What Retirees Regret Most About the First 10 Years of Retirement

The first decade of retirement offers some of your greatest opportunities. Learn the most common regrets retirees share and how thoughtful planning can help you avoid them.

Ask retirees what they wish they had done differently, and you'll hear many of the same answers.

Rarely do they say they wish they had saved more after retirement.

More often, they regret waiting.

Waiting to travel. Waiting to spend. Waiting to make tax planning decisions. Waiting to enjoy the freedom they spent decades working toward.

While every retirement is different, a few common regrets come up time and time again.

1. Claiming Social Security Too Early

Many retirees claim Social Security as soon as they're eligible without fully understanding how the decision affects lifetime income.

Claiming early can make sense in certain situations, but for others, waiting may provide:

Higher lifetime benefits.

Greater survivor benefits for a spouse.

More guaranteed income later in life.

This is one of the most permanent retirement decisions you'll make, so it's worth evaluating carefully.

2. Being Too Conservative With Investments

It's natural to become more cautious after retiring.

However, some retirees become so conservative that their portfolios struggle to keep pace with inflation.

The goal isn't to avoid all market risk.

It's to build an investment strategy that supports decades of retirement while still providing growth potential.

3. Waiting Too Long to Travel

Many retirees plan to travel "someday."

Unfortunately, health issues often become a limiting factor before finances do.

Example

A couple spends the first eight years of retirement delaying international travel because they're worried about market volatility.

By the time they feel financially comfortable, one spouse develops mobility challenges that make those trips much more difficult.

Key Insight

Your healthiest retirement years are often your most valuable. Don't assume they'll last forever.

4. Delaying Roth Conversions

Many retirees spend the years between retirement and Required Minimum Distributions (RMDs) in relatively low tax brackets.

Some never take advantage of that window.

Later, large RMDs increase:

Taxable income.

Medicare premiums.

Taxes paid by surviving spouses.

Tax burdens for heirs.

Proactive tax planning early in retirement can create flexibility later.

5. Not Simplifying Their Finances

Over the years, it's easy to accumulate:

Multiple retirement accounts.

Old 401(k)s.

Several brokerage accounts.

Numerous bank accounts.

Insurance policies that no longer serve a purpose.

Many retirees wish they had simplified sooner.

Consolidating accounts doesn't just reduce paperwork. It can make managing finances easier for both spouses and eventually for family members.

6. Focusing So Much on Saving That They Forgot to Enjoy Retirement

Perhaps the most common regret has little to do with money.

Many retirees realize they spent decades preparing for retirement but struggled to actually enjoy it.

They postponed experiences because they were afraid of spending too much.

Years later, they recognized they had far more financial security than they believed.

A good retirement plan should provide confidence, not just caution.

Learn While You Have Options

One reason these regrets are so common is that many retirement decisions become harder to change over time.

The first decade of retirement often provides the greatest flexibility for:

Tax planning.

Travel.

Spending decisions.

Lifestyle changes.

Charitable giving.

Family experiences.

Making thoughtful decisions early can have benefits for years to come.

Common Theme: Waiting Too Long

Although every retiree's story is different, many regrets come back to the same idea.

"I wish we hadn't waited."

Whether it's traveling, spending, simplifying finances, or reducing future taxes, opportunities are often greatest when you're healthy and have the most flexibility.

Planning Helps Turn Regret Into Confidence

No retirement plan will eliminate every surprise.

But thoughtful planning can reduce the chances of looking back and wishing you had made different decisions.

At Greenbush Financial Group, we encourage clients to think beyond investment returns. Retirement is about making the most of your time, your resources, and the opportunities that matter most while you still have them.

Final Thoughts

The first 10 years of retirement are often called the "go-go years" for a reason.

They're typically the years when retirees have the most freedom, energy, and flexibility.

Looking back, many retirees don't regret spending too much.

They regret waiting too long to do the things they had always planned to do.

A well-designed retirement plan should help you protect your future while giving you the confidence to enjoy the present.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

Frequently Asked Questions

- What's the biggest regret retirees have?Many retirees say they waited too long to travel, spend on meaningful experiences, or make important financial planning decisions.

- Is claiming Social Security early always a mistake?No. The best claiming age depends on your health, marital status, income needs, and overall retirement plan.

