Can Anyone Open an HSA Account?

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Health Savings Accounts (HSAs) are one of the most tax-advantaged accounts available and can be a powerful tool for paying healthcare costs in retirement. Contributions are made with pre-tax dollars, the account grows tax-deferred, and distributions are tax-free when used for qualified medical expenses. However, not everyone is eligible to contribute to an HSA, and understanding the eligibility rules is critical.

In this article, we’ll cover:

Who is eligible to contribute to an HSA

What qualifies as a High Deductible Health Plan (HDHP)

2026 HSA contribution limits

Special rules when approaching age 65 and Medicare

Frequently asked questions about HSA eligibility

Who Is Eligible to Contribute to an HSA?

To contribute to an HSA, you must meet all of the following requirements:

You must be enrolled in a High Deductible Health Plan (HDHP)

You cannot be covered by any other non-HDHP health insurance

You cannot be enrolled in Medicare

You cannot be claimed as a dependent on someone else’s tax return

The most common way people become eligible for an HSA is through their employer-sponsored high deductible health insurance plan. If your employer’s health insurance plan is not classified as a high deductible plan, then you are not eligible to contribute to an HSA.

What Qualifies as a High Deductible Health Plan in 2026?

Each year, the IRS defines what qualifies as a High Deductible Health Plan. For 2026, a plan must meet the following minimum deductible and maximum out-of-pocket limits:

If your health insurance plan does not meet these thresholds, it is not considered HSA-eligible, and you cannot contribute to an HSA.

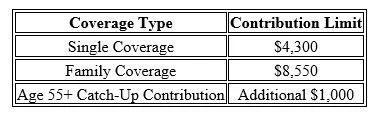

HSA Contribution Limits for 2026

The IRS also sets contribution limits each year. For 2026, the HSA contribution limits are:

These limits include both employee and employer contributions combined. So if your employer contributes to your HSA, that amount counts toward the total annual limit.

Because these limits are indexed for inflation, they typically increase slightly each year.

Be Careful as You Approach Age 65 (Medicare Rule)

There is a very important rule regarding HSAs and Medicare that many people are not aware of:

Once you enroll in Medicare, you can no longer contribute to an HSA.

However, there is an additional rule that affects individuals who work past age 65 and delay Medicare.

The 6-Month Medicare Retroactive Rule

When someone enrolls in Medicare Part A after age 65, Medicare coverage is retroactive for 6 months (but not earlier than age 65).

Because of this:

You must stop HSA contributions 6 months before applying for Medicare

Otherwise, those contributions become excess contributions

Excess contributions can result in tax penalties if not corrected

Example

Let’s say someone is 67, still working, and contributing to an HSA.

If they plan to enroll in Medicare in December, they should stop HSA contributions by June of that year.

If they do not, they may need to withdraw excess contributions and potentially pay penalties.

Important Exception

If you enroll in Medicare right at age 65, you do not need to stop contributions 6 months early because Medicare cannot retroactively start before age 65.

Why HSAs Can Be So Valuable

HSAs are often used as a retirement healthcare savings account because:

Contributions are pre-tax

Growth is tax-deferred

Withdrawals are tax-free for medical expenses

After age 65, withdrawals for non-medical expenses are penalty-free (taxable only)

Because healthcare is often one of the largest expenses in retirement, many individuals choose to save their HSA funds during their working years and use them later in retirement.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

-

Can anyone open an HSA account?No. You must be enrolled in a qualified High Deductible Health Plan.

-

Can I contribute to an HSA if I am self-employed?Yes, as long as you have an HSA-eligible high deductible health insurance plan.

-

Can I contribute to an HSA if I am on Medicare?No. Once enrolled in Medicare, you can no longer contribute.

-

Can my employer contribute to my HSA?Yes, and employer contributions count toward the annual limit.

-

What happens if I contribute to an HSA while on Medicare?Those contributions are considered excess contributions and may be subject to penalties.

-

Can both spouses contribute to an HSA?Yes, if both spouses are eligible and covered by an HSA-qualified plan.

-

Do HSA contribution limits change each year?Yes, they are typically adjusted annually for inflation.

-

What is the catch-up contribution for people over age 55?An additional $1,000 per year.

-

Can I still use my HSA after I go on Medicare?Yes, you just cannot contribute anymore.

-

What happens if I exceed the HSA contribution limit?You may have to withdraw the excess contribution and could owe penalties if not corrected.