2026 Retirement Planning: 7 Smart Purchases to Make Before You Stop Working

Retirement isn’t just about saving—it’s about spending wisely. From medical care and home repairs to travel and vehicles, this guide shows 7 smart purchases to consider before leaving the workforce, with tax and planning tips to help you retire stress-free.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Most retirees spend decades saving and investing, only to face one of the hardest transitions at the finish line: shifting from saver to spender. At Greenbush Financial Group, we often hear clients say they wish they had spent more strategically before retiring—not less. By making key purchases while you still have earned income, you can reduce stress, avoid costly surprises, and give yourself permission to fully enjoy retirement.

This article covers seven smart spending decisions to consider before leaving the workforce, along with the tax and planning angles that can make them even more effective.

Medical and Dental Work Before Medicare

Healthcare costs can spike in retirement, and Medicare doesn’t cover everything—especially dental, vision, and hearing. It’s often wise to complete major procedures while you’re still working.

Max out your Health Savings Account (HSA) during your last high-income years. HSAs offer triple tax benefits—deductible contributions, tax-deferred growth, and tax-free withdrawals for qualified expenses.

If modifications such as no-threshold showers or grab bars are medically necessary, some may qualify as itemized deductions. Proper documentation is essential.

Map out coverage if you retire before age 65. Compare COBRA, ACA marketplace options, and potential premium tax credits.

Secure Your Next Home While Still Employed

Qualifying for a mortgage is often easier with W-2 income than retirement income. Buying or refinancing before you retire can lock in more favorable terms.

Downsizing? Remember the §121 home sale exclusion allows couples filing jointly to exclude up to $500,000 of capital gain on the sale of a primary residence ($250,000 if single).

Considering upgrades? Look into energy-efficiency credits under the Inflation Reduction Act. For example, the Energy Efficient Home Improvement Credit (25C) can provide annual tax credits for qualifying improvements.

Complete Major Home Repairs and Aging-in-Place Upgrades

Addressing big-ticket items before retirement reduces future cash flow stress. Common examples include:

Roof, HVAC system, windows, and insulation

Whole-home surge protection or backup power systems

No-threshold showers, wider doorways, higher-seat toilets

Tackling these projects upfront means fewer disruptions—and potentially fewer withdrawals during a market downturn.

Buy a Reliable, Paid-Off Vehicle

Transportation is a non-negotiable retirement expense. Purchasing a reliable, low-maintenance car before retiring allows you to enter retirement debt-free.

Evaluate new vs. certified pre-owned (CPO) for warranty protection.

For those considering EVs or hybrids, federal and state incentives can significantly reduce net cost.

Budget for a replacement cadence of 7–10 years to spread costs evenly across retirement.

Prepay for Bucket-List Travel

The early years of retirement are often called the “go-go years.” Booking major trips while you’re healthy—and locking in refundable deposits or travel insurance—helps ensure you actually take them.

Build a “first 1,000 days of retirement” calendar to schedule must-do experiences.

Consider paying now while your income supports larger expenses. This reduces pressure on retirement withdrawals later.

Use High-Income Years to Fund Future Spending

Your final working years often come with peak income. This creates opportunities to front-load retirement readiness:

Roth conversions up to the top of your target bracket before Medicare enrollment can reduce future taxable income.

Watch for IRMAA (income-related monthly adjustment amounts) at ages 63–65, which can increase Medicare premiums if income is too high.

Consider donor-advised fund (DAF) contributions to pre-fund charitable giving while reducing taxable income.

Don’t Forget Estate and Administrative Prep

Beyond purchases, pre-retirees benefit from a final sweep of administrative tasks:

Separate credit cards for spouses to maintain access to credit.

Pre-need funeral planning or irrevocable funeral trusts to relieve future burdens.

Refresh wills, POA, health care proxies, and beneficiary designations.

Audit recurring subscriptions, timeshares, and other lifestyle costs.

Key Takeaway

Retirement is about more than accumulating assets—it’s about spending them wisely. By completing health care, housing, car, and travel purchases while still earning, you free up your retirement income for flexibility and enjoyment. At Greenbush Financial Group, we help clients not only save smart but also spend smart.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

What major expenses should I plan to cover before retiring?

Common pre-retirement purchases include completing medical or dental procedures, making home repairs or accessibility upgrades, and replacing your vehicle. Addressing these while you still have earned income helps reduce financial stress once you retire and may provide additional tax benefits.

Why should I complete medical and dental work before enrolling in Medicare?

Medicare generally doesn’t cover dental, vision, or hearing care. Completing major procedures before retirement—while you still have employer coverage—can save money and simplify your transition. It’s also smart to fully fund your Health Savings Account (HSA) in your final working years for future tax-free healthcare spending.

Is it better to buy or refinance a home before retiring?

Yes, qualifying for a mortgage is typically easier when you have active W-2 income. Buying, refinancing, or downsizing before retirement can secure better terms. Couples selling their primary residence may also exclude up to $500,000 in capital gains, and certain energy-efficient home upgrades may qualify for tax credits.

Why should I replace my car before retirement?

Buying a dependable, low-maintenance car before you retire allows you to enter retirement debt-free and avoid large future withdrawals.

How can I use my final high-income years to improve my retirement outlook?

Peak earning years are ideal for strategic financial moves like Roth conversions, funding a donor-advised fund (DAF), or prepaying for future travel. These steps can help lower future taxable income, manage Medicare premiums, and enhance your flexibility in retirement.

What estate and administrative steps should I complete before retiring?

Review and update your will, powers of attorney, and beneficiary designations. Consider establishing separate credit accounts for each spouse, planning funeral arrangements in advance, and canceling unnecessary subscriptions or timeshares to streamline post-retirement finances.

How do pre-retirement purchases support a more enjoyable retirement?

Spending strategically before you stop working lets you handle big expenses with current income, freeing future cash flow for experiences and lifestyle choices. At Greenbush Financial Group, we encourage clients to view retirement not just as saving wisely—but spending wisely, too.

