Should You Retire at 62, 65, or 67? The Tradeoffs Most People Overlook

Should you retire at 62, 65, or 67? The answer involves much more than Social Security. Learn how healthcare costs, taxes, Roth conversions, and portfolio withdrawals can influence the best retirement age for your situation.

Deciding whether to retire at 62, 65, or 67 involves much more than simply choosing when to claim Social Security. Your retirement age can impact healthcare costs, taxes, portfolio withdrawals, Roth conversion opportunities, and long-term financial security. In this article, Greenbush Financial Group breaks down the real tradeoffs retirees should consider, including situations where retiring earlier may make sense and when waiting could provide better long-term outcomes.

Should You Retire at 62, 65, or 67? The Tradeoffs Most People Overlook

For many Americans, retirement planning often centers around one question:

“When should I retire?”

The most common ages people consider are 62, 65, and 67 because each one connects to major financial milestones:

Age 62: Earliest Social Security eligibility

Age 65: Medicare eligibility

Age 67: Full Retirement Age (FRA) for many retirees

But the reality is that retirement timing is rarely just about Social Security.

The age you stop working can affect:

Your healthcare costs

Your tax strategy

Your withdrawal rate

Your investment risk

Your long-term retirement security

Your emotional well-being

And despite what many headlines suggest, there is no universally “perfect” retirement age.

At Greenbush Financial Group, we often find that the best retirement age depends less on rules and more on how all the moving pieces fit together for a household.

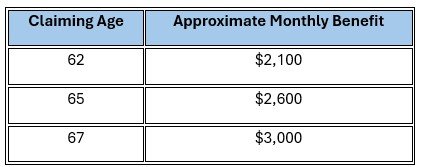

The Real Difference in Social Security at 62 vs. 65 vs. 67

One of the biggest factors in retirement timing is Social Security income.

Here’s a simplified example using someone whose Full Retirement Age benefit at 67 is $3,000 per month.

That difference can become substantial over a 25- to 30-year retirement.

For a married couple, coordinated claiming decisions may impact lifetime income by hundreds of thousands of dollars.

However, larger Social Security checks do not automatically mean delaying retirement is always better.

The bigger question is:

What are you giving up by waiting?

The Tradeoff Most People Miss

Many retirement articles focus only on maximizing Social Security benefits.

But retiring later can also mean:

Fewer healthy retirement years

Higher stress or burnout

Less flexibility with family

Missing Roth conversion opportunities

Paying more taxes later

Delaying goals you care about

Meanwhile, retiring earlier may increase:

Portfolio withdrawal pressure

Healthcare costs before Medicare

Sequence of returns risk

Longevity concerns

The goal is not simply maximizing one variable.

The goal is building a retirement plan that balances income, taxes, lifestyle, healthcare, and risk.

How Retiring Early Impacts Medicare and Healthcare Costs

One of the largest financial gaps in early retirement is health insurance before Medicare begins at 65.

If you retire at 62, you may need to bridge three years of healthcare costs before Medicare eligibility.

Depending on your income and coverage needs, that could mean:

ACA marketplace plans

COBRA coverage

Private insurance

Spousal employer coverage

For many couples, healthcare premiums and out-of-pocket costs can easily exceed:

$15,000 to $30,000+ annually before age 65

That expense is often underestimated.

Example: Retiring at 62 Before Medicare

A couple retires at 62 with:

$1.2 million invested

No pension

$70,000 annual spending goal

Because Social Security has not started yet, they may need to withdraw:

$70,000+ annually from investments

Plus healthcare costs

Plus taxes

If markets decline early in retirement, those larger withdrawals can create pressure on the portfolio much sooner than expected.

The Sequence of Returns Risk Most Retirees Ignore

One of the biggest risks in early retirement is something called sequence of returns risk.

This means poor market returns early in retirement can damage a portfolio more severely when withdrawals are happening simultaneously.

For example:

A major market decline at age 63 may hurt far more than the same decline at age 78.

Early losses combined with withdrawals can permanently reduce future recovery potential.

This becomes especially important for retirees stopping work before Social Security and Medicare begin.

Example

Two retirees both average 6% annual returns over retirement.

