Inherited IRA $20,000 State Tax Exemption for New York Beneficiaries Under Age 59 ½

Have you or someone you know recently inherited an IRA in New York? There’s a tax-saving opportunity that many beneficiaries overlook, and we’re here to help you take full advantage of it.

Did you know that if the decedent was 59 ½ or older, you might qualify for a $20,000 New York State income tax exemption on distributions from the inherited IRA—even if you’re under age 59 ½? This little-known benefit could save you a significant amount on taxes, but navigating the rules can be tricky.

Topics covered:

🔹 The $20,000 annual NY State tax exemption for inherited IRAs

🔹 Rules for New York beneficiaries under age 59 ½

🔹 How this exemption can impact the 10-Year Rule distribution strategy

🔹 How tax exemptions are split between multiple beneficiaries

🔹 What if one of the beneficiaries is located outside of NY?

For individuals who inherit a retirement account in New York state, there is a little-known tax law that allows an owner of an inherited IRA to distribute up to $20,000 from their inherited IRA EACH YEAR without having to pay New York State income tax on those distributions. While this $20,000 state tax exemption typically only applies to individuals age 59 ½ or older, there is a special rule that allows beneficiaries of retirement accounts to “inherit” the $20,000 tax exemption from the decedent and avoid having to pay state tax on the distributions from their Inherited IRA, even though they themselves are under the age of 59 ½.

Inherited IRA Owners Under Age 59½

If you inherit a retirement account and you are under the age of 59 ½, there is a whole host of rules that you have to follow in regard to the new 10-Year Distribution Rule, required minimum distributions, and beneficiaries grandfathered in under the old “stretch rules.” We have a separate article that covers these topics in detail:

GFG Article on Inherited IRA Rules for Non-spouse Beneficiaries

However, for the purposes of this article, we are just going to focus on the taxation of distributions from inherited IRAs, specifically the tax exemption for residents of New York State.

Universal Tax Rules at the Federal Level

Regardless of what state you live in, there are tax laws at the federal level that apply to all owners of inherited IRA accounts. The two main rules are:

For inherited IRA owners that are under the age of 59 ½, the 10% early withdrawal penalty does not apply to distributions taken from an inherited IRA.

All distributions from inherited IRA accounts are subject to taxation at the federal level.

IRA Taxation Rules Vary State by State

While the federal taxation rules are the same for everyone, the state rules for the taxation of inherited IRAs vary from state to state. In this article, we will be focusing on the inherited IRA tax rules for residents of New York State.

New York State IRA Taxation

New York has a special rule that once an individual reaches age 59 ½ they are allowed to take distributions from pre-tax retirement account sources and not pay NYS Income tax on the first $20,000 each year. This includes distributions from any type of pre-tax IRA, 401(k), private pension plans, or other types of pre-tax employer-sponsored retirement plans.

But……..New York has another special rule that allows a beneficiary of a retirement account to INHERIT the decedent’s $20,000 state income tax exemption and use it when they take distributions from the inherited IRA account, even though the beneficiary may be under the age of 59 ½.

Rule 1: Decedent Must Have Reached Age 59 ½

For the beneficiary to “inherit” the decedent’s $20,000 NYS IRA tax exemption, the decent must have reached age 59 ½ before they passed away. If the decedent passed away prior to age 59 ½, the beneficiaries of the retirement account are not eligible to inherit the $20,000 NYS tax exemption.

Rule 2: The Beneficiary Must Be A Resident of New York

In order to qualify for the $20,000 NYS tax exemption on the distributions from the inherited IRA account, the beneficiary must be a resident of New York State, which makes sense because if the beneficiary was not a resident of New York, they would not be filing a NY tax return.

Rule 3: The $20,000 NYS Exemption with Multiple Beneficiaries

It’s not uncommon for someone to have more than one beneficiary assigned to their retirement accounts. For purposes of the allocation of the NYS $20,000 exemption, the $20,000 annual exemption is split evenly between the beneficiaries of their retirement accounts. For example, if Sue passed away at age 62 and her 2 children Tracy and Mia, both New York Residents, are listed as 50%/50% beneficiaries, once the assets have been moved into the inherited IRAs for Tracy and Mia, they would both be eligible to claim a $10,000 state tax exemption each year for any distributions taken from the Inherited IRA even though Tracy & Mia are both under that age of 59 ½.

Rule 4: What If One of the Beneficiaries Lives Outside of New York?

But what happens if not all of the beneficiaries are New York residents? Does the beneficiary that lives in New York get to keep the full $20,000 New York State tax exemption?

Answer: No. In cases where one beneficiary is a NY resident and there are other beneficiaries that live outside of New York State, the $20,000 New York State tax exemption is still split evenly among the number of beneficiaries even though there is no tax benefit for the beneficiaries that are domiciled outside of New York.

Follow Up Question: Is there any way for the beneficiaries outside of New York to assign their portion of the $20,000 NYS IRA tax exemption to the beneficiary that lives in New York? Answer: No.

Rule 5: Multiple Retirement Accounts with Different Beneficiaries

So what happens if Tim is age 35, and is the 100% beneficiary of his father’s Traditional IRA, but his father also had a 401(k) account with Tim and his 3 siblings listed as beneficiaries? Does Tim get the full $20,000 NYS exemption for distribution from his Inherited IRA that came from the IRA that he was the sole beneficiary of?

Answer: No. Technically, the $20,000 exemption is split evenly among all of the beneficiaries of the decedent’s retirement accounts in aggregate. In the example above, since Tim was one of four beneficiaries on his father’s 401(k), he would be allocated $5,000 (25%) of the $20,000 New York State exemption each year.

Rule 6: How Would You Find Out “IF” There Are Other Beneficiaries?

There are cases where someone will get notified that they are a beneficiary of a retirement account without knowing who the other beneficiaries are on that account. Most custodians will not disclose who the other beneficiaries are, they typically just notify you of the share of the retirement account that you are entitled to. In this case, how do you know how to split up the $20,000 NYS exemption?

Answer: That is an excellent question. I have no idea.

Rule 7: The $20,000 exemption is an ANNUAL Exemption

The $20,000 NYS tax exemption for distributions from inherited IRAs is an ANNUAL exemption, meaning the owners of the inherited IRAs can use this exemption each year. For example, Ryan’s father passed away at age 70, Ryan is only age 45, he was the sole beneficiary of his father’s Traditional IRA account, Ryan would be allowed to distribute $20,000 per year for his Inherited IRA account and he would avoid having to pay New York State income tax on those distributions up to $20,000 each year.

Tax Note: Once the annual distributions exceed $20,000, NYS income tax will apply.

Rule 8: Beneficiary Already Age 59 ½ or Older

If a non-spouse beneficiary is a New York resident and already age 59 ½ or older, do they get to claim both their own $20,000 NYS tax exemption on distributions from their personal pre-tax retirement accounts and then another $20,000 exemption from the inherited accounts?

Answer: No. The $20,000 NYS tax exemption has an aggregate limit for all pre-tax retirement accounts in a given tax year.

Rule 9: State Pensions PLUS $20,000 NYS Exemption

New York also has the favorable rule that if you are receiving a NYS pension, the amount received from the state pension does not count towards the $20,000 annual IRA tax exemption rule. For example, you could have someone who retired from NYS at age 55 is receiving a NYS pension for $40,000 per year, and if they inherited an IRA, they may also be able to exclude the first $20,000 distributed from the IRA from NYS income taxation.

Tax Strategies For Non-Spouse Beneficiaries Subject to 10-Year Rule

Now that many non-spouse beneficiaries are subject to the new Secure Act 10-Year Rule, requiring them to deplete the inherited IRA within 10 years, if the decedent was over the age of 59 ½ when they passed, it’s important to proactively plan the distribution schedule to take full advantage of the $20,000 NYS tax exemption otherwise owners of the inherited IRA could end up paying more taxes to New York State that could have been avoided.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What is the New York State $20,000 exemption for inherited IRAs?

