How to Minimize Taxes on Social Security

Many retirees are surprised to find that up to 85% of their Social Security benefits could be taxable. But with the right planning, it's possible to reduce or even eliminate those taxes.

The IRS determines how much of your Social Security is taxable using your provisional income, which includes:

Your adjusted gross income (AGI)

Plus any tax-exempt interest (such as from municipal bonds)

Plus 50% of your annual Social Security benefit

Example:

If your AGI is $20,000, you receive $5,000 in municipal bond interest, and your annual Social Security benefit is $30,000, your provisional income would be $40,000 — putting you in the 50% taxable range if you file your taxes married filing joint.

Based on this calculation, here are the income thresholds that determine how much of your benefit is taxable:

Single filers

$25,000 to $34,000 in provisional income: up to 50% of benefits may be taxable

Over $34,000: up to 85% may be taxable

Married filing jointly

$32,000 to $44,000 in provisional income: up to 50% of benefits may be taxable

Over $44,000: up to 85% may be taxable

Note: This doesn’t mean your benefits are taxed at 85%. Rather, it means up to 85% of your benefit amount is included in your taxable income and taxed at your ordinary income tax rate.

Strategies to Reduce or Eliminate Social Security Taxes

1. Delay Taking Social Security

Delaying benefits until age 70 not only increases your monthly payout, but also creates an income “gap window” where you can take advantage of other planning opportunities — such as Roth conversions — before your benefit starts impacting your tax return.

2. Draw Down Pre-Tax Assets Before Claiming

In the early years of retirement, before beginning Social Security, consider withdrawing from traditional IRAs or 401(k)s. These distributions are taxable now, but doing so may reduce your future required minimum distributions (RMDs), which in turn lowers taxable income once you begin collecting Social Security.

3. Consider Roth Conversions

Similar to item 2, Roth conversions allow you to shift money from a traditional IRA to a Roth IRA, paying tax now in order to avoid higher taxes later. By shifting money from a Traditioanl IRA to a Roth IRA prior to starting your social security benefit, it may keep you in lower tax brackets in future years especially when RMDs (requirement minimum distribution) begin at age 73 or 75. Also, once in a Roth IRA, future withdrawals are tax-free and do not count toward provisional income — helping keep more of your Social Security sheltered from taxation.

Note: Keep in mind that conversions count as income in the year they’re done — and can impact provisional income temporarily.

4. Use Qualified Charitable Distributions (QCDs)

QCDs allow individuals age 70½ or older to donate up to $100,000 per year directly from an IRA to a qualified charity. These donations count toward your RMD but are excluded from taxable income.

Clarification: The $100,000 QCD limit applies per individual IRA owner — so a married couple could potentially exclude up to $200,000 in charitable distributions if each spouse qualifies.

This is another way to reduce the size of a pre-tax retirement account balance which counts toward the RMD calculation. Also since the QCD counts toward the RMD amount it can reduce your taxable income, potentially making less of your Social Security benefit subject to taxation at the federal level.

Example: Sue is 78 and is required to take RMD from her traditional IRA of $10,000. Sue decides to process a QCD from her IRA sending $10,000 to her church. She has met the RMD requirement but the $10,000 does not represent taxable income to Sue. Sue’s provision income as a single filer is $30,000 making her Social Security benefit 50% taxable. If she did not process the QCD, that would have raised her provisional income to $40,000 making 85% of her social security benefit subject to taxation.

5. Be Cautious With Tax-Free Interest

Although interest from municipal bonds is federally tax-exempt and potentially state income tax, it is included in the provisional income calculation. If your portfolio includes significant tax-free bond income, it could unintentionally push you into the 50% or 85% taxable Social Security range.

Final Thoughts

Social Security is a cornerstone of retirement income, but managing how it’s taxed is just as important as deciding when to claim. The key to minimizing Social Security taxes is planning around when you claim benefits and where your income is coming from. Strategies like Roth conversions, QCDs, and pre-Social Security IRA withdrawals can all work together to help you keep more of your benefits.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

How does the IRS determine how much of my Social Security is taxable?

The IRS uses your “provisional income” to determine taxation, which includes your adjusted gross income (AGI), tax-exempt interest, and 50% of your annual Social Security benefits. Depending on your filing status and total provisional income, up to 50% or 85% of your Social Security benefits may be taxable.

What are the income thresholds for Social Security taxation?

For single filers, provisional income between $25,000 and $34,000 makes up to 50% of benefits taxable, and income above $34,000 makes up to 85% taxable. For married couples filing jointly, the 50% range applies between $32,000 and $44,000, with anything above $44,000 potentially making up to 85% taxable.

Does “85% taxable” mean I pay 85% tax on my benefits?

No. It means that up to 85% of your Social Security benefit is included in your taxable income and taxed at your ordinary income tax rate. You’re not taxed at 85%; rather, that portion is subject to your regular tax bracket.

How can I reduce or avoid taxes on my Social Security benefits?

You can lower taxable income by delaying Social Security, making Roth conversions before claiming benefits, or drawing down pre-tax accounts early in retirement. Using qualified charitable distributions (QCDs) from IRAs after age 70½ can also reduce taxable income and lower how much of your benefit is taxed.

How do Qualified Charitable Distributions (QCDs) affect Social Security taxation?

QCDs let you donate up to $100,000 per year directly from an IRA to a charity, satisfying required minimum distributions (RMDs) without increasing taxable income. By lowering your income, QCDs can reduce the portion of your Social Security benefits subject to tax.

Does tax-free interest from municipal bonds affect Social Security taxation?

Yes. Although municipal bond interest is exempt from federal income tax, it is included in the provisional income formula. Large amounts of tax-free interest can unintentionally increase the taxable portion of your Social Security benefits.

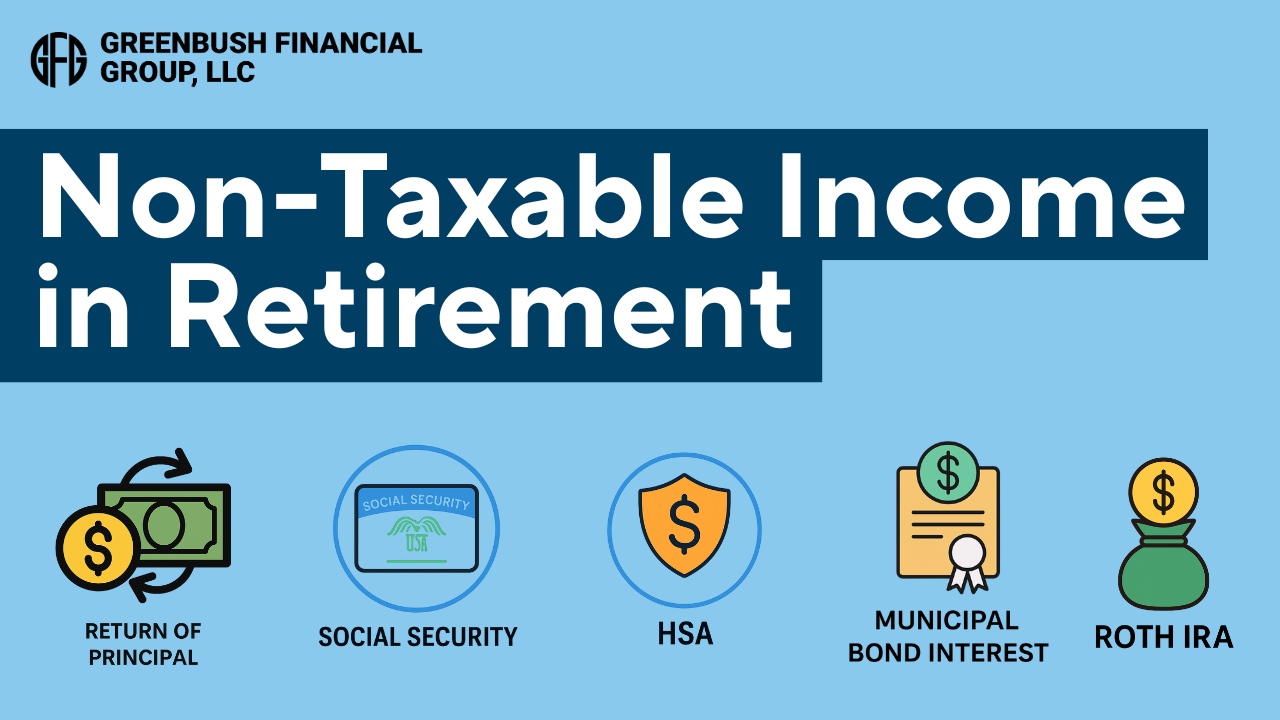

Non-Taxable Income in Retirement: 5 Sources You Should Know About

When it comes to retirement income, not all dollars are created equal. Some income sources are fully taxable, others partially — but a select few can be completely tax-free. And understanding the difference could mean thousands of dollars in savings each year.

