Gifting Strategies

Thoughtful Ways to Share Wealth and Plan for the Next Generation

Gifting strategies often sit at the intersection of financial planning and estate planning. We frequently have gifting conversations with clients when it becomes clear that there will be excess assets left over to pass on to the next generation.

At that point, the question often becomes:

Would you rather your children and grandchildren receive their inheritance after you’re gone, or would you prefer to share some of your wealth now—and experience the joy of watching them benefit from it while you’re still alive?

For many families, this is one of the most meaningful conversations in the planning process. At the same time, gifting can also serve as a powerful strategy to reduce estate size and manage future tax exposure.

Gifting as an Estate Planning Strategy

For clients with sizable estates—particularly those approaching or exceeding federal or state estate tax exemption limits—gifting can be an effective way to reduce the overall value of the estate.

Key considerations include:

The annual gift tax exclusion, which allows individuals to gift up to a set amount per recipient each year without using lifetime exemption

Gifting assets during life to reduce estate size

Coordinating gifts across spouses and family members

Because annual gifts do not count against lifetime gift and estate tax limits, they can be a strategic tool when used consistently over time.

The Emotional Side of Gifting

Beyond taxes, gifting is often about family, legacy, and connection.

Many clients prefer:

Helping children with home purchases

Funding education for grandchildren

Supporting family businesses or career transitions

Seeing the impact of their generosity firsthand

When structured properly, gifting can enhance both financial outcomes and family relationships.

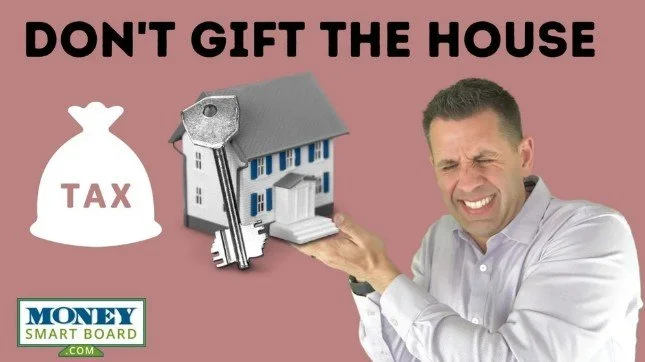

Be Careful What You Gift

While gifting can be powerful, not all assets should be gifted, and doing so incorrectly can create unintended tax consequences.

When you gift an asset:

The recipient inherits your cost basis

Any built-in capital gains transfer with the asset

Future taxes may be significantly higher for the beneficiary

This is especially important for:

Real estate

Investment securities

Highly appreciated assets

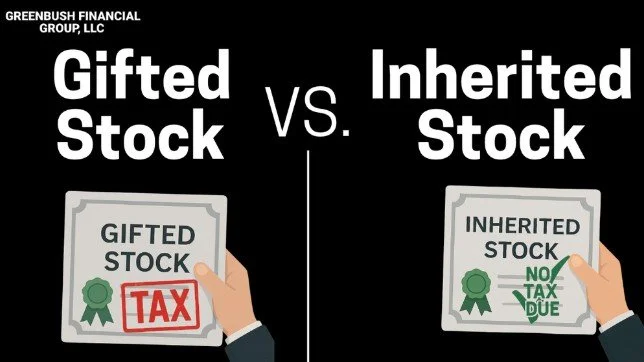

Understanding Cost Basis and the Step-Up Rule

One of the most important estate planning concepts is the step-up in cost basis.

When assets are inherited at death:

Beneficiaries typically receive a step-up in cost basis to the asset’s fair market value

This often eliminates capital gains taxes if the asset is sold shortly thereafter

By contrast, when assets are gifted:

The original cost basis carries over to the recipient

Future capital gains taxes may be substantial

We frequently see individuals make costly mistakes by gifting assets as part of long-term care or estate planning—only to unintentionally shift a large tax burden to their children.

Alternatives to Outright Gifting

In many cases, there are more tax-efficient alternatives than outright gifting, including:

Trust-based planning

Gifting with a life estate (particularly for real estate)

Retaining assets to preserve step-up benefits

Coordinating gifting with broader estate and Medicaid planning

Choosing the right strategy depends on tax implications, asset types, long-term care planning, and family goals.

Our Gifting Strategy Articles

Frequently Asked Questions About Gifting Strategies

-

What is the annual gift tax exclusion?The annual gift tax exclusion allows individuals to gift up to a set amount per recipient each year without using lifetime gift or estate tax exemption.

-

Do I have to file a tax return if I make a gift?Cash gifts within the annual exclusion typically do not require filing. Larger gifts may require a gift tax return but do not necessarily result in taxes owed.

-

Does gifting reduce the size of my estate?Yes. Assets gifted during your lifetime are removed from your estate, which can help reduce estate tax exposure.

-

Is it better to gift assets now or leave them as an inheritance?It depends. Gifting can be beneficial in some cases, but retaining appreciated assets may preserve step-up in basis benefits.

-

What happens to cost basis when I gift an asset?The recipient inherits your original cost basis, which can lead to higher capital gains taxes when the asset is sold.

-

Is gifting cash better than gifting appreciated securities?Often, yes. Gifting cash avoids transferring embedded capital gains, whereas gifting appreciated securities can shift tax liability to the recipient.

-

Can gifting impact Medicaid eligibility?Yes. Gifts may trigger penalties under Medicaid look-back rules and must be carefully planned.

-

Should I work with a financial planner before gifting assets?Typically, yes. Gifting decisions affect taxes, estate planning, and family dynamics and should be evaluated as part of a comprehensive plan.

Contact Us . . . .

All of our services start with a complimentary consult. No high pressure sales tactics. We are financial planners, not salesmen.

About Our Firm: Greenbush Financial Group is an independent registered investment advisory firm based in Albany, New York, that provides four main services to clients: fee-based financial planning services, investment management, employer-sponsored retirement plans, and retirement planning services. The firm serves clients locally in the Albany region and virtually across the United States.