- Why are the first 10 years of retirement so important?For many people, these are the healthiest and most active years of retirement, making them an ideal time for travel, hobbies, and proactive financial planning.

- Why do retirees regret delaying Roth conversions?Converting retirement assets during lower-income years may reduce future RMDs and lifetime taxes. Waiting can mean losing that planning opportunity.

- How can I avoid common retirement regrets?Create a comprehensive retirement plan that addresses not only investments but also taxes, spending, healthcare, and your personal goals for retirement.

The First Year of Retirement: 7 Financial Moves to Make…and 5 to Avoid

The first year of retirement is one of the most important financial transition periods retirees face. This article explains how to build a retirement withdrawal strategy, evaluate Social Security timing, manage Roth conversion opportunities, avoid Medicare IRMAA surprises, and adjust investment risk after leaving work. Learn the financial mistakes many retirees make during year one and how thoughtful planning can improve long-term retirement income sustainability. Greenbush Financial Group outlines practical retirement planning strategies designed to help retirees build confidence and flexibility during the transition into retirement.

The first year of retirement is one of the most important financial transition periods you’ll ever experience. Decisions around withdrawals, Social Security, taxes, investments, and healthcare can affect your retirement income for decades. Many retirees focus on enjoying newfound freedom but overlook key planning opportunities that exist before year-end and before required distributions begin. At Greenbush Financial Group, we often see that the retirees who build confidence early are the ones who slow down and make intentional first-year decisions.

The First Year of Retirement Is a Transition Year, Not Just a Celebration Year

Retirement changes more than your schedule. It changes how your household generates income, pays taxes, handles market volatility, and manages financial decisions.

For decades, most people operated under a simple formula:

Work

Receive paycheck

Save for retirement

Repeat

Then retirement arrives, and suddenly everything reverses.

Now your investments may need to generate income. Tax planning becomes more flexible but also more important. Healthcare costs become more visible. Market declines can feel more emotional once paychecks stop.

The first year of retirement is often what we call an “adjustment year.” The decisions made during this period can shape:

Future tax brackets

Medicare premiums

Portfolio longevity

Social Security income

Roth conversion opportunities

Spending habits

Confidence during market volatility

The goal is not perfection.

The goal is avoiding expensive mistakes while building a sustainable retirement income strategy.

7 Smart Financial Moves to Make During Your First Year of Retirement

1. Build a Retirement Paycheck Plan Before Taking Withdrawals

One of the biggest mistakes new retirees make is randomly pulling money from accounts as expenses arise.

Retirement income should be coordinated intentionally.

Before taking withdrawals, determine:

How much monthly income you actually need

Which accounts will fund that income

How taxes will affect withdrawals

Which accounts should remain invested longer

How cash reserves will be handled

Many retirees discover their actual spending differs from what they expected.

The first year is often more expensive because of:

Travel

Home projects

Healthcare changes

Helping family

Celebration spending

A paycheck-style withdrawal strategy can create structure and reduce emotional decision-making.

Example

A retired couple needs $7,000 per month after taxes.

They have:

$1.2 million invested

$700,000 in IRAs

$300,000 in taxable accounts

$200,000 in Roth IRAs

No Social Security yet

Instead of withdrawing entirely from their IRA, they may benefit from:

Using taxable savings first

Realizing lower capital gains

Keeping taxable income lower

Preserving future Roth growth opportunities

The order of withdrawals matters more than many retirees realize.

2. Reevaluate Whether to Claim Social Security Immediately

Many retirees automatically claim Social Security as soon as work ends.

That decision can permanently reduce lifetime income.

For healthy retirees with adequate assets, delaying benefits can sometimes improve long-term retirement security.

Key factors include:

Health and longevity expectations

Spousal benefits

Survivor income planning

Tax brackets

Portfolio withdrawal needs

Other income sources

Important Note

Claiming early is not always wrong.

But the first year of retirement is the time to evaluate the decision carefully rather than defaulting to “I stopped working, so I should claim now.”

Example

A retiree eligible for $2,200/month at age 62 may receive roughly $3,900/month if delaying until age 70.

For married couples, this can significantly affect survivor income later.

3. Review Roth Conversion Opportunities Before Year-End

The years between retirement and Required Minimum Distributions (RMDs) can create unusually low-income tax years.

Those years may offer valuable Roth conversion opportunities.