When it comes to retirement income, not all dollars are treated equally. Some are fully taxable, others partially taxable, and a select few are entirely tax-free. Understanding the difference is critical to building a retirement income plan that protects your nest egg from unnecessary taxation, especially in a high-inflation, high-cost-of-living environment.

In this article, we break down five sources of non-taxable income in retirement, how they work, and how to strategically use them to lower your tax bill and preserve long-term wealth.

1. Roth IRA Withdrawals

A Roth IRA offers one of the most powerful tax benefits available to retirees — tax-free growth and qualified tax-free withdrawals.

To qualify, withdrawals must occur after age 59½ and at least five years after your first contribution or Roth conversion. If both conditions are met, all distributions (contributions and growth) are 100% tax-free.

Why it matters:

Withdrawals from pre-tax retirement accounts like Traditional IRAs and 401(k)s are taxed as ordinary income, which can push you into a higher tax bracket, increase Medicare premiums, and reduce the portion of your Social Security benefits that are tax-free. With Roth IRAs, none of those problems exist.

Planning strategy:

Many retirees choose to complete Roth conversions during low-income years (such as early retirement) to move pre-tax funds into a Roth IRA while controlling their tax rate. This allows them to create a future pool of tax-free income while reducing Required Minimum Distributions (RMDs) down the line.

2. Health Savings Account (HSA) Distributions for Medical Expenses

HSAs are the only account type that offers triple tax advantages:

Contributions are tax-deductible

Growth is tax-deferred

Withdrawals are tax-free if used for qualified medical expenses

Qualified expenses include Medicare premiums, prescriptions, dental and vision care, long-term care insurance premiums (subject to limits), and more.

Why it matters:

Healthcare is often one of the largest expenses in retirement, and using HSA funds tax-free for these costs allows retirees to preserve their other taxable accounts.

Planning strategy:

For clients who are still working and enrolled in a high-deductible health plan, the strategy may be to contribute the maximum amount to an HSA and pay current medical expenses out-of-pocket. This allows the HSA to grow and be used as a supplemental retirement account for tax-free medical reimbursements later in life.

3. Social Security (Partially Non-Taxable)

Up to 85% of Social Security benefits can be taxable at the federal level, depending on your provisional income (which includes half of your Social Security benefits, taxable income, and tax-exempt interest).

However, if a retiree has very little income other than their social security, it’s possible that they may not pay any tax on their social security benefits.

Why it matters:

Retirees who rely heavily on Roth IRA withdrawals or return of principal from brokerage accounts may be able to keep their provisional income low enough to shield some or all of their Social Security benefits from taxation.

Planning strategy:

By building a tax-efficient distribution plan in retirement, retirees can often reduce the amount of tax paid on their Social Security benefits and improve net income in retirement.

4. Municipal Bond Interest

Interest from municipal bonds is generally exempt from federal income tax. If you reside in the state where the bond was issued, that interest may also be exempt from state and local taxes.

Why it matters:

For retirees in high tax brackets, municipal bonds can provide steady, tax-advantaged income without adding to provisional income or triggering taxes on Social Security.

Planning strategy:

Retirees in high-income tax brackets may hold municipal bonds in taxable brokerage accounts, while keeping higher-yield taxable bonds inside IRAs or 401(k)s where the interest won’t be taxed annually.

5. Return of Principal from Non-Retirement Accounts

Withdrawals from taxable brokerage accounts can be structured to return your cost basis first, which is not subject to tax. Only the gains portion of a sale is subject to capital gains tax — and long-term capital gains may be taxed at 0% if your taxable income is below certain thresholds.

Why it matters:

This allows retirees to tap into their investments in a low-tax or no-tax manner — especially when drawing from principal rather than interest, dividends, or gains.

Planning strategy:

Coordinate asset sales to manage taxable gains, and consider drawing from principal early in retirement to reduce future RMDs or pay the tax liability generated by Roth conversions in lower-income years.

Final Thoughts: Build a Tax-Efficient Retirement Income Plan

Most retirees understand the importance of investment performance, but few give the same attention to tax efficiency, even though taxes can quietly erode thousands of dollars in retirement income each year.

By blending these non-taxable income sources into your withdrawal strategy, you can:

Reduce your tax liability

Lower Medicare surcharges

Improve portfolio longevity

Increase the amount of inheritance passed to the next generation

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What types of retirement income are tax-free?

Common sources of tax-free retirement income include qualified Roth IRA withdrawals, Health Savings Account (HSA) distributions for medical expenses, a portion of Social Security benefits, municipal bond interest, and the return of principal from non-retirement investments. These sources can help retirees reduce overall taxable income and extend portfolio longevity.

Why are Roth IRA withdrawals tax-free in retirement?

Roth IRA withdrawals are tax-free if you’re over age 59½ and the account has been open for at least five years. Because Roth withdrawals don’t count toward taxable income, they won’t increase your tax bracket, affect Medicare premiums, or reduce the tax-free portion of your Social Security benefits.

How can a Health Savings Account (HSA) provide tax-free income in retirement?

HSAs offer triple tax advantages: contributions are tax-deductible, growth is tax-deferred, and withdrawals are tax-free for qualified medical expenses. Retirees can use HSA funds to pay for Medicare premiums, prescriptions, and other healthcare costs without generating taxable income.

Are Social Security benefits always taxable?

No. Depending on your provisional income, up to 85% of Social Security benefits may be taxable, but some retirees owe no tax on their benefits. Keeping taxable income low through Roth withdrawals or return of principal from brokerage accounts can help reduce or eliminate Social Security taxation.

How are municipal bond earnings taxed?

Interest earned from municipal bonds is typically exempt from federal income tax and, if the bonds are issued by your home state, may also be exempt from state and local taxes. This makes municipal bonds a valuable source of tax-advantaged income for retirees in higher tax brackets.

What does “return of principal” mean for taxable accounts?

When you sell investments in a taxable brokerage account, the portion representing your original cost basis is considered a return of principal and isn’t taxed. Only the gains portion is subject to capital gains tax, which may be as low as 0% for retirees in lower income brackets.

How can retirees use non-taxable income to improve their financial plan?

Strategically blending tax-free and taxable income sources can lower your overall tax burden, reduce Medicare surcharges, and improve long-term portfolio sustainability. This approach helps preserve wealth and increase the amount that can ultimately be passed to heirs.

Why Do Wealthy Families Set Up Foundations and How Do They Work?

When a business owner sells their business and is looking for a large tax deduction and has charitable intent, a common solution is setting up a private foundation to capture a large tax deduction. In this video, we will cover how foundations work, what is the minimum funding amount, the tax benefits, how the foundation is funded, and more…….