How to Protect Yourself from Stock Market Crashes in Retirement

Market downturns feel different in retirement than during your working years. Learn strategies to protect your nest egg, avoid irreversible mistakes, and balance growth with safety to keep your retirement plan on track.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

The stock market has always gone through ups and downs, but when you’re retired, a downturn can feel much scarier than when you were working. Retirement alters the way you interact with your investments, and the strategies you use to protect yourself from market volatility must also adapt accordingly.

In this article, we’ll cover:

The difference between the accumulation years and distribution years

Why market downturns can be so damaging in retirement

The “irreversible mistake” retirees need to avoid

The risk of holding concentrated positions in retirement

Why being too conservative in retirement can also create problems

Accumulation vs. Distribution Years

One of the most important distinctions in retirement planning is understanding how your relationship with your portfolio changes once you leave the workforce.

Accumulation Years (Working Years):

During your career, you’re regularly contributing to retirement accounts. When the market drops, it can actually work in your favor because you’re buying shares “on sale.” Plus, you’re not taking withdrawals, so your full account balance is still in the market to participate in the rebound when it eventually happens.Distribution Years (Retirement Years):

Once retired, the dynamic shifts. Instead of contributing, you’re taking money out to fund your lifestyle. When a market downturn hits, withdrawals can force you to sell at the worst possible time—locking in losses. Unlike in your working years, your portfolio might not fully recover because the assets you sold are no longer invested when the market rebounds.

This difference makes retirees more vulnerable to something called sequence of returns risk, which is the risk of experiencing poor market returns early in retirement while simultaneously taking withdrawals.

The Irreversible Mistake

We call this the irreversible mistake—waiting too long to reduce your allocation to stocks and riskier asset classes post-retirement. Once those dollars are gone, there’s no “do-over button” to replace them, and trying to recoup the losses by staying overly aggressive can be too much of a gamble.

So, what’s the solution? It depends on:

The size of your retirement accounts

The percentage of income you need to withdraw each year

The purpose assigned to each investment account

For example, you might have a Roth IRA that you plan to leave untouched. Since you don’t need it for income, that account could stay invested more aggressively throughout retirement. On the other hand, accounts you draw from regularly may require a more balanced or conservative allocation to help weather downturns.

There’s no universal “right” equity allocation for retirees—it has to be determined account by account, based on your unique situation.

The Risk of Concentrated Positions

Another important consideration is whether you hold a concentrated position—a large percentage of your portfolio invested in a single stock or company.

During the accumulation years, an employee may accumulate significant shares of their employer’s stock, or investors may ride the success of a single company. Since you’re still working, contributing, and have decades before tapping retirement accounts, you may be able to absorb some of that added single stock risk.

During retirement, however, concentrated positions can pose an even bigger danger. At that point, it’s not just overall market volatility you’re exposed to, but also the unique risks of one company or business. If that single investment declines sharply—or worse, collapses—it could disproportionately impact your retirement security.

Diversifying concentrated positions before entering retirement may help reduce the risk of a single company determining the fate of your entire portfolio. Strategies such as gradually selling shares, using tax-efficient planning, or shifting portions of the concentrated holding into more diversified securities may all help manage that risk.

The Risk of Being Too Conservative

While it’s common (and often smart) to reduce risk in retirement, going too far in the opposite direction can create another set of problems.

People today are living longer—well into their 80s and 90s. That means a large portion of your retirement savings may remain invested for 15, 20, or even 30 years. If your portfolio is too conservative, you run two major risks:

Longevity Risk: You could outlive your savings because your money didn’t grow enough to keep pace with how long you live.

Inflation Risk: The cost of living rises every year. If your portfolio isn’t growing faster than inflation, your purchasing power declines over time.

For example, imagine someone retires and moves all their assets into bonds. While bonds may provide stability, they may not generate enough long-term growth to outpace inflation. Over decades, this could erode their ability to afford the same lifestyle.

Final Thoughts

Protecting yourself from stock market crashes in retirement isn’t about eliminating risk—it’s about managing it. That means:

Reducing volatility in the accounts you rely on for income

Avoiding the irreversible mistake of delaying the step down in risk post-retirement

Diversifying away from concentrated positions

Keeping enough growth in the portfolio to offset longevity and inflation risks

Every retiree’s situation is unique, and the best allocation depends on your income needs, time horizon, and goals. A thoughtful strategy that adapts as your life unfolds can help you weather market downturns while keeping your long-term financial plan on track.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

What makes market downturns more dangerous for retirees than for younger investors?

Retirees face greater risk during downturns because they’re no longer adding to their investments and must withdraw funds to cover living expenses. Selling investments during a market decline can lock in losses and make it difficult for a portfolio to recover.

What is sequence of returns risk, and why does it matter in retirement?

Sequence of returns risk refers to the danger of experiencing poor investment returns early in retirement while taking withdrawals. Negative returns early on can deplete assets faster, leaving less money invested to benefit from future market recoveries.

What is the “irreversible mistake” retirees should avoid with their portfolios?

The irreversible mistake occurs when retirees wait too long to reduce their exposure to risky assets after leaving the workforce. A severe market downturn early in retirement can permanently damage a portfolio if withdrawals and losses happen simultaneously.

Why are concentrated stock positions especially risky in retirement?

Holding too much of a single stock can expose retirees to the financial health of one company rather than the broader market. If that company’s value falls sharply, it can disproportionately harm retirement security and long-term income stability.

Can being too conservative with investments in retirement cause problems?

Yes. While reducing risk is important, overly conservative portfolios may not generate enough growth to keep up with inflation or sustain income over a long retirement. This can increase the chance of outliving your savings.

How can retirees balance growth and safety in their portfolios?

A balanced strategy often includes maintaining conservative allocations in income-producing accounts while keeping some exposure to growth assets for long-term needs. Adjusting investment risk account by account can help align stability with the potential for continued growth.

