When Retirement Goes Better Than Planned: The Tax Problems of Having Too Much Money

Retirement planning becomes more complex as income, taxes, Social Security, healthcare, and withdrawals begin working together. Learn the signs that professional coordination may help reduce costly mistakes.

For decades, retirement planning has centered around one question:

"Will I have enough?"

It's an understandable concern. No one wants to outlive their savings.

But after working with hundreds of retirees, we've noticed another problem that receives far less attention:

What happens when retirement goes better than expected?

Many retirees discover they saved diligently, invested wisely, spent less than anticipated, and watched their portfolios continue to grow throughout retirement. While that's certainly preferable to running out of money, it can create a new set of planning challenges.

Large retirement accounts, growing investment portfolios, and conservative spending habits often lead to higher taxes, increased Medicare premiums, and more complicated estate planning.

In other words, financial success can create tax inefficiencies if it isn't managed strategically.

Why More Money Doesn't Always Mean More Financial Flexibility

Accumulating wealth is only one part of retirement planning.

The other part is figuring out how to use that wealth efficiently.

Many retirees assume that if they don't need to withdraw money from their retirement accounts, they'll simply leave it invested. Unfortunately, the IRS has other plans.

Once Required Minimum Distributions (RMDs) begin, retirees lose much of their control over the timing of taxable withdrawals.

Even if they don't need the income, they're generally required to take distributions from traditional IRAs and many employer-sponsored retirement plans.

Those distributions can create a ripple effect across nearly every aspect of a retirement plan.

The Challenge of Large Required Minimum Distributions

For retirees with substantial tax-deferred savings, RMDs often become the biggest source of taxable income later in retirement.

What starts as a manageable annual withdrawal can grow significantly over time if investment returns outpace distributions.

Example

Mark retires at age 65 with:

$2.8 million in traditional retirement accounts

A paid-off home

A pension

Social Security benefits

He doesn't need to touch his IRA during his first several years of retirement.

By the time RMDs begin, his account has grown to more than $4 million.

Now he's required to withdraw well over $150,000 annually, regardless of whether he needs the money.

Those withdrawals increase:

Federal taxable income

State taxable income (where applicable)

Medicare premiums

Taxes on investment income

Ironically, delaying withdrawals because he didn't need the money ultimately resulted in larger taxable distributions.

Key Insight

Sometimes the biggest tax bill isn't caused by poor planning. It's caused by successful investing combined with years of deferred taxation.

Medicare IRMAA Can Turn Success Into Higher Healthcare Costs

Many retirees are surprised to learn that Medicare isn't priced the same for everyone.

Higher-income retirees pay Income-Related Monthly Adjustment Amount (IRMAA) surcharges on:

Medicare Part B

Medicare Part D

As retirement income increases, so do Medicare premiums.

Large RMDs are one of the most common reasons retirees unexpectedly cross into higher IRMAA brackets.

Unlike income taxes, these higher premiums often feel like an additional tax on retirement success.

Conservative Spending Can Create Bigger Tax Problems Later

Many retirees underspend because they're worried about the future.

They postpone vacations.

Delay home improvements.

Skip experiences they've always wanted.

Meanwhile, their retirement accounts continue growing.

While financial discipline is admirable, consistently spending far less than your plan allows can unintentionally increase future tax liabilities.

Example

Susan budgets $130,000 annually for retirement but only spends about $75,000 because she's afraid of running out of money.

As a result:

Her IRA continues growing.

Future RMDs become much larger.

She pays more in taxes.

Medicare premiums increase.

She ultimately leaves a larger tax-deferred account to her children.

The money she spent decades saving may eventually be taxed at higher rates than if she had withdrawn it more strategically during retirement.

A Large Traditional IRA May Not Be the Gift You Think It Is

Many retirees view their IRA as a legacy for their children.

While those accounts can certainly provide meaningful inheritances, they also come with tax consequences.

