When One Social Security Check Disappears: What Retired Couples Need to Plan For

Many couples plan carefully for retirement together but overlook the financial realities of retirement alone. Learn how survivor Social Security benefits, taxes, healthcare costs, and estate planning can impact a surviving spouse.

Many married couples plan carefully for retirement together but spend very little time preparing for the financial realities of retirement alone. When one spouse dies, income may drop faster than expenses, taxes can increase, and important financial decisions suddenly fall on one person. Understanding survivor Social Security rules, tax changes, healthcare costs, and estate planning issues can help protect the surviving spouse financially and emotionally. At Greenbush Financial Group, we often find that the best survivor planning happens before a crisis occurs.

Most Couples Plan for Retirement Together—But Not for Retirement Alone

Many retired couples assume that if one spouse dies, household expenses simply get cut in half.

In reality, that rarely happens.

When one spouse passes away:

One Social Security check may disappear

Taxes may increase

Healthcare costs may remain high

Housing costs often stay similar

One person may suddenly manage all financial decisions alone

At the same time, the surviving spouse may also be dealing with grief, paperwork, legal decisions, and emotional stress.

This is why survivor planning is one of the most important and overlooked parts of retirement planning.

The goal is not to think pessimistically.

The goal is making sure either spouse could continue forward financially with clarity and confidence.

What Financially Changes When One Spouse Dies?

Several important financial changes can happen almost immediately after a spouse passes away.

Social Security Income Often Drops

This is one of the biggest surprises for many couples.

When both spouses are receiving Social Security, one benefit usually disappears after the first death.

The surviving spouse generally keeps:

Their own benefit

Or the higher of the two benefits

But not both full checks.

Example

John receives:

$3,200/month from Social Security

Susan receives:

$2,100/month

Combined household income:

$5,300/month

After John dies, Susan may keep the larger $3,200 benefit, but the smaller benefit disappears.

Household Social Security income drops by:

$2,100/month

Or more than $25,000 annually

Meanwhile, many expenses continue.

Expenses Often Do NOT Drop by 50%

This is one of the most important retirement realities couples should understand.

Certain expenses may decrease modestly:

Food

Travel

Clothing

Some healthcare expenses

But many major costs remain similar:

Property taxes

Utilities

Insurance

Home maintenance

Car expenses

Healthcare premiums

In many cases, household expenses may only decline by 20%–30% while income drops significantly more.

That gap can create financial pressure for surviving spouses.

Why Surviving Spouses Often Pay Higher Taxes

This surprises many retirees.

After one spouse dies, the surviving spouse usually transitions from:

Married Filing Jointly

to:Single tax filing status

That change can happen quickly.

The problem is that single tax brackets are less favorable at lower income levels.

This means surviving spouses may pay higher taxes even if household income decreases.

The Survivor Tax Trap

A surviving spouse may face:

Similar IRA balances

Similar investment income

Similar Required Minimum Distributions (RMDs)

But now with:

Less favorable tax brackets

One standard deduction instead of two

Potentially higher Medicare premiums

Example

A married couple may comfortably remain in the 22% bracket while filing jointly.

After one spouse dies, the survivor could move into higher effective tax exposure as a single filer with nearly the same retirement account balances.

This is one reason Roth conversion planning during joint lifetimes can become extremely valuable.

Why Roth Conversions Can Matter More Than Couples Realize

Many couples focus only on their current taxes.

But survivor planning often changes the equation.

Converting portions of traditional IRAs to Roth IRAs while both spouses are alive may help:

Reduce future RMDs

Lower future survivor tax exposure

Create tax-free withdrawal flexibility

Improve long-term tax diversification

Example

A retired couple in their mid-60s delays Social Security and intentionally converts moderate IRA amounts annually while remaining within a manageable tax bracket.

Years later, if one spouse dies, the surviving spouse may have:

Smaller RMDs

More Roth flexibility

Lower taxable income

Better control over Medicare premium exposure

The key is evaluating these opportunities before tax brackets potentially tighten later.

Pension Survivor Decisions Matter More Than Many Couples Realize

Some pensions offer choices such as:

Single-life payout

Joint-and-survivor payout

Reduced survivor benefits

Many retirees choose larger monthly income initially without fully understanding how survivor income changes later.

Important Question

If one spouse dies:

Will pension income continue?

Reduce?

Or disappear entirely?

These decisions are often permanent once retirement begins.

Healthcare and Long-Term Care Planning Become More Important

Healthcare planning can become more difficult for surviving spouses because:

One spouse may eventually need care alone

Adult children may live far away

Financial management responsibilities may suddenly shift

Couples should discuss:

Long-term care preferences

Healthcare directives

Emergency contacts

Account access

Caregiving expectations

These conversations are uncomfortable for many families, but avoiding them often creates more stress later.

One of the Biggest Risks: Only One Spouse Understands the Finances

In many households, one spouse handles:

Investments

Taxes

Bills

Insurance

Account logins

Estate planning

That may work fine until something unexpected happens.

Then the surviving spouse may suddenly feel overwhelmed managing decisions they were never involved in previously.

Important Step

Both spouses should understand:

Where accounts are located

How income is generated

Who to contact for help

How bills are paid

What the retirement income plan looks like

Financial organization itself can become a form of protection.

Beneficiary Mistakes Can Create Major Problems

Many retirement accounts pass through beneficiary designations rather than wills.

Outdated beneficiaries can create unintended outcomes.

Common issues include:

Ex-spouses still listed

Missing contingent beneficiaries

Unequal inheritance structures

Children added improperly to accounts

Retirement transitions are a good time to review:

IRA beneficiaries

Roth IRA beneficiaries

Life insurance

Transfer-on-death accounts

Trust coordination

A Real-World Survivor Planning Example

David and Karen retire at age 66.

They have:

$1.5 million invested

Two Social Security benefits totaling $5,800/month

Moderate IRA balances

A paid-off home

Initially, they focus mostly on investment growth and travel spending.

But after reviewing survivor planning, they realize several risks:

One Social Security check would disappear

Karen would likely face higher taxes as a single filer

Future RMDs could become problematic

Karen was unfamiliar with many financial accounts

They decide to:

Complete partial Roth conversions annually

Organize account records and passwords

Review estate documents

Stress-test survivor income needs

Ensure both spouses understand the retirement plan

None of these changes were dramatic.

But together, they significantly improved financial clarity and flexibility for the surviving spouse.

Questions Every Retired Couple Should Ask

If one spouse died tomorrow:

Would the surviving spouse know where everything is?

Would income still cover expenses?

Which Social Security benefit would remain?

Would taxes increase?

Would healthcare costs still be manageable?

Are beneficiaries updated?

Are estate documents current?

Does each spouse understand the financial plan?

These are difficult questions.

But they are often easier to address proactively than during a crisis.

Common Survivor Planning Mistakes

1. Ignoring Survivor Income Changes

Many couples underestimate how much income could disappear after the first death.

2. Delaying Estate Organization

Missing documents and unclear account structures create unnecessary stress.

3. Claiming Social Security Without Survivor Planning

Social Security timing decisions can significantly affect long-term survivor income.

4. Ignoring Future Survivor Tax Rates

Surviving spouses often face higher taxes with less favorable filing brackets.

5. Letting One Spouse Handle Everything Alone

Retirement planning works best when both spouses understand the overall strategy.