When a business owner sells their business or a corporate executive receives a windfall in W2 compensation, some of these individuals will set up and fund a private foundation to capture a significant tax deduction, and potentially pre-fund their charitable giving for the rest of their lives and beyond. In this video, David Wojeski of the Wojeski Company CPA firm and Michael Ruger of Greenbush Financial Group will be covering the following topics regarding setting up a private foundation:

What is a private foundation

Why do wealthy individuals set up private foundations

What are the tax benefits associated with contributing to a private foundation

Minimum funding amount to start a private foundation

Private foundation vs. Donor Advised Fund vs. Direct Charitable Contributions

Putting family members on the payroll of the foundation

What is the process of setting up a foundation, tax filings, and daily operations

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What is a private foundation?

A private foundation is a nonprofit organization typically funded by a single individual, family, or business. It’s designed to support charitable activities, either by making grants to other nonprofits or by conducting its own charitable programs. The foundation is controlled by its founders or appointed board members rather than by the public.

Why do wealthy individuals set up private foundations?

High-net-worth individuals often establish private foundations to create a lasting legacy of charitable giving, maintain control over how funds are distributed, and involve family members in philanthropy. It also allows donors to give strategically over time rather than making one-time gifts to multiple organizations.

What are the tax benefits of contributing to a private foundation?

Contributions to a private foundation are tax-deductible. Assets contributed to the foundation grow tax-free, and donors can make grants to charities in future years while capturing the tax deduction in the year of the initial contribution.

What is the minimum funding amount to start a private foundation?

While there is no legal minimum, some experts recommend starting with at least $1 million to $2 million in assets. This level of funding helps offset administrative, tax filing, and compliance costs associated with running the foundation.

How does a private foundation compare to a Donor Advised Fund or direct charitable giving?

A Donor Advised Fund (DAF) is easier and less expensive to set up and maintain than a private foundation. However, a private foundation offers more control over investment management, grant-making, and governance. Direct charitable contributions are simpler still but provide no long-term control or legacy-building opportunities.

Can family members receive compensation from a private foundation?

Yes. Family members can serve on the foundation’s board or be paid for legitimate services such as administration, accounting, or grant oversight. However, compensation must be reasonable and documented to comply with IRS rules for private foundations.

What is involved in setting up and maintaining a private foundation?

Setting up a foundation involves establishing a nonprofit corporation or trust, applying for IRS tax-exempt status under Section 501(c)(3), and creating bylaws or a governing document. Ongoing operations include annual IRS Form 990-PF filings, distributing at least 5% of assets annually to charitable causes, maintaining proper records, and adhering to self-dealing and investment regulations.

529 to Roth IRA Transfers: A New Backdoor Roth Contribution Strategy Is Born

With the passing of the Secure Act 2.0, starting in 2024, owners of 529 accounts will now have the ability to transfer up to $35,000 from their 529 college savings account directly to a Roth IRA for the beneficiary of the account. While on the surface, this would just seem like a fantastic new option for parents that have money leftover in 529 accounts for their children, it is potentially much more than that. In creating this new rule, the IRS may have inadvertently opened up a new way for high-income earners to move up to $35,000 into a Roth IRA, creating a new “backdoor Roth IRA contribution” strategy for high-income earners and their family members.

With the passing of the Secure Act 2.0, starting in 2024, owners of 529 accounts will now have the ability to transfer up to $35,000 from their 529 college savings account directly to a Roth IRA for the beneficiary of the account. While on the surface, this would just seem like a fantastic new option for parents that have money leftover in 529 accounts for their children, it is potentially much more than that. In creating this new rule, the IRS may have inadvertently opened up a new way for high-income earners to move up to $35,000 into a Roth IRA, creating a new “backdoor Roth IRA contribution” strategy for high-income earners and their family members.

Money Remaining In the 529 Account for Your Children

I will start by explaining this new 529 to Roth IRA transfer provision using the scenario that it was probably intended for; a parent that owns a 529 account for their children, the kids are done with college, and there is still a balance remaining in the 529 account.

The ability to shift money from a 529 account directly to a Roth IRA for your child is a fantastic new distribution option for balances that may be leftover in these accounts after your child or grandchild has completed college. Prior to the passage of the Secure Act 2.0, there were only two options for balances remaining in 529 accounts:

Change the beneficiary on the account to someone else

Process a non-qualified distribution from the account

Both options created potential challenges for the owners of 529 accounts. For the “change the beneficiary option”, what if you only have one child, or what if the remaining balance is in the youngest child’s account? There may not be anyone else to change the beneficiary to.

The second option, processing a “non-qualified distribution” from the 529 account, if there were investment earnings in the account, those investment earnings are subject to taxes and a 10% penalty because they were not used to pay a qualified education expense.

The “Roth Transfer Option” not only gives account owners a third attractive option, but it’s so attractive that planners may begin advising clients to purposefully overfund these 529 accounts with the intention of processing these Roth transfers after the child has completed college.

Requirements for 529 to Roth IRA Transfers

Before I get into explaining the advanced tax and wealth accumulation strategies associated with this new 529 distribution option, like any new tax law, there is a list of rules that you have to follow to be eligible to process these 529 to Roth IRA transfers.

The 15 Year Rule

The first requirement is the 529 account must have been in existence for at least 15 years to be eligible to execute a Roth transfer from the account. The clock starts when you deposit the first dollar into that 529 account. The planning tip here is to fund the 529 as soon as you can after the child is born, if you do, the 529 account will be eligible for Roth IRA transfers by their 15th or 16th birthday.

There is an unanswered question surrounding rollovers between state plans and this 15-year rule. Right now, you are allowed to rollover let’s say a Virginia 529 account into a New York 529 account. The question becomes, since the New York 529 account is a new account, would that end up re-setting the 15-year inception clock?

Contributions Within The Last 5 Years Are Not Eligible

When you go to process a Roth transfer from a 529 account, contributions made to the 529 account within the previous 5 years are not eligible for Roth transfers.

The Beneficiary of the 529 Account and the Owners of the Roth IRA Must Be The Same Person

A third requirement is the beneficiary listed on the 529 account and the owner of the Roth IRA account must be the same person. If your daughter is the beneficiary of the 529 account, she would also need to be the owner of the Roth IRA that is receiving the transfer directly from the 529 account. There is a big question surrounding this requirement that we still need clarification on from the IRS. The question is this: Is the account owner allowed to change the beneficiary on the 529 account without having to re-satisfy a new 15-year account inception requirement?

If they allow beneficiary changes without a new 15-year inception period, with 529 accounts, the account owner can change the beneficiary on these accounts to whomever they want……..including themselves. This would allow a parent to change the beneficiary to themselves on the 529 account and then transfer the balance to their own Roth IRA, which may not be the intent of the new law.

No Roth IRA Income Limitations

As many people are aware, if you make too much, you are not allowed to contribute to a Roth IRA. For 2026, the ability to make Roth IRA contributions begins to phase out at the following income levels:

Single Filer: $153,000

Married Filer: $242,000

These transfers directly from 529 accounts to the beneficiary’s Roth IRA do not carry the income limitation, so regardless of the income level of the 529 account owner or the beneficiary, there a no maximum income limit that would preclude these 529 to Roth IRA transfers from taking place.

The IRA Owner Must Have Earned Income

With exception of the Roth IRA income phaseout rules, the rest of the Roth RIA rules still apply when determining whether or not a 529 to Roth IRA transfer is allowed in a given tax year. First, the beneficiary of the 529 (also the owner of the Roth IRA) needs to have earned income in the year that the transfer takes place to be eligible to process a transfer from the 529 to their Roth IRA.

Annual 529 to Roth IRA Transfer Limits

The amount that can be transferred from the 529 to the Roth IRA is also limited each year by the regular Roth IRA annual contribution limits. For 2026, an individual under the age of 50, is allowed to make a Roth IRA contribution of up to $7,500. That is the most that can be moved from the 529 account to Roth IRA in a single tax year. But in addition to this hard dollar limit, you have to also take into account any other Roth IRA contributions that were made to the IRA owner’s account and the IRA owners earned income for that tax year.

