2026 Medicare IRMAA Brackets: What Triggers Higher Premiums and How to Avoid

Medicare IRMAA increases Part B and Part D premiums when your income exceeds specific thresholds based on your MAGI from two years prior. In 2026, managing income through strategies like Roth conversions, withdrawal timing, and tax planning can help reduce or avoid these surcharges. Even small income increases can trigger higher premiums, making proactive planning essential. Greenbush Financial Group helps retirees minimize IRMAA and control long-term healthcare costs.

Medicare IRMAA (Income-Related Monthly Adjustment Amount) is a surcharge added to Medicare Part B and Part D premiums when your income exceeds certain thresholds. These surcharges are based on your Modified Adjusted Gross Income (MAGI) from two years prior. At Greenbush Financial Group, our analysis shows that proactive tax and withdrawal planning can help retirees avoid or minimize IRMAA and significantly reduce long-term healthcare costs.

What Is Medicare IRMAA and How Does It Work?

IRMAA is an additional premium Medicare beneficiaries pay if their income exceeds specific limits.

Key Facts

Applies to Medicare Part B and Part D

Based on income from two years prior

Uses Modified Adjusted Gross Income (MAGI)

Adjusted annually for inflation

Example

Your 2026 Medicare premiums are based on your 2024 income.

This lag creates planning opportunities, especially in early retirement years.

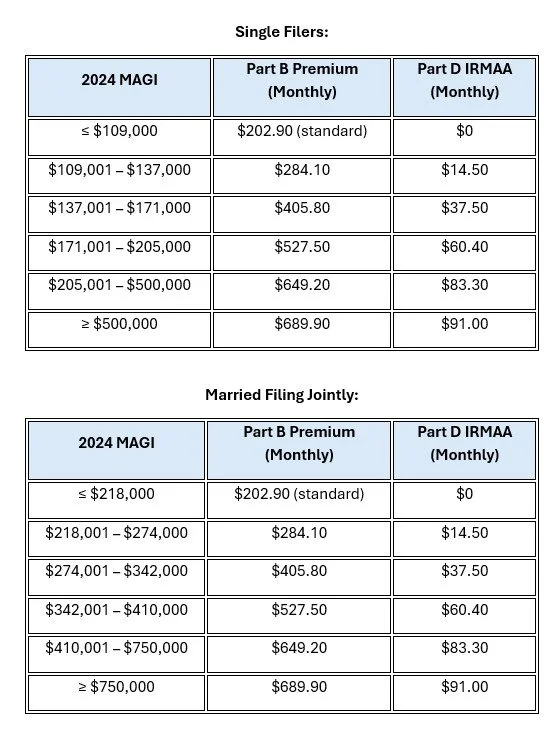

2026 IRMAA Income Limits and Surcharge Brackets

IRMAA is triggered when your income crosses certain thresholds.

2026 Estimated IRMAA Thresholds

At Greenbush Financial Group, we emphasize that even $1 over a threshold can trigger a significantly higher premium.

What Counts as Income for IRMAA (MAGI)?

IRMAA is based on Modified Adjusted Gross Income, which includes more than just wages.

Included Income Sources

IRA and 401(k) withdrawals

Capital gains from investments

Dividends and interest

Rental income

Social Security (partially taxable portion)

Roth conversions

Important Note

Tax-free municipal bond interest is also included in MAGI for IRMAA purposes.

How Much Are IRMAA Surcharges?

IRMAA increases both Part B and Part D premiums.

Example Impact

Standard Part B premium (baseline)

IRMAA can increase premiums by hundreds of dollars per month per person

Part D surcharges are smaller but still meaningful

Key Insight

Over a 10–20 year retirement, IRMAA can add up to tens of thousands of dollars in additional healthcare costs if not managed properly.

Planning Strategies to Reduce or Avoid IRMAA

Strategic income planning is the most effective way to manage IRMAA.

1. Manage Your Taxable Income Each Year

Stay below key IRMAA thresholds when possible

Avoid large one-time income spikes

2. Use Roth Conversions Strategically

Convert funds in lower-income years before Medicare

Reduce future taxable income and RMDs

3. Time Large Withdrawals Carefully

Spread income over multiple years

Avoid triggering IRMAA in a single year

4. Leverage Roth Accounts

Roth withdrawals do not increase MAGI

Provides tax-free income flexibility

5. Consider Capital Gains Timing

Harvest gains in lower-income years

Offset gains with losses when possible

At Greenbush Financial Group, we often build multi-year tax projections to help clients stay below IRMAA thresholds.

