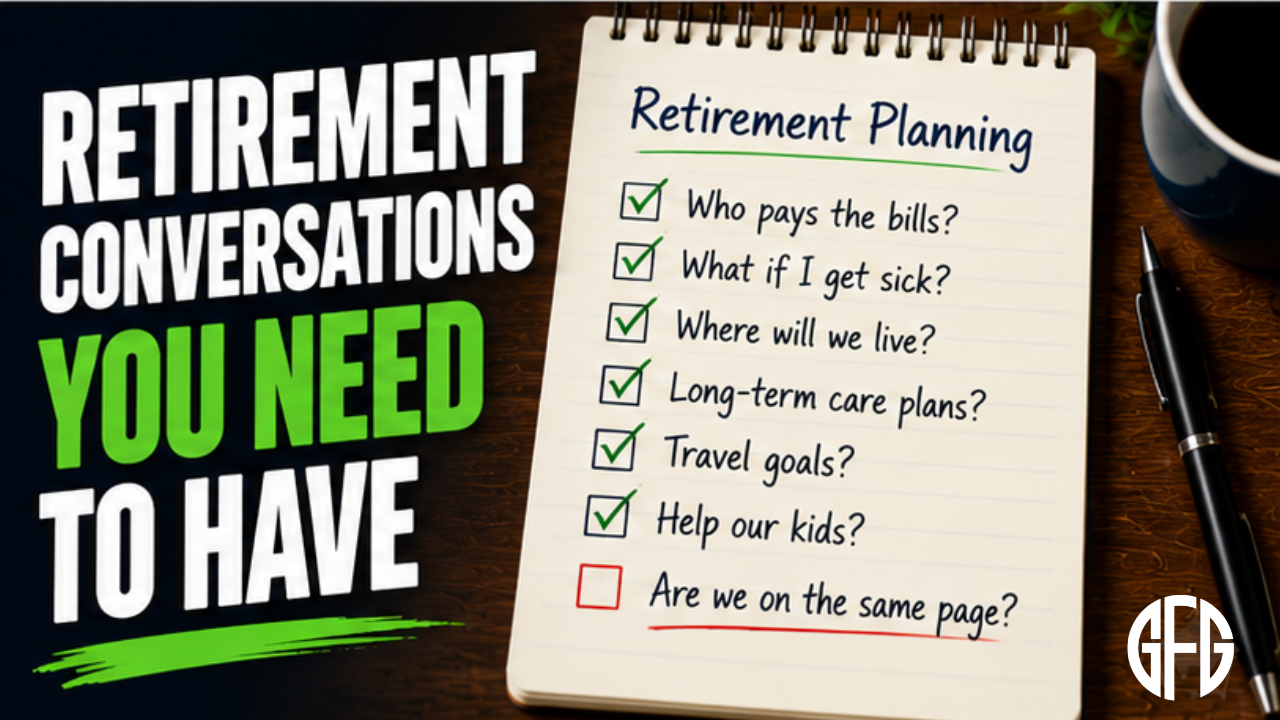

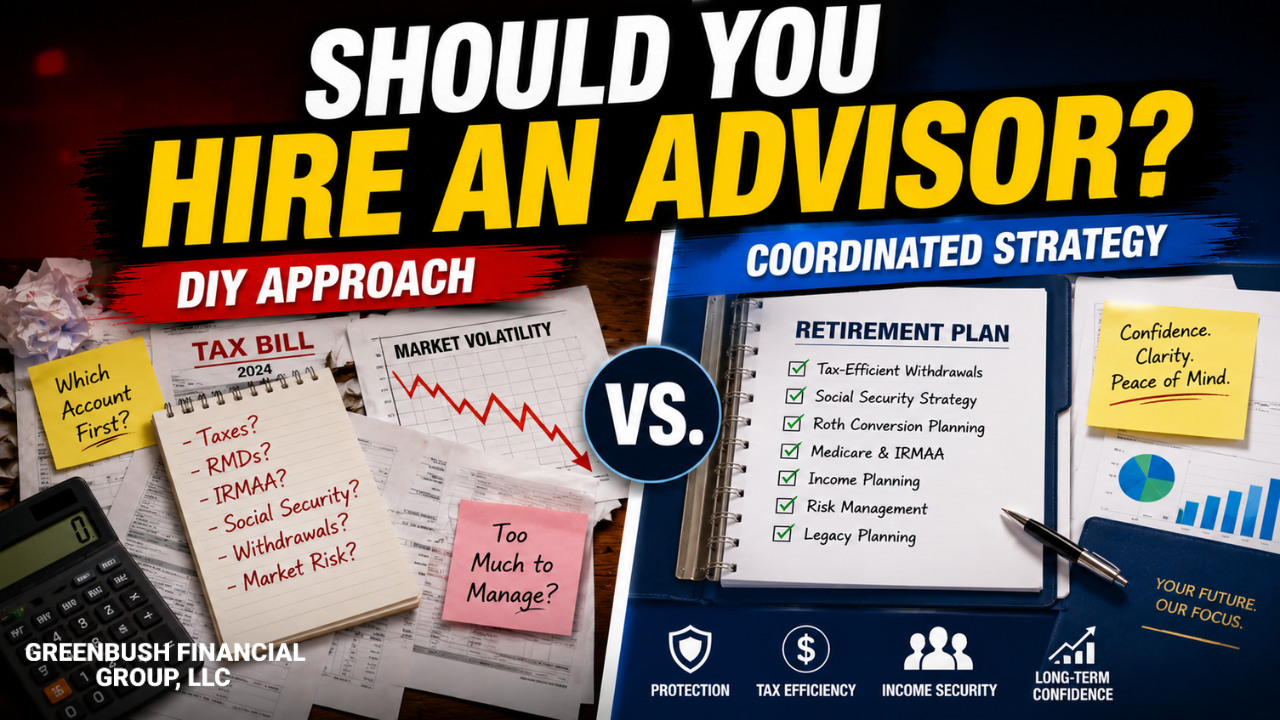

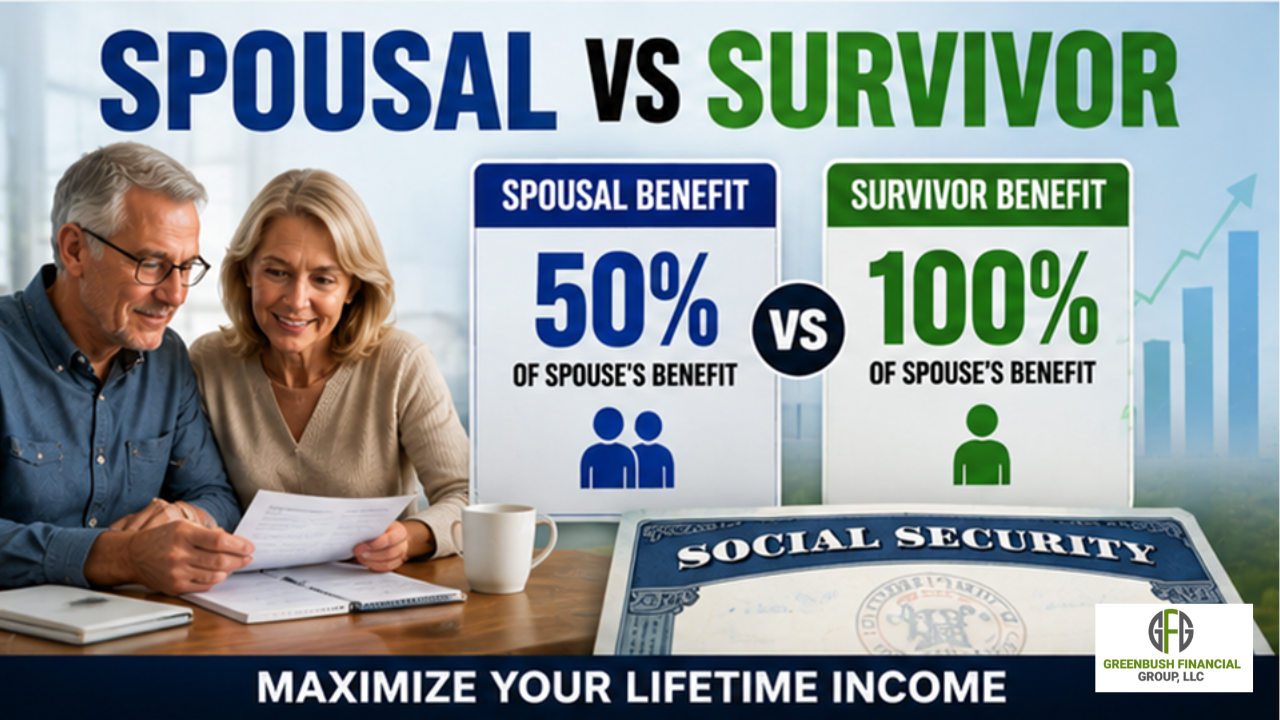

The years leading up to retirement are often when the most important financial decisions are made. This article explores 10 key retirement planning considerations, including Social Security claiming strategies, Medicare enrollment, retirement tax planning, investment risk, pension elections, and estate planning. Understanding these decisions can help retirees avoid costly mistakes and improve long-term financial confidence. Proper retirement planning requires coordinating income, taxes, healthcare, investments, and risk management into a comprehensive strategy.