New Ways to Plan for Long-Term Care Costs: Self-Insure & Medicaid Trusts

Planning for long-term care is harder than ever as insurance premiums rise and availability shrinks. In 2025, families are turning to two main strategies: self-insuring with dedicated assets or using Medicaid trusts for protection and eligibility. This article breaks down how each option works, their pros and cons, and which approach fits your financial situation. Proactive planning today can help you protect assets, reduce risks, and secure peace of mind for retirement.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Planning for long-term care has always been one of the most challenging aspects of a retirement plan. For decades, the go-to solution was purchasing long-term care insurance. But as we move into 2025, this option is becoming less viable for many families due to skyrocketing premiums and shrinking availability associated with long-term care insurance. For example, in New York, there is now only one insurance company still offering new long-term care insurance policies. Carriers are exiting the market because the probability of policies paying out is high, and the dollar amounts associated with these claims can easily be in excess of $100,000 per year.

So where does that leave retirees and their families? Fortunately, there are two primary strategies that have emerged as alternatives:

Self-insuring by setting aside a dedicated pool of assets for potential care.

Using Irrevocable or Medicaid trusts to protect assets and plan for Medicaid eligibility.

In this article, we’ll break down each approach, their pros and cons, and what you should consider when deciding which path makes sense for you.

The Self-Insurance Strategy

Self-insuring means you create a separate “bucket” of assets earmarked specifically for long-term care needs. Instead of paying tens or even hundreds of thousands of dollars in premiums over the years for the long-term insurance coverage, those funds stay in your name. If a long-term care event never occurs, those assets simply pass on to your beneficiaries.

The benefits:

Flexibility—you decide how, when, and where care is provided.

Assets remain under your control and stay in your estate.

Avoid the risk of paying for insurance you never use.

The challenges:

You need significant extra assets, beyond what you already need to meet your retirement income goals.

Costs can be substantial—long-term care can run $120,000 to $200,000 per year, depending on location and type of care.

Self-insuring works best for those who have enough wealth to comfortably dedicate a portion of their portfolio to this potential risk without jeopardizing their retirement lifestyle.

The Trust Approach

For individuals or couples without the level of assets needed to fully self-insure, the next common strategy is using Irrevocable trusts (often called Medicaid trusts). These trusts are designed to protect non-retirement assets so that if you need long-term care in the future, you may qualify for Medicaid without having to spend down all your savings.

How it works:

Assets placed into an irrevocable trust are no longer counted as yours for Medicaid eligibility purposes.

If structured properly and far enough in advance, this can preserve assets for heirs while ensuring that Medicaid can help cover long-term care.

Important considerations:

There is typically a five-year look-back period in most states. If assets aren’t in the trust at least five years before applying for Medicaid, the strategy can fail.

Medicaid doesn’t cover everything. For example, around-the-clock home health care often isn’t fully covered, which limits flexibility.

The trust strategy is most effective for individuals who wish to protect their assets but recognize that care options may be limited to facilities and providers that accept Medicaid.

Which Approach is Right for You?

Ultimately, the choice between self-insuring and using a trust comes down to your financial position and your preferences for future care.

If you value flexibility and have the assets, self-insuring is often the preferred option.

If resources are more limited, a trust strategy can provide asset protection and access to Medicaid, even though it may reduce your care options.

The Key Takeaway: Plan Ahead

Whether you choose to self-insure, set up a trust, or use a combination of both, the most important factor is timing. These strategies require proactive planning—often years in advance. With costs continuing to rise and traditional long-term care insurance becoming less accessible, exploring these new approaches early can help protect both your assets and your peace of mind.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

Why is traditional long-term care insurance becoming less viable?

Long-term care insurance has become less practical due to rising premiums, stricter underwriting, and fewer insurers offering new policies. Many carriers have exited the market because claim payouts are large and frequent, making policies increasingly expensive for consumers.

What does it mean to self-insure for long-term care?

Self-insuring means setting aside a dedicated portion of your assets to cover potential long-term care expenses instead of paying insurance premiums. This approach offers flexibility and keeps assets under your control but requires sufficient wealth to handle potentially high annual costs.

Who is best suited for a self-insurance strategy?

Self-insuring typically works best for individuals or couples with substantial savings beyond what’s needed for retirement income. Those with enough assets can earmark funds for potential care without endangering their financial security or lifestyle.

What is a Medicaid or irrevocable trust, and how does it help with long-term care planning?

An irrevocable or Medicaid trust allows individuals to transfer assets out of their name, potentially helping them qualify for Medicaid coverage without depleting all their savings. If created properly and early enough, it can preserve wealth for heirs while enabling access to Medicaid-funded care.

What are the limitations of using a trust for long-term care planning?

Medicaid trusts must be established at least five years before applying for benefits to meet look-back rules. Additionally, Medicaid may not cover all types of care, such as full-time home assistance, which can limit personal choice and flexibility.

When should you start planning for long-term care needs?

It’s best to plan well in advance—ideally several years before care is needed. Early planning allows time to build assets for self-insuring or to structure a trust properly for Medicaid eligibility, reducing financial and emotional stress later.

If You Retire With $1 Million, How Long Will It Last?

Is $1 million enough to retire? The answer depends on withdrawal rates, inflation, investment returns, and taxes. This article walks through different scenarios to show how long $1 million can last and what retirees should consider in their planning.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Retirement planning often circles around one big question: If I save $1 million, how long will it last once I stop working? The answer isn’t one-size-fits-all. It depends on a handful of key factors, including:

Your annual withdrawal rate

Inflation (the rising cost of goods and services over time)

Your assumed investment rate of return

Taxes (especially if most of your money is in pre-tax retirement accounts)

In this article, we’ll walk through each of these factors and then run the numbers on a few different scenarios. By the end, you’ll have a much clearer idea of how far $1 million can take you in retirement.

Step 1: Determining Your Withdrawal Rate

Your withdrawal rate is simply the amount of money you’ll need to take from your retirement accounts each year to cover living expenses. Everyone’s number looks different:

Some retirees might only need $60,000 per year after tax.

Others might need $90,000 per year after tax.

The key is to determine your annual expenses first. Then consider:

Other income sources (Social Security, pensions, part-time work, rental income, etc.)

Tax impact (if pulling from pre-tax accounts, you’ll need to withdraw more than your net spending need to cover taxes).

For example, if you need $70,000 in after-tax spending money, you might need to withdraw closer to $75,000–$90,000 per year from your 401(k) or IRA to account for taxes.

