When One Social Security Check Disappears: What Retired Couples Need to Plan For

Many couples plan carefully for retirement together but overlook the financial realities of retirement alone. Learn how survivor Social Security benefits, taxes, healthcare costs, and estate planning can impact a surviving spouse.

Many married couples plan carefully for retirement together but spend very little time preparing for the financial realities of retirement alone. When one spouse dies, income may drop faster than expenses, taxes can increase, and important financial decisions suddenly fall on one person. Understanding survivor Social Security rules, tax changes, healthcare costs, and estate planning issues can help protect the surviving spouse financially and emotionally. At Greenbush Financial Group, we often find that the best survivor planning happens before a crisis occurs.

Most Couples Plan for Retirement Together—But Not for Retirement Alone

Many retired couples assume that if one spouse dies, household expenses simply get cut in half.

In reality, that rarely happens.

When one spouse passes away:

One Social Security check may disappear

Taxes may increase

Healthcare costs may remain high

Housing costs often stay similar

One person may suddenly manage all financial decisions alone

At the same time, the surviving spouse may also be dealing with grief, paperwork, legal decisions, and emotional stress.

This is why survivor planning is one of the most important and overlooked parts of retirement planning.

The goal is not to think pessimistically.

The goal is making sure either spouse could continue forward financially with clarity and confidence.

What Financially Changes When One Spouse Dies?

Several important financial changes can happen almost immediately after a spouse passes away.

Social Security Income Often Drops

This is one of the biggest surprises for many couples.

When both spouses are receiving Social Security, one benefit usually disappears after the first death.

The surviving spouse generally keeps:

Their own benefit

Or the higher of the two benefits

But not both full checks.

Example

John receives:

$3,200/month from Social Security

Susan receives:

$2,100/month

Combined household income:

$5,300/month

After John dies, Susan may keep the larger $3,200 benefit, but the smaller benefit disappears.

Household Social Security income drops by:

$2,100/month

Or more than $25,000 annually

Meanwhile, many expenses continue.

Expenses Often Do NOT Drop by 50%

This is one of the most important retirement realities couples should understand.

Certain expenses may decrease modestly:

Food

Travel

Clothing

Some healthcare expenses

But many major costs remain similar:

Property taxes

Utilities

Insurance

Home maintenance

Car expenses

Healthcare premiums

In many cases, household expenses may only decline by 20%–30% while income drops significantly more.

That gap can create financial pressure for surviving spouses.

Why Surviving Spouses Often Pay Higher Taxes

This surprises many retirees.

After one spouse dies, the surviving spouse usually transitions from:

Married Filing Jointly

to:Single tax filing status

That change can happen quickly.

The problem is that single tax brackets are less favorable at lower income levels.

This means surviving spouses may pay higher taxes even if household income decreases.

The Survivor Tax Trap

A surviving spouse may face:

Similar IRA balances

Similar investment income

Similar Required Minimum Distributions (RMDs)

But now with:

Less favorable tax brackets

One standard deduction instead of two

Potentially higher Medicare premiums

Example

A married couple may comfortably remain in the 22% bracket while filing jointly.

After one spouse dies, the survivor could move into higher effective tax exposure as a single filer with nearly the same retirement account balances.

This is one reason Roth conversion planning during joint lifetimes can become extremely valuable.

Why Roth Conversions Can Matter More Than Couples Realize

Many couples focus only on their current taxes.

But survivor planning often changes the equation.

Converting portions of traditional IRAs to Roth IRAs while both spouses are alive may help:

Reduce future RMDs

Lower future survivor tax exposure

Create tax-free withdrawal flexibility

Improve long-term tax diversification

Example

A retired couple in their mid-60s delays Social Security and intentionally converts moderate IRA amounts annually while remaining within a manageable tax bracket.

Years later, if one spouse dies, the surviving spouse may have:

Smaller RMDs

More Roth flexibility

Lower taxable income

Better control over Medicare premium exposure

The key is evaluating these opportunities before tax brackets potentially tighten later.

Pension Survivor Decisions Matter More Than Many Couples Realize

Some pensions offer choices such as:

Single-life payout

Joint-and-survivor payout

Reduced survivor benefits

Many retirees choose larger monthly income initially without fully understanding how survivor income changes later.

Important Question

If one spouse dies:

Will pension income continue?

Reduce?

Or disappear entirely?

These decisions are often permanent once retirement begins.

Healthcare and Long-Term Care Planning Become More Important

Healthcare planning can become more difficult for surviving spouses because:

One spouse may eventually need care alone

Adult children may live far away

Financial management responsibilities may suddenly shift

Couples should discuss:

Long-term care preferences

Healthcare directives

Emergency contacts

Account access

Caregiving expectations

These conversations are uncomfortable for many families, but avoiding them often creates more stress later.