New York allows beneficiaries of inherited retirement accounts to exclude up to $20,000 per year in distributions from New York State income tax. This rule typically applies to individuals age 59½ or older, but beneficiaries can “inherit” this exemption from the decedent even if they are under 59½.

Who qualifies for the $20,000 New York State exemption on inherited IRAs?

To qualify, the decedent must have been at least age 59½ at the time of death, and the beneficiary must be a current resident of New York State. If both conditions are met, the beneficiary can exclude up to $20,000 in distributions per year from state income tax.

Does the decedent’s age matter for the exemption?

Yes. The decedent must have reached age 59½ before passing away for the beneficiary to inherit the $20,000 exemption. If the decedent died before age 59½, the exemption does not apply to the inherited IRA.

Can beneficiaries outside of New York use this exemption?

No. The beneficiary must be a New York State resident to claim the exemption. Beneficiaries living outside New York cannot use or assign their portion of the $20,000 exemption to others.

How is the $20,000 exemption divided among multiple beneficiaries?

If multiple beneficiaries inherit the decedent’s retirement accounts, the $20,000 annual exemption is split evenly among them. For example, if there are two beneficiaries, each can claim a $10,000 exemption per year; if there are four, each can claim $5,000.

What happens if only one of several beneficiaries lives in New York?

The $20,000 exemption is still split evenly among all beneficiaries, even if only one resides in New York. Nonresident beneficiaries cannot transfer their unused exemption to New York residents.

Does the exemption apply separately to each inherited account?

No. The $20,000 exemption applies in total across all inherited retirement accounts from the same decedent. It does not reset per account.

Can beneficiaries use this exemption every year?

Yes. The $20,000 exemption is an annual benefit. Beneficiaries can exclude up to $20,000 in inherited IRA distributions from New York State income tax each year until the account is depleted.

If the beneficiary is already age 59½, can they claim two exemptions?

No. A beneficiary who is already 59½ or older can only claim one $20,000 exemption per year in total across all their retirement accounts, including both personal and inherited accounts.

Does the exemption affect New York State pensions?

No. New York State pension income is already fully exempt from state income tax. The $20,000 retirement distribution exemption applies separately to IRA and 401(k) distributions, meaning eligible retirees can exclude both their NYS pension income and up to $20,000 in IRA distributions annually.

How can beneficiaries maximize the tax benefit under the 10-Year Rule?

Beneficiaries subject to the Secure Act’s 10-Year Rule should consider spreading withdrawals strategically to use the $20,000 New York exemption each year, reducing overall state taxes on inherited IRA distributions.

Tax-Loss Harvesting Rules: Short-Term vs Long-Term, 30-Day Wash Rule, $3,000 Tax Deduction, and More…….

As an investment firm, November and December is considered “tax-loss harvesting season” where we work with our clients to identify investment losses that can be used to offset capital gains that have been realized throughout the year in an effort to reduce their tax liability for the year. But there are a lot of IRS rule surrounding what “type” of realized losses can be used to offset realized gains and retail investors are often unaware of these rules which can lead to errors in their lost harvesting strategies.

As an investment firm, November and December is considered “tax-loss harvesting season”, where we work with our clients to identify investment losses that can be used to offset capital gains that have been realized throughout the year to reduce their tax liability for the year. But there are a lot of IRS rules surrounding what “type” of realized losses can be used to offset realized gains, and retail investors are often unaware of these rules which can lead to errors in their lost harvesting strategies. In this article, we will cover loss harvesting rules for:

Realized Short-term Gains

Realized Long-term Gains

Mutual Fund Capital Gains Distributions

The $3,000 Annual Realized Loss Income Deduction

Loss Carryforward Rules

Wash Sale Rules

Real Estate Investments

Business Gains or Losses

Short-Term vs Long-Term Gain and Losses

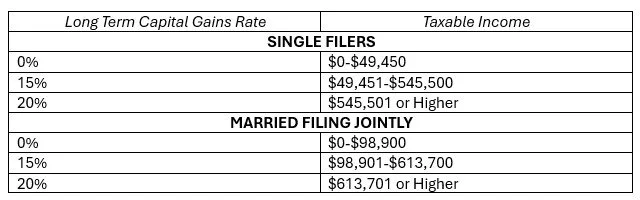

Investment gains and losses fall into two categories: Long-Term and Short-Term. Any investment, whether it’s a stock, mutual fund, or real estate, if you buy it and then sell it within 12 months, that gain or loss is classified as a “short-term” capital gain or loss and is taxed to you as ordinary income.

If you make an investment and hold it for more than 1 year before selling it, your gain or loss is classified as a “long-term” capital gain or loss. If it’s a gain, it’s taxed at the preferential long-term capital gains rates. The long-term capital gains tax rate that you pay varies based on the amount of your income for the year (including the amount of the long-term capital gain). For 2026, here is the table:

Note: For individuals in the top tax bracket, there is a 3.8% Medicare surcharge added on top of the federal 20% long-term capital gains tax rate, so the top long-term capital gains rate ends up being 23.8%. For individuals that live in states with income tax, many do not have special tax rates for long-term capital gains and they are simply taxed as additional ordinary income at the state level.

What Is Year End Loss Harvesting?

Loss harvesting is a tax strategy where investors intentionally sell investments that have lost value to generate a realized loss to offset a realized gain that they may have experienced in another investment. Example, if a client sold Nvidia stock in May 2025 and realized a long-term capital gain of $100,000 in November and they look at their investment portfolio an notice that their Plug Power stock has an unrealized loss of $100,000, if they sell the Plug Power stock and generate a $100,000 realized loss, it would completely wipes out the tax liability on the $100,000 gain that they realized on the sale of their Nvidia stock earlier in the year.

Loss harvesting is not an all or nothing strategy. In that same example above, even if that client only had $30,000 in unrealized losses in Plug Power, realizing the loss would at least offset some of the $100,000 realized gain in their Nvidia stock sale.

Long-Term Losses Only Offset Long-Term Gains

It's common for investors to have both short-term realized capital gains and long-term realized capital gains in a given tax year. It’s important for investors to understand that there are specific IRS rules as to what TYPE of investment losses offset investment gains. For example, realized long-term losses can only be used to offset realized long-term capital gains. You cannot use realized long-term losses to offset a short-term capital gain.

Short-Term Losses Can Offset Both Short-Term & Long-Term Gain

However, realized short-term losses can be used to offset EITHER short-term or long-term capital gains. If an investor has both short-term and long-term gains, the short-term realized losses are first used to offset any short-term gains, and then the remainder is used to offset the long-term gains.

Loss Carryforward

What happens when your realized loss is greater than your realized gain? You have what’s called a “loss carryforward”. If you have unused realized investment losses, those unused losses can be used to offset investment gains in future tax years. Example, Joe sells company XYZ and has a $30,000 realized long-term loss. The only other investment income that Joe has is a short-term gain of $5,000. Since you cannot use a long-term loss to offset a short-term gain, Joe’s $30,000 in realized long-term losses cannot be used in this tax year. However, that $30,000 loss will carryforward to the next tax year, and if Joe has a long-term realized gain of $40,000 that next year, he can use the $30,000 carryforward loss to offset a larger portion of that $40,000 realized gain.

When do carryforward losses expire? Answer: never (except for when you pass away). The carryforward loss will continue until you have a gain to offset it.

$3,000 Capital Loss Annual Tax Deduction

Even if you have no realized capital gains for the year, it may still make sense from a tax standpoint to generate a $3,000 realized loss from your investment accounts because the IRS allows you deduct up to $3,000 per year in capital losses against your ordinary income. Both short-term and long-term losses qualify toward that $3,000 annual tax deduction.

