Potential Consequences of Taking IRA Distributions to Pay Off Debt

Once there is no longer a paycheck, retirees will typically meet expenses with a combination of social security, withdrawals from retirement accounts, annuities, and pensions. Social security, pensions, and annuities are usually fixed amounts, while withdrawals from retirement accounts could fluctuate based on need. This flexibility presents

Taking IRA Distributions to Pay Off Debt: The Tax Consequences

Once there is no longer a paycheck, retirees will typically meet expenses with a combination of social security, withdrawals from retirement accounts, annuities, and pensions. Social security, pensions, and annuities are usually fixed amounts, while withdrawals from retirement accounts could fluctuate based on need. This flexibility presents opportunities to use retirement savings to pay off debt; but before doing so, it is important to consider the possible consequences.

Clients often come to us saying they have some amount left on a mortgage and they would feel great if they could just pay it off. Lower monthly bills and less debt when living on a fixed income is certainly good, both from a financial and psychological point of view, but taking large distributions from retirement accounts just to pay off debt may lead to tax consequences that can make you worse off financially.

Below are three items I typically consider before making a recommendation for clients. Every retiree is different so consulting with a professional such as a financial planner or accountant is recommended if you’d like further guidance.

Impact on State Income and Property Taxes

Depending on what state you are in, withdrawals from IRA’s could be taxed very differently. It is important to know how they are taxed in your state before making any big decision like this. For example, New York State allows for tax free withdrawals of IRA accounts up to a maximum of $20,000 per recipient receiving the funds. Once the $20,000 limit is met in a certain year, any distribution you take above that will be taxed.

If someone normally pulls $15,000 a year from a retirement account to meet expenses and then wanted to pull another $50,000 to pay off a mortgage, they have created $45,000 of additional taxable income to New York State. This is typically not a good thing, especially if in the future you never have to pull more than $20,000 in a year, as you would have never paid New York State taxes on the distributions.

Note: Another item to consider regarding states is the impact on property taxes. For example, New York State offers an “Enhanced STAR” credit if you are over the age of 65, but it is dependent on income. Here is an article that discusses this in more detail STAR Property Tax Credit: Make Sure You Know The New Income Limits.

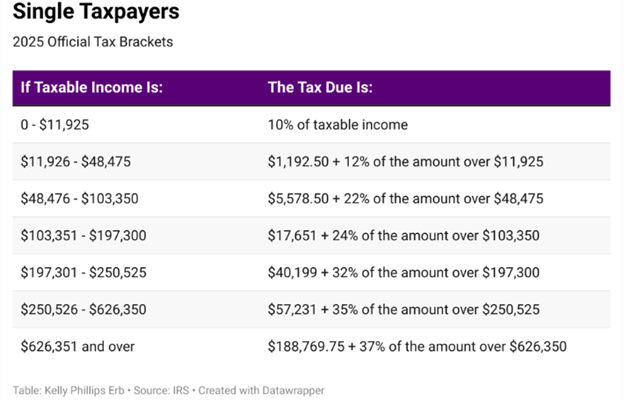

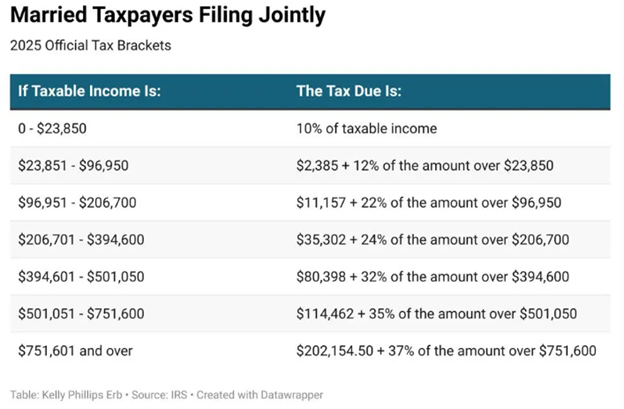

What Tax Bracket Are You in at the Federal Level?

Federal income taxes are determined using a “Progressive Tax” calculation. For example, if you are filing single, the first $12,400 of taxable income you have is taxed at a lower rate than any income you earn above that. Below are charts of the 2025 tax tables so you can review the different tax rates at certain income levels for single and married filing joint (IRS ). ( Source: Nerd Wallet ).

There isn’t much of a difference between the first two brackets of 10% and 12%, but the next jump is to 22%. This means that, if you are filing single, you are paying the government 10% more on any additional taxable income from $50,401 – $105,700. Below is a basic example of how taking a large distribution from the IRA could impact your federal tax liability.

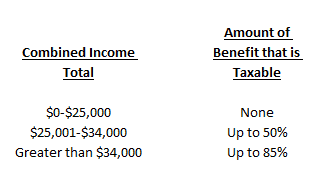

How Will it Impact the Amount of Social Security You Pay Tax on?

This is usually the most complicated to calculate. Basically, by showing more income, you may have to pay tax on more of your Social Security benefit. Below is a chart put together with information from the IRS to show how much of your benefit may be taxed.

To calculate “Combined Income”, you take your Adjusted Gross Income + Nontaxable Interest + Half of your Social Security benefit. For the purpose of this discussion, remember that any amount you withdraw from your IRA is counted in your Combined Income and therefore could make more of your social security benefit subject to tax.

Peace of mind is key and usually having less bills or debt can provide that, but it is important to look at the cost you are paying for it. There are times that this strategy could make sense, but if you have questions about a personal situation please consult with a professional to put together the correct strategy.

