Removing Excess Contributions From A Roth IRA

If you made the mistake of contributing too much to your Roth IRA, you have to go through the process of pulling the excess contributions back out of the Roth IRA. The could be IRS taxes and penalties involved but it’s important to understand your options.

You discovered that you contributed too much to your Roth IRA, now it’s time to fix it. This most commonly happens when individuals make more than they expected which causes them to phaseout of their ability to make a contribution to their Roth IRA for a particular tax year. In 2026, the phase out ranges for Roth IRA contributions are:

· Single Filer: $153,000 - $167,999

· Married Filing Joint: $242,000 - $251,999

The good news is there are a few options available to you to fix the problem but it’s important to act quickly because as time passes, certain options for removing those excess IRA contributions will be eliminated.

You Discover The Error Before You File Your Taxes

If you discover the contribution error prior to filing your tax return, the most common fix is to withdraw the excess contribution amount plus EARNINGS by your tax filing deadline, April 18th. Custodians typically have a special form for removing excess contributions from your Roth IRA that you will need to complete.

If you withdraw the excess contribution before the tax deadline, you will avoid having to pay the IRS 6% excise penalty on the contribution, but you will still have to pay income tax on the earnings generated by the excess contribution. In addition, if you are under the age of 59½, you will also have to pay the 10% early withdrawal penalty on just the earnings portion of the excess contribution.

Example, you contribute $6,000 to your Roth IRA in September 2025 but you find out in March 2026 that your income level only allows you to make a $2,000 contribution to your Roth IRA for 2025 so you have a $4,000 excess contribution. You will have to withdraw not just the $4,000 but also the earnings produced by the $4,000 while it was in the account, for purposes of this example let’s assume that’s $400. The $4,000 is returned to you tax and penalty free but when the $400 in earnings is distributed from the account, you will have to pay tax on the earnings, and if under age 59½, a 10% withdrawal penalty on the $400.

October 15th Deadline

If you have already filed your taxes and you discover that you have an excess contribution to a Roth IRA, but it’s still before October 15th, you can avoid having to pay the 6% penalty by filing an amended tax return. You still have pay taxes and possibly the 10% early withdrawal penalty on the earnings but you avoid the 6% penalty on the excess contribution amount. This is only available until October 15th following the tax year that the excess contribution was made.

You Discover The Mistake After The October 15th Extension Deadline

If you already filed your taxes and you did not file an amended tax return by October 15th, the IRS 6% excess contribution penalty applies. If you contributed $6,000 to Roth IRA but your income precluded you from contributing anything to a Roth IRA in that tax year, it would result in a $360 (6%) penalty. But it’s important to understand that this is not a one-time 6% penalty but rather a 6% PER YEAR penalty on the excess amount UNTIL the excess amount is withdrawn from the Roth IRA. If you discovered that 5 years ago you made a $5,000 excess contribution to your Roth IRA but you never removed the excess contributions, it would result in a $1,500 penalty.

6% x 5 Years = 30% Total Penalty x $5,000 Excess Contribution = $1,500 IRS Penalty

A 6% Penalty But No Earnings Refund

Here’s a little known fact about the IRS excess contribution rules, if you are subject to the 6% penalty because you did not withdraw the excess contributions out of your Roth IRA prior to the tax deadline, when you go to remove the excess contribution, you are no longer required to remove the earnings generated by the excess contribution.

Reminder: If you remove the excess contribution prior to the initial tax deadline, you AVOID the 6% penalty on the excess contribution amount but you have to pay taxes and possibly the 10% early withdrawal penalty on just the earnings portion of the excess contribution.

If you remove the excess contribution AFTER the tax deadline, you do not have to pay taxes or penalties on the EARNINGS portion because you are not required to distribute the earnings, but you pay a flat 6% penalty per year based on the actual excess contribution amount.

Example: You contributed $6,000 to your Roth IRA in 2025, your income ended up being too high to allow any Roth IRA contributions in 2025, you discover this error in November 2026. You will have to withdraw the $6,000 excess contribution, pay the 6% penalty of $360, but you do not have to distribute any of the earnings associated with the excess contribution.

Why does it work this way? This is only a guess but since most taxpayers probably try to remove the excess contributions as soon as possible, maybe the 6% IRS penalty represents an assumed wipeout of a modest rate of return generated by those excess contributions while they were in the IRA.