The annual contribution limit to a Roth IRA for 2026 is actually the LESSER of:

$7,500; or

100% of the earned income of the account owner

Assuming the IRA contribution limits stay the same in 2027, if a child only has $3,000 in income, the maximum amount that could be transferred from the 529 to the Roth IRA in 2027 is $3,000.

If the child made a contribution of their own to the Roth IRA, that would also count against the amount that is available for the 529 to Roth IRA transfer. For example, the child makes $10,000 in earned income, making them eligible for the full $7,500 Roth IRA contribution, but if the child contributes $2,000 to their Roth IRA throughout the year, the maximum 529 to Roth IRA transfer would be $5,500 ($7,500 - $2,000 = $5,500)

$35,000 Limiting Maximum Per Beneficiary

The maximum lifetime amount that can be transferred from a 529 to a Roth IRA is $35,000 for each beneficiary. Given the annual contribution limits that we just covered, you would not be allowed to just transfer $35,000 from the 529 to the Roth IRA all in one shot. The $35,000 lifetime limit would be reached after making multiple years of transfers from the 529 to the Roth IRA over a number of tax years.

Advanced 529 Planning Strategies Using Roth Transfers

Now I’m going to cover some of the advanced tax and wealth accumulation strategies that may be able to be executed under this 529 Roth Transfer provision.

Super Funding A Roth IRA For Your Child

While 529 accounts have traditionally been used to save exclusively for future college expenses for your children or grandchild, they just become much more than that. Parents and grandparents can now fund these accounts when a child is young with the pure intention of NOT using the funds for college but rather creating a supercharged Roth IRA as soon as that child begins earning income in their teenage years and into their 20s.

This is best illustrated in an example. You have a granddaughter that is born in 2026, you open a 529 account for her and fund it with $15,000. By the time your granddaughter has reached age 18, let’s assume through wise investment decisions, the account has tripled to $45,000. Between ages 18 and 21, she works a summer job making $8,000 in earned income each year and then gets a job after graduating college making $80,000 per year. Assuming she made no contributions to a Roth IRA over the years, you would be able to make transfers between her 529 account and her Roth IRA up to the annual contribution limit until the total transfers reached the $35,000 lifetime maximum.

If that $35,000 lifetime maximum is reached when she turns age 24, assuming she also makes wise investment decisions and earns 8% per year on her Roth IRA until she reaches age 60, at age 60 she would have $620,000 in that Roth IRA account that could be withdrawal ALL TAX-FREE.

Now multiply that $620,000 across EACH of your children or grandchildren, and it becomes a truly fantastic way to build tax-free wealth for the next generation.

529 Backdoor Roth Contribution Strategy

A fun fact, there are no age limits on either the owner or beneficiary of a 529 account. At the age of 40, I could open a 529 account, be the owner and the beneficiary of the account, fund the account with $15,000, wait the 15 years, and then when I turn age 55, begin processing transfers directly from the 529 to my Roth IRA up to the maximum annual IRA limit each year until I reach my $35,000 lifetime limit.

I really don’t care that the money has to sit in the 529 for 15 years because 529 accumulate tax deferred anyways, and by the time I hit age 59.5, making me eligible for tax-free withdrawal of the earnings, I will have already moved most of the balance over to my Roth IRA. Oh and remember, even if you make too much to contribute directly to a Roth IRA, the income limits do not apply to these 529 to Roth IRA direct transfers.

The IRS may have inadvertently created a new “Backdoor Roth IRA Contribution” strategy for high-income earners.

Now there may be some limitations that can come into play with the age of the individual executing this strategy, it’s really less about their age, and more about whether or not they will have earned income 15 years from now when the 529 to Roth IRA transfer window opens. If you are 65, fund a 529, and then at age 80 want to begin these 529 to Roth IRA transfers, if you have no earned income, you can process these 529 to Roth IRA transfers because you are limited by the regular IRA annual contribution limits that require you to have earned income to process the transfers.

Advantage Over Traditional Backdoor Roth Conversions

For individuals that have a solid understanding of how the traditional “Backdoor Roth IRA Contribution” strategy works, the new 529 to Roth IRA transfer strategy potentially contains additional advantages over and above the traditional backdoor Roth strategy. These movements from the 529 to Roth IRA are not considered “conversions”, they are considered direct transfers. Why is that important? Under the traditional Backdoor Roth Contribution strategy the taxpayer is making a non-deductible contribution to a traditional IRA and then processes a conversion to a Roth IRA.

One of the IRS rules during this conversion process is the “aggregation rule”. When a Roth conversion is processed, the taxpayer has to aggregate all of their pre-tax IRA balance together in determining how much of the conversion is taxable, so if the taxpayer has other pre-tax IRAs, it came sometimes derail the backdoor Roth contribution strategy. If they instead use the 529 to Roth IRA direct transfer processes, since as of right now it is not technically a “conversion”, the aggregate rule is avoided.

The second big advantage is with the 529 to Roth IRA transfer strategy, the Roth IRA is potentially being funded with “untaxed earnings” as opposed to after-tax dollar. Again, in the traditional Backdoor Roth Strategy, the taxpayer is using after-tax money to make a nondeductible contribution to a Traditional IRA and then converting those dollars to a Roth IRA. If instead the taxpayer funds a 529 with $15,000 in after-tax dollars, but during the 15-year holding, The account grows the $35,000, they are then able to begin direct transfers from the 529 to the Roth IRA when $20,000 of that account balance represents earnings that were never taxed. Pretty cool!!

State Tax Deduction Clawbacks?

There are some states, like New York, that offer tax deductions for contributions to 529 accounts up to annual limits. When the federal government changes the rules for 529 accounts, the states do not always follow suit. For example, when the federal government changed the tax laws allowing account owners to distribute up to $10,000 per year for K – 12 qualified expenses from 529 accounts, some states, like New York, did not follow suit, and did not recognize the new “qualified expenses”. Thus, if someone in New York distributed $10,000 from a 529 for K – 12 expenses, while they would not have to pay federal tax on the distribution, New York viewed it as a “non-qualified distribution”, not only making the earnings subject to state taxes but also requiring a clawback of any state tax deduction that was taken on the contribution amounts.

The question becomes will the states recognize these 529 to Roth IRA transfers as “qualified distributions,” or will they be subject to taxes and deduction clawbacks at the state level? Time will tell.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What is the new 529 to Roth IRA transfer rule under the Secure Act 2.0?

Starting in 2024, owners of 529 college savings accounts can transfer up to $35,000 over their lifetime from a 529 directly to a Roth IRA for the account’s beneficiary. This gives families a new tax-free way to repurpose unused education savings.

What are the main requirements for a 529 to Roth IRA transfer?

The 529 account must be at least 15 years old, and contributions made within the last 5 years cannot be transferred. The 529 beneficiary and the Roth IRA owner must be the same person, and the beneficiary must have earned income in the year of transfer.

How much can be transferred each year?

Transfers are subject to the annual Roth IRA contribution limit—currently $6,500 per year (or less if earned income is lower). It may take several years to reach the $35,000 lifetime transfer cap.

Do income limits apply to 529 to Roth IRA transfers?

No. These transfers are not subject to Roth IRA income phaseouts, meaning high-income earners can use this rule even if they’re normally ineligible to contribute directly to a Roth IRA.

Can parents use this rule as a backdoor Roth IRA strategy?

Potentially. If future IRS guidance allows changing a 529 beneficiary to oneself without restarting the 15-year clock, high-income earners could fund their own Roth IRAs using this method—creating a new type of “backdoor Roth” strategy.

Are there potential state tax implications?

Yes. Some states may not treat 529-to-Roth transfers as qualified distributions, which could trigger state taxes or clawbacks of prior state tax deductions.