What Good Survivor Planning Really Looks Like

Good survivor planning is not about predicting the future perfectly.

It is about creating flexibility and reducing unnecessary uncertainty.

That may include:

Reviewing Social Security timing

Evaluating Roth conversions

Stress-testing survivor income

Organizing estate documents

Updating beneficiaries

Maintaining adequate liquidity

Ensuring both spouses understand the plan

The goal is not fear.

The goal is preparedness.

Final Thoughts

Most married couples spend years planning for retirement together.

Far fewer spend time planning for the financial realities one spouse may eventually face alone.

At Greenbush Financial Group, we often find that the strongest retirement plans are not just designed for ideal scenarios. They are also built to protect the surviving spouse from unnecessary financial stress, tax surprises, and confusion during difficult transitions.

These conversations are not always easy.

But they are some of the most valuable retirement planning discussions couples can have.

Good retirement planning is not just about helping both spouses retire comfortably.

It is about helping either spouse continue confidently if life changes unexpectedly.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

FAQ

-

What happens to Social Security when one spouse dies?The surviving spouse generally keeps the larger of the two Social Security benefits, while the smaller benefit stops.

-

Do taxes increase for surviving spouses?Often, yes. Surviving spouses usually transition from married filing jointly to single filing status, which can create higher tax exposure at lower income levels.

-

Do household expenses get cut in half after one spouse dies?Usually not. Many fixed expenses remain similar even though household income may decline significantly.

-

Why are Roth conversions important for married retirees?Roth conversions during joint lifetimes may help reduce future taxes, lower survivor RMDs, and improve tax flexibility for the surviving spouse.

-

Should both spouses understand the retirement plan?Absolutely. Both spouses should know where accounts are held, how income is generated, and who to contact for financial guidance.

-

What estate planning documents should retirees review?Retirees should review wills, trusts, powers of attorney, healthcare directives, and beneficiary designations regularly.

-

Can Medicare premiums increase for surviving spouses?Yes. Higher taxable income combined with single filing status may increase Medicare IRMAA exposure.

-

What is the biggest survivor planning mistake couples make?One of the biggest mistakes is assuming the surviving spouse will automatically be financially secure without reviewing income reductions, taxes, and account organization ahead of time.

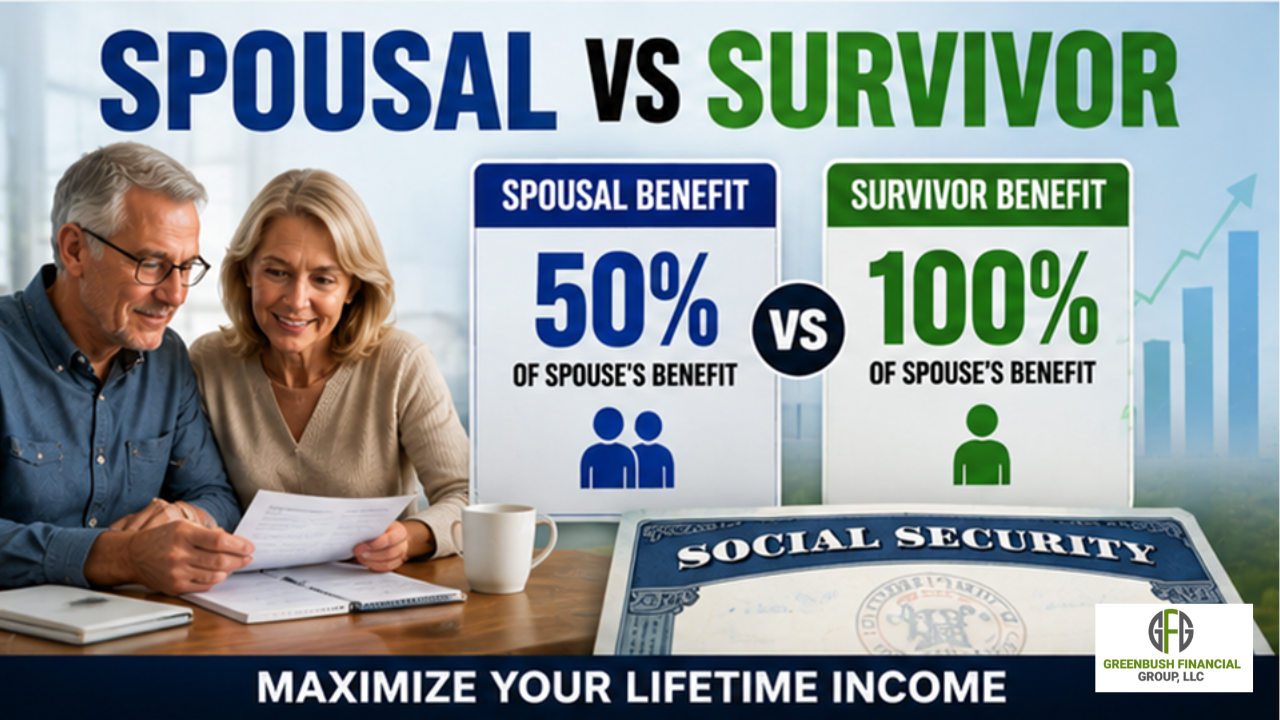

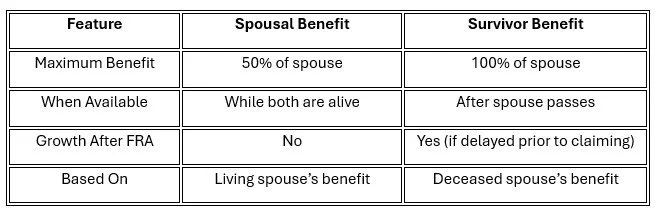

2026 Spousal vs Survivor Benefits Explained: How Social Security Works for Couples

Social Security spousal and survivor benefits can significantly impact retirement income for married couples. Learn the key rules, claiming strategies, and common mistakes that can affect lifetime benefits and financial security.

Social Security spousal and survivor benefits are critical components of retirement planning for married couples. A spouse may be eligible to receive up to 50% of their partner’s benefit while both are alive, and up to 100% of the higher benefit after a spouse passes away. At Greenbush Financial Group, our analysis shows that understanding how these benefits work can significantly impact lifetime income and financial security.

What Are Social Security Spousal Benefits?

Spousal benefits allow one spouse to receive a portion of the other spouse’s Social Security benefit.

Key Rules

Spousal benefit is up to 50% of the higher earner’s benefit

Must wait until the primary earner files for benefits

Available to current spouses and some divorced spouses

Example

Higher earner benefit = $2,000/month

Spousal benefit = up to $1,000/month

Important Note

You do not receive both your own benefit and the spousal benefit. Social Security pays the higher of the two amounts.

At Greenbush Financial Group, we often see this misunderstood, leading to unrealistic income expectations.

When Can You Claim Spousal Benefits?

Timing affects how much you receive.

Claiming Ages

Age 62 → Reduced spousal benefit

Full Retirement Age (67) → Full 50% benefit

No additional increase beyond FRA for spousal benefits

Key Insight

Unlike your own benefit, spousal benefits do not grow after full retirement age.

What Are Social Security Survivor Benefits?

Survivor benefits apply when one spouse passes away.

