In Retirement, What Healthcare Costs Can Be Paid from an HSA Account?

Health Savings Accounts offer tax-free withdrawals for qualified medical expenses in retirement, but understanding eligibility rules is critical. This guide explains which expenses qualify, including Medicare premiums, dental, vision, and out-of-pocket costs. It also covers non-eligible expenses and key withdrawal rules before and after age 65. Use this resource to avoid costly HSA mistakes and maximize your retirement healthcare strategy.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

As people approach retirement, or enter retirement, healthcare costs often become one of the largest expenses in a financial plan. The good news is that Health Savings Accounts (HSAs) can be a powerful tool to help cover many of these costs using tax-free dollars. However, not every healthcare expense qualifies, so it’s important to understand both what can and cannot be paid from an HSA in retirement.

In this article, we’ll cover:

Which Medicare premiums are HSA-eligible

Whether COBRA premiums qualify

Dental, vision, and hearing expenses

Out-of-pocket medical costs

Medical equipment and prescriptions

Expenses that are not HSA-eligible

HSA withdrawal rules before and after age 65

Frequently asked HSA questions in retirement

Medicare Premiums

One of the most common uses for HSA funds in retirement is paying for Medicare premiums. HSA distributions can be used tax-free for:

Medicare Part B premiums

Medicare Part D premiums

Medicare Advantage (Part C) premiums

However, Medigap (Medicare Supplement) premiums are not considered a qualified HSA expense, even though Medicare Advantage plans are. This is a commonly misunderstood rule and an important one for retirees to be aware of when planning healthcare costs.

COBRA Coverage

If you retire before age 65 or leave an employer and elect COBRA coverage, those health insurance premiums can be paid from an HSA. This can be especially helpful for early retirees who need to bridge the gap before Medicare begins.

Dental, Vision, and Hearing Expenses

Dental, vision, and hearing costs are some of the most common out-of-pocket healthcare expenses in retirement — especially since many retirees no longer have employer coverage for these services.

HSA-eligible expenses include:

Dental cleanings, fillings, crowns, dentures, braces, and X-rays

Vision exams, eyeglasses, contact lenses, and LASIK surgery

Hearing aids and hearing aid batteries

Hearing aids alone can cost several thousand dollars, making the HSA a valuable tax-free resource for these expenses.

Out-of-Pocket Medical Expenses

Many routine healthcare costs in retirement are HSA-eligible, including:

Doctor visits

Specialist visits

Hospital services

Co-pays

Deductibles

Coinsurance

Surgery costs

Lab work and imaging

These are often the “everyday” medical expenses retirees experience each year.

Medical Equipment

If medical equipment is needed later in retirement, many of these expenses qualify for HSA distributions, including:

Walkers

Wheelchairs

Blood pressure monitors

Crutches

CPAP machines

Glucose monitors

Prescription Medications

Prescription drugs that are prescribed by a doctor are qualified HSA expenses.

However, over-the-counter medications typically do NOT qualify unless they are prescribed by a physician.

Expenses That Are NOT HSA-Eligible

Some healthcare-related expenses are not considered qualified medical expenses. These typically include:

Gym memberships

Nutritional supplements

Cosmetic procedures

Teeth whitening

General health items not prescribed by a doctor

Even though these may improve health, they are not considered qualified medical expenses under HSA rules.

Why HSAs Are So Powerful for Retirement

HSAs are one of the most tax-advantaged accounts available because they offer:

Tax-deductible contributions

Tax-free growth

Tax-free withdrawals for qualified medical expenses

Because healthcare costs are often highest in retirement, many individuals choose to pay for medical expenses out-of-pocket during their working years and allow their HSA to grow, using it later in retirement when healthcare costs increase.

HSA Withdrawal Rules: Before and After Age 65

It’s also important to understand the rules around HSA withdrawals:

Before age 65

Non-qualified withdrawals = taxable income + 20% penalty

After age 65

Non-qualified withdrawals = taxable income only (no penalty)

Works similar to a Traditional IRA if not used for healthcare

This provides additional flexibility later in retirement.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

-

Can HSA funds be used for Medicare premiums?Yes, for Medicare Part B, Part D, and Medicare Advantage premiums.

-

Can HSA funds be used for Medigap premiums?No, Medigap premiums are not considered a qualified expense.

-

Can I use my HSA for dental expenses in retirement?Yes, most dental expenses qualify.

-

Are vision expenses HSA-eligible?Yes, including exams, glasses, contacts, and LASIK.

-

Are hearing aids covered by an HSA?Yes, including hearing aid batteries.

