How Does Depreciation Work for Rental Properties?

Rental property depreciation allows investors to reduce taxable income by spreading the cost of a property over 27.5 years. This article explains how depreciation works, how it offsets rental income, and how improvements are treated. It also covers what happens when a property is fully depreciated and how depreciation recapture impacts taxes when selling. Understanding these rules can help investors maximize tax efficiency and avoid costly surprises.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Depreciation is one of the most important tax benefits of owning rental property. It allows property owners to offset part of the cost of owning the property against the rental income they receive, which can significantly reduce taxes in the early years of ownership.

In this article, we’ll cover:

What depreciation is and how it works

The 27.5-year depreciation rule for rental properties

How depreciation can offset rental income

How improvements are depreciated

What happens when depreciation runs out

What depreciation recapture is when you sell the property

What Is Depreciation?

Depreciation is a tax deduction that allows rental property owners to recover the cost of a property over time. Even though real estate often increases in value, the IRS allows you to treat the property as if it is wearing out over time and deduct a portion of its value each year.

This deduction can be used to offset rental income, which may reduce how much tax you owe on the income the property generates.

The 27.5-Year Depreciation Rule

Residential rental properties are typically depreciated over 27.5 years.

This means you take the purchase price of the property (excluding land value) and divide it by 27.5 to determine your annual depreciation deduction.

Example:

So, if you purchased a rental property for $300,000, you can depreciate roughly $11,000 per year.

How Depreciation Offsets Rental Income

Depreciation is considered a non-cash expense, meaning you don’t actually write a check for it, but you still get the tax deduction.

Example Scenario:

Rental income: $11,000 per year

Depreciation: $11,000 per year

In this example, the depreciation deduction offsets the rental income, which may result in little to no taxable rental income for that year.

This is one of the reasons rental real estate can be a very tax-efficient investment.

Depreciation on Improvements

Many rental property owners make improvements to their property, such as:

New roof

New furnace or heating system

Kitchen renovation

Bathroom remodel

Flooring

Additions

These are called capital improvements, and each improvement typically has its own depreciation schedule separate from the original property purchase.

For example:

Appliances: Often 5-year depreciation

Carpeting: Often 5–7 years

Roof: Often 27.5 years

HVAC systems: Often 15–27.5 years depending on classification

There are also situations where bonus depreciation or Section 179 may allow you to deduct a larger portion of the improvement cost upfront.

This is an area where working with a knowledgeable tax professional is very important, because depreciation schedules vary depending on the type of improvement.

What Happens When a Property Is Fully Depreciated?

After 27.5 years, the property is considered fully depreciated.

This means:

You no longer receive the annual depreciation deduction

More of your rental income becomes taxable

Your tax liability on rental income may increase

However, you still own the property and still collect rental income — you just don’t get the depreciation tax benefit anymore.

What Is Depreciation Recapture?

Depreciation is a great tax benefit while you own the property, but when you sell the property, the IRS requires something called depreciation recapture.

When you sell a rental property:

You pay capital gains tax on the profit from the sale

You also pay tax on all the depreciation you took over the years

Depreciation recapture is taxed at a flat 25% federal tax rate

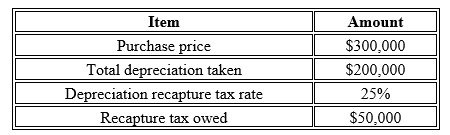

Example:

So in this example, when the property is sold, the owner would owe:

Capital gains tax on the profit plus

$50,000 in depreciation recapture tax

This surprises many real estate investors if they are not prepared for it.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

-

How long do you depreciate a rental property?Residential rental property is depreciated over 27.5 years.

-

What happens if I don't take depreciation?The IRS assumes you took it anyway, and you may still have to pay depreciation recapture when you sell.

-

Can I depreciate renovations on my rental property?Yes, but renovations and improvements typically have their own depreciation schedules.

-

What is bonus depreciation?Bonus depreciation allows you to deduct a large portion of certain improvements upfront instead of spreading the deduction over many years.

-

Do I have to pay depreciation back when I sell the property?When you sell the property, you may be subject to depreciation recapture, which taxes the total depreciation amount taken by 25%.

-

What happens after 27.5 years of depreciation?The property is fully depreciated and you no longer receive the annual depreciation deduction.

-

Does depreciation reduce my capital gains when I sell?No. Depreciation actually lowers your cost basis, which can increase your taxable gain and trigger depreciation recapture.

-

Can depreciation create a loss on paper?Yes. Depreciation can sometimes create a taxable loss even if the property is producing positive cash flow.

-

Should I work with a CPA if I own rental property?It's highly recommended. Depreciation, improvements, and recapture rules are complex, and a knowledgeable CPA can help you maximize tax benefits and avoid costly mistakes.

Should I Gift A Stock To My Kids Or Just Let Them Inherit It?

Many of our clients own individual stocks that they either bought a long time ago or inherited from a family member. If they do not need to liquidate the stock in retirement to supplement their income, the question comes up “should I just gift the stock to my kids while I’m still alive or should I just let them inherit it after I pass away?” The right answer is

Many of our clients own individual stocks that they either bought a long time ago or inherited from a family member. If they do not need to liquidate the stock in retirement to supplement their income, the question comes up “should I just gift the stock to my kids while I’m still alive or should I just let them inherit it after I pass away?” The right answer is largely influenced by the amount of appreciation or depreciation in the stock.

Gifting Stock

When you make a non-cash gift such as a stock, house, or even a business, the person receiving the gift assumes your cost basis in the assets. They do not receive a “step-up” in basis at the time the gift is made. Example, I buy XYZ Corp stock in 1995 for $10,000. In 2017, those shares of XYZ are now worth $100,000. If I gift them to my kids, no one owes tax on the gift at the time that the gift is made but my kids carry over my cost basis in the stock. If my kids hold the stock for 10 more years and sell it for $150,000, their basis in the stock is $10,000, and they owe capital gains tax on the $140,000 gain. Thus, creating an adverse tax consequence for my kids.

Inheriting Stock

Instead, let’s say I continue to hold XYZ stock and when I pass away my kids inherited the stock. If I pass away in 10 years and the stock is worth $150,000 then my kids receive a “step-up” in basis which means that their cost basis in the stock is the value of the stock as of the date of my death. They inherit the stock at $150,000 value, sell it the next day, and they owe $0 in taxes due to the step-up in basis upon my death.

In general, if you have assets that have low cost basis it is usually better for your heirs to inherit the assets as opposed to gifting it to them.

The concept is often times reversed for assets that have depreciated in value…..with an important twist. If I purchase XYZ Corp stock in 1995 for $10,000 but in 2017 it’s only worth $5,000, if I sold the stock myself I would capture the realized investment loss and could use it to offset investment gains or reduce my income by $3,000 for the IRS realized loss allowance.

Here is a very important rule......

In most cases, do not gift a depreciated asset to someone else. Why? When you gift an asset that has depreciated in value the carry over basis rules change. For an asset that has depreciated in value, the carry over basis for the person receiving the gift is the higher of the fair market value of the asset or the cost basis of the person making the gift. In other words, the loss evaporates when I gift the asset to someone else and no one gets the tax advantage of using the realized loss for tax purposes. It would be better if I sold the stock, captured the investment loss, and then gifted the cash.

If they inherit the stock that has lost value there is no value to the step-up in basis because the stock has not appreciated in value.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.