Example: Sarah has no realized capital gains for the year, but on December 15th she intentionally sells shares of a mutual fund to generate a $3,000 long-term realized loss. Sarah can now use that $3,000 loss to take a deduction against her ordinary income.

Tax Note: You do not need to itemize to take advantage of the $3,000 tax deduction for capital losses. You can elect to take the standard deduction when filing your taxes and still capture the $3,000 tax deduction for capital losses.

The $3,000 annual loss tax deduction can also be used to eat up carryforward losses. If we go back to our example with Joe who had the $30,000 realized long-term loss, if he does not have any future capital gains to offset them with the carryforward loss, he could continue to deduct $3,000 per year against his ordinary income over the next 10 years, until the loss has been fully deducted.

Mutual Fund Capital Gain Distribution

For investors that use mutual funds as an investment vehicle within a taxable investment account, certain mutual funds will issue a “capital gains distribution”, typically in November or December of each year, which then generates taxable income to the shareholder of that mutual fund, whether they sold any shares during the year.

When mutual funds issue capital gains distributions, it’s common that a majority of the capital gains distributions will be long-term capital gains. Similar to normal realized long-term capital gains, investors can loss harvest and generate realized losses to offset the long-term capital gains distribution from their mutual fund holdings in an effort to reduce their tax liability.

The Wash Sale Rule

When loss harvesting, investors have to be aware of the IRS “Wash Sale Rule”. The wash sale rule states that if you sell a security at a loss and the rebuy a substantially identical security within 30 days following the date of the sale, a realized loss cannot be captured by the taxpayer.

Example: Scott sells the Nike stock on December 1, 2026 which generates a $10,000 realize loss, but then Scott repurchases Nike stock on December 25, 2025. Since Scott repurchased Nike stock within 30 days of the sell day, he can no longer use the $10,000 realized loss generated by his sell transaction on December 1st due to the IRS 30 Day Wash Rule.

Also make note of the term “substantially identical” security. If you sell the Vanguard S&P 500 Index ETF to realize a loss but then purchase the Fidelity S&P 500 Index ETF 15 days later, while they are two different investments with different ticker symbols, the IRS would most likely consider them substantially identical triggering the Wash Sale rule.

Real Estate & Business Loss Harvesting

While most of the examples today have been centered around stock investments, the lost harvesting strategy can be used across various asset classes. We have had clients that have sold their business, generating a large long-term capital gain, and then we have them going into their taxable brokerage account looking for investment holdings that have unrealized losses that we can realize to offset the taxable long-term gain from the sale of their business.

The same is true for real estate investments. If a client sells a property at a gain, they may be able to use either carryforward losses from previous tax years or intentionally realize losses in their investment accounts in the same tax year to offset the taxable gain from the sale of their investment property.

Last updated June, 2026

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What is tax-loss harvesting?

Tax-loss harvesting is a year-end tax strategy where investors sell investments that have declined in value to realize a loss that can be used to offset realized capital gains for the year. For example, if you realized a $100,000 gain from one stock, selling another stock with a $100,000 loss could eliminate the tax liability from that gain.

What is the difference between short-term and long-term capital gains and losses?

Short-term gains or losses come from investments held for one year or less and are taxed as ordinary income. Long-term gains or losses come from investments held for more than one year and qualify for lower, preferential long-term capital gains tax rates.

Can long-term losses offset short-term gains?

No. Realized long-term losses can only be used to offset realized long-term gains. However, realized short-term losses can be used to offset both short-term and long-term capital gains.

What happens if my realized losses are greater than my gains?

If your realized losses exceed your gains, the remaining amount becomes a loss carryforward. You can carry forward unused losses indefinitely and use them to offset future realized gains.

What is the $3,000 capital loss deduction?

Even if you have no capital gains, you can deduct up to $3,000 in realized capital losses per year against ordinary income. For married couples filing separately, the limit is $1,500. Any remaining unused losses can continue to carry forward to future tax years.

What are mutual fund capital gain distributions?

Mutual funds often distribute capital gains to shareholders at the end of the year, usually in November or December. These distributions create taxable income for the investor—even if no shares were sold. Tax-loss harvesting can help offset the tax impact of these mutual fund capital gains distributions.

What is the wash sale rule?

The IRS wash sale rule disallows a realized loss if you sell a security at a loss and buy a “substantially identical” security within 30 days before or after the sale. For instance, selling a Vanguard S&P 500 Index ETF and repurchasing a similar Fidelity S&P 500 ETF within 30 days would likely violate the wash sale rule.

Do loss harvesting rules apply to real estate and business sales?

Yes. The same loss-harvesting concept can apply when selling real estate or a business at a gain. Investors can use realized losses from their taxable brokerage accounts or carryforward losses from prior years to offset taxable gains from these sales.

Can You Process A Qualified Charitable Distribution (QCD) From an Inherited IRA?

Qualified Charitable Distributions are an advanced tax strategy used by individuals who are age 70½ or older who typically make annual contributions to their church, charity, or other not-for-profit organizations. QCDs allow individuals who have pre-tax IRAs to send money directly from their IRA to their charity of choice, and they avoid having to pay tax on those distributions. However, a client recently asked an excellent question:

“Can you process a qualified charitable distribution from an Inherited IRA? If yes, does that QCD also count toward the annual RMD requirement?”

Qualified Charitable Distributions are an advanced tax strategy used by individuals who are age 70½ or older who typically make annual contributions to their church, charity, or other not-for-profit organizations. QCDs allow individuals who have pre-tax IRAs to send money directly from their IRA to their charity of choice, and they avoid having to pay tax on those distributions. However, a client recently asked an excellent question:

“Can you process a qualified charitable distribution from an Inherited IRA? If yes, does that QCD also count toward the annual RMD requirement?”

QCD from an Inherited IRA

The short answer to both of those questions is “Yes”. As long as the owner of the Inherited IRA account is age 70½ or older, they would have the option to process a QCD from their inherited IRA, and that QCD amount would count towards the annual required minimum distribution (RMD) if one is required.

What is a QCD?

When you process distributions from a Traditional IRA account, in most cases, those distributions are taxed to the account owner as ordinary income. However, once an individual reaches the age of 70½, a new distribution option becomes available called a “QCD” or a qualified charitable distribution. This allows the owner of the IRA to issue a distribution directly to their church or charity of choice, and they do not have to pay tax on the distribution.

Backdoor Way To Recapture Tax Deduction for Charitable Contribution

Due to the changes in the tax laws, about 90% of the taxpayers in the U.S. elect to take the standard deduction when they file their taxes, as opposed to itemizing. Since charitable contributions are an itemized deduction, that means that 90% of taxpayers no longer receive a tax benefit for their charitable contributions throughout the year.

A backdoor way to recapture that tax benefit is by making a QCD from a Traditional IRA or Inherited Traditional IRA, because the taxpayer can now avoid paying income tax on a pre-tax retirement account by directing those distributions to a church or charity. So, in a way, they are recapturing the tax benefits associated with making a charitable contribution, and they do not have to itemize on their tax return to do it.

QCD Limitations

There are three main limitations associated with processing qualified charitable distributions:

The first rule that was already mentioned multiple times is that the individual processing the QCD must be 70½ or older. For individuals turning 70½ this year, a very important note, you cannot process the QCD until you have actually turned 70½ to the DAY. I have seen individuals make the mistake of processing a QCD in the year that they turn 70½ but before the exact day that they reached age 70½. In those cases, the distribution no longer qualifies as a QCD.

Example: Jen turned 70 in February 2024, and she wants to make a QCD from her Inherited IRA. Jen would have to wait until August 2024, when she officially reaches age 70½, to process the QCD. If she attempts to process the QCD before she turns 70½, the full amount of the IRA distribution will be taxable to Jen.

