How Much Should You Have In An Emergency Fund?

Establishing an emergency fund is an important step in achieving financial stability and growth. Not only does it help protect you when big expenses arise or when a spouse loses a job but it also helps keep your other financial goals on track.

Establishing an emergency fund is an important step in achieving financial stability and growth. Not only does it help protect you when big expenses arise or when a spouse loses a job but it also helps keep your other financial goals on track. When we educate clients on emergency funds, the follow questions typically arise:

How much should you have in an emergency fund?

Does the amount vary if you are retired versus still working?

Should your emergency fund be held in a savings account or invested?

When is your emergency fund too large?

How do you coordinate this with your other financial goals?

Emergency Fund Amount

In general, your emergency fund should typically be 4 to 6 months of your total monthly expenses. To calculate this, you will have to complete a monthly budget listing all of your expenses. Here is a link to an excel spreadsheet that we provide to our clients to assist them with this budgeting exercise: GFG Expense Planner.

Big unforeseen expenses come in all shapes and sizes but frequently include:

You or your spouse lose a job

Medical expenses

Unexpected tax bill

Household expenses (storm, flooding, roof, furnace, fire)

Major car expenses

Increase in childcare expenses

Family member has an emergency and needs financial support

Without a cash reserve, surprise financial events like these can set you back a year, 5 years, 10 years, or worse, force you into bankruptcy, require you to move, or to sell your house. Having the discipline to establish an emergency fund will help to insulate you and your family from these unfortunate events.

Cash Is King

We usually advise clients to keep their emergency fund in a savings account that is liquid and readily available. That will usually prompt the question: “But my savings account is earning minimal interest, isn’t it a waste to have that much sitting in cash earning nothing?” The purpose of the emergency fund it to be able write a check on the spot in the event of a financial emergency. If your emergency fund is invested in the stock market and the stock market drops by 20%, it may be an inopportune time to liquidate that investment, or your emergency fund amount may no longer be the adequate amount.

Even though that cash is just sitting in your savings account earning little to no interest, it prevents you from having to go into debt, take a 401(k) loan, or liquidate investments at an inopportune time to meet the unforeseen expense.

Cash Reserve When You Retire

I will receive the question from retirees: “Should your cash reserve be larger once you are retired because you are no longer receiving a paycheck?” In general, my answer is “no”, as long as you have your 4 months of living expenses in cash, that should be sufficient. I will explain why in the next section.

Your Cash Reserve Is Too Large

There is such a thing as having too much cash. Cash can provide financial security but beyond that, holding cash does not provide a lot of financial benefits. If 4 months of your living expenses is $20,000 and you are holding $100,000 in cash in your savings account, whether you are retired or not, that additional $80,000 in cash over and above your emergency fund amount could probably be working harder for you doing something else. There is a long list of options, but it could include:

Paying down debt (including the mortgage)

Making contributions to retirement accounts to lower your income tax liability

Roth conversions

College savings accounts for your kids or grandchildren\

Gifting strategies

Investing the money in an effort to hedge inflation and receive a higher long-term return

Emergency Fund & Other Financial Goals

It’s not uncommon for individuals and families to find it difficult to accumulate 4 months worth of savings when they have so many other bills. If you are living paycheck to paycheck right now and you have debt such as credit cards or student loans, you may first have to focus on a plan for paying down your debt to increase the amount of extra money you have left over to begin working toward your emergency fund goal. If you find yourself in this situation, a great book to read is “The Total Money Makeover” by Dave Ramsey.

The probability of achieving your various financial goals in life increases dramatically once you have an emergency fund in place. If you plan to retire at a certain age, pay for your children to go college, be mortgage and debt free, purchase a second house, whatever the goal may be, large unexpected expenses can either derail those financial goals completely, or set you back years from achieving them.

Remember, life is full of surprises and usually those surprises end up costing you money. Having that emergency fund in place allows you to handle those surprise expenses without causing stress or jeopardizing your financial future.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

How much should you have in an emergency fund?

Most financial experts recommend saving between four and six months’ worth of essential living expenses. To determine your target amount, create a monthly budget of housing, utilities, insurance, food, transportation, and other recurring costs, then multiply that total by the desired number of months.

Should your emergency fund be different if you’re retired?

Not necessarily. A reserve of about four months of living expenses is usually sufficient for retirees, provided that regular income sources such as pensions or Social Security are stable. Holding too much cash in retirement can limit growth opportunities and reduce purchasing power over time.

Where should you keep your emergency fund?

An emergency fund should be kept in a liquid, low-risk account such as a savings or money market account. While the interest rate may be modest, the priority is accessibility and protection from market fluctuations, ensuring the money is available when needed.

Can an emergency fund be too large?

Yes. Once your fund exceeds four to six months of expenses, the extra cash could be more productive elsewhere—such as paying down debt, contributing to retirement accounts, or investing for long-term goals. Cash beyond what you truly need for emergencies often loses value to inflation.

How can you build an emergency fund while managing debt or other goals?

If you’re living paycheck to paycheck or carrying high-interest debt, start small and automate savings to gradually build your fund. Paying off debt first can free up monthly cash flow, making it easier to reach your savings goal without sacrificing progress toward other financial priorities.

Why is an emergency fund important for long-term financial success?

An emergency fund protects you from having to use credit cards, take loans, or sell investments at a loss when unexpected expenses occur. It provides peace of mind and keeps your retirement, education, and other financial goals on track even during difficult times.

What Causes Bonds To Lose Value In Certain Market Environments?

Bonds are often revered as a safe investment compared to stocks but make no mistake, bonds like other investments are not risk-free, and there are certain market environments where they can lose value. As I write this article in May 2022, the Aggregate Bond Index is currently down 8% year to date.

Bonds are often revered as a safe investment compared to stocks but make no mistake, bonds like other investments are not risk-free, and there are certain market environments where they can lose value. As I write this article in May 2022, the Aggregate Bond Index is currently down 8% year to date. While this is definitely a more extreme year for the bond market, there are other years in the past where bonds have lost value.

How do bonds work?

Bonds in their most basic form are essentially loans paid with interest. Companies, government entities, and countries issue bonds to raise money to fund their operations. When you buy a bond you are essentially lending money to these organizations in return for interest payments and potentially appreciation on the value of the bond. Similar to traditional loans, bonds can default, interest can be fixed or variable, and bonds are issued for varying durations. But unlike loans, the value of your original investment can fluctuate over the life of the bond.

Bond example

Before we get into all of the variables associated with bonds, let’s first look at a basic example. The US government is issuing a 10-year treasury bond with a 3% interest rate. You buy $10,000 worth of bonds so essentially you are lending the US government $10,000 for a duration of 10 years and during that 10 years, the US government will pay you 3% interest every single year, then after 10 years, the bond matures, the US government hands you back your $10,000.

Credit worthiness

Similar to someone asking to borrow money from you, all bond issuers are not created equal. You have to assess the credit worthiness of the company or organization that is issuing the bonds to make sure that they are going to be able to make their interest payments and return your principal at the maturity date. “Maturity date” is just bond lingo for when the bond issuer has to repay you the amount that you lent to them. When the US government issues bonds, they are considered by the market to be some of the safest bonds in the world because they are backed by the credit worthiness of the United States government. It would be a historic event if the US government were to default on its debt because the government can always print more money or raise taxes to make the debt payments. Compare this to a risky company, that is trying to emerge from bankruptcy, and is issuing bonds to raise capital to turn the company around. This could be viewed as a much riskier investment because if you lend that company $10,000, you may never see it again if the company is unable to emerge from bankruptcy successfully. For this reason, you have to be selective as to who is issuing you the bond.

