2026 Spousal vs Survivor Benefits Explained: How Social Security Works for Couples

Social Security spousal and survivor benefits can significantly impact retirement income for married couples. Learn the key rules, claiming strategies, and common mistakes that can affect lifetime benefits and financial security.

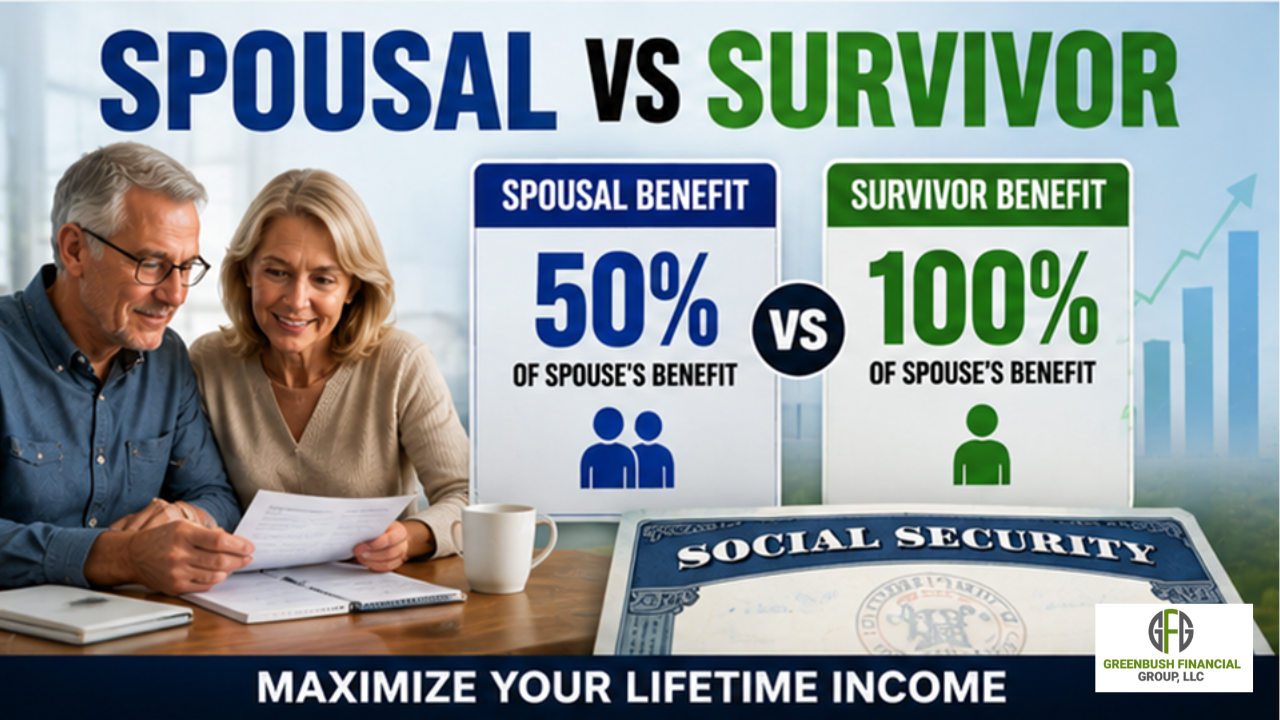

Social Security spousal and survivor benefits are critical components of retirement planning for married couples. A spouse may be eligible to receive up to 50% of their partner’s benefit while both are alive, and up to 100% of the higher benefit after a spouse passes away. At Greenbush Financial Group, our analysis shows that understanding how these benefits work can significantly impact lifetime income and financial security.

What Are Social Security Spousal Benefits?

Spousal benefits allow one spouse to receive a portion of the other spouse’s Social Security benefit.