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

Last updated June, 2026

The Medicaid Spend Down Process In New York

You are most likely reading this article because you had a family member that had a health event and the doctors have informed you that they are not allowed to go back home to their house and will need some form of health assistance going forward. This article was written to help you understand from a high level the steps that you may need to take to

You are most likely reading this article because you had a family member who had a health event, and the doctors have informed you that they are not allowed to go back home to their house and will need some form of health assistance going forward. This article was written to help you understand, from a high level, the steps that you may need to take to get them the care that they need and to get a preview of the Medicaid application process and the spend-down process, if that’s the path that needs to be taken.

Everyone is living longer, which is a good thing, but it creates more complications later in life. It is becoming much more common that people have family members who have a health event in their 80s or 90s that renders them unable to continue to live independently. Without advance planning, a lot of the important decisions then have to be made by family and friends, so it is important for even younger individuals to understand how the process works because you may be in this situation some day for a loved one.

Do I Have To Apply For Medicaid To Pay For Their Care?

What you will find out very quickly is any type of care whether it's home health care, assisted living, or a nursing home, is very expensive. Very few individuals have the assets and the income to enable them to pay out of pocket for their care without going broke. It's not uncommon for kids or family members to have no idea what mom or dad's income and asset picture looks like. But no one is going to provide you with this information unless you have a power of attorney.

Power of Attorney, Health Proxy, and Will

A power of attorney (“POA”) is a document that allows you to step into the shoes of a person who has been incapacitated. It allows you to get information on their bank accounts, investments, insurance policies, and anything else financial. If you do not have a power of attorney, you need to get one quickly. A lot of financial decisions will most likely need to be made in a very short period of time. You will need to contact an estate attorney to draft the power of attorney. There are some choices that you will have to make when you draft the documents as to what powers the “POA” will have. They can usually be turned around by an attorney in 48 hours if needed.

While you have the estate attorney on the phone, you also will want to make sure that they have a health proxy and a will. The health proxy allows you to make health decisions for a family member if they are unable to do so. While it’s difficult to think about, health proxies will typically list out the end-of-life decisions. For example, a health proxy may state that mom or dad refuses to have a machine breathe for them if they are no longer able to breathe on their own. The questions are tough to answer, but it’s very important to have this document in place.

Home Care, Assisted Living, or Nursing Home

Prior to the health event, mom or dad may have been living by themselves at their house. Now the doctor is telling them that because of the damage done by the stroke, that they will not release them from the hospital until other arrangements are made for their care. There are three options to receive care:

Receiving care in the home via home care by health aids

Assisted living facility

Nursing home facility

People that cannot pay for 100% of their care and that do not have a long term care insurance policy, typically have to spend down their personal assets and then apply for Medicaid. Now that is said, let's jump right into what is protected and not protected as far as income and assets for Medicaid.

Different Rules For Different States

Each state has different eligibility and spends down rules when it comes to Medicaid. For purposes of this article, we will assume that the person needing the care is a resident of New York. If you live in a different state, the process will be similar but the actual amounts and the definition of "protected" assets may be different. It's usually best to work with a Medicaid planner, estate attorney, or local social services office that is located within your state/county to obtain the rules for your family member that needs care.

The Medicaid Rules In New York

There are different limits based on whether the family member needing care is married and their spouse is still alive or if they are single or widowed. In general, if a couple is married and one spouse needs care, more assets and income will be able to be protected and they will be able to qualify for Medicaid because they recognize that income and assets have to be available to support the spouse that does not need the care. But for purposes of this article, we will assume that mom passed away and dad now needs care.

Asset Limit

In 2026, to qualify for Medicaid, an individual is only allowed to keep $33,038 in assets. The next question I get is "what counts toward that number?" It's actually easier to explain what DOES NOT count toward that number. The only assets that do not count toward that threshold are as follows:

Primary Residence

1 Vehicle

Pre-Tax Retirement Accounts (if older than age 70½) - (However Required Minimum Distribution goes toward care)

Irrevocable Trust (Funded at least 5 years ago)

Pre-paid burial expenses

That's it. If Dad has $50,000 in his checking account, $20,000 in a Roth IRA, and an RV, the RV will need to be sold, and he will need to spend down the Roth IRA and the checking account until the balance reaches $33,038 in order to apply for Medicaid.

Primary Residence

Very important, while the primary residence is a protected asset for purposes of the Medicaid application, Medicaid will place a lien against dad’s estate for the money that they paid on his behalf. Meaning when he passes away, the kids do not automatically get the house. Medicaid will be first in line after the house is sold waiting to get paid. The amount depends on how much Medicaid paid out. If dad lives in a house that is worth $200,000 and Medicaid during his lifetime paid out $120,000 for his care, when the house sells, Medicaid will get $120,000 and the beneficiaries of the estate will only get the remaining $80,000.

When kids hear this, they typically get upset because mom and dad worked their whole life to pay off the mortgage and maintain the house, and now they are going to lose it to Medicaid. Is there anything that can be done to protect it? If the house was not put into a Medicaid Trust 5 years before needing to qualify for Medicaid, then no, there is nothing that can be done. That’s why advanced planning is so important.

If dad worked with an estate attorney to establish a Medicaid trust 5 years ago, the attorney could have changed the ownership of the house to the trust, once dad makes it by 5 years without a health event, it’s no longer a countable asset for Medicaid and Medicaid cannot place a lien against the house. The question I usually ask our clients is, “Do you want Medicaid to get your house, or do you want your kids to have it?” Most people say their kids but if advanced planning was not completed, you lose this options.