QCD $100,000 Annual Limit

Each taxpayer is limited to a total of $100,000 in QCDs in any given tax year, so the dollar limit each year is relatively high. That full $100,000 could be remitted to a single charity or it could be split up among any number of charities.

QCD’s Can Only Be Processed From IRAs

If you inherit a pre-tax 401(k) account, you would not be able to process a QCD directly from the 401(K) plan. 401(k) accounts are not eligible for QCDs. You would first have to rollover the balance in the 401(K) to an Inherited IRA, and then process the QCD from there.

QCDs Count Toward the RMD Requirement

If you have inherited a retirement account, you may or may not be subject to the new 10-year rule and/or required to take annual RMDs (required minimum distributions) for your inherited IRA each year. For purposes of this article, if you subject to the annual RMD requirement, these QCD count toward the annual RMD amount.

Example: Tom has an inherited IRA and he is subject to the new 10-year rule and is also required to distribute annual RMD’s from the IRA during the 10 year period. If the RMD amount of 2025 is $5,000, assuming that Tom has reached age 70½, he would be eligible to process an QCD for the full amount of the RMD, he will be deemed as satisfying the annual RMD requirement, and does not have to pay tax on the $5,000 distribution that was directed to charity.

This is also true for 10-year rule distributions. If someone gets to the end of the 10-year period, there is $60,000 remaining in the inherited IRA, and the account owner is age 70½ or older, they could process a QCD for all or a portion of that remaining balance and avoid having to pay tax on any amount that was directed to a charity or not-for-profit.

QCD Distributions Must Be Sent Directly To Church or Charity

One of the important rules with processing these QCDs is the owner of the Inherited IRA can never come into contact with the money. The distribution has to be sent directly from the IRA custodian to the church or charity.

For our clients, a common situation is sending money directly to their church as opposed to putting money in the offering plate each Sunday. If they estimate that they donate about $4,000 to their church throughout the year, in January, they request that we process a QCD from their inherited IRA to their church in the amount of $4,000 and that amount is a non-taxable distribution from their IRA.

When the distribution is requested, we have to ask the client how to make the check payable and the mailing address of the church, and then our custodian (Fidelity) processes the check directly from their IRA to the church.

No Special Tax Code on 1099-R for QCDs

Anytime you process a distribution from an inherited IRA, the custodian of the IRA will issue you a 1099-R tax form at the end of the year so you can report the distribution amount on your tax return. With QCD, there is not a special tax code indicating that it was a QCD. If you use an accountant to prepare your taxes, you must let them know about the QCD, so they do not report the distribution as taxable income to you.

Summary

For individuals who inherit Traditional IRAs and have charitable intent, processing Qualified Charitable Distributions each year can be an excellent way to recapture the tax deduction that is being lost for their charitable contributions while at the same time counting toward the annual RMD requirement for that tax year.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

Can you make a Qualified Charitable Distribution (QCD) from an inherited IRA?

Yes. If the owner of the inherited IRA is age 70½ or older, they can make Qualified Charitable Distributions (QCDs) directly from their inherited IRA. These distributions can also count toward satisfying their annual Required Minimum Distribution (RMD).

What is a Qualified Charitable Distribution (QCD)?

A QCD allows individuals age 70½ or older to transfer funds directly from their Traditional IRA to a qualified charity without paying federal income tax on the distribution. It’s a tax-efficient way to give to charity while reducing taxable income.

Do QCDs count toward required minimum distributions (RMDs)?

Yes. If you are required to take RMDs from your IRA or inherited IRA, the amount of any QCDs you make during the year will count toward satisfying your RMD obligation for that year.

Can you process a QCD from a 401(k)?

No. QCDs can only be made from IRA accounts, including inherited IRAs. If you inherit a 401(k), you must first roll it over into an inherited IRA before making a Qualified Charitable Distribution.

What is the annual limit for QCDs?

Each taxpayer can make up to $100,000 in Qualified Charitable Distributions per year. Married couples filing jointly can each contribute up to $100,000 from their respective IRAs.

What age must you be to make a QCD?

You must be at least 70½ years old to the day before making a Qualified Charitable Distribution. If the QCD is processed before you reach 70½, the entire amount will be treated as a taxable distribution.

Do you get a tax deduction for a QCD?

No separate deduction is taken, but the QCD amount is excluded from taxable income. This provides a “backdoor” tax benefit for charitable giving, especially for those who take the standard deduction and do not itemize.

How must QCD funds be sent to the charity?

The funds must go directly from the IRA custodian to the charity. The account owner cannot receive the money first. For example, if donating to a church, the custodian issues the check directly payable to the church, not the IRA owner.

How are QCDs reported on tax forms?

The IRA custodian will issue a Form 1099-R showing the distribution, but it will not be coded as a QCD. It’s important to inform your tax preparer that the distribution was a QCD so it isn’t mistakenly reported as taxable income.

Why use QCDs from inherited IRAs?

QCDs from inherited IRAs allow charitably minded individuals to reduce taxable income while meeting RMD requirements. It’s especially useful for retirees and beneficiaries who no longer itemize deductions but still make annual charitable donations.

What Happens When A Minor Child Inherits A Retirement Account?

There are special non spouse beneficiary rules that apply to minor children when they inherit retirement accounts. The individual that is assigned is the custodian of the child, we'll need to assist them in navigating the distribution strategy and tax strategy surrounding they're inherited IRA or 401(k) account. Not being aware of the rules can lead to IRS tax penalties for failure to take requirement minimum distributions from the account each year.

There are special non-spouse beneficiary rules that apply to minor children when they inherit retirement accounts. The individual who is assigned as the custodian of the child will need to assist them in navigating the distribution strategy and tax strategy surrounding their inherited IRA or 401(k) account. Not being aware of the rules can lead to IRS tax penalties for failure to take the required minimum distributions from the account each year.

Minor Child Rule After December 31, 2019

Congress changed the rules for minor children as beneficiaries of retirement accounts when they passed the Secure Act in 2019. If the Minor child inherits a retirement account from someone who passes away after December 31, 2019, the minor child is subject to the new nonspouse beneficiary rules associated with the new tax law. The new tax law creates a blend of the old “stretch rule” and the new 10-year rule for children that inherit retirement accounts. It also matters who the child inherited the account from - a parent, or someone other than a parent.

Minor Child Inherits Retirement Account From A Parent

If a minor child inherits a retirement account from their parents, and the parent that they inherited the account from passed away after December 31, 2019, the minor child will need to move the 401(k) or IRA into an Inherited IRA before December 31st of the year after their parent passes away, and then begin taking annual Required minimum distributions (RMDs) from the inherited IRA each year until they reach age 21. Once they reach age 21, they are then subject to the 10-year rule, which requires the minor to fully deplete the account within 10 years of turning age 21.

Age of Majority is 21

Different states have different ages of majority, some 18 and others 21. But the IRS released clarifying final regulations in July 2024, stating that for purposes of minor children moving from the annual RMD requirement to the 10-year rule would be the age of 21 regardless of the state the child lives in and regardless of whether or not the child is a student after age 18.

Here is an example: Richard passes away in a car accident in March 2024, the sole beneficiary of his 401 (k) at work is his 10-year-old daughter, Kelly. Kelly’s guardian would need to assist her with setting up an inherited IRA before December 31, 2025, and rollover Richard’s 401K balance into that Inherited IRA account. Since Kelly is under the age of 21, she would be required to take annual required minimum distributions from the account, which are calculated based on her age and an IRS life expectancy table beginning in 2025. When she receives those annual RMDs for the Inherited IRA, she has to pay income tax on them, but does not incur a 10% early withdrawal penalty for being under the age of 59 1/2 since they are considered death distributes.