This is one of the most overlooked planning opportunities in retirement.

Converting portions of a traditional IRA to a Roth IRA during lower-income years may help:

Reduce future RMDs

Lower future tax exposure

Create tax-free income later

Reduce widow’s tax risk

Improve long-term tax flexibility

Example

A couple retires at 64 and delays Social Security until 67.

For several years, their taxable income may be significantly lower than during their working years.

They may intentionally convert enough IRA assets annually to “fill up” a lower tax bracket before:

RMDs begin

Social Security increases taxable income

Medicare IRMAA thresholds become an issue

Key Insight

The first retirement year is often more valuable for tax planning than people realize because income may temporarily drop before other retirement income sources begin.

4. Review Medicare IRMAA Exposure Early

Many retirees are surprised when Medicare premiums increase because of prior-year income.

IRMAA stands for Income-Related Monthly Adjustment Amount.

Higher-income retirees can pay significantly more for Medicare Part B and Part D premiums.

Common triggers include:

Large IRA withdrawals

Roth conversions

Capital gains

Selling property

Large bonuses during retirement year

Why This Matters in Year One

The retirement transition often creates unusual tax years.

Without planning, retirees can accidentally trigger higher Medicare premiums two years later.

Important Note

Sometimes triggering IRMAA still makes sense.

For example, a strategic Roth conversion today may still save substantial taxes later.

The key is understanding the tradeoff before making the move.

5. Keep a Larger Cash Reserve Than You Think You Need

The first few years of retirement are emotionally different from the accumulation years.

Market volatility can feel more stressful when paychecks stop.

A properly structured cash reserve can help retirees avoid selling investments during market declines.

This reserve may cover:

12–24 months of spending needs

Major healthcare expenses

Home repairs

Unexpected family support

Market downturns

What Many Retirees Get Wrong

Some retirees stay fully invested because they fear missing returns.

Others hold too much cash and reduce long-term growth potential.

The goal is balance.

A thoughtful reserve strategy can improve both flexibility and emotional confidence.

6. Recheck Your Investment Risk Now That You’re Retired

Many investors discover they were comfortable with risk only while employed.

Once retirement begins, market declines feel different.

This does not mean retirees should abandon growth investments entirely.

But it does mean portfolios should reflect:

Withdrawal needs

Time horizon

Income stability

Emotional tolerance for volatility

Sequence-of-returns risk

What Is Sequence Risk?

Poor market returns early in retirement can create lasting damage when withdrawals are occurring simultaneously.

This is why investment structure matters more after retirement begins.

Common First-Year Mistake

Making aggressive investment changes during a market drop.

Some retirees panic after their first retirement correction and move heavily to cash after losses already occurred.

That can permanently damage long-term retirement sustainability.

7. Review Estate Documents and Beneficiaries

Retirement is a major life transition and an ideal time to revisit estate planning.

Review:

Wills

Trusts

Powers of attorney

Healthcare directives

IRA beneficiaries

Life insurance beneficiaries

Common Issue

Beneficiary designations often override wills.

We regularly see outdated beneficiaries remain unchanged for decades.

Also Important

Review how retirement accounts align with tax planning and legacy goals.

For some households, Roth accounts may be more attractive legacy assets than traditional IRAs because of future tax implications for heirs.

5 Financial Moves to Avoid During Your First Year of Retirement

1. Avoid Major Lifestyle Purchases Too Quickly

Many retirees make large purchases immediately after retiring:

Vacation homes

RVs

Boats

Major renovations

Large gifts to children

The issue is not the purchase itself.

The issue is making irreversible financial decisions before understanding your long-term retirement spending pattern.

Better Approach

Give yourself time to observe:

Actual spending

Healthcare costs

Tax changes

Lifestyle adjustments

Market conditions

Your first-year spending may not reflect your long-term retirement reality.

2. Avoid Claiming Social Security Without Running the Numbers

Social Security timing is often permanent.

Many retirees underestimate:

Survivor implications

Inflation protection

Longevity risk

Tax coordination opportunities

Even delaying benefits by a few years can substantially improve long-term retirement income in some situations.

3. Avoid Taking Large IRA Withdrawals Without Tax Planning

Large withdrawals can create ripple effects:

Higher tax brackets

Increased Medicare premiums

Taxation of Social Security

Reduced Roth conversion opportunities

Example

A retiree withdraws $150,000 from an IRA for home renovations and gifting.

