Retirement Income Planning: How to Pay Yourself Without a Job

Creating retirement income requires more than simply withdrawing money from investment accounts. This guide explains how retirees can coordinate Social Security benefits, investment withdrawals, and cash reserves to build a reliable retirement paycheck while managing taxes, sequence-of-returns risk, and market volatility. Learn practical withdrawal strategies that help improve long-term portfolio sustainability and increase retirement confidence. Discover why organized income planning often matters more than chasing investment returns alone.

The hardest part of retirement is not saving money. It is turning your savings into a paycheck that can last for decades. A strong retirement income strategy combines Social Security, investments, and cash reserves in a way that helps retirees manage taxes, market downturns, and long-term spending needs. At Greenbush Financial Group, we often find that retirees feel more confident once they move from random withdrawals to a structured retirement paycheck plan.

The Hardest Part of Retirement Is Not Saving. It’s Replacing Your Paycheck.

For most of your working life, income was automatic.

You worked, your paycheck arrived, taxes were withheld, and bills were paid.

Retirement changes that system overnight.

Now your income may need to come from:

Social Security

Investment accounts

IRAs

Roth IRAs

Cash savings

Brokerage accounts

Maybe a pension

That transition can feel uncomfortable even for financially responsible retirees.

Many people spend decades learning how to save for retirement but very little time learning how to withdraw from retirement.

That is why one of the biggest retirement questions becomes:

“How do I actually turn my savings into reliable monthly income?”

The answer is usually not:

Living only on dividends

Using the 4% rule blindly

Pulling money randomly from accounts

Staying fully invested with no cash reserves

A retirement paycheck works best when it is intentional, flexible, tax-aware, and designed to handle both good markets and bad ones.

What a Retirement Paycheck Actually Looks Like

A retirement paycheck is usually built from three primary sources:

Guaranteed income

Investment withdrawals

Cash reserves

Each source plays a different role.

The goal is not maximizing investment returns.

The goal is creating sustainable monthly income while reducing unnecessary financial stress.

The 3 Buckets of Retirement Income

Bucket #1: Guaranteed Income

This includes predictable income sources such as:

Social Security

Pensions

Certain annuities

For many retirees, this income helps cover core living expenses like:

Housing

Utilities

Groceries

Insurance

Basic healthcare costs

Guaranteed income creates stability.

The more predictable income a retiree has, the less pressure there may be on investment withdrawals during difficult markets.

Bucket #2: Investment Withdrawals

This is where retirees often generate additional income beyond Social Security.

Withdrawals may come from:

Traditional IRAs

401(k)s

Taxable brokerage accounts

Roth IRAs

This is also where many costly mistakes happen.

Without a strategy, retirees may:

Withdraw too much

Trigger unnecessary taxes

Increase Medicare premiums

Sell investments during downturns

Deplete the wrong accounts too early

The order of withdrawals matters.

Bucket #3: Cash Reserves

Cash reserves are one of the most overlooked parts of retirement income planning.

Cash reserves may include:

Savings accounts

Money market funds

CDs

Treasury bills

Short-term bond holdings

The purpose of cash is not maximizing returns.

Its purpose is flexibility.

Cash reserves help retirees avoid selling investments during bad markets when emotions are elevated and portfolio values are temporarily down.

How Retirement Income Is Structured Month to Month

Retirement income planning usually starts with one simple question:

“How much do you actually need each month?”

Step 1: Identify Monthly Spending Needs

Example:

John and Linda retire at age 66.

They estimate they need:

$8,000/month after taxes

That includes:

Property taxes

Insurance

Healthcare

Travel

Utilities

Food

Entertainment

Home maintenance

Step 2: Subtract Guaranteed Income

They receive:

$4,500/month combined from Social Security

That leaves:

$3,500/month that must come from investments and savings

This is called the income gap.

Step 3: Build a Withdrawal Strategy

Their assets include:

$950,000 in IRAs

$300,000 in brokerage accounts

$150,000 in cash reserves

$200,000 in Roth IRAs

Instead of taking income randomly, they decide to:

Use brokerage assets first for flexibility

Maintain 18 months of cash reserves

Delay larger IRA withdrawals strategically

Refill cash reserves during stronger market periods

Keep Roth assets growing longer for future flexibility

Now their retirement income becomes organized and repeatable rather than reactive.