Bond rating agencies

Thankfully there are bond rating agencies that help investors assess the credit worthiness of the bond issuer. The two main credit rating agencies are Standard & Poors and Moody’s. Both have grades that they assign to each bond issuer that can range from AAA for the highest quality issuers all the way down to D. It’s important to look at both rating agencies because they may assign different credit scores or in the bond world called “quality ratings” to a bond issuer. But as we learned during the 2008 and 2009 recession, even the bond rating agencies sometimes make the wrong call, so you should complete your own due diligence in assessing the credit worthiness of a particular bond issuer.

Bond defaults

When a company or government agency defaults on its debt it’s ugly. All of the creditors of the company including the bondholders line up to split up whatever’s left, if there is anything left. There could be a number of creditors that have priority over bondholders of a company even though bondholders have priority over stockholders in a company. If you bought a $10,000 bond from a company that goes bankrupt, you have to wait for the bankruptcy process to play out to find out how much, if any, of your original $10,000 investment will be returned to you.

Bond coupon rate

A bond coupon is the interest rate that is paid to the bondholder each year. If a bond has a 5% coupon that means it pays the bondholder 5% in interest each year over the life of that bond. While there are many factors that determine the interest rate of a bond, two of the primary factors are the credit worthiness of the organization issuing the bonds and the bond’s duration.

The credit worthiness of the bond issuer probably has the greatest weight. If a high-risk company is issuing bonds, investors will most likely demand a high coupon rate compared to a more financial stable company to compensate them for the increased level of risk. If a 10 year US government bond is being issued for a 3% coupon rate, a high-risk corporate bond may be issued at a coupon rate of 7% or more. Higher risk bonds are sometimes referred to as high yield bonds or junk bonds. On the flipside, organizations with higher credit ratings, normally have the luxury of issuing their bonds at lower interest rates because the market views them as safer.

The coupon payments, or interest payments, can be made to the bondholder in different durations during the year depending on the terms of the bond. Some bonds issue interest payments quarterly, semi-annually, once a year, and some bonds don’t issue any interest payments until the bonds matures.

It’s because of this fixed interest-rate structure that high quality bonds are often viewed as a safer investment than stocks because the value of a stock varies every day based on what the value of the company is perceived to be. Whereas bonds just make fixed interest payments and then re-pay you the face value of the bond at a future date. “Face value” is bond lingo for the dollar amount the bond was issued for and the amount that is returned to the bondholder at maturity.

Fixed interest versus variable interest

While most bonds are issued with a fixed interest rate, some bonds have a variable interest rate. If it’s a fixed interest rate, the bond pays the holder a set interest payment over the life of the bond. If it’s a variable interest rate, the interest rate paid to the bond holder can vary throughout the life of the bond. Some of the more common types of bonds that have variable interest rates are floating rate bonds. The interest rate that these bonds pay is typically tied to the variable rate associated with a short term bond benchmark like the LIBOR or the fed funds rate. As the interest of those benchmarks moves up and down, so do the corresponding interest rate paid by the bond.

Duration of a bond

The next big factor that influences the interest rate on a bond is the duration of the bond. “Duration” is bond lingo for the length from time between when the bond is first issued and when the bond matures. Typically, the longer the duration of the bond, the higher the interest rate which makes sense. If a company wants to borrow $10,000 from you for 1 year versus 10 years, as the person lending them the money, you will most likely want a higher interest rate for a 10 year loan versus a 1 year loan because they are holding onto your money for a longer period of time which represents a greater risk to you as the bondholder.

Interest rate risk

Bonds also have something called interest rate risk. Typically, when interest rates rise, the value of a bond falls, and vice versa if interest rates fall, the value of a bond rises. Up until this point, we have really just talked about coupon payments or interest payments made to a bondholder but the bond itself can change in value over the life of the bond. Let’s say a company is issuing bonds at $1,000 face value each, you buy a bond for $1,000 and at maturity you would expect to receive $1,000 back, but from the time that bond is issued and when it matures, you can normally trade that bond in the open market, and the value of that bond could sell for more or less than your original $1,000 investment.

If you buy a bond from a company that is a 10 year bond with a 5% interest rate but then interest rates across the economy begin to fall, and a year from now investors have difficulty finding bonds that are being issued with a 5% interest rate, another investor may pay you more than $1,000 to buy your bond and collect the 5% interest payment for the rest of that bonds life. So instead of just receiving $1,000 for the bond you may receive $1,500. The value paid over and above the bonds face value is considered appreciation which adds to your total return so the total return on a bond investment includes both dividends received and any appreciation if you sell it prior to maturity.

But that is a two way street, using that same example above, let’s say a company issues you a bond for $1,000 paying a 5% coupon, but now interest rates have moved higher over the next year, and that same company is now issuing bonds at a 7% interest rate, no one wants your 5% bond because they can get a higher interest-rate by buying the new bonds today. If you were to try and sell your bond in the open market you may only receive $900 from another investor because again, they can just pay $1,000 by purchasing the new bonds with the higher interest rate.

Holding to maturity

If you hold bonds to their maturity, which means you don’t trade them while you’re waiting for the bond to mature, it eliminates a lot of this interest-rate risk because then it’s just a pure loan. You lent a company $1,000, they pay you interest over the life of the loan, and then they hand you back your $1,000 at maturity. Interest rates do not impact the face value of a bond in most cases.

However, when we talk about bond mutual funds, those bond funds can hold hundreds or thousands of bonds, and those mutual funds are priced by “marking to market” each day, meaning they total up all of the value of the bonds in that portfolio as if they were all being sold at 4pm each day. It’s similar with bond ETFs but they trade intraday. Thus, if you own bonds via mutual funds or ETFs, interest-rate fluctuations will have a greater influence on the total return of your bond investment because there’s no option to just hold it to maturity. Depending on the interest rate environment this could either work for you or against you. The reason why many high-quality bond funds have lost value in 2022 is because interest rates have risen rapidly this year which has caused the value of those bonds to fall.

Duration Matters

There is a correlation between the time to maturity and the impact of interest rates on the price of a bond. The longer the duration of the bond, the more that can happen to interest rates between the time a bond is issued and the time the bond matures. For this reason, when interest rates move, it typically has a greater price impact on longer term bonds versus short-term bond.

Simple example, your own a bond paying 4% that is maturing in 1 year and another bond paying 4% that matures in 20 years, interest rates are moving higher, and the equivalent bonds are now being issued at a 5% coupon rate. Both of your bonds would most likely drop in value but the bond that is maturing in one year will most likely drop by less because they will return your investment sooner, and you can reinvest that money at the new higher rate compared to the 20 year bond that is locked in at the lower interest rate for the next 20 years.

Why would you own a bond mutual fund?

After reading this, I’ll have investors ask, “why would you own a bond mutual fund versus individual bonds if you have this interest rate risk?” For most investors, the answer is diversification. If you have $100,000 to allocate to bonds, purchasing a few different bond funds may be a more efficient and cost-effective way to obtain a diversified bond portfolio compared to purchasing individual bonds. As mentioned earlier, these bond mutual funds may have thousands of bonds within this single investment which have been selected by a professional bond manager that understands all of the intricacies of the fixed income markets. Compare this to an individual investor that now has to go out and select each bond, do their own analysis on a variety of different bond issuer‘s to create diversification of credit, duration, and coupon payments to create their own diversified portfolio. Also, since we’ve been in historically low interest rate environments, many fixing income investors have been reluctant to lock into a bond ladder which is a popular strategy for individual bond investors.

