Self-Employment Side Hustle? Benefits of a Solo 401(k) Plan

A Solo 401(k) offers business owners and side hustlers a powerful way to reduce taxable income and accelerate retirement savings. This guide explains contribution limits, tax strategies, and how to choose between pre-tax and Roth contributions in 2026. Learn how to build a tax-efficient retirement plan and potentially eliminate income taxes on self-employment income. Discover why Solo 401(k) plans can outperform SEP IRAs in many cases.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Today, more and more individuals have side hustles in addition to their main W-2 jobs. Others may be full-time business owners but only generate a modest amount of self-employment income. In both cases, one of the most powerful retirement and tax planning tools available is the Solo 401(k) plan.

In this article, we’re going to walk through some of the tax strategies and wealth accumulation strategies we use with clients who have self-employment income and may benefit from a Solo 401(k). Specifically, we’ll cover:

What a Solo 401(k) plan is

How a Solo 401(k) can reduce tax liability

How to use a Solo 401(k) to build a larger Roth bucket

How to decide between pre-tax vs. Roth contributions

What happens when the Solo 401(k) is terminated

What Is a Solo 401(k) Plan?

A Solo(k) plan, also called an Individual(k), is a retirement plan designed for owner-only businesses. This means the business cannot have any full-time employees working more than 1,000 hours per year, other than the owner and possibly their spouse.

Because these plans only cover the business owner, they are typically simple to administer, often have little to no administrative costs, and still provide the full benefits of a traditional 401(k) plan.

Solo 401(k) plans include:

Pre-tax employee deferrals

Roth employee deferrals

Employer contributions

Potential 401(k) loan provisions

Contribution Limits (2026)

Solo 401(k) plans allow for relatively high contribution limits. For 2026:

Employee deferral limit: $24,500 (under age 50)

Age 50+ catch-up: $32,500 total deferral

Employer contribution: Up to 20% of net self-employment income (sole proprietor/partnership)

S-Corp employer contribution: Up to 25% of W-2 wages

Example

Let’s say a sole proprietor generates $40,000 in net self-employment income and is under age 50.

They could contribute:

$24,500 as an employee deferral

$8,000 as an employer contribution (20% of $40,000)

That’s a total of $32,500 going into a retirement account from just $40,000 of side hustle income.

That’s a powerful savings and tax planning opportunity.

Reducing Tax Liability

One of the primary reasons business owners establish Solo 401(k) plans is to reduce their overall tax liability.

If someone has:

W-2 income: $200,000

Self-employment income: $40,000

That self-employment income gets stacked on top of their W-2 income and may be taxed at a high marginal tax rate.

However, if that business owner contributes $30,000 of that $40,000 into a Solo 401(k) using pre-tax contributions, they may only pay income tax on $10,000 instead of the full $40,000.

That can result in significant tax savings.

Solo(K) Plans Can Potentially Eliminate Federal & State Income Taxes

If a business owner has less than the annual employee deferral limit in net income, they may be able to defer 100% of their self-employment income into the Solo 401(k).

Example:

Net self-employment income: $20,000

Employee deferral limit: $24,500

Since the income is lower than the limit, they could defer the entire $20,000 pre-tax, avoiding federal and state income tax on that income.

Note: They still must pay self-employment tax, but they can avoid income tax on that portion.

Building a Larger Roth Bucket

Another major benefit of a Solo 401(k) is the ability to build Roth retirement assets, which can be extremely valuable long-term.

Roth contributions are made after-tax, but:

The money grows tax-deferred

Withdrawals after age 59½ are tax-free

One major advantage of a Roth Solo 401(k) is:

There are no income limits for Roth 401(k) contributions.

This is very important because many high-income earners are phased out of Roth IRA contributions, but they can still contribute to a Roth Solo 401(k).

Example

Imagine a 29-year-old business owner with a side hustle contributing $24,500 per year to a Roth Solo 401(k). The money grows tax-deferred for 30 years and then all of the earning in the account can be withdrawn tax free after age 59½.

We also see this strategy used for retirees who do consulting work. If someone is 65+ and earning self-employment income but doesn’t need the income, they can contribute to a Roth Solo 401(k) and move that money into a tax-free growth bucket instead of a taxable brokerage account.

This can be a powerful long-term tax strategy regardless of age of the business owner.

To Roth or Not to Roth?

Remember, there are two types of contributions to a Solo 401(k):

1. Employee Deferral → Can be Pre-Tax or Roth

2. Employer Contribution → Typically Pre-Tax

For sole proprietors and partnerships:

Employer contribution = 20% of net earned income

For S-Corps:

Employer contribution = 25% of W-2 wages

Important: Only W-2 wages count — not S-Corp distributions

While SECURE Act 2.0 opened the door for Roth employer contributions, we are still waiting on full IRS guidance for this to be widely implemented in Solo 401(k) plans. So for now, employer contributions are generally still pre-tax, while employee deferrals can be Roth or pre-tax.

General Rule of Thumb

You might consider:

Pre-tax contributions if you are in a high tax bracket today

Roth contributions if you are in a lower tax bracket today or want tax-free income later

This is where tax planning and coordination with a financial advisor and CPA becomes very important.

What Happens When the Solo 401(k) Is Terminated?

Eventually, the self-employment income may stop. When that happens, the Solo 401(k) is typically terminated, and the assets are rolled into IRAs.

Typically:

Pre-tax Solo 401(k) money → Traditional IRA

Roth Solo 401(k) money → Roth IRA

The money can then continue growing in those IRA accounts, and the Solo 401(k) plan is closed.

Working With an Advisor Who Understands Solo 401(k) Plans

Solo 401(k) plans are extremely powerful, but there are important rules and nuances business owners must be aware of.

For example:

If you hire employees, you may have to discontinue the plan

Plan documents must be set up properly

Once plan assets exceed $250,000, you must file Form 5500 annually

There are coordination issues between your CPA and financial advisor

You must choose between pre-tax vs. Roth strategies

You must compare Solo 401(k) vs. SEP IRA vs. SIMPLE IRA

Because of these moving parts, it’s important to work with an advisor who understands how to design and manage Solo 401(k) plans properly as part of an overall financial and tax strategy.

Our firm offers free consultations for business owners and individuals with side hustle income who want to evaluate whether a Solo 401(k) plan makes sense for their situation. If you’d like help determining whether this strategy is right for you, we’d be happy to help you build a plan around your specific goals. Feel free to schedule your complementary consult via our website.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions About Solo 401(k) Plans

-

Who qualifies for a Solo 401(k)?Business owners with no full-time employees working more than 1,000 hours per year.

-

Can I have a W-2 job and a Solo 401(k)?Yes. As long as you have self-employment income, you can open a Solo 401(k) for that income.

-

How much can I contribute to a Solo 401(k)?In 2026, employee deferrals are $24,500 (under 50), plus employer contributions up to 20% of income (or 25% of W-2 wages for S-Corps).

-

Can I contribute 100% of my side hustle income?Yes, if your income is below the employee deferral limit, you may be able to defer the entire amount.

-

Do Solo 401(k) contributions reduce taxes?Yes, pre-tax contributions reduce your taxable income.

-

Can I make Roth contributions to a Solo 401(k)?Yes, employee deferrals can be Roth, with no income limits.

-

What happens when I stop my side hustle?The Solo 401(k) is typically rolled into a Traditional IRA and/or Roth IRA.

-

Is a Solo 401(k) better than a SEP IRA?In many cases, yes, because it allows Roth contributions and higher contributions at lower income levels.