-

Can I use my HSA for COBRA premiums?Yes, COBRA premiums are a qualified expense.

-

Are prescription drugs HSA-eligible?Yes, if prescribed by a doctor.

-

Are over-the-counter medications HSA-eligible?Typically no, unless prescribed by a physician.

-

What happens if I use HSA money for non-medical expenses before 65?You will owe income tax and a 20% penalty.

-

What happens if I use HSA money for non-medical expenses after 65?You will owe income tax, but no penalty.

Can Anyone Open an HSA Account?

Health Savings Accounts offer powerful tax advantages, but strict eligibility rules apply. This guide explains who can contribute to an HSA in 2026, including HDHP requirements, contribution limits, and Medicare restrictions. Learn how to avoid costly mistakes, especially as you approach age 65. A must-read for retirement-focused healthcare planning.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Health Savings Accounts (HSAs) are one of the most tax-advantaged accounts available and can be a powerful tool for paying healthcare costs in retirement. Contributions are made with pre-tax dollars, the account grows tax-deferred, and distributions are tax-free when used for qualified medical expenses. However, not everyone is eligible to contribute to an HSA, and understanding the eligibility rules is critical.

In this article, we’ll cover:

Who is eligible to contribute to an HSA

What qualifies as a High Deductible Health Plan (HDHP)

2026 HSA contribution limits

Special rules when approaching age 65 and Medicare

Frequently asked questions about HSA eligibility

Who Is Eligible to Contribute to an HSA?

To contribute to an HSA, you must meet all of the following requirements:

You must be enrolled in a High Deductible Health Plan (HDHP)

You cannot be covered by any other non-HDHP health insurance

You cannot be enrolled in Medicare

You cannot be claimed as a dependent on someone else’s tax return

The most common way people become eligible for an HSA is through their employer-sponsored high deductible health insurance plan. If your employer’s health insurance plan is not classified as a high deductible plan, then you are not eligible to contribute to an HSA.

What Qualifies as a High Deductible Health Plan in 2026?

Each year, the IRS defines what qualifies as a High Deductible Health Plan. For 2026, a plan must meet the following minimum deductible and maximum out-of-pocket limits:

If your health insurance plan does not meet these thresholds, it is not considered HSA-eligible, and you cannot contribute to an HSA.

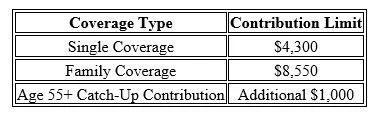

HSA Contribution Limits for 2026

The IRS also sets contribution limits each year. For 2026, the HSA contribution limits are:

These limits include both employee and employer contributions combined. So if your employer contributes to your HSA, that amount counts toward the total annual limit.

Because these limits are indexed for inflation, they typically increase slightly each year.

Be Careful as You Approach Age 65 (Medicare Rule)

There is a very important rule regarding HSAs and Medicare that many people are not aware of:

Once you enroll in Medicare, you can no longer contribute to an HSA.

However, there is an additional rule that affects individuals who work past age 65 and delay Medicare.

The 6-Month Medicare Retroactive Rule

When someone enrolls in Medicare Part A after age 65, Medicare coverage is retroactive for 6 months (but not earlier than age 65).

Because of this:

You must stop HSA contributions 6 months before applying for Medicare

Otherwise, those contributions become excess contributions

Excess contributions can result in tax penalties if not corrected

Example

Let’s say someone is 67, still working, and contributing to an HSA.

If they plan to enroll in Medicare in December, they should stop HSA contributions by June of that year.

If they do not, they may need to withdraw excess contributions and potentially pay penalties.

Important Exception

If you enroll in Medicare right at age 65, you do not need to stop contributions 6 months early because Medicare cannot retroactively start before age 65.

Why HSAs Can Be So Valuable

HSAs are often used as a retirement healthcare savings account because:

Contributions are pre-tax

Growth is tax-deferred

Withdrawals are tax-free for medical expenses

After age 65, withdrawals for non-medical expenses are penalty-free (taxable only)

Because healthcare is often one of the largest expenses in retirement, many individuals choose to save their HSA funds during their working years and use them later in retirement.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

-

Can anyone open an HSA account?No. You must be enrolled in a qualified High Deductible Health Plan.

-

Can I contribute to an HSA if I am self-employed?Yes, as long as you have an HSA-eligible high deductible health insurance plan.

-

Can I contribute to an HSA if I am on Medicare?No. Once enrolled in Medicare, you can no longer contribute.

