Types of Retirement Plans

The comparing retirement plans chart gives business owners the ability to compare different types of plans available to their company.

Types of Retirement Plans

RC2

The comparing retirement plans chart gives business owners the ability to compare different types of plans available to their company.

Click on the PDF link in the green box below.

Rollover Chart

Provides individuals with clarification on the rollover rules for retirement accounts and IRA’s.

Rollover Chart

RC

Provides individuals with clarification on the rollover rules for retirement accounts and IRA’s.

Click on the PDF link in the green box below.

Simple IRA vs. 401(k) - Which one is right for your company?

There are a lot of options available to small companies when establishing an employer sponsored retirement plan. For companies that have employees in addition to the owners of the company, the question is do they establish a 401(k) plan or a Simple IRA?The right fit for your company depends on:

compare simple ira and 401k

There are a lot of options available to small companies when establishing an employer sponsored retirement plan. For companies that have employees in addition to the owners of the company, the question is do they establish a 401(k) plan or a Simple IRA?The right fit for your company depends on:

What are the company's primary goals for establishing the plan?

How much the owner(s) plan to contribute to the plan?

How many employees does the company have?

Do you want to restrict the plan to only full time employees?

The cost of maintaining each plan?

Does the company intend to make an employer contribution to the plan?

Diversity of the investment menu

Below is a chart that contains a quick comparison of some of the main features of each type of plan:

simple ira vs 401K comparison chart

For many small companies it often makes sense to start with a Simple IRA plan and then transition to a 401K plan as the company grows or when the owner intends to start accessing the upper deferral limits offered by the 401(k) plan.

Simple IRA's are relatively easy to setup and the administrative fees to maintain these plans are typically lower in comparison to 401(k) plans. Most Simple IRA providers will only charge $10 - $30 to custody the accounts.

By comparison, 401(k) plans are ERISA covered plans which require a TPA Firm (third party administrator) to maintain the plan documents, conduct year end plan testing, and file the 5500 each year. The TPA fees vary based on the provider and the number of employees eligible to participate in the plan. A ballpark range is $1,500 - $2,500 for companies with under 50 employees.

However, the additional TPA fees associated with establishing a 401(k) plan may be justified if:

The owners intend to max out their employee deferrals

The owners are approaching retirement and need to make big contributions

The company wants to maintain flexibility with the employer contribution

The company would like to make Roth contributions, loans, or rollovers available

WARNING: Most investment providers are "one trick ponies". They will talk about 401(k) plans and not present other options because they either do not have a thorough understand of how Simple IRA plans work or they are only able to offer 401(k) plans. Before establishing a retirement plan it is important to work with a firm that presents both options, helps you to understand the difference between the two types of plans, and assist you in evaluating which plan would best meet your company's goals and objectives.

Michael Ruger

About Michael.........

Hi, I'm Michael Ruger. I'm the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Comparing Different Types of Employer Sponsored Retirement Plans

Employer sponsored retirement plans are typically the single most valuable tool for business owner when attempting to:

Reduce their current tax liability

Attract and retain employees

Accumulate wealth for retirement

But with all of the different types of plans to choose from which one is the right one for your business? Most business owners are familiar with how 401(k) plans work but that might not be the right fit given variables such as:

comparison of different types of retirement plans

Employer sponsored retirement plans are typically the single most valuable tool for business owner when attempting to:

Reduce their current tax liability

Attract and retain employees

Accumulate wealth for retirement

But with all of the different types of plans to choose from which one is the right one for your business? Most business owners are familiar with how 401(k) plans work but that might not be the right fit given variables such as:

# of Employees

Cash flows of the business

Goals of the business owner

There are four main stream employer sponsored retirement plans that business owners have to choose from:

SEP IRA

Single(k) Plan

Simple IRA

401(k) Plan

Since there are a lot of differences between these four types of plans we have included a comparison chart at the conclusion of this newsletter but we will touch on the highlights of each type of plan.

SEP IRA PLAN

This is the only employer sponsored retirement plan that can be setup after 12/31 for the previous tax year. So when you are sitting with your accountant in the spring and they deliver the bad news that you are going to have a big tax liability for the previous tax year, you can establish a SEP IRA up until your tax filing deadline plus extension, fund it, and take a deduction for that year.

However, if the company has employees that meet the plan’s eligibility requirement, these plans become very expensive very quickly if the owner(s) want to make contributions to their own accounts. The reason being, these plans are 100% employer funded which means there are no employee contributions allowed and the employer contribution is uniform for all plan participants. For example, if the owner contributes 15% of their income to the SEP IRA, they have to make an employer contribution equal to 15% of compensation for each employee that has met the plans eligibility requirement. If the 5305-SEP Form, which serves as the plan document, is setup correctly a company can keep new employees out of the plan for up to 3 years but often times it is either not setup correctly or the employer cannot find the document.

Single(k) Plan or “Solo(k)”

These plans are for owner only entities. As soon as you have an employee that works more than 1000 hours in a 12 month period, you cannot sponsor a Single(k) plan.