When will the IRS provide more guidance on this rule?

The IRS is expected to issue clarifications before the rule takes effect in 2024. Guidance will determine whether advanced strategies—like beneficiary changes or state conformity—are allowed.

Self-Employment Income In Retirement? Use a Solo(k) Plan To Build Wealth

It’s becoming more common for retirees to take on small self-employment gigs in retirement to generate some additional income and to stay mentally active and engaged. But, it should not be overlooked that this is a tremendous wealth-building opportunity if you know the right strategies. There are many, but in this article, we will focus on the “Solo(k) strategy

It’s becoming more common for retirees to take on small self-employment gigs in retirement to generate some additional income and to stay mentally active and engaged. But, it should not be overlooked that this is a tremendous wealth-building opportunity if you know the right strategies. There are many, but in this article, we will focus on the “Solo(k) strategy.”

What Is A Solo(K)

A Solo(k) plan is an employer-sponsored retirement plan that is only allowed to be sponsored by owner-only entities. It works just like a 401(k) plan through a company but without the high costs or administrative hassles. The owner of the business is allowed to make both employee deferrals and employer contributions to the plan.

Solo(k) Deferral Limits

For 2025, a business owner is allowed to contribute employee deferrals up to a maximum of the LESSER of:

100% of compensation; or

$31,000 (Assuming the business owner is age 50+) or

$34,750 (For individuals age 60-63)

Pre-tax vs. Roth Deferrals

Like a regular 401(K) plan, the business owner can contribute those employee deferrals as all pre-tax, all Roth, or some combination of the two. Herein lies the ample wealth-building opportunity. Roth assets can be an effective wealth accumulation tool. Like Roth IRA contributions, Roth Solo(k) Employee Deferrals accumulate tax deferred, and you pay NO TAX on the earnings when you withdraw them as long as the account owner is over 59½ and the Roth account has been in place for more than five years.

Also, unlike Roth IRA contributions, there are no income limitations for making Roth Solo(k) Employee Deferrals and the contribution limits are higher. If a business owner has at least $31,000 in compensation (net profit) from the business, they could contribute the entire $31,000 all Roth to the Solo(K) plan. A Roth IRA would have limited them to the max contribution of $8,000 and they would have been excluded from making that contribution if their income was above the 2025 threshold.

A quick note, you don’t necessarily need $31,000 in net income for this strategy to work; even if you have $18,000 in net income, you can make an $18,000 Roth contribution to your Solo(K) plan for that year. The gem to this strategy is that you are beginning to build this war chest of Roth dollars, which has the following tax advantages down the road……

Tax-Free Accumulation and Withdrawal: If you can contribute $100,000 to your Roth Solo(k) employee deferral source by the time you are 70, if you achieve a 6% rate of return at 80, you have $189,000 in that account, and the $89,000 in earnings are all tax-free upon withdrawal.

No RMDs: You can roll over your Roth Solo(K) deferrals into a Roth IRA, and the beautiful thing about Roth IRAs are no required minimum distributions (RMD) at age 73 or 75. Pre-tax retirement accounts like Traditional IRAs and 401(k) accounts require you to begin taking RMDs at age 73 or 75 based on your date of birth, which are forced taxable events; by having more money in a Roth IRA, those assets continue to build.

Tax-Free To Beneficiaries: When you pass assets on to your beneficiaries, the most beneficial assets to inherit are often a Roth IRA or Roth Solo(k) account. When they changed the rules for non-spouse beneficiaries, they must deplete IRAs and retirement accounts within ten years. With pre-tax retirement accounts, this becomes problematic because they have to realize taxable income on those potentially more significant distributions. With Roth assets, not only is there no tax on the distributions, but the beneficiary can allow that Roth account to grow for another ten years after you pass and withdraw all the earnings tax and penalty-free.

Why Not Make Pre-Tax Deferrals?

It's common for these self-employed retirees to have never made a Roth contribution to retirement accounts, mainly because, during their working years, they were in high tax brackets, which warranted pre-tax contributions to lower their liability. But now that they are retired and potentially showing less income, they may already be in a lower tax bracket, so making pre-tax contributions, only to pay tax on both the contributions and the earnings later, may be less advantageous. For the reasons I mentioned above, it may be worth foregoing the tax deduction associated with pre-tax contributions and selecting the long-term benefits associated with the Roth contributions within the Solo(k) Plan.

Now there are situations where one spouse retires and has a small amount of self-employment income while the other spouse is still employed. In those situations, if they file a joint tax return, their overall income limit may still be high, which could warrant making pre-tax contributions to the Solo(k) plan instead of Roth contributions. The beauty of these Solo(k) plans is that it’s entirely up to the business owner what source they want to contribute to from year to year. For example, this year, they could contribute 100% pre-tax, and then the following year, they could contribute 100% Roth.

Solo(k) versus SEP IRA

Because this question comes up frequently, let's do a quick walkthrough of the difference between a Solo(k) and a SEP IRA. A SEP IRA is also a popular type of retirement plan for self-employed individuals; however, SEP IRAs do not allow Roth contributions, and SEP IRAs limit contributions to 20% of the business owner’s net earned income. Solo(K) plans have a Roth contribution source, and the contributions are broken into two components, an employee deferral and an employer profit sharing.

As we looked at earlier, the employee deferral portion can be 100% of compensation up to the Solo(K) deferral limit of the year, but in addition to that amount, the business owner can also contribute 20% of their net earned income in the form of a profit sharing contribution.

When comparing the two, in most cases, the Solo(K) plan allows business owners to make larger contributions in a given year and opens up the Roth source.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What is a Solo(k) plan?

A Solo(k) is a 401(k)-style retirement plan designed for self-employed individuals or business owners with no employees other than a spouse. It allows both employee and employer contributions, offering high contribution limits and flexible tax options.

How much can you contribute to a Solo(k) in 2025?

For 2025, you can contribute the lesser of 100% of your compensation or up to:

$31,000 if age 50 or older

$34,750 if age 60–63

These limits include employee deferrals and do not count potential employer profit-sharing contributions.

Can Solo(k) contributions be Roth or pre-tax?

Yes. You can choose to make contributions as pre-tax, Roth, or a combination of both. Roth contributions are made with after-tax dollars but grow tax-free, and qualified withdrawals are also tax-free.

Why might Roth Solo(k) contributions be advantageous for retirees?

Roth Solo(k) assets grow tax-free, have no required minimum distributions (RMDs) once rolled into a Roth IRA, and can be passed to beneficiaries without income tax. For retirees in lower tax brackets, contributing to Roth accounts may provide long-term tax benefits over pre-tax deferrals.

Can you make Roth contributions to a SEP IRA?

No. SEP IRAs only allow pre-tax contributions and do not offer a Roth option. This makes the Solo(k) plan a more flexible choice for self-employed individuals looking to build tax-free retirement income.

How does a Solo(k) compare to a SEP IRA?

A Solo(k) allows both employee deferrals (up to 100% of income) and employer profit-sharing contributions, plus the option for Roth contributions. A SEP IRA limits contributions to 20% of net earned income and only allows pre-tax contributions, typically resulting in lower total contribution potential.

Is a Solo(k) a good option for retirees with part-time income?

Yes. For retirees earning even modest self-employment income, a Solo(k) can be a powerful tool to continue saving for retirement—especially with Roth contributions that provide future tax-free income and estate planning advantages.

Kiddie Tax & Other Pitfalls When Gifting Assets To Your Kids

Before you gift assets to your children make sure you fully understand the Kiddie Tax rule and other pitfalls associated with making gift to your children……….