No Gifts To Kids

So what if you change the name on the house to the kids? It's considered a "gift". All gifts made within the last five years are a countable assets. It's called the "5-year look back period". When you apply for Medicaid for your dad, you have to provide them with a ton of information, including 5 years of all statements for bank accounts and investment accounts. Also, you have to provide them with copies of all checks written over the past 5 years that were in excess of $1,000. Medicaid is making sure that you did not "give" all of Dad's assets away last minute so he could qualify for Medicaid and avoid the spend down.

Income Limits

We have talked about assets but what about income? It's not uncommon for a parent to be receiving a pension and/or social security. They are only allowed to keep $1,836 per month in 2026. The rest of their income will be applied toward their care. This can create some tough decisions if dad has to go to assisted living or a nursing home and the family has to maintain the house and meet his financial needs on $1,836 per month. Again, Medicaid is trying to recoup as much as it can to pay for dad's care.

Medicaid Pooled Trust

There are ways to protect income above the $1,836 threshold through the use of a Medicaid Pooled Trust. Unlike the Medical Irrevocable Trust to protect assets that needs to be established 5 years prior, these trusts can be establish now to protect more income. They work like a special checking account that can only be used to pay bills in dad's name. You can never withdraw cash out of the accounts. As long as dad is considered "disabled" by the social security administration or NYS he may qualify to setup this trust. There are not-for-profit entities that administer this income trust. Basically his income from social security and pension would be deposited to this trust account and then when bills show up for utilities, property taxes, car payment, etc, you submit the bill to the organization that is administering the trust and they pay the bill on behalf of that individual.

Home Care Limitation

Most individuals want to return to their home and have the care provided at their house via home health aids. This may or may not be an option. It all depends on the level of care needed. If Medicaid will be paying for dad's care, you will need to call the social services office in the county that he lives in. They will send an "assessor" to his house to determine if the living conditions are adequate for home care and they will also determine the level of care that is needed. In general, if the estimated cost of home care is expected to be at least 90% of what it would cost for care at a facility, Medicaid will not pay for home care and will require them to go to an assisted living or nursing home facility.Home health aids typically range in price from $15 - $30 per hour. Assume it cost $25 per hour, if dad needs care 8 hours a day, 7 days a week that would cost $5,600 per month. If you need a nurse or registered nurse to administer medication at the home, you are looking at $40+ per hour for those services.

Steps From Start To Finish

We have covered a lot of ground and this is just a general overview. But here is a general list of the steps that need to be taken assuming dad had a health event and you need to apply for Medicaid on his behalf:

Contact an estate attorney to establish a power of attorney and requirement for Medicaid application

Using the POA, begin collecting financial information for the Medicaid process

Contact the county social services office to request an assessment to determine if home care will be an option if it's in question

If a spend down is required to qualify for Medicaid, work with estate attorney to develop spend down strategy

If monthly income is above threshold, determine if a Medicaid pooled trust is an option

About Michael.........

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Last updated June, 2026

Warning To All Employees: Review The Tax Withholding In Your Paycheck Otherwise A Big Tax Bill May Be Waiting For You

As a result of tax reform, the IRS released the new income tax withholding tables in January and your employer probably entered those new withholding amounts into the payroll system in February. It was estimated that about 90% of taxpayers would see an increase in their take home pay once the new withholding tables were implemented.

As a result of tax reform, the IRS released the new income tax withholding tables in January and your employer probably entered those new withholding amounts into the payroll system in February. It was estimated that about 90% of taxpayers would see an increase in their take home pay once the new withholding tables were implemented. While lower tax rates and more money in your paycheck sounds like a good thing, it may come back to bite you when you file your taxes.

The Tax Withholding Guessing Game

Knowing the correct amount to withhold for federal and state income taxes from your paycheck is a bit of a guessing game. Withhold too little throughout the year and when you file your taxes you have a tax bill waiting for you equal to the amount of the shortfall. Withhold too much and you will receive a big tax refund but that also means you gave the government an interest free loan for the year.

There are two items that tell your employer how much to withhold for federal income tax from your paycheck:

Income Tax Withholding Tables

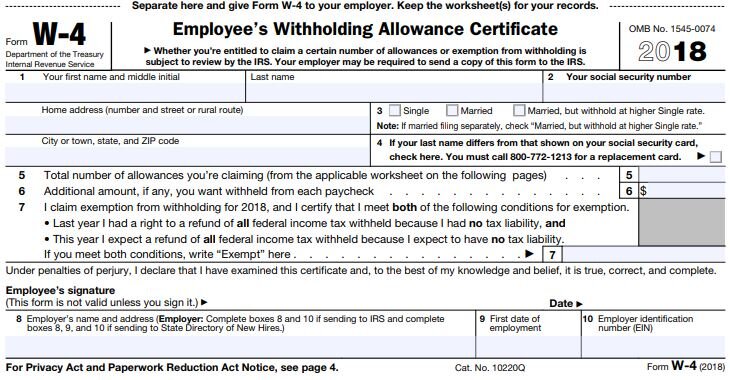

Form W-4

The IRS provides your employer with the Income Tax Withholding Tables. On the other hand, you as the employee, complete the Form W-4 which tells your employer how much to withhold for taxes based on the “number of allowances” that you claim on the form.

What Is A W-4 Form?