Key Rules

Surviving spouse can receive up to 100% of the higher benefit

Can switch from their own benefit to survivor benefit if advantageous

Available as early as age 60 (reduced), or full benefit at FRA

Example

Spouse A benefit = $2,500

Spouse B benefit = $1,500

After Spouse A passes, Spouse B receives $2,500

At Greenbush Financial Group, survivor planning is one of the most important considerations for long-term income security.

Spousal vs Survivor Benefits: Key Differences

How Timing Impacts Couples’ Benefits

The timing of when each spouse claims benefits can significantly affect total lifetime income.

Key Strategy

Higher earner delays benefits to increase survivor income

Lower earner may claim earlier depending on income needs

Why This Matters

Delaying benefits for the higher earner increases:

Monthly retirement income

Survivor benefit for the remaining spouse

At Greenbush Financial Group, we often prioritize maximizing the higher earner’s benefit for long-term protection.

Divorced Spouse Benefits

Even divorced individuals may qualify for spousal or survivor benefits.

Requirements

Marriage lasted at least 10 years

Individual is currently unmarried

Ex-spouse is eligible for benefits

Key Insight

Claiming on an ex-spouse’s record does not reduce their benefit.

Common Mistakes to Avoid

Claiming too early without considering survivor impact

Assuming both spouses receive full benefits simultaneously

Ignoring the importance of the higher earner delaying benefits

Not coordinating claiming strategies as a couple

Overlooking divorced spouse eligibility

A Real-World Planning Example

Scenario

Husband benefit: $2,800

Wife benefit: $1,200

Strategy

Husband delays until age 70

Wife claims earlier or at FRA

Outcome

Higher household income later

Increased survivor benefit for wife

This type of coordinated strategy can significantly improve long-term outcomes.

How Taxes Impact Spousal and Survivor Benefits

Social Security benefits may be taxable depending on total income.

Key Considerations

Up to 85% of benefits can be taxable

IRA withdrawals can increase taxation

Survivor filing status may increase tax burden

Planning Insight

A surviving spouse often files as single, which can lead to higher taxes on the same income.

At Greenbush Financial Group, tax planning is often integrated with Social Security decisions.

Final Thoughts

Social Security spousal and survivor benefits are not just supplemental income, they are a core part of retirement planning for couples. The decisions around timing and coordination can have a lasting impact on both partners.

At Greenbush Financial Group, our analysis shows that couples who plan their Social Security strategy together tend to maximize lifetime income and provide better financial security for the surviving spouse.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

Frequently Asked Questions

-

How much is a spousal Social Security benefit?

Up to 50% of the higher earner's benefit at full retirement age. -

Do spousal benefits increase after age 67?

No, they do not increase beyond full retirement age. -

What happens to Social Security when a spouse dies?

The surviving spouse can receive up to 100% of the higher benefit. -

Can a divorced spouse claim Social Security benefits?

Yes, if the marriage lasted at least 10 years and other requirements are met. -

Can I receive both my benefit and my spouse's benefit?

No, you receive the higher of the two, not both.

Claiming Social Security Early or Late: Which Age Is Right for You?

Deciding when to claim Social Security can impact your lifetime income. Learn how ages 62, 67, and 70 affect benefits and how to maximize retirement income with strategic timing.

Deciding when to claim Social Security is one of the most important retirement decisions because it directly impacts your lifetime income. Claiming early at 62 reduces your benefit, waiting until full retirement age (67) provides your standard benefit, and delaying to age 70 increases your benefit significantly. At Greenbush Financial Group, our analysis shows that the right decision depends on your life expectancy, income needs, tax strategy, and overall retirement plan.

How Social Security Benefits Change by Age

Your benefit amount is based on your Full Retirement Age (FRA), which is typically 67 for those born in 1960 or later.

Benefit Adjustments by Claiming Age

Age 62 → ~30% reduction

Age 67 → 100% of your benefit

Age 70 → ~24% increase from FRA

Example

If your FRA benefit is $2,000 per month:

At Greenbush Financial Group, we emphasize that this is a permanent decision that affects income for life.

Why This Decision Matters So Much

Social Security is one of the only income sources in retirement that is:

Guaranteed for life

Adjusted for inflation

Not impacted by market performance

This makes it a critical foundation for retirement income planning.

When It May Make Sense to Claim at Age 62

Claiming early provides income sooner, but at a reduced level.

Situations Where Age 62 May Make Sense

You need income to retire

Health concerns or shorter life expectancy

You want to preserve investment assets

You are concerned about future policy changes

Trade-Off

Lower monthly income for life.

At Greenbush Financial Group, we typically see this strategy used when income needs outweigh long-term maximization.

When Claiming at Full Retirement Age (67) Makes Sense

Full Retirement Age provides your standard benefit without reductions or credits.

Situations Where Age 67 May Make Sense

You want a balanced approach

You are still working into your mid-to-late 60s

You want to avoid early reduction penalties

You are unsure about delaying further

Key Advantage

No reduction, no delay risk.

When It Makes Sense to Delay Until Age 70

Delaying increases your benefit through delayed retirement credits.

Benefits of Waiting

Higher guaranteed monthly income

Better inflation-adjusted income over time

Increased survivor benefits for a spouse

Situations Where Age 70 May Make Sense

You have longevity in your family

You do not need income immediately

You want to maximize lifetime income

You are concerned about outliving your money

You have significant Tax Deferred Assets to drawdown

At Greenbush Financial Group, delaying to 70 is often one of the most effective ways to increase guaranteed retirement income.

The Break-Even Analysis: When Do You Come Out Ahead?

A common way to evaluate this decision is through a break-even analysis.

General Insight

Break-even age is often around 78–82

If you live beyond this range, delaying may result in higher lifetime income

Important Note

This analysis does not account for:

Taxes

Investment returns

Spousal benefits

Personal spending needs

How Taxes Impact Your Social Security Decision

Your Social Security benefits may be taxable depending on your income.

Key Considerations

Up to 85% of benefits can be taxable

IRA withdrawals can increase taxation

Claiming earlier may reduce taxable income in some scenarios

Planning Strategy

Coordinate Social Security with retirement withdrawals to manage your tax bracket effectively.

Spousal and Survivor Benefit Considerations

Married couples should evaluate this decision together.

Key Rules

Spouse can receive up to 50% of the higher earner’s benefit

Survivor receives the higher of the two benefits

Planning Insight

Delaying benefits for the higher earner can increase survivor income significantly.

At Greenbush Financial Group, spousal coordination is often one of the most impactful strategies.

A Simple Decision Framework

Instead of looking for a one-size-fits-all answer, consider these key questions:

Ask Yourself

Do I need the income now?

What is my health and life expectancy?

Do I have other income sources?

What is my tax situation?

Am I planning for a spouse or survivor benefit?

Common Mistakes to Avoid

Claiming early without a plan

Ignoring spousal benefits

Focusing only on break-even analysis

Not considering taxes

Making the decision in isolation from your full retirement plan

Final Thoughts

There is no universally “correct” age to claim Social Security. The best decision depends on your financial situation, health, and long-term goals.

At Greenbush Financial Group, our analysis shows that integrating Social Security into a broader retirement income and tax strategy leads to better outcomes than focusing on the decision in isolation.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

-

Is it better to take Social Security at 62 or 70?It depends on your health, income needs, and life expectancy. Delaying increases lifetime income if you live long enough.