Advanced Tax Strategy

There is an advanced tax strategy that involves evaluating the difference between the flat 6% penalty on the excess contribution amount and paying tax and possibly the 10% penalty on the earnings. Before I explain the strategy, I strongly advise that you consult with your tax advisor before executing this strategy.

I’ll show you how this works in an example. You make a $6,000 contribution to your Roth IRA in 2025 but then find out in March 2026 that based on your income, you are not allowed to make a Roth contribution for 2025. Your Roth IRA experienced a 50% investment return between the time you made the $6,000 contribution and now. You are 35 years old. So now you have a choice:

Option A: Prior to your 2025 tax filing, withdraw the $6,000 tax and penalty free, and also withdraw the $3,000 in earnings which will be subject to ordinary income tax and a 10% penalty. Assuming you are in a 32% Fed bracket, 6% State Bracket, that would cost you 48% in taxes and penalties on the $3,000 in earnings.

Total Taxes and Penalties = $1,440

Option B: Waiting until November 2026, pull out the $6,000 excess contribution, and pay the 6% penalty, but you get to leave the $3,000 in earnings in your Roth IRA. $6,000 x 6% = $360

Total Taxes and Penalties = $360

PLUS you have an additional $3,000 that gets to stay in your Roth IRA, compound returns, and then be withdrawn tax and penalty free after age 59½.

FINANCIAL NERD NOTE: If the only balance in your Roth IRA is from earnings that originated from excess contributions, it’s does not start the 5-year holding period required to receive the Roth IRA earnings tax free after age 59½ because they are considered ineligible contributions retained within the Roth IRA.

Losses Within The Roth IRA

Since I’m writing this in March 2026 and most of the equity indexes are down year-to-date, I’ll explain how losses within a Roth IRA impact the excess contribution calculation. If your Roth IRA has lost value between the time you made the excess contribution and the withdrawal date, it does reduce the amount that you have to withdraw from the IRA. If your excess contribution amount is $3,000 but the Roth IRA dropped 20% in value, you would only have to withdraw $2,400 from the Roth IRA to satisfy the removal of the excess contributions. If withdrawn prior to your tax filing deadline, no taxes or penalties would be due because there were no earnings.

Other Options Besides Cash Withdrawals

Up until now we have just talked about withdrawing the excess contribution from your IRA by taking the cash back but there are a few other options that are available to satisfy the excess contribution rules.

The first is “recharacterizing” your excess Roth contribution as a traditional IRA contribution. If your income allows, you may be able to transfer the excess Roth contribution amount and earnings from your Roth IRA to your Traditional IRA but this must be done in the same tax year to avoid the 6% penalty.

Second option, if you are eligible to make a Roth IRA contribution the following year, the excess contribution can be used to offset the Roth contribution amount for the following tax year. Example, if you had an excess Roth IRA contribution of $1,000 in 2025 and your income will allow you to make a $6,000 Roth IRA contribution in 2026, you can reduce the Roth contribution limit by $1,000 in 2026, leave the excess in the account, and just deposit the remaining $5,000. You would still have to pay the 6% penalty on the $1,000 because you never withdrew it from the Roth IRA but it’s $60 penalty versus having to take the time to go through the excess withdrawal process.

Which Contributions Get Pulled Out First

It’s not uncommon for investors to make monthly contributions to their Roth IRA accounts but when it comes to an excess contribution scenario, you don’t get to choose which contributions are entered into the earning calculation. The IRS follows the LIFO (last-in-first-out) method for determining which contributions should be removed to satisfy the excess refund.

You Have Multiple IRA’s

If you have multiple Roth IRA’s and there is an excess contribution, you have to remove the excess contribution from the same Roth IRA that the contribution was made to, you can’t take it from a different Roth IRA to satisfy the removal of the excess.

If you have both a Traditional IRA and a Roth IRA and you exceed the aggregate contribution limit for the year, by default, the IRS assumes the excess contribution was made to the Roth IRA, so you have to begin taking corrective withdrawals from your Roth IRA first.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What happens if I contribute too much to my Roth IRA?

If your income is too high or you accidentally contribute more than the annual Roth IRA limit, the excess amount is considered an “excess contribution.” The IRS assesses a 6% penalty each year that the excess remains in the account until it’s corrected.

How can I fix a Roth IRA excess contribution before filing my taxes?