Step 2: Don’t Forget About Inflation

Inflation is the silent eroder of retirement plans. Even if you’re comfortable living on $70,000 today, that number won’t stay static. If we assume a 3% inflation rate, here’s how that changes over time:

At age 65: $70,000

At age 80: $109,000

At age 90: $147,000

Expenses like healthcare, insurance, and groceries tend to rise faster than other categories, so it’s critical to build inflation adjustments into your plan.

Step 3: The Assumed Rate of Return

Once you retire, you move from accumulation mode (saving and investing) to distribution mode (spending down your assets). This shift raises important questions about asset allocation.

During accumulation years, you weren’t withdrawing, so market dips didn’t permanently hurt your portfolio.

In retirement, selling investments during downturns locks in losses, making it harder for your account to recover.

That’s why most retirees take at least one or two “step-downs” in portfolio risk when they stop working.

For most clients, a reasonable retirement assumption is 4%–6% annual returns, depending on risk tolerance.

Step 4: The Impact of Taxes

Taxes can make a significant difference in how long your retirement savings last.

If most of your money is in pre-tax accounts (401k, traditional IRA), you’ll need to gross up withdrawals to cover taxes.

Example: If you need $80,000 after tax, and your tax bill is $10,000, you’ll really need to withdraw $90,000 from your retirement accounts.

Now, if you have Social Security income or other sources, that reduces how much you need to pull from your investments.

Example:

Annual after-tax expenses: $80,000

Grossed-up for taxes: $90,000

Social Security provides: $30,000

Net needed from retirement accounts: $60,000 (indexed annually for inflation)

Scenarios: How Long Does $1 Million Last?

Now let’s put the numbers into action. Below are four scenarios that show how long a $1 million retirement portfolio lasts under different withdrawal rates. Each assumes:

Retirement age: 65

Beginning balance: $1,000,000

Inflation: 3% annually

Investment return: 5% annually

Scenario 1: Withdrawal Rate $40,000 Per Year

Assumptions:

Annual withdrawal: $40,000 (indexed for 3% inflation)

Rate of return: 5%

Result: Portfolio lasts 36 years (until age 100).

Why not forever? Because inflation steadily raises the withdrawal amount. At age 80, withdrawals rise to $62,000/year. By age 90, they reach $83,000/year.

Math Note: For the duration math, while age 90 minus age 65 would be 35 years. We are also counting the first year age 65 all the way through age 90, which is technically 36 years. (Same for all scenarios below)

Scenario 2: Withdrawal Rate $50,000 Per Year

Assumptions:

Annual withdrawal: $50,000 (indexed for 3% inflation)

Rate of return: 5%

Result: Portfolio lasts 26 years (until age 90).

By age 80, withdrawals grow to $77,000/year. By age 90, they reach $104,000/year.

Scenario 3: Withdrawal Rate $60,000 Per Year

Assumptions:

Annual withdrawal: $60,000 (indexed for 3% inflation)

Rate of return: 5%

Result: Portfolio lasts 21 years (until age 85).

Scenario 4: Withdrawal Rate $80,000 Per Year

Assumptions:

Annual withdrawal: $80,000 (indexed for 3% inflation)

Rate of return: 5%

Result: Portfolio lasts 15 years (until age 79).

Even if you bump the return to 6%, it only extends one more year to age 80. Higher withdrawals create a significant risk of outliving your money.

Final Thoughts

If you retire with $1 million, the answer to “How long will it last?” depends heavily on your withdrawal rate, inflation, taxes, and investment returns. A $40,000 withdrawal rate can potentially last through age 100, while a more aggressive $80,000 withdrawal rate may deplete funds before age 80.

The bottom line: Everyone’s situation is unique. Your lifestyle, income sources, tax situation, and risk tolerance will shape your plan. This is why working with a financial advisor is so important — to stress-test your retirement under different scenarios and give you peace of mind that your money will last as long as you do.

For more information on our fee based financial planning services to run your custom retirement projections, please visit our website.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

What is a safe withdrawal rate in retirement?

A commonly used guideline is the 4% rule, meaning you withdraw 4% of your starting balance each year, adjusted for inflation. However, personal factors—such as market performance, expenses, and longevity—should guide your specific rate.

How does inflation affect retirement spending?

Inflation steadily increases the cost of living, which raises how much you need to withdraw each year. At a 3% inflation rate, an annual $70,000 expense today could grow to over $100,000 within 15 years, reducing how long savings can last.

Why do investment returns matter so much in retirement?

Once you start taking withdrawals, poor market performance can have a lasting impact because you’re selling investments during downturns.

How do taxes impact retirement withdrawals?

Withdrawals from pre-tax accounts like traditional IRAs and 401(k)s are taxable, so you may need to take out more than your net spending needs. For instance, needing $80,000 after tax could require withdrawing around $90,000 or more before tax.

What can help make retirement savings last longer?

Strategies like moderating withdrawal rates, maintaining some stock exposure for growth, and factoring in Social Security or pension income can extend portfolio longevity. Regularly reviewing your plan helps ensure it stays aligned with your goals and spending needs.

The Risk of Outliving Your Retirement Savings

Living longer is a blessing, but it also means your savings must stretch further. Rising costs, inflation, and healthcare expenses can quietly erode your nest egg. This article explains how to stress-test your retirement plan to ensure your money lasts as long as you do.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

When you imagine retirement, perhaps you see time with family, travel, golf, and more time for your hobbies. What many don’t realize is how two forces—longer lifespans and rising costs—can quietly erode your nest egg while you're still enjoying those moments. Living longer is a blessing, but it means your savings must stretch further. And inflation, especially for healthcare and long-term care, can quietly chip away at your financial comfort over the years. Let’s explore how these factors shape your retirement picture—and what you can do about it.

What you’ll learn in this article:

How life expectancy is evolving, and how it’s increasing the need for more retirement savings

The impact of inflation on a retiree's expenses over the long term

How inflation on specific items like healthcare and long-term care are running at much higher rates than the general rate of inflation

How retirees can test their retirement projections to ensure that they are properly accounting for inflation and life expectancy

How pensions can be both a blessing and a curse

1. Living Longer: A Good But Bad Thing

The Social Security life tables estimate that a 65-year-old male in 2025 is expected to live another 21.6 years (reaching about age 86.6), while a 65-year-old female can expect about 24.1 more years, extending to around 89.1 (ssa.gov).

