Is $1 Million Enough to Retire? A Practical Income and Longevity Analysis

Pre-retirees can take actionable steps now to strengthen their financial future. Learn essential retirement planning strategies and avoid costly mistakes.

A $1 million retirement portfolio can generate meaningful income, but whether it is enough depends on your spending, longevity, and withdrawal strategy. In many cases, a balanced approach suggests withdrawing around 3% to 4% annually, which translates to $30,000 to $40,000 per year before taxes. At Greenbush Financial Group, our analysis shows that $1 million is often a solid foundation, but rarely a complete solution without additional income sources like Social Security.

How Much Income Can $1 Million Generate in Retirement?

The most common starting point is the safe withdrawal rate, which estimates how much you can withdraw annually without running out of money.

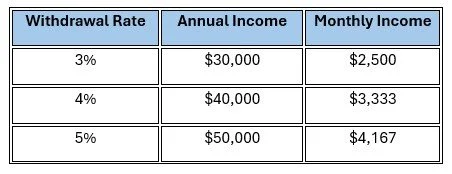

Typical Withdrawal Guidelines

3% withdrawal rate = $30,000 per year

4% withdrawal rate = $40,000 per year

5% withdrawal rate = $50,000 per year (higher risk of depletion)

What This Means in Practice

How Social Security Changes the Equation

For most retirees, Social Security becomes a critical piece of the income plan.

Example Scenario

Portfolio withdrawal (4%) = $40,000

Social Security benefit = $25,000

Total annual income = $65,000

This is where $1 million becomes much more realistic.

Key Insight

Without Social Security, $1 million alone often supports a moderate lifestyle. With Social Security, it can support a comfortable retirement for many households, depending on spending habits.

Inflation: The Silent Risk to Your Retirement Plan

One of the biggest risks retirees face is rising costs over time.

Example

Year 1 expenses = $60,000

20 years later at 3% inflation ≈ $108,000

This is why simply matching your current expenses is not enough. Your income needs to grow over time, which will usually require keeping a portion of your portfolio invested.

At Greenbush Financial Group, we emphasize maintaining a growth component even in retirement portfolios to help offset inflation risk.

How Long Will $1 Million Last?

The longevity of your portfolio depends heavily on:

Withdrawal rate

Investment returns

Market volatility

Lifespan

General Guidelines

3% withdrawal → Often sustainable for 30+ years

4% withdrawal → Historically sustainable, but not guaranteed

5%+ withdrawal → Increased risk of running out of money

Sequence of Returns Risk

Early market downturns in retirement can significantly impact how long your money lasts. This is known as sequence of returns risk, and it is one of the most important planning factors.

What Lifestyle Does $1 Million Support?

The answer varies widely depending on location, spending, and lifestyle expectations.

Likely Scenarios

Modest Lifestyle

Lower cost-of-living area

Limited travel

Paid-off home

Income need: $40,000–$60,000

Moderate Lifestyle

Some travel and discretionary spending

Healthcare costs rising over time

Income need: $60,000–$90,000

High-Spending Lifestyle

Frequent travel, luxury expenses

Higher healthcare and insurance costs

Income need: $100,000+

In many cases, $1 million alone may fall short for higher spending lifestyles without additional income sources.

Tax Considerations on Retirement Income

Not all $40,000 of income is actually spendable.

Key Tax Factors

Traditional IRA/401(k) withdrawals are taxed as ordinary income

Roth IRA withdrawals may be tax-free

Social Security may be partially taxable

Required Minimum Distributions (RMDs) begin in your 70s

At Greenbush Financial Group, tax-efficient withdrawal strategies are often the difference between a plan that works and one that struggles.

Strategies to Make $1 Million Last Longer

There are several ways to improve the sustainability of a $1 million portfolio.

Planning Strategies

Delay Social Security to increase guaranteed income

Use Roth conversions to reduce future taxes

Adjust withdrawals based on market performance

Maintain a diversified portfolio with growth exposure

Reduce fixed expenses before retirement

Real-World Insight

We often see that retirees who remain flexible with spending and withdrawals tend to have significantly better outcomes than those who follow a rigid income plan.

When $1 Million May Not Be Enough

There are specific situations where $1 million may fall short:

Early retirement (before age 62 or 65)

High healthcare costs before Medicare

Significant debt or mortgage payments

High inflation environments

Supporting family members financially

Market downturns and investment mismanagement

In these cases, additional planning becomes critical.

Final Thoughts

A $1 million portfolio can absolutely support retirement, but it is not a one-size-fits-all solution. At Greenbush Financial Group, our analysis shows that success depends on how income is generated, how taxes are managed, and how flexible the retiree is with spending.

For many households, $1 million works best when combined with Social Security and a well-structured withdrawal strategy.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

- Can you retire comfortably with $1 million?Yes, but it depends on your spending level, location, and whether you have additional income like Social Security.