-

Do I have to file anything for a Solo 401(k)?Once the account exceeds $250,000, you must file Form 5500 annually.

-

Can I take a loan from a Solo 401(k)?Some Solo 401(k) plans allow participant loans, similar to traditional employer 401(k) plans.

Borrowing from Your 401(k)? One Wrong Move Could Trigger a Massive Tax Bill

Borrowing from your 401(k) may seem simple, but one mistake, like leaving your job, can trigger taxes, penalties, and long-term damage to your retirement savings. Understanding the rules before you borrow is critical.

Borrowing from your 401(k) might seem like an easy way to access cash, no credit check, low interest, and you’re paying yourself back. But one wrong move can trigger immediate taxes, penalties, and a permanent hit to your retirement savings. The IRS has strict rules on how 401(k) loans must be repaid and what happens if you leave your job before it’s paid off. Understanding those rules before you borrow can help you avoid costly surprises.

How 401(k) Loans Work

Most employer-sponsored 401(k) plans allow participants to borrow up to the lesser of $50,000 or 50% of their vested balance. Loans typically have to be repaid within five years through automatic payroll deductions, and the interest you pay goes back into your account.

On paper, it looks simple. You’re borrowing from yourself and putting the money back over time. But the biggest risk comes if your employment status, or repayment schedule, changes.

The Costly Mistake: Leaving Your Job Before Repayment

If you leave your employer, voluntarily or otherwise, with an outstanding 401(k) loan, the clock starts ticking. Under IRS rules, you must repay the entire remaining balance by the tax-filing deadline of the following year.

If you don’t repay it in time, the IRS classifies the unpaid balance as a “deemed distribution.” That means:

The outstanding amount is treated as taxable income in that year.

If you’re under age 59½, you’ll also face a 10% early withdrawal penalty.

Example:

If you owe $20,000 on a 401(k) loan when you change jobs and don’t repay it, that $20,000 becomes taxable income. Assuming a 22% federal bracket, you’ll owe $4,400 in federal tax, plus a $2,000 early withdrawal penalty—a total of $6,400 lost instantly.

Our analysis at Greenbush Financial Group shows that many borrowers underestimate this risk, particularly if they expect to switch jobs or retire early.

Why the Real Cost Is Even Higher

Taxes and penalties are only part of the loss. When you default on a 401(k) loan:

You lose future growth on the money permanently removed from your retirement plan.

You can’t simply “rollover” the unpaid balance into an IRA—it’s treated as distributed cash.

In long-term projections, a $20,000 distribution today can mean over $60,000 less in retirement savings 20 years from now, assuming a 7% annual return.

Smart Ways to Borrow Without Derailing Your Retirement

If you’re considering a 401(k) loan, these steps can help minimize the risk:

Understand your plan’s terms. Confirm repayment rules, interest rates, and whether you can continue contributing while repaying the loan.

Have a backup plan. Keep cash reserves or other assets available in case you leave your job unexpectedly.

Avoid borrowing for depreciating expenses. Using retirement funds for short-term needs like vacations or vehicles can compound long-term losses.

Check your employment stability. If you expect to change jobs soon, it’s better to wait or use other financing options.

Compare alternatives. A home equity line of credit (HELOC) or personal loan may cost less in taxes and missed growth over time.

At Greenbush Financial Group, we often help clients run side-by-side projections showing the real long-term cost of borrowing from their 401(k) compared to other options. In most cases, the total impact of lost compounding far outweighs the short-term benefit of easy access to funds.

The Bottom Line

A 401(k) loan can make sense in limited cases, such as paying off high-interest debt or covering an emergency expense when other options are exhausted. But understanding the repayment rules—and the risk of job loss—is critical. One mistake, like leaving your employer before repaying the loan, can trigger thousands in taxes and permanently shrink your retirement balance.

Before taking out a loan, it’s worth modeling different scenarios with a financial planner to ensure your short-term decision doesn’t create a long-term setback.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

FAQs: 401(k) Loan Rules and Risks

-

What’s the maximum I can borrow from my 401(k)?Generally, up to $50,000 or 50% of your vested balance, whichever is less.

-

How long do I have to repay a 401(k) loan?Most plans require repayment within five years, except when borrowing to purchase a primary residence.

-

What happens if I default on my loan?The unpaid balance is treated as a taxable distribution and may incur a 10% early withdrawal penalty if you’re under age 59½.

-

Can I roll my 401(k) loan into an IRA or new employer plan?No, loans cannot be rolled over. The balance must be repaid directly to avoid taxes.

-

Should I ever take a 401(k) loan?Only if the need is critical and you’re confident you’ll remain employed through the repayment period.

2026 New York State Mandatory IRA Rules: What Employers Must Do to Stay Compliant

New York State’s Secure Choice IRA program is creating new compliance requirements for many employers beginning in 2026. Businesses with 10 or more employees that do not already offer a qualified retirement plan may be required to enroll workers in this state-facilitated Roth IRA program. Our analysis at Greenbush Financial Group explains who must comply, employer responsibilities, potential penalties, and why alternative retirement plans like SIMPLE IRAs or 401(k)s may offer greater long-term value.

New York State now requires many employers to offer a retirement savings option through the state-mandated Secure Choice IRA program. If your business has at least 10 employees and does not already offer a qualified retirement plan, participation is mandatory. Our analysis at Greenbush Financial Group shows that understanding who must comply, how the program works, and what alternatives exist can help business owners avoid penalties while improving employee retention. This article explains New York’s mandatory IRA rules and outlines smarter planning options for employers.

What Is the New York State Mandatory IRA Program?

The New York State mandatory IRA requirement applies through the New York State Secure Choice Savings Program, a state-facilitated retirement savings option for private-sector employees.

Secure Choice is designed for workers who do not have access to an employer-sponsored retirement plan. Employers act as facilitators, while the state oversees the program’s administration.

Key characteristics:

Roth IRA structure for employees

Automatic payroll deductions

No employer contributions required

State-administered investment options

Which New York Employers Are Required to Offer a Mandatory IRA?

Under New York law, participation is mandatory if all of the following apply:

You have 10 or more employees

You have been in business for at least two years

You do not currently offer a qualified retirement plan such as a 401(k), SIMPLE IRA, or SEP IRA

At Greenbush Financial Group, we commonly see confusion around part-time and seasonal employees. For Secure Choice purposes, employees are generally counted if they are on payroll, regardless of hours worked.

Which Businesses Are Exempt From the Requirement?

You are exempt from the New York mandatory IRA requirement if your business already offers:

A 401(k) or Safe Harbor 401(k)

A SIMPLE IRA

A SEP IRA

A defined benefit or cash balance pension plan

Offering any qualified retirement plan removes the obligation to participate in Secure Choice. This exemption often creates an opportunity for employers to choose a more flexible and customizable plan instead.

How the Secure Choice IRA Works for Employees

Eligible employees are automatically enrolled unless they opt out.

Default program features include:

Automatic enrollment at a preset contribution rate

Contributions made on a Roth (after-tax) basis

Employee-owned accounts that move with them if they change jobs

Limited investment menu selected by the state

Employees can:

Change contribution amounts

Opt out at any time

Withdraw funds subject to Roth IRA rules and penalties

Employer Responsibilities Under the Mandatory IRA Law

Although employers do not contribute financially, they still carry administrative responsibilities.

Employer duties include:

Registering with the Secure Choice program

Providing employee information

Processing payroll deductions

Submitting contributions on schedule

Distributing required employee notices

Failure to comply may result in state enforcement actions once deadlines are fully phased in.