Key Rules

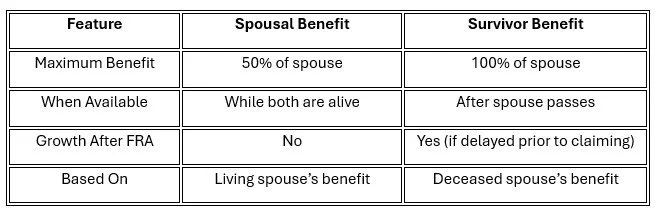

Spousal benefit is up to 50% of the higher earner’s benefit

Must wait until the primary earner files for benefits

Available to current spouses and some divorced spouses

Example

Higher earner benefit = $2,000/month

Spousal benefit = up to $1,000/month

Important Note

You do not receive both your own benefit and the spousal benefit. Social Security pays the higher of the two amounts.

At Greenbush Financial Group, we often see this misunderstood, leading to unrealistic income expectations.

When Can You Claim Spousal Benefits?

Timing affects how much you receive.

Claiming Ages

Age 62 → Reduced spousal benefit

Full Retirement Age (67) → Full 50% benefit

No additional increase beyond FRA for spousal benefits

Key Insight

Unlike your own benefit, spousal benefits do not grow after full retirement age.

What Are Social Security Survivor Benefits?

Survivor benefits apply when one spouse passes away.

Key Rules

Surviving spouse can receive up to 100% of the higher benefit

Can switch from their own benefit to survivor benefit if advantageous

Available as early as age 60 (reduced), or full benefit at FRA

Example

Spouse A benefit = $2,500

Spouse B benefit = $1,500

After Spouse A passes, Spouse B receives $2,500

At Greenbush Financial Group, survivor planning is one of the most important considerations for long-term income security.

Spousal vs Survivor Benefits: Key Differences

How Timing Impacts Couples’ Benefits

The timing of when each spouse claims benefits can significantly affect total lifetime income.

Key Strategy

Higher earner delays benefits to increase survivor income

Lower earner may claim earlier depending on income needs

Why This Matters

Delaying benefits for the higher earner increases:

Monthly retirement income

Survivor benefit for the remaining spouse

At Greenbush Financial Group, we often prioritize maximizing the higher earner’s benefit for long-term protection.

Divorced Spouse Benefits

Even divorced individuals may qualify for spousal or survivor benefits.

Requirements

Marriage lasted at least 10 years

Individual is currently unmarried

Ex-spouse is eligible for benefits

Key Insight

Claiming on an ex-spouse’s record does not reduce their benefit.

Common Mistakes to Avoid

Claiming too early without considering survivor impact

Assuming both spouses receive full benefits simultaneously

Ignoring the importance of the higher earner delaying benefits

Not coordinating claiming strategies as a couple

Overlooking divorced spouse eligibility

A Real-World Planning Example

Scenario

Husband benefit: $2,800

Wife benefit: $1,200

Strategy

Husband delays until age 70

Wife claims earlier or at FRA

Outcome

Higher household income later

Increased survivor benefit for wife

This type of coordinated strategy can significantly improve long-term outcomes.

How Taxes Impact Spousal and Survivor Benefits

Social Security benefits may be taxable depending on total income.

Key Considerations

Up to 85% of benefits can be taxable

IRA withdrawals can increase taxation

Survivor filing status may increase tax burden

Planning Insight

A surviving spouse often files as single, which can lead to higher taxes on the same income.

At Greenbush Financial Group, tax planning is often integrated with Social Security decisions.

Final Thoughts

Social Security spousal and survivor benefits are not just supplemental income, they are a core part of retirement planning for couples. The decisions around timing and coordination can have a lasting impact on both partners.

At Greenbush Financial Group, our analysis shows that couples who plan their Social Security strategy together tend to maximize lifetime income and provide better financial security for the surviving spouse.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

Frequently Asked Questions

-

How much is a spousal Social Security benefit?

Up to 50% of the higher earner's benefit at full retirement age. -

Do spousal benefits increase after age 67?

No, they do not increase beyond full retirement age. -

What happens to Social Security when a spouse dies?

The surviving spouse can receive up to 100% of the higher benefit. -

Can a divorced spouse claim Social Security benefits?

Yes, if the marriage lasted at least 10 years and other requirements are met. -

Can I receive both my benefit and my spouse's benefit?

No, you receive the higher of the two, not both.