The New $40,000 SALT Cap: What It Means for Taxpayers After the Big Beautiful Tax Bill

Congress just passed the “Big Beautiful Tax Bill,” and one of the biggest changes is a major update to the SALT (State and Local Tax) deduction cap. Instead of being limited to $10,000, some taxpayers will now be eligible for a $40,000 SALT deduction — but only temporarily and only if certain income limits are met.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

After months of negotiation and political tug-of-war, Congress has officially passed what’s being dubbed the “Big Beautiful Tax Bill.” While the legislation covers a broad range of tax reforms, one of the most talked-about provisions is the dramatic change to the SALT (State and Local Tax) deduction cap—raising it from the current $10,000 to a new maximum of $40,000 for some taxpayers. If you’ve felt handcuffed by the old SALT limits, this update could provide much-needed relief—but the details matter.

In this article we will cover:

The effective date of the new $40,000 SALT Cap

Income limitations for single and joint filers

The SALT phaseout calculation

Who benefits the most from the higher SALT Cap?

Do you have to itemize to capture the new SALT Cap?

When the new $40,000 SALT Cap expires

Quick Refresher: What Is the SALT Deduction?

The SALT deduction allows taxpayers who itemize to deduct certain state and local taxes from their federal taxable income. This typically includes:

State and local income taxes

Property taxes paid on real estate

Under the 2017 Tax Cuts and Jobs Act (TCJA), this deduction was capped at $10,000, which hit high-tax states like New York, New Jersey, California, and Massachusetts especially hard. Many taxpayers in those states were no longer able to deduct their full property and income tax payments, resulting in higher federal tax bills.

What’s in the New Bill?

The Big Beautiful Tax Bill raises the SALT cap from $10,000 to $40,000, but with a few catches:

Income limitations apply

The increase applies only to tax years 2025 through 2029.

Starting in 2030, the cap reverts back to $10,000 (unless future legislation says otherwise).

You have to itemize to capture the SALT deduction

So, this is a temporary reprieve—but for many, a meaningful one.

Who Benefits Most?

This new SALT cap will be most beneficial to:

Homeowners in high-tax states (especially those with large property tax bills)

High-income earners who pay significant state income taxes

Taxpayers who itemize deductions (rather than taking the standard deduction)

If you're someone who was paying $25,000–$40,000 in combined state income and property taxes, this change could mean an additional $15,000–$30,000 in deductions, depending on your filing status.

That’s real money back in your pocket—especially if you're in a higher federal tax bracket.

Income Phase‑Outs: Who Gets How Much

While the new SALT cap jump to $40,000 is significant, its benefit isn't universal. There are income limitations for taxpayers based on their modified adjusted gross income.