That single decision could:

Push income into higher brackets

Trigger IRMAA surcharges

Increase future tax exposure

Coordinating withdrawals over multiple years may create a better outcome.

4. Avoid Panic Decisions During Market Declines

The first market downturn after retirement can feel emotionally different.

This is often when retirees second-guess their entire plan.

Selling after declines can lock in losses and reduce future recovery potential.

Better Approach

Build a plan before volatility happens:

Maintain cash reserves

Diversify appropriately

Understand withdrawal flexibility

Revisit spending priorities

The goal is not eliminating volatility.

The goal is reducing the need for emotional decisions during volatility.

5. Avoid Treating Retirement Like a Permanent Vacation

Many retirees spend aggressively during the first year before understanding what sustainable retirement spending actually looks like.

This does not mean retirement should be restrictive.

But retirees benefit from observing:

Real monthly expenses

Healthcare changes

Inflation effects

Travel patterns

Long-term lifestyle costs

The first year should help establish sustainable habits and confidence.

A Real-World First-Year Retirement Scenario

John and Susan retire at 64.

They have:

$1.2 million invested

$80,000 in cash

A paid-off home

No pension

Estimated spending needs of $7,000/month after taxes

Their first instinct is:

Claim Social Security immediately

Withdraw additional income entirely from IRAs

Renovate the home

Increase stock exposure after hearing “retirees need growth”

Instead, after planning carefully, they decide to:

Delay Social Security until age 67

Use taxable savings for part of their income

Complete partial Roth conversions annually

Maintain 18 months of cash reserves

Reduce portfolio volatility modestly

Delay large home projects for one year

The Result

They create:

Lower projected lifetime taxes

Higher future guaranteed income

Better Medicare premium management

Greater flexibility during market declines

More confidence about long-term sustainability

None of the decisions were dramatic.

But together, they improved the odds of long-term retirement success.

Questions to Review Before December 31 of Your First Retirement Year

Your first retirement year may create unique tax planning opportunities before year-end.

Questions worth reviewing include:

Should you do a Roth conversion this year?

Are capital gains unusually low this year?

Should you harvest gains before Social Security begins?

Are Medicare IRMAA thresholds an issue?

Are you withholding enough taxes from withdrawals?

Should you rebalance investments?

Are charitable giving strategies appropriate?

Have beneficiaries been updated?

These decisions are often easier and more valuable before future retirement income sources begin.

Common First-Year Retirement Mistakes

Here are several patterns we frequently see:

Spending before building a withdrawal strategy

Claiming Social Security too quickly

Ignoring Roth conversion windows

Taking unnecessary taxable withdrawals

Underestimating healthcare costs

Overreacting to market volatility

Maintaining outdated investment allocations

Forgetting beneficiary reviews

Making emotional investment changes

The first year of retirement often sets the tone for future decision-making.

Final Thoughts

Your first year of retirement is not just about leaving work. It is about transitioning from accumulation to distribution, from saving to creating sustainable income.

The retirees who navigate this transition best are usually not the ones making dramatic moves.

They are the ones slowing down, reviewing tax opportunities carefully, building intentional withdrawal strategies, and avoiding irreversible mistakes too early.

At Greenbush Financial Group, we often find that the most successful retirement transitions come from thoughtful planning rather than reacting emotionally to headlines, market volatility, or uncertainty.

The goal of year one is not perfection.

It is building confidence, flexibility, and a financial foundation that can support the next several decades.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

FAQ

-

What is the biggest financial mistake retirees make in their first year?One of the biggest mistakes is withdrawing money from retirement accounts without a coordinated tax and income strategy. Poor withdrawal sequencing can increase taxes, Medicare premiums, and long-term portfolio stress.

-

Should I take Social Security as soon as I retire?Not necessarily. Many retirees benefit from delaying benefits, especially if they expect longer life expectancy or want to maximize survivor income for a spouse.

-

Should retirees use cash first before withdrawing from investments?In many cases, maintaining a cash reserve for near-term spending can reduce the need to sell investments during market declines. The right approach depends on taxes, market conditions, and withdrawal needs.

-

Why are Roth conversions often valuable early in retirement?Early retirement years may temporarily lower taxable income before RMDs and Social Security begin. This can create opportunities to convert IRA assets at lower tax rates.