Deadlines and Penalties for Non-Compliance

New York’s rollout is being phased in by employer size, with enforcement expected to increase through 2026.

Potential consequences of non-compliance include:

Monetary penalties

State enforcement notices

Increased scrutiny for repeat violations

Our analysis at Greenbush Financial Group suggests that many business owners delay action simply because they are unaware the rule applies to them.

Is Secure Choice the Best Option for Employers?

For some businesses, Secure Choice meets the minimum requirement. However, it may not be the best long-term solution.

Limitations of the mandatory IRA include:

No employer contribution flexibility

Roth-only structure

Limited investment choices

Reduced perceived benefit compared to a 401(k)

In contrast, alternatives such as SIMPLE IRAs or 401(k) plans can:

Increase tax deductions for employers

Improve employee recruitment and retention

Offer higher contribution limits

Allow customized plan design

At Greenbush Financial Group, we often help employers compare Secure Choice with private retirement plans to determine the most cost-effective and strategic solution.

Planning Considerations for Business Owners

When deciding how to comply, consider:

Your employee demographics and turnover

Tax deductions available to the business

Administrative complexity

Long-term growth and scalability

Choosing the right retirement plan is not just about compliance; it is a strategic business decision.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

Frequently Asked Questions About New York State Mandatory IRAs

-

Is the New York State Secure Choice IRA mandatory for all businesses?No. It is only mandatory for businesses with 10 or more employees that do not already offer a qualified retirement plan.

-

Do employers have to contribute to the Secure Choice IRA?No. Employers are not allowed or required to make contributions; only employee payroll deductions are permitted.

-

What happens if my business ignores the mandatory IRA requirement?Non-compliance may result in penalties and enforcement actions as the state increases oversight.

-

Can employees opt out of the New York mandatory IRA?Yes. Employees are automatically enrolled but may opt out or change contributions at any time.

-

Does offering a SIMPLE IRA exempt my business from Secure Choice?Yes. Offering a SIMPLE IRA, 401(k), or SEP IRA fully satisfies the requirement.

-

Is Secure Choice better than a 401(k) for small businesses?Not always. While Secure Choice is simple, many businesses benefit more from private plans with higher limits and tax advantages.

New York State Secure Choice Law — Companies Are Now Required to Sponsor Retirement Plans for Employees

New York’s SECURE Choice program is changing how many employers must handle retirement benefits. If your business doesn’t currently offer a qualified retirement plan, you may be required to either register for SECURE Choice or implement an alternative plan option. In this article, we break down who must comply, key deadlines, and what employers should do now to avoid penalties and ensure employees have a retirement savings solution.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

The New York State Secure Choice Savings Program requires most companies and not-for-profit organization in New York to either:

Sponsor a qualified employer-sponsored retirement plan, or

Register for the state-run Roth IRA program and remit employee contributions.

This law affects businesses based on size and existing retirement plan offerings. In this article, we’ll explain:

Who is covered under the law

Important effective dates by company size

What qualifies as an exempt employer-sponsored retirement plan

How to certify exemptions

Employer responsibilities in remitting contributions

How employees interact with their state-run IRAs

Penalties for non-compliance

Practical tips for employers to prepare

What Is the NY Secure Choice Savings Program?

The Secure Choice program is a state-sponsored retirement savings program that allows participating employees to save for retirement through automatic payroll deductions into a Roth IRA. Employers who do not already offer a qualified plan are required to facilitate the program.

The program is overseen by the New York Secure Choice Savings Program Board and is designed to expand retirement savings access to private-sector workers across the state.

Who Must Comply?

An employer must either offer a employer-sponsored retirement plan or participate in the Secure Choice program if all of the following are true:

The employer has 10 or more employees in New York during the prior calendar year;

The employer has been in business for at least two years;

The employer does not already offer an employer-sponsored retirement plan to employees.

Employers with fewer than 10 employees are generally not required to participate in the state program, though they must still register and certify exemption if applicable.

Effective Dates Based on Employer Size

Secure Choice implementation in 2026 is staggered based on the number of New York employees:

These are the dates by which employers must either:

Register for the Secure Choice program, or

Certify exemption via the official state portal.

Exemptions: Qualifying Employer-Sponsored Retirement Plans

However, even if an employer meets the employee-size threshold above, it is exempt from the Secure Choice program if it already sponsors an employer-sponsored retirement plan. Employers must still certify their exemption through the Secure Choice portal.

Qualifying employer-sponsored plans include:

401(k) plans

403(a) qualified annuity plans

403(b) tax-sheltered annuity plans

SEP IRAs

SIMPLE IRA plans

457(b) plans

If you offer one of the above, your business can avoid participation in the state program — but you must still submit an exemption through the official portal.

How to Certify an Exemption

Employers seeking exemption need to log in to the Secure Choice employer portal and submit documentation of their qualified plan. Details include:

Federal Employer Identification Number (EIN)

Access Code (typically sent to employers by mail or email)

Plan documentation showing current retirement plan offerings

Official website for registration and exemptions: www.NewYorkSecureChoice.com

Employer Responsibilities if Participating in Secure Choice

If your business does not qualify for an exemption, you must:

Register for Secure Choice by the deadline assigned to your employer size.

Automatically enroll eligible employees into the program. (Eligibility is all employee age 18 or older with earned taxable wages)

Set up payroll deductions and begin subtracting employee contributions.

Remit contributions to the state-administered Roth IRAs.

Upload employee data and maintain records via the program portal.

Employers do not contribute to the accounts, and they cannot offer matching contributions under the Secure Choice IRA program.

How Contributions Work

Remitting Employee Payroll Contributions

Contributions are deducted from employee paychecks via automatic payroll withholding.

Employers are responsible for timely remittance of these contributions to the state program’s recordkeeper (program administrators).

Employers do not make employer contributions.

Default Contribution and Adjustments

Employees are typically auto-enrolled at a default 3% contribution rate of gross pay.

Employees may adjust the contribution amount or opt out entirely within the enrollment period or later open enrollment windows.

Employee Experience With Secure Choice

Account Setup and Features

Each participating employee gets a Roth IRA account through the Secure Choice program.

Contributions are after-tax, meaning withdrawals in retirement are generally tax-free (subject to Roth IRA rules).

Accounts are portable — employees keep them even if they change jobs.

Investing, Contribution Limits, and Withdrawals

Employees can choose investment options provided by the program or stay with the default investment.

They can change contribution rates or opt out after the initial enrollment period.

Roth IRA contribution limits apply (e.g., the standard IRA annual limits — $7,500 for 2026 before catch-up, potentially higher with catch-up contributions for those 50+, etc.).

Distributions follow general Roth IRA rules (qualified distributions tax-free and penalty-free after meeting age/service requirements).

How Employees Are Enrolled in the NY Secure Choice Roth IRA Program

A common question from employers is whether they are responsible for enrolling employees, or whether employees must sign themselves up. Under the New York State Secure Choice Savings Program, the process works as follows:

Employers Facilitate Enrollment — Employees Do Not Self-Enroll

Employers do not actively “sign up” employees, and employees do not enroll themselves directly. Instead, enrollment happens through automatic payroll facilitation by the employer.

Here’s how the process works step-by-step:

Step 1: Employer Registers and Uploads Employee Information

Once an employer registers for Secure Choice (or confirms participation is required), the employer must:

Upload required employee data into the Secure Choice employer portal, including:

Employee name

Social Security number or Tax ID

Date of hire

Contact information

Identify eligible employees who meet program requirements

For newly hired employees, the employer needs to enroll them in the Secure Choice Program within 30 days of their hire date

This step triggers the enrollment process, but it does not immediately deduct contributions.