Kelly will need to continue to take those RMD's each year until she reaches age 21. At age 21, she is then subject to the new 10-year rule associated with non-spouse beneficiaries which requires her to fully deplete that inherited IRA balance within 10 years of reaching the age 21.

Tax Strategy For Inherited IRAs for Minors

The guardians of the minor child will need to assist them with the tax strategy associated with taking distributions from their inherited IRA account, since any money withdrawn from these accounts is considered taxable income to the child. While the IRS requires the minor child to take a small distribution each year to satisfy the annual RMD requirement, they are allowed to take any amount they would like out of the inherited IRA which creates a tax planning opportunity since most children have very little taxable income, and are in very low tax brackets.

However, distributions from inherited IRAs are considered “unearned income” subject to Kidde tax so the custodian’s of the minor’s inherited IRA have to be very careful of taking distribution above the current $1,350 amount which then triggers the Kiddie tax.

FAFSA Warning

Another factor to consider one taking distributions from a minor’s inherited IRA is the impact on their college financial aid if they are college bound after high school. Distributions from these inherited IRA accounts are considered income of the child which is the most punitive category within the college financial aid award formula. A child’s income, over a specific threshold, counts approximately 50% against any college financial aid that could potentially be awarded. So, if a child processes a distribution from their inherited IRA for $20,000, while it might be a good tax move, if that child would have qualified for need based college financial aid, they may have just lost $10,000 in aid due to that IRA distribution during a determination year.

When a FAFSA application is completed for a child, the determined year for income purposes of the financial aid award looks back 2 years, so there is a lot of advanced planning by the guardian of the child that needs to take place to make sure larger inherited IRA distributions do not adversely affect the FAFSA award.

Example: If the child will be entering college in the fall of 2025, the FAFSA calculations looks at their income from 2023 to determine how much college financial aid they qualify for.

Traditional IRA vs Roth IRA

It does matter whether the child inherits a Traditional IRA or a Roth IRA. The RMD rule and the 10-year rule are the same, but the taxation of the distributions from the IRA to the child are different. If the child has an Inherited Traditional IRA, the guardian has to be more careful about making distributions to the minor child because all distributions are considered taxable income. If the child has an Inherited Roth IRA, by nature of the Roth IRA rules the distributions are not taxable to the minor child. However, Roth IRA's are extremely valuable because all the accumulation within the inherited Roth IRA are tax free upon withdrawal, so typically the strategy is to keep the account intact as long as possible so the child receives as much tax free appreciation as possible at the end of the 10 years.

Minor Child 10-Year Rule

Once the child reaches age 21, the rules change to the 10-year rule, which requires the child to deplete any remaining balance in the inherited IRA within 10 years of turning age 21. The child has full discretion on the amounts that they wish to withdraw from their inherited IRA each year.

Minor Child Inherits A Retirement Account From A Non-Parent

If a minor child inherits a retirement account from someone other than their parents, the inherited IRA rules are different. The child is no longer allowed to take RMD’s from the inherited IRA each year until age 21, and then switch to the 10 year rule. If the child inherits a retirement account from someone other than their parent, they are treated the same as any other non-spouse beneficiary, and are immediately subject to the 10 year rule. They may or may not be required to take RMDs each year IN ADDITION to being required to deplete the account within 10 years, but that depends on what the age of the decedent was when they passed.

When the decedent passed away, if they had already reached their Required Beginning Date for RMDs, then the minor child would be required to continue to take annual RMD’s from the inherited IRA in addition to the 10-year rule starting immediately. If the decedent has yet to reach the required beginning date for RMDs, then the minor child is just subject to the 10-year rule.

In either situation, a minor child immediately subject to the 10-year rule requires detailed tax planning to avoid adverse and toxic consequences of poor distribution planning to avoid the loss of college financial aid due to the taxable income assigned to the child associated with those distributions from the inherited IRA.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What are the special inheritance rules for minor children who inherit retirement accounts?

When a minor inherits a retirement account, the account must be transferred into an inherited IRA, and the child’s custodian must ensure required distributions are taken each year. The Secure Act of 2019 created specific rules for minors that combine annual required minimum distributions (RMDs) with the 10-year depletion rule once the child reaches age 21.

How do the inherited IRA rules differ if the minor inherits from a parent versus a non-parent?

If the child inherits from a parent, they must take annual RMDs until age 21 and then deplete the account within 10 years after turning 21. If the inheritance comes from someone other than a parent, the child is treated as a standard non-spouse beneficiary and must follow the 10-year rule immediately, with RMDs possibly required depending on the age of the deceased.

What did the 2024 IRS guidance clarify about the age of majority for inherited IRAs?

In July 2024, the IRS confirmed that for inherited IRA purposes, the age of majority is 21 nationwide, regardless of state laws or student status. This means the 10-year distribution clock begins when the child turns 21, not earlier.

How are inherited IRA distributions for minors taxed?

Distributions from inherited traditional IRAs are taxable income to the child, though they are exempt from early withdrawal penalties. These withdrawals count as unearned income and may trigger the Kiddie Tax if annual unearned income exceeds $2,700.

How can inherited IRA distributions affect college financial aid?

Withdrawals from an inherited IRA are counted as the child’s income for FAFSA purposes, which can significantly reduce need-based financial aid. Because FAFSA reviews income from two years prior, guardians should time distributions carefully to avoid lowering aid eligibility.

Do inherited Roth IRAs follow the same rules as inherited traditional IRAs?

Yes, both types are subject to RMD and 10-year rules, but Roth IRA distributions are tax-free. This makes inherited Roth IRAs especially valuable if left to grow for the full 10-year period, allowing for maximum tax-free appreciation.

What steps should guardians take when managing a minor’s inherited IRA?

Guardians should ensure the account is properly set up as an inherited IRA, monitor RMD compliance, and plan withdrawals to balance tax efficiency, Kiddie Tax exposure, and college aid implications. Proper planning helps avoid penalties and unnecessary loss of financial aid.

Last updated June, 2026

What Happens When You Inherit an Already Inherited IRA?

When you are the successor beneficiary of an Inherited IRA the rules are very complex.

When someone passes away and they have a retirement account, if there are non-spouse beneficiaries listed on the account, they will typically rollover the balance in the inherited retirement account to either an Inherited Traditional IRA or Inherited Roth IRA. But what happens when the original beneficiary passes away and there is still a balance remaining in that inherited IRA account? The answer is that a successor beneficiary inherits the account, and then the distribution rules become complex very quickly.

Beneficiary of an Inherited IRA (Successor Beneficiaries)

As a beneficiary of an inherited IRA, it's important to understand that the options available to you for taking distributions for the account will be determined by the distribution options that were available to the original beneficiary of the retirement account that you inherited it from, which vary from beneficiary to beneficiary.

Non-spouse Inherited IRA Rule

The IRS changed the rules for non-spouse beneficiaries back in 2019 with the passing of the Secure Act, which put original non-spouse beneficiaries in two camps: beneficiaries that inherited a retirement account from someone that passed away prior to January 1, 2020, and beneficiaries that inherited retirement accounts some someone that passed January 1, 2020 or later.

We have a whole article dedicated to these new non-spouse beneficiary rules that can be found on our website but for now I will move forward with the cliff notes version.

Stretch Rule vs 10-Year Rule Beneficiaries

As the beneficiary of an inherited IRA, you must be able to answer two questions:

Was the original beneficiary subject to the “RMD stretch rule” or “10-year rule”?

If that beneficiary was required to take an RMD in the year they passed, did they already distribute the full amount?