Why Random Withdrawals Can Create Long-Term Problems

Many retirees withdraw from whichever account feels easiest at the time.

That can create ripple effects.

Example

Suppose a retiree withdraws $80,000 entirely from an IRA for spending and home renovations.

That withdrawal may:

Push income into higher tax brackets

Increase taxation of Social Security

Trigger Medicare IRMAA surcharges

Reduce future Roth conversion opportunities

A different withdrawal strategy may have created a better long-term outcome.

Retirement income planning is not just about generating cash.

It is about generating cash efficiently.

Why Cash Reserves Matter So Much in Retirement

Many retirees underestimate how emotionally different investing feels after paychecks stop.

During working years, market declines may feel temporary because new paychecks continue arriving.

Retirement changes that dynamic.

Now withdrawals may be happening while investments are falling.

That creates what planners call sequence-of-returns risk.

What Is Sequence Risk?

Sequence risk occurs when poor market returns happen early in retirement while withdrawals are occurring simultaneously.

This combination can permanently reduce long-term portfolio sustainability.

Example

Two retirees start with identical portfolios and identical spending.

One is forced to sell investments during a major downturn to fund living expenses.

The other uses cash reserves temporarily while allowing investments time to recover.

The long-term outcomes can look dramatically different.

How Much Cash Should Retirees Keep?

There is no perfect answer.

But many retirees feel more comfortable keeping:

12–24 months of planned withdrawals in cash or short-term reserves

The appropriate amount depends on:

Risk tolerance

Market exposure

Spending flexibility

Healthcare concerns

Pension income

Comfort during volatility

Important Note

Too little cash may force investment sales during downturns.

Too much cash may reduce long-term purchasing power because inflation slowly erodes cash value.

The goal is balance.

Should Retirees Live Off Dividends Only?

Many retirees like the idea of “never touching principal” and living entirely off dividends.

While dividend income can help, retirement income planning is usually more nuanced than that.

Dividend-only strategies can create problems such as:

Concentrated portfolios

Reduced diversification

Lower flexibility

Chasing yield

Tax inefficiencies

What matters most is not whether income comes from dividends or withdrawals.

What matters is:

Total return

Sustainability

Tax efficiency

Risk management

Flexibility during market declines

A well-designed retirement paycheck should focus on the overall income strategy, not just one type of investment income.

How Social Security Fits Into a Retirement Paycheck

Social Security is often the foundation of retirement income.

The timing decision affects:

Monthly income

Portfolio withdrawals

Survivor income

Longevity protection

Taxes

Claiming at 62

Taking benefits early provides income sooner but permanently reduces monthly payments.

This may reduce portfolio withdrawals initially.

But it also lowers guaranteed lifetime income.

Claiming at Full Retirement Age

Waiting until full retirement age increases monthly benefits and avoids early claiming reductions.

For many retirees, this creates a balance between income needs and future benefit growth.

Delaying Until Age 70

Benefits increase each year benefits are delayed beyond full retirement age.

For healthy retirees, delayed Social Security can act as additional protection against longevity risk later in retirement.

Especially for married couples, this can significantly affect survivor income.

How Retirees Avoid Selling Investments During Market Declines

A strong retirement paycheck strategy is designed before market volatility happens.

That strategy often includes:

Cash reserves

Diversification

Flexible withdrawals

Annual tax reviews

Periodic rebalancing

Spending flexibility

Example Strategy

A retiree may:

Hold 18 months of withdrawals in cash

Use Social Security for core expenses

Withdraw from brokerage accounts during stable markets

Reduce discretionary spending during downturns

Refill cash reserves after stronger market periods

This creates options during stressful periods instead of forcing emotional decisions.

How Often Should Retirement Income Plans Be Reviewed?

Retirement income planning is not a one-time event.

Most retirees should review their strategy annually.

Areas worth reviewing include:

Withdrawal rates

Tax brackets

Roth conversion opportunities

Medicare IRMAA exposure

Cash reserve levels

Investment allocation

Spending changes

Inflation adjustments

The goal is not constantly changing the plan.

