Health Savings Account Distribution Tax and Penalty Rules

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Health Savings Accounts (HSAs) are one of the most tax-advantaged accounts available, but the tax treatment of distributions depends on how the money is used and the age of the account owner. There are essentially four different distribution scenarios that HSA owners can run into, and each scenario has different tax and penalty rules that are important to understand.

In this article, we’ll cover:

The four HSA distribution scenarios

Tax treatment before age 65

Tax treatment after age 65

Why HSAs are so valuable for retirement planning

Advanced HSA distribution strategies

Common HSA distribution mistakes to avoid

Frequently asked questions about HSA distributions

Why HSA Accounts Are So Valuable

Health Savings Accounts are unique because they offer a rare triple tax advantage:

Contributions are made pre-tax

The account grows tax-deferred

Distributions are tax-free if used for qualified medical expenses

Very few accounts receive this type of tax treatment. Traditional retirement accounts are tax-deferred, and Roth accounts are tax-free on the way out, but HSAs can be tax-free on both the contribution and distribution side when used correctly.

Because of this, many financial planners recommend not spending HSA funds during working years if possible, and instead allowing the account to grow and using it later in retirement when healthcare costs are typically much higher.

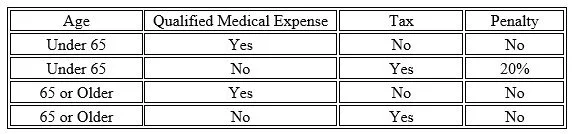

The Four HSA Distribution Scenarios

There are four main distribution scenarios that determine whether you owe taxes and/or penalties on HSA withdrawals:

Let’s walk through each scenario.

Distributions Prior to Age 65 (Qualified Medical Expenses)

If you take a distribution from an HSA before age 65 and use the money for a qualified medical expense, the distribution is:

Tax-free

Penalty-free

This is the ideal use of an HSA. Qualified expenses can include:

Doctor visits

Deductibles and coinsurance

Dental and vision care

Hearing aids

Prescription medications

Medicare premiums (after age 65)

Medical equipment

In these cases, the HSA functions exactly as intended — a tax-free healthcare account.

Distributions Prior to Age 65 (Non-Qualified Expenses)

If you take a distribution before age 65 and the expense is not qualified, the distribution is:

Subject to ordinary income tax

Subject to a 20% penalty

For example, if someone is in a 30% tax bracket and takes a non-qualified distribution:

30% tax

20% penalty

Total loss = 50% of the distribution

This is why it is usually recommended to preserve HSA funds for medical expenses whenever possible.

Distributions Age 65 or Older (Qualified Medical Expenses)

This scenario works the same as before age 65.

If the distribution is used for qualified medical expenses, the withdrawal is:

Tax-free

Penalty-free

This is why HSAs are often used as a retirement healthcare fund.

Common qualified expenses in retirement include:

Medicare Part B premiums

Medicare Part D premiums

Medicare Advantage premiums

Out-of-pocket medical expenses

Deductibles and coinsurance

Dental and vision care

Hearing aids

Medical equipment

Distributions Age 65 or Older (Non-Qualified Expenses)

This is where the rules change.

After age 65, if you take money from an HSA for non-qualified expenses:

You pay ordinary income tax

No 20% penalty

At this point, the HSA starts to function similarly to a Traditional IRA. The money can be used for anything, but it becomes taxable income if not used for medical expenses.

This provides flexibility in retirement in case the funds are needed for non-medical expenses.

Important Rule: Reimbursed Expenses Do NOT Qualify

One important rule that retirees need to be aware of:

If a medical expense is reimbursed by insurance or a former employer, you cannot also take a tax-free HSA distribution for that same expense.

For example:

Some retirees have employer retiree health plans that reimburse Medicare premiums.

If the retiree is reimbursed for Medicare Part B or Part D, those expenses cannot also be reimbursed from the HSA tax-free.

This would be considered a non-qualified distribution, and taxes would apply.

Advanced HSA Distribution Strategies

There are several advanced strategies that can make HSAs even more powerful:

1. Save Receipts and Reimburse Yourself Later

There is no time limit on when you reimburse yourself from an HSA for a qualified expense, as long as:

The expense occurred after the HSA was established

You kept the receipt

This means someone could:

Pay medical expenses out-of-pocket during working years

Allow the HSA to grow

Reimburse themselves years later tax-free

This effectively turns the HSA into a tax-free retirement account.

2. Use HSA for Medicare Premiums

HSA funds can be used tax-free for:

Medicare Part B

Medicare Part D

Medicare Advantage

(This becomes a built-in retirement healthcare fund.)

3. Treat HSA Like a Backup Traditional IRA

After age 65, if needed, HSA funds can be withdrawn for non-medical expenses and simply taxed as income, with no penalty.

Common HSA Distribution Mistakes

Some of the most common mistakes include:

Using HSA funds for non-qualified expenses before 65

Losing receipts for reimbursement

Using HSA funds for reimbursed expenses

Spending HSA funds during working years instead of investing them

Not investing HSA funds for long-term growth

Forgetting that non-qualified withdrawals before 65 have a 20% penalty

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

-

Do I pay taxes on HSA distributions?Only if the distribution is used for a non-qualified expense.

-

What is the penalty for non-qualified HSA withdrawals before age 65?A 20% penalty plus ordinary income tax.

-

What happens to the penalty after age 65?The 20% penalty goes away, but distributions are still taxable if not used for medical expenses.

-

Can I use my HSA for Medicare premiums?Yes, for Medicare Part B, Part D, and Medicare Advantage.

-

Can I reimburse myself years later from my HSA?Yes, as long as the expense occurred after the HSA was established and you kept the receipt.

-

Are HSA distributions reported on a tax return?Yes, distributions are reported on IRS Form 8889.

-

Can I use my HSA for my spouse's medical expenses?Yes, even if your spouse is not on your health insurance plan.

-

What happens to my HSA when I turn 65?You can still use it tax-free for medical expenses, and penalty-free for non-medical expenses (taxable).

-

Can I use my HSA for dental and vision expenses?Yes, most dental and vision expenses qualify.

-

Is an HSA better than a 401(k)?For medical expenses, an HSA can be more tax-efficient because it is tax-free on both contributions and qualified distributions.