If you catch the mistake before your tax filing deadline (typically April 15), you can withdraw the excess contribution and any earnings. You’ll avoid the 6% penalty, but the earnings portion is taxable—and may be subject to a 10% early withdrawal penalty if you’re under age 59½.

What if I already filed my tax return but it’s before October 15?

You can file an amended return and withdraw the excess contribution plus earnings before October 15 to avoid the 6% excise tax. However, you’ll still owe income taxes and possibly the 10% early withdrawal penalty on the earnings portion.

What happens if I discover the excess contribution after October 15?

Once the October 15 deadline passes, you can no longer avoid the 6% annual penalty. The penalty continues each year until the excess amount is removed from your Roth IRA, but you no longer have to withdraw the earnings associated with that excess contribution.

Can I recharacterize or apply the excess contribution to a future year?

Yes. You can recharacterize the excess Roth contribution as a traditional IRA contribution, if eligible, by transferring it and any earnings. Alternatively, you can apply the excess toward next year’s contribution limit, but you’ll owe a 6% penalty for the current year.

What if my Roth IRA lost money after I made the excess contribution?

If the value of your Roth IRA declines, you only need to withdraw the reduced value of the excess contribution. For example, if your $3,000 excess contribution dropped 20% in value, you would only withdraw $2,400, and no taxes or penalties would apply if withdrawn before the filing deadline.

How does the IRS determine which contributions to remove?

The IRS uses a last-in, first-out (LIFO) method, meaning the most recent contributions are treated as the ones being withdrawn first. Excess withdrawals must come from the same Roth IRA where the contribution was made.

Last updated June, 2026

Can You Contribute To An IRA & 401(k) In The Same Year?

There are income limits that can prevent you from taking a tax deduction for contributions to a Traditional IRA if you or your spouse are covered by a 401(k) but even if you can’t deduct the contribution to the IRA, there are tax strategies that you should consider

The answer to this question depends on the following items:

Do you want to contribute to a Roth IRA or Traditional IRA?

What is your income level?

Will the contribution qualify for a tax deduction?

Are you currently eligible to participate in a 401(k) plan?

Is your spouse covered by a 401(k) plan?

If you have the choice, should you contribute to the 401(k) or IRA?

Advanced tax strategy: Maxing out both and spousal IRA contributions

Traditional IRA

Traditional IRA’s are known for their pre-tax benefits. For those that qualify, when you make contributions to the account you receive a tax deduction, the balance accumulates tax deferred, and then you pay tax on the withdrawals in retirement. The IRA contribution limits for 2025 are:

Under Age 50: $7,500

Age 50+: $8,600

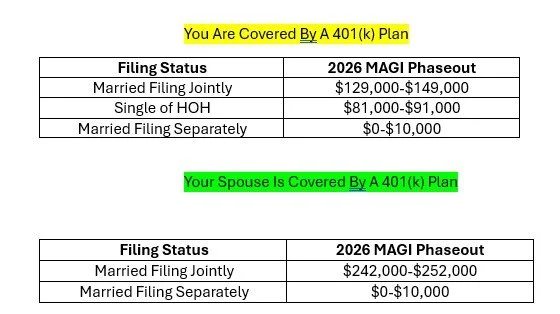

However, if you or your spouse are covered by an employer sponsored plan, depending on your level of income, you may or may not be able to take a deduction for the contributions to the Traditional IRA. Here are the phaseout thresholds for 2025:

Note: If both you and your spouse are covered by a 401(k) plan, then use the “You Are Covered” thresholds above.

BELOW THE BOTTOM THRESHOLD: If you are below the thresholds listed above, you will be eligible to fully deduct your Traditional IRA contribution

WITHIN THE PHASEOUT RANGE: If you are within the phaseout range, only a portion of your Traditional IRA contribution will be deductible

ABOVE THE TOP THRESHOLD: If your MAGI (modified adjusted gross income) is above the top of the phaseout threshold, you would not be eligible to take a deduction for your contribution to the Traditional IRA

After-Tax Traditional IRA

If you find that your income prevents you from taking a deduction for all or a portion of your Traditional IRA contribution, you can still make the contribution, but it will be considered an “after-tax” contribution. There are two reasons why we see investors make after-tax contributions to traditional IRA’s. The first is to complete a “Backdoor Roth IRA Contribution”. The second is to leverage the tax deferral accumulation component of a traditional IRA even though a deduction cannot be taken. By holding the investments in an IRA versus in a taxable brokerage account, any dividends or capital gains produced by the activity are sheltered from taxes. The downside is when you withdraw the money from the traditional IRA, all of the gains will be subject to ordinary income tax rates which may be less favorable than long term capital gains rates.