-

Can my employer contribute to my HSA?Yes, and employer contributions count toward the annual limit.

-

What happens if I contribute to an HSA while on Medicare?Those contributions are considered excess contributions and may be subject to penalties.

-

Can both spouses contribute to an HSA?Yes, if both spouses are eligible and covered by an HSA-qualified plan.

-

Do HSA contribution limits change each year?Yes, they are typically adjusted annually for inflation.

-

What is the catch-up contribution for people over age 55?An additional $1,000 per year.

-

Can I still use my HSA after I go on Medicare?Yes, you just cannot contribute anymore.

-

What happens if I exceed the HSA contribution limit?You may have to withdraw the excess contribution and could owe penalties if not corrected.

Health Savings Account Distribution Tax and Penalty Rules

Health Savings Account (HSA) withdrawals have different tax and penalty rules depending on age and how funds are used. This guide explains the four distribution scenarios, tax treatment before and after age 65, and advanced strategies to maximize tax-free benefits. Learn how HSAs can serve as a powerful retirement healthcare tool and how to avoid common withdrawal mistakes. Ideal for pre-retirees planning tax-efficient income strategies.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Health Savings Accounts (HSAs) are one of the most tax-advantaged accounts available, but the tax treatment of distributions depends on how the money is used and the age of the account owner. There are essentially four different distribution scenarios that HSA owners can run into, and each scenario has different tax and penalty rules that are important to understand.

In this article, we’ll cover:

The four HSA distribution scenarios

Tax treatment before age 65

Tax treatment after age 65

Why HSAs are so valuable for retirement planning

Advanced HSA distribution strategies

Common HSA distribution mistakes to avoid

Frequently asked questions about HSA distributions

Why HSA Accounts Are So Valuable

Health Savings Accounts are unique because they offer a rare triple tax advantage:

Contributions are made pre-tax

The account grows tax-deferred

Distributions are tax-free if used for qualified medical expenses

Very few accounts receive this type of tax treatment. Traditional retirement accounts are tax-deferred, and Roth accounts are tax-free on the way out, but HSAs can be tax-free on both the contribution and distribution side when used correctly.

Because of this, many financial planners recommend not spending HSA funds during working years if possible, and instead allowing the account to grow and using it later in retirement when healthcare costs are typically much higher.

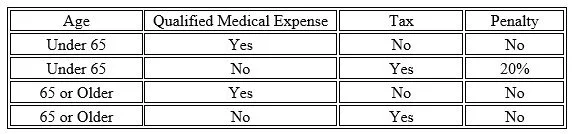

The Four HSA Distribution Scenarios

There are four main distribution scenarios that determine whether you owe taxes and/or penalties on HSA withdrawals:

Let’s walk through each scenario.

Distributions Prior to Age 65 (Qualified Medical Expenses)

If you take a distribution from an HSA before age 65 and use the money for a qualified medical expense, the distribution is:

Tax-free

Penalty-free

This is the ideal use of an HSA. Qualified expenses can include:

Doctor visits

Deductibles and coinsurance

Dental and vision care

Hearing aids

Prescription medications

Medicare premiums (after age 65)

Medical equipment

In these cases, the HSA functions exactly as intended — a tax-free healthcare account.

Distributions Prior to Age 65 (Non-Qualified Expenses)

If you take a distribution before age 65 and the expense is not qualified, the distribution is:

Subject to ordinary income tax

Subject to a 20% penalty

For example, if someone is in a 30% tax bracket and takes a non-qualified distribution:

30% tax

20% penalty

Total loss = 50% of the distribution

This is why it is usually recommended to preserve HSA funds for medical expenses whenever possible.

Distributions Age 65 or Older (Qualified Medical Expenses)

This scenario works the same as before age 65.

If the distribution is used for qualified medical expenses, the withdrawal is:

Tax-free

Penalty-free

This is why HSAs are often used as a retirement healthcare fund.

Common qualified expenses in retirement include:

Medicare Part B premiums

Medicare Part D premiums

Medicare Advantage premiums

Out-of-pocket medical expenses

Deductibles and coinsurance

Dental and vision care

Hearing aids

Medical equipment

Distributions Age 65 or Older (Non-Qualified Expenses)

This is where the rules change.

After age 65, if you take money from an HSA for non-qualified expenses:

You pay ordinary income tax

No 20% penalty

At this point, the HSA starts to function similarly to a Traditional IRA. The money can be used for anything, but it becomes taxable income if not used for medical expenses.

This provides flexibility in retirement in case the funds are needed for non-medical expenses.