-

How much cash should retirees keep during the first year?Many retirees benefit from holding 12-24 months of spending needs in cash or short-term reserves, especially during the retirement transition period.

-

Can retirement withdrawals increase Medicare premiums?Yes. Large IRA withdrawals, Roth conversions, and capital gains can increase income enough to trigger IRMAA surcharges for Medicare Part B and Part D.

-

Should retirees change investments immediately after retiring?Not automatically. However, retirement is a good time to reassess whether your portfolio still aligns with your income needs, risk tolerance, and withdrawal strategy.

-

What should retirees review before the end of their first retirement year?Retirees should review taxes, Roth conversions, Medicare income thresholds, investment allocations, withdrawal strategies, and beneficiary designations before December 31.

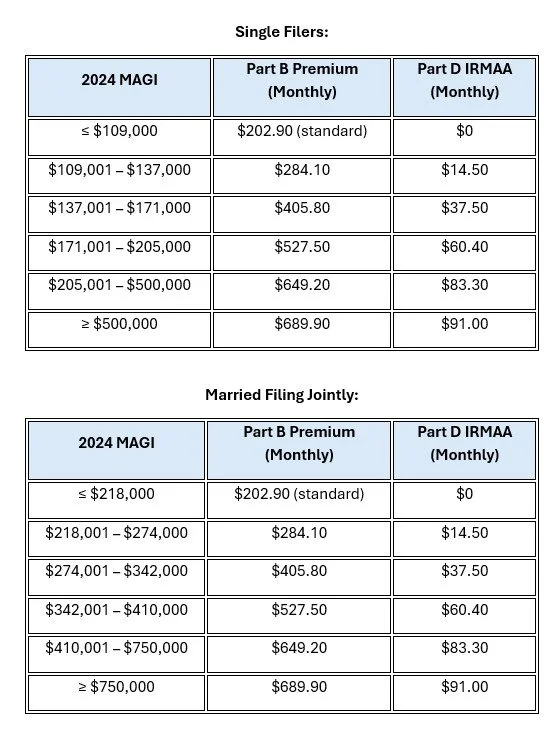

2026 Medicare IRMAA Brackets: What Triggers Higher Premiums and How to Avoid

Medicare IRMAA increases Part B and Part D premiums when your income exceeds specific thresholds based on your MAGI from two years prior. In 2026, managing income through strategies like Roth conversions, withdrawal timing, and tax planning can help reduce or avoid these surcharges. Even small income increases can trigger higher premiums, making proactive planning essential. Greenbush Financial Group helps retirees minimize IRMAA and control long-term healthcare costs.

Medicare IRMAA (Income-Related Monthly Adjustment Amount) is a surcharge added to Medicare Part B and Part D premiums when your income exceeds certain thresholds. These surcharges are based on your Modified Adjusted Gross Income (MAGI) from two years prior. At Greenbush Financial Group, our analysis shows that proactive tax and withdrawal planning can help retirees avoid or minimize IRMAA and significantly reduce long-term healthcare costs.

What Is Medicare IRMAA and How Does It Work?

IRMAA is an additional premium Medicare beneficiaries pay if their income exceeds specific limits.

Key Facts

Applies to Medicare Part B and Part D

Based on income from two years prior

Uses Modified Adjusted Gross Income (MAGI)

Adjusted annually for inflation

Example

Your 2026 Medicare premiums are based on your 2024 income.

This lag creates planning opportunities, especially in early retirement years.

2026 IRMAA Income Limits and Surcharge Brackets

IRMAA is triggered when your income crosses certain thresholds.

2026 Estimated IRMAA Thresholds

At Greenbush Financial Group, we emphasize that even $1 over a threshold can trigger a significantly higher premium.

What Counts as Income for IRMAA (MAGI)?

IRMAA is based on Modified Adjusted Gross Income, which includes more than just wages.

Included Income Sources

IRA and 401(k) withdrawals

Capital gains from investments

Dividends and interest

Rental income

Social Security (partially taxable portion)

Roth conversions

Important Note

Tax-free municipal bond interest is also included in MAGI for IRMAA purposes.

How Much Are IRMAA Surcharges?

IRMAA increases both Part B and Part D premiums.