The W-4 form is one of the many forms that HR had you complete when you were first hired by the company. Here is what it looks like:

Section 3 of this form tells your employer which withholding table to use:

Single

Married

Married, but withhold at higher Single Rate

Section 5 tells your employer how many "allowances" you are claiming. Allowance is just another word for "dependents". The more allowances your claim, the lower the tax withholding in your paycheck because it assumes that you will have less "taxable income" because in the past you received a deduction for each dependent. This is where the main problem lies. Due to the changes in the tax laws, the tax deduction for personal exemptions was eliminated. This may adversely affect some taxpayers the were claiming a high number of allowances on their W-4 form because even though the number of their dependents did not change, their taxable income may be higher in 2018 because the deduction for personal exemptions no longer exists.

Even though everyone should review their Form W-4 form this year, employees that claimed allowances on their W-4 form are at the highest risk of either under withholding or over withholding taxes from their paychecks in 2018 due to the changes in the tax laws.

How Much Should I Withhold From My Paycheck For Taxes?

So how do you go about calculating that right amount to withhold from your paycheck for taxes to avoid an unfortunate tax surprise when you file your taxes for 2018? There are two methods:

Ask your accountant

Use the online IRS Withholding Calculator

The easiest and most accurate method is to ask your personal accountant when you meet with them to complete your 2017 tax return. Bring them your most recent pay stub and a blank Form W-4. Based on the changes in the tax laws, they can assist you in the proper completion of your W-4 Form based on your estimated tax liability for the year.If you complete your own taxes, I would highly recommend visiting the updated IRS Withholding Calculator. The IRS calculator will ask you a series of questions, such as:

How many dependents you plan to claim in 2018

Are you over the age of 65

The number of children that qualify for the dependent care credit

The number of children that will qualify for the new child tax credit

Estimated gross wages

How much fed income tax has already been withheld year to date

Payroll frequency

At the end of the process it will provide you with your personal results based on the data that you entered. It will provide you with guidance as to how to complete your Form W-4 including the number of allowances to claim and if applicable, the additional amount that you should instruct your employer to withhold from your paycheck for federal income taxes. Additional withholding requests are listed in Section 6 of the Form W-4.

Avoid Disaster

Having this conversation with your accountant and/or using the new IRS Withholding Calculator will help you to avoid a big tax disaster in 2018. Unfortunately, many employees may not learn about this until it's too late. Employees that are used to getting a tax refund may find out in the spring of next year that they owe thousands of dollars to the IRS because the combination of the new tax tables and the changes in the tax law that caused them to inadvertently under withhold federal income taxes throughout the year.

Action Item!!

Take action now. The longer you wait to run this calculation or to have this conversation with your accountant, the larger the adjustment may be to your paycheck. It's easier to make these adjustments now when you have nine months left in the year as opposed to waiting until November.I would strongly recommend that you share this article with your spouse, children in the work force, and co-workers to help them avoid this little known problem. The media will probably not catch wind of this issue until employees start filing their tax returns for 2018 and they find out that there is a tax bill waiting for them.

About Michael.........

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

More Taxpayers Will Qualify For The Child Tax Credit

There is great news for parents in the middle to upper income tax brackets in 2018. The new tax law dramatically increased the income phaseout threshold for claiming the child tax credit. In 2017, parents were eligible for a $1,000 tax credit for each child under the age of 17 as long as their adjusted gross income (“AGI”) was below $75,000 for single

There is great news for parents in the middle to upper income tax brackets. The new tax law dramatically increased the income phase-out threshold for claiming the child tax credit. In 2017, parents were eligible for a $1,000 tax credit for each child under the age of 17 as long as their adjusted gross income (“AGI”) was below $75,000 for single filers and $110,000 for married couples filing a joint return. If your AGI was above those amounts, the $1,000 credit was reduced by $50 for every $1,000 of income above those thresholds. In other words, the child tax credit completely phased out for a single filer with an AGI greater than $95,000 and for a married couple with an AGI greater than $130,000.

Note: If you are not sure what the amount of your AGI is, it’s the bottom line on the first page of your tax return (Form 1040).

New Phaseout Thresholds Beginning In 2018

Starting in 2018 and for years going forward, the new phaseout thresholds for the Child Tax Credit begin at the following AGI levels:

Single Filer: $200,000

Married Filing Joint: $400,000

If your AGI falls below these thresholds, you are eligible for the full Child Tax Credit. For taxpayers with an AGI amount that exceeds these thresholds, the phaseout calculation is the same as 2017. The credit is reduced by $50 for every $1,000 in income over the AGI threshold.

Wait......It Gets Better

Not only will more families now qualify for the child tax credit but the amount of the credit was doubled. The new tax law increased the credit from $1,000 to $2,000 for each child under the age of 17.

In 2025, a married couple, with three children, with an AGI of $200,000, would have received nothing for the child tax credit. Now, that same family will receive a $6,000 tax credit. That’s huge!! Remember, “tax credits” are more valuable than “tax deductions”. Tax credits reduce your tax liability dollar for dollar whereas tax deductions just reduce the amount of your income subject to taxation.

