Understanding the Order of Withdrawals In Retirement

The order in which you withdraw money in retirement can make a huge difference in how long your savings last—and how much tax you pay. In this article, we break down a smart withdrawal strategy to help retirees and pre-retirees keep more of their hard-earned money.

When entering retirement, one of the most important financial questions you’ll face is: What’s the smartest order to pull funds from my various retirement accounts? Getting this order wrong can lead to unnecessary taxes, reduced portfolio longevity, and even higher Medicare premiums.

While there’s no universal rule that fits everyone, there are strategic guidelines that can help most retirees withdraw more efficiently and keep more of what they’ve saved.

1. Use Tax-Deferred Accounts (Traditional IRA / 401(k))

For clients who have both after-tax brokerage accounts or cash reserves as well as pre-tax retirement accounts, they are often surprised to find out that there are large tax advantages to taking distributions from pre-tax retirement accounts in the early years of retirement. Since all Traditional IRA and 401(k) distributions are taxed, retirees unknowingly will fully deplete their after-tax sources before turning to their pre-tax retirement accounts.

I’ll explain why this is a mistake.

When most individuals retire, their paychecks stop, and they may, tax-wise, find themselves in low to medium tax brackets. Knowing they are in low to medium tax brackets, by not taking distributions from pre-tax retirement accounts, a retiree could be wasting those low-bracket years.

For example, Scott and Kelly just retired. Prior to retirement their combine income was $300,000. Scott and Kelly have a cash reserve of $100,000, an after tax brokerage account with $250,000, and Traditional IRA’s totaling $800,000. Since their only fixed income source in retirement is their social security benefits totaling $60,000, if they need an additional $20,000 per year to meet their annual expenses, it may make sense for them to withdrawal that money from their Traditional IRAs as opposed to their cash reserve or brokerage account.

Reason 1: For a married couple filing a joint tax return, the 12% Federal tax bracket caps out at $96,000, that is relatively low tax rate. If they need $20,000 after tax to meet their expenses, they could gross up their IRA distribution to cover the 12% Fed Tax and withdrawal $22,727 from their IRA’s and still be in the 12% Fed bracket.

Reason 2: If they don't take withdrawals from their pretax retirement accounts, those account balances will keep growing, and at age 75, Scott and Kelly will be required to take RMD’s from their pre-tax retirement account, and those RMDs could be very large pushing them into the 22% Fed tax bracket.

Reason 3: For states like New York that have state income tax, depending on the state you live in, they may provide an annual state tax exemption for a certain amount of distributions from pre-tax retirement accounts each year. In New York, the state does not tax the first $20,000 EACH YEAR withdrawn from pre-tax retirement accounts. By not taking distributions in their early years and retirement, a retiree may be wasting that annual $20,000 New York state exemption, making a larger portion of their IRA distribution subject to state tax in the future.

For client who have both pre-tax retirement accounts and after-tax brokerage accounts, it can sometimes be a blend of the two, depending on how much money they need to meet their expenses. It could be that the first $20,000 comes from their Traditional IRA to keep them in the low tax bracket, but the remainder comes from their brokerage account. It varies on a case-by-case basis.

2. After-Tax Brokerage Accounts and Cash Reserve (Brokerage)

For individuals who retire after age 59 ½, the distribution strategy usually involves a blend of pre-tax retirement account distributions and distributions from after-tax brokerage accounts. When selling holdings in a brokerage account to raise cash for distributions, retirees have to be selective as to which holdings they sell. Selling holdings that have appreciated significantly in value could trigger large capital gains, adding to their taxable income in the retirement years. But there are typically holdings that may either have minimal gains that could be sold with very little tax impact or holding that have long-term capital gains treatment taxed at a flat 15% federal rate. Since every dollar is taxed coming out of a pre-tax retirement account, having after-tax cash or a brokerage account can sometimes allow a retiree to pick their tax bracket from year to year.

There is often an exception for individuals that retire prior to age 59½ or in some cases prior to age 65. In these cases, taking withdrawals from after-tax sources may be the primary objective. For individual under the age of 59 1/2 , if distributions are taken from a Traditional IRA prior to age 59 1/2, the individual faced taxation and a 10% early withdrawal penalty.

Note: There are some exceptions for 401(k) distributions after age 55 but prior to age 59 1/2.

For individuals who retire prior to age 65 and do not have access to retiree health benefits, they frequently have to obtain their insurance coverage through the state exchange, which has income subsidies available. Meaning the less income an individual shows, the less they have to pay out of pocket for their health insurance coverage. Taking taxable distributions from pre-tax retirement accounts could potentially raise their income, forcing them to pay more for their health insurance coverage. If instead they take distributions from after-tax sources, they could potentially receive very good health insurance coverage for little to no cost.