Creating a diversified bond portfolio

Similar to stocks, when investing in bonds, it’s important to create a diversified portfolio to help safeguard bondholders against risk. Within a diversified bond portfolio, you may have bonds with varying credit ratings to help achieve a higher level of interest overall with the safer bond issuer‘s offsetting some of the more risky ones that are paying a higher interest rate. You may have bonds that are varying in duration from short-term, intermediate term, all the way to long-term bonds which may also allow a bond investor to achieve higher rates of return over the long term but maintain the necessary amount of liquidity because the short-term bonds are always maturing and are less sensitive to interest rate risks.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

How do bonds work?

Bonds are loans made by investors to governments, corporations, or other entities in exchange for regular interest payments and the return of principal at maturity. The bond’s interest rate, called a “coupon,” is determined by factors such as the issuer’s creditworthiness and the bond’s duration.

Why do bonds lose value when interest rates rise?

When market interest rates increase, newly issued bonds offer higher yields, making older bonds with lower rates less attractive. As a result, the market value of existing bonds typically falls, even though the issuer continues to make the same interest payments.

What is interest rate risk?

Interest rate risk is the potential for bond prices to decrease when interest rates rise. The longer the bond’s duration, the more sensitive it is to interest rate changes, which is why long-term bonds generally experience greater price swings than short-term bonds.

Are government bonds safer than corporate bonds?

Generally, yes. U.S. government bonds are backed by the full faith and credit of the federal government, making them among the safest investments. Corporate bonds, on the other hand, carry varying degrees of risk depending on the company’s financial health and credit rating.

What role do bond rating agencies play?

Agencies like Standard & Poor’s and Moody’s assign credit ratings to bond issuers, helping investors assess default risk. Ratings range from AAA (highest quality) to D (in default). While helpful, investors should still perform their own due diligence.

Why would an investor choose a bond fund instead of individual bonds?

Bond mutual funds and ETFs provide diversification by holding many bonds across different sectors, maturities, and credit qualities. This approach spreads risk and simplifies management, though it also exposes investors to daily price fluctuations and interest rate risk.

What is the difference between fixed and variable rate bonds?

Fixed-rate bonds pay a set interest rate for their entire term, while variable-rate bonds adjust their interest payments periodically based on a benchmark rate, such as the federal funds rate or LIBOR. Variable-rate bonds can help reduce interest rate risk in rising-rate environments.

Additional Disclosure: All bonds are subject to interest rate risk and you may lose money. Before investing in, you should carefully consider and understand the risks associated with investing. U.S. Treasury bonds and municipal bonds maybe susceptible to some of the following risks: Lower yields, interest rate risk, call risk, inflation risk and credit or default risk. Investors need to be aware that bonds may have the risk of default.

Is Inflation Peaking? That’s The Wrong Question…….

While a lot of investors are asking if inflation has peaked, there is a more importnat question they should be asking which will have a bigger impact on our path forward…….

As I write this article on May 11, 2022, the inflation number was just released for April indicating an 8.3% increase in the Consumer Price Index (CPI) which is the primary measure of the inflation rate. The news and market analysts seem to be consumed with the question “has inflation peaked?” Since the April CPI reading was below the March CPI of 8.5%, the answer may very well be “yes”, but I think there is a more important question that analysts and investors should be paying attention to and I would argue that the answer to this question will be more meaningful to the markets. Here it is, looking at all of the drivers of inflation right now, how does the inflation rate get back down to a level that will help the U.S. economy to avoid a recession?

Claiming victory that inflation has peaked could be a very short celebration if the level of inflation REMAINS at an elevated level for longer than the market and the Fed expects.

The Inflation Problem Has Become More Complex

At the end of 2021, it seemed to be the consensus that the primary driver of higher inflation was due to supply chain constraints in a post COVID world. The solution to that problem seemed fairly simple, as the global supply chain heals, there will be more goods to buy, and prices will gradually come down throughout 2022; but that has changed now. It’s not just supply chain issues that are driving inflation any longer, we now have:

Global supply chain issues

Russian / Ukraine conflict

Oil still over $100 per barrel

Tight labor markets

Wage growth

Strong corporate earnings but weaker forecasts

Fed policy

I would also argue that some of the inflation catalysts listed above will have a more significant impact on the rate of inflation than just the COVID supply constraints. In this article I’m going to walk you through the trends that we are seeing in each of these inflation catalysts and how they could impact inflation going forward. We do not believe that the market is doomed to enter a recession at this point but with so many more forces driving inflation higher, monitoring what really matters to the longer term inflation trend should be foremost in the mind of investors as the war against inflation enters the second half of the 2022.

Russia / Ukraine Conflict

Russia’s continued assault on Ukraine has caused a number of supply chain disruptions in itself but none more impactful to the U.S. than the price of oil. The price of oil has been over $100 per barrel for months which is huge driver of inflation since goods need to be transported on planes, ships, trucks, and trains. Oil companies are not in a rush to produce more because they are enjoying lofty profits and they realize that the price of oil could come down quickly if the violence ends in Ukraine. This is why they are hesitant to spend a lot of money to bring more production online because the price of oil could drop down to $80 or below within the next few months. Could oil go higher from here? It could. The Chinese economy has recently been hampered by COVID outbreaks so demand for oil has eased within the last month, but if this changes you could see the price of oil hit new highs on increased demand from China and we are about to enter the summer travel season in the U.S. If oil prices stay above $100 per barrel throughout the summer, it may keep inflation at elevated levels for longer than anticipated.

The Price of Oil

We just went through what’s driving the price of oil higher but if the price of oil drops within the next few months it’s not an automatic victory. If the price of oil is dropping because there is more supply coming online or because there is peace in Ukraine that is excellent, that should reduce inflationary pressures. However, if the price of oil is decreasing because demand is beginning to soften because the consumer is beginning to buy less, that’s not a positive indicator.

More Jobs Than Workers

Currently there are 5.9 million unemployed people in the U.S., and as of March there are 11.5M job openings which puts us at 2 job openings for every 1 person looking for work. If you look at the chart below of the total job openings, it’s easy to see that we are in uncharted territory here:

So, when you have more jobs than people looking for work, what do you think is going to happen to wages? They are going to go up. When you look back in history, one of the largest drivers of big inflationary periods is wage growth. Think about it this way, if the government hands you a stimulus check, you will be able to buy more stuff or pay higher prices for goods and services than you normally would, but this is temporary. Once you have spent that government stimulus money, you can no longer afford to pay higher prices.

If you change jobs, and you receive a $30,000 raise, now you can pay higher prices, not just this year but next year, and the year after that. Wage growth creates “sticky inflation”. It doesn’t just go away when the supply chain recovers or when oil prices retreat. As of April, wage growth has risen 6.4% over the past year, and the last time we saw wage growth over 6% was the 1970’s which not so coincidentally was a period of prolonged hyperinflation.

The only way I can foresee wage growth decreasing is a slow down in the economy which raises the risk of a recession. It’s simple supply and demand. If you have more jobs than people to fill them, companies will have to pay hire wages to attract and keep employees, the companies will most likely pass those higher costs onto the consumer in the form of higher prices, eventually the consumer can no longer afford those higher prices, the economy slows down, and then those excess jobs are eliminated. Not a fun storyline.

