How to Minimize Taxes on Social Security

Many retirees are surprised to find that up to 85% of their Social Security benefits could be taxable. But with the right planning, it's possible to reduce or even eliminate those taxes.

The IRS determines how much of your Social Security is taxable using your provisional income, which includes:

Your adjusted gross income (AGI)

Plus any tax-exempt interest (such as from municipal bonds)

Plus 50% of your annual Social Security benefit

Example:

If your AGI is $20,000, you receive $5,000 in municipal bond interest, and your annual Social Security benefit is $30,000, your provisional income would be $40,000 — putting you in the 50% taxable range if you file your taxes married filing joint.

Based on this calculation, here are the income thresholds that determine how much of your benefit is taxable:

Single filers

$25,000 to $34,000 in provisional income: up to 50% of benefits may be taxable

Over $34,000: up to 85% may be taxable

Married filing jointly

$32,000 to $44,000 in provisional income: up to 50% of benefits may be taxable

Over $44,000: up to 85% may be taxable

Note: This doesn’t mean your benefits are taxed at 85%. Rather, it means up to 85% of your benefit amount is included in your taxable income and taxed at your ordinary income tax rate.

Strategies to Reduce or Eliminate Social Security Taxes

1. Delay Taking Social Security

Delaying benefits until age 70 not only increases your monthly payout, but also creates an income “gap window” where you can take advantage of other planning opportunities — such as Roth conversions — before your benefit starts impacting your tax return.

2. Draw Down Pre-Tax Assets Before Claiming

In the early years of retirement, before beginning Social Security, consider withdrawing from traditional IRAs or 401(k)s. These distributions are taxable now, but doing so may reduce your future required minimum distributions (RMDs), which in turn lowers taxable income once you begin collecting Social Security.

3. Consider Roth Conversions

Similar to item 2, Roth conversions allow you to shift money from a traditional IRA to a Roth IRA, paying tax now in order to avoid higher taxes later. By shifting money from a Traditioanl IRA to a Roth IRA prior to starting your social security benefit, it may keep you in lower tax brackets in future years especially when RMDs (requirement minimum distribution) begin at age 73 or 75. Also, once in a Roth IRA, future withdrawals are tax-free and do not count toward provisional income — helping keep more of your Social Security sheltered from taxation.

Note: Keep in mind that conversions count as income in the year they’re done — and can impact provisional income temporarily.

4. Use Qualified Charitable Distributions (QCDs)

QCDs allow individuals age 70½ or older to donate up to $100,000 per year directly from an IRA to a qualified charity. These donations count toward your RMD but are excluded from taxable income.

Clarification: The $100,000 QCD limit applies per individual IRA owner — so a married couple could potentially exclude up to $200,000 in charitable distributions if each spouse qualifies.

This is another way to reduce the size of a pre-tax retirement account balance which counts toward the RMD calculation. Also since the QCD counts toward the RMD amount it can reduce your taxable income, potentially making less of your Social Security benefit subject to taxation at the federal level.

Example: Sue is 78 and is required to take RMD from her traditional IRA of $10,000. Sue decides to process a QCD from her IRA sending $10,000 to her church. She has met the RMD requirement but the $10,000 does not represent taxable income to Sue. Sue’s provision income as a single filer is $30,000 making her Social Security benefit 50% taxable. If she did not process the QCD, that would have raised her provisional income to $40,000 making 85% of her social security benefit subject to taxation.

5. Be Cautious With Tax-Free Interest

Although interest from municipal bonds is federally tax-exempt and potentially state income tax, it is included in the provisional income calculation. If your portfolio includes significant tax-free bond income, it could unintentionally push you into the 50% or 85% taxable Social Security range.

Final Thoughts

Social Security is a cornerstone of retirement income, but managing how it’s taxed is just as important as deciding when to claim. The key to minimizing Social Security taxes is planning around when you claim benefits and where your income is coming from. Strategies like Roth conversions, QCDs, and pre-Social Security IRA withdrawals can all work together to help you keep more of your benefits.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

How does the IRS determine how much of my Social Security is taxable?

The IRS uses your “provisional income” to determine taxation, which includes your adjusted gross income (AGI), tax-exempt interest, and 50% of your annual Social Security benefits. Depending on your filing status and total provisional income, up to 50% or 85% of your Social Security benefits may be taxable.

What are the income thresholds for Social Security taxation?

For single filers, provisional income between $25,000 and $34,000 makes up to 50% of benefits taxable, and income above $34,000 makes up to 85% taxable. For married couples filing jointly, the 50% range applies between $32,000 and $44,000, with anything above $44,000 potentially making up to 85% taxable.