3. Save Roth IRA Funds for Last

Roth IRAs grow tax-free and offer tax-free withdrawals in retirement. Because they don’t have RMDs and don’t increase your taxable income, Roth IRAs are ideal for later in retirement, or even as a legacy asset to pass on to heirs. To learn more about creating generational wealth with Roth Conversions, watch this video.

Keeping your Roth untouched early in retirement also gives you flexibility in higher-income years. Need to take a larger withdrawal to fund a home project or major expense? Roth distributions won’t impact your tax bracket or Medicare premiums.

4. Special Considerations

Health Savings Accounts (HSAs):

If you have a balance in an HSA, use it for qualified medical expenses tax-free. These can be especially valuable in later years as healthcare costs increase.

Social Security Timing:

Delaying Social Security can reduce taxable income in early retirement, opening the door for Roth conversions and other tax strategies.

Sequence of Return Risk:

Withdrawing from the wrong accounts during a market downturn can permanently damage your portfolio. Diversifying your income sources can reduce that risk.

5. Avoid These Common Withdrawal Mistakes

Triggering higher Medicare premiums (IRMAA): Large withdrawals can push your income over thresholds that increase Medicare Part B and D premiums.

Missing Roth Conversion Opportunities: Processing Roth conversions to take advantage of low tax brackets and reduce future RMDs.

Tapping after-tax accounts too early: Maintaining a balance in a brokerage account can provide more tax flexibility in future years, and when it comes to estate planning these asset receive a step-up in cost basis before passing to your beneficiaries.

Final Thoughts

The order you withdraw your funds in retirement can significantly affect your taxes, benefits, and long-term financial security. A smart strategy blends tax awareness, income needs, and market conditions.

Every retiree’s situation is unique and working with a financial planner who understands the coordination of retirement income can help you keep more of your wealth and make it last longer.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What is the best order to withdraw funds from retirement accounts?

The “best” withdrawal strategy truly varies from person to person. A common mistake retirees make is fully retiring and withdrawing money first from after-tax sources, then, once depleted, from pre-tax sources. Depending on the types of investment accounts someone has and their income needs, a blended approach can often be ideal.

Why might it make sense to take IRA withdrawals early in retirement?

Early retirement years often come with lower taxable income, allowing retirees to withdraw from pre-tax accounts at favorable tax rates. Doing so can reduce the size of future RMDs and help avoid being pushed into higher tax brackets later in life.

How do after-tax brokerage accounts fit into a retirement income strategy?

After-tax brokerage accounts offer flexibility since withdrawals are not fully taxable—only gains are. They can help retirees manage their tax brackets from year to year, especially when balancing withdrawals from pre-tax and Roth accounts.

When should retirees use Roth IRA funds?

Roth IRAs are typically best reserved for later in retirement because withdrawals are tax-free and don’t affect Medicare premiums or tax brackets. They also have no required minimum distributions, making them valuable for legacy or estate planning.

How can withdrawal timing affect Medicare premiums?

Large distributions from pre-tax accounts can raise your income and trigger higher Medicare Part B and D premiums through the Income-Related Monthly Adjustment Amount (IRMAA). Spreading withdrawals over multiple years or using Roth funds strategically can help avoid these surcharges.

What are common mistakes to avoid when withdrawing retirement funds?

Common pitfalls include depleting after-tax accounts too early, missing Roth conversion opportunities, or taking large taxable withdrawals that increase Medicare costs. Coordinating withdrawals with tax brackets and healthcare needs can help prevent these costly errors.

How does delaying Social Security affect retirement withdrawal strategy?

Delaying Social Security reduces taxable income in early retirement, which can open opportunities for Roth conversions or strategic IRA withdrawals. Once benefits begin, managing income sources carefully helps minimize taxes and maximize long-term income.