This information is for educational purposes only. Please consult your accountant for personal tax advice.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

How Rental Income Will Be Taxed In Years 2019+

Tax reform will change the way rental income is taxed to landlords beginning in 2018. Under current law, rental income is classified as "passive income" and that income simply passes through to the owner's personal tax return and they pay ordinary income tax on it. Beginning in 2018, rental income will be eligible to receive the same preferential tax

Tax reform will change the way rental income is taxed to landlords beginning in 2018. Under current law, rental income is classified as "passive income" and that income simply passes through to the owner's personal tax return and they pay ordinary income tax on it. Beginning in 2018, rental income will be eligible to receive the same preferential tax treatment as the "qualified business income" (QBI) for small business owners.

20% Deduction

Starting in 2018, taxpayers with qualified business income (including rental income), may be eligible to take a tax deduction up to 20% of their QBI. Determining whether or not you will be eligible to capture the full 20% deduction on your rental income will be based on your total taxable income for year. The taxable income thresholds are as follows:Single filers: $157,500Married filing joint: $315,000"Total taxable income" is not your AGI (adjusted gross income) and it's not just income from your real estate business or self-employment activities. It's your total taxable income less some deductions. The IRS has yet to provide us with full guidance on the definition of "total taxable income". For example, let's assume you have three rental properties owned by an LLC and you net $50,000 in income from the LLC each year. But your wife is a lawyer that makes $350,000 per year. Your total taxable income for the year would be $400,000 landing you above the $315,000 threshold.

Below The Income Threshold

If your total taxable income is below the income thresholds listed above, the calculation is very easy. Take your total QBI and multiply it by 20% and that's your tax deduction.

Above The Income Threshold

If your total taxable income is above the thresholds, the calculation gets more complex. If you exceed the income thresholds, your deduction is the LESSER of:

20% of QBI

The GREATER OF:

50% of W-2 wages paid to employees

25% of W-2 wages paid to employees PLUS 2.5% of the unadjusted asset basis

The best way to explain the calculation is by using an example. Assume the following:

I bought a commercial building 3 years ago for $1,000,000

I have already captured $100,000 in depreciation on the building

After expenses, I net $150,000 in income each year

The LLC that owns the property has no employees

I'm married

I own a separate small business that makes $400,000 in income

Since I'm over the $315,000 total taxable income threshold for a married couple filing joint, I will calculate my deduction as follows:The LESSER of:

20% of QBI = $30,000 ($150,000 x 20%)

The GREATER of:

50% of W-2 wage paid to employees = $0 (no employees)

25% of W-2 wages page to employees plus 2.5% of unadjusted basis

(25% of wages = $0) + (2.5% of unadjusted basis = $25,000) = $25KIn this example, my deduction would be limited to $25,000. Here are a few special notes about the calculation listed above. In the 11th hour, Congress added the "2.5% of unadjusted basis" to the calculation. Without it, it would have left most landlords with a $0 deduction. Why? Real estate owners typically do not have W-2 employees, so 50% of W-2 wages would equal $0. Some larger real estate investors have "property management companies" but they are usually set up as a separate entity. In which case, the W-2 income of the property management company would not be included in the calculation for the QBI deduction. If you are someone who owns a property or properties and is need of a Property management company to help you with organizing and operating your property, then doing research in your general area to find a real estate company that can help you with that is important.Another special note, 2.5% is based on an unadjusted basis and it's not reduced by depreciation. However, the tangible property has to be subject to depreciation on the last day of the year to be eligible for the deduction. Meaning, even though the 2.5% is not reduced for the amount of depreciation already taken on the property, the property must still be in the "depreciation period" on the last day of the year to be eligible for the QBI deduction.Tony Nitti, a writer for Forbes, also makes the following key points:

The depreciable period starts on the date the property is placed in service and ends on the LATER of:

- 10 years, or- The last day of the last full year in the asset's "regular" (not ADS) depreciation periodMeaning, if you purchase a non-residential rental building that is depreciated over 39 years, the owner can continue to capture the depreciation on the building but that will not impact the 2.5% unadjusted basis number for the full 39 years of the depreciation period.

Any asset that was fully depreciated prior to 2018, unless it was placed in service after 2008, will not count toward the basis.

Shareholders or partners may only take into consideration for purposes of applying the limitation 2.5% his or her allocable share of the basis of the property. So if the total basis of commercial property is $1,000,000 and you are a 20% owner, you basis limitation is $1,000,000 x 20% x 2.5% = $5,000

Phase-In Of The Threshold

The questions I usually get next is: "If I'm married and our total taxable income is $320,000 which is only $5,000 over the threshold, do I automatically have to use the more complex calculation?" The special calculation "phases in" over the following total taxable income thresholds:Single filers: $157,500 - $207,500Married filing joint: $315,000 - $415,000I won't get into the special phase-in calculation because it's more complex than the special "above the income threshold" calculation that we already walked through but just know that it will be a blend of the straight 20% deduction and the W-2 & 2.5% adjusted basis calculation.

Qualified Trade or Business Requirement

In August 2018, the IRS came out with further clarification of how the QBI deduction would apply to real estate. In order to qualify for the QBI deduction for real estate income, your real estate holdings have to qualify as a "trade or business". The definition of a trade or business for QBI purposes deviates slightly from the traditional IRS definition. There is a safe harbor that states if you spend more than 250 hours a year working on that business it will qualify for the deduction.There are a few items to consider in the 250 hour calculation. So called "drive bys" where the owner is spending time driving by their properties to check on them does not count toward the 250 hours. If you have a property management company, the hours that they spend managing your propoerty can be credited toward your 250 hour requirement. However, the property management company has to provide you with proper documentation to qualify for those credited hours.