One of the Biggest Risks: Only One Spouse Understands the Finances

In many households, one spouse handles:

Investments

Taxes

Bills

Insurance

Account logins

Estate planning

That may work fine until something unexpected happens.

Then the surviving spouse may suddenly feel overwhelmed managing decisions they were never involved in previously.

Important Step

Both spouses should understand:

Where accounts are located

How income is generated

Who to contact for help

How bills are paid

What the retirement income plan looks like

Financial organization itself can become a form of protection.

Beneficiary Mistakes Can Create Major Problems

Many retirement accounts pass through beneficiary designations rather than wills.

Outdated beneficiaries can create unintended outcomes.

Common issues include:

Ex-spouses still listed

Missing contingent beneficiaries

Unequal inheritance structures

Children added improperly to accounts

Retirement transitions are a good time to review:

IRA beneficiaries

Roth IRA beneficiaries

Life insurance

Transfer-on-death accounts

Trust coordination

A Real-World Survivor Planning Example

David and Karen retire at age 66.

They have:

$1.5 million invested

Two Social Security benefits totaling $5,800/month

Moderate IRA balances

A paid-off home

Initially, they focus mostly on investment growth and travel spending.

But after reviewing survivor planning, they realize several risks:

One Social Security check would disappear

Karen would likely face higher taxes as a single filer

Future RMDs could become problematic

Karen was unfamiliar with many financial accounts

They decide to:

Complete partial Roth conversions annually

Organize account records and passwords

Review estate documents

Stress-test survivor income needs

Ensure both spouses understand the retirement plan

None of these changes were dramatic.

But together, they significantly improved financial clarity and flexibility for the surviving spouse.

Questions Every Retired Couple Should Ask

If one spouse died tomorrow:

Would the surviving spouse know where everything is?

Would income still cover expenses?

Which Social Security benefit would remain?

Would taxes increase?

Would healthcare costs still be manageable?

Are beneficiaries updated?

Are estate documents current?

Does each spouse understand the financial plan?

These are difficult questions.

But they are often easier to address proactively than during a crisis.

Common Survivor Planning Mistakes

1. Ignoring Survivor Income Changes

Many couples underestimate how much income could disappear after the first death.

2. Delaying Estate Organization

Missing documents and unclear account structures create unnecessary stress.

3. Claiming Social Security Without Survivor Planning

Social Security timing decisions can significantly affect long-term survivor income.

4. Ignoring Future Survivor Tax Rates

Surviving spouses often face higher taxes with less favorable filing brackets.

5. Letting One Spouse Handle Everything Alone

Retirement planning works best when both spouses understand the overall strategy.

What Good Survivor Planning Really Looks Like

Good survivor planning is not about predicting the future perfectly.

It is about creating flexibility and reducing unnecessary uncertainty.

That may include:

Reviewing Social Security timing

Evaluating Roth conversions

Stress-testing survivor income

Organizing estate documents

Updating beneficiaries

Maintaining adequate liquidity

Ensuring both spouses understand the plan

The goal is not fear.

The goal is preparedness.

Final Thoughts

Most married couples spend years planning for retirement together.

Far fewer spend time planning for the financial realities one spouse may eventually face alone.

At Greenbush Financial Group, we often find that the strongest retirement plans are not just designed for ideal scenarios. They are also built to protect the surviving spouse from unnecessary financial stress, tax surprises, and confusion during difficult transitions.

These conversations are not always easy.

But they are some of the most valuable retirement planning discussions couples can have.

Good retirement planning is not just about helping both spouses retire comfortably.

It is about helping either spouse continue confidently if life changes unexpectedly.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

FAQ

-

What happens to Social Security when one spouse dies?The surviving spouse generally keeps the larger of the two Social Security benefits, while the smaller benefit stops.

-

Do taxes increase for surviving spouses?Often, yes. Surviving spouses usually transition from married filing jointly to single filing status, which can create higher tax exposure at lower income levels.

-

Do household expenses get cut in half after one spouse dies?Usually not. Many fixed expenses remain similar even though household income may decline significantly.

-

Why are Roth conversions important for married retirees?Roth conversions during joint lifetimes may help reduce future taxes, lower survivor RMDs, and improve tax flexibility for the surviving spouse.

-

Should both spouses understand the retirement plan?Absolutely. Both spouses should know where accounts are held, how income is generated, and who to contact for financial guidance.

-

What estate planning documents should retirees review?Retirees should review wills, trusts, powers of attorney, healthcare directives, and beneficiary designations regularly.

-

Can Medicare premiums increase for surviving spouses?Yes. Higher taxable income combined with single filing status may increase Medicare IRMAA exposure.