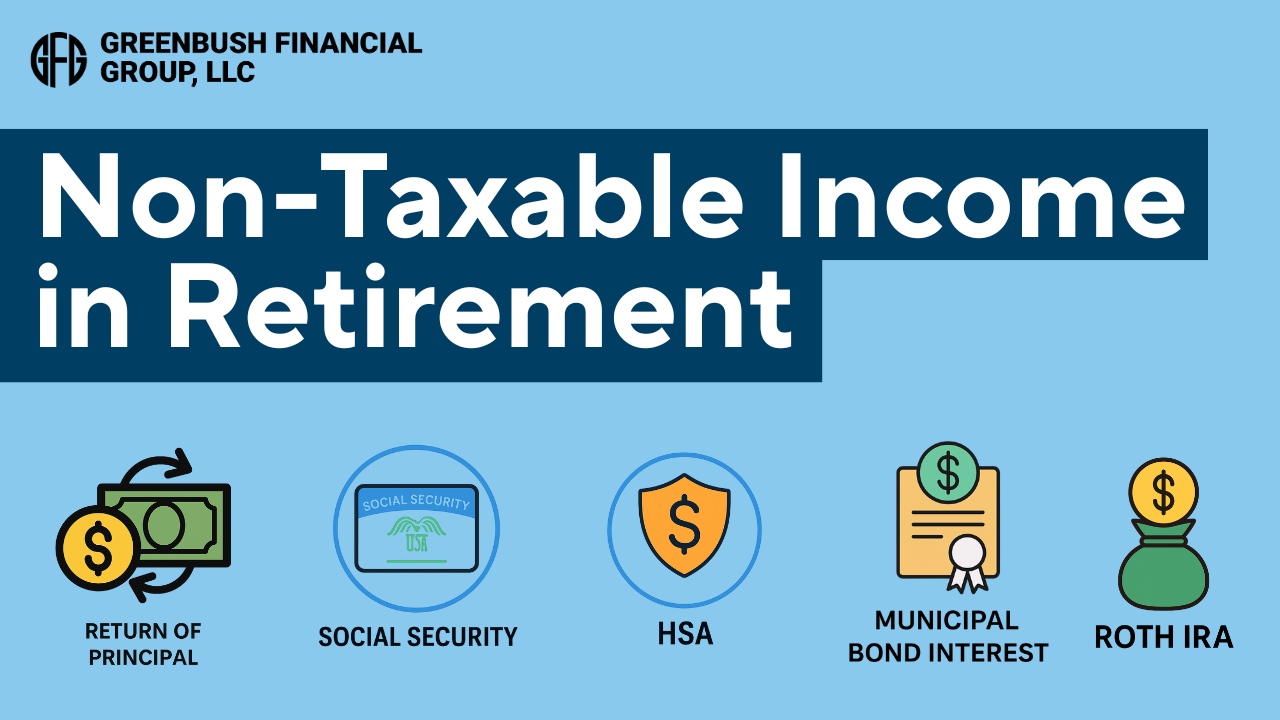

Non-Taxable Income in Retirement: 5 Sources You Should Know About

When it comes to retirement income, not all dollars are created equal. Some income sources are fully taxable, others partially — but a select few can be completely tax-free. And understanding the difference could mean thousands of dollars in savings each year.

When it comes to retirement income, not all dollars are treated equally. Some are fully taxable, others partially taxable, and a select few are entirely tax-free. Understanding the difference is critical to building a retirement income plan that protects your nest egg from unnecessary taxation, especially in a high-inflation, high-cost-of-living environment.

In this article, we break down five sources of non-taxable income in retirement, how they work, and how to strategically use them to lower your tax bill and preserve long-term wealth.

1. Roth IRA Withdrawals

A Roth IRA offers one of the most powerful tax benefits available to retirees — tax-free growth and qualified tax-free withdrawals.

To qualify, withdrawals must occur after age 59½ and at least five years after your first contribution or Roth conversion. If both conditions are met, all distributions (contributions and growth) are 100% tax-free.

Why it matters:

Withdrawals from pre-tax retirement accounts like Traditional IRAs and 401(k)s are taxed as ordinary income, which can push you into a higher tax bracket, increase Medicare premiums, and reduce the portion of your Social Security benefits that are tax-free. With Roth IRAs, none of those problems exist.

Planning strategy:

Many retirees choose to complete Roth conversions during low-income years (such as early retirement) to move pre-tax funds into a Roth IRA while controlling their tax rate. This allows them to create a future pool of tax-free income while reducing Required Minimum Distributions (RMDs) down the line.

2. Health Savings Account (HSA) Distributions for Medical Expenses

HSAs are the only account type that offers triple tax advantages:

Contributions are tax-deductible

Growth is tax-deferred

Withdrawals are tax-free if used for qualified medical expenses

Qualified expenses include Medicare premiums, prescriptions, dental and vision care, long-term care insurance premiums (subject to limits), and more.

Why it matters:

Healthcare is often one of the largest expenses in retirement, and using HSA funds tax-free for these costs allows retirees to preserve their other taxable accounts.

