the rest of the employees to pass testing. This is why safe harbor plans have become so popular in the 401(k) market.

But what happens if the tax reform is passed and the business owners tax rate drops from 45% to 25%? You would have to make the case that when the business owner retires 5+ years from now that their tax rate will be below 25%. That is a very difficult case to make.

An Incentive NOT To Contribute To Retirement Plans

This creates an incentive for business owners NOT to contribution to employer sponsored retirement plans. Just doing the simple math, it would make sense for the business owner to stop contributing to their company sponsored retirement plan, pay tax on the income at a lower rate, and then accumulate those assets in a taxable account. When they withdraw the money from that taxable account in retirement, they will realize most of that income as long term capital gains which are more favorable than ordinary income tax rates.

If the owner is not contributing to the plan, here are the questions they are going to ask themselves:

Why am I paying to sponsor this plan for the company if I’m not using it?

Why make an employer contribution to the plan if I don’t have to?

This does not just impact 401(k) plans. This impacts all employer sponsored retirement plans: Simple IRA’s, SEP IRA’s, Solo(k) Plans, Pension Plans, 457 Plans, etc.

Where Does That Leave Employees?

For these reasons, as soon as tax reform is passed, in a very short time period, you will most likely see companies terminate their retirement plans or at a minimum, lower or stop the employer contributions to the plan. That leaves the employees in a boat, in the middle of the ocean, without a paddle. Without a 401(k) plan, how are employees expected to save enough to retire? They would be forced to use IRA’s which have much lower contribution limits and IRA’s don’t have employer contributions.

Employees all over the United States will become the unintended victim of tax reform. While the tax reform may not specifically place limitations on 401(k) plans, I’m sure they are aware that just by lowering the corporate tax rate from 35% to 20% and allowing all pass through business income to be taxes at a flat 25% tax rate, the pre-tax contributions to retirement plans will automatically go down dramatically by creating an environment that deters high income earners from deferring income into retirement plans. This is a complete bomb in the making for the middle class.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.