- How much monthly income does $1 million generate?At a 4% withdrawal rate, about $3,300 per month before taxes.

- Is the 4% rule still safe in 2026?It is a useful guideline, but many financial planners now recommend closer to 3% to 4% depending on market conditions.

- What is the safest withdrawal rate for retirement?Around 3% is generally considered more conservative for long retirements.

- How long will $1 million last in retirement?It can last 25 to 30+ years depending on withdrawal rate, investment returns, and market conditions.

Borrowing from Your 401(k)? One Wrong Move Could Trigger a Massive Tax Bill

Borrowing from your 401(k) may seem simple, but one mistake, like leaving your job, can trigger taxes, penalties, and long-term damage to your retirement savings. Understanding the rules before you borrow is critical.

Borrowing from your 401(k) might seem like an easy way to access cash, no credit check, low interest, and you’re paying yourself back. But one wrong move can trigger immediate taxes, penalties, and a permanent hit to your retirement savings. The IRS has strict rules on how 401(k) loans must be repaid and what happens if you leave your job before it’s paid off. Understanding those rules before you borrow can help you avoid costly surprises.

How 401(k) Loans Work

Most employer-sponsored 401(k) plans allow participants to borrow up to the lesser of $50,000 or 50% of their vested balance. Loans typically have to be repaid within five years through automatic payroll deductions, and the interest you pay goes back into your account.

On paper, it looks simple. You’re borrowing from yourself and putting the money back over time. But the biggest risk comes if your employment status, or repayment schedule, changes.

The Costly Mistake: Leaving Your Job Before Repayment

If you leave your employer, voluntarily or otherwise, with an outstanding 401(k) loan, the clock starts ticking. Under IRS rules, you must repay the entire remaining balance by the tax-filing deadline of the following year.

If you don’t repay it in time, the IRS classifies the unpaid balance as a “deemed distribution.” That means:

The outstanding amount is treated as taxable income in that year.

If you’re under age 59½, you’ll also face a 10% early withdrawal penalty.

Example:

If you owe $20,000 on a 401(k) loan when you change jobs and don’t repay it, that $20,000 becomes taxable income. Assuming a 22% federal bracket, you’ll owe $4,400 in federal tax, plus a $2,000 early withdrawal penalty—a total of $6,400 lost instantly.

Our analysis at Greenbush Financial Group shows that many borrowers underestimate this risk, particularly if they expect to switch jobs or retire early.

Why the Real Cost Is Even Higher

Taxes and penalties are only part of the loss. When you default on a 401(k) loan:

You lose future growth on the money permanently removed from your retirement plan.

You can’t simply “rollover” the unpaid balance into an IRA—it’s treated as distributed cash.

In long-term projections, a $20,000 distribution today can mean over $60,000 less in retirement savings 20 years from now, assuming a 7% annual return.

Smart Ways to Borrow Without Derailing Your Retirement

If you’re considering a 401(k) loan, these steps can help minimize the risk:

Understand your plan’s terms. Confirm repayment rules, interest rates, and whether you can continue contributing while repaying the loan.

Have a backup plan. Keep cash reserves or other assets available in case you leave your job unexpectedly.

Avoid borrowing for depreciating expenses. Using retirement funds for short-term needs like vacations or vehicles can compound long-term losses.

Check your employment stability. If you expect to change jobs soon, it’s better to wait or use other financing options.

Compare alternatives. A home equity line of credit (HELOC) or personal loan may cost less in taxes and missed growth over time.

At Greenbush Financial Group, we often help clients run side-by-side projections showing the real long-term cost of borrowing from their 401(k) compared to other options. In most cases, the total impact of lost compounding far outweighs the short-term benefit of easy access to funds.

The Bottom Line

A 401(k) loan can make sense in limited cases, such as paying off high-interest debt or covering an emergency expense when other options are exhausted. But understanding the repayment rules—and the risk of job loss—is critical. One mistake, like leaving your employer before repaying the loan, can trigger thousands in taxes and permanently shrink your retirement balance.

Before taking out a loan, it’s worth modeling different scenarios with a financial planner to ensure your short-term decision doesn’t create a long-term setback.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

FAQs: 401(k) Loan Rules and Risks

-

What’s the maximum I can borrow from my 401(k)?Generally, up to $50,000 or 50% of your vested balance, whichever is less.

-

How long do I have to repay a 401(k) loan?Most plans require repayment within five years, except when borrowing to purchase a primary residence.

-

What happens if I default on my loan?The unpaid balance is treated as a taxable distribution and may incur a 10% early withdrawal penalty if you’re under age 59½.

-

Can I roll my 401(k) loan into an IRA or new employer plan?No, loans cannot be rolled over. The balance must be repaid directly to avoid taxes.

-

Should I ever take a 401(k) loan?Only if the need is critical and you’re confident you’ll remain employed through the repayment period.