The plans are often times the most advantageous for self-employed individuals that have no employees and want to have access to higher pre-tax contribution levels. For all intensive purposes it is a 401(k) plan, same contributions limits, ERISA protected, they allow loans and Roth contributions, etc. However, they can be sponsored at a much lower cost than traditional 401(k) plans because there are no non-owner employees. So there is no year-end testing, it’s typically a boiler plate plan document, and the administration costs to establish and maintain these plans are typically under $400 per year compared to traditional 401(k) plans which may cost $1,500+ per year to administer.

The beauty of these plans is the “employee contribution” of the plan which gives it an advantage over SEP IRA plans. With SEP IRA plans you are limited to contributes up to 25% of your income. So if you make $24,000 in self-employment income you are limited to a $6,000 pre-tax contribution.

With a Single(k) plan, for 2016, I can contribute $18,000 per year (another $6,000 if I’m over 50) up to 100% of my self-employment income and in addition to that amount I can make an employer contribution up to 25% of my income. In the previous example, if you make $24,000 in self-employment income, you would be able to make a salary deferral contribution of $18,000 and an employer contribution of $6,000, effectively wiping out all of your taxable income for that tax year.

Simple IRA

Simple IRA’s are the JV version of 401(k) plans. Smaller companies that have 1 – 30 employees that are looking to start a retirement plan will often times start with implementing a Simple IRA plan and eventually graduate to a 401(k) plan as the company grows. The primary advantage of Simple IRA Plans over 401(k) Plans is the cost. Simple IRA’s do not require a TPA firm since they are self-administered by the employer and they do not require annual 5500 filings so the cost to setup and maintain the plan is usually much less than a 401(k) plan.

What causes companies to choose a 401(k) plan over a Simple IRA plan?

Owners want access to higher pre-tax contribution limits

They want to limit to the plan to just full time employees

The company wants flexibility with regard to the employer contribution

The company wants a vesting schedule tied to the employer contributions

The company wants to expand the investment menu beyond just a single fund family

401(k) Plans

These are probably the most well recognized employer sponsored plans since at one time or another each of us has worked for a company that has sponsored this type of plan. So we will not spend a lot of time going over the ins and outs of these types of plan. These plans offer a lot of flexibility with regard to the plan features and the plan design.

We will issue a special note about the 401(k) market. For small business with 1 -50 employees, you have a lot of options regarding which type of plan you should sponsor but it’s our personal experience that most investment advisors only have a strong understanding of 401(k) plans so they push 401(k) plans as the answer for everyone because it’s what they know and it’s what they are comfortable talking about. When establishing a retirement plan for your company, make sure you consult with an advisor that has a working knowledge of all these different types of retirement plans and can clearly articulate the pros and cons of each type of plan. This will assist you in establishing the right type of plan for your company.

Michael Ruger

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

The Shift from Defined Benefit to Defined Contribution Plans

As defined benefit plans continue to become a thing of the past and workers realize they will not have a pension (and possibly Social Security) to rely on during retirement, it is important to be educated on the investments and opportunities available in employer sponsored defined contribution plans. This newsletter will briefly discuss the

The Shift from Defined Benefit to Defined Contribution Plans

As defined benefit plans continue to become a thing of the past and workers realize they will not have a pension (and possibly Social Security) to rely on during retirement, it is important to be educated on the investments and opportunities available in employer sponsored defined contribution plans. This newsletter will briefly discuss the difference between defined benefit plans and defined contribution plans, why the dramatic shift from one to the other, and why it is important to be educated on retirement and the investment options available.

Defined Benefit Plans

Defined benefit plans (commonly referred to as pension plans) are promises made by an organization to pay a specific amount, usually monthly, to an employee during retirement. These amounts are calculated based on a number of factors including an employees earnings history, service, and age. Since the organization is responsible for funding these plans during an employee’s retirement, investment returns are the concern of the organization, not the employee.

Defined Contribution Plans

Rather than an employer guaranteeing a benefit during retirement as is the case with defined benefit plans, the employee (and often times the employer) will make contributions to a defined contribution plan which accumulates over time and is drawn upon by the employee during retirement. One of the most common forms of defined contribution plans available to workers is the 401(k) plan. Since the guarantee of a monthly benefit during retirement is not there in a 401(k) plan, whatever is accumulated from employee/employer contributions and investment returns over the years is what will be available to the employee throughout retirement. In other words, this is the amount that must last throughout retirement.

Why the shift to 401(k)s and other defined contribution plans?

Defined benefit plans were set up to reward employees with consistent income during retirement since they are no longer earning. This is a great benefit to employees if available but these plans are becoming obsolete. As baby boomers continue to retire and live longer than previous generations, defined benefit plans are becoming too expensive to fund.

It is extremely difficult for companies (and municipalities) to turn a profit when they continue paying employees twenty years after their last day. Think of a defined benefit plan like you would a bad contract in baseball. Let me use one of the most scrutinized contracts in baseball history as an example. The Mets contract with Bobby Bonilla.

The last time Bonilla had an at bat for the Mets was in 1999, yet in 2015 he received a check for $1.19 million dollars. That amount is more than 17 of the current 25 players will make in 2015. Not the best business model when you are paying that kind of money to a player that hasn’t filled a seat (generated income for a company) in 15 years. The payment is guaranteed to Bonilla through 2035, which can be compared to a worker retiring at 55 and receiving a guaranteed payment for life.

