Should You Invest Your HSA Account?

Health Savings Accounts can be more than just a tool for current medical expenses. This article explains when it makes sense to invest your HSA, when to keep funds in cash, and how to use an HSA as a long-term retirement strategy. Learn about tax advantages, contribution limits for 2026, and how to transfer funds to investment-friendly HSA providers. Discover how to maximize tax-free growth for future healthcare costs.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Health Savings Accounts (HSAs) are a valuable tool that allow individuals to use pre-tax dollars to pay for qualified medical expenses. But there is also a more advanced planning strategy that many people are not aware of — using an HSA as a long-term investment account for future healthcare costs, especially in retirement when healthcare expenses are typically at their highest.

So the question becomes: If you’re not planning to spend your HSA money this year, should you invest it so it grows over time?

In this article, we’ll cover:

When it makes sense to invest your HSA

When you should keep HSA funds in cash

What to do if your employer HSA doesn’t allow investing

How HSA transfers work

The tax advantages of investing an HSA

2026 HSA contribution limits

Frequently asked questions about investing HSAs

The Long-Term HSA Strategy

Many people use their HSA to pay for current medical expenses. But another strategy is to:

Contribute to an HSA each year

Do NOT spend the HSA

Pay current medical expenses out-of-pocket

Allow the HSA to grow over time

Use the HSA later in retirement for healthcare expenses

This strategy can be powerful because:

Contributions are pre-tax

Growth is tax-deferred

Withdrawals are tax-free for qualified medical expenses

This makes the HSA one of the only accounts that can be tax-free on the way in and tax-free on the way out when used correctly.

Should You Invest Your HSA?

In general, if the money in your HSA is not going to be used within the next year, it can often make sense to invest those funds so they can grow over time.

This is especially true for individuals who:

Are 10+ years away from retirement

Can afford to pay current medical expenses out-of-pocket

Want to build a retirement healthcare fund

By investing the HSA, you are not only getting the tax deduction on the contribution, but you are also getting tax-free growth on the investments if used for qualified medical expenses later.

When You Should NOT Invest Your HSA

If you are using your HSA for current or short-term medical expenses, it usually makes sense to keep that portion in cash or a money market account.

A common strategy is to split the HSA into two buckets:

Short-term medical expenses → Keep in cash

Long-term retirement healthcare → Invest for growth

This way, you maintain stability for current expenses while still allowing long-term funds to grow.

What If Your Employer’s HSA Doesn’t Allow Investing?

This is a very common issue. Some employer HSA providers only allow cash or money market accounts and do not offer investment options.

Many people don’t realize this, but you are allowed to have more than one HSA account, and you are allowed to transfer money between HSA accounts with no taxes or penalties.

How to Get the Best of Both Worlds

You can:

Contribute to your employer’s HSA through payroll

Then transfer money to a self-directed HSA (such as Fidelity, Schwab, HealthEquity, etc.)

Invest the money in the self-directed HSA

This strategy allows you to take advantage of the tax benefits of payroll contributions while still having access to investment options.

Why Contribute to Your Employer’s HSA First?

There are two major advantages:

1. Payroll Deduction Convenience

Contributions go directly from your paycheck into the HSA.

2. FICA Tax Savings

If contributions are made through payroll deductions:

You avoid federal tax

You avoid state tax

You avoid FICA tax (Social Security and Medicare tax)

If you contribute to an HSA on your own outside of payroll, you still avoid federal and state tax, but you do NOT avoid FICA tax.

That FICA savings alone can be an additional 7.65% tax savings on contributions.

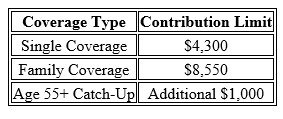

2026 HSA Contribution Limits

HSA contribution limits typically increase each year with inflation. For 2026, the limits are:

These limits include both employee and employer contributions combined.

A Blended Strategy

Some individuals use a combination approach:

Use part of the HSA for current medical expenses

Invest the remainder for retirement healthcare

In these cases, it is usually a good idea to:

Keep enough in cash to cover your deductible and expected medical costs

Invest the remaining balance for long-term growth

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

-

Should I invest my HSA or keep it in cash?If you need the money within a year, keep it in cash. If it's long-term money, investing may make sense.

-

What can I invest in inside an HSA?Many HSAs allow investments in mutual funds, ETFs, and sometimes individual stocks.

-

Can I lose money in an invested HSA?Yes. If invested in the market, the value can go up or down.

-

Can I move my HSA to another provider?Yes, you can transfer HSA funds between providers with no taxes or penalties.

-

Why should I use my employer HSA first?Payroll contributions avoid FICA tax.

-

Can I have two HSA accounts?Yes, as long as total contributions do not exceed annual limits.

-

Is an HSA better than a 401(k)?For medical expenses, an HSA can be more tax-efficient because it can be tax-free on both contributions and withdrawals.

-

When should I stop investing my HSA?Typically when you are getting closer to needing the funds for medical expenses.

-

Can I reimburse myself years later from my HSA?Yes, as long as you kept receipts and the expense occurred after the HSA was opened.

-

What is the biggest advantage of investing an HSA?Tax-free growth and tax-free withdrawals for medical expenses in retirement.

5 Must-Read Financial Books to Build Wealth and Success at Any Stage of Life

Looking to build wealth and sharpen your money skills? Greenbush Financial Group highlights 5 must-read financial books that cover debt, investing, business strategy, and long-term success. Perfect for every stage of life.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Knowledge is power—especially when it comes to money. The earlier you learn the fundamentals of personal finance and business, the faster you can avoid mistakes and build wealth compared to your peers. But whether you’re just starting out in your career, navigating mid-life financial challenges, or planning for retirement, the right financial knowledge can create opportunities and help you achieve greater freedom.