-

How much more do you get by waiting until 70?About 8% per year after full retirement age, up to age 70.

-

What is the break-even age for Social Security?Typically around age 78 to 82.

-

Can I work while collecting Social Security at 62?Yes, but your benefits may be reduced if you exceed income limits before full retirement age.

-

What happens if I delay Social Security past 70?There is no additional benefit increase after age 70.

Understanding the Social Security 50% Spousal Benefit

The Social Security 50% spousal benefit allows married or divorced individuals to receive up to half of their spouse’s full retirement age benefit. This guide explains eligibility rules, timing strategies, and why delaying benefits may not always maximize household income. Learn how filing decisions affect both spouses and how to coordinate benefits for optimal retirement income. Understanding these rules is essential for building an efficient Social Security strategy.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

When married couples are deciding when to file for Social Security, there are several strategies to consider. One of the most important — and often misunderstood — is the 50% spousal benefit. This rule can have a major impact on when each spouse should file and how to maximize total household Social Security income over retirement.

In this article, we’ll walk through:

What the 50% spousal benefit is

Special filing rules to qualify

Why “file and suspend” is no longer allowed

Why delaying to age 70 may not always make sense

Special rules for divorced spouses

Other factors to consider when choosing a filing strategy

What Is the 50% Spousal Benefit?

When you are married and eligible for Social Security, you have the option to receive:

100% of your own Social Security benefit, or

50% of your spouse’s benefit, whichever is higher.

You do not get both — Social Security will essentially give you the higher of the two amounts.

Example

Let’s look at an example:

Paul’s Full Retirement Age (FRA) benefit: $3,600 per month

Sharon’s FRA benefit: $800 per month

When Sharon files at her full retirement age (67), she can choose:

Her own benefit: $800/month

50% of Paul’s benefit: $1,800/month

Since $1,800 is higher than $800, she would elect the 50% spousal benefit.

This filing strategy is extremely important in situations where one spouse earned significantly more than the other.

Special Filing Rules

One of the most important rules for the 50% spousal benefit is this:

The higher-earning spouse must be receiving their Social Security benefit in order for the lower-earning spouse to claim the 50% spousal benefit.

Using Paul and Sharon again:

Both are age 67

Paul’s FRA benefit = $3,600

Sharon’s FRA benefit = $800

If Paul decides to delay his Social Security until age 70, Sharon cannot collect the spousal benefit until Paul actually turns his benefit on.

So Sharon would:

Take her own benefit of $800 at 67

Elect the 50% spousal benefit when Paul turn on at age 70 increasing to $1,800

This rule alone often drives a lot of the Social Security filing decision for married couples.

File and Suspend Is No Longer Allowed

Years ago, there was a strategy called “file and suspend.”

This allowed the higher-earning spouse to:

File for Social Security

Immediately suspend their benefit

Allow their benefit to continue growing until age 70

Meanwhile, the lower-earning spouse could collect the 50% spousal benefit

This strategy was very powerful, but the Social Security Administration eliminated the file and suspend strategy. Now, the higher-earning spouse must actually be receiving benefits for the spouse to receive the spousal benefit.

Delaying Until Age 70 May Not Always Make Sense

Many people know that if you delay Social Security past full retirement age, your benefit increases by approximately 8% per year until age 70.

From an individual standpoint, delaying can make a lot of sense. However, for married couples, the spousal benefit changes the math.

Here’s the key rule:

The 50% spousal benefit is based on 50% of the higher earner’s Full Retirement Age benefit, not their age 70 benefit.

Example

Let’s go back to Paul and Sharon:

Paul’s FRA benefit: $3,600/month

Paul’s age 70 benefit: about $4,500/month

Sharon’s own benefit: $800/month

Sharon’s spousal benefit: $1,800/month (50% of $3,600)

If Paul delays until age 70:

Sharon cannot collect the spousal benefit for 3 years

Her spousal benefit does not increase — it stays at $1,800

So the couple must evaluate:

Is the increase in Paul’s benefit worth Sharon not receiving the addition $1,000/month for three years? ($1,800 spousal benefit less Sharon’s $800 FRA benefit)

In situations where the spousal benefit is a large increase for the lower-earning spouse, it may make sense for the higher earner to file earlier, even if that means giving up the delayed credits.

However, if the spousal benefit is only slightly higher than the lower earner’s own benefit, delaying may still make sense.

This is why Social Security filing decisions should always be looked at from a household strategy, not just an individual strategy.

Divorced Couples: Special Consideration

Many people don’t realize that divorced spouses may still be eligible for the spousal benefit.

You may qualify for a 50% spousal benefit on an ex-spouse’s record if:

The marriage lasted at least 10 years

You are currently unmarried

Your own Social Security benefit is less than 50% of your ex-spouse’s benefit

Your ex-spouse is eligible for Social Security (they do not have to be collecting yet if divorced more than 2 years)

Even if your ex-spouse has remarried, you may still be eligible for the spousal benefit based on their record.

Importantly:

Your ex-spouse collecting a spousal benefit does NOT reduce their benefit and does not impact their current spouse.

Other Factors to Consider When Filing for Social Security

The 50% spousal benefit is just one piece of the Social Security planning puzzle. When building a filing strategy, we also consider:

Survivor benefits

Life expectancy of both spouses

Taxation of Social Security

Other retirement income sources

Roth conversion strategy

Required Minimum Distributions (RMDs)

The difference between each spouse’s benefit

The survivor benefit is especially important — when one spouse passes away, the surviving spouse keeps the higher of the two Social Security benefits, which is another reason why delaying the higher earner’s benefit can sometimes make sense.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions About the Social Security 50% Spousal Benefit

- What is the Social Security spousal benefit?The spousal benefit allows a married spouse to receive up to 50% of their spouse's full retirement age Social Security benefit if that amount is higher than their own benefit.

- Do I get my own benefit plus 50% of my spouse's benefit?No. You receive either your own benefit or the spousal benefit - whichever is higher - but not both.

- When can I claim the spousal benefit?You can claim the spousal benefit as early as age 62, but the benefit will be reduced if taken before your full retirement age.

- Does my spouse have to file before I can receive the spousal benefit?Yes. The higher-earning spouse must be actively receiving Social Security benefits before the lower-earning spouse can claim the 50% spousal benefit.

- Is the spousal benefit based on my spouse's age 70 benefit?No. The spousal benefit is based on 50% of your spouse's full retirement age benefit, not their age 70 benefit.

- If my spouse delays until age 70, does my spousal benefit increase?No. Your spousal benefit does not increase if your spouse delays past full retirement age. However, you must wait until they file to receive it.

- Can a divorced spouse collect a spousal benefit?Yes, if the marriage lasted at least 10 years and the individual is currently unmarried, they may be eligible for a spousal benefit based on their ex-spouse's record.

- Does my ex-spouse need to be collecting for me to claim a spousal benefit?If you have been divorced for more than two years, you may be able to claim a spousal benefit even if your ex-spouse has not filed yet, as long as they are eligible.

- What happens to the spousal benefit if my spouse passes away?The spousal benefit is replaced by a survivor benefit, which allows the surviving spouse to receive up to 100% of the deceased spouse's benefit.

- How do we know when we should file for Social Security?The optimal time to file depends on several factors including life expectancy, income needs, taxes, and the difference between each spouse's benefit. This decision should be evaluated as part of a full retirement income plan.