IRMAA Planning Before and After Retirement

Before Retirement (Ages 55–63)

Ideal window for Roth conversions

Lower income years create planning opportunities

Reduce future IRMAA exposure

Early Retirement (Before Medicare)

Control income levels carefully

Balance withdrawals across accounts

After Age 65

Monitor RMDs and income levels

Use Roth withdrawals to manage thresholds

Plan ahead for future income spikes

What Happens If Your Income Drops?

You may be able to appeal IRMAA if your income has decreased due to certain life events.

Qualifying Life-Changing Events

Retirement

Marriage or divorce

Death of a spouse

Loss of income-producing property

You can file an appeal with Social Security to request a lower premium.

Common IRMAA Mistakes to Avoid

Ignoring IRMAA when doing Roth conversions

Taking large IRA withdrawals in a single year

Not planning for RMDs

Overlooking capital gains impact

Assuming Medicare premiums are fixed

At Greenbush Financial Group, we often see that IRMAA surprises retirees who focus only on taxes without considering healthcare costs.

Final Thoughts

IRMAA is one of the most overlooked retirement expenses, yet it can significantly increase your Medicare costs. The key is not just minimizing taxes in a single year but managing income over time to avoid crossing key thresholds.

At Greenbush Financial Group, our analysis shows that proactive planning around withdrawals, Roth conversions, and income timing can help reduce IRMAA and improve overall retirement outcomes.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

Frequently Asked Questions

-

What does IRMAA stand for?Income-Related Monthly Adjustment Amount, a surcharge on Medicare premiums based on income.

-

What income is used to calculate IRMAA?Modified Adjusted Gross Income (MAGI) from two years prior.

-

Can Roth withdrawals trigger IRMAA?No, qualified Roth withdrawals do not increase MAGI.

-

Can IRMAA be appealed?Yes, if you have a qualifying life-changing event such as retirement or loss of income.

-

How can I avoid IRMAA surcharges?By managing taxable income, using Roth strategies, and avoiding large income spikes.

How to Maximize Social Security Benefits with Smart Claiming and Income Planning

Social Security is a cornerstone of retirement income—but when and how you claim can have a major impact on lifetime benefits. This article from Greenbush Financial Group explains 2025 thresholds, how benefits are calculated, and smart strategies for delaying, coordinating with taxes, and managing Medicare costs. Learn how to maximize your Social Security benefits and plan your income efficiently in retirement.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

For many retirees, Social Security is a cornerstone of their retirement income. But when and how you claim your benefits—and how you plan your income around them—can have a major impact on the total amount you receive over your lifetime. With updated Social Security thresholds, limits, and rules, there are new opportunities to optimize your claiming strategy and coordinate Social Security with your broader financial plan.

In this article, we’ll cover:

How Social Security benefits are calculated and funded

Four ways to increase your Social Security benefit amount

How income and taxes affect your benefits

The impact of Medicare premiums and income planning

How delaying Social Security can create opportunities for Roth conversions

What to know about the earned income penalty if you claim early

Answers to common Social Security claiming questions

Maximizing Social Security During the Working Years

The foundation for a strong Social Security benefit starts during your working years. Understanding how the system works helps you make informed decisions about your career, income, and retirement planning.

How Social Security Is Funded and Calculated

Social Security is primarily funded through payroll taxes under the Federal Insurance Contributions Act (FICA). In 2025, workers and employers each pay 6.2% of wages (for a total of 12.4%) up to the taxable wage base, which is $176,000 in 2025. Any earnings above that amount are not subject to Social Security tax and do not increase your benefit.

Your benefit is based on your highest 35 years of indexed earnings—meaning each year’s income is adjusted for inflation to reflect its value in today’s dollars. If you worked fewer than 35 years, zeros are included in the calculation, which can significantly reduce your average and therefore your monthly benefit.

Key takeaway: Once your annual income exceeds the taxable wage base, additional earnings don’t raise your future Social Security benefit. However, working longer can still increase your benefit if you replace lower-earning years or zeros in your 35-year average.

Four Ways to Increase Your Social Security Benefits

1. Fill in or Replace Zero Years

If you have fewer than 35 years of work history, each missing year is counted as zero. Even one extra year of income can replace a zero and raise your benefit.

