Should You Invest Your HSA Account?

Health Savings Accounts can be more than just a tool for current medical expenses. This article explains when it makes sense to invest your HSA, when to keep funds in cash, and how to use an HSA as a long-term retirement strategy. Learn about tax advantages, contribution limits for 2026, and how to transfer funds to investment-friendly HSA providers. Discover how to maximize tax-free growth for future healthcare costs.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Health Savings Accounts (HSAs) are a valuable tool that allow individuals to use pre-tax dollars to pay for qualified medical expenses. But there is also a more advanced planning strategy that many people are not aware of — using an HSA as a long-term investment account for future healthcare costs, especially in retirement when healthcare expenses are typically at their highest.

So the question becomes: If you’re not planning to spend your HSA money this year, should you invest it so it grows over time?

In this article, we’ll cover:

When it makes sense to invest your HSA

When you should keep HSA funds in cash

What to do if your employer HSA doesn’t allow investing

How HSA transfers work

The tax advantages of investing an HSA

2026 HSA contribution limits

Frequently asked questions about investing HSAs

The Long-Term HSA Strategy

Many people use their HSA to pay for current medical expenses. But another strategy is to:

Contribute to an HSA each year

Do NOT spend the HSA

Pay current medical expenses out-of-pocket

Allow the HSA to grow over time

Use the HSA later in retirement for healthcare expenses

This strategy can be powerful because:

Contributions are pre-tax

Growth is tax-deferred

Withdrawals are tax-free for qualified medical expenses

This makes the HSA one of the only accounts that can be tax-free on the way in and tax-free on the way out when used correctly.

Should You Invest Your HSA?

In general, if the money in your HSA is not going to be used within the next year, it can often make sense to invest those funds so they can grow over time.

This is especially true for individuals who:

Are 10+ years away from retirement

Can afford to pay current medical expenses out-of-pocket

Want to build a retirement healthcare fund

By investing the HSA, you are not only getting the tax deduction on the contribution, but you are also getting tax-free growth on the investments if used for qualified medical expenses later.

When You Should NOT Invest Your HSA

If you are using your HSA for current or short-term medical expenses, it usually makes sense to keep that portion in cash or a money market account.

A common strategy is to split the HSA into two buckets:

Short-term medical expenses → Keep in cash

Long-term retirement healthcare → Invest for growth

This way, you maintain stability for current expenses while still allowing long-term funds to grow.

What If Your Employer’s HSA Doesn’t Allow Investing?

This is a very common issue. Some employer HSA providers only allow cash or money market accounts and do not offer investment options.

Many people don’t realize this, but you are allowed to have more than one HSA account, and you are allowed to transfer money between HSA accounts with no taxes or penalties.

How to Get the Best of Both Worlds

You can:

Contribute to your employer’s HSA through payroll

Then transfer money to a self-directed HSA (such as Fidelity, Schwab, HealthEquity, etc.)

Invest the money in the self-directed HSA

This strategy allows you to take advantage of the tax benefits of payroll contributions while still having access to investment options.

Why Contribute to Your Employer’s HSA First?

There are two major advantages:

1. Payroll Deduction Convenience

Contributions go directly from your paycheck into the HSA.

2. FICA Tax Savings

If contributions are made through payroll deductions:

You avoid federal tax

You avoid state tax

You avoid FICA tax (Social Security and Medicare tax)

If you contribute to an HSA on your own outside of payroll, you still avoid federal and state tax, but you do NOT avoid FICA tax.

That FICA savings alone can be an additional 7.65% tax savings on contributions.

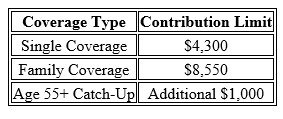

2026 HSA Contribution Limits

HSA contribution limits typically increase each year with inflation. For 2026, the limits are:

These limits include both employee and employer contributions combined.

A Blended Strategy

Some individuals use a combination approach:

Use part of the HSA for current medical expenses

Invest the remainder for retirement healthcare

In these cases, it is usually a good idea to:

Keep enough in cash to cover your deductible and expected medical costs

Invest the remaining balance for long-term growth

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

-

Should I invest my HSA or keep it in cash?If you need the money within a year, keep it in cash. If it's long-term money, investing may make sense.

-

What can I invest in inside an HSA?Many HSAs allow investments in mutual funds, ETFs, and sometimes individual stocks.

-

Can I lose money in an invested HSA?Yes. If invested in the market, the value can go up or down.

-

Can I move my HSA to another provider?Yes, you can transfer HSA funds between providers with no taxes or penalties.

-

Why should I use my employer HSA first?Payroll contributions avoid FICA tax.

-

Can I have two HSA accounts?Yes, as long as total contributions do not exceed annual limits.

-

Is an HSA better than a 401(k)?For medical expenses, an HSA can be more tax-efficient because it can be tax-free on both contributions and withdrawals.

-

When should I stop investing my HSA?Typically when you are getting closer to needing the funds for medical expenses.

-

Can I reimburse myself years later from my HSA?Yes, as long as you kept receipts and the expense occurred after the HSA was opened.

-

What is the biggest advantage of investing an HSA?Tax-free growth and tax-free withdrawals for medical expenses in retirement.