-

What is the biggest survivor planning mistake couples make?One of the biggest mistakes is assuming the surviving spouse will automatically be financially secure without reviewing income reductions, taxes, and account organization ahead of time.

The Inflation Problem Conservative Retirees Often Underestimate

Many retirees prioritize safety after leaving work, but being too conservative can create risks of its own. Learn how inflation, longevity, and portfolio growth affect long-term retirement income.

Many retirees become more conservative after leaving work, and that instinct is understandable. But avoiding too much market risk can create other risks that are easier to overlook, including inflation erosion, reduced long-term income growth, and the possibility of running out of money later in retirement. A retirement portfolio should not only protect against market declines but also support spending needs over decades. At Greenbush Financial Group, we often help retirees balance safety, growth, and income without taking unnecessary risk.

Many Retirees Focus on One Risk While Overlooking Another

Most retirees worry about losing money in the market.

That concern is completely reasonable.

Once paychecks stop, market declines often feel more emotional because withdrawals may now be coming directly from investment accounts.

As a result, many retirees react by moving heavily into:

Cash

CDs

Savings accounts

Short-term bonds

Extremely conservative portfolios

At first, this can feel safer.

Balances may fluctuate less. Monthly statements may feel calmer. Market headlines may feel less threatening.

But there is another risk retirees sometimes underestimate:

The risk of becoming too conservative for too long.

Because retirement is not usually a 5-year plan.

For many households, retirement may need to last:

20 years

30 years

Or longer

And over long periods of time, inflation can quietly become one of the biggest financial pressures retirees face.

The Hidden Risk: Losing Purchasing Power Over Time

One of the biggest challenges in retirement is that expenses rarely stay flat forever.

Even moderate inflation can slowly increase the cost of:

Healthcare

Insurance

Property taxes

Utilities

Food

Travel

Long-term care

Example

Suppose a retiree needs:

$80,000 per year today

If inflation averages 3% annually, that same lifestyle could require roughly:

$145,000 annually in 20 years

That does not mean spending suddenly doubles overnight.

It means purchasing power slowly erodes over time.

And portfolios that are too conservative may struggle to keep pace.

Why Too Much Cash Can Become a Retirement Problem

Cash plays an important role in retirement.

But many retirees unintentionally turn short-term safety into a long-term strategy.

That can create problems.

The Challenge With Excess Cash

Cash and low-yield investments may provide stability, but they often generate returns that struggle to outpace inflation over longer periods.

Over time, retirees may face:

Reduced purchasing power

Greater withdrawal pressure

Lower portfolio growth

Increased longevity risk

This becomes especially important later in retirement when:

Healthcare costs rise

Inflation compounds

One spouse may eventually live alone

Required withdrawals increase

The Difference Between Volatility Risk and Purchasing-Power Risk

Most retirees understand volatility risk.

That is the risk of market declines.

But retirement planning also involves purchasing-power risk.

That is the risk that your money loses real spending power over time because growth fails to keep up with inflation.

Both Risks Matter

An overly aggressive portfolio can create uncomfortable volatility.

But an overly conservative portfolio may quietly lose ground for years.

Retirement planning is often about balancing these risks rather than eliminating one entirely.

Why Retirees Still Need Some Growth

One of the biggest retirement misconceptions is:

“Once I retire, I should stop investing for growth.”

In reality, many retirees still need a portion of their portfolio invested for long-term growth because retirement may last decades.

Growth investments may help:

Offset inflation

Support future withdrawals

Reduce longevity risk

Maintain purchasing power

Improve portfolio sustainability

This does not mean retirees should become aggressive investors.

It means retirement portfolios usually need balance.

A Real-World Example: Conservative vs Balanced Retirement Strategies

Let’s compare two retirees.

Both retire at age 65 with:

$1.5 million invested

Spending needs of $75,000 annually

No pension

Moderate Social Security income

Retiree #1: Extremely Conservative

This retiree keeps:

80% in cash and CDs

20% in short-term bonds

The portfolio experiences very little volatility.

But over time:

Inflation reduces purchasing power

Withdrawals slowly increase

Portfolio growth struggles to keep pace

Future flexibility declines

Initially, this strategy feels emotionally comfortable.

But the long-term pressure builds quietly.

Retiree #2: Balanced Retirement Allocation

This retiree keeps:

Cash reserves for near-term spending

Bonds for stability

A diversified stock allocation for long-term growth

The portfolio experiences more short-term fluctuations.

But it also maintains greater long-term growth potential to help offset:

Inflation

Rising healthcare costs

Longer retirement timelines

The goal is not maximizing returns.

The goal is balancing stability and sustainability.