Example: If you worked 32 years and earned $80,000 annually in your final three years, adding those years could significantly boost your benefit calculation.

2. Delay Claiming to Earn Higher Benefits

You can claim Social Security as early as age 62, but doing so permanently reduces your benefit—up to 30% less than your full retirement age (FRA) amount. For those born in 1960 or later, FRA is 67.

If you wait past FRA, your benefit grows by 8% per year up to age 70, plus annual cost-of-living adjustments (COLAs).

Example:

Claiming at 62: $1,400/month

Claiming at 67: $2,000/month

Claiming at 70: $2,480/month

That’s a $1,080 per month difference for waiting between the ages of 62 and 70.

3. Maximize Spousal and Dependent Benefits

Spousal and dependent benefits can be valuable for married couples or retirees with young children.

Spousal Benefit: A spouse can claim up to 50% of the higher earner’s FRA benefit, provided the higher earner has already filed.

Divorced Spouse Benefit: You may qualify if the marriage lasted 10 years or longer, and you haven’t remarried prior to age 60.

Dependent Benefit: Retirees age 62+ with children under 18 may receive additional benefits for dependents.

Planning tip: For individuals who plan to utilize the 50% spousal benefit and/or the dependent benefit, the path to the optimal filing strategy is more complex because the spouse and dependents cannot receive these benefits until that individual has actually turned on their social security benefit, which, in some cases, can favor not waiting until age 70 to file.

4. Understand Survivor Benefits

If one spouse passes away, the surviving spouse receives the higher of the two benefits. This makes it especially beneficial for the higher-earning spouse to delay claiming to age 70, maximizing the survivor benefit and providing long-term income protection.

How Social Security Benefits Are Taxed

Up to 85% of your Social Security benefits may be taxable, depending on your combined income (adjusted gross income + nontaxable interest + half of your Social Security benefits).

Single filers: Taxes begin at $25,000 of combined income

Married filing jointly: Taxes begin at $32,000 of combined income

If you don’t need Social Security to cover living expenses right away, delaying benefits can not only increase your future income but may also help manage taxes by controlling your income levels in early retirement.

Medicare Premiums and Income Planning

Once you reach age 65, you’ll typically enroll in Medicare Part B and D, and your premiums are based on your Modified Adjusted Gross Income (MAGI). Higher income means higher premiums under the Income-Related Monthly Adjustment Amount (IRMAA) rules.

Because Social Security benefits count as income for these purposes, timing your claiming strategy can help you manage Medicare costs.

Roth Conversions: Turning Delay into an Opportunity

Delaying Social Security creates a window for Roth conversions—moving money from a traditional IRA to a Roth IRA at potentially lower tax rates before Required Minimum Distributions (RMDs) begin at age 73 or 75.

Benefits of Roth conversions include:

Paying tax now at potentially lower rates

Reducing future RMDs

Potentially reduce future Medicare premiums

Creating a tax-free income source in retirement

Leaving tax-free assets to heirs

Coordinating your claiming strategy with Roth conversions can improve long-term tax efficiency and enhance your retirement flexibility.

Claiming Early? Know the Earned Income Penalty

If you claim Social Security before full retirement age and continue to work, your benefits may be temporarily reduced.

In 2025, the earnings limit is $23,400. For every $2 earned over the limit, $1 in benefits is withheld.

In the year you reach FRA, a higher limit applies: $62,160, and only $1 is withheld for every $3 earned above that.

Once you reach full retirement age, the penalty disappears, and your benefit is recalculated to credit any withheld amounts.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQ)

How are Social Security benefits calculated?

Social Security benefits are based on your highest 35 years of indexed earnings, adjusted for inflation. If you worked fewer than 35 years, zeros are included in your calculation, which can reduce your benefit.

What are the main ways to increase your Social Security benefits?

You can boost your benefit by replacing “zero” earning years, delaying your claim up to age 70 for an 8% annual increase past full retirement age, and coordinating spousal or survivor benefits strategically. Working longer and earning more during high-income years can also improve your benefit calculation.

How does delaying Social Security affect taxes and Medicare premiums?

Delaying benefits can help you manage taxable income in early retirement and avoid higher Medicare premiums triggered by the IRMAA income thresholds. This window can also allow for Roth conversions, which reduce future Required Minimum Distributions (RMDs) and create tax-free income in later years.

How are Social Security benefits taxed?