Subtle Warning Signs In Corporate Earnings

The tone from the Fed at the beginning of 2022 was that they will be raising rates to slow down inflation, but the economy is strong enough to withstand the rate hikes and we should be able to avoid a recession. The U.S. economy is driven primarily by consumer spending, and the consumer definitely showed up to spend in the first quarter of 2022. However, while many of the companies in the S&P 500 Index exceeded earning expectations, a number of them softened their outlook for the remainder of 2022 due to rising input costs and the impact of higher prices on consumer spending. Knowing that the stock market and bond market are forward looking animals, even though inflation has not taken a huge toll on corporate earnings yet, clouds are beginning to form which investors should pay close attention to.

Tech Stocks Getting Hit

As of May 9th, the S&P 500 Index is down 16% but the Nasdaq is down 26%. When inflation shows up, valuations begin to matter over a company’s growth story because cash becomes king. Here is how I explain it, if inflation is going up at 8% per year, if I ask you if you want me to give you $1 today or $1 a year from now, you would choose $1 today because a year from now, that dollar would have less purchasing power, because inflation is causing the price of everything to go up. It works the same way with stock prices.

The market uses P/E Ratios to determine how expensive stock is which is simply a company’s stock price divided by its earnings per share. If a company’s stock price is $100 and they are expected to earn $100 in profit for each share of stock, the P/E ratio would be 1. But it’s common for stocks to trade at 10, 15, or even 30 times one year of forward earnings. The higher the PE ratio, the more assumed future growth is built into the price of that stock. Some growth companies have very little in terms of net profit because they are spending a lot of money to make their big growth dreams come to life. These growth stocks can sometimes trade at a PE of 50, 100, or higher!!

When inflation hits and investors realize a dollar today is more valuable than a dollar tomorrow, they have to begin to discount those future returns that are built into stock prices. A stock that is trading at 50 times their one year earnings will typically have to drop in price a lot more than a stock that is only trading at 10 times it’s future one year earnings because you have to discount 50 years of earnings instead of 10.

Fed Policy

The last variable in the inflation equation is Fed policy. The Fed has a really tough job right now, reduce inflation without pushing the economy into a recession. When it was just supply chain issues, I think the market had it right by describing it as “the Fed is trying to engineer a soft landing”. With new inflationary forces now entering the equation, I would describe the Feds task as “threading a needle while the needle is moving”.

At the May meeting, the Fed announced, as expected, a 0.50% increase to the Fed funds rate, but during that meeting they also dismissed that a future 0.75% rate hike was on the table. The markets cheered and rose significantly that day hearing that a 0.75% hike was unlikely but then the next day the market lost all of those gains, and continues to add to the losses - worried that the Fed was not raising rates fast enough to keep higher inflation at bay.

It's All About Inflation

While a lot of attention is being given to the Fed and what the Fed might do next, the focus has to come back to not just stopping inflation from going higher but how do they get inflation to decrease fast enough before it derails the consumer. I highlight all of these inflation variables because you could get good news on supply chain improvements and corporate earnings but if oil remains above $100 per barrel and wage growth is still 6%+, it difficult to picture how the year over year change in the inflation rate gets below 4% or 5% before the end of the year.

The consumer is everything. If the consumer has higher wages and the cash reserves to withstand the higher prices while the Fed is working to bring inflation down, it is possible that we could see a rally in the second half of the year. But the long inflation persists, the less likely that relief rally scenario becomes.

This Time It’s Different

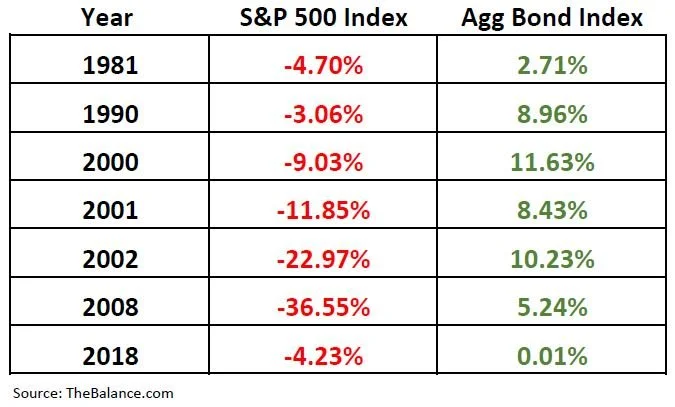

I urge all investors to be careful here. In the investment world you will sometimes hear the phase “this time it’s different” or “we have never been here before” which can add additional stress and anxiety to a market environment that is already scary. I urge caution here because in 2022 there has been a trend that is very different. In most market downturns, when stocks go down, bonds will typically be up, which is one of the benefits of a properly diversified portfolio. When you compare historical returns of the S&P 500 Index versus the Aggregate Bond Index, you will see this pattern:

Unfortunately, as of May 9, 2022, stocks and bonds are both down a significant amount year-to -date:

It feels like we are getting close to a fork in the road. Either we will begin to see meaningful improvement in the inflation rate over the next few months setting both the stock and bond market on a path to recovery in the second half of 2022, or despite the Fed’s best efforts, regardless of whether or not we have seen a peak in inflation, if inflation does not come down a meaningful amount by the fall, the U.S. economy may slip into a mild recession in 2023. Until we know, investors will have to pay very close attention to these monthly indicators that are driving the inflation rate.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What is driving inflation in the U.S. right now?

Inflation remains elevated due to several overlapping factors, including ongoing supply chain disruptions, the Russia–Ukraine conflict, high oil prices, labor shortages, and rising wages. These pressures have made inflation more complex than it was during the early stages of the post-COVID recovery.

Has inflation peaked?

While inflation readings may have eased slightly since their highs, a single month’s data does not confirm a lasting peak. The more important question is how quickly inflation can return to sustainable levels without triggering a recession.

Why does the Russia–Ukraine conflict matter for inflation?

The war has pushed global energy prices higher, particularly oil, which remains above $100 per barrel. Because fuel costs affect nearly all goods and transportation, elevated oil prices can keep inflation high even if other pressures, such as supply chains, improve.

How do wage increases affect inflation?

Strong wage growth creates what economists call “sticky inflation.” When workers earn significantly more, they can afford to pay higher prices for longer, which keeps overall inflation elevated. Wage growth above 6%—as seen recently—makes it harder for inflation to decline quickly.

What role does the Federal Reserve play in controlling inflation?

The Federal Reserve raises or lowers interest rates to influence borrowing, spending, and overall economic activity. In 2022, the Fed began aggressively hiking rates to cool inflation. The challenge is to slow demand enough to lower prices without pushing the economy into recession.

Why are both stocks and bonds down at the same time?

In most downturns, bonds rise when stocks fall, providing diversification. But in 2022, both declined because rising interest rates hurt bond prices while inflation pressures weighed on stock valuations—an unusual combination that made diversification less effective.

Could persistent inflation lead to a recession?

If inflation remains high for too long, it can erode consumer purchasing power and corporate profits, forcing the Fed to tighten policy further. Prolonged inflation without significant progress in lowering prices increases the risk of a mild recession in 2023.

Can You Contribute To An IRA & 401(k) In The Same Year?