Why Fear Often Drives Overly Conservative Decisions

Many retirees become more conservative after:

Major market declines

Retirement timing stress

Watching account balances fluctuate

Financial news headlines

Economic uncertainty

These reactions are understandable.

Retirement changes how risk feels emotionally.

But investment decisions driven entirely by fear can sometimes create new risks that are less obvious initially.

Important Note

The answer is not ignoring risk.

The answer is understanding that retirement includes multiple risks:

Market risk

Inflation risk

Longevity risk

Tax risk

Healthcare cost risk

Strong retirement planning considers all of them together.

Sequence Risk Still Matters

Some retirees hear that they should maintain growth investments and assume they should remain heavily invested aggressively.

That can also create problems.

This is where sequence-of-returns risk becomes important.

What Is Sequence Risk?

Sequence risk occurs when poor market returns happen early in retirement while withdrawals are occurring simultaneously.

This can permanently damage long-term portfolio sustainability.

That is why retirement portfolios should balance:

Growth potential

Stability

Cash reserves

Withdrawal flexibility

Not simply maximize stock exposure.

The Role of Cash Reserves in a Balanced Retirement Plan

Cash is still important.

The issue is not holding cash.

The issue is relying too heavily on cash for too long.

Many retirees benefit from maintaining:

12–24 months of planned withdrawals in cash or short-term reserves

This may help cover spending needs during market declines without forcing investment sales at poor times.

Key Insight

Cash works best as a stability tool, not a complete long-term retirement strategy.

What About CDs and Bonds?

CDs and bonds can absolutely play an important role in retirement income planning.

But relying exclusively on conservative fixed-income investments can become more difficult when:

Inflation rises

Interest rates change

Spending needs increase

Retirement lasts longer than expected

The challenge is that many retirees need portfolios to do two things simultaneously:

Provide stability

Maintain long-term purchasing power

That often requires diversification across multiple asset types.

How Conservative Portfolios Can Increase Withdrawal Pressure

This is one of the least understood retirement risks.

If portfolio growth remains too low for too long:

Withdrawals may consume a larger percentage of assets

Future income flexibility may shrink

Spending adjustments may become necessary later

Ironically, some retirees become more conservative specifically because they fear running out of money.

But insufficient growth can sometimes increase that risk over longer periods.

The Goal Is Not Aggressive Investing

This is important.

A balanced retirement strategy should not feel like speculation.

The goal is not chasing returns.

The goal is building a portfolio designed for:

Reliable income

Long-term sustainability

Inflation protection

Emotional comfort

Flexibility during downturns

The right allocation depends on factors such as:

Age

Spending needs

Guaranteed income

Health

Risk tolerance

Legacy goals

Withdrawal rates

There is no universal retirement portfolio.

Questions Retirees Should Ask

Important retirement planning questions include:

How much cash is appropriate for my situation?

Could inflation pressure my spending later?

Am I too conservative for a 25–30 year retirement?

What happens if healthcare costs rise significantly?

How would my spouse manage if I died first?

Is my withdrawal strategy sustainable?

Do I have enough growth potential built into the plan?

These questions are often more valuable than trying to predict short-term market movements.

Common Mistakes Conservative Retirees Make

1. Moving Entirely to Cash After Retirement

This may feel safer emotionally but can increase long-term purchasing-power risk.

2. Ignoring Inflation

Even moderate inflation compounds significantly over decades.

3. Assuming Conservative Means “Risk-Free”

Every retirement strategy involves tradeoffs.

Low volatility does not eliminate long-term retirement risk.

4. Separating Safety and Growth Incorrectly

Many retirees benefit from separating:

Short-term spending reserves from:

Long-term growth assets

This creates flexibility during volatility.

5. Reacting Emotionally After Market Declines

Emotional investment decisions can permanently alter long-term retirement outcomes.

Final Thoughts

Wanting safety in retirement is completely understandable.

Most retirees are not trying to maximize returns. They are trying to protect the life they worked decades to build.

But retirement planning is not just about avoiding market declines.

It is also about protecting future purchasing power, maintaining flexibility, and creating income that can last through decades of changing expenses and inflation.

At Greenbush Financial Group, we often help retirees balance multiple retirement risks at once rather than focusing on only one type of fear or uncertainty.

The goal is not taking unnecessary risk.

The goal is making sure your retirement plan protects you from both short-term volatility and long-term erosion.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

FAQ

-

Can being too conservative in retirement be risky?Yes. Holding too much cash or low-growth investments for long periods may increase inflation risk and reduce long-term purchasing power.

-

Why do retirees still need growth investments?Many retirements last 20-30 years or longer. Growth investments may help offset inflation and support long-term income sustainability.