4 Reasons Why You Would Not Delay Social Security Benefits to Age 70

The Social Security 50% spousal benefit allows married or divorced individuals to receive up to half of their spouse’s full retirement age benefit. This guide explains eligibility rules, timing strategies, and why delaying benefits may not always maximize household income. Learn how filing decisions affect both spouses and how to coordinate benefits for optimal retirement income. Understanding these rules is essential for building an efficient Social Security strategy.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Many people have heard that the optimal strategy is to delay Social Security benefits until age 70 so that you receive the maximum possible benefit. While that can be true in some situations, there are many scenarios where filing before age 70 may actually make more sense from a financial planning standpoint.

In this article, we’re going to walk through five reasons why you may not want to delay Social Security benefits to age 70, and why the decision should be based on your personal financial situation, health, and retirement goals.

1. Health Concerns and Life Expectancy

The decision to file early or delay Social Security is largely based on longevity. If there are health concerns or a shorter life expectancy, it may make more sense to file earlier rather than later.

While Social Security benefits increase over time, if you delay too long and pass away earlier than expected, you may never make up the years of missed payments.

Example

Let’s say someone is entitled to receive:

$3,000 per month at age 67

If they file at age 62, their benefit is reduced by about 30% to $2,100 per month

By filing at age 62 instead of 67, they would receive:

$2,100 × 12 = $25,200 per year

Over 5 years = $126,000 received before age 67

The question becomes: how long do you have to live for waiting to pay off?

The break-even point is typically somewhere between age 80 and 82.

If you live past 82, delaying often results in more lifetime income

If you pass away before 82, taking benefits earlier often results in more total dollars received

So when there are health concerns or reduced life expectancy, filing earlier can make financial sense.

2. The 50% Spousal Benefit

For married couples, the 50% spousal benefit can significantly impact when the higher-earning spouse should file.

Remember:

The lower-earning spouse can receive their own benefit or 50% of their spouse’s benefit, whichever is higher.

However, the lower-earning spouse cannot receive the spousal benefit until the higher-earning spouse files.

Example

Ken and Tracy:

Ken’s Full Retirement Age benefit: $3,000/month

Tracy’s FRA benefit: $1,000/month

Tracy’s 50% spousal benefit: $1,500/month

If Ken files at 67:

Ken receives $3,000

Tracy receives $1,500

Total household benefit = $4,500/month

If Ken delays until 70:

Tracy can only collect her own $1,000 until Ken files

She must wait 3 years before increasing to $1,500

The spousal benefit does not increase based on Ken waiting until 70

So when there is a large gap between the lower-earning spouse’s benefit and the spousal benefit, it can often make sense for the higher-earning spouse to file before age 70 to unlock the spousal benefit earlier.

3. You Need the Income to Retire

Sometimes the decision is simple: you need the income to retire.

Many individuals plan to retire at 62, 65, or 67, and Social Security is a key part of their retirement income plan along with pensions, investments, or other income sources.

If delaying Social Security to age 70 means:

You have to continue working longer than you want, or

You have to withdraw heavily from retirement accounts early,

Then filing earlier may be the better decision because it allows you to retire when you want while maintaining your lifestyle.

In other words, Social Security is not always about maximizing the monthly benefit — sometimes it’s about making retirement possible.

4. Delaying Withdrawals from Investment Accounts

Another reason someone may file earlier is to preserve their investment accounts.

Here’s the math:

Social Security increases about 6% per year before full retirement age

Social Security increases about 8% per year from full retirement age to age 70

If someone has investment accounts that are earning more than 6–8% per year, it may make sense to:

Turn on Social Security earlier

Use Social Security income

Allow investment accounts to continue growing

However, this is not a perfect apples-to-apples comparison because:

Social Security increases are guaranteed

Investment returns are not guaranteed and require market risk

But in strong market environments or for aggressive investors, this strategy can sometimes make sense.

Summary

While delaying Social Security until age 70 can increase your monthly benefit, it is not always the best financial decision. The right decision depends on:

Health and life expectancy

Spousal benefits

Retirement income needs

Investment returns

Estate planning goals

Social Security decisions should be made as part of a full retirement income plan, not in isolation.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions

-

Is age 70 always the best age to take Social Security?No. Age 70 provides the highest monthly benefit, but not always the highest lifetime benefit.

-

What is the Social Security break-even age?Typically between age 80 and 82.

-

When should I take Social Security if I have health issues?Filing earlier may make sense if life expectancy is shorter.

-

How does the spousal benefit affect when we should file?The higher-earning spouse filing earlier may allow the lower-earning spouse to collect a larger spousal benefit sooner.

-

Does Social Security increase every year I wait?Yes, roughly 6% per year before full retirement age and 8% per year after full retirement age until age 70.

-

Should I take Social Security early to preserve my investments?In some cases, yes - especially if your investments are growing faster than the Social Security increase.

-

What happens to my Social Security when I die?Your spouse may be eligible for a survivor benefit equal to your benefit.

-

Can I work and still collect Social Security?Yes, but if you collect before full retirement age, there may be an earnings limit.

-

Is Social Security taxable?Yes, depending on your total income, up to 85% of your Social Security may be taxable at the Federal level.

-

Should I talk to a financial advisor before filing for Social Security?Yes. The timing decision can impact hundreds of thousands of dollars over your lifetime.

How to Maximize Social Security Benefits with Smart Claiming and Income Planning

Social Security is a cornerstone of retirement income—but when and how you claim can have a major impact on lifetime benefits. This article from Greenbush Financial Group explains 2025 thresholds, how benefits are calculated, and smart strategies for delaying, coordinating with taxes, and managing Medicare costs. Learn how to maximize your Social Security benefits and plan your income efficiently in retirement.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

For many retirees, Social Security is a cornerstone of their retirement income. But when and how you claim your benefits—and how you plan your income around them—can have a major impact on the total amount you receive over your lifetime. With updated Social Security thresholds, limits, and rules, there are new opportunities to optimize your claiming strategy and coordinate Social Security with your broader financial plan.

In this article, we’ll cover:

How Social Security benefits are calculated and funded

Four ways to increase your Social Security benefit amount

How income and taxes affect your benefits

The impact of Medicare premiums and income planning

How delaying Social Security can create opportunities for Roth conversions

What to know about the earned income penalty if you claim early

Answers to common Social Security claiming questions

Maximizing Social Security During the Working Years

The foundation for a strong Social Security benefit starts during your working years. Understanding how the system works helps you make informed decisions about your career, income, and retirement planning.

How Social Security Is Funded and Calculated

Social Security is primarily funded through payroll taxes under the Federal Insurance Contributions Act (FICA). In 2025, workers and employers each pay 6.2% of wages (for a total of 12.4%) up to the taxable wage base, which is $176,000 in 2025. Any earnings above that amount are not subject to Social Security tax and do not increase your benefit.

Your benefit is based on your highest 35 years of indexed earnings—meaning each year’s income is adjusted for inflation to reflect its value in today’s dollars. If you worked fewer than 35 years, zeros are included in the calculation, which can significantly reduce your average and therefore your monthly benefit.

Key takeaway: Once your annual income exceeds the taxable wage base, additional earnings don’t raise your future Social Security benefit. However, working longer can still increase your benefit if you replace lower-earning years or zeros in your 35-year average.