Does “85% taxable” mean I pay 85% tax on my benefits?

No. It means that up to 85% of your Social Security benefit is included in your taxable income and taxed at your ordinary income tax rate. You’re not taxed at 85%; rather, that portion is subject to your regular tax bracket.

How can I reduce or avoid taxes on my Social Security benefits?

You can lower taxable income by delaying Social Security, making Roth conversions before claiming benefits, or drawing down pre-tax accounts early in retirement. Using qualified charitable distributions (QCDs) from IRAs after age 70½ can also reduce taxable income and lower how much of your benefit is taxed.

How do Qualified Charitable Distributions (QCDs) affect Social Security taxation?

QCDs let you donate up to $100,000 per year directly from an IRA to a charity, satisfying required minimum distributions (RMDs) without increasing taxable income. By lowering your income, QCDs can reduce the portion of your Social Security benefits subject to tax.

Does tax-free interest from municipal bonds affect Social Security taxation?

Yes. Although municipal bond interest is exempt from federal income tax, it is included in the provisional income formula. Large amounts of tax-free interest can unintentionally increase the taxable portion of your Social Security benefits.

The Hidden Tax Traps in Retirement Most People Miss

Many retirees are caught off guard by unexpected tax hits from required minimum distributions (RMDs), Social Security, and even Medicare premiums. In this article, we break down the most common retirement tax traps — and how smart planning can help you avoid them.

Most people think retirement is the end of tax planning. But nothing could be further from the truth. There are several tax traps that retirees encounter, which range from:

How RMDs create tax surprises

How Social Security is taxed

How Medicare Premiums (IRMAA) are affected by income

A lack of tax-specific distribution planning

We will be covering each of these tax traps in this article to assist retirees in avoiding these costly mistakes in the retirement years.

RMD Tax Surprises

Once you reach a specific age, the IRS requires individuals to begin taking mandatory distributions from their pre-tax retirement accounts, called RMDs (required minimum distributions). Distributions from pre-tax retirement accounts represent taxable income to the retiree, which requires advanced planning to ensure that that income is not realized at an unnecessarily high tax rate.

All too often, Retirees will make the mistake of putting off distributions from their pre-tax retirement accounts until RMDs are required to begin, which allows the pretax accounts to accumulate and become larger during retirement, which in turn requires larger distributions once the RMD start age is reached.

Here is a common example: Tim and Sue retire from New York State at age 55 and both have pensions that are more than enough to meet their current expenses. Both of them also have retirement accounts through NYS, totaling $500,000. Assuming Tim and Sue start taking their required minimum distributions (RMDs) at age 75, and since Tim and Sue do not need to take withdrawals from their retirement account to supplement their income, those retirement accounts could grow to over $1,000,000. This sounds like a good thing, but it creates a potential tax problem. By age 75, they’ll both be receiving their pensions and have turned on Social Security, which under current tax law is 85% taxable at the federal level. On top of that, they’ll need to take a required minimum distribution of $37,735 which stacks up on top of all their other income sources.

This additional income from age 75 and beyond could:

Be subject to higher tax rates

Trigger higher Medicare Premiums

Cause them to phase out of certain tax deductions or credits

In hindsight, it may have been more prudent for Tim & Sue to begin taking distributions from their retirement accounts each year beginning the year after they retired, to avoid many of these unforeseen tax consequences 20 years after they retired.

How Is Social Security Taxed?

I start this section by saying, based on current law, because the Trump administration has on its agenda to make social security tax-free at the Federal level. At the time of this article, social security is potentially subject to taxation at the federal level for individuals based on their income. A handful of states also tax social security benefits.

Here is a quick summary of the proportion of social security benefits subject to taxation at the Federal level in 2025:

0% Taxable: Combined income for single filers below $25,000 and joint filers below $32,000.

50% Taxable: Combined income for single filers between $25,000 - $34,000 and joint filers between $32,000 - $44,000

85% Taxable: Combined income for single filers above $34,000 and joint filers above $44,000.

One-time events that occur in retirement could dramatically impact the amount of a retiree's social security benefit, subject to taxation. For example, a retiree might sell a stock at a gain in a brokerage account, surrender an insurance policy, earn part-time income, or take a distribution from a pre-tax retirement account. Any one of these events could inadvertently trigger a larger tax liability associated with the amount of an individual’s social security that is subject to taxation at the Federal level.