Consult Your Accountant

I'm a Certified Financial Planner®, not an accountant. I wrote this article to give real estate investors a broad view of what tax reform may have instore for them in 2018. If you own rental property, you should be actively consulting with our accountant through the year. As the IRS continues to release guidance regarding the QBI deduction throughout 2018, you will want to make sure that your real estate holdings are positioned properly to take full advantage of the new tax rules.

About Michael.........

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Tax Reform Could Lead To A Spike In The Divorce Rate In 2018

The Tax Cut & Jobs Act that was recently passed has already caused taxpayers to accelerate certain financial decisions as we transition from the current tax laws to the new tax laws over the course of the next two years.

The Tax Cut & Jobs Act that was recently passed has already caused taxpayers to accelerate certain financial decisions as we transition from the current tax laws to the new tax laws over the course of the next two years.

Current Tax Law: Alimony Is Tax Deductible

Under the current tax law, alimony payments are taxable income to the ex-spouse receiving the payments and they are tax deductible to the ex-spouse making the payments. When alimony is awarded pursuant to a divorce, it’s typically because there was a disparity in the level of income between the two spouses during the marriage. The ex-spouse paying the alimony, in most cases, is the higher income earning spouse both before and after the divorce finalized.

Let’s look at this in a real life example. Jim and Sarah have decided to get a divorce. Jim makes $300,000 per year and Sarah is a homemaker with $0 income. Pursuant to the divorce agreement, Jim will be required to pay Sarah $50,000 per year for 5 years. Jim will be able to deduct the $50,000 each year against his taxable income and Sarah will claim the $50,000 as taxable income on her tax return. Based on the 2018 Individual Tax Brackets, the top end of Jim’s income is in the 35% tax bracket. Thus, paying $50,000 in alimony really results in an “after-tax” expense to Jim of $32,500.

$50,000 x 35% = $17,500 (fed tax savings)

$50,000 – $17,500 = $32,500 (after tax expense to Jim)

Sarah will claim that $50,000 in alimony payments as income and let’s assume that the alimony payments are her only income for the year. Next year, as a single filer, Sarah will receive a standard deduction of $12,000, and the remainder of the $38,000 will be taxed at a blend of her 10% & 12% tax rate. As a result, Sarah will only pay about $4,400 in taxes on the $50,000 in alimony income.

To sum it all up, if the $50,000 is taxed to Sarah, approximately $4,400 will be paid to the IRS in taxes and she nets $45,600 in after tax income. However, if Jim was not able to deduct the alimony payments and had to pay tax on that $50,000, he would first have to pay the $17,500 in taxes to the IRS, and then he would hand Sarah a check for $32,500 after tax. Sarah is worse off because she received less after tax income. Jim would ultimately be worse off because he would need to part with more pre-tax income to create the same after tax benefit for Sarah. The IRS is the only one that wins.

Gaming The System

Since divorce agreements, in most states, are not required to adhere to predefined calculations for splitting assets, alimony payments, and in some cases child support, the tax game can be played when there is a high income earning spouse and alimony payments in the mix. In exchange for fewer assets or less child support, some divorce agreements have purposefully shifted more to alimony. The ex-spouse with the big income gets a bigger tax deduction and the ex-spouse receiving the alimony payment is able to take full advantage of their lower tax brackets and maximize their after tax income.

Alimony Is No Longer Deductible

To stop the tax game, included in the new tax bill was a provision that specifically states that alimony payments will no longer be deductible by the payor, nor reportable as income by the recipient, for divorce agreements signed after December 31, 2018.

The good news is this will not impact the ability to deduct alimony payments for divorce agreements that are currently in place. The bad news is for divorce agreements signed after December 31, 2018, the high income earner will no longer be able to deduct the alimony payments. That eliminates the tax arbitrage that has been used in the past to make the pie larger for both spouses. In general, if you shrink the size of the asset and income pie, it leaves more to fight about because each spouse is trying to preserve their standard of living as much as possible post-divorce.

For couples that have been sitting on the fence about getting divorced, this could be the catalyst to start the process in 2018 to make sure they have a signed agreement prior to December 31, 2018.

About Michael.........

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

How Pass-Through Income Will Be Taxed For Small Business Owners

While one of the most significant changes incorporated in the new legislation was reducing the corporate tax rate from the current 35% rate to a 21% rate in 2018, the tax bill also contains a big tax break for small business owners. Unlike large corporations that are taxed at a flat rate, most small businesses, are "pass-through" entities, meaning that the

While one of the most significant changes incorporated in the new legislation was reducing the corporate tax rate from the current 35% rate to a 21% rate in 2018, the tax bill also contains a big tax break for small business owners. Unlike large corporations that are taxed at a flat rate, most small businesses, are "pass-through" entities, meaning that the profits from the business flow through to the business owner's personal tax return and then are taxed at ordinary income tax rates.While pass-through income will continue to be taxed at ordinary income tax rates, many small business owners will be eligible to deduct 20% of their "qualified business income" (QBI) starting in 2018. In other words, some pass-through entities will only be taxes on 80% of their pass-through income.

Pass-through entities include

Sole proprietorships

Partnerships

LLCs

S-Corps

Unanswered Questions

I wanted to write this article to give our readers the framework of what we know at this point about the treatment of the pass-through income in 2018. However, as many accountants will acknowledge, there seems to be more questions at this point then there are answers. The IRS will need to begin issuing guidance at the beginning of 2018 to clear up many of the unanswered questions as to who will be eligible and not eligible for the new 20% deduction.