Step 2: Employees Receive Enrollment Notice From the State Program

After the employer uploads employee information:

The Secure Choice program (or its appointed program administrator) sends official enrollment notices directly to employees

The notice explains:

That the employee will be automatically enrolled

The default contribution rate

How to opt out or change contribution levels

Where to access their account online

This communication comes from the state program, not the employer.

Step 3: Automatic Enrollment Occurs Unless the Employee Opts Out

If the employee takes no action during the notice period:

The employee is automatically enrolled in a state-sponsored Roth IRA

Payroll deductions begin at the default contribution rate (generally 3% of gross pay, unless adjusted by the employee)

If the employee chooses to opt out:

No deductions are taken

The employer must maintain records showing the opt-out election

Step 4: Employer Begins Payroll Withholding and Remittance

Once enrollment is active:

The employer withholds the elected contribution amount from each paycheck

Contributions are remitted to the Secure Choice program on a recurring basis, aligned with payroll schedules

The employer’s role is limited to withholding and remitting contributions — similar to payroll taxes

Importantly:

Employers do not select investments

Employers do not manage accounts

Employers do not provide investment advice

Employers do not contribute employer funds

Step 5: Ongoing Employee Control

After enrollment:

Employees manage their own accounts directly through the Secure Choice program

Employees can:

Change contribution percentages

Opt out or opt back in later

Select or change investment options

Request distributions (subject to Roth IRA rules)

The account belongs to the employee and is fully portable if they change jobs.

Penalties for Non-Compliance

While specific penalties in the Secure Choice law are still being formalized, failure to register or certify your exemption by the applicable deadline can subject employers to:

Administrative penalties and fines

Potential liability for missed remittance obligations

Ongoing penalties until compliance is achieved

For example, programs in other states have assessed penalties like $250 per employee per month for non-compliance, escalating over time. While New York’s specific fines may vary, the risk of enforcement is real and growing as the program rolls out statewide. However, as of February 2026, New York has yet to communicate when penalities will begin and what the amounts will be.

Tips for Employers

Start Early — Don’t Wait

Act well in advance of your registration deadline. If your company currently sponsors an employer-sponsored retirement plan, it’s making sure someone on your team will be logging into the NYS portal to file the exemption. For companies that plan to implement an employer-sponsored retirement plan prior to their deadline, there is extreme urgency to start evaluating as soon as possible both the type of plan that is best for the company and the platform for their plan. Establishing an employer-sponsored plan often involves:

Plan design and adoption

Document creation and compliance testing

Employee communications and elections

Payroll integration

If it’s the intent of your company / organization not establish a retirement plan and enroll employees in the state-mandated Roth IRAs, advanced action is still required. Companies will be required to gather the employee data and upload it to the NYS Secure Choice website, confirm how payroll will handle the automatic Roth deductions from payroll, who will be responsible for remitting the contributions to the NYS platform each pay period, and communication to the employees in advance of the payroll deduction is highly recommended.

Many businesses will be acting on these requirements in 2026 — waiting until the last minute can create unnecessary compliance risk.

Evaluate Whether to Offer Your Own Plan

Offering a 401(k) or other qualified plan may be more attractive for recruiting and retention, may allow employer matching, and could provide tax incentives not available under the state program. Also, there are a number of tax credits currently available to help offset some or all of the plan fees associated with establishing an employer-sponsored retirement plan for the first time. See our article below for detail on the start-up plan tax credits available:

GFG Article: 3 New Start-up 401(k) Tax Credits

How Many Other States Have Similar Mandated Retirement Programs?

New York is not alone in adopting a mandatory retirement savings program for private-sector employees. In fact, Secure Choice builds on a growing national trend aimed at addressing the retirement savings gap for workers who do not have access to an employer-sponsored plan.

As of today:

More than a dozen states (15+) have enacted legislation requiring certain employers to either:

Offer a qualified employer-sponsored retirement plan, or

Participate in a state-facilitated IRA program funded through payroll deductions.

Several of these programs are fully operational, while others are in various stages of implementation or phased rollout.

States that were early adopters (such as California, Oregon, and Illinois) now have millions of workers enrolled and billions of dollars in assets within their state-facilitated retirement programs.

New York Has Selected Vestwell

New York has selected a company by the name of Vestwell to serve as the program administrator for the state-mandated Roth IRA accounts.

Choosing a Startup Retirement Plan Provider: What Employers Should Know

For many employers, the Secure Choice law will prompt a first-time decision about whether to start an employer-sponsored retirement plan instead of participating in the state-run IRA program. While this can be a positive move for employee recruitment and retention, it’s important to understand that not all startup plan providers — or pricing models — are the same.

There Are Many Choices — and Fees Vary Widely

Employers exploring startup plans will quickly find a wide range of providers, including bundled platforms, payroll-integrated solutions, and self-directed providers. Costs can differ significantly depending on:

Plan administration fees

Investment platform and fund expenses

Recordkeeping and compliance costs

Per-participant charges

Advisor or fiduciary service fees (if applicable)

Some providers advertise low headline pricing but layer on additional costs elsewhere. Others charge flat fees that may be economical at certain asset levels but expensive for smaller plans. Understanding how fees are structured — and how they may grow over time — is critical when selecting a provider.

Start-up 401(k) Provider

In the past, we have worked with companies that successfully used Employee Fiduciary as a start-up 401(k) solution. Employee Fiduciary is a national-level 401(k) provider that offers flexibility with plan design, Vanguard index funds for investment options, and fee transparency.

Disclosure: This statement is not an endorsement of Employee Fiduciary or their 401(k) solution. Our firm has had experience in working with Employee Fiduciary in the past, and since we do not offer investment services to start-up plans, we want to be able to connect readers with what I, as the author of this article, deem to be a high-quality start-up 401(k) plan solution. Our firm does not receive any form of compensation for referring clients to Employee Fiduciary.

Conclusion

The New York Secure Choice Savings Program represents a significant change for private employers in the state. Whether you must register for the state-run IRA program or certify exemption with your existing retirement plan, compliance is mandatory and deadlines are coming fast in 2026.

By planning ahead — and consulting legal, tax, or benefits professionals if needed — employers can meet these requirements smoothly while ensuring their employees have access to valuable retirement savings opportunities.

A Note on Our Firm’s Focus

Our firm does not offer solutions for brand-new startup plans. We specialize in working with established retirement plans that already have at least $250,000 in plan assets, for which we provide investment management and plan consulting services.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

How Do Executive Non-Qualified Deferred Compensation Plans Work?

If you're a high-income executive, you’ve likely hit the contribution ceiling on your 401(k) or other qualified plans. So what’s next?

Enter the non-qualified deferred compensation (NQDC) plan—a tax deferral strategy designed for executives who want to save more for retirement beyond traditional limits.

For highly compensated employees, saving for retirement isn’t always as simple as maxing out a 401(k). When income exceeds traditional plan limits, non-qualified deferred compensation (NQDC) plans—often offered to executives—can provide a powerful way to defer taxes and accumulate wealth beyond standard retirement vehicles.

But how do these plans actually work? And what should executives know before deferring compensation?

Let’s break it down.