There are income limits that can prevent you from taking a tax deduction for contributions to a Traditional IRA if you or your spouse are covered by a 401(k) but even if you can’t deduct the contribution to the IRA, there are tax strategies that you should consider

The answer to this question depends on the following items:

Do you want to contribute to a Roth IRA or Traditional IRA?

What is your income level?

Will the contribution qualify for a tax deduction?

Are you currently eligible to participate in a 401(k) plan?

Is your spouse covered by a 401(k) plan?

If you have the choice, should you contribute to the 401(k) or IRA?

Advanced tax strategy: Maxing out both and spousal IRA contributions

Traditional IRA

Traditional IRA’s are known for their pre-tax benefits. For those that qualify, when you make contributions to the account you receive a tax deduction, the balance accumulates tax deferred, and then you pay tax on the withdrawals in retirement. The IRA contribution limits for 2025 are:

Under Age 50: $7,000

Age 50+: $8,000

However, if you or your spouse are covered by an employer sponsored plan, depending on your level of income, you may or may not be able to take a deduction for the contributions to the Traditional IRA. Here are the phaseout thresholds for 2025:

Note: If both you and your spouse are covered by a 401(k) plan, then use the “You Are Covered” thresholds above.

BELOW THE BOTTOM THRESHOLD: If you are below the thresholds listed above, you will be eligible to fully deduct your Traditional IRA contribution

WITHIN THE PHASEOUT RANGE: If you are within the phaseout range, only a portion of your Traditional IRA contribution will be deductible

ABOVE THE TOP THRESHOLD: If your MAGI (modified adjusted gross income) is above the top of the phaseout threshold, you would not be eligible to take a deduction for your contribution to the Traditional IRA

After-Tax Traditional IRA

If you find that your income prevents you from taking a deduction for all or a portion of your Traditional IRA contribution, you can still make the contribution, but it will be considered an “after-tax” contribution. There are two reasons why we see investors make after-tax contributions to traditional IRA’s. The first is to complete a “Backdoor Roth IRA Contribution”. The second is to leverage the tax deferral accumulation component of a traditional IRA even though a deduction cannot be taken. By holding the investments in an IRA versus in a taxable brokerage account, any dividends or capital gains produced by the activity are sheltered from taxes. The downside is when you withdraw the money from the traditional IRA, all of the gains will be subject to ordinary income tax rates which may be less favorable than long term capital gains rates.

Roth IRA

If you are covered by a 401(K) plan and you want to make a contribution to a Roth IRA, the rules are more straight forward. For Roth IRAs, you make contributions with after-tax dollars but all the accumulation is received tax free as long as the IRA has been in existence for 5 years, and you are over the age of 59½. Unlike the Traditional IRA rules, where there are different income thresholds based on whether you are covered or your spouse is covered by a 401(k), Roth IRA contributions have universal income thresholds.

The contribution limits are the same as Traditional IRA’s but you have to aggregate your IRA contributions meaning you can’t make a $7,000 contribution to a Traditional IRA and then make a $7,000 contribution to a Roth IRA for the same tax year. The IRA annual limits apply to all IRA contributions made in a given tax year.

Should You Contribute To A 401(k) or an IRA?

If you have the option to either contribute to a 401(k) plan or an IRA, which one should you choose? Here are some of the deciding factors:

Employer Match: If the company that you work for offers an employer matching contribution, at a minimum, you should contribute the amount required to receive the full matching contribution, otherwise you are leaving free money on the table.

Roth Contributions: Does your 401(k) plan allow Roth contributions? Depending on your age and tax bracket, it may be advantageous for you to make Roth contributions over pre-tax contributions. If your plan does not allow a Roth option, then it may make sense to contribute pre-tax up the max employer match, and then contribute the rest to a Roth IRA.

Fees: Is there a big difference in fees when comparing your 401(k) account versus an IRA? With 401(k) plans, typically the fees are assessed based on the total assets in the plan. If you have a $20,000 balance in a 401(K) plan that has $10M in plan assets, you may have access to lower cost mutual fund share classes, or lower all-in fees, that may not be available within a IRA.

Investment Options: Most 401(k) plans have a set menu of mutual funds to choose from. If your plan does not provide you with access to a self-directed brokerage window within the 401(k) plan, going the IRA route may offer you more investment flexibility.

Easier Is Better: If after weighing all of these options, it’s a close decision, I usually advise clients that “easier is better”. If you are going to be contributing to your employer’s 401(k) plan, it may be easier to just keep everything in one spot versus trying to successfully manage both a 401(k) and IRA separately.

Maxing Out A 401(k) and IRA

As long as you are eligible from an income standpoint, you are allowed to max out both your employee deferrals in a 401(k) plan and the contributions to your IRA in the same tax year. If you are age 51, married, and your modified AGI is $180,000, you would be able to max your 401(k) employee deferrals at $31,000, you are over the income limit for deducting a contribution to a Traditional IRA, but you would have the option to contribute $8,000 to a Roth IRA.

Advanced Tax Strategy: In the example above, you are above the income threshold to deduct a Traditional IRA but your spouse may not be. If your spouse is not covered by a 401(k) plan, you can make a spousal contribution to a Traditional IRA because the $180,000 is below the income threshold for the spouse that is NOT COVERED by the employer sponsored retirement plan.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

Can you contribute to both a 401(k) and an IRA in the same year?

Yes, as long as you meet the income requirements for IRA eligibility. For example, in 2025 you could contribute the full employee deferral limit to your 401(k) ($23,000 plus $7,500 catch-up if age 50+) and still contribute up to $7,000 or $8,000 to an IRA.

What is a spousal IRA contribution?

If one spouse does not work or isn’t covered by an employer retirement plan, the working spouse can make an IRA contribution on their behalf. This strategy allows a couple to potentially double their retirement savings and may preserve tax deductibility for the non-covered spouse.

Kiddie Tax & Other Pitfalls When Gifting Assets To Your Kids

Before you gift assets to your children make sure you fully understand the Kiddie Tax rule and other pitfalls associated with making gift to your children……….

There are a number of reasons why parents gift assets to their kids which include:

Reduce tax liability

Protecting assets from the nursing home

Estate planning: Avoiding probate

But the pitfalls are many and most people do not find out about the pitfalls until it’s too late. These pitfalls include:

Kiddie tax rules

Children with self-directed investment accounts

Treatment of long-term capital gains

Gifting cost basis rules

College financial aid impact

Control of the assets

5 Year look-back rule

Divorce

Lawsuits

Distributions from Inherited IRA’s

Kiddie Tax

The strategy of shifting assets from a parent to a child on the surface seems like a clever tax strategy in an effort to shift investment income or capitals gains from the parent that may be in a high tax bracket to their child that is in a low tax backet. Unfortunately, the IRS is aware of this strategy, and they have been aware of it since 1986, which is the year the “Kiddie Tax” was signed into law.

Here is how the Kiddie tax works; if your child’s income is over a certain amount, then the income is taxed NOT at the child’s tax rate, but at the PARENT’S tax rate. Kiddie tax rules do NOT apply to earned income which includes wages, salary, tips, or income from self-employment. Kiddie tax ONLY applies to UNEARNED INCOME which includes:

Taxable interest

Dividends

Capital gains

Taxable Scholarships

Income produced by gifts from grandparents

Income produced by UTMA or UGMA accounts

IRA distributions

There are some exceptions to the rule but in general, your child would be subject to the Kiddie tax if they are:

Under the age of 19; or

Between the ages of 19 and 23, and a full-time student

The only exceptions that apply are if your child:

Has earned income totaling more than half the cost of their support; or

Your child files their tax return as married filing joint

Kiddie Tax Calculation

Here is how the Kiddie tax calculation works. For 2025, the first $1,350 of a child’s unearned income is tax-free, the next $1,350 is taxed at the child’s rate, and any unearned income above $2,700 is taxed at the parent’s marginal income tax rate.