Above or Below "The Line"

This 20% deduction will be a below-the-line deduction which is an important piece to understand. Tax lingo makes my head spin as well, so let's pause for a second to understand the difference between an "above-the-line deduction" and a "below-the-line deduction".The "line" refers to the AGI line on your tax return which is the bottom line on the first page of your Form 1040. While both above-the-line and below-the-line deductions reduce your taxable income, it's important to understand the difference between the two.

Above-The-Line Deductions

Above-the-line deductions happen on the first page of your tax return. These deductions reduce your gross income to eventually reach your AGI (adjusted gross income) for the year. Above-the-line deductions include:

Contributions to health savings accounts

Contributions to retirement plans

Deduction for one-half of the self-employment taxes

Health insurance premiums paid

Alimony paid, student loan interest, and a few others

The AGI is important because the AGI is used to determine your eligibility for certain tax credits and it will also have an impact on which below-the-line deductions you are eligible for. In general, the lower your AGI is, the more deductions and credits you are eligible to receive.

Below-The-Line Deductions

Below-the-line deductions are reported on lines that come after the AGI calculation. They are comprised mainly of your “standard deduction” or “itemized deductions” and “personal exemptions” (most of which will be gone starting in 2018). The 20% deduction for qualified business income will fall into this below-the-line category. It will lower the income of small business owners but it will not lower their AGI.

However, it was stated in the tax legislation that even though the 20% qualified business deduction will be a below –the-line deduction it will not be considered an “itemized deduction”. This is a huge win!!! Why? If it’s not an itemized deduction, then small business owners can claim the 20% qualified business income deduction and still claim the standard deduction. This is an important note because many small business owners may end up taking the standard deduction for the first time in 2018 due to all of the deductions and tax exemptions that were eliminated in the new tax bill. The tax bill took away a lot of big deductions:

Capped state and local taxes at $10,000 (this includes state income taxes and property taxes)

Eliminated personal exemptions ($4,050 for each individual) (Eliminated in 2018)

Family of 4 = $4,050 x 4 = $16,200 (Eliminated in 2018)

Miscellaneous itemized deductions subject to 2% of AGI floor (Eliminated in 2018)

Restrictions On The 20% Deduction

If life were easy, you could just assume that I'm a sole proprietor, I make $100,000 all in pass-through income, so I will get a $20,000 deduction and only have to pay tax on $80,000 of my income. For many small business owners it may be that easy but what's a tax law without a list of restrictions.The restriction were put in place to prevent business owners from reclassifying their W2 wages into 100% pass-through income to take advantage of the 20% deduction . They also wanted to restrict employees from leaving their company as a W2 employee, starting a sole proprietorship, and entering into a sub-contractor relationship with their old employer just to reclassify their W2 wages into 100% pass-through income.

S-Corps

Qualified business income will specifically exclude "reasonable compensation" paid to the owner-employee of an S-corp. While it would seem like an obvious reaction by S-corp owners to reduce their W2 wages in 2018 to create more pass through income, they will still have to adhere to the "reasonable compensation" restriction that exists today.

Partnerships & LLCs

Qualified business income will specifically exclude guaranteed payments associated with partnerships and LLCs. This creates a grey area for these entities. Partnerships do not have a “reasonable compensation” requirement like S-corps since companies taxed as partnerships are not allowed to pay W2 wages to the owners. Also the owners of partnerships are not required to take guaranteed payments. My guess is, and this is only a guess, that as we get further into 2018, the IRS may require partnerships to classify a percentage of a owners total compensation as a “guaranteed payment” similar to the “reasonable compensation” restriction that S-corps currently adhere too. Otherwise, partnerships can voluntarily eliminate guaranteed payments and take the 20% deduction on 100% of the pass-through income.

This may also prompt some S-corps to look at changing their structure to a partnership or LLC. For high income earners, S-corps have an advantage over the partnership structure in that the owners do not pay self-employment tax on the pass-through income that is distribution to the owner over and above their W2 wages. However, S-corp owners will have to weigh the self-employment tax benefit against the option of changing their corporate structure to a partnership and potentially receiving a 20% deduction on 100% of their income.

Sole Proprietors

Sole proprietors do not have "reasonable compensation" requirement or "guaranteed payments" so it would seem that 100% of the income generated by sole proprietors will count as qualified business income. Unless the IRS decides to enact a "reasonable compensation" requirement for sole proprietors in 2018, similar to S-corps. Before everyone runs from a single member LLC to a sole proprietorship, remember, a sole proprietorship offers no liability barrier between the owner and liabilities that could arise from the business.

Income Restrictions

There are limits that are imposed on the 20% deduction based on how much the owner makes in “taxable income”. The thresholds are set at the following amounts:

Individual: $157,500

Married: $315,000

The thresholds are based on each business owner’s income level, not on the total taxable income of the business. We need help from the IRS to better define what is considered “taxable income” for purposes of this phase out threshold. As of right now, it seems that “taxable income” will be defined as the taxpayer’s own taxable income (not AGI) less deductions.

If the owner’s taxable income is below this threshold, then the calculation is a simple 20% deduction of the pass-through income. If the owner’s taxable income exceeds the threshold, the qualified business deduction is calculated as follows:

The LESSER of:

20% of its business income OR 50% of the total wages paid by the business to its employees

Let’s look at this in a real life situation. A manufacturing company has a net profit of $2M in 2018 and pays $500,000 in wages to its employees during the year. That company would only be able to take the qualified business income deduction for $250,000 since 50% of the total employee wages ($500,000 x 50% = $250,000) are less than 20% of the net income of the business ($2M x 20% = $400,000).