Original Beneficiary was the Spouse

A common situation is that a child has two parents - the first parent passes away, and the balance in those retirement accounts are then inherited by the surviving spouse and moved into the surviving spouse’s own retirement accounts. A spouse of an original owner of a retirement account has special rules available to them which allow them to roll their deceased spouse’s retirement accounts into their own retirement accounts and treat them as their own. When their children inherited the remaining balance in the retirement accounts from the second to parent, they are considered non spouse beneficiaries and are most likely subject to the new 10-year distribution rule unless they qualify for an exception.

Non-spouse Beneficiary 10-Year Rule

If the original beneficiary of the Inherited IRA received that account from someone that passed away after December 31, 2019 and they are a non-spouse beneficiary, they are most likely subject to the new 10-Year Rule which requires the original beneficiary to fully deplete that retirement within 10 year of the year following the original decedent’s death.

Example: Sue, the original owner of a Traditional IRA passes away in 2022, and her daughter Katie is the sole beneficiary of her IRA. Since Katie is a non-spouse beneficiary, she would be required to fully deplete the IRA by 2032, 10 years following the year after that Sue passed away.

But what happens if Katie, the original beneficiary of that inherited IRA passes away in 2026, and she is only 4 years into the 10-year depletion cycle? In this example, when Katie set up her inherited IRA, she named her two children Scott & Mara as 50/50 beneficiary on her inherited IRA account. Scott and Mara would move their respective 50% balance into their own inherited IRA account but as beneficiaries of an already inherited IRA, the 10-year rule does not reset. Scott & Mara would be bound to the same 10-year depletion date that Katie was subject to so Scott & Mara would have to deplete the Inherited IRA (2 times inherited) by 2032 which was Katie’s original 10-year depletion date.

10-Year Rule: The basic rule is if the original beneficiary of the inherited IRA was subject to the 10-year rule, as the new beneficiary of that existing inherited IRA, you get whatever time is remaining in that original 10-year period to fully deplete that Inherited IRA. It does not matter whether the inherited IRA that you inherited was a Traditional IRA or a Roth IRA, the same rules apply.

Original Beneficiary was a “Stretch Rule” beneficiary or the Spouse

For original non-spouse beneficiaries that inherited the retirement account from an account owner that passed away before January 1st, 2020, they have access to what is called the Stretch Rule. Those non-spouse beneficiaries are allowed to move the original owners balance of the retirement account to their own inherited IRA and they are not required to deplete the account in 10 years.

Instead, those non-spouse beneficiaries are only required to take an annual RMD (required minimum distribution) each year, which are small distributions from the Inherited IRA each year, but they could effectively stretch the existence of that inherited account over their lifetime. But it’s also important to note, that some non-spouse beneficiaries that inherited a retirement account from someone who passes on or after January 1, 2020, may have qualified for a stretch rule exception which are as follows:

Surviving spouse

Person less than 10 years younger than the decedent

Minor children

Disabled person

Chronically ill person

Some See-Through Trusts benefitting someone on this exception list

If the original beneficiary of the inherited IRA was eligible for the stretch rule, and you inherited that inherited IRA from that individual, you would NOT be eligible for the Stretch Rule, you would be subject to the 10-year rule, but you would have a full 10-years after the owner of that inherited IRA passes away to fully deplete the balance in that inherited IRA that you inherited.

When we are talking about beneficiaries of an already inherited IRA, it does not matter whether you were their spouse or non-spouse because the spouse exceptions only apply to the spouse of the original decedent.

Example: John inherited a Traditional IRA from his father who passed away in 2018. John was a non-spouse beneficiary, but since his father passed before 2020, he was eligible for the stretch provision which allowed John to roll over the Traditional IRA to an inherited IRA in his name and he was only required to take annual RMD’s each year but was not required to deplete the account in 10 years. John passes in 2025, his daughter Sarah is the beneficiary of the Inherited IRA, since Sarah inherited the inherited IRA from John who passes after December 31, 2019, Sarah would be required to deplete the balance in John’s inherited IRA by 2035, 10-year following the year after John passes.

RMD of Beneficiaries of Inherited IRAs

Now we have to move on to the second question that beneficiaries of Inherited IRAs need to ask, which is “does the successor beneficiary of an inherited IRA need to take annual RMD’s from the account each year?” The answer is “it depends”.

It’s common for beneficiaries of Inherited IRAs to be subject to both the 10-year rule and be required to take annual required minimum distributions from the account. Whether or not the beneficiary needs to take an RMD will depend on the whether or not the original beneficiary of the account was required to take RMDs. The basic rule is if the current owner of the Inherited IRA was required to take annual RMD’s from the account, you as the beneficiary of the Inherited will be required to continue to take RMD’s from the account. The IRS has a rule that once an owner of an IRA or Inherited IRA has started taking RMDs, they cannot be stopped.

If the answer is “Yes:”, the person that you inherited the Inherited IRA from was already taking RMD’s from the Inherited IRA account, then you as the beneficiary of that inherited IRA would be subject to whatever time is left in the 10-year rule, and you would also be required to take RMDs from the account each year.

Don’t Forget To Take The Decedent’s RMD

RMD’s are usually required to begin the year after an individual passes away which is true of Inherited IRAs but as the beneficiary of an retirement account, where the decedent was required to take an RMD for that year, you have to ask the question: did they satisfy their RMD requirement before they passed away.

If the answer is “yes”, no action is required in the year that they passed away unless they were in year 10 year of the depletion cycle.

If the answer is “no”, then you as the beneficiary of that existing Inherited IRA are required to take the undistributed RMD amount from that inherited IRA in the year that the decedent passed away.

Example: Kelly inherits an Inherited IRA from her mother Linda. Linda originally inherited the IRA from her father when he passed in 2022. At the time that her father passed, he was 80, which made him subject to RMDs. When Linda inherited the account from her father, since he was subject to RMDs, Linda was subject to the 10-year rule and annual RMDs. Linda passed in 2024, her daughter Kelly inherits her Inherited IRA, and Kelly would be required to fully deplete the inherited IRA by 2032 (Linda original 10 year rule date), she would be required to take annual RMD’s from the account because Linda was receiving RMDs, and if Linda did not receive her full RMD in 2024 when she passed, Kelly would have to distribute any amount that Linda would have been required to take in the year that she passes.

A lot of rules, but all very important to avoid the IRS penalties that await the taxpayers that fail to take the proper RMD amount or fail to adhere to the new 10-year rule.

Summary of 3 Successor IRA Questions

When you are the beneficiary of an inherited IRA, you must be able to answer the following questions:

Was the person that you inherited the inherited IRA from subject to the 10-year rule?

Was the person that you inherited the Inherited IRA from required to take annual RMDs?

Did the decedent take their RMD before they passed?

What was the age of the decedent when that passed?

The last question is important because there are potential situations where someone is the original beneficiary of an Inherited IRA subject to the 10-year rule, based on the age of the original owner when they passed and the age when the original beneficiary when they inherited the IRA may not make them subject to the annual RMD requirement. However, if the original beneficiary passes away after their “Required Beginning Date” for RMDs, the beneficiary of that inherited IRA may be subject to an annual RMD requirements even though the original beneficiary was not.

The IRS has unfortunately made the rules very complex for beneficiaries of an Inherited IRA account, so I would strongly recommend consulting with a professional to make sure you fully understand the rules.

General Rules Successor IRA Rules

If you are a successor beneficiary:

If the owner on the inherited IRA was subject to the stretch rule, you as the successor beneficiary are now subject to the 10-year rule

If the owner of the Inherited IRA was subject to the 10-year rule, you have whatever time is remaining within that original 10 year window to deplete the account balance.

Whether or not you have to take an RMD in the year they pass and in future years, is more complex, seek help from a professional.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What happens when a beneficiary of an inherited IRA passes away?

When the original beneficiary of an inherited IRA dies, the account passes to a successor beneficiary. The successor inherits both the account and the distribution rules that applied to the original beneficiary, meaning the timing and requirements for withdrawals depend on how the first beneficiary inherited the IRA.

