Tax-Free Tips and Overtime: What the Big Beautiful Tax Bill Means for Workers

The Big Beautiful Tax Bill introduced two worker-friendly provisions aimed at boosting take-home pay: tax-free tips and tax-free overtime pay.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

The Big Beautiful Tax Bill introduced two worker-friendly provisions aimed at boosting take-home pay: tax-free tips and tax-free overtime pay.

Starting in 2025, many employees in service-based and hourly industries will see a new opportunity to earn more without increasing their federal tax bill. But before you get too excited, there are income phaseouts that limit the benefit for higher earners, and both provisions are temporary—ending in 2028.

Let’s break down how each works, who qualifies, and how you might use this limited-time tax relief to your advantage.

Tax-Free Tips (2025–2028)

Under the new law, cash and electronic tips earned by employees will be excluded from federal income tax starting in 2025. This means waitstaff, bartenders, valets, and other tipped workers can keep more of their tips without paying federal income tax on that income.

Key Details:

Up to $25,000 of qualified tip income is deductible

Applies to all reported tips, including cash, credit card, and digital payment platforms (like Venmo or Square).

Employers are still required to track and report tip income, but it won’t count toward federal taxable wages.

FICA (Social Security and Medicare taxes) still apply to tips unless further guidance says otherwise.

Income Phaseouts for Tax-Free Tips

The benefit is phased out for higher earners. Once your income reaches a certain threshold, the tax-free status begins to shrink—and disappears entirely once fully phased out. The $25,000 deduction amount is reduced by $100 for each $1,000 of modified AGI over $150,000 for single filers and $300,000 for joint filers.

If you’re within the phaseout range, the portion of your tips that are tax-free decreases gradually until it reaches zero.

Tax-Free Overtime Pay (2025–2028)

In a rare move to incentivize additional work hours, the bill also makes overtime pay exempt from federal income tax from 2025 through 2028. This applies to time-and-a-half wages earned beyond 40 hours per week.

Key Details:

Up to $12,500 ($25,000 joint) of qualified overtime compensation is deductible

Applies to hourly workers eligible for overtime under the Fair Labor Standards Act.

Only the premium portion of overtime (typically the 1.5x wage rate) is tax-free. The base rate is still taxable.

Overtime must be properly documented on pay stubs or employer payroll systems.

Income Phaseouts for Tax-Free Overtime

As with tax-free tips, this benefit is designed to help middle-income earners and begins to phase out at higher income levels. The phaseout calculation is the same as the tips deduction, the $12,500 deduction is reduced by $100 for each $1,000 of modified AGI over $150,000 (single) and $300,000 (joint).

If your income falls within the range, only a portion of your overtime premium pay will be excluded from taxes. Above the threshold, none of the overtime qualifies for the exemption.

Could Employers Shift Salaried Workers to Hourly?

One of the more interesting (and perhaps unintended) consequences of the tax-free tips and overtime provisions is that it may incentivize employers to reclassify certain employees from salaried to hourly.

Here’s why:

Only hourly workers are eligible for tax-free overtime under the new law.

Salaried employees—particularly those exempt from overtime rules—don’t benefit at all from this provision.

Employers looking to attract and retain workers in a competitive labor market may consider restructuring compensation models to help employees take advantage of the new tax savings.

For example, a business might:

Reclassify a lower-level manager from salary to hourly, allowing them to earn overtime that’s now tax-free.

Shift part of a base salary into a tip-eligible role (such as hybrid front-of-house service positions) to access the tax-free tip benefit.

Of course, this type of reclassification must be done carefully to remain compliant with wage and hour laws, and may not be appropriate in every industry. But in sectors like hospitality, healthcare, retail, and logistics, this kind of shift could become more common—particularly as employees become more aware of the tax advantages.

Planning Considerations

These two provisions present real planning opportunities for wage earners, especially those working in hospitality, retail, healthcare, and skilled trades.

1. Stack Your Hours Smartly

For hourly workers who are near the phaseout thresholds, it may make sense to shift hours into lower-income years to maximize the benefit.