-

How much cash should retirees keep?Many retirees benefit from holding 12-24 months of planned withdrawals in cash or short-term reserves, depending on risk tolerance and spending needs.

-

Is cash bad in retirement?No. Cash plays an important role for stability and near-term spending. Problems usually arise when retirees rely too heavily on cash long-term.

-

What is purchasing-power risk?Purchasing-power risk is the risk that inflation gradually reduces the real value of your money over time.

-

What is sequence-of-returns risk?Sequence risk occurs when poor market returns happen early in retirement while withdrawals are occurring simultaneously.

-

Should retirees avoid the stock market completely?Not necessarily. Many retirees benefit from maintaining some diversified growth exposure while balancing stability and income needs.

-

What is the biggest mistake overly conservative retirees make?One of the biggest mistakes is focusing only on avoiding short-term market volatility while underestimating long-term inflation and longevity risks.

Retirement Income Planning: How to Pay Yourself Without a Job

Creating retirement income requires more than simply withdrawing money from investment accounts. This guide explains how retirees can coordinate Social Security benefits, investment withdrawals, and cash reserves to build a reliable retirement paycheck while managing taxes, sequence-of-returns risk, and market volatility. Learn practical withdrawal strategies that help improve long-term portfolio sustainability and increase retirement confidence. Discover why organized income planning often matters more than chasing investment returns alone.

The hardest part of retirement is not saving money. It is turning your savings into a paycheck that can last for decades. A strong retirement income strategy combines Social Security, investments, and cash reserves in a way that helps retirees manage taxes, market downturns, and long-term spending needs. At Greenbush Financial Group, we often find that retirees feel more confident once they move from random withdrawals to a structured retirement paycheck plan.

The Hardest Part of Retirement Is Not Saving. It’s Replacing Your Paycheck.

For most of your working life, income was automatic.

You worked, your paycheck arrived, taxes were withheld, and bills were paid.

Retirement changes that system overnight.

Now your income may need to come from:

Social Security

Investment accounts

IRAs

Roth IRAs

Cash savings

Brokerage accounts

Maybe a pension

That transition can feel uncomfortable even for financially responsible retirees.

Many people spend decades learning how to save for retirement but very little time learning how to withdraw from retirement.

That is why one of the biggest retirement questions becomes:

“How do I actually turn my savings into reliable monthly income?”

The answer is usually not:

Living only on dividends

Using the 4% rule blindly

Pulling money randomly from accounts

Staying fully invested with no cash reserves

A retirement paycheck works best when it is intentional, flexible, tax-aware, and designed to handle both good markets and bad ones.

What a Retirement Paycheck Actually Looks Like

A retirement paycheck is usually built from three primary sources:

Guaranteed income

Investment withdrawals

Cash reserves

Each source plays a different role.

The goal is not maximizing investment returns.

The goal is creating sustainable monthly income while reducing unnecessary financial stress.

The 3 Buckets of Retirement Income

Bucket #1: Guaranteed Income

This includes predictable income sources such as:

Social Security

Pensions

Certain annuities

For many retirees, this income helps cover core living expenses like:

Housing

Utilities

Groceries

Insurance

Basic healthcare costs

Guaranteed income creates stability.

The more predictable income a retiree has, the less pressure there may be on investment withdrawals during difficult markets.

Bucket #2: Investment Withdrawals

This is where retirees often generate additional income beyond Social Security.

Withdrawals may come from:

Traditional IRAs

401(k)s

Taxable brokerage accounts

Roth IRAs

This is also where many costly mistakes happen.

Without a strategy, retirees may:

Withdraw too much

Trigger unnecessary taxes

Increase Medicare premiums

Sell investments during downturns

Deplete the wrong accounts too early

The order of withdrawals matters.

Bucket #3: Cash Reserves

Cash reserves are one of the most overlooked parts of retirement income planning.

Cash reserves may include:

Savings accounts

Money market funds

CDs

Treasury bills

Short-term bond holdings

The purpose of cash is not maximizing returns.

Its purpose is flexibility.

Cash reserves help retirees avoid selling investments during bad markets when emotions are elevated and portfolio values are temporarily down.

How Retirement Income Is Structured Month to Month

Retirement income planning usually starts with one simple question:

“How much do you actually need each month?”

Step 1: Identify Monthly Spending Needs

Example:

John and Linda retire at age 66.

They estimate they need:

$8,000/month after taxes

That includes:

Property taxes

Insurance

Healthcare

Travel

Utilities

Food

Entertainment

Home maintenance

Step 2: Subtract Guaranteed Income

They receive:

$4,500/month combined from Social Security

That leaves:

$3,500/month that must come from investments and savings

This is called the income gap.