Do successor beneficiaries get a new 10-year window to deplete the inherited IRA?

No. If the original beneficiary was subject to the 10-year rule, the successor beneficiary only has the remaining time left in that original 10-year period to fully deplete the account. The clock does not reset when the account passes to a new beneficiary.

What if the original beneficiary was following the stretch rule?

If the first beneficiary inherited the IRA before 2020 and was allowed to “stretch” distributions over their lifetime, the successor beneficiary must follow the 10-year rule instead. They have a full 10 years from the year after the first beneficiary’s death to empty the account.

How do required minimum distributions (RMDs) work for successor beneficiaries?

If the person you inherited the IRA from was already taking RMDs, you must continue taking them each year and still meet the 10-year depletion rule. Once RMDs have begun on an IRA or inherited IRA, they cannot be stopped.

Do successor beneficiaries need to take the decedent’s final RMD?

Yes. If the previous account holder had not yet taken their full RMD for the year in which they passed away, the successor beneficiary is responsible for distributing that remaining amount before year-end to avoid IRS penalties.

Does it matter if the IRA was Traditional or Roth?

The same successor rules apply to both Traditional and Roth IRAs. The difference is that distributions from inherited Roth IRAs are tax-free if the account has met the five-year rule, while withdrawals from inherited Traditional IRAs are taxed as ordinary income.

What key questions should successor beneficiaries ask?

Successor beneficiaries should confirm:

Was the prior owner under the 10-year rule or stretch rule?

Were they already taking RMDs?

Did they complete their RMD for the year of death?

What was their age at death?

Beneficiaries May Need To Take An RMD From A Decedent’s IRA In The Year They Pass Away

A common mistake that beneficiaries of retirement accounts make when they inherit either a Traditional IRA or 401(k) account is not knowing that if the decedent was required to take an RMD (required minimum distribution) for the year but did not distribute the full amount before they passed, the beneficiaries are then required to withdrawal that amount from the retirement account prior to December 31st of the year they passed away. Not taking the RMDs prior to December 31st could trigger IRS penalties unless an exception applies.

A common mistake that beneficiaries of retirement accounts make when they inherit either a Traditional IRA or 401(k) account is not knowing that if the decedent was required to take an RMD (required minimum distribution) for the year but did not distribute the full amount before they passed, the beneficiaries are then required to withdrawal that amount from the retirement account prior to December 31st of the year they passed away. Not taking the RMDs prior to December 31st could trigger IRS penalties unless an exception applies.

The RMD Requirement for the Decedent

Once you reach a specific age, the IRS requires taxpayers to begin taking mandatory annual distributions from their pre-tax retirement account each year. These mandatory annual distributions are called RMDs or required minimum distributions. The age at which an individual is required to begin taking RMDs is also referred to as the “Required Beginning Date” (RBD). The Required Beginning Date is based on your date of birth:

Born 1950 or earlier: Age 72

Born 1951 – 1959: Age 73

Born 1960 or later: Age 75

Example: If Jim was born in 1953 and turns age 73 this year, and Jim has a Traditional IRA with a $500,000 balance, in 2026, Jim would be required to withdraw $18,867 from his IRA as his annual RMD and pay tax on the distribution.

Undistributed RMD Amount When Someone Passes Away

It’s a common situation for an individual who has reached their Required Beginning Date for RMDs to pass away prior to distributing the required amount from their IRA account for that calendar year.

Example: Jen is age 81; she passed away in February 2026 with a $300,000 balance in her Traditional IRA. Her RMD amount for 2026 would be $15,463. If Jen only distributed $3,000 from her IRA prior to passing away in February, the beneficiary or beneficiaries of Jen’s IRA would be required to withdraw the remaining amount of her RMD, $12,463, prior to December 31, 2026, otherwise the beneficiaries will be faced with a 10% to 25% excise tax on the amount of the RMD that was not withdrawn prior to December 31st.

A Single Beneficiary

If there is only one beneficiary that is inheriting the entire account balance, the process is easy: determine the remaining amount of the decedent’s RMD, and then process the remaining RMD amount from the IRA account prior to December 31st of the year that they passed away.

Multiple Beneficiaries

When there are multiple beneficiaries of a pre-tax retirement account, the IRS recently released new regulations clarifying a question that has been in existence for a very long time.

The question has been, “If there are multiple beneficiaries of a retirement account, does EACH beneficiary need to distribute an equal share of the decedent’s remaining RMD amount OR do they collectively just have to make sure the remaining RMD amount was distributed but it does not have to be in equal shares?”

I’ll show you why this matters in an example:

Susan passed away before taking her $20,000 RMD for the year. She has a $200,000 balance in her Traditional IRA, and her two kids, Scott and Wanda, are both 50% primary beneficiaries on her account. The kids set up separate inherited IRAs and transfer their $100,000 shares into their respective accounts. Scott intends to take a $50,000 distribution from his Inherited IRA, pay the tax, and buy a boat, but Wanda, who is a high-income earner, wants to avoid taking taxable distributions from her Inherited IRA until after she retires.

Since Scott took enough out of his Inherited IRA to cover Susan’s full $20,000 undistributed RMD in the year she passed, is Wanda relieved of having to take an RMD from her account in the year that Susan passed, or does she still need to distribute her $10,000 share of the $20,000 RMD?

The new IRS regulations state that the decedent’s undistributed RMD amount is allowed to be satisfied by “any beneficiary” in the year that they pass away. Meaning the RMD does not have to be distributed in equal amounts to each beneficiary, as long as the total remaining RMD amount is distributed by one or more of the beneficiaries of the decedent.

In the example above, if Scott processed $50,000 from his inherited IRA in the year that Susan passed, Wanda would not be required to take a distribution from her inherited IRA that year because Susan’s $20,000 remaining RMD amount is deemed to be fulfilled.

A Decedent With Multiple IRAs

It’s not uncommon for an individual to have more than one Traditional IRA account when they pass away. The question becomes if they have multiple IRAs and each of those IRAs has an undistributed RMD amount at the time the decedent passes away, can the beneficiaries total up all of the undistributed RMD amounts and take the full amount from one single IRA account OR do they have to take the undistributed RMD amount from each IRA account?

The answer is “it depends”. It depends on whether the beneficiaries are the same or different for each of their IRA accounts.

Multiple IRAs – Same Beneficiaries

If the decedent has multiple IRAs but the beneficiaries are exactly the same as all of their IRAs, then the beneficiaries are allowed to aggregate the undistributed RMD amounts together and distribute that amount from any IRA or IRAs that they choose before the end of the year.

Multiple IRAs – Different Beneficiaries

However, in the instance that the decedent has multiple IRAs but has different beneficiaries listed amongst the different IRA accounts, then the decedent’s undistributed RMD amount needs to be taken from each IRA account.

Privacy Issue with Multiple Beneficiaries

I have been a financial planner long enough to know that not all family members get along after someone passes away. If the decedent had an undistributed RMD amount in the year that they passed and the beneficiaries are not openly sharing their plans regarding how much they plan to withdraw out of their inherited IRA in the year the decedent passed away, it may be impossible to coordinate the disproportionate distributions between the multiple beneficiaries defaulting the beneficiary to taking their equal share of the undistributed RMD amount.

IRS Penalty For Missing RMD

If the beneficiaries fail to distribute the decedent’s remaining RMD amount before December 31st of the year that they pass away, then the IRS will assess a 25% penalty against the amount that was not timely distributed from the IRA account.

Special Note: The IRS penalty is reduced to 10% if corrected in a timely fashion.