Example Impact

Standard Part B premium (baseline)

IRMAA can increase premiums by hundreds of dollars per month per person

Part D surcharges are smaller but still meaningful

Key Insight

Over a 10–20 year retirement, IRMAA can add up to tens of thousands of dollars in additional healthcare costs if not managed properly.

Planning Strategies to Reduce or Avoid IRMAA

Strategic income planning is the most effective way to manage IRMAA.

1. Manage Your Taxable Income Each Year

Stay below key IRMAA thresholds when possible

Avoid large one-time income spikes

2. Use Roth Conversions Strategically

Convert funds in lower-income years before Medicare

Reduce future taxable income and RMDs

3. Time Large Withdrawals Carefully

Spread income over multiple years

Avoid triggering IRMAA in a single year

4. Leverage Roth Accounts

Roth withdrawals do not increase MAGI

Provides tax-free income flexibility

5. Consider Capital Gains Timing

Harvest gains in lower-income years

Offset gains with losses when possible

At Greenbush Financial Group, we often build multi-year tax projections to help clients stay below IRMAA thresholds.

IRMAA Planning Before and After Retirement

Before Retirement (Ages 55–63)

Ideal window for Roth conversions

Lower income years create planning opportunities

Reduce future IRMAA exposure

Early Retirement (Before Medicare)

Control income levels carefully

Balance withdrawals across accounts

After Age 65

Monitor RMDs and income levels

Use Roth withdrawals to manage thresholds

Plan ahead for future income spikes

What Happens If Your Income Drops?

You may be able to appeal IRMAA if your income has decreased due to certain life events.

Qualifying Life-Changing Events

Retirement

Marriage or divorce

Death of a spouse

Loss of income-producing property

You can file an appeal with Social Security to request a lower premium.

Common IRMAA Mistakes to Avoid

Ignoring IRMAA when doing Roth conversions

Taking large IRA withdrawals in a single year

Not planning for RMDs

Overlooking capital gains impact

Assuming Medicare premiums are fixed

At Greenbush Financial Group, we often see that IRMAA surprises retirees who focus only on taxes without considering healthcare costs.

Final Thoughts

IRMAA is one of the most overlooked retirement expenses, yet it can significantly increase your Medicare costs. The key is not just minimizing taxes in a single year but managing income over time to avoid crossing key thresholds.

At Greenbush Financial Group, our analysis shows that proactive planning around withdrawals, Roth conversions, and income timing can help reduce IRMAA and improve overall retirement outcomes.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

Frequently Asked Questions

-

What does IRMAA stand for?Income-Related Monthly Adjustment Amount, a surcharge on Medicare premiums based on income.

-

What income is used to calculate IRMAA?Modified Adjusted Gross Income (MAGI) from two years prior.

-

Can Roth withdrawals trigger IRMAA?No, qualified Roth withdrawals do not increase MAGI.

-

Can IRMAA be appealed?Yes, if you have a qualifying life-changing event such as retirement or loss of income.

-

How can I avoid IRMAA surcharges?By managing taxable income, using Roth strategies, and avoiding large income spikes.

2026 Roth IRA Conversions Explained: Smart Timing and Costly Mistakes

Roth IRA conversions allow retirees to move pre-tax assets into tax-free accounts by paying taxes now, but timing is critical. The most effective strategies involve spreading conversions over multiple years, managing tax brackets, and coordinating with Social Security and IRMAA thresholds. Poorly timed conversions can increase taxes and Medicare costs. Greenbush Financial Group helps retirees use Roth conversions to reduce lifetime taxes and improve income flexibility.

Roth conversions can be one of the most powerful tax planning tools in retirement, but they are not always beneficial. A Roth conversion involves moving money from a pre-tax account into a Roth account and paying taxes now to avoid taxes later. At Greenbush Financial Group, our analysis shows that Roth conversions are most effective when done strategically across multiple years, not as a one-time decision.

What Is a Roth Conversion and How Does It Work?

A Roth conversion moves funds from a Traditional IRA or 401(k) into a Roth IRA or 401(k).

Key Mechanics

Converted amount is taxed as ordinary income

No early withdrawal penalty if done correctly

Future growth and withdrawals are tax-free

No Required Minimum Distributions (RMDs) for Roth IRAs

Example

Convert $50,000 from an IRA to a Roth IRA

Pay taxes on $50,000 this year

Future withdrawals are tax-free

At Greenbush Financial Group, we view Roth conversions as a way to “prepay taxes” at potentially lower rates.