Step 3: Build a Withdrawal Strategy

Their assets include:

$950,000 in IRAs

$300,000 in brokerage accounts

$150,000 in cash reserves

$200,000 in Roth IRAs

Instead of taking income randomly, they decide to:

Use brokerage assets first for flexibility

Maintain 18 months of cash reserves

Delay larger IRA withdrawals strategically

Refill cash reserves during stronger market periods

Keep Roth assets growing longer for future flexibility

Now their retirement income becomes organized and repeatable rather than reactive.

Why Random Withdrawals Can Create Long-Term Problems

Many retirees withdraw from whichever account feels easiest at the time.

That can create ripple effects.

Example

Suppose a retiree withdraws $80,000 entirely from an IRA for spending and home renovations.

That withdrawal may:

Push income into higher tax brackets

Increase taxation of Social Security

Trigger Medicare IRMAA surcharges

Reduce future Roth conversion opportunities

A different withdrawal strategy may have created a better long-term outcome.

Retirement income planning is not just about generating cash.

It is about generating cash efficiently.

Why Cash Reserves Matter So Much in Retirement

Many retirees underestimate how emotionally different investing feels after paychecks stop.

During working years, market declines may feel temporary because new paychecks continue arriving.

Retirement changes that dynamic.

Now withdrawals may be happening while investments are falling.

That creates what planners call sequence-of-returns risk.

What Is Sequence Risk?

Sequence risk occurs when poor market returns happen early in retirement while withdrawals are occurring simultaneously.

This combination can permanently reduce long-term portfolio sustainability.

Example

Two retirees start with identical portfolios and identical spending.

One is forced to sell investments during a major downturn to fund living expenses.

The other uses cash reserves temporarily while allowing investments time to recover.

The long-term outcomes can look dramatically different.

How Much Cash Should Retirees Keep?

There is no perfect answer.

But many retirees feel more comfortable keeping:

12–24 months of planned withdrawals in cash or short-term reserves

The appropriate amount depends on:

Risk tolerance

Market exposure

Spending flexibility

Healthcare concerns

Pension income

Comfort during volatility

Important Note

Too little cash may force investment sales during downturns.

Too much cash may reduce long-term purchasing power because inflation slowly erodes cash value.

The goal is balance.

Should Retirees Live Off Dividends Only?

Many retirees like the idea of “never touching principal” and living entirely off dividends.

While dividend income can help, retirement income planning is usually more nuanced than that.

Dividend-only strategies can create problems such as:

Concentrated portfolios

Reduced diversification

Lower flexibility

Chasing yield

Tax inefficiencies

What matters most is not whether income comes from dividends or withdrawals.

What matters is:

Total return

Sustainability

Tax efficiency

Risk management

Flexibility during market declines

A well-designed retirement paycheck should focus on the overall income strategy, not just one type of investment income.

How Social Security Fits Into a Retirement Paycheck

Social Security is often the foundation of retirement income.

The timing decision affects:

Monthly income

Portfolio withdrawals

Survivor income

Longevity protection

Taxes

Claiming at 62

Taking benefits early provides income sooner but permanently reduces monthly payments.

This may reduce portfolio withdrawals initially.

But it also lowers guaranteed lifetime income.

Claiming at Full Retirement Age

Waiting until full retirement age increases monthly benefits and avoids early claiming reductions.

For many retirees, this creates a balance between income needs and future benefit growth.

Delaying Until Age 70

Benefits increase each year benefits are delayed beyond full retirement age.

For healthy retirees, delayed Social Security can act as additional protection against longevity risk later in retirement.

Especially for married couples, this can significantly affect survivor income.

How Retirees Avoid Selling Investments During Market Declines

A strong retirement paycheck strategy is designed before market volatility happens.

That strategy often includes:

Cash reserves

Diversification

Flexible withdrawals

Annual tax reviews

Periodic rebalancing

Spending flexibility

Example Strategy

A retiree may:

Hold 18 months of withdrawals in cash

Use Social Security for core expenses

Withdraw from brokerage accounts during stable markets

Reduce discretionary spending during downturns

Refill cash reserves after stronger market periods

This creates options during stressful periods instead of forcing emotional decisions.

How Often Should Retirement Income Plans Be Reviewed?

Retirement income planning is not a one-time event.

Most retirees should review their strategy annually.

Areas worth reviewing include:

Withdrawal rates

Tax brackets

Roth conversion opportunities

Medicare IRMAA exposure

Cash reserve levels

Investment allocation

Spending changes

Inflation adjustments

The goal is not constantly changing the plan.

The goal is making thoughtful adjustments as retirement evolves.