But:

Retiree A experiences strong returns early

Retiree B experiences a bear market immediately after retiring

Even with identical average returns, Retiree B may run out of money significantly sooner because withdrawals occurred during market declines.

This is why retirement timing and market conditions should be evaluated together.

Break-Even Analysis: How Long Do You Need to Live for Waiting to Pay Off?

One of the most common questions retirees ask is:

“How long do I need to live for delaying Social Security to make sense?”

A simplified break-even analysis often shows:

Delaying from 62 to 67 may break even somewhere in the late 70s or early 80s

But this analysis is incomplete unless you also consider:

Taxes

Investment withdrawals

Survivor benefits

Healthcare costs

Portfolio growth

Longevity expectations

Spousal coordination

For married couples especially, the higher earner delaying benefits may significantly improve survivor income later.

That can become critically important if one spouse lives well into their 80s or 90s.

Situations Where Retiring at 62 May Actually Make Sense

Retiring at 62 is not automatically a mistake.

In some situations, it may be entirely reasonable.

Retiring Earlier May Work Well If:

1. You Have Strong Savings Relative to Spending

For example:

$1.5 million portfolio

Low debt

Moderate spending needs

Flexible lifestyle

In this case, early retirement may create manageable withdrawal rates.

2. Your Health or Energy Is Declining

Many retirees prioritize healthy active years over maximizing income later.

This is especially true if:

Work stress is affecting health

A physically demanding career becomes difficult

Family longevity expectations are shorter

3. You Want Roth Conversion Opportunities

Retiring before Social Security and RMDs begin can create lower-income years.

Those years may allow:

Strategic Roth conversions

Lower future RMDs

Reduced future tax exposure

Potentially lower IRMAA surcharges later

This planning opportunity is often overlooked.

Situations Where Waiting Until 67 May Be Smarter

In other cases, delaying retirement may improve long-term security substantially.

Waiting May Make More Sense If:

1. You Are Heavily Reliant on Social Security

If Social Security represents a large portion of future retirement income, delaying may significantly improve financial flexibility later.

Example

Someone expecting:

$3,200/month at 67

Only $2,200/month at 62

That additional guaranteed income may reduce long-term portfolio pressure considerably.

2. You Have Limited Retirement Savings

Working longer may provide:

More years to save

Fewer years withdrawing

Higher Social Security benefits

Additional healthcare coverage through work

3. You Are Concerned About Longevity Risk

For retirees with strong family longevity histories, larger guaranteed income later may provide more confidence throughout retirement.

The Tax Consequences Most People Never Consider

Retirement timing is not just an income decision.

It is also a tax planning decision.

Roth Conversion Windows

Many retirees temporarily fall into lower tax brackets between:

Retirement

Social Security

Required Minimum Distributions (RMDs)

That window may create opportunities to convert portions of traditional IRAs into Roth accounts strategically.

Waiting too long to evaluate this can lead to:

Larger future RMDs

Higher Medicare premiums

Increased survivor tax burdens

IRMAA Brackets and Medicare Premiums

Higher retirement income can increase Medicare premiums through IRMAA surcharges.

Large:

Roth conversions

Capital gains

IRA withdrawals

Can trigger higher Medicare costs later.

Strategic income coordination becomes especially important after age 63 because Medicare premiums use a two-year lookback.

Capital Gains Timing

Retirement may temporarily create years with lower taxable income.

That could allow:

Tax-efficient capital gains harvesting

Reduced future embedded gains

More efficient portfolio repositioning

This planning window often closes once:

RMDs begin

Social Security starts

Pension income increases

Common Mistakes Couples Make When Coordinating Retirement Timing

Couples often retire at different times or have different income levels.

That creates additional planning complexity.

Common Mistakes Include:

Both Spouses Claiming Social Security Too Early

This may permanently reduce survivor income later.

Ignoring Healthcare Coordination

One spouse retiring early while the other still has employer coverage may create valuable healthcare planning opportunities.

Not Coordinating Tax Brackets

Retirement timing affects:

Roth conversions

IRA withdrawals

Medicare premiums

Social Security taxation

Assuming Both Spouses Should Retire Simultaneously

Sometimes staggered retirement dates improve:

Cash flow

Healthcare access

Tax flexibility

Emotional adjustment

The Emotional Side of Retirement Timing

Retirement decisions are not purely mathematical.