Here is an example, the parents bought Apple stock a long time ago and the stock now has a $30,000 unrealized long term capital gain. Assuming the parents make $200,000 per year in income, if they sell the stock, they will have to pay the Federal 15% long term capital gains tax on the $30,000 gain. But they have a child that is age 16 with no income, so they gift the stock to them, have them sell it, with the hopes of the child capturing the 0% long term cap gains rate since they have no income. Kiddie tax is triggered!! The first $2,700 would be tax free but the rest would be taxed at the parent’s federal 15% long term cap gain rate; oh and if that family was expecting to receive college financial aid two years from now, they might have just made a grave mistake because now that teenager is showing income. A topic for later.

That was an example using long term capital gains rates but if we used a source of unearned income subject to ordinary income tax rates, the jump could go from an assumed 0% to the parents 37% tax rate if they are in the highest fed bracket.

Putting Your Kids on Payroll

While we are on the subject of Kiddie Tax, our clients that own small businesses will sometimes ask “Do I have to worry about the Kiddie tax if I put my kids on payroll through my company?” Fortunately the answer is “No”. Paying your child W2 wages through your company is considered “earned income” and earned income is not subject to the kiddie tax rules.

Children with Self-Directed Investment Accounts

It’s becoming more common for high school and college students to have their own brokerage accounts where they are trading stocks, ETFs, options, cryptocurrency, and mutual funds. But the kiddie rules can come into play when they are buying and selling investments in their accounts. If the parents claim the child as a dependent on their tax return and they buy and then sell an investment within a 12 month period, that would create a short term gain subject to ordinary income tax rates. If that gain is above $2,700, then the kiddie tax is triggered, and the gain would be taxed at the parent’s tax rate not the child’s tax rate. This can lead to tax surprises when the child receives the tax forms from the brokerage platform and then realizes there are big taxes due, and the child may or may not have the money to pay it.

For the child to file their own tax return to avoid this Kiddie tax situation, the child must be earning enough income to provide at least half of their financial support.

Kiddie Tax Form 8615

How do you report the Kiddie tax on your tax return? I spoke with a few CPA’s about this and they normally advise their clients that once the child has unearned income over $2,700, the child, even though they may be a dependent on your tax return, files their own tax return, and with their tax return they file Form 8615 which calculates the Kiddie Tax liability based on their parent’s tax rate.

Impact on College Financial Aid

Before gifting any assets to your child, income producing or not, if you are expecting to receive any form of need based financial aid for your child for college in the future, be very very careful. The FAFSA calculation weighs assets and income differently depending on whether it belongs to the parent or the child.

For assets, if the parent owns it, the balance counts 5.64% against the aid awarded. If the child owns it, the balance counts 20% against the aid awarded. You move a stock into your child’s name that is worth $30,000, if you would have qualified for financial aid, you just cost yourself $4,300 PER YEAR in financial aid.

Income is worse. If you gift your child an asset that produces income or capital gains, income of the parents counts 22% - 47% against college financial aid depending on the size of the household. If the income belongs to the child, it counts 50% against the FAFSA award. Another note, the FAFSA process looks back 2 years for purposes of determining the financial aid award, so even though they may only be a sophomore or junior in high school, you don’t find out about that mistake until 2 years later when they are applying for FAFSA as a freshman in college.

Long Term Capital Gains Treatment

The example that I used earlier with the Apple stock highlights another useful tax lesson. If you are selling a stock, mutual fund, or investment property that you have owned for more than a year, it’s taxed at the preferential long term capital gain rate of 15% as long as your taxable income does not exceed $533,400 for single filers or $600,050 for married filing joint in 2025, it’s a flat 15% tax rate whether it’s a $20,000 gain or a $200,000 gain because the rate does not increase like it does for “earned income”. I make this point because long term capital gain rates are already taxed at a relatively low rate, and if realized by your child, are subject to Kiddie tax so before you jump through all the hoops of making the gift, make sure the tax strategy is going to work.

Gift Cost Basis Rules

When you make a gift, it’s important to understand how the cost basis rules work. When you make a gift, there typically is not an immediate tax event, but the recipient inherits your cost basis in that asset. Gifting an asset does not provide the person making the gift with a tax deduction or erase the unrealized gains, unless of course you are gifting it to a charity or not-for-profit. Let’s keep running with that Apple stock example, you gift the Apple stock to your child with a $30,000 unrealized gain, there is no tax event when the gift is made, but if the child sells the stock the next day, they will have to pay tax on the $30,000 realized gain, and if the kiddie tax applies, it will be taxed at the parent’s tax rate.

Estate Tax Planning: Avoid Probate

Sometimes people will gift assets to their kids in an effort to remove those assets from their estate to avoid probate, a big tax issue surfaces with this strategy. Normally when someone passes away and their kids inherit a house or investments, they receive a “step-up in basis”. A step-up in basis means no matter what the gain was in the house or investment prior to a person passing away, the cost basis to the person that inherits the assets is now the fair market value of that asset as of decedent’s date of death.

Example: You bought your house 20 years ago for $200,000 and it’s now worth $400,000. If you were to pass away tomorrow and your kids inherit your house, they receive a step-up in basis to $400,000 so if they sell the house the next day, they have no tax liability. A huge tax benefit.

But if you gift the house to your kids while you are still alive in an effort to avoid the probate process, your kids now lose the step-up in cost basis because the house never passes through your estate. If you kids sell your house the next day, they will realize a $200,000 gain and have to pay tax on it which at the Federal level of 15%, could cost them $30,000 in taxes which could have been avoided.

There are other ways to avoid probate besides gifting that asset to your kids which allows the asset to avoid the probate process and receive a step up in basis. You could setup a trust to own the asset or change the registration on the account to a “transfer on death” account.

Distributions From An IRA Owned By The Child

If your child inherits an IRA, they may be required to take RMD’s (required minimum distributions) each year from the IRA. Distribution are not only subject to ordinary income tax but they are also subject to Kiddie tax since IRA distributions are considered unearned income. If you child inherits a pre-tax IRA or 401(k) be very careful when taking distribution from the account, especially taking into consideration the new distribution rules for non-spouse beneficiaries.

Control of the Asset

As financial planners, we have seen a lot of crazy things happen. While some teenagers are very responsible, others are not. When you gift an asset directly to child, they may not use that gift as intended. Even with UTMA and UGMA account, the parents only have control until the child reaches age of majority, and then account belongs to them. If there is any concern about how the gifted asset will be managed or distributed, you may want to consider a trust or another type of account that provides the you with more control of the asset.

Lawsuits

From a liability standpoint, if you gift assets to your child, and those assets have a meaningful amount of value, those assets could be exposed to a lawsuit if your child were to ever be sued.

Divorce

If you gift assets to your child and they are already married or get married in the future, depending on what state they live in or how those assets are titled, they could be considered marital property. If a divorce happens at some point in the future, their soon to be ex-spouse could now be entitled to a portion of those gifted assets.