That has consequences:

If a retiree spends $60,000 per year, a male might need 21.6 × $60,000 = $1,296,000 in total

A female might need 24.1 × $60,000 = $1,446,000

These totals—before considering inflation—highlight how long-term retirement can quickly become a multi-million-dollar endeavor.

2. Inflation: The Silent Retirement Thief

Inflation steadily erodes the real value of money. Over the past 20 years, average annual inflation has held near 3%. Let’s model how inflation reshapes $60,000 in annual after-tax expenses for a 65 year-old retiree over time with a 3% annual increase:

At age 80 (15 years after retirement):

$60,000 × (1.03)^15 ≈ $93,068 per yearAt age 90 (25 years after retirement):

$60,000 × (1.03)^25 ≈ $127,278 per year

In just the first 15 years, this retiree’s annual expenses increased by $33,068 per year, a 55% increase.

3. The Hidden Risk of Relying Too Much on Pensions

One of the most common places retirees feel this pinch is with pensions. Most pensions provide a fixed monthly amount that does not rise meaningfully with inflation. That can create a false sense of security in the early years of retirement.

Example:

A married couple has after-tax expenses of 70,000 per year.

They receive $50,000 from pensions and $30,000 from Social Security.

At retirement, their $80,000 of income in enough to meet their $70,000 in after-tax annual expenses.

Here’s the problem:

The $50,000 pension payment will not increase.

Their expenses, however, will rise with inflation. After 15 years at 3% inflation, those same expenses could total about $109,000 per year.

By then, their combined pension and Social Security will fall well short, forcing them to dip heavily into savings—or cut back their lifestyle.

This illustrates why failing to account for inflation often means retirees “feel fine” at first, only to face an unexpected shortfall 10–15 years later.

4. Healthcare & Long-term Care Expenses

While the general rise in expenses by 3% per year would seem challenging enough, there are two categories of expenses that have been rising by much more than 3% per year for the past decade: healthcare and long-term care. Since healthcare often becomes a large expense for individuals 65 year of age and older, it’s created additional pressure on the retirement funding gap.

Prescription drugs shot up nearly 40% over the past decade, outpacing overall inflation (~32.5%) (nypost.com).

Overall healthcare spending jumped 7.5% from 2022 to 2023, reaching $4.9 trillion—well above historical averages (healthsystemtracker.org).

In-home long-term care is also hefty—median rates for a home health aide have skyrocketed, with 24-hour care nearing $290,000 annually in some cases (wsj.com).

5. The Solution: Projections That Embrace Uncertainty

When retirement may stretch 20+ years, and inflation isn’t uniform across expense categories, guessing leads to risk. A projection-driven strategy helps you:

Model life expectancy: living until age 85 – 95 (depending on family longevity)

Incorporate general inflation (3%) on your expenses within your retirement projections

Determine if you have enough assets to retire comfortably

Whether your plan shows a wide cushion or flags a potential shortfall, you’ll make confident decisions—about savings, investments, expense reduction, or part-time work—instead of crossing your fingers.

6. Working with a Fee-Based Financial Planner Can Help

Here’s the bottom line: Living longer is wonderful, but it demands more planning in the retirement years as inflation, taxes, life expectancy, and long-term care risks continue to create larger funding gaps for retirees.

A fee-based financial planner can help you run personalized retirement projections, taking these variables into account—so you retire with confidence. And if the real world turns out kinder than your model, that's a bonus. If you would like to learn more about our fee-based retirement planning services, please feel free to visit our website at: Greenbush Financial Group – Financial Planning.

Learn more about our financial planning services here.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

How does longer life expectancy affect retirement planning?

People are living well into their 80s and 90s, meaning retirement savings must cover 20–30 years or more. The longer you live, the more years your portfolio must fund, increasing the importance of conservative withdrawal rates and sustainable planning.

Why is inflation such a big risk for retirees?

Inflation steadily raises the cost of living, reducing the purchasing power of fixed income sources like pensions. Even at a modest 3% inflation rate, living expenses can rise more than 50% over 15 years, requiring larger withdrawals from savings.

How does inflation impact pensions and fixed income sources?

Most pensions don’t increase with inflation, so their purchasing power declines over time. A pension that comfortably covers expenses at retirement may fall short within 10–15 years as costs rise, forcing retirees to draw more from savings.

Why are healthcare and long-term care costs such a concern in retirement?

Healthcare and long-term care expenses have been increasing faster than general inflation. Costs for prescriptions, medical services, and in-home care can grow at 5–7% annually, putting additional strain on retirement savings.

How can retirees plan for inflation and longevity risk?

Running detailed retirement projections that factor in inflation, longer life expectancy, and varying rates of return helps reveal whether savings are sufficient. This approach allows retirees to make informed decisions about spending, investing, and lifestyle adjustments.

When should retirees work with a financial planner?

Consulting a fee-based financial planner early in the retirement planning process can help test different inflation and longevity scenarios. A planner can build customized projections and ensure your plan remains flexible as costs and life circumstances evolve.

How Much Money Will You Need to Retire Comfortably?

Retirement planning isn’t just about hitting a number. From withdrawal rates and inflation to taxes and investment returns, several factors determine if your savings will truly last. This article explores how to test your retirement projections and build a plan for financial security.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

As a Certified Financial Planner who runs retirement projections on a daily basis, one of the most common questions I get is: “How much money do I need to retire?”

The answer may surprise you—because there’s no universal number. The amount you’ll need depends largely on one thing: your expenses.

In this article, we’ll walk through:

Why expenses are the biggest driver of how much you need to retire

How inflation impacts retirement spending

Why the type of account you own matters

The importance of factoring in all your income sources

A quick 60-second way to test your own retirement readiness

Expenses: The Biggest Driver

When you ask, “Can I retire comfortably?”, the first question to answer is: How much do you spend each year?

For example:

If your expenses are $40,000 per year, then $500,000 in retirement savings could potentially be enough—especially if you’re supplementing withdrawals with Social Security or a pension.