2. Watch for Unintended Phaseout Triggers

Bonuses, side gigs, or spousal income could push you into the phaseout range and reduce or eliminate your tax-free eligibility. Tax planning with a professional can help you anticipate this.

3. Use the Extra Take-Home Pay Wisely

Since these benefits are temporary (expiring at the end of 2028), consider putting the extra income to work:

Pay down high-interest debt

Build your emergency fund

Contribute more to retirement or a Roth IRA

Save for large purchases without relying on credit

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What are the new tax-free tip and overtime provisions under the Big Beautiful Tax Bill?

Starting in 2025 and lasting through 2028, workers can exclude certain tip income and overtime pay from federal income tax. Up to $25,000 in tips and up to $12,500 ($25,000 for joint filers) in overtime pay may qualify each year, subject to income limits.

Who qualifies for the tax-free tip provision?

Hourly and service-based workers who earn tips—such as restaurant servers, bartenders, or valets—can exclude up to $25,000 of reported tip income from federal income tax. The deduction phases out for single filers with income above $150,000 and joint filers above $300,000.

How does the tax-free overtime pay rule work?

Hourly employees eligible for overtime under the Fair Labor Standards Act can exclude the “premium” portion of overtime pay (the extra half-time pay above their base rate) from federal income tax. The same income phaseouts apply as for tips.

Do workers still pay Social Security and Medicare taxes on tax-free tips and overtime?

Yes. Even though the new law exempts certain tips and overtime from federal income tax, FICA taxes (Social Security and Medicare) still apply unless further IRS guidance states otherwise.

Will salaried employees benefit from the new provisions?

No. Only hourly workers qualify for the tax-free overtime benefit. Some employers may consider reclassifying certain employees as hourly to allow them to take advantage, but any reclassification must comply with labor laws.

How long do the tax-free tip and overtime benefits last?

Both provisions are temporary. They take effect in 2025 and are scheduled to expire at the end of 2028 unless Congress extends them.

What should workers do with the extra take-home pay?

Since the benefits are short-term, consider using the additional after-tax income to pay down high-interest debt, build savings, or contribute to retirement accounts. A financial professional can help you plan the most effective use of the extra cash flow.

Big Beautiful Tax Bill Overhauls Student Loan Repayment Options: End of the SAVE Program

The Big Beautiful Tax Bill has made headlines for reshaping major areas of the tax code but buried within the legislation is a sweeping overhaul of the federal student loan system, which will have long-term implications for both current and future borrowers.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

The Big Beautiful Tax Bill has made headlines for reshaping major areas of the tax code but buried within the legislation is a sweeping overhaul of the federal student loan system, which will have long-term implications for both current and future borrowers.

If you—or your children—have federal student loans or plan to take them out, here’s what you need to know about repayment plans, loan forgiveness, and graduate borrowing limits as we head toward a new era in federal student aid.

Starting in 2026: Only Two Main Repayment Options

One of the biggest shifts takes effect in July 2026, when the federal government will consolidate most repayment options into just two primary plans for new borrowers:

1. Standard Repayment Plan

Fixed monthly payments over 10 years

Similar to current standard plans

Ideal for borrowers with stable income who want to eliminate debt quickly

2. Repayment Assistance Plan (RAP)

Monthly payments based on income and family size

Forgiveness available after 20–30 years, depending on the loan type

Unpaid interest does not capitalize annually, but continues to accrue

While the RAP offers more flexibility, it comes with a longer repayment horizon. This model mirrors existing income-driven plans, but with stricter forgiveness timelines and reduced subsidies over time.

Existing Income-Driven Repayment Plans Will Be Phased Out

The bill also mandates the sunset of current income-driven repayment (IDR) plans such as IBR, PAYE, REPAYE, and even the more recently introduced SAVE plan (discussed later).