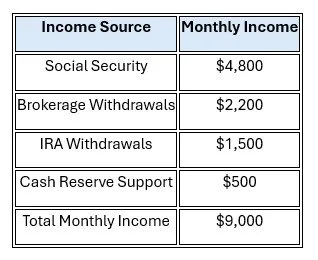

A Real-World Retirement Paycheck Example

Susan and Mark retire at ages 65 and 63.

They need:

$9,000/month after taxes

Their income plan looks like this:

Their Strategy

They maintain:

18 months of cash reserves

Moderate stock exposure for long-term growth

Diversification across account types

Annual withdrawal reviews

Flexible discretionary spending

During strong markets, they replenish cash reserves.

During weaker markets, they temporarily rely more heavily on cash rather than aggressively selling investments.

This approach helps reduce emotional pressure during volatility.

Common Retirement Paycheck Mistakes

1. Withdrawing Randomly From Accounts

Random withdrawals often create tax inefficiencies and unnecessary portfolio stress.

2. Keeping Too Little Cash

Without adequate reserves, retirees may be forced to sell investments during downturns.

3. Keeping Too Much Cash

Excessive cash can reduce long-term purchasing power because of inflation.

4. Ignoring Taxes

Taxes affect:

IRA withdrawals

Social Security taxation

Medicare premiums

Roth conversion opportunities

Retirement income should be coordinated at the household level.

5. Assuming the Same Strategy Works Forever

Retirement income plans should evolve over time as:

Spending changes

Healthcare costs rise

Markets fluctuate

RMDs begin

Tax laws change

Flexibility matters.

What Retirees Often Discover

Many retirees initially focus almost entirely on investment performance.

But over time, confidence often comes more from:

Organized cash flow

Predictable income

Tax coordination

Flexibility during downturns

Understanding where each dollar comes from

A retirement paycheck is not about finding a perfect strategy.

It is about building a system that feels sustainable and manageable over time.

Final Thoughts

The hardest part of retirement is usually not building wealth.

It is learning how to turn decades of savings into reliable monthly income.

A thoughtful retirement paycheck strategy can help retirees:

Reduce financial stress

Improve tax efficiency

Navigate market downturns

Protect long-term portfolio sustainability

Feel more confident about spending decisions

At Greenbush Financial Group, we often find that retirees gain confidence when they stop thinking about retirement income as random withdrawals and start viewing it as a coordinated household paycheck strategy.

The goal is not predicting every market movement perfectly.

The goal is creating a flexible income system that can support retirement through both strong markets and difficult ones.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

FAQ

-

How do retirees create a monthly paycheck from investments?Most retirees combine Social Security, investment withdrawals, and cash reserves to create consistent monthly income. Withdrawals are typically coordinated across different account types to improve tax efficiency and manage market risk.

-

How much cash should retirees keep?Many retirees benefit from holding 12-24 months of planned withdrawals in cash or short-term reserves, especially during the early retirement years.

-

What accounts should retirees withdraw from first?The answer depends on taxes, age, income needs, and long-term planning goals. Many retirees use a combination of taxable accounts, IRAs, and Roth accounts strategically rather than withdrawing from only one source.

-

What is sequence-of-returns risk?Sequence risk occurs when poor market returns happen early in retirement while withdrawals are being taken. This can permanently reduce long-term portfolio sustainability.

-

Should retirees rely only on dividends for income?Not necessarily. While dividends can help, most retirement income plans work better when they focus on total return, diversification, flexibility, and tax efficiency rather than dividends alone.

-

How does Social Security fit into a retirement paycheck?Social Security often acts as the foundation of retirement income by covering a portion of essential expenses and reducing pressure on investment withdrawals.

-

How often should retirement income plans be reviewed?Most retirees should review income strategies annually to evaluate taxes, spending, investment allocation, withdrawal rates, and healthcare costs.

-

What is the biggest retirement income mistake?One of the biggest mistakes is withdrawing money randomly from investment accounts without coordinating taxes, cash reserves, and long-term income sustainability.

2026 Bear Market Retirement Planning: How to Avoid Running Out of Money

Retiring in a down market increases sequence of returns risk, which can reduce how long your savings last. The most effective strategies include maintaining a cash reserve, using a bucket income approach, reducing withdrawals, and delaying Social Security. Tax planning and portfolio rebalancing can also improve long-term outcomes. Greenbush Financial Group emphasizes flexibility and disciplined decision-making to help retirees protect income during market volatility.

Retiring during a market downturn can significantly impact how long your retirement savings last due to sequence of returns risk. When withdrawals begin during a declining market, losses can compound and reduce long-term portfolio sustainability. At Greenbush Financial Group, our analysis shows that implementing the right withdrawal, allocation, and income strategies can help protect your retirement plan even in volatile markets.