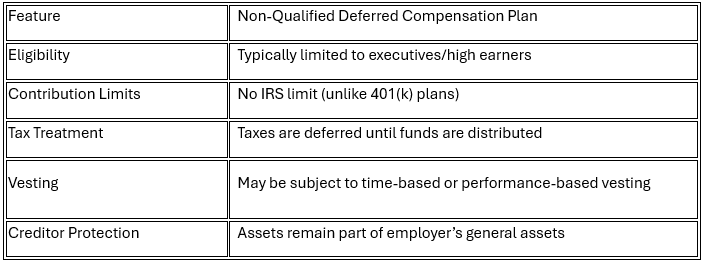

What Is a Non-Qualified Deferred Compensation Plan?

An NQDC plan is an employer-sponsored agreement that allows certain employees—typically executives or other key personnel—to defer a portion of their income to a future date, such as retirement or separation from service.

Unlike qualified plans (such as a 401(k)), these plans do not fall under ERISA coverage and do not have contribution limits set by the IRS. This makes them attractive for those whose income exceeds the maximum deferral limits in traditional plans.

Key Features

How Deferrals Work

An executive elects—in advance of the year earned—to defer a portion of salary, bonus, or other compensation. This election is typically irrevocable for that year and must comply with IRC Section 409A.

For example:

Jane, a CFO earning $600,000, defers $100,000 of her 2025 compensation into her company’s NQDC plan. She’ll pay no income tax on that $100,000 in 2025—it'll be taxed when she receives the funds in retirement or at a future distribution date.

Distribution Options

The executive can usually choose from a menu of payout options, such as:

Lump sum at retirement

Installments over 5–10 years

Specific distribution events (e.g., separation from service, death, disability)

Important: Once the distribution schedule is set, changing it often requires a five-year delay and must follow 409A regulations to avoid penalties.

Tax Considerations

Deferred income is not taxed until it’s actually received.

Funds may grow tax-deferred in an investment vehicle selected by the participant or the employer.

Unlike a 401(k), contributions are not protected from creditors—they remain employer assets until distributed.

Distributions are taxed as ordinary income, not capital gains.

What Are the Risks?

NQDC plans can be valuable, but they come with risks not present in qualified plans:

Employer Solvency: Since funds remain part of the employer’s general assets, they could be lost in bankruptcy.

Limited Access: You cannot take early withdrawals without triggering taxes and penalties under 409A.

Inflexibility: Election and distribution decisions are difficult to change once made.

Unfunded plan: NQDC plans are not required to be “funded” by the employer like a 401(k) plan so it may just be a future promise of the employer to pay those amounts out to the employee when the benefit vests. This adds additional risk for the executive.

When Does an NQDC Plan Make Sense?

An NQDC plan can be a smart tool for:

High W2 earners who max out traditional retirement plans and want to save more

Executives with predictable income and long-term tenure at the company

Those expecting to be in a lower tax bracket in retirement

Executives who are employed by a financially strong company

However, it may not be suitable for someone with:

Uncertainty around staying with the employer long-term

Concerns about the company’s financial health

A need for liquidity or access to funds before retirement

Final Thought

Non-qualified deferred compensation plans can be a powerful tax deferral and wealth-building tool for high-income executives, but they require careful planning. Because these plans carry unique risks and limited flexibility, it’s important to review your full financial picture, long-term goals, and employer stability before making a deferral election.

If you're considering participating in your company’s NQDC plan, talk to a financial planner who understands executive compensation and tax strategy. The right guidance can help you avoid missteps and make the most of what these plans have to offer.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What is a Non-Qualified Deferred Compensation (NQDC) plan?

A Non-Qualified Deferred Compensation (NQDC) plan is an employer-sponsored arrangement that allows select employees—typically executives or highly compensated individuals—to defer a portion of their income to a future date, such as retirement or separation from service. These plans are not subject to the same IRS limits as 401(k)s, allowing for greater savings potential.

How does an NQDC plan work?

Participants elect in advance to defer a portion of their salary, bonuses, or other compensation before it is earned. The deferred income grows tax-deferred until distributed, usually at retirement or another specified event. Because the funds technically remain part of the employer’s assets, they are not taxed until paid out to the employee.

When do I have to make my deferral election?

Under IRS Section 409A, deferral elections must be made before the start of the year in which the income is earned. These elections are generally irrevocable for that year and must follow strict timing and compliance rules to avoid penalties.

How are NQDC distributions paid?

Participants usually choose a distribution schedule when enrolling in the plan. Common options include a lump sum at retirement or installment payments over 5–10 years. Once the schedule is selected, it’s difficult to change without a five-year delay and compliance with Section 409A regulations.

How is deferred compensation taxed?

Deferred income and its growth are not taxed until distributed. When payouts occur, the amounts are taxed as ordinary income—not capital gains. However, if the plan violates 409A rules, deferred amounts could become immediately taxable with additional penalties.

Are NQDC plans protected from creditors?

No. Unlike 401(k)s, NQDC plan assets remain part of the employer’s general assets until distributed. This means that if the company faces bankruptcy or insolvency, participants may lose their deferred compensation.

What are the main risks of participating in an NQDC plan?

The key risks include employer insolvency, lack of liquidity, and limited flexibility. Because plans are often unfunded and cannot be accessed early without tax penalties, participants rely on their employer’s financial strength and long-term stability.

Who should consider using an NQDC plan?

These plans are best suited for high earners who have already maxed out qualified retirement plans, expect to stay with their employer long-term, and anticipate being in a lower tax bracket in retirement. They may also be attractive for executives at financially stable companies.

Who might want to avoid an NQDC plan?

NQDC plans may not be appropriate for individuals who expect to leave their employer soon, need short-term access to funds, or are concerned about the company’s financial health. Those uncertain about their future tax situation should also evaluate carefully before deferring large amounts.

What’s the difference between an NQDC plan and a 401(k)?

A 401(k) is a qualified, ERISA-protected plan with contribution limits and creditor protection. An NQDC plan is non-qualified, has no IRS contribution limits, offers greater flexibility in savings amounts, but lacks creditor protection and carries employer solvency risk.

Can I change my payout schedule after enrolling?

Generally no—changes to distribution timing or method require at least a five-year deferral from the original payout date and must follow strict Section 409A rules to avoid penalties.

Should I consult a financial planner before enrolling in an NQDC plan?

Yes. Because NQDC plans involve complex tax, investment, and timing decisions, working with a financial planner or tax advisor experienced in executive compensation can help you optimize your deferral strategy and manage potential risks.

Mandatory 401(k) Roth Catch-up Details Confirmed by IRS January 2025

IRS Issues Guidance on Mandatory 401(k) Roth Catch-up Starting in 2026

Starting January 1, 2026, high-income earners will face a significant shift in retirement savings rules due to the new Mandatory Roth Catch-Up Contribution requirement. If you earn more than $145,000 annually (indexed for inflation), your catch-up contributions to 401(k), 403(b), or 457 plans will now go directly to Roth, rather than pre-tax.

The IRS just released guidance in January 2025 regarding how the new mandatory Roth catch-up provisions will work for high-income earners. This article dives into everything you need to know!

On January 10, 2025, the IRS issued proposed regulations that provided much-needed clarification on the details associated with the Mandatory Roth Catch-up Contribution rule for high-income earners that are set to take effect on January 1, 2026. Employers, payroll companies, and 401(k) providers alike will undoubtedly be scrambling for the remainder of 2025 to get their systems ready for this restriction that will be placed on 401(k) plans starting in 2026.

This is a major change within 401(k) plans, and it is not a welcome change for high-income earners, since individuals in high tax brackets typically like to defer as much as they can pre-tax into 401(k), 403(b), and 457 plans to reduce their current tax liability. Here’s a quick list of the items that will be covered in this article:

General overview of new mandatory 401(k) Roth Catch-up Requirement

Income threshold for employees that will be impacted by the new rule

Definition of “wages” for purposes of the income threshold

Will it apply to Simple IRA plans as well?