But if your expenses are $90,000 per year, that same $500,000 likely won’t stretch nearly as far.

Your retirement lifestyle drives your retirement savings need. Someone with modest expenses may not need millions to retire, while someone with higher spending will require significantly more.

Don’t Forget About Inflation

It’s not just today’s expenses you need to plan for—it’s tomorrow’s too. Inflation quietly eats away at your purchasing power, making your cost of living higher every single year.

Here’s an example:

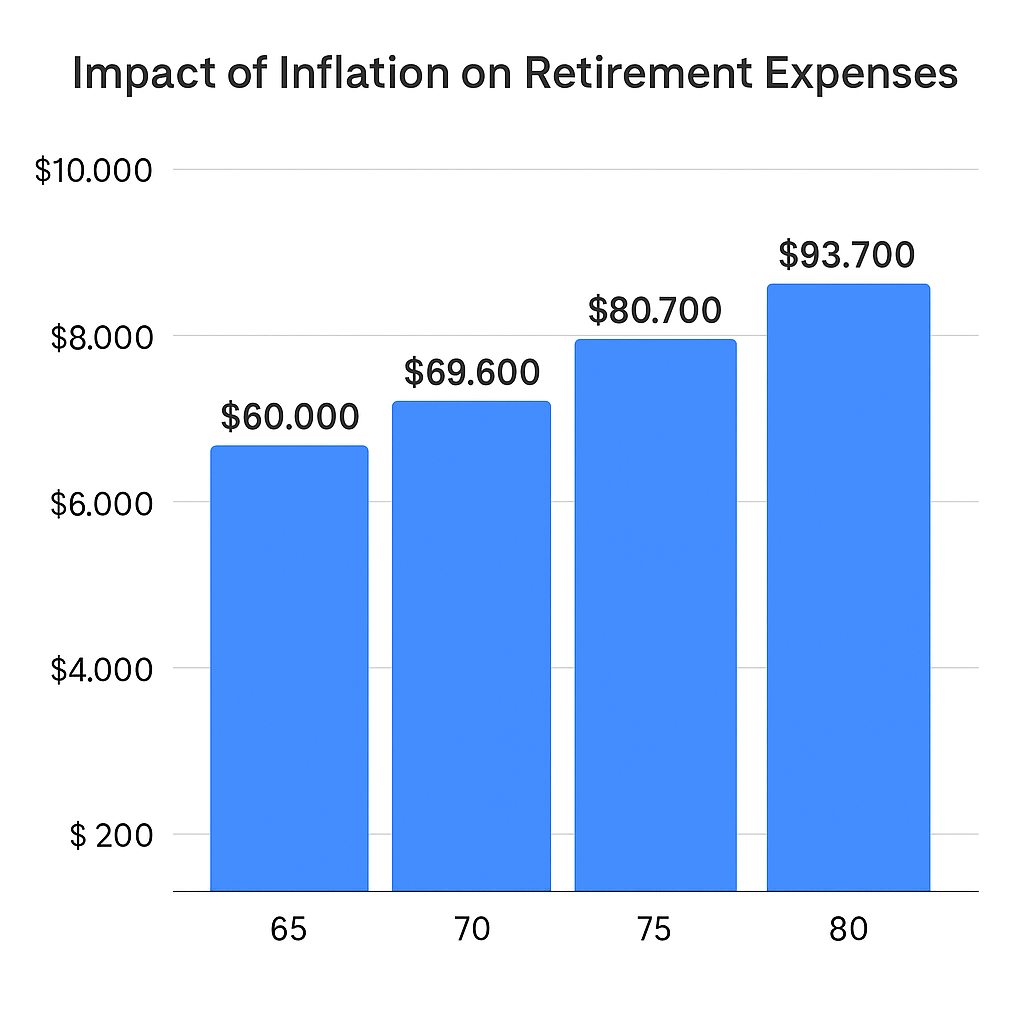

At age 65, your expenses are $60,000 per year.

If expenses rise at 3% annually, by age 80 they’ll be roughly $93,700 per year.

That’s a 50% increase in just 15 years—and you’ll need your retirement assets to keep up.

This is one of the hardest factors for individuals to quantify without financial planning software. Inflation not only increases expenses, but it changes your withdrawal rate from investments, which can impact how long your money lasts.

The Type of Account Matters

Not all retirement accounts are created equal. The type of retirement/investment accounts you own has a big impact on whether you can retire comfortably.

Pre-tax accounts (401k, traditional IRA): Every dollar withdrawn is taxed as ordinary income. A $1,000,000 account might really be worth closer to $700,000 after taxes.

Roth accounts: Withdrawals are tax-free, making these extremely valuable in retirement.

After-tax brokerage accounts: Withdrawals often receive more favorable capital gains treatment, so the tax drag can be lighter compared to pre-tax accounts.

Cash: Offers liquidity but typically earns little return, making it best for short-term expenses.

In short: Roth and after-tax brokerage accounts often provide more after-tax value compared to pre-tax accounts.

Factor in All Your Income Sources

Getting a general idea of your retirement income picture is key. This means adding up:

Social Security benefits

Pensions

Investment income (dividends, interest, etc.)

Part-time income in retirement

Withdrawals from retirement accounts

Once you total these income sources, you’ll need to apply the tax impact. Only then can you compare your after-tax income against your after-tax expenses (adjusted for inflation each year) to see if there’s a gap.

This is exactly how financial planners build retirement projections to determine sustainability.

Find Out If You Can Retire in 60 Seconds

Curious if you’re on track? We’ve built a 60-second retirement check-up that can help you quickly see if you have enough to retire.

Bottom line: There’s no magic retirement number. The amount you need depends on your expenses, inflation, account types, and income sources. By running the numbers—and stress-testing them with a financial planner—you can gain the confidence to know whether you’re truly ready to retire comfortably.

Partner with a Fee-Based Financial Planner to Build Your Retirement Plan

While rules of thumb and calculators can provide a helpful starting point, everyone’s retirement picture looks different. Your income needs, lifestyle goals, and unique financial situation will ultimately determine how much you need to retire comfortably.

