Paying Down Debt: What is the Best Strategy?

Living with debt is not easy. It can be a constant burden and easily disrupt day-to-day life. Having debt will also ruin your credit score too. The worse your credit score gets, the less likely you will be accepted for any type of loan. One of the fastest ways to get rid of your debt is to pay your debt off in the correct order.

strategies for paying off debt

Living with debt is not easy. It can be a constant burden and easily disrupt day-to-day life. Having debt will also ruin your credit score too. The worse your credit score gets, the less likely you will be accepted for any type of loan. One of the fastest ways to get rid of your debt is to pay your debt off in the correct order.

STEP 1: Create a list of all your current debts

The first step is understanding what you owe. To start, make a master list of all your monthly credit card and loan statements. For each bill, include:

The creditor's name

The total amount you owe on that bill

The minimum required monthly payment

The interest rate (also known as APR)

The payment due date

STEP 2: List all of your monthly expenses

Add up all your monthly expenses: rent, car, food, utilities, health insurance and the minimum payments on your debts; as well as regular spending on things such as entertainment and clothing. Subtract that figure from your monthly after-tax income. The remaining amount is what you could put toward debt repayment each month-though it may make sense for you to save some.

STEP 3: Call your lenders

Call your lenders and explain your situation. They may be willing to lower your interest rate temporarily or waive late fees. You may also be able to lower your interest rate by transferring some high-interest credit card debt onto a new credit card with a lower rate (though that's not a long-term solution).

STEP 4: Payoff high interest rate or small balances first

You can start with the bill carrying the highest interest, or the one with the smallest balance. Prioritizing the highest-rate debt can save you more money: You pay off your most expensive debt sooner. Paying off the smallest debt can eliminate a bill faster, providing a motivating boost. Whichever you choose, make sure to pay at least the minimum on all your debts.

credit card debt

Pay the monthly minimum on each debt. The exception: your target bill. Put more money toward this one to pay it down faster. Once you pay off that bill, choose another to pay down aggressively. Your monthly debt repayment total shouldn't change, even when you eliminate bills. This way you gain momentum as you go, putting more and more money toward each remaining bill.

STEP 5: Get creative

You can use your annual tax refund or holiday bonus to pay down debt. Look for small ways to save money every day, such as riding your bike to work, or eating in instead of dining out. Another way to make a dent quickly is to sell unused or unnecessary belongings-maybe downgrading your car to a more affordable model with lower monthly payments.

STEP 6: Break the cycle

As you start to escape debt, it can be tempting to reward yourself by splurging on a new smartphone or an expensive dinner but just a few purchases can erase all your hard work. Instead, buy things with cash or your debit card, and think long and hard before taking on any new debt.

Read this book

If you want to live a debt free life, I strongly recommend you read the book "Total Money Makeover" by Dave Ramsey. Ramsey's book really paves the way to get out of debt and stay out of debt.

dave ramsey book

Michael Ruger

About Michael.........

Hi, I'm Michael Ruger. I'm the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

What is the Process for Setting Up a Will?

Creating a will is often a task that everyone knows they should do but it gets put on the back burner. Creating a will is one of the most critical things you can do for your loved ones. Putting your wishes on paper helps your heirs avoid unnecessary hassles, and you gain the peace of mind knowing that a life's worth of possessions will end up in the right

What is the Process for Setting Up a Will?

Creating a will is often a task that everyone knows they should do but it gets put on the back burner. Creating a will is one of the most critical things you can do for your loved ones. Putting your wishes on paper helps your heirs avoid unnecessary hassles, and you gain the peace of mind knowing that a life's worth of possessions will end up in the right hands. But before for you do, it helps to know the overall process of setting up a will to save you time and money.

What is a will?

A will is simply a legal document in which you, the testator, declare who will manage your estate after you die. Your estate can consist of big, expensive things such as a vacation home but also small items that might hold sentimental value such as photographs. The person named in the will to manage your estate is called the executor because he or she executes your stated wishes. Sometimes though, people get confused by this and aren't too sure what the meaning of an executor.