5 Year Lookback Rule

Some parents will gift assets to their children to avoid the spend down process should a long term care event happen at some point in the future and they need to go into a nursing home. Different states have different Medicaid rules but in New York, the gift has to take place 5 years prior to the Medicaid application otherwise the assets are subject to spend down.

The other pitfall of gifting assets to your children is that while you may be able to successfully protect those assets from a Medicaid lookback period, the cost basis issue that we discussed earlier still exists. If you gift the house to your kids, they inherit your cost basis, so when they go to sell the house after you pass, they have to pay tax on the full gain amount, versus if you established a grantor irrevocable trust to own your house, it could satisfy the gift for the 5 year look back period in NY, but then your kids receive a step up in basis when you pass away since the house passes through your estate, and they can sell the house with no tax liability.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What are common reasons parents gift assets to their children?

Parents often gift assets to reduce future tax liabilities, protect assets from potential nursing home costs, or simplify estate transfers by avoiding probate. While these goals can be achieved, gifting assets can also create unintended tax and legal consequences if not properly structured.

What is the Kiddie Tax and when does it apply?

The Kiddie Tax applies to a child’s unearned income—such as dividends, interest, or capital gains—above $2,700 (in 2025). Any income over that amount is taxed at the parents’ marginal tax rate instead of the child’s lower rate. It generally applies to dependents under age 19, or under 24 if they are full-time students.

How does gifting affect college financial aid?

Assets and income in a child’s name significantly reduce eligibility for need-based aid. Parental assets count about 5.6% against aid eligibility, while a child’s assets count 20%. Additionally, a child’s income can count as high as 50% against financial aid calculations for two years following the income year.

What are the tax implications of gifting appreciated assets?

When you gift an asset like stock or real estate, your cost basis carries over to the recipient. If the recipient sells the asset, they owe tax on the gain from your original purchase price. This means gifting appreciated assets can shift, but not eliminate, future tax liability.

How does gifting differ from inheritance when it comes to taxes?

Inherited assets generally receive a “step-up in basis” to their fair market value on the date of the decedent’s death, eliminating unrealized capital gains. Gifting assets during your lifetime forfeits this step-up, potentially leaving your heirs with larger future tax bills if they sell the asset.

Can gifting affect Medicaid eligibility or nursing home planning?

Yes. Medicaid’s five-year lookback rule allows the state to review gifts made within five years before a long-term care application. Assets transferred during that period may still be counted toward Medicaid eligibility, delaying benefits and forcing asset spend-down.

What are the risks of gifting assets directly to children?

Once assets are gifted, they legally belong to the child. This means they could be lost in a lawsuit, subject to division in a divorce, or spent irresponsibly. Parents concerned about control or protection may prefer using trusts or transfer-on-death designations instead of outright gifts.

Selecting The Best Pension Payout Option

When you retire and turn on your pension, you typically have to make a decision as to how you would like to receive your benefits which includes making a decision about the survivor benefits. Do you select….

When you retire and turn on your pension, you typically have to make a decision as to how you would like to receive your benefits which includes making a decision about the survivor benefits. Do you select….

Lump sum

Single Life Benefit

100% Survivor Benefit

50% Survivor Benefit

Survivor Benefit Plus Pop-up Election

The right option varies person by person but some of the primary considerations are:

Marital status

Your age

Your spouse’s age

Income needed in retirement

Retirement assets that you have outside of the pension

Health considerations

Life expectancy

Financial stability of the company sponsoring the plan

Tax Strategy

Risk Tolerance

There are a lot of factors because the decision is not an easy one. In this article, I’m going to walk you through how we evaluate these options for our clients so you can make an educated decision when selecting your pension payout option.

Understanding The Options

To give you a better understanding of the various payout options, I’m going to walk you through how each type of benefit works. Not all pension plans are the same, some plans may only offer some of these options, others after all of these options, and some plans have additional payout options available.

Lump Sum: Some pension plans will give you the option of receiving a lump sum dollar amount instead of receiving monthly payment for the rest of your life. Retirees will typically rollover these lump sum amounts into their IRA’s, which is a non-taxable event, and then take distributions as needed from their IRA.

Single Life Benefit: This is also referred to as the “straight life benefit”. This option usually offers the highest monthly pension payments because there are no survivor benefits attached to it. You receive a monthly payment for the rest of your life but when you pass away, all pension payments stop.

Survivor Benefits: There are usually multiple survivor benefit payout options. They are typically listed as:

100% Survivor Benefit

75% Survivor Benefit

50% Survivor Benefit

25% Survivor Benefit

The percentages represent the amount of the benefit that will continue to your spouse should you pass away first. The higher the survivor benefit, typically the lower your monthly pension payment will be because the pension plans realize they may have to make payments for longer because it’s based on two lives instead of one.

Example: If the Single Life pension payment is $3,000, if instead you elect a 50% survivor benefit, your pension payment may only be $2,800, but if you elect the 100% survivor benefit it may only be $2,700. The monthly pension payments go down as the survivor benefits go up.

Here is an example of the survivor benefit, let’s say you elect the $2,800 pension payment with a 50% survivor benefit. Your pension will pay you $2,800 per month when you retire but if you were to pass away, the pension plan will continue to pay your spouse $1,400 per month (50% of the benefit) for the rest of their life.

Pop-Up Elections: Some pension plans, like the New York State Pension Plan, provide retirees with a “Pop-Up Election”. With the pop-up, if you select a survivor benefit which provides you with a lower monthly pension payment amount but your spouse passes away first, thus eliminating the need for a survivor benefit, your monthly pension payment “pops-up” to the amount that you would have received if you elected the Single Life Benefit.

Example: You are married, getting ready to retire, and you have the following pension payout options:

Single Life: $3,000 per month

50% Survivor Benefit: $2,800 per month

50% Survivor Benefit with Pop-Up: $2,700 per month

If you elect the Single Life option, you would receive $3,000 per month, but when you pass away the pension payments stop.

If you elect the 50% Survivor Benefit, you would receive $2,800 per month, but if you pass away before your spouse, they will continue to receive $1,400 for the rest of their life.

If you elect the 50% Survivor Benefit WITH the Pop-Up, you would receive $2,700 per month, if you were to pass away before your spouse, your spouse would continue to receive $1,350 per month. But if your spouse passes away before you, your pension payment pops-up to the $3,000 Single Life amount for the rest of your life.

Why do people select the pop-up? It’s more related to what happens to the social security benefits when a spouse passes away. If your spouse were to pass away, one of the social security benefits is going to stop, and you receive the higher of the two but some of that lost social security income could be made up by the higher pop-up pension amount.

Marital Status

The easiest variable to address is marital status. If you are not married or there are no domestic partners that depend on your pension payments to meet their expenses, then typically it makes sense to elect either the Lump Sum or Straight Life payment option. Whether or not the lump sum or straight life benefit makes sense will depend on your age, tax strategy, income need, if you want to preserve assets for your children, and other factors.

Income Need

If you are married or have someone that depends on your pension income, by far, the number one factors becomes your income need in retirement when making your pension election. If the primary source of your retirement income is your pension and you were to pass away, your spouse would need to continue to receive all or a portion of those pension payments to meet their expenses, you have to weigh very heavily the survivor benefit options. We have seen people make the mistake of electing the Single Life Option because it was the highest monthly payout and then the spouse with the pension unexpectedly passes away at an earlier age. It’s a devastating financial event for the surviving spouse because the pension payments just stop. If someone were to pass away 5 years after leaving their company, they worked all of those year to receive 5 years worth of pension payments, and then they just stopped.