Borrowers currently enrolled in these programs will have a transition period until 2028 to switch into the new Repayment Assistance Plan (RAP). After that date:

New enrollment in existing IDR plans will be closed

Borrowers will need to opt into RAP or move into the standard plan

Previously accrued progress toward forgiveness may carry over, depending on guidance from the Department of Education (still pending)

Borrowers currently on track for loan forgiveness in an existing plan should carefully review how the transition may affect their timelines.

Graduate Borrowers Face New Loan Caps

Graduate and professional students—who often rely on federal student loans to cover the full cost of attendance—are facing new borrowing limits:

New Federal Caps for Graduate Borrowers (Effective 2026):

$100,000 lifetime maximum for most graduate and professional programs

Applies across all federal programs, including Graduate PLUS

Borrowers may need to seek private loans or employer aid to cover costs beyond the cap

This is a dramatic departure from current rules, which allow grad students to borrow up to the full cost of attendance—including tuition, housing, and living expenses. Under the new system, graduate students will be expected to budget more conservatively or explore alternative financing.

Changes to the SAVE Program

The Saving on a Valuable Education (SAVE) plan, introduced in 2023 as a more generous income-driven repayment option, is also on the chopping block.

According to the Trump administration, the SAVE plan will:

As of August 1, 2025, interest will begin accruing again for SAVE plan borrowers, even though they may still be in forbearance

The SAVE Program will be eliminated by June 30, 2028, and borrowers will be moved into a new income-driven repayment plan called RAP.

Lose features such as interest subsidies and lowered income thresholds for $0 monthly payments

For many, this means monthly payments could increase significantly once the SAVE subsidies disappear. Borrowers may also need to recalculate their budgets as interest builds up again and full payments resume.

If you're enrolled in SAVE, expect updates from your servicer in late 2025 outlining your transition options.

Forgiveness Becomes Taxable Again After 2025

One of the more overlooked but financially critical changes in the bill relates to taxation of forgiven student loan balances.

Currently, through the end of 2025, student loan forgiveness—whether through IDR, PSLF, or closed school discharge—is not considered taxable income at the federal level. That exclusion is set to expire.

Starting January 1, 2026, any federal student loan balance that is forgiven will be treated as taxable income by the IRS. This change has major implications for borrowers expecting loan forgiveness in the next 5–10 years.

Example: If $100,000 in student loans is forgiven in 2026, the borrower may owe federal taxes on that full amount—potentially triggering a $20,000+ tax bill depending on their bracket.

Borrowers approaching forgiveness in IDR plans may want to accelerate their timelines, if possible, or start preparing for a potential future tax liability.

Final Thoughts

The student loan system has been gradually shifting over the last few years, but the Big Beautiful Tax Bill accelerates those changes in a way that will permanently reshape how future generations borrow and repay federal loans.

Whether you're a current borrower navigating the SAVE sunset, a parent helping a graduate student manage new loan caps, or someone on track for forgiveness after 2025, proactive planning will be essential. Understanding the timing, tax implications, and repayment structures will help you avoid financial surprises in the years ahead.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

What major changes does the Big Beautiful Tax Bill make to federal student loans?

Beginning in 2026, the law consolidates most federal student loan repayment options into two main plans—the Standard Repayment Plan and a new Repayment Assistance Plan (RAP). It also caps graduate borrowing at $100,000 and makes forgiven loan balances taxable again starting in 2026.

What are the two new repayment options starting in 2026?

Borrowers can choose between a 10-year Standard Repayment Plan with fixed payments or the new Repayment Assistance Plan (RAP), which bases payments on income and family size. The RAP offers forgiveness after 20–30 years, depending on loan type, but limits interest subsidies compared to current programs.

What happens to existing income-driven repayment (IDR) plans like SAVE, PAYE, or REPAYE?

These programs will be phased out by 2028. Borrowers currently enrolled in them can stay until the transition period ends but will eventually need to move into the new RAP or Standard Plan. Progress toward forgiveness may carry over, though official guidance is still pending.

How does the new law affect graduate and professional borrowers?

Starting in 2026, graduate students will face a $100,000 lifetime borrowing cap across all federal loan programs, including Graduate PLUS. Those who need additional funds may have to rely on private loans, scholarships, or employer tuition assistance.