Many people struggle with competing fears:

Fear of Working Too Long

Some retirees worry about:

Losing healthy years

Delaying travel

Missing time with family

Burnout

Fear of Running Out of Money

Others fear:

Market volatility

Healthcare costs

Inflation

Longevity risk

Both concerns are valid.

The best retirement decision often balances financial sustainability with quality of life.

A Simple Framework for Deciding

Retiring Earlier May Work If These 3 Things Are True

Your withdrawal rate appears sustainable

You have a healthcare bridge to Medicare

You value time and flexibility more than maximizing guaranteed income

Waiting Longer May Make Sense If These 3 Things Are True

Social Security will be a major income source

You need additional savings or healthcare coverage

You are concerned about long-term longevity risk

Real-World Example: Couple Retiring at 62

A married couple has:

$1.2 million portfolio

$85,000 annual spending target

Modest pension income

Social Security delayed until 67

Potential Advantages

More years for travel and family

Roth conversion opportunities

Reduced work stress

Potential Challenges

Larger portfolio withdrawals initially

Three years before Medicare eligibility

Greater exposure to early market downturns

In this scenario, success may depend heavily on:

Spending flexibility

Tax management

Investment allocation

Market conditions early in retirement

Real-World Example: Heavy Social Security Reliance

Another retiree has:

$350,000 portfolio

Social Security expected to cover most future expenses

For this retiree, delaying benefits and potentially working longer may significantly improve long-term stability because guaranteed income becomes more valuable than preserving leisure years earlier.

Important Note About “The Perfect Retirement Age”

There is no universally optimal age to retire.

The “best” decision depends on:

Your health

Your goals

Your savings

Your tax situation

Your family dynamics

Your spending needs

Your emotional priorities

At Greenbush Financial Group, retirement planning often involves evaluating tradeoffs rather than searching for a perfect answer.

Sometimes retiring earlier creates the better life decision.

Sometimes waiting provides more security and flexibility.

Most importantly, retirees should understand the long-term implications before making irreversible decisions.

Final Thoughts

The decision to retire at 62, 65, or 67 affects far more than your monthly Social Security check.

It can influence:

Taxes

Medicare costs

Investment risk

Withdrawal rates

Long-term portfolio sustainability

Survivor income

Lifestyle flexibility

The key is understanding the tradeoffs honestly rather than assuming there is one universally correct answer.

A well-designed retirement plan should coordinate:

Social Security

Tax strategy

Healthcare planning

Investment withdrawals

Roth conversion opportunities

Long-term income sustainability

At Greenbush Financial Group, we help retirees evaluate these decisions within the context of their full financial picture so retirement timing aligns with both financial security and personal goals.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

FAQ Section

-

Is it better to retire at 62 or 67?Neither is universally better. Retiring at 62 provides more flexibility and earlier retirement years, while waiting until 67 increases guaranteed Social Security income and may reduce long-term portfolio pressure.

-

How much less Social Security do you get at 62?Benefits may be reduced by roughly 30% compared to claiming at Full Retirement Age, depending on your birth year.

-

What is the biggest risk of retiring early?One of the biggest risks is sequence of returns risk, where poor market performance early in retirement combined with withdrawals can permanently weaken a portfolio.

-

Why is age 65 important for retirement?Age 65 is when most Americans become eligible for Medicare, which can significantly reduce healthcare costs compared to private insurance before 65.

-

Should married couples retire at the same time?Not necessarily. Staggering retirement dates can improve healthcare access, tax flexibility, and Social Security coordination.

-

Does delaying Social Security always pay off?No. Delaying benefits may improve lifetime income for some retirees, especially higher earners or couples concerned about longevity, but it is not automatically the best decision for everyone.

-

What are Roth conversion windows in retirement?These are lower-income years between retirement and RMD age that may allow retirees to convert IRA assets into Roth accounts at lower tax rates.

-

Can retiring too early increase taxes later?Yes. Larger future RMDs, higher Social Security taxation, and increased Medicare premiums can occur if tax planning opportunities are missed early in retirement.