Planning strategy:

For clients who are still working and enrolled in a high-deductible health plan, the strategy may be to contribute the maximum amount to an HSA and pay current medical expenses out-of-pocket. This allows the HSA to grow and be used as a supplemental retirement account for tax-free medical reimbursements later in life.

3. Social Security (Partially Non-Taxable)

Up to 85% of Social Security benefits can be taxable at the federal level, depending on your provisional income (which includes half of your Social Security benefits, taxable income, and tax-exempt interest).

However, if a retiree has very little income other than their social security, it’s possible that they may not pay any tax on their social security benefits.

Why it matters:

Retirees who rely heavily on Roth IRA withdrawals or return of principal from brokerage accounts may be able to keep their provisional income low enough to shield some or all of their Social Security benefits from taxation.

Planning strategy:

By building a tax-efficient distribution plan in retirement, retirees can often reduce the amount of tax paid on their Social Security benefits and improve net income in retirement.

4. Municipal Bond Interest

Interest from municipal bonds is generally exempt from federal income tax. If you reside in the state where the bond was issued, that interest may also be exempt from state and local taxes.

Why it matters:

For retirees in high tax brackets, municipal bonds can provide steady, tax-advantaged income without adding to provisional income or triggering taxes on Social Security.

Planning strategy:

Retirees in high-income tax brackets may hold municipal bonds in taxable brokerage accounts, while keeping higher-yield taxable bonds inside IRAs or 401(k)s where the interest won’t be taxed annually.

5. Return of Principal from Non-Retirement Accounts

Withdrawals from taxable brokerage accounts can be structured to return your cost basis first, which is not subject to tax. Only the gains portion of a sale is subject to capital gains tax — and long-term capital gains may be taxed at 0% if your taxable income is below certain thresholds.

Why it matters:

This allows retirees to tap into their investments in a low-tax or no-tax manner — especially when drawing from principal rather than interest, dividends, or gains.

Planning strategy:

Coordinate asset sales to manage taxable gains, and consider drawing from principal early in retirement to reduce future RMDs or pay the tax liability generated by Roth conversions in lower-income years.

Final Thoughts: Build a Tax-Efficient Retirement Income Plan

Most retirees understand the importance of investment performance, but few give the same attention to tax efficiency, even though taxes can quietly erode thousands of dollars in retirement income each year.

By blending these non-taxable income sources into your withdrawal strategy, you can:

Reduce your tax liability

Lower Medicare surcharges

Improve portfolio longevity

Increase the amount of inheritance passed to the next generation

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What types of retirement income are tax-free?

Common sources of tax-free retirement income include qualified Roth IRA withdrawals, Health Savings Account (HSA) distributions for medical expenses, a portion of Social Security benefits, municipal bond interest, and the return of principal from non-retirement investments. These sources can help retirees reduce overall taxable income and extend portfolio longevity.

Why are Roth IRA withdrawals tax-free in retirement?

Roth IRA withdrawals are tax-free if you’re over age 59½ and the account has been open for at least five years. Because Roth withdrawals don’t count toward taxable income, they won’t increase your tax bracket, affect Medicare premiums, or reduce the tax-free portion of your Social Security benefits.

How can a Health Savings Account (HSA) provide tax-free income in retirement?

HSAs offer triple tax advantages: contributions are tax-deductible, growth is tax-deferred, and withdrawals are tax-free for qualified medical expenses. Retirees can use HSA funds to pay for Medicare premiums, prescriptions, and other healthcare costs without generating taxable income.

Are Social Security benefits always taxable?

No. Depending on your provisional income, up to 85% of Social Security benefits may be taxable, but some retirees owe no tax on their benefits. Keeping taxable income low through Roth withdrawals or return of principal from brokerage accounts can help reduce or eliminate Social Security taxation.

How are municipal bond earnings taxed?

Interest earned from municipal bonds is typically exempt from federal income tax and, if the bonds are issued by your home state, may also be exempt from state and local taxes. This makes municipal bonds a valuable source of tax-advantaged income for retirees in higher tax brackets.

What does “return of principal” mean for taxable accounts?

When you sell investments in a taxable brokerage account, the portion representing your original cost basis is considered a return of principal and isn’t taxed. Only the gains portion is subject to capital gains tax, which may be as low as 0% for retirees in lower income brackets.

How can retirees use non-taxable income to improve their financial plan?

Strategically blending tax-free and taxable income sources can lower your overall tax burden, reduce Medicare surcharges, and improve long-term portfolio sustainability. This approach helps preserve wealth and increase the amount that can ultimately be passed to heirs.