Roth IRA

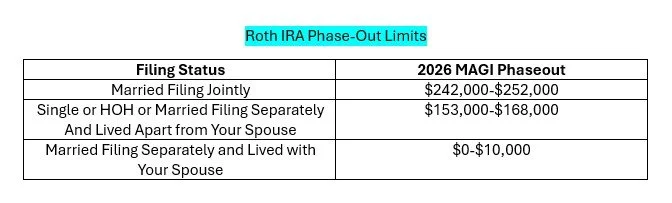

If you are covered by a 401(K) plan and you want to make a contribution to a Roth IRA, the rules are more straight forward. For Roth IRAs, you make contributions with after-tax dollars but all the accumulation is received tax free as long as the IRA has been in existence for 5 years, and you are over the age of 59½. Unlike the Traditional IRA rules, where there are different income thresholds based on whether you are covered or your spouse is covered by a 401(k), Roth IRA contributions have universal income thresholds.

The contribution limits are the same as Traditional IRA’s but you have to aggregate your IRA contributions meaning you can’t make a $7,500 contribution to a Traditional IRA and then make a $7,500 contribution to a Roth IRA for the same tax year. The IRA annual limits apply to all IRA contributions made in a given tax year.

Should You Contribute To A 401(k) or an IRA?

If you have the option to either contribute to a 401(k) plan or an IRA, which one should you choose? Here are some of the deciding factors:

Employer Match: If the company that you work for offers an employer matching contribution, at a minimum, you should contribute the amount required to receive the full matching contribution, otherwise you are leaving free money on the table.

Roth Contributions: Does your 401(k) plan allow Roth contributions? Depending on your age and tax bracket, it may be advantageous for you to make Roth contributions over pre-tax contributions. If your plan does not allow a Roth option, then it may make sense to contribute pre-tax up the max employer match, and then contribute the rest to a Roth IRA.

Fees: Is there a big difference in fees when comparing your 401(k) account versus an IRA? With 401(k) plans, typically the fees are assessed based on the total assets in the plan. If you have a $20,000 balance in a 401(K) plan that has $10M in plan assets, you may have access to lower cost mutual fund share classes, or lower all-in fees, that may not be available within a IRA.

Investment Options: Most 401(k) plans have a set menu of mutual funds to choose from. If your plan does not provide you with access to a self-directed brokerage window within the 401(k) plan, going the IRA route may offer you more investment flexibility.

Easier Is Better: If after weighing all of these options, it’s a close decision, I usually advise clients that “easier is better”. If you are going to be contributing to your employer’s 401(k) plan, it may be easier to just keep everything in one spot versus trying to successfully manage both a 401(k) and IRA separately.

Maxing Out A 401(k) and IRA

As long as you are eligible from an income standpoint, you are allowed to max out both your employee deferrals in a 401(k) plan and the contributions to your IRA in the same tax year. If you are age 51, married, and your modified AGI is $180,000, you would be able to max your 401(k) employee deferrals at $32,500, you are over the income limit for deducting a contribution to a Traditional IRA, but you would have the option to contribute $8,600 to a Roth IRA.

Advanced Tax Strategy: In the example above, you are above the income threshold to deduct a Traditional IRA but your spouse may not be. If your spouse is not covered by a 401(k) plan, you can make a spousal contribution to a Traditional IRA because the $180,000 is below the income threshold for the spouse that is NOT COVERED by the employer-sponsored retirement plan.

Last updated June, 2026

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

Can you contribute to both a 401(k) and an IRA in the same year?

Yes, as long as you meet the income requirements for IRA eligibility. For example, in 2025 you could contribute the full employee deferral limit to your 401(k) ($23,000 plus $7,500 catch-up if age 50+) and still contribute up to $7,000 or $8,000 to an IRA.

What is a spousal IRA contribution?

If one spouse does not work or isn’t covered by an employer retirement plan, the working spouse can make an IRA contribution on their behalf. This strategy allows a couple to potentially double their retirement savings and may preserve tax deductibility for the non-covered spouse.