Working with a fee-based financial planner can help take the guesswork out of retirement planning. A planner will create a customized strategy that factors in your retirement expenses, investments, Social Security, healthcare, and tax planning—so you know exactly where you stand and what adjustments to make.

If you’d like to explore your own numbers and build a retirement roadmap, we’d love to help. Learn more about our financial planning services here.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

How much money do I need to retire?

There’s no single number that fits everyone—the right amount depends primarily on your annual expenses, lifestyle, and income sources. A retiree spending $40,000 per year will need far less savings than someone spending $90,000.

Why are expenses the most important factor in retirement planning?

Your spending habits determine how much income your portfolio must generate. Knowing your annual expenses helps estimate your withdrawal needs, which directly drives how large your retirement savings must be.

How does inflation affect retirement spending?

Inflation gradually increases the cost of living, reducing the purchasing power of your money. At a 3% inflation rate, $60,000 in annual expenses today could rise to about $94,000 in 15 years, meaning your savings must grow to keep pace.

How does the type of retirement account impact how much you need to save?

Withdrawals from pre-tax accounts like 401(k)s and traditional IRAs are taxable, so you may need to save more to cover taxes. Roth IRAs and brokerage accounts often provide more after-tax value, since withdrawals may be tax-free or taxed at lower rates.

What income sources should I include when estimating retirement readiness?

Include all sources such as Social Security, pensions, dividends, part-time income, and withdrawals from savings. Comparing your total after-tax income against your inflation-adjusted expenses helps reveal whether you’re financially ready to retire.

How can I quickly estimate if I’m on track for retirement?

A simple way is to compare your projected annual expenses (adjusted for inflation) with your expected retirement income. Working with a fee-based financial planner can oftern provide a more comprehensive approach to answering the question “Do I have enough to retire?”

Don’t Gift Your House To Your Children

A common financial mistake that I see people make when attempting to protect their house from a long-term care event is gifting their house to their children. While you may be successful at protecting the house from a Medicaid spend-down situation, you will also inadvertently be handing your children a huge tax liability after you pass away. A tax liability, that with proper planning, could be avoided entirely.

A common financial mistake that I see people make when attempting to protect their house from a long-term care event is gifting their house to their children. While you may be successful at protecting the house from a Medicaid spend-down situation, you will also inadvertently be handing your children a huge tax liability after you pass away. A tax liability, that with proper planning, could be avoided entirely.

Asset Protection Strategy

As individuals enter their retirement years, they become rightfully more concerned about a long-term care event happening at some point in the future. The most recent statistic that I saw stated that “someone turning age 65 today has almost a 70% chance of needing some type of long-term care services at some point in the future” (Source: longtermcare.gov).

Long-term care is expensive, and most states require you to spend down your countable assets until you reach a level where Medicaid starts to pick up the tab. Different states have different rules about the spend-down process. However, there are ways to protect your assets from this Medicaid spend-down process.

In New York, the primary residence is not subject to the spend-down process but Medicaid can place a lien against your estate, so after you pass, they force your beneficiaries to sell the house, so Medicaid can recoup the money that they paid for your long-term care expenses. Since most people would prefer to avoid this situation and have their house passed to their children, they we'll sometimes gift the house to their kids while they're still alive to get it out of their name.

5 Year Look Back Rule

Gifting your house to your kids may be an effective way to protect the primary residence from a Medicaid lien, but this has to be done well before the long-term care event. In New York, Medicaid has a 5-year look back, which means anything that was gifted away 5 years before applying for Medicaid is back on the table for the spend down and Medicaid estate lien. However, if you gift your house to your kids more than 5 years before applying for Medicaid, the house is completely protected.

Tax Gifting Rules

So what’s the problem with this strategy? Answer, taxes. When you gift someone a house, they inherit your cost basis in the property. If you purchased your house 30 years ago for $100,000, you gift it to your children, and then they sell the house after you pass for $500,000; they will have to pay tax on the $400,000 gain in the value of the house. It would be taxed at a long-term capital gains rate, but for someone living in New York, tax liability might be 15% federal plus 7% state tax, resulting in a total tax rate of 22%. Some quick math:

$400,000 gain x 22% Tax Rate = $88,000 Tax Liability

Medicaid Trust Solution

Good news: there is a way to altogether avoid this tax liability to your beneficiaries AND protect your house from a long-term care event by setting up a Grantor Irrevocable Trust (Medicaid Trust) to own your house. With this solution, you establish an Irrevocable Trust to own your house, you gift your house to your trust just like you would gift it to your kids, but when you pass away, your house receives a “step-up in cost basis” prior to it passing to your children. A step-up in cost basis means the cost basis of that asset steps up the asset’s value on the day you pass away.

From the earlier example, you bought your house 30 years ago for $100,000, and you gift it to your Irrevocable Trust; when you pass away, the house is worth $500,000. Since a Grantor Irrevocable Trust owned your house, it passes through your estate, receives a step-up to $500,000, and your children can sell the house the next day and have ZERO tax liability.

The Cost of Setting Up A Medicaid Trust

So why doesn’t every one set up a Medicaid Trust to own their house? Sometimes people are scared away by the cost of setting up the trust. Setting up the trust could cost between $2,000 - $10,000 depending on the trust and estate attorney that you engage to set up your trust. Even though there is a cost to setting up the trust, I always compare that to the cost of not setting up your trust and leaving your beneficiaries with that huge tax liability. In the example we looked at earlier, paying the $3,000 to set up the trust would have saved the kids from having to pay $88,000 in taxes when they sold the house after you passed.

Preserves $500,000 Primary Residence Exclusion

By gifting your house to a grantor irrevocable trust instead of your children, you also preserve the long-term capital gain exclusion allowance if you decide to sell your house at some point in the future. When you sell your primary residence, you are allowed to exclude the following gain from taxation depending on your filing status:

Single Filer: $250,000

Joint Filer: $500,000

If you gift your house to your children and then five years from now, you decide to sell your house for whatever reason while you are still alive, it would trigger a tax event for your kids because they technically own your house, and it’s not their primary residence. By having your house owned by your Grantor Irrevocable Trust, if you were to sell your house, you would be eligible for the primary residence gain exclusion, and the trust could either buy your next house or you could deposit the proceeds to a trust account so the assets never leave the trust and remain protected for the 5-year lookback rule.