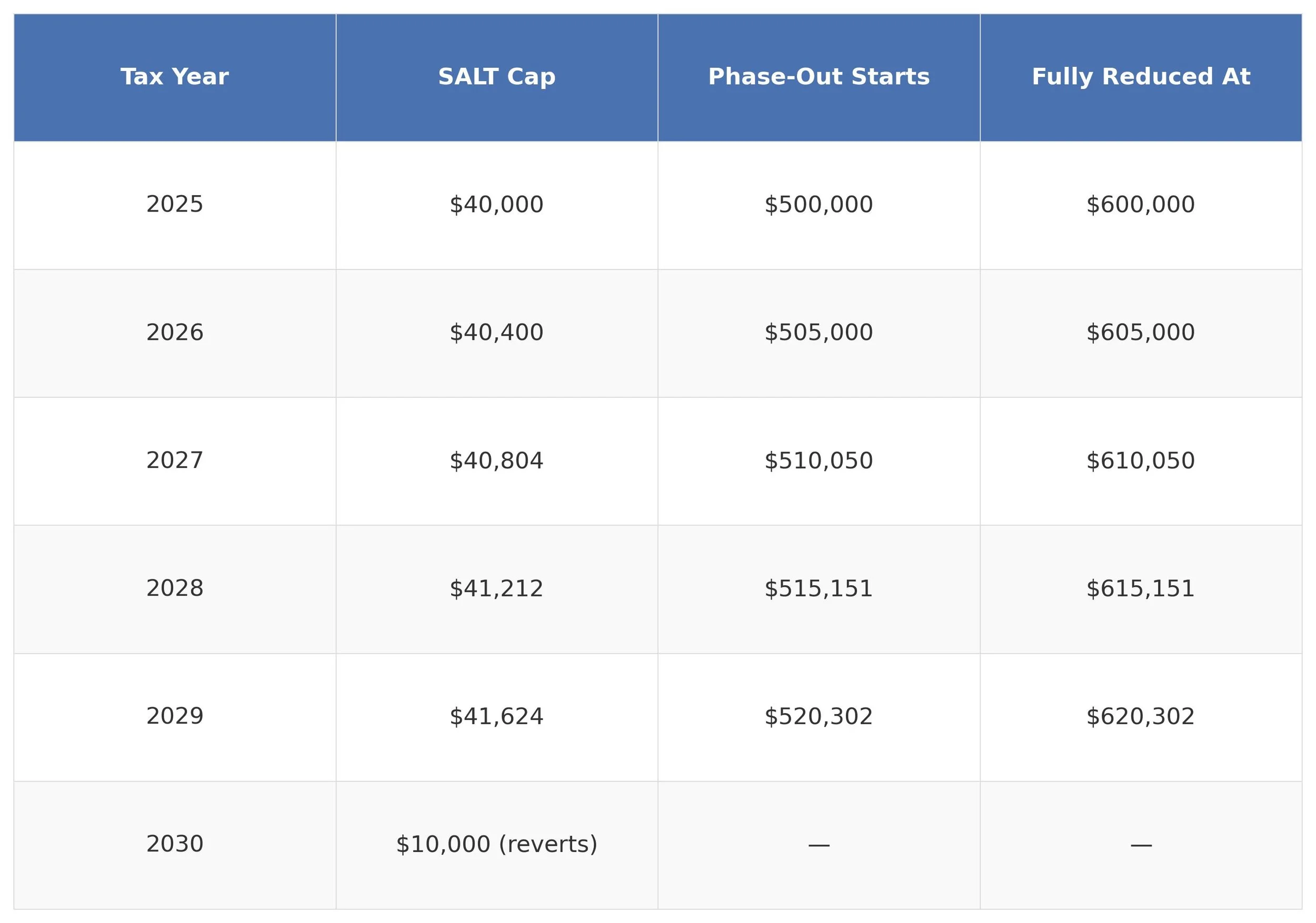

For tax year 2025, the full SALT cap applies to filers with Modified AGI less than $500,000

MAGI between $500,000 and $600,000: The cap is reduced by 30% of the income over $500,000.

Above MAGI $600,000, the cap is back down to $10,000—the same as the old limit.

Starting in 2026, both the cap and phase-out threshold rise 1% per year, with the reductions continuing until 2029. The $10,000 ceiling returns permanently in 2030

How the Phase‑Out Plays Out

Note: The deduction cannot be reduced below the old $10,000

Does Your Tax Filing Status Matter

The MAGI income thresholds are based on “household income” so both single filers and married filing joint filers have the same income limitations and phaseout range for the new $40,000 SALT Cap. However, for taxpayers who file married filing separately, the new max SALT Cap is $20,000.

Tax Planning Opportunities

If you fall into the group of taxpayers who stand to benefit, here are some strategies to consider:

1. Bunching Deductions

With the cap going up temporarily, it may make sense to accelerate state tax payments or property tax prepayments into the eligible years (2025–2029) to maximize the benefit.

2. Reevaluating Itemized vs. Standard Deduction

Many filers defaulted to the standard deduction under TCJA because of the $10,000 SALT cap. But with the cap raised, it’s time to revisit whether itemizing now produces a better tax result.

3. Rethinking Income Timing

If you have control over how and when you recognize income (e.g., through bonuses, deferred comp, self-employment, or retirement distributions), you might explore ways to align higher-income years with the higher SALT cap window.

4. AMT Considerations

While not as widespread as in the past, the Alternative Minimum Tax (AMT) can still limit your ability to take advantage of certain deductions—including SALT. Make sure your tax preparer checks how the new cap interacts with AMT exposure.

Final Thoughts

The new $40,000 SALT cap is a welcome change for many taxpayers who have felt the squeeze over the past few years. But it’s a temporary window of opportunity, and one that requires careful planning to take full advantage of.

If you live in a high-tax state, this change could have a significant impact on your tax strategy moving forward. As always, consult with your financial planner or tax advisor to determine how these changes fit into your overall financial picture.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What is the new $40,000 SALT deduction cap?

Under the Big Beautiful Tax Bill, the State and Local Tax (SALT) deduction cap increases from $10,000 to $40,000 for eligible taxpayers beginning in 2025. The expanded cap applies to combined state income and property taxes but is temporary—set to expire after 2029.

Who benefits most from the higher SALT cap?

The change primarily benefits homeowners and high-income earners in high-tax states such as New York, New Jersey, California, and Massachusetts. Those who pay substantial property and state income taxes and who itemize deductions stand to gain the most.

When does the new $40,000 SALT cap take effect—and when does it expire?

The increased cap is effective for tax years 2025 through 2029. Beginning in 2030, the cap reverts to the previous $10,000 limit unless new legislation extends it.

Are there income limits for the new SALT deduction?

Yes. The full $40,000 cap applies to taxpayers with Modified Adjusted Gross Income (MAGI) under $500,000. Between $500,000 and $600,000, the cap is reduced by 30% of the income over $500,000. Above $600,000 MAGI, the deduction returns to the old $10,000 limit.

Do you need to itemize to use the $40,000 SALT deduction?

Yes. The SALT deduction is only available to taxpayers who itemize deductions on their federal tax return. If you claim the standard deduction, you cannot take advantage of the higher SALT cap.

What tax strategies can help maximize the new SALT deduction?

Taxpayers can “bunch” property or state tax payments into the eligible years (2025–2029), reevaluate whether to itemize, and time income recognition to align with the higher cap window. Consulting a tax professional can help optimize these strategies within IRS guidelines.

Will the Alternative Minimum Tax (AMT) affect the SALT deduction?

It might. The AMT can limit or disallow SALT deductions, depending on your income level and deductions. Taxpayers subject to AMT should review how the new cap interacts with their overall tax situation.