Four Ways to Increase Your Social Security Benefits

1. Fill in or Replace Zero Years

If you have fewer than 35 years of work history, each missing year is counted as zero. Even one extra year of income can replace a zero and raise your benefit.

Example: If you worked 32 years and earned $80,000 annually in your final three years, adding those years could significantly boost your benefit calculation.

2. Delay Claiming to Earn Higher Benefits

You can claim Social Security as early as age 62, but doing so permanently reduces your benefit—up to 30% less than your full retirement age (FRA) amount. For those born in 1960 or later, FRA is 67.

If you wait past FRA, your benefit grows by 8% per year up to age 70, plus annual cost-of-living adjustments (COLAs).

Example:

Claiming at 62: $1,400/month

Claiming at 67: $2,000/month

Claiming at 70: $2,480/month

That’s a $1,080 per month difference for waiting between the ages of 62 and 70.

3. Maximize Spousal and Dependent Benefits

Spousal and dependent benefits can be valuable for married couples or retirees with young children.

Spousal Benefit: A spouse can claim up to 50% of the higher earner’s FRA benefit, provided the higher earner has already filed.

Divorced Spouse Benefit: You may qualify if the marriage lasted 10 years or longer, and you haven’t remarried prior to age 60.

Dependent Benefit: Retirees age 62+ with children under 18 may receive additional benefits for dependents.

Planning tip: For individuals who plan to utilize the 50% spousal benefit and/or the dependent benefit, the path to the optimal filing strategy is more complex because the spouse and dependents cannot receive these benefits until that individual has actually turned on their social security benefit, which, in some cases, can favor not waiting until age 70 to file.

4. Understand Survivor Benefits

If one spouse passes away, the surviving spouse receives the higher of the two benefits. This makes it especially beneficial for the higher-earning spouse to delay claiming to age 70, maximizing the survivor benefit and providing long-term income protection.

How Social Security Benefits Are Taxed

Up to 85% of your Social Security benefits may be taxable, depending on your combined income (adjusted gross income + nontaxable interest + half of your Social Security benefits).

Single filers: Taxes begin at $25,000 of combined income

Married filing jointly: Taxes begin at $32,000 of combined income

If you don’t need Social Security to cover living expenses right away, delaying benefits can not only increase your future income but may also help manage taxes by controlling your income levels in early retirement.

Medicare Premiums and Income Planning

Once you reach age 65, you’ll typically enroll in Medicare Part B and D, and your premiums are based on your Modified Adjusted Gross Income (MAGI). Higher income means higher premiums under the Income-Related Monthly Adjustment Amount (IRMAA) rules.

Because Social Security benefits count as income for these purposes, timing your claiming strategy can help you manage Medicare costs.

Roth Conversions: Turning Delay into an Opportunity

Delaying Social Security creates a window for Roth conversions—moving money from a traditional IRA to a Roth IRA at potentially lower tax rates before Required Minimum Distributions (RMDs) begin at age 73 or 75.

Benefits of Roth conversions include:

Paying tax now at potentially lower rates

Reducing future RMDs

Potentially reduce future Medicare premiums

Creating a tax-free income source in retirement

Leaving tax-free assets to heirs

Coordinating your claiming strategy with Roth conversions can improve long-term tax efficiency and enhance your retirement flexibility.

Claiming Early? Know the Earned Income Penalty

If you claim Social Security before full retirement age and continue to work, your benefits may be temporarily reduced.

In 2025, the earnings limit is $23,400. For every $2 earned over the limit, $1 in benefits is withheld.

In the year you reach FRA, a higher limit applies: $62,160, and only $1 is withheld for every $3 earned above that.

Once you reach full retirement age, the penalty disappears, and your benefit is recalculated to credit any withheld amounts.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQ)

How are Social Security benefits calculated?

Social Security benefits are based on your highest 35 years of indexed earnings, adjusted for inflation. If you worked fewer than 35 years, zeros are included in your calculation, which can reduce your benefit.

What are the main ways to increase your Social Security benefits?

You can boost your benefit by replacing “zero” earning years, delaying your claim up to age 70 for an 8% annual increase past full retirement age, and coordinating spousal or survivor benefits strategically. Working longer and earning more during high-income years can also improve your benefit calculation.

How does delaying Social Security affect taxes and Medicare premiums?

Delaying benefits can help you manage taxable income in early retirement and avoid higher Medicare premiums triggered by the IRMAA income thresholds. This window can also allow for Roth conversions, which reduce future Required Minimum Distributions (RMDs) and create tax-free income in later years.

How are Social Security benefits taxed?

Up to 85% of your benefits may be taxable depending on your combined income (adjusted gross income + nontaxable interest + half of your benefits). Taxes begin at $25,000 for single filers and $32,000 for married couples filing jointly. Managing income sources can help minimize these taxes.

What is the earned income penalty for claiming Social Security early?

If you claim before full retirement age and continue working, benefits are reduced by $1 for every $2 earned above $23,400 in 2025. In the year you reach full retirement age, the limit increases to $62,160, and only $1 is withheld for every $3 earned over that amount. The penalty ends at full retirement age, when your benefit is recalculated.

What are spousal and survivor Social Security benefits?

A spouse can claim up to 50% of the higher earner’s full retirement benefit once that person has filed. If one spouse passes away, the survivor receives the higher of the two benefits. This makes it especially advantageous for the higher earner to delay claiming to age 70 to maximize long-term income protection.

How can Roth conversions complement Social Security planning?

Performing Roth conversions in the years before claiming Social Security or reaching RMD age allows retirees to shift pre-tax funds into tax-free accounts at potentially lower tax rates. This strategy can reduce future taxable income, manage Medicare premiums, and increase retirement flexibility.

Social Security Claiming Strategies: Early vs. Delayed Benefits Explained

Social Security can be one of your most powerful retirement assets—if you claim it strategically. In this article from Greenbush Financial Group, we compare early versus delayed claiming paths, explore spousal and survivor benefits, and explain how tax and income planning can help you unlock more lifetime income.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

For many retirees, Social Security ends up being the single largest and most reliable income source in retirement. It is inflation-protected, provides survivor benefits, and lasts for life. Yet, many people cost themselves hundreds of thousands of dollars in lifetime income by claiming too early—or by ignoring the tax and spousal rules that make timing so important.

This article explores two common paths for claiming Social Security, the tax and survivor strategies that matter most, and how to build a decision framework that balances both the math and the emotional realities of retirement.

The Two Paths: Early & Active vs. Delay & Fortify

There is no one-size-fits-all answer to Social Security timing. Instead, retirees can think of two primary paths:

Path A: Early & Active (Claiming at 62–65)

Works best for those with health concerns or shorter life expectancy.

Provides cash flow to enjoy active early retirement years.

Can unlock additional benefits, such as spousal add-ons or child benefits.

Trade-off: Lower lifetime income and reduced survivor benefits.

Path B: Delay & Fortify (Claiming at 67–70)

Higher earner delays to 70, maximizing both their lifetime benefit and the survivor benefit for their spouse.

Serves as “longevity insurance,” providing a larger, inflation-adjusted check for life.

Opens the door for Roth conversions to reduce future required minimum distributions (RMDs) and future Medicare premiums.