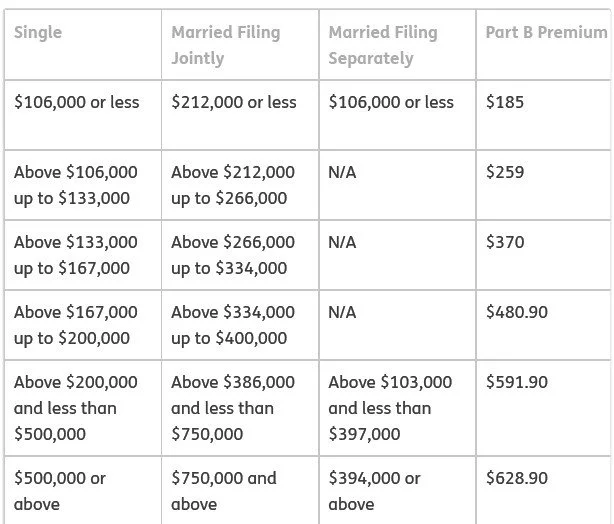

Medicare Premiums Are Income-Based

When you turn age 65, many retirees discover for the first time that there is a cost associated with enrolling in Medicare, primarily in the form of the Medicare Part B premiums that are deducted directly from a retiree's monthly social security benefit. The tax trap is that if a retiree shows too much income in a given year, it can cause their Medicare premium to increase for 2 years in the future.

Medicare looks back at your income from two years prior to determine the amount of your Medicare Part B premium in the current year. Here is the Medicare Part B premium table for 2025:

As you can see from the table, as income rises, so does the monthly premium charged by Medicare. There are no additional benefits, the retiree just has to pay more for their Medicare coverage.

This is where those higher RMDs can come back to haunt retirees once they reach the RMD start age. They might be ok between ages 65 – 75, but once they hit age 75 and must start taking RMDs from their pre-tax retirement accounts, those pre-tax RMD’s can sometimes push retirees over the Medicare based premium income threshold, and then they end up paying higher premiums to Medicare for the rest of their lives that could have been avoided.

Lack of Retirement Distribution Planning

All these tax traps surface due to a lack of proper distribution planning as an individual enters retirement. It’s incredibly important for retirees to look at their entire asset picture leading up to retirement, determine the income level that is needed to cover expenses in their retirement year, and then construct a long-term distribution plan that allows them to minimize their tax liability over the remainder of their life expectancy. This may include:

Processing sizable distributions from pre-tax accounts early in the retirement years

Processing Roth conversions

Delaying to file for social security

Developing a tax plan for surrendering permanent life insurance policies

Evaluating pension and annuity elections

A tax plan for realizing gains in taxable investment accounts

Forecasting RMDs at age 73 or 75

Developing a robust distribution plan leading up to retirement can potentially save retirees thousands of dollars in taxes over the long run and avoid many of the pitfalls and tax traps that we reviewed in the article today.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

Why is tax planning still important in retirement?

Many retirees assume that once they stop working, tax planning ends. In reality, retirement can bring new tax challenges — including required minimum distributions (RMDs), Social Security taxation, and income-based Medicare premium increases — that require proactive management to avoid costly surprises.

How do required minimum distributions (RMDs) create tax surprises?

Starting at age 73 or 75 (depending on birth year), retirees must begin taking taxable withdrawals from pre-tax retirement accounts. These RMDs can push retirees into higher tax brackets, increase Medicare premiums, and cause more of their Social Security benefits to become taxable if withdrawals aren’t planned carefully in advance.

Can delaying IRA withdrawals until RMD age cause higher taxes later?

Yes. Deferring all withdrawals until RMDs begin can cause retirement accounts to grow substantially, leading to larger mandatory distributions later in life. Spreading withdrawals earlier in retirement can help manage tax brackets, reduce future RMDs, and potentially lower long-term taxes.

How is Social Security taxed at the federal level?

In 2025, up to 85% of Social Security benefits may be taxable depending on your combined income (adjusted gross income + tax-exempt interest + 50% of benefits). For joint filers, benefits become partially taxable above $32,000 and up to 85% taxable above $44,000.

What income sources can increase the taxation of Social Security?

Capital gains, part-time wages, insurance policy surrenders, or withdrawals from pre-tax retirement accounts can all raise taxable income and cause a greater portion of Social Security benefits to become taxable.

How do Medicare premiums (IRMAA) depend on income?

Medicare Part B and Part D premiums increase for retirees with higher incomes, based on a two-year income lookback. For example, your 2025 premiums are based on your 2023 tax return. Large one-time income events — such as Roth conversions or asset sales — can trigger higher Medicare premiums for two years.

What strategies can help retirees reduce tax traps?

Effective planning may include drawing down pre-tax accounts earlier, using Roth conversions in low-income years, managing capital gains, and coordinating income sources to control how much is exposed to higher taxes or Medicare surcharges.