“First year of employment” exception for the new Roth rule

Will a 401(k) plan be required to adopt Roth deferrals prior to 1/1/26?

401(k) Mandatory Roth Catch-up Contributions

When an employee reaches age 50, they can make an additional employee deferral called a catch-up contribution. Prior to 2026, all employees were allowed to select whether they wanted to make their catch-up contributions in pre-tax, Roth, or a combination of both. Starting in 2026, the freedom of choice will be taken away from W-2 employees that have more than $155,000 in wages in the prior calendar year (indexed for inflation).

Employees that are above the $155,000 threshold for the previous calendar year, are with the SAME employer, and are age 50 or older, will not be given the option to make their catch-up in pre-tax dollars. If an employee over this wage threshold wishes to make a catch-up contribution to their qualified retirement plan (401K, 403b, 457b), they will only be given the Roth deferral option.

Definition of Wages

One of the big questions that surfaced when the Secure Act 2.0 regulations were first released regarding the mandatory Roth catch-up contribution was the definition of “wages” for the purpose of the $145,000 income threshold. The IRS confirmed in their new regulation that only wages subject to FICA tax would count towards the $145,000 threshold. This is good news for self-employed individuals such as sole proprietors and partnerships that have earnings that are more than the $145,000 threshold, but do not receive W-2 wage, allowing them to continue to make their catch-up contributions all pre-tax for years 2026+.

So essentially, you could have partners of a law firm making $500,000+, and they would be able to continue to make catch-up contributions all pre-tax, but the firm could have a W-2 attorney on their staff that makes $180,000 in wages, and that individual would be forced to make their catch-up contributions all in Roth dollars and pay income tax on those amounts.

Will Mandatory Roth Catch-up Apply to Simple IRA Plans?

Many small employers sponsor Simple IRA plans, which also allow employees aged 50 or older to make pre-tax catch-up contributions, but at lower dollar limits. Fortunately, Simple IRA plans have been granted a pass by the IRS when it comes to the new mandatory Roth catch-up contributions. All employees that are covered by a Simple IRA plan, regardless of their wages, will be allowed to continue to make their catch-up contributions, all pre-tax, for tax years 2026+.

First Year of Employment Exception

Since the $145,000 wage threshold is based on an employee’s “prior year” wages, the IRS confirmed in the new regulations that an employer is allowed to give employees a pass on making pre-tax catch-up contributions during the first calendar year that the company employs them. Meaning, if Sue is hired by Company ABC in February of 2025 and makes $250,000 from February – December in 2025, she would be allowed to contribute her 401(k) catch-up contributions all pre-tax if she is over 50 years old, since Sue doesn’t have wages with Company ABC in 2024, even though her wages for the 2025 were over the $145,000 threshold.

Some High-Income Employees Will Get A 2-Year Pass

There are also situations where new employees with wages over $155,000 will get a 2-year pass on the application of the mandatory Roth catch-up rule. Let’s say Tim is hired by a law firm as a W-2 employee on July 1, 2026, at an annual salary of $200,000. Tim automatically gets a pass for 2026 for the mandatory Roth catch-up, because he did not have wages in 2025 with that company. However, between July 1, 2026 – December 31, 2026, he will only earn half his salary ($100,000), so when they look at Tim’s W-2 wages for purposes of the mandatory Roth catch-up in 2027, his 2026 W-2 will only be showing $100,000, allowing him to make his catch-up contribution all pre-tax in both 2026 and 2027.

Will 401(k) Plans Be Forced to Adopt Roth Deferrals

Not all 401(k) or 403(b) plans allow employees to make Roth employee deferrals. Roth deferrals have historically been an optional provision within an employer-sponsored retirement plan that a company had to voluntarily adopt. When the regulations for the new mandatory Roth catch-up were first released, the regulations seemed to state that if a plan did not allow Roth deferrals, NO EMPLOYEES, regardless of their wage level, were allowed to make catch-up contributions to the plan.

In the proposed regulations that the IRS just released, the IRS clarified that if a retirement plan does not allow Roth deferrals, only the employees above the $155,000 wage threshold would be precluded from making contributions. Employees below the $155,000 wage threshold would still be able to make catch-up contributions pre-tax, even without the Roth deferral feature in the plan.

Due to this restriction, it is expected that if a plan did not previously allow Roth deferrals, many plans will elect to adopt a Roth deferral option by January 1, 2026, to avoid this restriction on their employees with wages in excess of $155,000 (indexed for inflation).

For more information on this new Mandatory Roth Catch-Up Contribution effective 2026, please see our article: https://www.greenbushfinancial.com/all-blogs/roth-catch-up-contributions-high-wage-earners-secure-act-2

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What is the new Mandatory Roth Catch-Up Contribution rule?

Beginning January 1, 2026, employees age 50 and older who earned more than $145,000 in wages (indexed for inflation) from their employer in the previous calendar year must make all catch-up contributions to their 401(k), 403(b), or 457(b) plan as Roth (after-tax) contributions. High-income employees will no longer have the option to make pre-tax catch-up contributions.

Who is affected by the new Roth catch-up rule?

Only W-2 employees with wages over $145,000 in the previous calendar year from the same employer are affected. Employees earning $145,000 or less may continue to choose between pre-tax and Roth catch-up contributions.

How does the IRS define “wages” for this rule?

The IRS clarified that “wages” refer to compensation subject to FICA tax (i.e., W-2 wages). This means self-employed individuals, partners, or sole proprietors whose income is not reported as W-2 wages are not subject to the mandatory Roth catch-up requirement and can continue making pre-tax catch-up contributions after 2026.

Do Simple IRA or SEP IRA plans have to comply with this rule?

No. The Mandatory Roth Catch-Up rule applies only to qualified employer-sponsored plans such as 401(k), 403(b), and 457(b) plans. Simple IRAs and SEP IRAs are exempt, allowing all employees to continue making pre-tax catch-up contributions regardless of income.

What is the “first year of employment” exception?

The IRS confirmed that the $145,000 wage limit applies only to wages from the prior calendar year with the same employer. Therefore, employees in their first year with a new employer are not subject to the Roth catch-up rule, even if their current-year wages exceed $145,000.

Can new high-income employees get a two-year pass?

Yes, in some cases. For example, if an employee joins a company midyear (e.g., July 2025) and earns less than $145,000 that year, they will be exempt in both 2025 and 2026 because their prior-year wages were below the threshold.

What if my 401(k) plan doesn’t currently allow Roth deferrals?

If a plan does not offer a Roth option, the IRS clarified that only high-income employees (earning over $145,000) will be barred from making catch-up contributions starting in 2026. Employees earning below the threshold can continue making pre-tax catch-ups even if the plan lacks a Roth feature.

Will employers be required to add Roth deferral options to their 401(k) plans?

While not legally required, most employers are expected to add Roth deferral options by January 1, 2026, to prevent their high-income employees from losing the ability to make catch-up contributions altogether.

Why are these changes being implemented?

The new Roth catch-up rule was introduced under the SECURE Act 2.0 to increase tax revenue in the short term by requiring high-income employees to pay income tax on their catch-up contributions now rather than deferring taxation until retirement withdrawals.