Important Rule: Reimbursed Expenses Do NOT Qualify

One important rule that retirees need to be aware of:

If a medical expense is reimbursed by insurance or a former employer, you cannot also take a tax-free HSA distribution for that same expense.

For example:

Some retirees have employer retiree health plans that reimburse Medicare premiums.

If the retiree is reimbursed for Medicare Part B or Part D, those expenses cannot also be reimbursed from the HSA tax-free.

This would be considered a non-qualified distribution, and taxes would apply.

Advanced HSA Distribution Strategies

There are several advanced strategies that can make HSAs even more powerful:

1. Save Receipts and Reimburse Yourself Later

There is no time limit on when you reimburse yourself from an HSA for a qualified expense, as long as:

The expense occurred after the HSA was established

You kept the receipt

This means someone could:

Pay medical expenses out-of-pocket during working years

Allow the HSA to grow

Reimburse themselves years later tax-free

This effectively turns the HSA into a tax-free retirement account.

2. Use HSA for Medicare Premiums

HSA funds can be used tax-free for:

Medicare Part B

Medicare Part D

Medicare Advantage

(This becomes a built-in retirement healthcare fund.)

3. Treat HSA Like a Backup Traditional IRA

After age 65, if needed, HSA funds can be withdrawn for non-medical expenses and simply taxed as income, with no penalty.

Common HSA Distribution Mistakes

Some of the most common mistakes include:

Using HSA funds for non-qualified expenses before 65

Losing receipts for reimbursement

Using HSA funds for reimbursed expenses

Spending HSA funds during working years instead of investing them

Not investing HSA funds for long-term growth

Forgetting that non-qualified withdrawals before 65 have a 20% penalty

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

-

Do I pay taxes on HSA distributions?Only if the distribution is used for a non-qualified expense.

-

What is the penalty for non-qualified HSA withdrawals before age 65?A 20% penalty plus ordinary income tax.

-

What happens to the penalty after age 65?The 20% penalty goes away, but distributions are still taxable if not used for medical expenses.

-

Can I use my HSA for Medicare premiums?Yes, for Medicare Part B, Part D, and Medicare Advantage.

-

Can I reimburse myself years later from my HSA?Yes, as long as the expense occurred after the HSA was established and you kept the receipt.

-

Are HSA distributions reported on a tax return?Yes, distributions are reported on IRS Form 8889.

-

Can I use my HSA for my spouse's medical expenses?Yes, even if your spouse is not on your health insurance plan.

-

What happens to my HSA when I turn 65?You can still use it tax-free for medical expenses, and penalty-free for non-medical expenses (taxable).

-

Can I use my HSA for dental and vision expenses?Yes, most dental and vision expenses qualify.

-

Is an HSA better than a 401(k)?For medical expenses, an HSA can be more tax-efficient because it is tax-free on both contributions and qualified distributions.

The HSA 6-Month Rule: What Happens When You Enroll in Medicare at Age 65

If you’re approaching age 65 and contributing to a Health Savings Account (HSA), there’s a little-known Medicare rule that could quietly cost you.

Many people know that Health Savings Accounts (HSAs) offer triple tax benefits: tax-deductible contributions, tax-deferred growth, and tax-free withdrawals for qualified medical expenses. But what’s less commonly understood is the 6-month rule tied to Medicare Part A enrollment—and how it can affect your HSA eligibility.

If you’re turning 65 and planning to sign up for Medicare, this rule could impact when you must stop HSA contributions and potentially trigger a tax penalty if not handled properly.

Let’s walk through what the 6-month rule is, when it applies, and how to avoid costly mistakes.

What Is the HSA 6-Month Rule?

The 6-month rule refers to a Medicare regulation stating that when you apply for Medicare Part A after age 65, your coverage may retroactively begin up to six months prior to your application date—but no earlier than your 65th birthday.

Why does this matter for HSAs?

Because you cannot contribute to an HSA once you are enrolled in any part of Medicare. If your Medicare Part A enrollment is retroactive, and you weren’t aware, you could accidentally contribute to your HSA while you were technically ineligible—and face a tax penalty.

When Does the 6-Month Rule Apply?

This rule only comes into play if:

You are 65 or older, and

You delay enrolling in Medicare Part A, and

You later apply for Medicare Part A (for example, when retiring at 67 or 68)

At that point, the Social Security Administration may retroactively activate your Part A coverage up to 6 months prior to your application date.

Important: If you enroll in Medicare at age 65 or earlier, this rule does not apply. Your Part A coverage starts based on your enrollment date.