This creates another grey area because it seems that the additional calculation is triggered by the taxable income of each individual owner but the calculation is based on the total profitability and wages paid by the company. For the owners that required this special calculation for exceeding the threshold, how is their portion of the lower deduction amount allocated? Multiplying the lower total deduction amount by the percent of their ownership? Just more unanswered questions.:

Restrictions For "Service Business"

There will be restrictions on the 20% deduction for pass-through entities that are considered a "service business" under IRC Section 1202(e)(3)(A). The businesses specifically included in this definition as a services business are:

Health

Law

Accounting

Actuarial Sciences

Performing Arts

Consulting

Athletics

Financial Services

Any other trade or business where the principal asset of the business is the reputation or skill of 1 or more of its employees

In a last minute change to the regulations, to their favor, engineers and architects were excluded from the definition of “service businesses”.

This is another grey area. Many small businesses that fall outside of the categories listed above will undoubtedly be asking the question: “Am I considered a service business or not?” Outside of the industries specifically listed in the tax bill, we really need more guidance from the IRS.

If you are a “services business”, when the tax reform was being negotiated it looked like service businesses were going to be completely excluded from the 20% deduction. However, the final regulations were more kind and instead implemented a phase out of the 20% deduction for owners of service businesses over a specified income threshold. The restriction will only apply to those whose “taxable income” exceeds the following thresholds:

Individual: $157,500

Married: $315,000

If you are a consultant or owner of a services business and your taxable income is below these thresholds, it would seem at this point that you will be able to capture the 20% deduction for your pass-through income. As mentioned above, we need help from the IRS to clarify the definition of “taxable income”.

Phase Out For Service Businesses

The amounts listed above: $157,500 for individual and $315,000 for a married couple filing joint, are where the thresholds for the phase out begins. The service business owners whose income rises above those thresholds will phase out of the 20% deduction over the next $50,000 of taxable income for individual filers and $100,000 of taxable income for married filing joint. This means that the 20% pass-through deduction is completely gone by the following income levels:

Individual: $207,500

Married: $415,000

Any taxpayer’s falling in between the threshold and the phase out limit will receive a portion of the 20% deduction.

Since the thresholds are assessed based on the taxpayer’s own taxable income and not the total income of the business, a service business could be in a situation, like in an accounting firm, where the partners with the largest ownership percentage may not qualify for 20% deduction but the younger partners may qualify for the deduction because their income is lower.

Tax Planning For 2018

It's an understatement to say that most small business owners will need to spend a lot of time with their accountant in the first quarter of 2018 to determine the best of course of action for their company and their personal tax situation.While we are still waiting for clarification on a number of very important items associated with the 20% deduction for qualified business income, hopefully this article has provided our small business owners with a preview of things to come in 2018.

Disclosure: I'm a Certified Financial Planner® but not an accountant. The information contained in this article was generated from hours and hours of personal research on the topic. I advise each of our readers to consult with your personal tax advisor for tax advice.

About Michael.........

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Who Pays The Tax On A Cash Gift?

This question comes up a lot when a parent makes a cash gift to a child or when a grandparent gifts to a grandchild. When you make a cash gift to someone else, who pays the tax on that gift? The short answer is “typically no one does”. Each individual has a federal “lifetime gift tax exclusion” of $5,400,000 which means that I would have to give

This question comes up a lot when a parent makes a cash gift to a child or when a grandparent gifts to a grandchild. When you make a cash gift to someone else, who pays the tax on that gift? The short answer is “typically no one does”. Each individual has a federal “lifetime gift tax exclusion” of $15,000,000 which means that I would have to give away $15 million dollars before I would owe “gift tax” on a gift. For married couples, they each have a $15,000,000 dollar exclusion so they would have to gift away $30,000,000 before they would owe any gift tax. When a gift is made, the person making the gift does not pay tax and the person receiving the gift does not pay tax below those lifetime thresholds.

“But I thought you could only gift $19,000 per year per person?” The $19,000 per year amount is the IRS “gift exclusion amount” not the “limit”. You can gift $19,000 per year to any number of people and it will not count toward your $15,000,000 lifetime exclusion amount. A married couple can gift $38,000 per year to any one person and it will not count toward their $30,000,000 million lifetime exclusion. If you do not plan on making gifts above your lifetime threshold amount you do not have to worry about anyone paying taxes on your cash gifts.

Let’s look at an example. I’m married and I decide to gift $20,000 to each of my three children. When I make that gift of $60,000 ($20K x 3) I do not owe tax on that gift and my kids do not owe tax on the gift. Also, that $60,000 does not count toward my lifetime exclusion amount because it’s under the $38,000 annual exclusion for a married couple to each child.

In the next example, I’m single and I gift $1,000,000 my neighbor. I do not owe tax on that gift and my neighbor does not owe any tax on the gift because it is below my $15,000,000 threshold. However, since I made a gift to one person in excess of my $19,000 annual exclusion, I do have to file a gift tax return when I file my taxes that year acknowledging that I made a gift $981,000 in excess of my annual exclusion. This is how the IRS tracks the gift amounts that count against my $15,000,000 lifetime exclusion.

Important note: This article speaks to the federal tax liability on gifts. If you live in a state that has state income tax, your state’s gift tax exclusion limits may vary from the federal limits.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Last updated June, 2026