Last updated June, 2026

A Complex Mess: Simple IRA Maximum Contributions 2026 and Beyond

Prior to 2025, it was very easy to explain to an employee what the maximum Simple IRA contribution was for that tax year. Starting in 2025, it will be anything but “Simple”. Thanks to the graduation implementation of the Secure Act 2.0, there are 4 different limits for Simple IRA employee deferrals that both employees and companies will need to be aware of.

Before the IRS changed the rules in 2024 it was very easy to explain to an employee what the maximum Simple IRA contribution was for that tax year. For plan years 2025 and later, it will be anything but “Simple”. Thanks to the gradual implementation of the Secure Act 2.0, there are 4 different limits for Simple IRA employee deferrals that both employees and companies will need to be aware of.

2026 Normal Simple IRA Deferral Limit

Like past years, there is a normal employee deferral limit of $17,000 in 2026.

NEW: Roth Simple IRA Deferrals

When Secure Act 2.0 passed, for the first time ever, it allowed Roth Deferrals to Simple IRA plans. However, due to the lack of guidance from the IRS, there are very few Simple IRA platforms that allow Roth deferrals. However, we do know of one mainstream platform that has announced that it will allow Roth Simple IRA deferrals starting in the fall of 2026. So, for now, most employees are still limited to making pre-tax deferrals to their Simple IRA plan, but in the not-too-distant future, once more platforms allow this deferral option, it will be another layer of complexity, whether or not an employee wants to make pre-tax or Roth Simple IRA deferrals.

2026 Age 50+ Catch-up Contribution

Like in past years, any employee aged 50+ is also allowed to make a catch-up contribution to their Simple IRA over and above the regular $17,000 deferral limit. In 2026, the age 50+ catch-up is $4,000, for a total of $21,000 for the year.

Under the old rules, this would have been it, plain and simple, but here are the new more complex Simple IRA employee deferral maximum contribution rules for 2025+.

NEW: Age 60 to 63 Additional Catch-up Contribution

Secure Act 2.0 introduced a new enhanced catch-up contribution starting in 2025, but it is only available to employees that are age 60 – 63. Employees ages 60 – 63 are now able to contribute the regular deferral limit ($17,000) PLUS the age 50 catch-up ($4,000) PLUS the new age 60 – 63 catch-up ($1,250).

Regular Deferral: $17,000

Regular Age 50+ Catch-up: $4,000

New Age 60 – 63 Catch-up: $1,250

Total: $22,250

But, the additional age 60 – 63 catch-up contribution is lost in the year that the employee turns age 64. When they turn 64, they revert back to the regular catch-up limit of $4,000

NEW: Additional 10% EE Deferral for ALL Employees

I wish I could say the complexity stops there, but it doesn’t. Introduced in 2024 was a new additional 10% employee deferral contribution that is available to ALL employees regardless of age, but automatic adoption of this additional 10% contribution depends on the size of the employer sponsoring the Simple IRA plan.

If the employer that sponsors the Simple IRA plan has no more than 25 employees who received $5,000 or more in compensation on the preceding calendar year, adoption of this new additional 10% deferral limit is MANDATORY, even though no changes have been made to the 5304 and 5305 Simple Forms by the IRS.

What that means is for 2026 is if an employer had 25 or fewer employees that made $5,000 in the previous year, the regular employee deferral limit AND the regular catch-up contribution limit will automatically be increased by 10% of the 2024 limit. Something odd to note here: The additional 10% is based just on the 2024 contribution limits, even though there are new increased limits for 2025 and 2026.

Employee Deferral Limit: $17,000

Employee Deferral with Additional 10%: $17,600 ($16,000 x 110%)

Employee 50+ Catch-up Limit: $3,700

Employee 50+ Catch-up Limit with Additional 10%: $3,850 ($3,500 2024 limit x 110%)

What this means is if an employee is covered by a Simple IRA plan in 2026 and that employer had less than 26 employees in 2025, for an employee under the age of 50, the Simple IRA employee deferral limit is not $17,000 it’s $17,600. For employees ages 50 – 59 or 64+, the employee deferral limit with the catch-up is not $20,700, it’s $21,450.

For employers that have 26 – 100 employees who, in the previous year, made at least $5,000 in compensation, in order for the employees to gain access to the additional 10% employee deferral, the company has to sponsor either a 4% matching contribution or 3% non-elective which is higher than the current standard 3% match and 2% non-elective.

NOTE: The special age 60 – 63 catch-up contribution is not increased by this 10% additional contribution because it was not in existence in 2025, and this 10% additional contribution is based on 2025 limits. The age 60 – 63 special catch-up contribution remains at $1,250, regardless of the size of the employer sponsoring the Simple IRA plan.

Summary of Simple IRA Employee Deferral Limits for 2026

EMPLOYER UNDER 26 EMPLOYEES

Employee Deferral Limit: $17,600

Employees Ages 50 – 59: $21,450

Employees Ages 60 – 63: $22,850

Employees Age 64+: $21,450

EMPLOYERS 26 EMPLOYEES or MORE

(Assuming they do not sponsor the enhanced 4% match or 3% non-elective ER contribution)

Employee Deferral Limit: $17,000

Employees Ages 50 – 59: $21,000

Employees Ages 60 – 63: $22,250

Employees Age 64+: $21,000

However, if the employer with 26+ employees sponsors the enhanced employer contribution amounts, the employee deferral contribution limits would be the same as the Under 26 Employees grid.

What a wonderful mess……

Voluntary Additional Simple IRA Non-Elective Contribution

Everything we have addressed up to this point focuses solely on the employee deferral limits to Simple IRA plans. Secure Act 2.0 also introduced a voluntary non-elective contribution that employers can make to their employees in Simple IRA plans. Prior to Secure Act 2.0, the only EMPLOYER contributions allowed to Simple IRA plans was either the 3% matching contribution or the 2% non-elective contribution.

Starting in 2024, employers that sponsor Simple IRA plans are now allowed to voluntarily make an additional non-elective employer contribution to all of the eligible employees based on the LESSER of 10% of compensation or $5,000. This additional employer contribution can be made any time prior to the company’s tax filing, plus extensions.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What is the Simple IRA contribution limit for 2025?

For 2025, the standard Simple IRA employee deferral limit is $16,500 for employers with more than 25 employees. For employers with 25 or fewer employees, the 2025 employee deferral limit is $17,600. Employees aged 50 or older can make an additional $3,500 catch-up contribution for employer with 25 or more employees and the a catch-up contribution of $3,850 for employers with 25 or less employees, bringing their total allowable deferral to $20,000 or $21,450, depending on the size of the employer.

What new changes apply to Simple IRA plans in 2025?

Beginning in 2025, several new rules from the SECURE Act 2.0 will apply to Simple IRA plans. There are now four potential contribution limits depending on an employee’s age and employer size. These include new Roth deferrals, a special age 60–63 catch-up contribution, and an additional 10% deferral increase for smaller employers.

Can employees make Roth contributions to a Simple IRA in 2025?

Yes, the SECURE Act 2.0 allows Roth deferrals to Simple IRA plans. However, as of early 2025, most custodians and investment platforms have not yet implemented this option, so most employees are still limited to pre-tax contributions.

What is the age 50+ catch-up contribution limit for 2025?

It depends on the size of your employer. As mentioned above, employees aged 50 or older can make an additional $3,500 catch-up contribution for employers with 25 or more employees and the a catch-up contribution of $3,850 for employers with 25 or less employees, bringing their total allowable deferral to $20,000 or $21,450, depending on the size of the employer.

What is the new age 60–63 catch-up contribution?

