Tax Planning

A Core Pillar of Every Comprehensive Financial Plan

Tax planning and tax strategy are critical components of a well-designed financial plan—regardless of your stage of life. Taxes impact how much you save, how much you keep, how efficiently you retire, and how much ultimately passes to the next generation. Without proactive planning, taxes can quietly erode long-term wealth.

At Greenbush Financial Group, we integrate tax strategy into every facet of the financial planning process. Rather than treating taxes as a once-a-year exercise, we view them as an ongoing planning opportunity that evolves as your income, goals, and life circumstances change.

We generally organize tax planning into four key categories:

Tax Planning for Self-Employed Individuals

Tax Planning While You’re Still Working

Tax Planning in the Retirement Years

Tax Planning for Inheritance and Estate Planning

Each stage presents unique opportunities—and missing them can be costly.

Tax Planning for Self-Employed Individuals

Being self-employed opens the door to a wide range of tax strategies that are not available to W-2 employees or corporate executives. Business owners have significantly more control over how income is earned, taxed, deferred, and reinvested.

We are uniquely positioned to assist self-employed individuals because the founding partner of Greenbush Financial Group, David Wojeski, is also the Managing Partner of Wojeski & Company CPA firm which is located right across the hall from our office. This allows for close collaboration between financial planning and tax expertise.

Tax planning for self-employed clients typically includes:

Evaluating business entity structure

Reviewing current tax strategies and deductions

Aligning business cash flow with personal investment goals

Identifying additional opportunities to lower overall tax liability

Designing tax-efficient exit and business-sale strategies

One of the most significant tax events a business owner may face is the sale of their business, which requires years of advance planning to manage capital gains, timing, and structure.

Self-employed individuals also have the ability to choose from a wide range of employer-sponsored retirement plans, which are often among the most powerful tools available to reduce current taxes while building long-term wealth. We have indepth knowledge of the various employer sponsored retirement plans available to assist our clients with identifying the ideal type of retirement plan and plan design to meet their tax needs.

Tax Planning While You’re Still Working (Accumulation Years)

The accumulation years—when income is at its highest—offer a number of tax strategies that disappear once earned income stops. This makes proactive planning during working years especially important.

Key areas of focus include:

Pre-tax vs. Roth contributions to employer-sponsored plans

Executive deferred compensation plan options

Stock options and restricted stock plans

Backdoor Roth IRA contributions for high-income earners

Health Savings Accounts (HSAs)

529 college savings plans (state tax deductions?)

Tax-efficient investment solutions

We help clients coordinate tax strategies with other financial goals such as college funding, retirement savings, cash flow planning. and long-term investment planning.

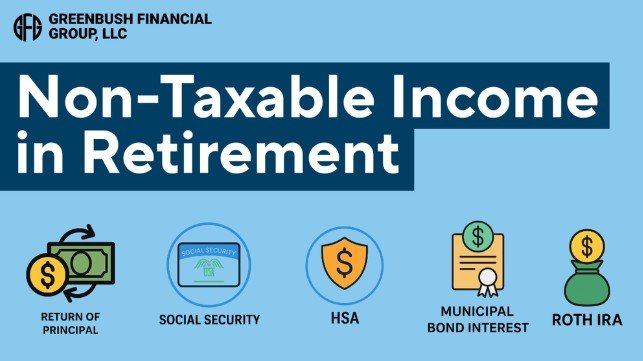

Tax Planning in the Retirement Years

Contrary to popular belief, tax planning often becomes more complex once someone retires. Without W-2 income or business earnings, retirees gain greater control over their taxable income—but that flexibility requires careful planning.

In retirement, income may come from:

Social Security

Pensions

Required Minimum Distributions (RMDs)

Investment income

Roth accounts

Each source is taxed differently. A key part of retirement tax planning is determining:

Which accounts to draw from first

How to manage tax brackets over time

How withdrawals affect Medicare premiums (IRMAA)

When Roth conversions make sense

How to minimize lifetime tax liability—not just annual taxes

Distribution strategy becomes one of the most important tools for controlling taxes throughout retirement.