Trade-off: Requires income from working or pensions, or drawing down on assets in the meantime

Path A: Early & Active (Claiming at 62–65)

For many retirees, claiming Social Security early feels like “getting what’s yours” after decades of paying into the system. And in some cases, it’s absolutely the right move. This path prioritizes flexibility and cash flow in the early years of retirement — often before traditional pensions, investment income, or part-time work fully kick in.

Let’s unpack when and why early claiming can make sense, and the trade-offs to watch out for.

Works Best for Those with Health Concerns or Shorter Life Expectancy

Social Security benefits are designed around actuarial averages. The longer you live, the more a delayed claim pays off. But if you have health concerns, a family history of shorter life expectancy, or simply want to maximize income during the “go-go” years of retirement, claiming early can be a rational and emotionally satisfying choice.

For example, a retiree who claims at 62 will receive about 70–75% of their full retirement age (FRA) benefit. While that’s a reduction, the earlier payments can add up over time if the individual doesn’t live into their 80s or 90s.

Rule of thumb: If you expect your life expectancy to be shorter than the early 80s, claiming before FRA may result in higher total lifetime benefits.

Provides Cash Flow to Enjoy Active Early Retirement Years

Many retirees want to travel, pursue hobbies, or help family members financially in their 60s while they’re still healthy and energetic. Social Security can serve as a predictable income base that helps fund this period — reducing the need to withdraw heavily from investment accounts during market downturns.

Consider a 63-year-old couple who wants to take advantage of early retirement while waiting for their portfolio to grow. Claiming one spouse’s benefit early might provide enough monthly income to bridge the gap and protect long-term assets.

Tip: Early claiming can work well as part of a “phased retirement” approach — easing out of the workforce while still maintaining a reliable income stream.

Can Unlock Additional Benefits, Such as Spousal Add-Ons or Child Benefits

Claiming early sometimes unlocks access to auxiliary benefits that wouldn’t otherwise be available. For instance:

A non-working spouse can start claiming a spousal benefit once the higher-earning spouse files for Social Security.

Dependent children under age 18 (or 19 if still in high school) may also qualify for benefits if a parent begins claiming.

This strategy can create a multi-benefit window, where the total family income from Social Security exceeds what the primary earner would receive alone — especially valuable for families still supporting dependents or paying for college.

Trade-Off: Lower Lifetime Income and Reduced Survivor Benefits

The biggest drawback to early claiming is mathematical: reduced monthly checks for life. Claiming at 62 permanently cuts benefits by roughly 25–30% compared to waiting until full retirement age. For married couples, this also means a smaller survivor benefit for the spouse who lives longer.

Over a 20- or 30-year retirement, that difference can add up to hundreds of thousands of dollars in lost income. It can also limit flexibility later in life when expenses like healthcare and long-term care rise.

To visualize this, here’s a simple comparison:

Path B: Delay & Fortify (Claiming at 67–70)

If the Early & Active path is about maximizing flexibility and early retirement enjoyment, the Delay & Fortify strategy is about building strength and security for the long haul. Delaying your Social Security claim allows your benefit to grow each year, providing powerful longevity insurance and boosting survivor protection for your spouse.

This path often works best for retirees who expect to live into their 80s or beyond, have other income sources to draw from in the meantime, or want to use the delay window for tax-efficient planning.

Higher Earner Delays to 70, Maximizing Both Their Lifetime Benefit and the Survivor Benefit for Their Spouse

For married couples, Social Security isn’t just an individual decision — it’s a household one. The higher-earning spouse’s benefit often becomes the survivor benefit for the remaining spouse.

By waiting to claim until age 70, the higher earner locks in delayed retirement credits that increase benefits by roughly 8% per year after full retirement age (up to age 70). That means a benefit that would have been $2,000 at age 67 could grow to about $2,480 per month by age 70 — a 24% increase for life.

That higher benefit continues for as long as either spouse is alive, making this strategy especially valuable for couples where one spouse is expected to live well into their 80s or 90s.

Example:

If one spouse claims early at 62 and the other delays to 70, the household creates a blend — immediate income now, and a larger, inflation-protected income base later that acts as a financial safety net for the survivor.

Serves as “Longevity Insurance,” Providing a Larger, Inflation-Adjusted Check for Life

Delaying Social Security is sometimes compared to buying an annuity — but without the fees or market risk. It’s an inflation-adjusted income stream that continues for life, backed by the U.S. government.

For those with strong health and longevity in their family history, this can be one of the best “investments” available, because the increase in monthly income provides protection against outliving assets in later years.

Breakeven point: Typically, the math favors delaying if you live past your early 80s. But beyond the numbers, many retirees value the peace of mind that comes with knowing they’ll always have a larger, guaranteed income base, no matter how long they live.

Opens the Door for Roth Conversions to Reduce Future RMDs and Medicare Premiums

One of the less-discussed advantages of delaying benefits is the tax planning window it creates. Between retirement (often mid-60s) and age 70, retirees may have lower taxable income, creating an opportunity to do Roth IRA conversions at favorable tax rates.

Here’s why this matters:

Converting pre-tax assets to Roth reduces future Required Minimum Distributions (RMDs) at age 73/75.

Lower RMDs can help manage Medicare premiums, which are based on income (IRMAA thresholds).

Roth income in retirement is tax-free, helping stabilize cash flow and protect against rising tax rates.

Strategy in action:

A retiree might use withdrawals from cash or taxable accounts to fund living expenses while converting portions of their traditional IRA to a Roth during those pre-70 years. Then, when Social Security finally starts, their taxable income is lower — improving long-term tax efficiency.

Trade-Off: Requires Income from Working or Pensions, or Drawing Down on Assets in the Meantime

The biggest hurdle in delaying Social Security is bridging the income gap. If you retire at 65 but delay claiming until 70, that’s five years of expenses that must be covered by savings, part-time work, or other income sources.

For some retirees, this is perfectly manageable. For others, it may mean drawing down more from investment accounts — which can be uncomfortable, especially during volatile markets.

The key is to view this period as a trade-off by drawing down on a larger portion of your retirement assets now for a higher guaranteed income stream later on. Many financial plans model this “bridge strategy” explicitly, showing how a few years of portfolio withdrawals can result in higher lifetime income and stronger survivor protection.

Building a Decision Framework: Balancing the Math and the Mindset

Choosing when to claim Social Security is part math, part mindset. The best decision balances financial optimization with personal goals and health considerations.

A helpful framework:

Start with longevity assumptions. Estimate based on family health and lifestyle.

Assess your income bridge. Can you fund living expenses until 67–70 without stress?

Run the household math. Model joint benefits, survivor income, and tax implications.

Weigh the emotional factors. Early claiming often feels more secure and immediate; delaying feels more strategic and protective.

Revisit regularly. If you’re 62 and unsure, you don’t have to decide today — claiming flexibility exists year to year.

The right Social Security claiming strategy isn’t about “winning” a mathematical breakeven test — it’s about creating confidence and control in retirement.

The Bottom Line

Social Security is one of the most valuable, inflation-protected income sources you’ll ever have. Taking the time to make a thoughtful, data-driven claiming decision can add tens or even hundreds of thousands of dollars to your lifetime benefits.

But just as importantly, it can bring peace of mind — knowing your retirement income is designed to support both your financial goals and your life priorities.

If you’re approaching retirement, consider running multiple claiming scenarios or working with a financial planner to build a customized Social Security plan that fits your household.