When Roth Conversions Make Sense

There are specific scenarios where Roth conversions can significantly improve long-term outcomes.

1. Low-Income Years in Early Retirement

The period between retirement and starting Social Security or RMDs is often ideal.

Lower taxable income

Opportunity to fill lower tax brackets

Reduce future tax burden

2. Before Required Minimum Distributions (RMDs)**

RMDs can force higher taxable income later in retirement.

Converting early reduces future RMDs

Helps avoid higher tax brackets in your 70s

3. Expecting Higher Future Tax Rates

If you believe your future tax rate will be higher:

Paying taxes now may be beneficial

Locks in current tax rates

4. Large Pre-Tax Account Balances

High IRA or 401(k) balances can create tax challenges later.

Large RMDs

Increased IRMAA surcharges

Higher Social Security taxation

5. Leaving Assets to Heirs

Roth accounts can be more tax-efficient for beneficiaries.

Tax-free withdrawals for heirs

No lifetime RMDs for original owner

At Greenbush Financial Group, Roth conversions are often used as part of a broader estate and tax planning strategy.

When Roth Conversions May Not Make Sense

Roth conversions are not always the right move.

1. Already in a High Tax Bracket

If converting pushes you into a higher bracket:

You may pay more tax than necessary

Reduces the benefit of the conversion

2. Short Time Horizon

If you expect to use the money soon:

Limited time for tax-free growth

Less benefit from conversion

3. Paying Taxes From the Conversion Itself

Using IRA funds to pay taxes reduces the amount converted.

Decreases long-term growth potential

Less efficient overall

4. Expecting Lower Future Tax Rates

If your income will decrease later:

You may pay more tax now than necessary

5. Impact on Medicare and Social Security

Conversions increase taxable income.

May trigger IRMAA surcharges

Can increase taxation of Social Security

At Greenbush Financial Group, we often see Roth conversions backfire when these factors are not considered.

The “Tax Bracket Filling” Strategy

One of the most effective ways to approach Roth conversions is by filling up lower tax brackets.

How It Works

Identify your current tax bracket

Convert just enough to stay within that bracket

Avoid jumping into higher brackets

Example

Top of 12% bracket = target income level

Convert enough to reach that limit

Stop before entering the 22% bracket

This strategy spreads conversions over multiple years, reducing overall tax impact.

Roth Conversions and IRMAA Considerations

Roth conversions increase your income for that year, which can affect Medicare premiums.

Key Impact

Higher income can trigger IRMAA surcharges

IRMAA is based on income from two years prior

Planning Tip

Balance Roth conversions with IRMAA thresholds to avoid unnecessary premium increases.

A Multi-Year Roth Conversion Strategy Example

Scenario

Age 62, recently retired

$800,000 in IRA

Low income before Social Security

Strategy

Convert $40,000–$60,000 annually

Stay within a lower tax bracket

Delay Social Security

Outcome

Reduced future RMDs

Lower lifetime taxes

Increased tax-free income later

At Greenbush Financial Group, this type of phased approach is often more effective than a single large conversion.

Common Roth Conversion Mistakes

Converting too much in one year

Ignoring tax bracket thresholds

Overlooking IRMAA impacts

Not coordinating with Social Security timing

Failing to plan conversions over multiple years

Final Thoughts

Roth conversions can be a powerful tool, but only when used strategically. The goal is not simply to convert assets, but to reduce lifetime taxes and create more flexibility in retirement income.

At Greenbush Financial Group, our analysis shows that the most successful strategies involve careful timing, tax bracket management, and long-term planning.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

-

Is it a bad idea to retire in a down market?Not necessarily, but it increases sequence of returns risk and requires careful planning.

-

How much cash and short-term fixed income should I have in retirement?Typically 1 to 3 years of living expenses.

-

Should I stop withdrawals during a downturn?Not entirely, but reducing withdrawals can improve long-term outcomes.

-

Can a market downturn ruin my retirement plan?It can if not managed properly, especially in the early years of retirement.

-

What is the best strategy during a market downturn?Maintain a cash reserve, adjust withdrawals, stay invested, and focus on long-term planning.