Under current law, most non-spouse beneficiaries must fully distribute inherited retirement accounts within ten years.

For adult children in their peak earning years, those required withdrawals can push them into much higher tax brackets.

Example

A daughter earning $250,000 inherits a $1.5 million traditional IRA.

Over the next ten years, she must withdraw those funds according to current distribution rules.

Those withdrawals may be taxed at some of the highest marginal rates she'll ever pay.

Meanwhile, a Roth IRA inherited under similar circumstances may provide significantly greater tax flexibility.

Important Note

Leaving pre-tax retirement assets to heirs often transfers a future tax liability along with the inheritance.

Tax Diversification Matters Just as Much as Investment Diversification

Many retirees have diversified portfolios but not diversified tax treatment.

It's common to see wealth concentrated in:

Traditional IRAs

401(k)s

403(b)s

While these accounts provide valuable tax deferral during working years, relying too heavily on them can reduce flexibility in retirement.

A diversified retirement income strategy may include assets held in:

Tax-deferred accounts

Roth accounts

Taxable brokerage accounts

Cash reserves

Having multiple sources of retirement income allows retirees to better manage taxable income from year to year.

Why Roth Conversions Become More Valuable

One of the best opportunities to manage future taxes often occurs before RMDs begin.

Many retirees experience several years between retirement and the start of mandatory distributions when taxable income is relatively low.

These years may provide an opportunity to convert portions of traditional retirement accounts into Roth IRAs.

The goal isn't simply to reduce taxes this year.

Instead, Roth conversions may help:

Reduce future RMDs.

Lower lifetime taxable income.

Improve Medicare premium planning.

Leave more tax-efficient assets to heirs.

Increase flexibility when generating retirement income.

Every conversion should be evaluated within the context of the retiree's overall tax situation and long-term objectives.

The Emotional Side of Having "Too Much"

Many retirees struggle with a mindset they developed during decades of saving.

They spent their careers accumulating wealth.

Then retirement arrives, and they're suddenly expected to spend it.

That's easier said than done.

Some retirees continue saving out of habit, even when they have more than enough to support their lifestyle.

Others hesitate to enjoy experiences they've worked decades to afford because they're focused on preserving every dollar.

Financial security is important.

But retirement planning should also support the life those savings were meant to fund.

Common Mistakes Successful Retirees Make

Retirees with significant assets often make similar planning mistakes, including:

Assuming tax-deferred always means tax-free.

Waiting until RMDs begin before addressing taxes.

Focusing only on investment returns instead of after-tax income.

Ignoring future Medicare premium increases.

Leaving large traditional IRAs to children without considering the tax burden.

Becoming so focused on preserving wealth that they never enjoy it.

Planning Strategies for High-Net-Worth Retirees

Every situation is unique, but retirees with substantial assets should regularly evaluate strategies such as:

Multi-year Roth conversion planning.

Coordinating withdrawals across different account types.

Harvesting capital gains strategically.

Qualified Charitable Distributions (QCDs) after becoming eligible.

Reviewing estate plans alongside tax projections.

Modeling lifetime taxes instead of focusing only on annual tax returns.

The objective isn't necessarily to minimize taxes every year.

It's to reduce taxes over the course of retirement while creating greater flexibility for both retirees and their heirs.

More Wealth Should Create More Choices

One of the greatest benefits of financial success is flexibility.

Unfortunately, taxes can quietly reduce that flexibility if they aren't considered alongside investment performance.

Retirement planning doesn't end once you've accumulated enough assets.

In many ways, that's when some of the most important decisions begin.

At Greenbush Financial Group, we often remind clients that successful retirement planning isn't measured by the size of a portfolio. It's measured by how efficiently that wealth supports your lifestyle, your family, and your long-term goals.

Final Thoughts

Running out of money isn't the only retirement risk.

For many successful retirees, accumulating substantial wealth creates a different challenge: managing taxes, Medicare costs, Required Minimum Distributions, and legacy planning in a tax-efficient way.