Because in the end, smart Social Security planning isn’t just about maximizing a benefit — it’s about maximizing the life you can live in retirement.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

What are the main differences between claiming Social Security early versus delaying benefits?

Claiming early (ages 62–65) provides immediate income and flexibility but permanently reduces monthly benefits by up to 30%. Delaying to age 70 increases benefits by 8% per year after full retirement age and strengthens survivor protection for a spouse.

When does it make sense to claim Social Security early?

Early claiming can make sense for retirees with health concerns, shorter life expectancy, or those who need income to support active early retirement years. It can also unlock spousal or dependent benefits sooner. However, it reduces lifetime and survivor benefits, so it’s best suited for households prioritizing flexibility over long-term income maximization.

What are the advantages of delaying Social Security until age 70?

Delaying benefits boosts lifetime and survivor income, provides inflation-adjusted longevity protection, and can create a valuable tax-planning window. Those extra years often allow retirees to perform Roth conversions at lower tax rates and reduce future Required Minimum Distributions (RMDs) and Medicare premiums.

How do spousal and survivor benefits factor into Social Security claiming decisions?

For married couples, the higher earner’s benefit often becomes the survivor benefit. By delaying their claim to age 70, the higher earner ensures the surviving spouse receives a larger, inflation-adjusted income for life—providing greater long-term financial stability.

What is the breakeven point for delaying Social Security?

Generally, if you live beyond your early 80s, delaying your claim tends to produce higher lifetime benefits. However, the optimal strategy depends on personal health, family longevity, and income needs during the delay period. Financial modeling can help identify the most efficient approach.

How can delaying Social Security support tax and Medicare planning?

The years between retirement and claiming benefits often provide a “low-income window” ideal for Roth conversions. This can lower future RMDs and taxable income, helping retirees stay below the IRMAA thresholds that trigger higher Medicare premiums.

How should I decide which Social Security claiming strategy is best for me?

The right approach balances math and mindset—combining life expectancy estimates, income bridge options, household tax impact, and emotional comfort. Working with a financial planner to test multiple claiming scenarios can clarify which path offers the best balance of income security and lifestyle freedom.

Will Social Security Be There When You Retire?

Social Security is projected to face a funding shortfall in 2034, leading many Americans to wonder if it will still be there when they retire. While the system won’t go bankrupt, benefits could be reduced by about 20% unless Congress acts. Our analysis at Greenbush Financial Group explores what 2034 really means, why lawmakers are likely to intervene, and how to plan your retirement with Social Security uncertainty in mind.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

If you’ve looked at your Social Security statement recently, you may have noticed a troubling note: beginning in 2034, the system will no longer have enough funding to pay out full promised benefits. For many Americans, this raises a big question: Will Social Security even be there when I retire?

In this article, we’ll break down:

How Social Security is currently funded and why it faces challenges

What the 2034 date really means (hint: it’s not “bankruptcy”)

Why Congress is likely to act before major benefit cuts happen

Practical solutions that could shore up the system for future retirees

Why meaningful reform may not happen until the last minute

How Social Security Works Today

Social Security is funded primarily through FICA payroll taxes. Workers and employers each pay 6.2% of wages (12.4% total) into the system, which goes toward funding retirement benefits for current retirees.

Here’s the key point: the money doesn’t accumulate in a large “savings account” for future benefits. Instead, today’s payroll taxes go right back out the door to pay today’s beneficiaries. This setup worked well when there were many workers for each retiree, but demographic trends are changing the math.

Baby Boomers are retiring in large numbers.

People are living longer, so they collect benefits for more years.

Birth rates are low, meaning fewer workers are paying into the system.

This imbalance is the root of Social Security’s funding challenge.

What Happens in 2034?

Many people think 2034 is the year Social Security “goes bankrupt.” That’s not the full story.

According to the Social Security Trustees’ report, if Congress does nothing, the system’s trust funds will be depleted by 2034. At that point, incoming payroll taxes would still be enough to pay about 80% of promised benefits.

In practical terms, this would mean an immediate 20% cut in benefits for all recipients. While Social Security wouldn’t disappear, such a cut would have a huge impact on retirees who rely on it as their primary source of income.

Why We Believe Congress Will Act

It’s our opinion that Congress will not allow benefits to be cut so dramatically. Here’s why:

For a large portion of Americans over age 65, Social Security is the primary source of retirement income.

Cutting benefits by 20% would potentially impoverish millions of retirees.

Retirees also represent a powerful voting population, making it politically unlikely that lawmakers would let the system fail without intervention.

That doesn’t mean changes won’t come—but it does make drastic benefit cuts less likely.

Possible Solutions to Fix Social Security

The challenge is real, but there are several practical options available. The earlier these changes are made, the smaller the adjustments need to be. If lawmakers wait until 2034, the fixes may be more drastic. Some of the most common proposals include:

1. Increasing the Taxable Wage Base

Right now, Social Security taxes only apply to wages up to $176,100 (2025 limit). Someone earning $400,000 pays Social Security tax on less than half of their income.

Raising or eliminating the cap would bring more revenue into the system.

While no one likes higher taxes, it may be less painful than the economic impact of the sudden cut in Social Security Benefits starting in 2034

2. Extending the Full Retirement Age

Currently, full retirement age is 67. But Social Security hasn’t been properly indexed for life expectancy. Studies suggest that if it were, the full retirement age could be in the early 70s.

Extending retirement age would reduce how long people collect benefits.

This adjustment reflects the fact that Americans are living longer and the Social Security system was not originally designed to make payments to retirees for 15+ years

3. Limiting Early Filing Options

Right now, many people file early at 62, locking in a reduced benefit.

One proposal is to require younger workers (e.g., those 50 and under) to wait until full retirement age to claim.

This would preserve more assets in the trust over the long term.

Why Reform May Be Delayed

Unfortunately, even though the math is clear, we don’t expect Congress to make many changes before 2034. Why? Because fixing Social Security is a politically unfriendly topic.

To save the system, lawmakers must either raise taxes or cut benefits.

Neither of those options wins votes, which makes reform easy to push off.

This likely means the situation will get more tense as we approach 2034. If reforms aren’t passed in time, one possibility is a government bailout of the Social Security Trust, with additional money created to keep it solvent. While this could buy time, it doesn’t address the underlying funding imbalance—and could carry broader economic consequences.

How We Plan Around Social Security Uncertainty

For our clients, we don’t take a “wait and see” approach. Since we don’t know the exact fate of Social Security, for clients under a specific age, we build retirement plans that assume a reduction in benefits.

If Social Security benefits are reduced in the future, our clients’ plans are already designed to account for the cut, meaning their retirement income won’t be derailed.

If, on the other hand, Congress keeps Social Security fully intact, that’s fantastic—it simply means more income than we initially projected.

This conservative approach provides peace of mind and ensures that retirement strategies remain flexible no matter what happens in Washington.

The Bottom Line

Social Security faces real funding challenges, but it’s highly unlikely to disappear. Instead, it will probably undergo adjustments to ensure long-term solvency.

For retirees and pre-retirees, the key takeaway is this: don’t panic, but don’t ignore it either. Build your retirement plan with the assumption that Social Security may look different in the future. A fee-based financial planner can help you model different scenarios and build a strategy that works no matter how Congress acts.

If you’d like to explore how Social Security fits into your retirement plan, learn more about our financial planning services here.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.