Timeline Example

Turns 65: July 2023

Continues working and delays Medicare

Applies for Medicare: October 2025 (at age 67)

Medicare Part A effective date: April 1, 2025

Last eligible month to contribute to an HSA: March 2025

Why You Must Stop HSA Contributions Before Medicare Coverage Starts

HSA rules state that:

You must stop making contributions to your HSA the month before your Medicare coverage begins.

Medicare coverage always begins on the first day of the month—so plan your final HSA contribution accordingly.

If you accidentally contribute while enrolled in Medicare—even retroactively—you may owe a 6% excise tax on those excess contributions.

How to Plan Around the 6-Month Rule

To avoid penalties and protect your tax savings:

1. Stop HSA Contributions at Least 6 Months Before Applying for Medicare

If you plan to delay Medicare past age 65, stop HSA contributions at least 6 months before you submit your Medicare application. This helps avoid retroactive coverage overlapping with HSA eligibility.

2. Calculate and Remove Excess Contributions Promptly

If you do contribute after your Medicare Part A effective date, you must remove the excess to avoid penalties.

How to calculate excess: Total the amount contributed after your Medicare coverage began. This includes both your own and any employer contributions during that ineligible period.

Penalty timeline: You must remove the excess contributions (plus any earnings) by your tax filing deadline—typically April 15 of the following year—to avoid the 6% excise tax.

If you miss that deadline, the 6% penalty applies for each year the excess amount remains in the account.

3. Use a Mid-Year Retirement Strategy

If retiring mid-year, prorate your annual HSA contribution based on the number of months you were eligible. Contributions made after Medicare enrollment—even by your employer—count toward your annual limit and must be removed if you were ineligible.

Final Thought:

The HSA 6-month rule is easy to overlook—but understanding how it works can help you avoid costly mistakes as you transition to Medicare. Whether you’re retiring soon or planning ahead, coordinating your HSA contributions with Medicare enrollment is an essential part of a tax-efficient retirement strategy.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What is the HSA 6-month rule?

The HSA 6-month rule refers to a Medicare regulation stating that when you apply for Medicare Part A after age 65, your coverage can be retroactive for up to six months—but no earlier than your 65th birthday. Since you cannot contribute to a Health Savings Account (HSA) while enrolled in any part of Medicare, this retroactive coverage can make you ineligible to contribute for that six-month period.

Why does the 6-month rule matter for HSA contributions?

Because Medicare Part A coverage may be applied retroactively, you could unknowingly contribute to your HSA during months when you were technically covered by Medicare. Those contributions would be considered “excess contributions” and subject to a 6% excise tax if not corrected.

When does the 6-month rule apply?

The rule applies only if you delay enrolling in Medicare Part A beyond age 65 and later apply. At that point, the Social Security Administration may backdate your Medicare Part A coverage up to six months. If you enroll at or before age 65, the rule does not apply.

How does retroactive Medicare coverage affect my HSA?

Once your Medicare Part A coverage begins—whether retroactively or not—you lose HSA eligibility from that start date. You must stop making contributions the month before your Medicare coverage begins to avoid excess contributions.

Can you give an example of the 6-month rule?

Yes. Suppose you turn 65 in July 2023 and continue working with an HSA-eligible plan. You apply for Medicare in October 2025 (at age 67). Your Medicare Part A effective date will be April 1, 2025—six months retroactive. Therefore, your last eligible HSA contribution month is March 2025.

When should I stop contributing to my HSA?

You should stop contributing at least six months before applying for Medicare Part A to ensure your contributions don’t overlap with retroactive coverage. This applies to both your own and any employer contributions.

What happens if I accidentally contribute while covered by Medicare?

Any contributions made after your Medicare Part A effective date are considered excess. You must withdraw those excess contributions (plus earnings) by your tax filing deadline—typically April 15 of the following year—to avoid a 6% penalty.

How do I calculate my excess contributions?

Add up all contributions (including employer contributions) made after your Medicare Part A effective date. That total must be withdrawn from your HSA. If not removed by your tax deadline, a 6% penalty applies each year the excess remains.

How should I handle HSA contributions if I retire mid-year?

If you retire partway through the year, prorate your HSA contribution limit based on the number of months you were eligible before Medicare enrollment. Contributions made after that date—even by your employer—count toward your annual limit and may need to be withdrawn.

What’s the best way to avoid penalties from the 6-month rule?

Plan ahead. Stop HSA contributions at least six months before applying for Medicare, coordinate with your HR or benefits department, and track contributions closely to prevent ineligible deposits.