Starting in 2025, employees aged 60 through 63 can make an additional catch-up contribution equal to 50% of the standard catch-up limit. For 2025, this adds $1,750, to the maximum limits listed above. Once an employee turns 64, this enhanced catch-up no longer applies.

How does the new 10% additional employee deferral rule work?

Employers with 25 or fewer employees who earned $5,000 or more in the previous year must automatically offer a 10% higher employee deferral limit. This raises the standard limit from $16,500 to $17,600 and the age 50+ catch-up from $3,500 to $3,850.

Do larger employers also have access to the 10% deferral increase?

Employers with 26 to 100 employees can offer the additional 10% deferral if they increase their matching contribution to 4% or provide a 3% non-elective contribution.

Does the 10% increase apply to the new age 60–63 catch-up contribution?

No. The 10% deferral increase is based on 2024 contribution limits, and since the age 60–63 catch-up did not exist in 2024, it remains at $1,750 for 2025 regardless of employer size.

What are the 2025 Simple IRA limits for small employers (25 or fewer employees)?

Under age 50: $17,600

Ages 50–59: $21,450

Ages 60–63: $22,850

Age 64 and older: $21,450

What are the 2025 limits for larger employers (26 or more employees)?

If the employer does not offer the enhanced match or non-elective contribution:

Under age 50: $16,500

Ages 50–59: $20,000

Ages 60–63: $21,750

Age 64 and older: $20,000

If the employer does offer the enhanced contribution, the higher limits for small employers apply.

What is the new voluntary employer non-elective contribution option?

Starting in 2024, employers may make an additional non-elective contribution equal to the lesser of 10% of employee compensation or $5,000. This contribution is optional and can be made in addition to the standard employer match or non-elective contribution before the company’s tax filing deadline, including extensions.

Last updated June, 2026

New Age 60 – 63 401(k) Enhanced Catch-up Contribution Starting in 2025

Good news for 401(k) and 403(b) plan participants turning age 60 – 63 starting in 2025: there is now an enhanced employee catch-up contribution thanks to Secure Act 2.0 that passed back in 2022. For 2025, the employee contributions limits are as follows: Employee Deferral Limit $23,500, Age 50+ Catch-up Limit $7,500, and the New Age 60 – 63 Catch-up: $3,750.

Good news for 401(k) and 403(b) plan participants turning age 60 – 63 starting in 2025: there is now an enhanced employee catch-up contribution thanks to Secure Act 2.0 that passed back in 2022. For 2025, the employee contributions limits are as follows:

Employee Deferral Limit: $24,500

Age 50+ Catch-up: $8,000

New Age 60 – 63 Catch-up: $3,250

401K Age 60 – 63 Catch-up Contribution

Under the old rules, in 2025, a 401(k) plan participant age 60 – 63 would have been limited to the employee deferral limit of $24,500 plus the age 50+ catch-up of $8,000 for a total employee contribution of $32,500.

However, thanks to the passing of the Secure Act in 2022, an additional catch-up contribution will be introduced to employer-sponsored qualified retirement plans, only available to employees age 60 – 63. In 2026, the catch-up contribution is $8,000, and making the additional catch-up contribution for employees age 60 – 63 $3,750 ($8,000 x 50%). Thus, a plan participant age 60 – 63 would be able to contribute the regular employee deferral limit of $24,500, plus the normal age 50+ catch-up of $8,000, PLUS the new age 60 – 63 catch-up contribution of $3,250, for a total employee contribution of $35,750 in 2025.

Age 64 – Revert Back To Normal 401(k) Catch-up Limit

This is a very odd way to assess a special catch-up contribution because it is ONLY available to employees between the ages of 60 and 63. In the year the 401(k) plan participant obtains age 64, the new additional age 60 – 63 contribution is completely eliminated. Here is a quick list of the contribution limits for 2025 based on an employee’s age:

Under Age 50: $24,500

Age 50 – 59: $32,500

Age 60 – 63: $35,750

Age 64+: $32,500

The Year The Employee OBTAINS Age 60 – 63

The employee just has to OBTAIN age 60 – 63 during that year to be eligible for the enhanced catch-up contribution. The enhanced catch-up contribution is not pro-rated based on WHEN the employee turns age 60. For example, if an employee turns 60 on December 31st, they are eligible to make the full $3,250 additional catch-up contribution for the year.

By that same token, if the employee turns age 64 by December 31st, they are no longer allowed to make the new enhanced catch-up contribution for that year.

Optional Provision At The Plan Level

The new 60 – 63 enhanced catch-up contribution is an OPTIONAL provision for qualified retirement plans, meaning some employers may allow this new enhanced catch-up contribution while others may not. If no action is taken by the employer sponsoring the plan, be default, the new age 60 – 63 catch-up contributions starting in 2025 will be allowed.

If an employer prefers to opt out of allowing employees ages 60 – 63 from making this new enhanced catch-up contribution, they will need to contact their TPA firm (third-party administrator) as soon as possible to amend their plan to disallow this new type of employee contributions starting in 2025.

Contact Payroll Company

Since this a brand new 401(k) employee contribution starting in 2025, we strongly recommend that plan sponsors reach out to their payroll company to make sure they are aware that your plan will either ALLOW or NOT ALLOW this new age 60 – 63 catch-up contribution, so the payroll system doesn’t incorrectly cap employees age 60 – 63 from making the additional catch-up contribution.

Formula: 50% of Normal Catch-up Contribution

For future years, the formula for this age 60 – 63 enhanced catch-up contribution is 50% of the regular catch-up contribution limit. The IRS usually announces the updated 401(k) contribution limits in either October or November of each year for the following calendar year. For example, if the IRS announces that the new catch-up limit in 2026 is $8,000, the enhanced age 60 – 63 catch-up contribution would be $3,250 over the regular $8,000 catch-up limit.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What is the new 401(k) and 403(b) age 60–63 catch-up contribution for 2025?

Starting in 2025, employees aged 60–63 can contribute an extra “enhanced” catch-up contribution to their 401(k) or 403(b) plan. This new contribution equals 50% of the standard catch-up contribution for that year. For 2025, that means an additional $3,750 on top of the normal catch-up limit.

How much can employees aged 60–63 contribute to a 401(k) in 2025?

For 2025, employees aged 60–63 can contribute:

Regular employee deferral: $23,500

Standard age 50+ catch-up: $7,500

New age 60–63 catch-up: $3,750

Total: $34,750

What happens when an employee turns 64?

The new enhanced catch-up contribution is only available through age 63. In the year an employee turns 64, they revert back to the standard catch-up limit of $7,500, for a total maximum contribution of $31,000 in 2025.

Do employees need to be 60 for the full year to qualify?

No. The employee only needs to obtain age 60–63 during the tax year to be eligible. Even if they turn 60 on December 31, they qualify for the full additional $3,750 catch-up contribution for that year.

Is the new 60–63 catch-up contribution mandatory for employers?

No. The provision is optional. Employers must decide whether to allow the new enhanced catch-up contribution in their retirement plan. If an employer takes no action, the new contribution will automatically be allowed starting in 2025.

Should employers notify their payroll company?

Yes. Plan sponsors should confirm with their payroll provider whether their plan will allow the new 60–63 catch-up contributions. Payroll systems will need to be updated to ensure eligible employees can contribute correctly.

How will future enhanced catch-up amounts be calculated?

Each year, the enhanced age 60–63 catch-up limit will equal 50% of that year’s regular catch-up contribution. For example, if the standard catch-up limit rises to $8,000 in 2026, the new enhanced catch-up would be $4,000.

Last updated June, 2026