We usually have to run projections for clients to answer this question, if the spouse with the pension passes away will their surviving spouse need 50%, 75%, or 100% of the pension payments to meet their income needs? In most cases it’s worth accepting a slightly lower monthly pension payment to reduce this survivor risk.

Retirement Assets Outside Of The Pension

If you have substantial retirement savings outside of your pension like 401(k) accounts, investment accounts, 457, IRA’s, 403(b) plans, this may give you more flexibility with your pension options. Having those outside assets almost creates a survivor benefit for your spouse that if the pension payments were to stop or be reduced, there are other retirement assets to draw from to meet their income needs.

Example: You have a retired couple, both have pensions, and they have also accumulated $1M in retirement accounts outside the pension, if one spouse were to pass away, even though the pension payments may stop or be reduced, there may be enough assets to draw from the outside retirement accounts to make up for that lost pension income. This may allow a couple to elect a 50% survivor benefit and receive a higher monthly pension payment compared to electing the 100% survivor benefit with the lower monthly pension payment.

Risk Management

This last example usually leads us into another discussion about long-term risk. Even though you may have the outside assets to accept a higher monthly pension payment with a lower survivor benefit, should you? When we create retirement plans for clients we have to make a lot of assumptions about assumed rates of return, life expectancy, expenses, etc. But what if your investment accounts take a big hit during the next recession or a spouse passes away much sooner than expected, accepting a lower survivor benefit may increase the impact of those risks on your plan. If you and your spouse are both able to elect the 100% survivor benefit on your pensions, you then know, that no matter what happens in the future, that pension income will always be there, so it’s one less variable in your long-term financial plan.

While this could be looked at as a less risky path, there is also the flip side to that. If you lock up the 100% survivor benefit on the pension, that may allow you to take more risk in your outside retirement accounts, because you are not as dependent on those accounts to supplement a survivor benefit depending on which spouse passes away first.

Age

The age of you and your spouse can also be a factor. If the spouse with the pension is quite a bit older than the spouse without pension, it may make sense for normal life expectancy reasons, to elect a larger survivor benefit. Visa versa, if the spouse with then pension is much younger, it may warrant a lower survivor benefit elect. But in the end, it all goes full circle back to the income need if the pension payments were to stop, are there enough other assets to supplement income for the surviving spouse?

Health Considerations / Life Expectancy

When conducting a pension analysis, we will typically use age 90 as a life expectancy for most clients. But there are factors that can alter the use of age 90 such as special health considerations and longevity. If the spouse that has the pension is forced to retire for health reasons, it gives greater weight to electing a pension benefit with a higher survivor benefit. When a client tells us that their father, mother, and grandmother, all lived past age 93, that can impact the pension decision. Since people are living longer, it increases the risk of spending through their traditional retirement savings, whereas the pension payments will be there for as long as they live.

Financial Stability Of The Company / Organization

You are seeing more and more stories about workers that were promised a pension but then their company, union, or not-for-profit goes bankrupt. This is a real risk that should factor into your pension decision. While there are government agencies like the PBGC that are there to help backstop these failed pension plans, there have been so many bankrupt pensions over the past two decades that the PBGC fund itself is at risk of running out of assets. If a retiree is worried about the financial solvency of their employer, it may give greater weight to electing the “Lump Sum Option”, taking your money out of the plan, getting it over to your IRA, and then taking monthly payments from the IRA. Since this is becoming a greater risk to employees, we created a video dedicated to this topic: What Happens To Your Pension If The Company Goes Bankrupt?

Tax Strategy

Tax strategy also comes into play when electing your pension benefit. If we have retirees that have both a pension and retirement accounts outside the pension plan, we have to map out the distribution / tax strategy for the next 10 to 20 years. Depending on who you worked for and what state you live in, the monthly pension payments may be taxed at the federal level, state level, or both. Also, many retirees don’t realize that social security will also be considered taxable income in retirement. Then, if you have pre-tax retirement accounts, at age 72, you have to begin taking Required Minimum Distributions which are taxable.

There are situations where we will have a retiree forego the monthly pension payment from the pension plan and elect the Lump Sum Benefit option, so they can rollover the full balance to an IRA, and then we have more flexibility as to what their taxable income will be each year to execute a long term tax strategy that can save them thousands and thousands of dollars in taxes over their lifetime. We may have them process Roth conversions, or realize long term capital gains at a 0% tax rate, neither of which may be available if the pension income is pushing them up into the higher tax brackets.

There are so many other tax strategies, long term care strategies, and wealth accumulation strategies that come into the mix when deciding whether to take the monthly pension payments or the lump sum payment of your pension benefit.

Pension Option Analysis

These pension decisions are very important because you only get one shot at them. Once the decision is made you are not allowed to go back and change your mind to a different option. We run this pension analysis for clients all of the time, so before you make the decision, feel free to reach out to us and we can help you to determine which pension benefit is the right one for you.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What are the main pension payout options available at retirement?

Most pension plans offer several payout choices, including a lump sum, single life benefit, and various survivor benefit options such as 50%, 75%, or 100% survivor benefits. Some plans also include a pop-up feature, which increases your payment to the single life amount if your spouse passes away first.

How does the lump sum option work?

The lump sum option provides a one-time payout that retirees often roll over into an IRA to avoid immediate taxes. This choice offers more flexibility and control over investments but transfers market and longevity risk to the retiree.

What is the difference between single life and survivor benefit options?

A single life pension pays the highest monthly amount but ends when the retiree dies. A survivor benefit option pays a reduced monthly amount during the retiree’s life, but continues payments—often 50%, 75%, or 100%—to the surviving spouse after death.

What is a pop-up survivor benefit?

A pop-up election reduces your monthly pension slightly compared to a standard survivor benefit but increases (“pops up”) your payment to the full single life amount if your spouse passes away first. This feature can help offset lost Social Security income when one spouse dies.

How does marital status influence your pension decision?

Married retirees or those with financial dependents often need to prioritize survivor benefits to ensure continued income for a spouse. Single retirees, by contrast, may benefit more from the lump sum or single life option since there are no survivor needs to plan for.

How do other retirement assets impact pension elections?

If you have substantial savings in 401(k)s, IRAs, or investment accounts, you may be able to take on more risk with your pension option by selecting a smaller survivor benefit or a lump sum. These outside assets can act as a backup income source for your spouse or emergencies.

What role does health and life expectancy play in choosing a pension option?

Shorter expected life spans or significant health issues may make a lump sum or 100% survivor benefit more appealing.

How does company stability affect pension decisions?

If the employer’s financial health or pension funding is uncertain, a lump sum rollover may provide greater security. While the PBGC insures many pensions, its coverage limits may not fully protect large benefits if a plan fails.

Can taxes influence which pension option you choose?

Yes. Pension income is generally taxable at both federal and state levels. Rolling a lump sum into an IRA provides more control over withdrawals and potential tax strategies, such as Roth conversions or managing tax brackets in retirement.

Russia & Ukraine: Where Does The Stock Market Go From Here?

Russia’s invasion of Ukraine continues to add uncertainty to global markets. It’s left investors asking the following questions:

Russia’s invasion of Ukraine continues to add uncertainty to global markets. It’s left investors asking the following questions:

What is the most likely outcome of the invasion?

How will this impact the U.S. stock market and global economy?

How high will oil prices go?

Should the U.S. be worried about a Russia cyberattack?

What is China’s role in this conflict?