Up to 85% of your benefits may be taxable depending on your combined income (adjusted gross income + nontaxable interest + half of your benefits). Taxes begin at $25,000 for single filers and $32,000 for married couples filing jointly. Managing income sources can help minimize these taxes.

What is the earned income penalty for claiming Social Security early?

If you claim before full retirement age and continue working, benefits are reduced by $1 for every $2 earned above $23,400 in 2025. In the year you reach full retirement age, the limit increases to $62,160, and only $1 is withheld for every $3 earned over that amount. The penalty ends at full retirement age, when your benefit is recalculated.

What are spousal and survivor Social Security benefits?

A spouse can claim up to 50% of the higher earner’s full retirement benefit once that person has filed. If one spouse passes away, the survivor receives the higher of the two benefits. This makes it especially advantageous for the higher earner to delay claiming to age 70 to maximize long-term income protection.

How can Roth conversions complement Social Security planning?

Performing Roth conversions in the years before claiming Social Security or reaching RMD age allows retirees to shift pre-tax funds into tax-free accounts at potentially lower tax rates. This strategy can reduce future taxable income, manage Medicare premiums, and increase retirement flexibility.

Medicare Is Projected To Be Insolvent In 2028

The trustees of the Medicare program just released their 2022 annual report and it came with some really bad news. The Medicare Part A Hospital Insurance (HI) Trust is expected to be insolvent in 2028 which currently provides health benefits to over 63 million Americans. We have been kicking the can down the road for the past 40 years and we have finally run out of road.

The trustees of the Medicare program just released their 2022 annual report and it came with some really bad news. The Medicare Part A Hospital Insurance (HI) Trust is expected to be insolvent in 2028 which currently provides health benefits to over 63 million Americans. The U.S. has been kicking the can down the road for the past 40 years and we have finally run out of road. In this article I will be covering:

What benefits Medicare Part A provides that are at risk

The difference between the Medicare HI Trust & Medicare SMI Trust

If Medicare does become insolvent in 2028, what happens?

Changes that Congress could make to prevent insolvency

Actions that retirees can take to manage the risk of a Medicare insolvency

Medicare HI Trust vs. Medicare SMI Trust

The Medicare program provides health insurance benefits to U.S. citizens once they have reached age 65, or if they become disabled. Medicare is made up of a few parts: Part A, Part B, Part C, and Part D.

Part A covers services such as hospitalization, hospice care, skilled nursing facilities, and some home health service. Medicare is made up of two trusts, the Hospital Insurance (HI) Trust and the Supplemental Medical Insurance (SMI) Trust. The HI Trust supports the Medicare Part A benefits and that is the trust that is in jeopardy of becoming insolvent in 2028. This trust is funded primarily through the 2.9% payroll tax that is split between employees and employers.

Medicare Part B, C, and D cover the following:

Part B: Physician visits, outpatient services, and preventative services

Part C: Medicare Advantage Programs

Part D: Prescription drug coverage

Part B and Part D are funded through a combination of general tax revenues and premiums paid by U.S. citizens that are deducted from their social security benefits. Most of the funding though comes from the tax revenue portion, in 2021, about 73% of Part B and 74% of Part D were funded through income taxes (CNBC). Even though they are supported by the SMI Trust, it would be very difficult for these sections of Medicare to go insolvent because they can always raise the premiums charged to retirees, which they did in 2022 by 14%, or increase taxes.

Part C is Medicare Advantage plans which are partially supported by both the HI and SMI Trust, and depending on the plan selected, premiums from the policyholder.

What Happens If Medicare Part A Becomes Insolvent in 2028?

The trustees of the Medicare trusts issue a report every year providing the public the funding status of the HI and SMI trusts. Based on the 2022 report, if no changes are made, there would not be enough money in the HI trust that supports all of the Part A health benefits to U.S. citizen. The system does not completely implode but there would only be enough money in the trust to pay about 90% of the promised benefits starting in 2029.

This mean that Medicare would not have the funds needed to fully pay hospitals and skilled nursing facilities for the services covered by Medicare. It could force these hospital and healthcare providers to accept a lower reimbursement from the service provider or it could delay when the reimbursement payments are received. In response, hospitals may have to cut cost, layoff workers, stop providing certain services, and certain practices may choose not to accept patients with Medicare coverage, limiting access to certain doctors.