A will can also serve to declare who you wish to become the guardian for any minor children or dependents, and who you want to receive specific items that you own - Aunt Sally gets the silver, Cousin Billy the bone china, and so on. Someone designated to receive any of your property is called a "beneficiary."

Some types of property, including certain insurance policies and retirement accounts, generally aren't covered by wills. You should've listed beneficiaries when you took out the policies or opened the accounts. Check if you can't remember, and make sure you keep beneficiaries up to date, since what you have on file when you die should dictate who receives those assets.

What happens if I die without a will?

If you die without a valid will, you'll become what's called intestate. That usually means your estate will be settled based on the laws of your state that outline who inherits what. Probate is the legal process of transferring the property of a deceased person to the rightful heirs.

Since no executor was named, a judge appoints an administrator to serve in that capacity. An administrator also will be named if a will is deemed to be invalid. All wills must meet certain standards such as being witnessed to be legally valid. Again, requirements vary from state to state.

An administrator will most likely be a stranger to you and your family, and he or she will be bound by the letter of the probate laws of your state. As such, an administrator may make decisions that wouldn't necessarily agree with your wishes or those of your heirs.

Do I need an attorney to prepare my will?

No, you aren't required to hire a lawyer to prepare your will, though an experienced attorney can provide useful advice on estate-planning strategies such as establishing testamentary, revocable, and irrevocable trusts. But as long as your will meets the legal requirements of your state, it's valid whether a lawyer drafted it or you wrote it yourself on the back of a napkin.

Do-it-yourself will kits are widely available online which are of course better than nothing but we usually recommend that our clients at least have an attorney review their will and make sure the specifications in their will match their wishes.

Should my spouse and I have a joint will or separate wills?

Estate planners almost universally advise against joint wills, and some states don't even recognize them. Odds are you and your spouse won't die at the same time, and there's probably property that's not jointly held. That's why separate wills make better sense, even though your will and your spouse's will might end up looking remarkably similar.

In particular, separate wills allow for each spouse to address issues such as ex-spouses and children from previous relationships. Ditto for property that was obtained during a previous marriage. Be very clear about who gets what. Probate laws generally favor the current spouse.

Who should I name as my executor?

You can name your spouse, an adult child, or another trusted friend or relative as your executor. If your affairs are complicated, it might make more sense to name an attorney or someone with legal and financial expertise. You can also name joint executors, such as your spouse or partner and your attorney.

One of the most important things your will can do is empower your executor to pay your bills and deal with debt collectors. Make sure the wording of your will allows for this, and also gives your executor leeway to take care of any related issues that aren't specifically outlined in your will.

How do I leave specific items to specific heirs?

If you wish to leave certain personal property to certain heirs, indicate as much in your will. In addition, you can create a separate document called a letter of instruction that you should keep with your will.

A letter of instruction, which isn't legally binding in some states, can be written more informally than a will and can go into detail about which items go to whom. You can also include specifics about any number of things that will help your executor settle your estate including account numbers, passwords and even burial instructions.

Another option is to leave everything to one trusted person who knows your wishes for distributing your personal items. This, of course, is risky because you're relying on this person to honor your intentions without fail. Consider carefully.

Who has the right to contest my will?

Contesting a will refers to challenging the legal validity of all or part of the document. A beneficiary who feels slighted by the terms of a will might choose to contest it. Depending on which state you live in, so too might a spouse, ex-spouse or child who believes your stated wishes go against local probate laws.

A will can be contested for any number of other reasons: it wasn't properly witnessed; you weren't competent when you signed it; or it's the result of coercion or fraud. It's usually up to a probate judge to settle the dispute. The key to successfully contesting a will is finding legitimate legal fault with it. A clearly drafted and validly executed will is the best defense.

Michael Ruger

About Michael.........