How Do Medicaid Trusts Work?

This article was meant to highlight the pitfall of gifting your house to your kids; however, if you would like to learn more about the Medicaid Trust solution and the Medicaid spend down process, please feel free to watch our videos on these topics below:

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

Why is gifting your house to your children a mistake for Medicaid planning?

While gifting your home can protect it from Medicaid’s spend-down rules, it also transfers your cost basis to your children. When they sell the property after your death, they may owe significant capital gains taxes on the home’s appreciation—liability that could have been avoided with proper planning.

What is Medicaid’s five-year look-back rule?

Medicaid reviews all asset transfers made within five years prior to applying for benefits. If you gifted your home or other assets during that time, Medicaid may count those transfers against you, delaying eligibility or subjecting the home to a lien for care costs.

How does a Medicaid Trust protect your home and reduce taxes?

A Grantor Irrevocable Trust (commonly called a Medicaid Trust) allows you to transfer ownership of your home while retaining the right to live in it. When you pass away, the home passes through your estate and receives a step-up in cost basis, eliminating capital gains taxes for your heirs while protecting the home from Medicaid recovery.

What is a step-up in cost basis?

A step-up in cost basis resets the home’s taxable value to its fair market value on the date of your death. For example, if you bought your home for $100,000 and it’s worth $500,000 when you die, your heirs’ cost basis becomes $500,000—allowing them to sell it with little or no tax owed.

Can you still use the home sale exclusion with a Medicaid Trust?

Yes. Because a Grantor Irrevocable Trust maintains your tax identity, you retain the $250,000 (single) or $500,000 (married) exclusion on the sale of your primary residence. This benefit is lost if you transfer ownership directly to your children.

What does it cost to set up a Medicaid Trust?

Setting up a Medicaid Trust typically costs between $2,000 and $10,000, depending on the attorney and complexity of your estate. While this is an upfront expense, it often saves families tens of thousands of dollars in future tax liability and asset protection.

Can the trust sell or hold proceeds from the home?

Yes. If the home is sold, the proceeds can remain in the trust or be used to purchase another home, keeping the funds protected under the five-year Medicaid look-back rule. The key is ensuring the sale proceeds never leave the trust’s ownership.

Secure Act 2.0: RMD Start Age Pushed Back to 73 Starting in 2023

On December 23, 2022, Congress passed the Secure Act 2.0, which moved the required minimum distribution (RMD) age from the current age of 72 out to age 73 starting in 2023. They also went one step further and included in the new law bill an automatic increase in the RMD beginning in 2033, extending the RMD start age to 75.

On December 23, 2022, Congress passed the Secure Act 2.0, which moved the required minimum distribution (RMD) age from the current age of 72 out to age 73 starting in 2023. They also went one step further and included in the new law bill an automatic increase in the RMD beginning in 2033, extending the RMD start age to 75.

This is the second time within the past 3 years that Congress has changed the start date for required minimum distributions from IRAs and employer-sponsored retirement plans. Here is the history and the future timeline of the RMD start dates:

1986 – 2019: Age 70½

2020 – 2022: Age 72

2023 – 2032: Age 73

2033+: Age 75

You can also determine your RMD start age based on your birth year:

1950 or Earlier: RMD starts at age 72

1951 – 1959: RMD starts at age 73

1960 or later: RMD starts at age 75

What Is An RMD?

An RMD is a required minimum distribution. Once you hit a certain age, the IRS requires you to start taking a distribution each year from your various retirement accounts (IRA, 401(K), 403(b), Simple IRA, etc.) because they want you to begin paying tax on a portion of your tax-deferred assets whether you need them or not.

What If You Turned Age 72 In 2022?

If you turned age 72 anytime in 2022, the new Secure Act 2.0 does not change the fact that you would have been required to take an RMD for 2022. This is true even if you decided to delay your first RMD until April 1, 2023, for the 2022 tax year.

If you are turning 72 in 2023, under the old rules, you would have been required to take an RMD for 2023; under the new rules, you will not have to take your first RMD until 2024, when you turn age 73.

Planning Opportunities

By pushing the RMD start date from age 72 out to 73, and eventually to 75 in 2033, it creates more tax planning opportunities for individuals that do need to take distributions out of their IRAs to supplement this income. Since these distributions from your retirement account represent taxable income, by delaying that mandatory income could allow individuals the opportunity to process larger Roth conversions during the retirement years, which can be an excellent tax and wealth-building strategy.

Delaying your RMD can also provide you with the following benefits:

Reduce the amount of your Medicare premiums

Reduce the percentage of your social security benefit that is taxed

Make you eligible for tax credits or deductions that you would have phased out of

Potentially allow you to realize a 0% tax rate on long-term capital gains

Continue to keep your pre-tax retirement dollars invested and growing

Additional Secure Act 2.0 Articles

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What is the new RMD age under the Secure Act 2.0?

Starting in 2023, the required minimum distribution (RMD) age increased from 72 to 73. Beginning in 2033, the RMD age will rise again to 75.

How does the new RMD timeline compare to previous rules?

Before 2020, RMDs began at age 70½. The Secure Act of 2019 moved it to age 72, and Secure Act 2.0 now increases it to age 73 in 2023 and age 75 starting in 2033.

How do you determine your RMD start age based on birth year?

If you were born in 1950 or earlier, your RMD started at 72. Those born between 1951 and 1959 begin at 73, and anyone born in 1960 or later will start at 75.

What if I turned 72 in 2022?

If you reached age 72 in 2022, you are still required to take your first RMD for that tax year, even if you delayed it until April 1, 2023. The new rule applies only to individuals turning 72 in 2023 or later.

What are the benefits of delaying RMDs?

Delaying RMDs can create valuable tax planning opportunities, including the ability to complete larger Roth conversions, reduce taxable income, lower Medicare premiums, and minimize taxes on Social Security benefits.

Can delaying RMDs impact long-term investment growth?

Yes. By postponing mandatory withdrawals, your tax-deferred savings can remain invested and continue to grow, potentially increasing your retirement assets over time.