With thoughtful planning, retirees may be able to reduce lifetime taxes, preserve greater flexibility, and leave a more efficient legacy for future generations. The goal isn't simply to build wealth. It's to make the most of it.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

Frequently Asked Questions

- Can you have too much money in a traditional IRA?While it's difficult to have "too much" money, very large traditional IRAs can lead to substantial Required Minimum Distributions and higher lifetime taxes if no planning is done.

- Why do large RMDs increase taxes?Required Minimum Distributions are generally taxed as ordinary income. Larger distributions can push retirees into higher tax brackets, increase Medicare premiums, and affect other tax calculations.

- Should wealthy retirees still consider Roth conversions?In many cases, yes. Roth conversions may help reduce future RMDs, improve tax diversification, and create more tax-efficient inheritances. The right strategy depends on the retiree's projected tax situation.

- Can leaving an IRA to my children create tax problems?Potentially. Most non-spouse beneficiaries must distribute inherited retirement accounts within ten years under current law, which can increase their taxable income during peak earning years.

- Is underspending in retirement a problem?It can be. While spending conservatively provides peace of mind, consistently underspending may lead to larger retirement account balances, higher future RMDs, and missed opportunities to enjoy retirement.

- What's the difference between investment success and tax efficiency?Investment success focuses on growing assets. Tax efficiency focuses on how much of those assets you actually keep after taxes over your lifetime and how efficiently they're passed to future generations.

Should You Spend More in Retirement? The Case for Enjoying Your Money

Retirement planning becomes more complex as income, taxes, Social Security, healthcare, and withdrawals begin working together. Learn the signs that professional coordination may help reduce costly mistakes.

One of the biggest surprises in retirement isn't that people spend too much.

It's that many spend too little.

After decades of saving and living within a budget, it can be difficult to switch from accumulating wealth to spending it. Even retirees with healthy portfolios often hesitate to travel, remodel their home, or enjoy experiences they've worked their entire lives to afford.

Being financially responsible is important. But if fear keeps you from enjoying retirement, it may be time to revisit your plan.

Why Many Retirees Underspend

Saving becomes a habit over a 30- or 40-year career. Retirement requires a different mindset.

Common reasons retirees spend less than they could include:

Fear of running out of money

Concern about future healthcare costs

Uncertainty about market downturns

A desire to leave as much as possible to their children

These are valid concerns, but they shouldn't automatically prevent you from enjoying your retirement years.

How Do You Know If You Can Spend More?

The answer isn't based on your account balance alone.

Instead, it comes down to whether your financial plan shows your income and assets can support your goals over the long term.

Some encouraging signs include:

Your retirement income consistently exceeds your spending.

Your portfolio continues to grow despite withdrawals.

You've planned for healthcare and long-term care costs.

Your withdrawals remain well within sustainable levels.

If that's the case, spending a little more may not jeopardize your financial security.

The Cost of Waiting

Many retirees postpone experiences until "someday."

They delay travel, put off family vacations, or avoid spending on hobbies because they're worried they'll need the money later.

The reality is that your ability to enjoy those experiences may decline with age.

Example

Jim and Linda planned to travel extensively in retirement but kept delaying trips because the market felt uncertain.

By their late 70s, health issues made many of those trips unrealistic.

Their savings had grown well beyond what they expected, but the opportunities they had planned for were no longer available.

Key Insight

Money can often be replaced through investment returns. Time cannot.

Spending More Doesn't Mean Spending Carelessly

This isn't an argument for reckless spending.

It's about spending intentionally on the things that matter most.

That could mean:

Traveling while you're healthy.

Helping grandchildren with education.

Renovating your home to age in place.

Pursuing hobbies or lifelong interests.

Creating meaningful family experiences.

The goal isn't to spend more simply because you can. It's to use your money in ways that improve your quality of life.

Don't Let Taxes Make the Decision for You

Ironically, spending too little can sometimes create larger tax issues later.