Possible Solutions To Avoid Medicare Insolvency

The natural question is: If this is expected to happen in 2028, shouldn’t they make changes now to prevent the insolvency from taking place 6 years from now?” The definitely should but Medicare is a political football. When you have a government program that is at risk of going insolvent, there are really only three solutions:

Raise taxes

Cut Benefits

Restructure the Medicare Program

As a politician, whatever weapon you choose to combat the issue, you are going to tick off a large portion of the voting population which is why there probably have been no changes even though the warning bells has been ringing for years. The reality is that the longer they wait to implement changes, the larger, and more painful those changes need to be.

Some relatively small changes could go a long way if they act now. It’s estimated that if Congress raises the payroll tax that funds the HI Trust from 2.9% to 3.6% that would bump out the insolvency date of the HI Trust by about 75 years. If you go to the spending side, it’s estimated that if Part A were to cut its annual expenses by about 15% per year starting in 2022, it would have a similar positive impact (Source: Senate RPC).

Another possible fix, they could restructure the Medicare system, and move some of the Part A services to Part B. But this is not a great solution because even though it helps the Part A Trust insolvency issue, it pushes more of the cost to Part B which is funded be general tax revenues and premiums charged to retirees.

A third solution, Medicare could more aggressively negotiate the reimbursement rates paid to healthcare providers but that would of course have the adverse effect of putting revenue pressure on the hospitals and potentially jeopardize the quality of care provided.

The fourth, and in my opinion, the most likely outcome, no changes will be made between now and 2028, we will be on the doorstep of insolvency, and then Congress will pass legislation for an emergency bailout out package for the Medicare Part A HI Trust. This may buy them more time but it doesn’t solve the problem, and it will add a sizable amount to debt to the U.S. deficit.

What Should Retirees Do To Prepare For This?

Even though the government may try to issue more debt to bailout the Medicare Part A trust, as a retiree, you have to ask yourself the question, what if by the time we reach 2028, the U.S. can’t finance the amount a debt needed to stave off the insolvency? The Medicare Part A HI Trust is not the only government program facing insolvency over the next 15 years. One of the PBGC trusts that provides pension payments to workers that were once covered by a bankrupt pension plan is expected to be insolvent within the next 10 years. Social Security is expected to be insolvent in 2035 (2022 Trustees Report).

The solution may be to build a large expense cushion within your annual retirement budget so if the cost for your healthcare increases substantially in future years, you will already have a plan to handle those large expenses. This may mean paying down debt, not taking on new debt, cutting back on expenses, taking on some part-time income to build a large nest egg, or some combination of these planning strategies.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What is the Medicare Part A Hospital Insurance (HI) Trust and why is it at risk?

The Medicare Part A HI Trust funds hospital-related services such as inpatient care, hospice, and skilled nursing facilities. It is primarily funded through payroll taxes, but rising healthcare costs and an aging population are depleting the trust faster than it’s being replenished, putting it on track for insolvency by 2028.

What’s the difference between the Medicare HI Trust and the SMI Trust?

The HI Trust supports Medicare Part A, which covers hospital and inpatient services, while the Supplemental Medical Insurance (SMI) Trust funds Part B (doctor visits and outpatient care) and Part D (prescription drug coverage). The SMI Trust is less vulnerable to insolvency because it is financed by general tax revenues and premiums that can be adjusted as needed.

What happens if the Medicare Part A trust becomes insolvent?

If no changes are made, the HI Trust will only have enough funds to pay about 90% of promised Part A benefits beginning in 2029. Hospitals and healthcare providers could face lower reimbursements or payment delays, which might reduce access to certain services for retirees.

What options does Congress have to prevent Medicare insolvency?

Lawmakers could raise payroll taxes, cut benefits, or restructure the program. For example, increasing the Medicare payroll tax rate from 2.9% to 3.6% could extend the HI Trust’s solvency by decades. Delaying reforms, however, would require more drastic and painful adjustments later.

Could Medicare be bailed out if insolvency occurs?

A short-term bailout is possible, as Congress could allocate emergency funding to keep the HI Trust solvent temporarily. However, this would increase the national debt and delay rather than solve the underlying structural funding problem.

How can retirees prepare for potential Medicare funding issues?

Retirees can build financial resilience by paying down debt, reducing expenses, and saving more to cover potential increases in out-of-pocket healthcare costs. Establishing an emergency savings buffer or maintaining part-time income may also help offset rising healthcare expenses if Medicare benefits are reduced.