Tax Planning for Inheritance and Estate Planning

For clients who expect to leave assets to children, grandchildren, or other heirs, tax planning extends beyond their own lifetime.

Our goal in estate and inheritance tax planning is to:

Reduce taxes paid across generations

Structure assets to avoid probate

Evaluate Roth conversions as a legacy tool

Coordinate beneficiary designations

Incorporate trusts where appropriate

Minimize federal and state estate or inheritance taxes

With recent IRS rule changes affecting non-spouse beneficiaries, proactive planning is essential to preserve family wealth and avoid unnecessary taxation.

An Integrated, Collaborative Approach to Tax Strategy

Tax strategy is not a standalone service—it is woven into every financial plan we build. One of Greenbush Financial Group’s key advantages is the ability to collaborate directly with in-house accounting professionals when developing and implementing strategies.

This integrated approach allows us to:

Identify overlooked tax opportunities

Coordinate tax planning across life stages

Reduce overall lifetime tax liability

Align tax decisions with investment and retirement goals

Our objective is simple: help clients achieve their financial goals while minimizing their tax liability.

Our Tax Planning Articles

“Michael’s videos break down complex tax and financial topics in the clearest way possible. His explanation of investment loss deductions was a game-changer for me. Highly recommended!⭐⭐⭐⭐⭐”

This endorsement provided for Greenbush Financial Group, LLC on Google Review was made by a non-client, and it was a non-paid review. This non-client was solicited by Greenbush Financial Group, LLC to provide the endorsement.

“Michael was incredibly knowledgeable in a very nuanced tax law that I’ve been trying to get to the bottom of for months, elsewhere.⭐⭐⭐⭐⭐”

This endorsement provided for Greenbush Financial Group, LLC on Google Review was made by a non-client, and it was a non-paid review. This non-client was solicited by Greenbush Financial Group, LLC to provide the endorsement.

“Great video! Cleared up some confusion I had about the child tax credit.”

This endorsement provided for Greenbush Financial Group, LLC on YouTube was a non-solicited and non-paid comment by a non-client.

“Michael, I just found you on YT. I appreciate the way you get straight to the tax code without the usual time wasters or unrealistic scenarios. Thumbs up.”

This endorsement provided for Greenbush Financial Group, LLC on YouTube was a non-solicited and non-paid comment by a non-client.

Frequently Asked Questions About Tax Planning & Retirement

-

Why is tax planning important in retirement?Because retirees can often control when and how income is recognized, tax planning can significantly reduce lifetime taxes, Medicare premiums, and the risk of large tax spikes later in retirement.

-

What is the difference between tax preparation and tax planning?Tax preparation looks backward and reports what already happened. Tax planning looks forward and helps structure decisions to reduce future taxes.

-

When should I start tax planning for retirement?Ideally, tax planning should begin years before retirement. Many of the most effective strategies are only available while you still have earned income.

-

How do Roth conversions fit into tax planning?Roth conversions can reduce future RMDs, lower Medicare premiums, and create tax-free income later. They are often most effective in early retirement years.

-

How do taxes affect Social Security and Medicare premiums?Higher income can cause Social Security benefits to be taxed and trigger higher Medicare premiums through IRMAA. Tax planning helps manage these thresholds.

-

Is tax planning different for self-employed individuals?Yes. Business owners have access to additional deductions, retirement plans, and entity-level strategies that require specialized planning.

-

How does tax planning help with inheritance and estate planning?Tax planning can reduce the tax burden on heirs, especially under current rules requiring inherited retirement accounts to be distributed within 10 years.

-

Should I work with a financial planner or a CPA for tax strategy?The most effective approach is collaboration. A certified financial planner helps integrate tax strategy with investments, retirement, and estate planning—often working closely with a CPA.

Contact Us . . . .

All of our services start with a complimentary consult. No high pressure sales tactics. We are financial planners, not salesmen.

About Our Firm: Greenbush Financial Group is an independent registered investment advisory firm based in Albany, New York, that provides four main services to clients: fee-based financial planning services, investment management, employer-sponsored retirement plans, and retirement planning services. The firm serves clients locally in the Albany region and virtually across the United States.