If you rarely withdraw from traditional retirement accounts, those balances may continue growing until Required Minimum Distributions (RMDs) force larger taxable withdrawals.

In some cases, strategic withdrawals earlier in retirement can improve long-term tax efficiency while also providing money to enjoy retirement.

Balancing Lifestyle and Legacy

Many retirees want to leave an inheritance, and that's a worthwhile goal.

But it's also important to ask:

Are you sacrificing the retirement you envisioned to leave behind more than your family expects or needs?

In many families, children would rather see their parents enjoy retirement than leave the largest possible inheritance.

A thoughtful financial plan can help balance both objectives.

Common Signs You're Underspending

You may be living more conservatively than necessary if:

You're consistently spending less than your financial plan anticipated.

Your portfolio continues growing year after year.

You regularly postpone meaningful purchases out of fear.

You avoid experiences you've always wanted despite being financially able to afford them.

These patterns don't automatically mean you should spend more, but they're worth discussing with your financial advisor.

Planning Creates Confidence

The best spending decisions aren't driven by emotion. They're supported by a well-designed retirement plan.

When you understand how much you can safely spend, you're less likely to make decisions based solely on fear.

At Greenbush Financial Group, we believe retirement planning isn't just about preserving wealth. It's about helping clients use their resources to create the retirement they've spent decades working toward.

Final Thoughts

Saving for retirement requires discipline. Enjoying retirement requires confidence.

If your financial plan shows you have more than enough, it may be time to give yourself permission to spend on the people, experiences, and goals that matter most.

After all, the purpose of building wealth isn't simply to accumulate it. It's to use it to support a fulfilling retirement.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

Frequently Asked Questions

- Is it common for retirees to underspend?Yes. Research consistently shows many retirees spend less than they can afford because they're concerned about outliving their savings.

- How can I tell if I'm spending too little?A retirement income plan can project whether your current spending is sustainable. If your assets continue growing despite withdrawals, you may have room to spend more.

- Should I prioritize spending or leaving an inheritance?It depends on your goals. Most retirees can strike a balance between enjoying retirement and leaving a meaningful legacy with proper planning.

- Can spending too little create tax problems?Potentially. Delaying withdrawals from traditional retirement accounts can lead to larger RMDs and higher taxes later in retirement.

- What's the biggest mistake retirees make with spending?Many assume they need to preserve every dollar, even when their financial plan shows they can comfortably afford to enjoy more of their retirement.