For the reasons that seem obvious now, the past 30 years has seen a dramatic shift from defined benefit plans to defined contribution plans.

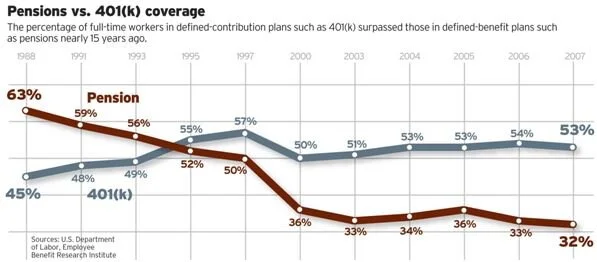

This chart illustrates the shift noted above. The breakeven point is shown around 1990 with no signs of the trend reversing.

As of June 30, 2014, 401(k) plans held an estimated $4.4 trillion in assets which is compared to $2.2 trillion in 2004.

Savings and Investment Performance

So, with less retirees having a pension plan to rely on for consistent income throughout retirement, how well are people preparing for retirement? The USA Today released an article in March 2015 titled “For millions, 401(k) plans have fallen short”, which describes the lack of retirement savings and inability for the majority of retirees to maintain their current lifestyle during retirement. The article references a report issued by the Employee Benefit Research Institute that stated the median amount in 401(k) savings accounts is $18,433. The median is higher for older employees as Vanguard 401(k) accounts for savers age 55 to 64 was $76,381 in 2013.

The Social Security website calculates life expectancy and determined that a man reaching age 65 today is expected to live until 84.3 years old (86.6 years old for women). That being said, an employee expecting to retire at age 65 with less than $100,000 in retirement savings has to live off that and social security for 20 plus years. The shift in retirement has led to many retirees not enjoying the retirement they had once planned.

As mentioned earlier, the migration from defined benefit plans to defined contribution plans has led to employees being responsible for managing their retirement. It is apparent that the savings rate for the average employee has not been sufficient to fund retirement, so now let us look at how employees are performing compared to major asset classes.

Contributions are only one part of a 401(k) balance with the other being interest earned. The chart above shows how the average investor has performed compared to different asset classes over the past 20 years. The 2.5% earned by the average investor was only .1% higher than inflation. This essentially means that in real dollars the average investor did not have any earnings during this period.

We typically look at the S&P 500 when determining how the stock market is performing which was up 9.9% over the same period. The other highlighted bar in the graph shows a portfolio with 60% in stocks and 40% in bonds, which is more of a conservative allocation but still saw an increase of 8.7%. When participating in a 401(k) for 20, 30, or 40 years, the majority of the balance when approaching retirement is not the contributions made but the interest that has compounded over an extended period of time. Losing 6-8% annually has a dramatic impact on an account, especially over a 20 year period.

This chart shows the impact of lost earnings over 40 years. In the example, the investor makes an initial investment of $10,000 earning 0%, 2%, 5%, and 8% annually with no additional contributions. Two quick takeaways are the interest that compounds at 5% and 8% are much more than the initial investment and after 20 years the difference between 5% and 8% is almost double.

Taking Control Of Your 401(k)

As defined contribution plans continue to takeover as the main income vehicle for retirees, how can employees benefit and take advantage of the available resources from these plans?

Start contributing as soon as possible - As shown earlier, the interest that compounds in a retirement account makes up the majority of the balance when invested for an extended period of time. The sooner you can start contributing the longer the account has to grow and the need to play catch-up as you approach retirement may be avoided. Also, you will be less reliable on the dollars being contributed as you are not used to the income each pay period.

Take advantage of the employer match - If your employer is generous enough to offer a match, take advantage of it. For example, you make $50,000 a year and your employer matches up to 3% of your compensation. This means that you can contribute $1,500 of pre-tax money and automatically double your investment. That is a 100% return just for participating in the plan.

Use the available resources - If your plan has a financial advisor, sit down with him or her and discuss your retirement goals and how to invest your contributions. The reason the average investor performs so poorly compared to the indexes is because they try to time the market and when they pull out they are reluctant to get back in. Discuss your time horizon and risk tolerance with your advisor and let them allocate your investments in a way that makes sense.

It is important to be educated, and historically, investors do not benefit over longer periods if they try to beat the market. JP Morgan put out a study that showed an investor who missed the 10 best days in the stock market from 1994-2014 earned a little more than half of an investor who was fully invested during the same period. If you have a long time horizon, it is important to hold through the ups and downs as historically the stock market goes up over long periods. For most investors, 10-15 years from retirement is when participants should start reassessing their allocation and determine if it is still the appropriate position for them.

Final Thoughts

As money continues to pour into defined contribution plans, it is important that the public be educated on what this means for retirement. Now more than ever it is up to employees to take responsibility for their retirement and save enough to last as defined benefit plans become obsolete and Social Security needs an overhaul that no one will touch.

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally , professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, pleas feel free to join in on the discussion or contact me directly.