The goal is making thoughtful adjustments as retirement evolves.

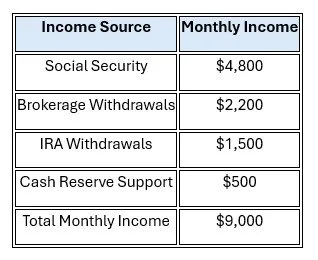

A Real-World Retirement Paycheck Example

Susan and Mark retire at ages 65 and 63.

They need:

$9,000/month after taxes

Their income plan looks like this:

Their Strategy

They maintain:

18 months of cash reserves

Moderate stock exposure for long-term growth

Diversification across account types

Annual withdrawal reviews

Flexible discretionary spending

During strong markets, they replenish cash reserves.

During weaker markets, they temporarily rely more heavily on cash rather than aggressively selling investments.

This approach helps reduce emotional pressure during volatility.

Common Retirement Paycheck Mistakes

1. Withdrawing Randomly From Accounts

Random withdrawals often create tax inefficiencies and unnecessary portfolio stress.

2. Keeping Too Little Cash

Without adequate reserves, retirees may be forced to sell investments during downturns.

3. Keeping Too Much Cash

Excessive cash can reduce long-term purchasing power because of inflation.

4. Ignoring Taxes

Taxes affect:

IRA withdrawals

Social Security taxation

Medicare premiums

Roth conversion opportunities

Retirement income should be coordinated at the household level.

5. Assuming the Same Strategy Works Forever

Retirement income plans should evolve over time as:

Spending changes

Healthcare costs rise

Markets fluctuate

RMDs begin

Tax laws change

Flexibility matters.

What Retirees Often Discover

Many retirees initially focus almost entirely on investment performance.

But over time, confidence often comes more from:

Organized cash flow

Predictable income

Tax coordination

Flexibility during downturns

Understanding where each dollar comes from

A retirement paycheck is not about finding a perfect strategy.

It is about building a system that feels sustainable and manageable over time.

Final Thoughts

The hardest part of retirement is usually not building wealth.

It is learning how to turn decades of savings into reliable monthly income.

A thoughtful retirement paycheck strategy can help retirees:

Reduce financial stress

Improve tax efficiency

Navigate market downturns

Protect long-term portfolio sustainability

Feel more confident about spending decisions

At Greenbush Financial Group, we often find that retirees gain confidence when they stop thinking about retirement income as random withdrawals and start viewing it as a coordinated household paycheck strategy.

The goal is not predicting every market movement perfectly.

The goal is creating a flexible income system that can support retirement through both strong markets and difficult ones.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

FAQ

-

How do retirees create a monthly paycheck from investments?Most retirees combine Social Security, investment withdrawals, and cash reserves to create consistent monthly income. Withdrawals are typically coordinated across different account types to improve tax efficiency and manage market risk.

-

How much cash should retirees keep?Many retirees benefit from holding 12-24 months of planned withdrawals in cash or short-term reserves, especially during the early retirement years.

-

What accounts should retirees withdraw from first?The answer depends on taxes, age, income needs, and long-term planning goals. Many retirees use a combination of taxable accounts, IRAs, and Roth accounts strategically rather than withdrawing from only one source.

-

What is sequence-of-returns risk?Sequence risk occurs when poor market returns happen early in retirement while withdrawals are being taken. This can permanently reduce long-term portfolio sustainability.

-

Should retirees rely only on dividends for income?Not necessarily. While dividends can help, most retirement income plans work better when they focus on total return, diversification, flexibility, and tax efficiency rather than dividends alone.

-

How does Social Security fit into a retirement paycheck?Social Security often acts as the foundation of retirement income by covering a portion of essential expenses and reducing pressure on investment withdrawals.

-

How often should retirement income plans be reviewed?Most retirees should review income strategies annually to evaluate taxes, spending, investment allocation, withdrawal rates, and healthcare costs.

-

What is the biggest retirement income mistake?One of the biggest mistakes is withdrawing money randomly from investment accounts without coordinating taxes, cash reserves, and long-term income sustainability.