2026 Medicare IRMAA Brackets: What Triggers Higher Premiums and How to Avoid

Medicare IRMAA (Income-Related Monthly Adjustment Amount) is a surcharge added to Medicare Part B and Part D premiums when your income exceeds certain thresholds. These surcharges are based on your Modified Adjusted Gross Income (MAGI) from two years prior. At Greenbush Financial Group, our analysis shows that proactive tax and withdrawal planning can help retirees avoid or minimize IRMAA and significantly reduce long-term healthcare costs.

What Is Medicare IRMAA and How Does It Work?

IRMAA is an additional premium Medicare beneficiaries pay if their income exceeds specific limits.

Key Facts

Applies to Medicare Part B and Part D

Based on income from two years prior

Uses Modified Adjusted Gross Income (MAGI)

Adjusted annually for inflation

Example

Your 2026 Medicare premiums are based on your 2024 income.

This lag creates planning opportunities, especially in early retirement years.

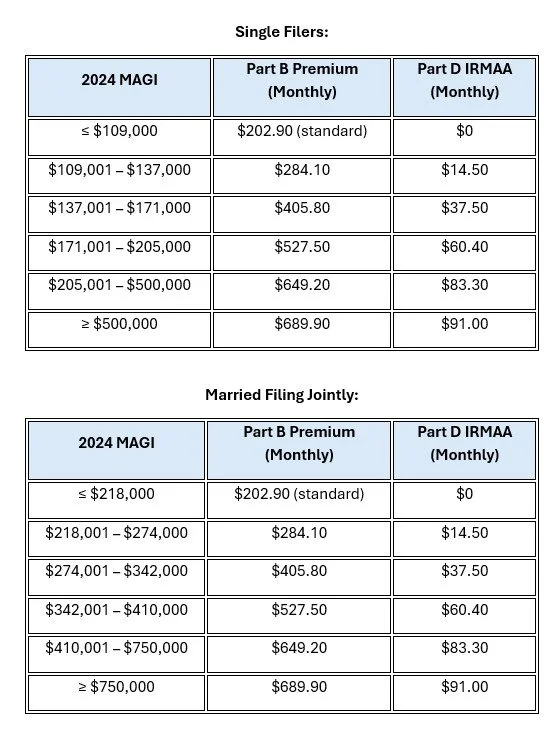

2026 IRMAA Income Limits and Surcharge Brackets

IRMAA is triggered when your income crosses certain thresholds.

2026 Estimated IRMAA Thresholds

At Greenbush Financial Group, we emphasize that even $1 over a threshold can trigger a significantly higher premium.

What Counts as Income for IRMAA (MAGI)?

IRMAA is based on Modified Adjusted Gross Income, which includes more than just wages.

Included Income Sources

IRA and 401(k) withdrawals

Capital gains from investments

Dividends and interest

Rental income

Social Security (partially taxable portion)

Roth conversions

Important Note

Tax-free municipal bond interest is also included in MAGI for IRMAA purposes.

How Much Are IRMAA Surcharges?

IRMAA increases both Part B and Part D premiums.

Example Impact

Standard Part B premium (baseline)

IRMAA can increase premiums by hundreds of dollars per month per person

Part D surcharges are smaller but still meaningful

Key Insight

Over a 10–20 year retirement, IRMAA can add up to tens of thousands of dollars in additional healthcare costs if not managed properly.

Planning Strategies to Reduce or Avoid IRMAA

Strategic income planning is the most effective way to manage IRMAA.

1. Manage Your Taxable Income Each Year

Stay below key IRMAA thresholds when possible

Avoid large one-time income spikes

2. Use Roth Conversions Strategically

Convert funds in lower-income years before Medicare

Reduce future taxable income and RMDs

3. Time Large Withdrawals Carefully

Spread income over multiple years

Avoid triggering IRMAA in a single year

4. Leverage Roth Accounts

Roth withdrawals do not increase MAGI

Provides tax-free income flexibility

5. Consider Capital Gains Timing

Harvest gains in lower-income years

Offset gains with losses when possible

At Greenbush Financial Group, we often build multi-year tax projections to help clients stay below IRMAA thresholds.

IRMAA Planning Before and After Retirement

Before Retirement (Ages 55–63)

Ideal window for Roth conversions

Lower income years create planning opportunities

Reduce future IRMAA exposure

Early Retirement (Before Medicare)

Control income levels carefully

Balance withdrawals across accounts

After Age 65

Monitor RMDs and income levels

Use Roth withdrawals to manage thresholds

Plan ahead for future income spikes

What Happens If Your Income Drops?

You may be able to appeal IRMAA if your income has decreased due to certain life events.

Qualifying Life-Changing Events

Retirement

Marriage or divorce

Death of a spouse

Loss of income-producing property

You can file an appeal with Social Security to request a lower premium.

Common IRMAA Mistakes to Avoid

Ignoring IRMAA when doing Roth conversions

Taking large IRA withdrawals in a single year

Not planning for RMDs

Overlooking capital gains impact

Assuming Medicare premiums are fixed

At Greenbush Financial Group, we often see that IRMAA surprises retirees who focus only on taxes without considering healthcare costs.

Final Thoughts

IRMAA is one of the most overlooked retirement expenses, yet it can significantly increase your Medicare costs. The key is not just minimizing taxes in a single year but managing income over time to avoid crossing key thresholds.

At Greenbush Financial Group, our analysis shows that proactive planning around withdrawals, Roth conversions, and income timing can help reduce IRMAA and improve overall retirement outcomes.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

Frequently Asked Questions

-

What does IRMAA stand for?Income-Related Monthly Adjustment Amount, a surcharge on Medicare premiums based on income.

-

What income is used to calculate IRMAA?Modified Adjusted Gross Income (MAGI) from two years prior.

-

Can Roth withdrawals trigger IRMAA?No, qualified Roth withdrawals do not increase MAGI.

-

Can IRMAA be appealed?Yes, if you have a qualifying life-changing event such as retirement or loss of income.

-

How can I avoid IRMAA surcharges?By managing taxable income, using Roth strategies, and avoiding large income spikes.