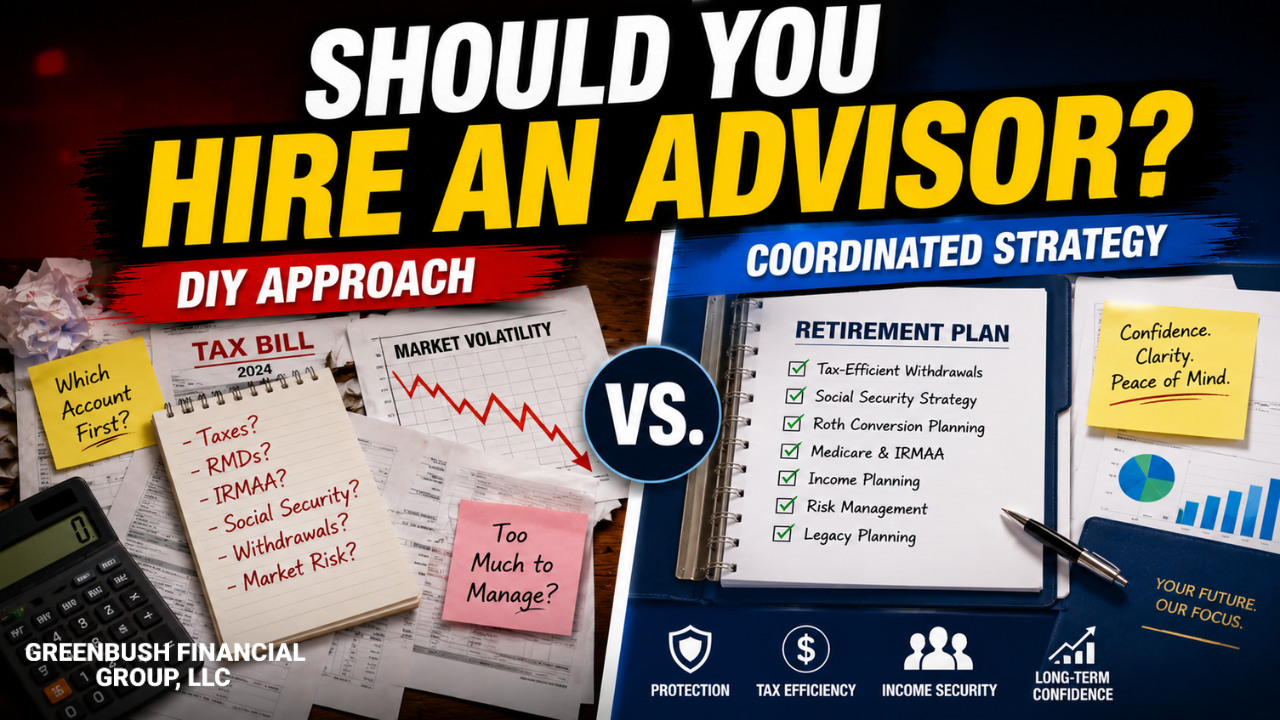

The Closer You Get to Retirement, the More Expensive Mistakes Become

Retirement planning becomes more complex as income, taxes, Social Security, healthcare, and withdrawals begin working together. Learn the signs that professional coordination may help reduce costly mistakes.

Many people successfully manage their finances for decades while saving for retirement. But as retirement approaches, decisions around taxes, Social Security, healthcare, withdrawals, and income planning become more interconnected and harder to reverse. The question is not whether someone is smart enough to manage retirement alone. The question is whether the complexity of retirement planning has reached the point where professional coordination could improve outcomes. At Greenbush Financial Group, we often find that retirees seek guidance not because they lack discipline, but because retirement introduces decisions that can affect income, taxes, and financial confidence for decades.

Retirement Planning Changes Once Paychecks Stop

Many successful professionals and disciplined investors manage their finances perfectly well during their working years.

Saving for retirement is often relatively straightforward:

Earn income

Contribute to retirement accounts

Invest consistently

Avoid major mistakes

Retirement changes the equation.

Now the questions become:

Which accounts should income come from first?

When should Social Security begin?

How do Roth conversions fit into the plan?

How much cash should be kept available?

How do withdrawals affect taxes?

What happens if markets decline early in retirement?

Would a surviving spouse still be financially secure?

This is why many people who comfortably handled accumulation planning begin questioning whether retirement distribution planning requires additional coordination.

Hiring a financial advisor is not about intelligence.

It is about complexity.

Retirement Planning Is More Than Investment Management

One of the biggest misconceptions about financial advisors is that their role is simply picking investments.

For retirees and pre-retirees, the larger value often comes from coordinating multiple moving parts together.

Retirement Planning Often Involves:

Income withdrawal sequencing

Social Security timing

Roth conversion analysis

Medicare IRMAA planning

Tax-efficient withdrawals

Required Minimum Distribution (RMD) planning

Survivor planning

Estate coordination

Long-term care considerations

Investment allocation

Sequence-of-returns risk management

As retirement approaches, these decisions begin affecting one another.

That complexity is often what pushes people toward seeking professional guidance.

Some People May Not Need a Financial Advisor

This is important to acknowledge honestly.

Not every retiree needs ongoing financial advisory services.

Some households may have:

Simple financial situations

Strong financial knowledge

Minimal tax complexity

Pension income covering most expenses

Small withdrawal needs

Comfort managing investments independently

For disciplined retirees with straightforward situations, DIY retirement planning may work perfectly well.