There are a number of reasons why parents gift assets to their kids which include:

Reduce tax liability

Protecting assets from the nursing home

Estate planning: Avoiding probate

But the pitfalls are many and most people do not find out about the pitfalls until it’s too late. These pitfalls include:

Kiddie tax rules

Children with self-directed investment accounts

Treatment of long-term capital gains

Gifting cost basis rules

College financial aid impact

Control of the assets

5 Year look-back rule

Divorce

Lawsuits

Distributions from Inherited IRA’s

Kiddie Tax

The strategy of shifting assets from a parent to a child on the surface seems like a clever tax strategy in an effort to shift investment income or capitals gains from the parent that may be in a high tax bracket to their child that is in a low tax backet. Unfortunately, the IRS is aware of this strategy, and they have been aware of it since 1986, which is the year the “Kiddie Tax” was signed into law.

Here is how the Kiddie tax works; if your child’s income is over a certain amount, then the income is taxed NOT at the child’s tax rate, but at the PARENT’S tax rate. Kiddie tax rules do NOT apply to earned income which includes wages, salary, tips, or income from self-employment. Kiddie tax ONLY applies to UNEARNED INCOME which includes:

Taxable interest

Dividends

Capital gains

Taxable Scholarships

Income produced by gifts from grandparents

Income produced by UTMA or UGMA accounts

IRA distributions

There are some exceptions to the rule but in general, your child would be subject to the Kiddie tax if they are:

Under the age of 19; or

Between the ages of 19 and 23, and a full-time student

The only exceptions that apply are if your child:

Has earned income totaling more than half the cost of their support; or

Your child files their tax return as married filing joint

Kiddie Tax Calculation

Here is how the Kiddie tax calculation works. For 2026, the first $1,350 of a child’s unearned income is tax-free, the next $1,350 is taxed at the child’s rate, and any unearned income above $2,700 is taxed at the parent’s marginal income tax rate.

Here is an example, the parents bought Apple stock a long time ago and the stock now has a $30,000 unrealized long term capital gain. Assuming the parents make $200,000 per year in income, if they sell the stock, they will have to pay the Federal 15% long term capital gains tax on the $30,000 gain. But they have a child that is age 16 with no income, so they gift the stock to them, have them sell it, with the hopes of the child capturing the 0% long term cap gains rate since they have no income. Kiddie tax is triggered!! The first $2,700 would be tax free but the rest would be taxed at the parent’s federal 15% long term cap gain rate; oh and if that family was expecting to receive college financial aid two years from now, they might have just made a grave mistake because now that teenager is showing income. A topic for later.

That was an example using long term capital gains rates but if we used a source of unearned income subject to ordinary income tax rates, the jump could go from an assumed 0% to the parents 37% tax rate if they are in the highest fed bracket.

Putting Your Kids on Payroll

While we are on the subject of Kiddie Tax, our clients that own small businesses will sometimes ask “Do I have to worry about the Kiddie tax if I put my kids on payroll through my company?” Fortunately the answer is “No”. Paying your child W2 wages through your company is considered “earned income” and earned income is not subject to the kiddie tax rules.

Children with Self-Directed Investment Accounts

It’s becoming more common for high school and college students to have their own brokerage accounts where they are trading stocks, ETFs, options, cryptocurrency, and mutual funds. But the kiddie rules can come into play when they are buying and selling investments in their accounts. If the parents claim the child as a dependent on their tax return and they buy and then sell an investment within a 12 month period, that would create a short term gain subject to ordinary income tax rates. If that gain is above $2,700, then the kiddie tax is triggered, and the gain would be taxed at the parent’s tax rate not the child’s tax rate. This can lead to tax surprises when the child receives the tax forms from the brokerage platform and then realizes there are big taxes due, and the child may or may not have the money to pay it.

For the child to file their own tax return to avoid this Kiddie tax situation, the child must be earning enough income to provide at least half of their financial support.

Kiddie Tax Form 8615

How do you report the Kiddie tax on your tax return? I spoke with a few CPA’s about this and they normally advise their clients that once the child has unearned income over $2,700, the child, even though they may be a dependent on your tax return, files their own tax return, and with their tax return they file Form 8615 which calculates the Kiddie Tax liability based on their parent’s tax rate.

Impact on College Financial Aid

Before gifting any assets to your child, income producing or not, if you are expecting to receive any form of need based financial aid for your child for college in the future, be very very careful. The FAFSA calculation weighs assets and income differently depending on whether it belongs to the parent or the child.

For assets, if the parent owns it, the balance counts 5.64% against the aid awarded. If the child owns it, the balance counts 20% against the aid awarded. You move a stock into your child’s name that is worth $30,000, if you would have qualified for financial aid, you just cost yourself $4,300 PER YEAR in financial aid.

Income is worse. If you gift your child an asset that produces income or capital gains, income of the parents counts 22% - 47% against college financial aid depending on the size of the household. If the income belongs to the child, it counts 50% against the FAFSA award. Another note, the FAFSA process looks back 2 years for purposes of determining the financial aid award, so even though they may only be a sophomore or junior in high school, you don’t find out about that mistake until 2 years later when they are applying for FAFSA as a freshman in college.

Long Term Capital Gains Treatment

The example that I used earlier with the Apple stock highlights another useful tax lesson. If you are selling a stock, mutual fund, or investment property that you have owned for more than a year, it’s taxed at the preferential long term capital gain rate of 15% as long as your taxable income does not exceed $545,500 for single filers or $613,700 for married filing joint in 2026, it’s a flat 15% tax rate whether it’s a $20,000 gain or a $200,000 gain because the rate does not increase like it does for “earned income”. I make this point because long term capital gain rates are already taxed at a relatively low rate, and if realized by your child, are subject to Kiddie tax so before you jump through all the hoops of making the gift, make sure the tax strategy is going to work.

Gift Cost Basis Rules

When you make a gift, it’s important to understand how the cost basis rules work. When you make a gift, there typically is not an immediate tax event, but the recipient inherits your cost basis in that asset. Gifting an asset does not provide the person making the gift with a tax deduction or erase the unrealized gains, unless of course you are gifting it to a charity or not-for-profit. Let’s keep running with that Apple stock example, you gift the Apple stock to your child with a $30,000 unrealized gain, there is no tax event when the gift is made, but if the child sells the stock the next day, they will have to pay tax on the $30,000 realized gain, and if the kiddie tax applies, it will be taxed at the parent’s tax rate.

Estate Tax Planning: Avoid Probate

Sometimes people will gift assets to their kids in an effort to remove those assets from their estate to avoid probate, a big tax issue surfaces with this strategy. Normally when someone passes away and their kids inherit a house or investments, they receive a “step-up in basis”. A step-up in basis means no matter what the gain was in the house or investment prior to a person passing away, the cost basis to the person that inherits the assets is now the fair market value of that asset as of decedent’s date of death.

Example: You bought your house 20 years ago for $200,000 and it’s now worth $400,000. If you were to pass away tomorrow and your kids inherit your house, they receive a step-up in basis to $400,000 so if they sell the house the next day, they have no tax liability. A huge tax benefit.

But if you gift the house to your kids while you are still alive in an effort to avoid the probate process, your kids now lose the step-up in cost basis because the house never passes through your estate. If you kids sell your house the next day, they will realize a $200,000 gain and have to pay tax on it which at the Federal level of 15%, could cost them $30,000 in taxes which could have been avoided.

There are other ways to avoid probate besides gifting that asset to your kids which allows the asset to avoid the probate process and receive a step up in basis. You could setup a trust to own the asset or change the registration on the account to a “transfer on death” account.

Distributions From An IRA Owned By The Child

If your child inherits an IRA, they may be required to take RMD’s (required minimum distributions) each year from the IRA. Distribution are not only subject to ordinary income tax but they are also subject to Kiddie tax since IRA distributions are considered unearned income. If you child inherits a pre-tax IRA or 401(k) be very careful when taking distribution from the account, especially taking into consideration the new distribution rules for non-spouse beneficiaries.