What happens to the SAVE repayment plan under the new law?

The SAVE plan will begin phasing out in 2025 and be fully eliminated by June 30, 2028. Borrowers will lose features such as interest subsidies and lower payment thresholds. They will be moved automatically into the new RAP once SAVE ends.

Will student loan forgiveness be taxable again?

Yes. Starting January 1, 2026, any federal student loan balance that is forgiven—through income-driven repayment, PSLF, or other discharge programs—will once again be treated as taxable income by the IRS. Borrowers expecting forgiveness soon should prepare for potential tax liability.

How should borrowers prepare for these changes?

Review your repayment plan, understand your eligibility under the new RAP, and talk to a financial or tax advisor about potential tax implications. If you’re approaching forgiveness before 2026, accelerating repayment or adjusting your timeline may reduce future tax exposure.

Residential Solar Tax Credit Eliminated Under the Big Beautiful Tax Bill: What It Means for Homeowners

The recently passed Big Beautiful Tax Bill made headlines for raising the federal estate tax exemption and increasing the SALT deduction cap, but not all of the provisions were taxpayer-friendly. One particularly significant change that’s flying under the radar is the elimination of the 30% Residential Solar Tax Credit—a program that’s been central to the rise in home solar installations over the past decade.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

The recently passed Big Beautiful Tax Bill made headlines for raising the federal estate tax exemption and increasing the SALT deduction cap, but not all of the provisions were taxpayer-friendly. One particularly significant change that’s flying under the radar is the elimination of the 30% Residential Solar Tax Credit—a program that’s been central to the rise in home solar installations over the past decade.

If you're a homeowner considering solar, you now have a deadline: install by December 31, 2025, or you’ll lose access to this valuable credit entirely. And the ripple effects could go well beyond individual tax savings.

Let’s break down what’s changing, what it means for homeowners and the energy grid, and how the solar industry may be reshaped by this policy shift.

What Is the Residential Solar Tax Credit?

The Residential Clean Energy Credit—commonly referred to as the 30% solar tax credit—allows homeowners to deduct 30% of the cost of installing solar panels, battery storage systems, and other qualifying equipment from their federal tax bill.

For example, if your solar installation costs $30,000, the credit could reduce your federal tax liability by $9,000. This credit has been one of the most effective incentives for encouraging adoption of clean energy at the residential level.

The Credit Is Going Away—Here’s the Timeline

Under the Big Beautiful Tax Bill, the federal solar tax credit is officially repealed for residential homeowners after December 31, 2025. Here’s what you need to know:

Installations must be fully complete and placed in service by December 31, 2025 to qualify for the 30% credit.

There is no phaseout—the credit simply ends.

The repeal applies to all residential installations, including solar panels, inverters, and eligible battery storage systems.

This means homeowners considering solar need to act quickly, as installations can take several months from contract to completion.

Higher Utility Bills on the Horizon?

The elimination of the solar credit could also have macro-level consequences. Here's why:

Fewer homeowners are likely to install solar once the credit expires, meaning less distributed generation contributing to local grids.

At the same time, electricity demand is rising sharply:

AI data centers are consuming massive amounts of power

More Americans are charging electric vehicles (EVs) at home

Electrification trends are increasing energy use in heating, cooking, and water systems

With less residential solar feeding energy back into the grid and more demand pulling from it, utility companies may need to invest in expensive infrastructure upgrades—costs that could ultimately be passed on to consumers in the form of higher utility bills.

In other words, the removal of the credit doesn’t just impact those who install solar—it could raise costs for those who don’t.

Solar Installation Industry Faces Uncertainty

The solar industry, which has grown rapidly in recent years, could face significant headwinds after the credit expiration. Many residential solar installers have built their business models around the financial appeal of the 30% tax credit.

Once that incentive disappears:

Residential demand is expected to drop sharply, especially among middle-income homeowners.

Smaller solar installation companies—which rely heavily on residential volume—could experience contraction, layoffs, or closures.