Automatic Waiver of the RMD Penalty

The final regulations released by the IRS in 2024 granted a very favorable automatic waiver of the missed RMD penalty that did not exist prior to July 2024. The automatic waiver originally stemmed from the common scenario that if the decedent passed away in December and had not yet satisfied their RMD amount for the year, it was often difficult for the beneficiaries to work with the custodians of the IRA to get those distributions processed prior to December 31st. However, the IRS, being oddly gracious, now provides beneficiaries with an automatic waiver of the missed RMD penalty, specifically for undistributed RMD amounts for a decedent, up until December 31st of the year AFTER the decedent’s death to satisfy the RMD requirement.

When Is No RMD Required?

I have gone through numerous scenarios without stating the obvious. If the decedent either died before their Required Beginning Date for RMDs or if they died AFTER their Required Beginning Date but distributed their full RMD amount prior to passing away, the beneficiaries are not required to distribute anything from the decedent’s IRA prior to December 31st in the year that they passed away.

Also, if the Decedent had a Roth IRA, Roth IRAs do not have an RMD requirement, so the beneficiaries of the Roth IRA would not be required to take an RMD prior to December 31st in the year the decedent passes away.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Last updated June, 2026

Frequently Asked Questions (FAQs):

What happens if someone dies before taking their full RMD for the year?

If a person passes away without taking their full required minimum distribution (RMD), their beneficiaries must withdraw the remaining amount by December 31 of that same year. Failing to do so can result in IRS penalties unless an exception or waiver applies.

How can beneficiaries determine if the decedent had an RMD requirement?

The RMD obligation depends on the decedent’s age and date of birth. The Required Beginning Date (RBD) is age 72 for those born in 1950 or earlier, 73 for those born between 1951 and 1959, and 75 for those born in 1960 or later. If the decedent was past their RBD, the RMD rule applies.

If there are multiple beneficiaries, does each person need to take part of the RMD?

No. The IRS clarified in 2024 that any one or more beneficiaries can collectively satisfy the decedent’s remaining RMD. As long as the total required amount is withdrawn from the inherited accounts before year-end, it doesn’t need to be split evenly among beneficiaries.

How are RMDs handled if the decedent had multiple IRA accounts?

If all IRAs have the same beneficiaries, the total RMD amount can be aggregated and taken from any one or more accounts. However, if the IRAs have different beneficiaries, each account’s undistributed RMD must be withdrawn separately from that account.

What are the penalties for missing a decedent’s RMD?

The IRS can impose a 25% excise tax on any undistributed RMD amount not withdrawn by year-end. If corrected promptly, the penalty may be reduced to 10%.

Did the IRS change the RMD penalty rules recently?

Yes. Under final regulations released in 2024, beneficiaries now have an automatic waiver of the missed RMD penalty if they take the decedent’s remaining RMD by December 31 of the year after the death. This provides flexibility in situations where distributions are delayed.

When are beneficiaries not required to take a decedent’s RMD?

No RMD is required if the decedent passed away before reaching their Required Beginning Date or had already completed their RMD for the year. In addition, Roth IRAs are exempt from RMD requirements, so beneficiaries of Roth accounts do not need to take year-of-death distributions.

The Final Rules For Non-spouse Beneficiary Inherited IRAs Has Been Released: The 10-Year Rule, Annual RMD Requirement, Tax Strategies, New 401(k) Roth Rules, and More…….

In July 2024, the IRS released its long-awaited final regulations clarifying the annual RMD (required minimum distribution) rules for non-spouse beneficiaries of retirement accounts that are subject to the new 10-year rule. But like most IRS regulations, it’s anything but simple and straightforward.

In July 2024, the IRS released its long-awaited final regulations clarifying the annual RMD (required minimum distribution) rules for non-spouse beneficiaries of retirement accounts that are subject to the new 10-year rule. But like most IRS regulations, it’s anything but simple and straightforward. The short answer is for non-spouse beneficiaries that are subject to the 10-year rule; some beneficiaries will be required to begin taking annual RMDs starting in 2025 while others will not. In this article, we will review:

The RMD requirement for non-spouse beneficiaries

RMD start date

IRS penalty relief for missed RMDs

Are one-time distributions required for missed RMDs 2020 - 2024?

Different RMD rules for Traditional IRAs versus Roth IRAs

Different RMD rules for Roth 401(k) versus Roth IRAs

Common RMD mistake for stretch rule beneficiaries

In addition to covering the topics above related to the new RMD rules, we want this article to be a “one-stop shop” for non-spouse beneficiaries to understand how these non-spouse inherited IRAs work from start to finish, so we will start this article by covering:

How Inherited IRA work for non-spouse beneficiaries

Rules for a decedent that pass either before or after 2019

The new 10-year Rule

Beneficiaries that are granted an exception to the new 10-year rule

Required minimum distributions (RMDs)

Taxation of distributions from inherited IRAs

Tax strategies and Pitfalls associated with Inherited IRA accounts

Special rules for minor children with Inherited IRAs

(If you are reading this just for the new RMD rules, you can skip to the second half of the article)

Non-spouse Beneficiaries of Retirement Accounts

When you inherit a retirement account, there are different options available to you depending on whether you are a “spouse beneficiary” or a “non-spouse beneficiary”. In this article, we are going to be focusing on the options available to a non-spouse beneficiary.

Non-spouse Beneficiary Rules Prior to 2020

In 2019, the SECURE Act 1.0 was passed, which greatly limited the inherited IRA options that were available to non-spouse beneficiaries of IRAs, 401(k)’s, and other types of employer-sponsored retirement plans. Under the old rules, if someone passed away prior to January 1, 2020, you as a non-spouse beneficiary, were allowed to move the balance of that IRA into an inherited IRA in your name, avoid any immediate tax implications, and you only had to take small distributions each year called RMDs (required minimum distributions) based on IRS life expectancy table. This was called the “stretch rule” which allowed a non-spouse beneficiary to stretch the distributions over their lifetime.

If you wanted to take more out of the account, you could, since it’s an inherited IRA, even if you were under the age of 59 ½, you avoided the 10% early withdrawal penalty and either had to pay income tax on a pre-tax retirement account or avoided tax altogether on Roth inherited IRA accounts. These beneficiaries had a lot of flexibility with this option with minimal emergency tax planning needed.

For individuals in this camp who inherited a retirement account from someone who passed away prior to January 1, 2020, the good news is you are grandfathered in under the old rules, and none of the changes that we are going to cover in this article apply to you. You still have access to the stretch provision.

Non-spouse Beneficiary of Decedent That Passed After December 31, 2019

SECURE Act 1.0, which passed in 2019, took away the “stretch option” for most non-spouse beneficiaries and replaced it with a much more restrictive “10-Year Rule,” which requires a non-spouse beneficiary to fully deplete the account balance of that inherited retirement account within 10 years start the year after the decedent passed away. If you inherited a retirement account from someone who passed away AFTER December 31, 2019, and you are non-spouse beneficiaries, you are subject to the new 10-Year Rule UNLESS you meet one of the exceptions. Non-spouse beneficiaries that qualify for an exception to the 10-year rule are referred to as “Eligible Designated Beneficiaries” in the new tax regulations if you choose to read the 260 pages that were just released by the IRS.

Here is the list of beneficiaries that are exempt from the new 10-year rule and still have the stretch option available to them:

Surviving spouse

Person less than 10 years younger than the decedent

Minor children

Disabled person

Chronically ill person

Some See-Through Trusts benefitting someone on this exception list

Non-Spouse Beneficiary Not More Than 10 Years Younger Than The Decedent

I wanted to highlight this exception because it’s the most common exception to the 10-rule for non-spouse beneficiaries that we see amongst our clients. If you are a non-spouse beneficiary of a retirement account from someone that was not more than 10 years younger than you like a sibling or a cousin, the new 10-year distribution rule does not apply to you. You are allowed to roll over the balance to your own inherited IRA and stretch annual RMDs over your lifetime.