Should You Spend or Save Your HSA Account?

Health Savings Accounts offer a unique triple tax advantage, making them one of the most powerful retirement planning tools available. This article explains when to spend versus save your HSA, how to invest it for long-term growth, and how it can be used for healthcare costs in retirement. You’ll also learn the 2026 HSA contribution limits and strategies to maximize your account’s value. Understanding how to use your HSA properly can significantly improve retirement income planning and reduce future medical expenses.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Health Savings Accounts (HSAs) are one of the most tax-advantaged accounts available, yet many people still wonder whether they should use the HSA now for medical expenses or save it for retirement. The answer depends on your financial situation, but in many cases, saving your HSA for the future can provide significant long-term benefits.

In this article, you’ll learn:

How HSAs receive triple tax advantages

When it makes sense to spend vs. save your HSA

How HSAs can be used for healthcare expenses in retirement

Why investing your HSA can dramatically increase its value

2026 HSA contribution limits

A real-life example showing long-term HSA growth

A hybrid strategy that works for many households

Understanding the Triple Tax Advantage of an HSA

HSAs are unique because they offer what is often called a triple tax benefit:

Contributions are made pre-tax

The money grows tax-deferred

Withdrawals are tax-free if used for qualified medical expenses

Very few accounts offer this type of tax treatment. Traditional retirement accounts are tax-deferred, Roth accounts are tax-free on withdrawal, but HSAs offer both benefits — which is why many financial planners consider HSAs one of the most powerful long-term savings tools available.

Should You Spend or Save Your HSA?

The original purpose of an HSA was to pay for current medical expenses with pre-tax dollars. However, a larger planning opportunity exists:

If you can afford to pay medical expenses out-of-pocket today, it may make sense to leave your HSA invested and growing for retirement.

Why? Because healthcare costs tend to increase significantly as we age, especially in retirement. Having a dedicated account for healthcare expenses reduces the risk that large medical costs will disrupt your retirement income plan.

What Can HSAs Be Used for in Retirement?

Many people don’t realize how many retirement healthcare expenses can be paid from an HSA, including:

Medicare Part B premiums

Medicare Part D premiums

Medicare Advantage premiums

Dental expenses

Vision expenses

Hearing aids

Long-term care insurance premiums (within limits)

Medical equipment (wheelchairs, walkers, etc.)

Deductibles and copays

Prescription medications

Because these expenses can be paid tax-free from an HSA, it effectively makes those healthcare costs tax deductible in retirement.

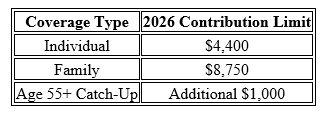

2026 HSA Contribution Limits

For 2026, the IRS increased HSA contribution limits:

These limits include both employee and employer contributions combined.

The Power of Investing Your HSA

If you plan to use your HSA more than 5 years in the future, it often makes sense to invest the HSA rather than leaving it in cash or a money market account. The reason is simple: compound interest.

Example:

If you are age 40, contribute $4,000 per year, and earn 8% annually, by age 62 your HSA could grow to approximately:

Total account value: $243,000

Total contributions: $92,000

Investment growth: $151,000

In this example, most of the account value came from investment growth, not contributions. That is the real power of using an HSA as a long-term healthcare investment account.

Not All HSA Providers Allow Investing

Some HSAs only allow cash savings, while others allow full investment access similar to a retirement account. Some popular HSA providers that offer investment options include:

Fidelity Investments

Charles Schwab

HealthEquity

If your HSA is through your employer, it often makes sense to:

Contribute through payroll to capture tax benefits

Then periodically transfer funds to an HSA provider with investment options

This strategy allows you to get the best of both worlds — tax savings and investment growth.

A Hybrid Strategy May Work Best

Not everyone can afford to pay medical expenses out-of-pocket. That’s where a hybrid strategy can work well:

Use your HSA for large medical expenses

Pay smaller expenses out-of-pocket when possible

Try to preserve and invest as much of the HSA as possible for retirement

This approach balances current needs with long-term planning.

Final Thoughts

Healthcare is one of the largest expenses in retirement. Having a dedicated, tax-free account to pay for those costs can significantly improve retirement security. For many individuals, the HSA becomes less of a short-term spending account and more of a long-term healthcare retirement account.

If used strategically, an HSA can become a healthcare safety net, helping reduce the financial risk of rising medical costs later in life.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

-

Should I max out my HSA every year?If you can afford to, many financial planners recommend maxing out your HSA due to the triple tax advantage.

-

Is an HSA better than a 401(k)?They serve different purposes, but an HSA often has better tax treatment if used for medical expenses.

-

Can I use my HSA for Medicare premiums?Yes, you can use HSA funds for Medicare Part B, Part D, and Medicare Advantage premiums.

-

Can I invest my HSA?Yes, but only if your HSA provider allows investment options.

-

What happens if I use HSA money for non-medical expenses?Before age 65, you pay income tax plus a 20% penalty. After age 65, you only pay income tax.

-

Do HSA funds expire?No. HSA funds roll over every year and stay with you for life.

-

Can I reimburse myself later for medical expenses?Yes. As long as you kept the receipt, you can reimburse yourself years later.

-

Should I invest my HSA or keep it in cash?If the money won't be used for several years, investing often makes sense due to compound growth.

-

Can I have more than one HSA account?Yes. You can contribute to one and transfer to another.

-

What is the biggest benefit of an HSA?The triple tax advantage: pre-tax contributions, tax-deferred growth, and tax-free withdrawals for medical expenses.