Control of the Asset

As financial planners, we have seen a lot of crazy things happen. While some teenagers are very responsible, others are not. When you gift an asset directly to child, they may not use that gift as intended. Even with UTMA and UGMA account, the parents only have control until the child reaches age of majority, and then account belongs to them. If there is any concern about how the gifted asset will be managed or distributed, you may want to consider a trust or another type of account that provides the you with more control of the asset.

Lawsuits

From a liability standpoint, if you gift assets to your child, and those assets have a meaningful amount of value, those assets could be exposed to a lawsuit if your child were to ever be sued.

Divorce

If you gift assets to your child and they are already married or get married in the future, depending on what state they live in or how those assets are titled, they could be considered marital property. If a divorce happens at some point in the future, their soon to be ex-spouse could now be entitled to a portion of those gifted assets.

5 Year Lookback Rule

Some parents will gift assets to their children to avoid the spend down process should a long term care event happen at some point in the future and they need to go into a nursing home. Different states have different Medicaid rules but in New York, the gift has to take place 5 years prior to the Medicaid application otherwise the assets are subject to spend down.

The other pitfall of gifting assets to your children is that while you may be able to successfully protect those assets from a Medicaid lookback period, the cost basis issue that we discussed earlier still exists. If you gift the house to your kids, they inherit your cost basis, so when they go to sell the house after you pass, they have to pay tax on the full gain amount, versus if you established a grantor irrevocable trust to own your house, it could satisfy the gift for the 5 year look back period in NY, but then your kids receive a step up in basis when you pass away since the house passes through your estate, and they can sell the house with no tax liability.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What are common reasons parents gift assets to their children?

Parents often gift assets to reduce future tax liabilities, protect assets from potential nursing home costs, or simplify estate transfers by avoiding probate. While these goals can be achieved, gifting assets can also create unintended tax and legal consequences if not properly structured.

What is the Kiddie Tax and when does it apply?

The Kiddie Tax applies to a child’s unearned income—such as dividends, interest, or capital gains—above $2,700 (in 2025). Any income over that amount is taxed at the parents’ marginal tax rate instead of the child’s lower rate. It generally applies to dependents under age 19, or under 24 if they are full-time students.

How does gifting affect college financial aid?

Assets and income in a child’s name significantly reduce eligibility for need-based aid. Parental assets count about 5.6% against aid eligibility, while a child’s assets count 20%. Additionally, a child’s income can count as high as 50% against financial aid calculations for two years following the income year.

What are the tax implications of gifting appreciated assets?

When you gift an asset like stock or real estate, your cost basis carries over to the recipient. If the recipient sells the asset, they owe tax on the gain from your original purchase price. This means gifting appreciated assets can shift, but not eliminate, future tax liability.

How does gifting differ from inheritance when it comes to taxes?

Inherited assets generally receive a “step-up in basis” to their fair market value on the date of the decedent’s death, eliminating unrealized capital gains. Gifting assets during your lifetime forfeits this step-up, potentially leaving your heirs with larger future tax bills if they sell the asset.

Can gifting affect Medicaid eligibility or nursing home planning?

Yes. Medicaid’s five-year lookback rule allows the state to review gifts made within five years before a long-term care application. Assets transferred during that period may still be counted toward Medicaid eligibility, delaying benefits and forcing asset spend-down.

What are the risks of gifting assets directly to children?

Once assets are gifted, they legally belong to the child. This means they could be lost in a lawsuit, subject to division in a divorce, or spent irresponsibly. Parents concerned about control or protection may prefer using trusts or transfer-on-death designations instead of outright gifts.

How To Use Your Retirement Accounts To Start A Business

One of the most challenging aspects of starting a new business is finding the capital that is needed to support your expenses as you begin to build up a revenue stream since it’s not always easy to ask friends and family for money to invest in a startup business. Luckily, for new entrepreneurs, there are some little-known ways on how you can use

One of the most challenging aspects of starting a new business is finding the capital that is needed to support your expenses as you begin to build up a revenue stream since it’s not always easy to ask friends and family for money to invest in a startup business. Luckily, for new entrepreneurs, there are some little-known ways on how you can use retirement accounts as a funding source for your new business. However, before you cash out your 401(k) account to start a business, you have to fully understand the pros and cons of each option.

ROBS Plans

ROBS stands for “Rollover for Business Startups”. ROBS is a special program that allows you to use the balance in your 401(k) or IRA account to fund your new business while avoiding having to pay taxes and the 10% early withdrawal penalty for business owners under age 59.5. Unlike a 401(k) loan that has limits, loan payments, and interest, ROBS plans allow you to use your full retirement account balance without having to enter into a repayment plan.

Why do business owners use ROBS plans?

The benefits are fairly obvious. First off, by using your own retirement assets to fund your new business, you don’t have to ask friends and family for money. Secondly, if you were to embark on the traditional lending route from a bank for your start-up, most would require you to pledge personal assets, such as your house, as collateral for the loan. Doing this puts an added pressure on the new entrepreneur because if the business fails you not only lose the business, but potentially your house as well. By using the ROBS plan, you are only risking your own assets, you have quick and easy access to those funds, and if the business fails, worst case scenario, you just have to work longer than you expected.

Is this too good to be true?

When I explain this funding strategy to new business owners, the question I usually get is, “Why haven’t I heard of these plans before?”, and here are a few reasons why. To begin, you are using retirement plan dollars and accessing the tax benefits, and in doing so there are a lot of complex rules surrounding these types of plans. It’s not uncommon for accountants, third-party administrators, and financial advisors to not know what a ROBS plan is, let alone understand the compliance rules surrounding these plans; thus, it’s rarely presented as a viable option. Over the course of this article we will cover the pros and cons of this funding mechanism.

How do ROBS plans work?

The concept is fairly simple, your retirement account essentially buys shares of stock in your new business which provides the business with the cash needed to grow. You do not have to be a publicly traded company for your retirement account to buy shares, however, you are required to establish your new company as a C-Corp in order for this plan to work.

This process entails incorporating your new business, as well as establishing a new 401(k) plan within that business, that contains the special ROBS features. Then, you can transfer assets from your various retirement accounts into the new 401(k) plan allowing the 401(k) plan to then buy shares in your new company. While this sounds easy, I cannot stress enough that you must work with a firm that fully understands these types of plans and the funding strategy. These plans are perfectly legal, but there are a lot of rules to follow. Since this funding strategy allows you to access retirement account dollars without having to pay tax to the IRS, the IRS will sometimes audit these plans hoping that you did not fully understand or comply with the rules surrounding the establishment and operations of these ROBS plans.

The steps to set up a ROBS plan

Here are the steps for setting up the plan:

1) Establish your new business as a C-Corp.

2) Establish a new 401(k) plan for your new business

3) Process direct rollovers from your 401(k) accounts and IRA accounts into your new 401(k) plan

4) Use the balance in your 401(k) account to purchase shares of the corporation

5) Now you have cash in your business checking account to pay expenses

You must be a C-Corp

The only type of corporate structure that works for a ROBS plan is a C-Corp because only a C-Corp can sell shares of the business to a retirement account legally. That means that LLCs, sole proprietorships, partnerships or even S-Corps will not work for this funding option.

Establishing the new 401(k) plan

ROBS plans have all the same features and benefits of a traditional 401(k) plan, profit-sharing plan, or defined benefit plan, except they also have special features that allow the plan to invest plan assets in the privately held C-Corp.

You need to work with a firm that knows these plans well because not all custodians will allow you to hold shares of a privately held corporation in a qualified retirement account. For many investment firms and custodians, this is considered either a “private placement” or an “alternative investment”. There is typically a special approval process that you must go through with the custodian before they allow your 401(k) account to purchase the shares of stock in your new company. Be ready, there are a lot of mainstream 401(k) providers that will not only not know what a ROBS plan is, but they often times limit the plan investment options to mutual funds; to avoid this, make sure you are aligning yourself with the right provider.