Hi, I'm Michael Ruger. I'm the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Need to Know College Savings Strategies

Our newsletter this quarter is dedicated to helping families plan for what has become a life-altering cost of paying for college. But do not fear, there are simple things you can do to boost your children's college fund. It is not news to anyone that over the past 30 years, the cost of college tuition and room & board at all levels has spun out of control.

college savings strategies

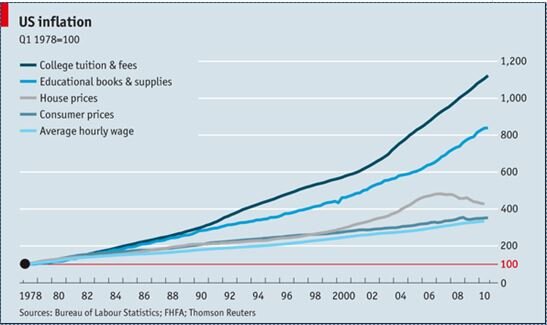

Our newsletter this quarter is dedicated to helping families plan for what has become a life-altering cost of paying for college. But do not fear, there are simple things you can do to boost your children's college fund. It is not news to anyone that over the past 30 years, the cost of college tuition and room & board at all levels has spun out of control. The year over year increase in the cost of tuition and fees since 1978 to date has far outpaced any reasonable rate of inflation, and demands a new look at college savings strategies. In the chart below, you will see the increase in the price of college tuition and fee versus other comparable expenses over the past 30 years. Its mind blowing!!

The need for College Savings Strategies - US Inflation Image

Fund A 529 Account*

As far as college savings strategies go, there are very few options that beat 529 accounts as a savings vehicle for college. In these accounts you make after tax contribution to the account and when the amounts are withdrawn, as long as those withdrawals are attributed to a qualified college expenses, the earnings generated by the account are tax free. Depending on the state you live in you may be eligible to receive a state tax deduction for contribution up to specified dollar amount. In New York, single filers receive a NYS tax deduction up to $5,000 and married filing joint $10,000.

Also for financial aid purposes these account are looked at very favorably in the EFC (Expected Family Contribution) calculation. They are looked at by FASFA as an asset of the "parent" not the asset of the "child". There are many contribution and withdrawal strategies associated with these accounts that can produce big tax benefits for individuals accumulating savings for themselves or their children.

Roth IRAs Are Not Just For Retirement

When clients have the dual goal of saving for retirement and saving for college, the Roth IRA is often times a great option. Even if you make too much to contribute directly to a Roth, you can implement a "non-deductible IRA to Roth IRA conversion strategy" that will allow you to still get money into a Roth IRA.

Contributions to Roth IRAs are made with after tax dollars but unlike a traditional IRA if you hold a Roth IRA for at least 5 years and make withdrawals after age 59 1/2 you pay no tax on the earnings.

Here is one college savings strategy technique: You are allowed at any time and at any age to withdrawal the contribution portion of your account balance from a Roth IRA tax and penalty free. For example, if I contribute $5,000 to a Roth IRA and 5 years later it is worth $10,000, I can contact my IRA provider and request that they distribute just my basis ($5,000) and leave the earnings in the account to continue to accumulate tax free. You can then use that basis distribution to fund college expenses but the earnings in the Roth IRA continue to accumulate tax free.

Maximize Your Financial Aid

There are strategies that can be implemented leading up to the filing of the FASFA form that can increase that amount of financial aid that you receive. When you apply for financial aid, FASFA has a complex EFC calculation that takes a snapshot of your assets and income to determine how much financial aid you will qualify for. There are ways to shift assets and shelter income from this calculation that can save individuals and families thousands of dollars when it come to paying for college. Here are a few of the strategies that can help to improve a EFC calculation:

Save money in the parents or grandparents name, not the childs name

Pay off consumer debt, such as credit cards and auto loans

Spend down the students asset and income first

Accelerate necessary expenses (such as computer purchase) to reduce cash

Minimize capital gains

Maximize your contributions to a retirement plan

Do not withdrawal money from a retirement plan to pay for college

Ask grandparents to wait to give grandchildren money until after college

Trust funds are generally ineffective at sheltering money from EFC

Prepay your mortgage

Contribute to 529 plans owned by the parent or grandparent

Choose the date to submit the FASFA carefully

Michael Ruger

About Michael...

Hi, Im Michael Ruger. Im the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.