The question is not:

“Can someone manage their own finances?”

The better question is:

“Has retirement planning become complex enough that coordination mistakes could become expensive?”

Why Retirement Mistakes Become More Expensive Later

During working years, mistakes are often easier to recover from because future earnings continue.

Retirement changes that dynamic.

Once paychecks stop:

Tax mistakes can compound

Poor withdrawal timing becomes harder to reverse

Market declines may affect withdrawals

Social Security decisions become permanent

Healthcare costs become more important

Sequence risk matters more

The closer someone gets to retirement, the fewer opportunities there may be to correct major planning errors later.

7 Signs Retirement Planning May Be Becoming Too Complex to Handle Alone

1. You’re Unsure How to Create Retirement Income

Many retirees know how to save.

Far fewer know how to create sustainable retirement income.

Questions often include:

Which account should I withdraw from first?

How much cash should I keep?

Should I delay Social Security?

How do taxes affect withdrawals?

If retirement income feels improvised instead of coordinated, that may indicate planning complexity has increased.

2. You Have Large IRA Balances

Large pre-tax retirement accounts can create future tax issues many retirees underestimate.

Potential concerns include:

Large RMDs later

Higher Medicare premiums

Widow’s tax trap

Increased Social Security taxation

This is where Roth conversion planning often becomes important.

The challenge is not just reducing taxes this year.

It is coordinating taxes across decades.

3. One Spouse Handles Most Financial Decisions

This is extremely common.

Often one spouse manages:

Investments

Taxes

Bills

Account access

Financial planning

That system may work well until a health issue or death creates a sudden transition.

Many couples seek financial guidance because they want:

Shared understanding

Organized planning

Continuity for the surviving spouse

Good retirement planning should work for both spouses, not just the financially engaged one.

4. You’re Concerned About Market Volatility Near Retirement

Market declines feel different once retirement approaches.

During working years, paychecks continue.

Near retirement, people often worry:

“What happens if the market drops right after I retire?”

“How much risk should I still take?”

“Should I move more to cash?”

These concerns are reasonable.

A strong retirement plan balances:

Growth

Income

Cash reserves

Withdrawal flexibility

Emotional comfort

Not just investment returns.

5. You’re Unsure About Social Security Timing

Social Security decisions can permanently affect:

Household income

Survivor benefits

Taxes

Withdrawal needs

Many retirees underestimate how much claiming timing affects long-term outcomes.

Especially for married couples, survivor planning becomes critical.

6. Your Financial Life Has Become More Complicated

Complexity often increases because of:

Business sales

Inheritances

Multiple investment accounts

Real estate holdings

Pension decisions

Stock compensation

Widow/widower concerns

Blended families

At a certain point, coordination becomes more valuable than simply managing investments independently.

7. You’re Worried You May Be Missing Something Important

This may be the most common reason retirees seek help.

Not because they feel incapable.

But because retirement decisions become interconnected.

Many retirees quietly wonder:

“Am I withdrawing efficiently?”

“Could I lower taxes long term?”

“What happens if one of us dies?”

“Are we taking too much risk?”

“Could one mistake hurt us later?”

Those are reasonable questions.

A Simple Retirement Situation vs. A More Complex One

Example #1: Simpler Retirement Scenario

A retiree may have:

Pension income

Social Security

Small IRA balances

Minimal taxes

Stable spending needs

This household may require relatively little ongoing planning complexity.

Example #2: More Complex Retirement Scenario

A married couple has:

$2 million invested

Large IRAs

Brokerage accounts

Deferred compensation

Rental property

Delayed Social Security decisions

Roth conversion opportunities

Widow planning concerns

Now retirement planning involves:

Tax coordination

Withdrawal sequencing

Survivor planning

Medicare considerations

Estate organization

At this stage, the value of coordination may increase significantly.