Transferring funds from your retirement accounts to your new 401(k) plan

Your new investment provider should assist you with coordinating the rollovers into your 401(k) account to avoid paying taxes and penalties. Also, if you have 401(K) Roth or after-tax money in your retirement accounts, special preparations need to be made prior to the rollover occurring for those sources.

Purchasing stock in the business

It’s not as easy as simply transferring money into the business checking account since you have to go through the process of issuing shares to the 401(k) account. In most cases, the percentage of ownership attributed to the 401(k) plan is based upon your total funding picture to start up the company. If your retirement accounts are the sole resource to fund the business, then technically your 401(k) plan owns 100% of the company. It’s not uncommon for new business owners to use multiple funding sources including personal savings, funding from friends and family, or a home-equity loan. In these instances, a ROBS plan is still allowed but the plan will own less than 100% of the business.

I don’t want to get too deep in the weeds with this point, but it’s usually advisable not to issue 100% of the shares of the business to your 401(k) plan. This could limit your ability to raise additional capital down the road because you don’t have any additional shares to issue to new investors or to share equity with a new partner.

Using the capital to grow your business

Once the share purchase is complete, the cash will be transferred from your retirement account into the business checking account allowing use those funds to start growing the business.

There is a very important rule when it comes to what you can use these funds for within the new business. First and foremost, you cannot use these funds to pay yourself compensation as the business owner. This is probably the biggest ‘no-no’ associated with these types of plans. The IRS does not want you circumnavigating income taxes and penalties just to pay yourself under a ROBS plan. In order to pay yourself as the business owner, you have to be able to generate revenue from the business. The assets from the stock purchase can be used to pay all of your expenses but before you’re able to take any money out of the business to pay yourself compensation you have to be showing revenue.

Once new business owners hear this, it’s often disheartening. It’s great that they have access to capital to build their business, but how do they pay their bills while they’re building up the revenue stream? Luckily, I have good news on this front. We have additional strategies that we can implement using your retirement accounts outside of the ROBS plan that will allow you to pay yourself compensation as the owner and it can work out better tax wise than paying yourself as a W2 income through the C-corp.

Requirements for ROBS plans

There are a few requirements you have to meet for this funding strategy to work.

1) The funds have to be held in a pre-tax retirement account. This means that money in Roth IRA’s and Roth 401(k)’s are not eligible for this funding strategy.

2) You typically need at least $50,000 in your new 401(k) account for the ROBS plan to make sense since there are special costs associated with establishing and maintaining a ROBS 401(k) plan. If your balance is less than $50,000, the cost to establish and maintain the plan begins to outweigh the benefit of executing this funding strategy.

3) If you’re rolling over a 401(k) plan to fund your ROBS 401(k) plan, it cannot be from a current employer. In other words, if you are still working for a company and you’re running this new business on the side, you are not able to rollover your 401(k) balance into your newly established 401(k) plan and implement this ROBS strategy. The 401(k) account must be coming from a former employer that you no longer work for.

4) You have to be an active employee in the business

There are special IRS rules that define if an employee is actively or materially participating in a business. Since ROBS plans do not work for passive business owners, it is difficult to use these plans for real estate investments unless you can prove that you are an active employee of that real estate corporation. If your new business is your only employer, you work over 1000 hours per year, and it’s your primary source of revenue, then you should not have a problem qualifying as an active employee. If you have multiple businesses however, you really need to consult your accountant and ROBS provider to make sure you satisfy the IRS definition of materially participating.

A ROBS plan can be used for more than just start-ups

While we have talked a lot about using ROBS plans to start up a business, they can also be used for other purposes. These plans can be a funding source to:

1) Buy an existing business

2) Recapitalize a business

3) Build a franchise

These plans can offer fast access to large amounts of capital without having to go through the traditional lending channels.

Cost of setting up and maintaining a ROBS plan

It typically costs $4,000 – $5,000 to set up a ROBS plan and you cannot use the balance in your retirement account to pay this fee. It must be paid with outside funds.

As for ongoing fees, you will have the regular administrative, recordkeeping, and investment advisory fees associated with sponsoring a 401(k) plan which vary from provider to provider. You may also have additional fees charged each year by the custodian for holding the privately held C-Corp shares in your retirement account. Make sure you clearly understand what the custodian will require from you each year to value those shares. If you wind up with a custodian that requires audited financial statements, this could easily run you an additional $8,000+ per year to obtain those audited financial statements from an accounting firm. If you are sponsoring one of these plans, you probably want to try to avoid this large additional cost.

Complications if you have employees

For start-up companies or established companies that have employees that would otherwise be eligible for the 401(k) plan, there are special issues that need to be addressed. The rules within the 401(k) world state that all investment options available within the plan must be made available to all eligible employees. That means if the business owner is able to purchase shares of the company within the retirement plan, the other eligible employees must also be given the same investment opportunity. You can see immediately where this would pose a challenge to the ROBS plan if you have eligible employees.

However, investment options can be changed which is why ROBS plans are the most common in start-ups where there are no employees yet, allowing the 401(k) plan to setup the only eligible plan participant, the business owner, allowing them to buy shares of the company. Once the share purchases are complete, the business owner can then remove those shares as an investment option in the plan going forward.

The Cons of a ROBS plan

Up until now we have presented the advantages of the ROBS plan but there are some disadvantages.

1) The first one is pretty obvious. You are risking your retirement account dollars in a start-up business. If the business fails, not only will you be looking for a new job, but you’ve depleted your retirement assets.

2) You are required to sponsor a C-Corp which may not be the most advantageous corporate structure.

3) You are required to sponsor a 401(k) plan. When running a start-up business, it’s sometimes more advantageous to sponsor a Simple IRA or SEP IRA which requires less cost and time to maintain, but you don’t have that option using this funding strategy.

4) The business owners can’t pay themselves compensation from the stock purchase

5) The cost to setup and maintain the plan. Paying $5,000 just to establish the plan isn’t exactly cheap. Plus, you’re looking at $2,000+ in annual maintenance costs for the plan. Other options like taking a home-equity loan or establishing a Solo 401(K) plan and taking a $50,000 401(k) loan from the plan may be the better funding option.

6) Audit risk. While it’s not the case that all these plans are audited, they do present an audit opportunity for the IRS given the compliance rules surrounding the operation of these plans. However, this risk can be managed with knowledgeable providers.

7) Asset sale of the business becomes complex. If 10 years from now you sell your company, there are two ways to sell it. An asset sale or a stock sale. While a stock sale jives very easily with this ROBS funding strategy, an asset sale becomes more complex.

Summary

Finding the capital to start up a business is never easy. Each funding option comes with its own set of pros and cons. The ROBS plan is just another option for consideration. While I have greatly simplified how these plans work and how they operate, if you are strongly considering using this plan as a funding vehicle for your new business, please reach out to us so we can have an open discussion about what you are trying to accomplish, and how the ROBS plan stacks up against other funding options that you may have available.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

New York May Deviate From The New 529 Rules

When the new tax rules were implemented on January 1, 2018, a popular college savings vehicle that goes by the name of a “529 plan” received a boost. Prior to the new tax rules, 529 plans could only be used to pay for college. The new tax rules allow account owners to withdraw up to $10,000 per year per child for K – 12 public school, private school,

When the new tax rules were implemented on January 1, 2018, a popular college savings vehicle that goes by the name of a “529 plan” received a boost. Prior to the new tax rules, 529 plans could only be used to pay for college. The new tax rules allow account owners to withdraw up to $10,000 per year per child for K – 12 public school, private school, religious school, or homeschooling expenses. These distributions would be considered “qualified” which means distributions are made tax free.

Initially we expected this new benefit to be a huge tax advantage for our clients that have children that attend private school. They could fully fund a 529 plan up to $10,000 per year, capture a New York State tax deduction for the $10,000 contribution, and then turn around and distribute the $10,000 from the account to make the tuition payment for their kids.