Why Retiring in a Down Market Is Risky

The primary concern is not just market losses, but when those losses occur.

Sequence of Returns Risk Explained

Sequence risk refers to the timing of market returns relative to your withdrawals.

Negative returns early in retirement can permanently reduce your portfolio

Withdrawals during downturns lock in losses

Recovery becomes more difficult over time

Example

Two retirees with identical portfolios and average returns can have very different outcomes depending on whether market losses occur early or later in retirement.

At Greenbush Financial Group, this is one of the most important risks we plan for when building retirement income strategies.

Strategy 1: Build a Cash Reserve Before Retirement

One of the most effective ways to protect your portfolio is to avoid selling investments during a downturn.

Recommended Approach

Maintain 1–3 years of living expenses in cash or short-term investments

Use this reserve instead of withdrawing from stocks during market declines

Why It Works

Gives your portfolio time to recover

Reduces the need to sell assets at depressed prices

Provides psychological comfort during volatility

Strategy 2: Use a Bucket Strategy for Income

Segmenting your portfolio into different “buckets” can help manage risk.

Example Structure

Short-Term Bucket (0–3 years)

Cash, money markets, short-term bonds

Used for immediate income needs

Mid-Term Bucket (3–10 years)

Bonds, conservative investments

Provides stability and income

Long-Term Bucket (10+ years)

Stocks and growth assets

Designed to outpace inflation

At Greenbush Financial Group, we often use this framework to align investments with time horizons and reduce sequence risk.

Strategy 3: Reduce Withdrawals During Down Markets

Flexibility is critical when markets are volatile.

Key Adjustments

Temporarily reduce discretionary spending

Delay large purchases

Pause inflation increases on withdrawals

Example

Instead of withdrawing $60,000 during a downturn, reducing withdrawals to $50,000 can significantly improve long-term sustainability.

Strategy 4: Delay Social Security If Possible

Social Security provides a guaranteed, inflation-adjusted income stream.

Why Delaying Helps

Increases your monthly benefit

Reduces reliance on portfolio withdrawals early

Provides more stable income later in retirement

Planning Insight

Using portfolio assets early while delaying Social Security can sometimes improve long-term outcomes.

Strategy 5: Rebalance and Stay Invested

Market downturns can create opportunities to rebalance your portfolio.

Key Principles

Avoid panic selling

Rebalance to maintain target allocation

Take advantage of lower asset prices

At Greenbush Financial Group, maintaining discipline during downturns is often the difference between success and failure in retirement planning.

Strategy 6: Consider Part-Time Income or Flexible Retirement

Even a small amount of income can reduce pressure on your portfolio.

Benefits

Reduces withdrawal rate

Allows more time for investments to recover

Provides flexibility in spending

Example

Earning $10,000–$20,000 per year can significantly extend portfolio longevity.

Strategy 7: Tax Planning During Market Downturns

Down markets can create tax planning opportunities.

Strategies

Harvest capital losses to offset gains

Convert IRA funds to Roth at lower market values

Manage taxable income to stay in lower tax brackets

At Greenbush Financial Group, we often see that downturns can be an ideal time to implement tax-efficient strategies.

Common Mistakes to Avoid

Selling investments out of fear

Maintaining rigid withdrawal strategies

Ignoring tax planning opportunities

Failing to adjust spending

Overreacting to short-term market movements

A Real-World Scenario

Scenario

Retiree with $1,000,000 portfolio

Market declines 20% in first year

Withdraws $50,000 annually

Without Adjustments

Portfolio drops significantly

Recovery becomes difficult

With Strategic Adjustments

Uses cash reserve instead of selling stocks

Reduces withdrawals temporarily

Rebalances portfolio

Delays Social Security

Result

Improved long-term sustainability

Reduced sequence risk impact

Final Thoughts

Retiring during a down market does not mean your plan will fail, but it usually does require adjustments. The key is managing withdrawals, maintaining flexibility, and staying disciplined with your investment strategy.

At Greenbush Financial Group, our analysis shows that retirees who proactively adapt their strategy during downturns are far more likely to preserve their wealth and maintain sustainable income throughout retirement.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

-

Is it a bad idea to retire in a down market?Not necessarily, but it increases sequence of returns risk and requires careful planning.

-

How much cash and short-term fixed income should I have in retirement?Typically 1 to 3 years of living expenses.

-

Should I stop withdrawals during a downturn?Not entirely, but reducing withdrawals can improve long-term outcomes.

-

Can a market downturn ruin my retirement plan?It can if not managed properly, especially in the early years of retirement.

-

What is the best strategy during a market downturn?Maintain a cash reserve, adjust withdrawals, stay invested, and focus on long-term planning.