What Good Financial Advisors Actually Help With

A good retirement-focused advisor should help coordinate:

Taxes

Retirement income

Investment allocation

Withdrawal strategy

Long-term planning

Estate coordination

Survivor preparation

The value is often not “beating the market.”

The value is reducing costly mistakes and improving long-term decision coordination.

Not All Advisors Provide the Same Value

This is important.

Retirees should understand that advisors vary significantly.

Some primarily focus on:

Investment products

Asset gathering

Insurance sales

Others focus on comprehensive retirement planning.

Important Questions to Ask

Before hiring someone, retirees should understand:

Are they acting as a fiduciary?

How are they compensated?

Do they provide tax-aware planning?

Do they coordinate retirement income strategy?

How do they communicate during market volatility?

Do they help with survivor planning?

Will both spouses understand the plan?

A good advisor relationship should create clarity, not confusion.

Common Mistakes Retirees Make When Hiring Advisors

1. Focusing Only on Investment Returns

Retirement planning is broader than portfolio performance alone.

2. Hiring Someone Without Understanding Fees

Transparency matters.

Retirees should clearly understand:

Advisory fees

Product commissions

Insurance incentives

Planning costs

3. Assuming All Advisors Coordinate Taxes

Many do not.

Tax planning often becomes one of the most valuable retirement planning areas.

4. Waiting Until a Crisis Happens

Some retirees delay planning until:

A spouse dies

Markets decline

RMDs begin

Taxes spike

Health changes occur

Planning is often easier before pressure builds.

Questions to Ask Yourself Before Hiring an Advisor

Consider questions like:

Is retirement planning becoming emotionally stressful?

Am I confident about withdrawal strategy?

Do I understand future tax exposure?

Would my spouse know what to do without me?

Am I coordinating Social Security properly?

Do I have a plan for market downturns?

Are estate documents and beneficiaries organized?

The answers may help clarify whether professional coordination could add value.

Final Thoughts

Many people successfully manage their finances during their working years.

But retirement planning often becomes more interconnected and more difficult to reverse once income, taxes, Social Security, healthcare, and withdrawals all begin interacting simultaneously.

At Greenbush Financial Group, we often find that retirees seek guidance not because they want to give up control, but because they want greater clarity and confidence as retirement decisions become more complex.

Hiring a financial advisor is not automatically necessary for everyone.

But for some retirees, especially those approaching major retirement decisions, thoughtful coordination may help reduce costly mistakes and improve long-term financial flexibility.

The goal is not dependency.

The goal is making informed decisions during one of the most financially important transitions of life.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

FAQ

-

When should someone hire a financial advisor before retirement?Many people consider hiring an advisor within 5-10 years of retirement, especially when decisions around taxes, withdrawals, Social Security, and healthcare become more complex.

-

Do all retirees need a financial advisor?No. Some retirees with simple financial situations and strong financial knowledge may manage retirement successfully on their own.

-

What is the difference between investment management and retirement planning?Investment management focuses primarily on portfolios. Retirement planning coordinates income, taxes, withdrawals, Social Security, healthcare, estate planning, and long-term sustainability.

-

Why does retirement planning become more complicated?Because decisions become interconnected. Withdrawals, taxes, Social Security, Medicare premiums, and market performance can all affect one another.

-

What are signs retirement planning may be too complex to handle alone?Common signs include large IRA balances, uncertainty around withdrawals, tax concerns, widow planning issues, and anxiety about market volatility.

-

Should DIY investors feel pressured to hire an advisor?No. Many successful DIY investors continue managing their finances independently. The question is whether retirement complexity has reached a level where coordination may improve outcomes.

-

What should retirees look for in a financial advisor?Retirees should evaluate fiduciary responsibility, fee transparency, retirement income planning experience, tax coordination, communication style, and survivor planning expertise.

-

What is the biggest mistake retirees make before hiring an advisor?One of the biggest mistakes is assuming retirement planning is only about investments instead of coordinating taxes, income, healthcare, and long-term financial decisions together.