As the Managing Partner of Greenbush Financial Group, I often recommend books as a way to jump-start that education. The right book can provide not only financial strategies but also the mindset shifts needed to succeed both personally and professionally. Below are five must-read books that cover everything from managing debt to investing to starting a business:

The Total Money Makeover by Dave Ramsey

How to Win Friends and Influence People by Dale Carnegie

Rich Dad Poor Dad by Robert Kiyosaki

Blue Ocean Strategy by W. Chan Kim and Renée Mauborgne

One Up on Wall Street by Peter Lynch

1. The Total Money Makeover by Dave Ramsey

For individuals who find themselves weighed down by student loans, credit card balances, or car payments, this book is the perfect starting point. Ramsey lays out a proven system—his famous “baby steps”—to help readers eliminate debt, build an emergency fund, and begin saving for the future. His approach is straightforward, no-nonsense, and centered on living a debt-free lifestyle.

Key Lessons:

Start with a written budget and tell every dollar where to go.

Attack debt with the “debt snowball” method—paying off the smallest balances first.

Build an emergency fund to protect against unexpected expenses.

Avoid credit cards and debt as a lifestyle—cash is freedom.

Live below your means to create margin for saving and investing.

2. How to Win Friends and Influence People by Dale Carnegie

Originally published in 1936, this timeless classic focuses on building strong relationships—a skill just as valuable in business as it is in everyday life. Carnegie teaches that success often depends more on how you treat people than on technical expertise. For anyone looking to grow their career, improve leadership skills, or strengthen communication, this book remains one of the best guides available.

Key Lessons:

Don’t criticize, condemn, or complain—lead with kindness.

Give honest and sincere appreciation—people thrive on recognition.

Become genuinely interested in others, and remember their names.

Avoid arguments—approach conversations with warmth and curiosity.

Let others feel ownership of ideas—collaboration builds stronger outcomes.

3. Rich Dad Poor Dad by Robert Kiyosaki

This book reshapes the way many people think about money. Through the contrast of his “rich dad” and “poor dad,” Kiyosaki explains why building assets and investing are essential, while relying solely on a paycheck can limit financial growth. The book highlights the benefits of owning a business or investing in income-producing assets versus being stuck in the cycle of working for money.

Key Lessons:

Assets put money in your pocket, liabilities take it out—know the difference.

Don’t work only for money—learn how money works and put it to work for you.

Entrepreneurship and investing create wealth faster than wages.

Financial education is more important than formal education.

Take calculated risks instead of seeking complete security.

4. Blue Ocean Strategy by W. Chan Kim and Renée Mauborgne

For those who aspire to start their own business, this book is essential. The authors explain how companies can break away from crowded, competitive “red oceans” and instead create innovative products or services in uncontested “blue oceans.” This strategy allows entrepreneurs to differentiate themselves, grow faster, and avoid the race-to-the-bottom competition.

Key Lessons:

Don’t compete in crowded markets—create new market space.

Focus on differentiation and value innovation, not price wars.

Eliminate what doesn’t add value, and elevate what customers truly care about.

Small, creative ideas can disrupt entire industries.

Long-term success comes from standing apart, not blending in.

5. One Up on Wall Street by Peter Lynch

Originally published in 1989, this classic investment book remains one of the most practical guides for everyday investors. Lynch, one of the most successful mutual fund managers of all time, explains how average people can use their everyday knowledge—like the products they buy and the companies they interact with—to make smart investment decisions. While the markets have evolved since the book’s release, the core principles remain timeless.

Key Lessons:

Invest in what you know—your everyday life can reveal great companies.

Do your own research before following Wall Street trends.

Long-term investing beats short-term speculation.

A simple, understandable company is often a better investment than a complex one.

Patience and discipline are critical—ignore market noise.

Final Thoughts

Each of these books delivers valuable lessons that can change the way you approach money, career, and business. From getting out of debt, to building stronger relationships, to launching innovative companies, these resources provide a roadmap to success.

No matter your stage of life or career, pick the book that speaks most to your current situation and commit to applying what you learn. Over time, the habits and strategies you gain will compound, setting you apart and positioning you for long-term wealth.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

Why is financial education so important?

Financial knowledge helps individuals make informed decisions about saving, investing, and managing debt. The earlier you learn core principles, the more effectively you can avoid mistakes, build wealth, and create financial independence over time.

What are the best books to start learning about personal finance?

Books like The Total Money Makeover by Dave Ramsey, Rich Dad Poor Dad by Robert Kiyosaki, and One Up on Wall Street by Peter Lynch offer practical guidance on budgeting, investing, and building long-term wealth. Each provides actionable strategies for different stages of life.

How can The Total Money Makeover help with debt management?

Dave Ramsey’s book focuses on eliminating debt through a structured “baby steps” plan. It teaches readers to live on a budget, build an emergency fund, and use the “debt snowball” method to gain momentum toward financial freedom.

What’s the main takeaway from Rich Dad Poor Dad?

The book emphasizes that wealth comes from owning assets and understanding how money works, not just earning a paycheck. It encourages entrepreneurship, investing, and financial education as the keys to long-term success.

Why is How to Win Friends and Influence People valuable for financial success?

Success in business and personal finance often depends on relationships and communication. Dale Carnegie’s classic teaches principles of empathy, influence, and connection that are vital for leadership, networking, and negotiation.

Who should read Blue Ocean Strategy?

Aspiring entrepreneurs and business leaders can benefit from this book’s insights on creating new markets instead of competing in saturated ones. It provides a framework for innovation, differentiation, and long-term growth.

What investing lessons does One Up on Wall Street teach?

Peter Lynch shows that everyday investors can identify great opportunities by observing products and companies they already know. His approach focuses on patience, research, and long-term investing rather than short-term speculation.