The market may shift focus to commercial-scale solar, battery backup systems, and states with additional local incentives—but that won't be enough to fully offset the change.

Consumers should be prepared for less pricing competition, longer wait times, and fewer installer options if demand falls off and the industry consolidates.

Final Thoughts: Should You Move Forward With Solar Now?

If you’re on the fence about going solar, the window to maximize your benefit is narrowing. Here's what you should consider:

Act soon: Begin the planning process now to ensure you can complete installation before year-end 2025.

Get quotes from multiple installers: With high demand expected before the credit expires, early planning can help avoid cost inflation and scheduling delays.

Run the numbers: Even without the credit, solar can make financial sense depending on your local utility rates, energy usage, and how long you plan to stay in your home. But with the credit? The payback period shortens considerably.

Summary

The 30% residential solar tax credit ends after December 31, 2025.

Homeowners must install and place systems in service before that date to claim the credit.

Fewer installations and higher energy demands could mean higher utility costs for everyone.

The solar installation industry may contract, affecting consumer pricing and service availability.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What is the 30% Residential Solar Tax Credit?

The Residential Clean Energy Credit allows homeowners to deduct 30% of the total cost of installing solar panels, inverters, battery storage, and related equipment from their federal tax bill. For example, a $30,000 system could reduce your tax liability by $9,000.

When does the solar tax credit expire?

Under the Big Beautiful Tax Bill, the federal residential solar tax credit ends after December 31, 2025. To qualify, systems must be fully installed and placed in service before that date. There is no phaseout—the credit simply disappears beginning in 2026.

Does the credit apply to battery storage systems?

Yes. The 30% credit covers qualifying home battery systems that store energy from solar panels or the electric grid. However, these installations must also be completed by the end of 2025 to qualify.

What happens if I install solar after 2025?

After December 31, 2025, there will be no federal tax credit for residential solar installations. Homeowners installing after that date will need to rely solely on any available state or utility-level incentives.

How could this change affect utility bills?

Without the federal incentive, fewer homeowners are expected to install solar panels. Combined with growing electricity demand from electric vehicles, AI data centers, and home electrification, utilities may face higher costs that could ultimately raise rates for all consumers.

How might the solar industry be impacted by the credit’s repeal?

Residential solar demand is expected to decline sharply after 2025. Smaller installation companies could face consolidation or closures, while consumers may see higher prices and longer wait times as the market contracts.

Should homeowners move forward with solar now?

If you’re considering solar, it’s best to act soon. Starting early ensures installation before the 2025 deadline and locks in the 30% tax credit. Even with strong local incentives, the loss of this federal benefit could significantly increase system payback times after 2025.

The New $6,000 Senior Tax Deduction Explained

The Big Beautiful Tax Bill that just passed is reshaping the tax landscape for many Americans, but one provision that stands out for retirees is the introduction of a new $6,000 senior tax deduction. This benefit, aimed at providing additional tax relief for older taxpayers, adds a generous layer of savings on top of the regular standard deduction and the existing age-based deduction.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

The Big Beautiful Tax Bill that just passed is reshaping the tax landscape for many Americans, but one provision that stands out for retirees is the introduction of a new $6,000 senior tax deduction. This benefit, aimed at providing additional tax relief for older taxpayers, adds a generous layer of savings on top of the regular standard deduction and the existing age-based deduction.

This new deduction took the place of the promised “100% tax-free social security benefits,” which was too costly to include in the new tax bill.

But as with many of the bill’s provisions, there are income limitations and expiration dates to be aware of. In this article, we break down how the deduction works, who qualifies, and how to make the most of it before it sunsets in 2028.

What Is the New $6,000 Senior Tax Deduction?

Beginning in 2025, taxpayers aged 65 or older will be eligible for a new $6,000 federal tax deduction. This deduction is designed to reduce taxable income and is stacked on top of the standard deduction and the existing senior (age-based) additional deduction.

In Addition to Existing Age 65 $2,000 Deduction

The new $6,000 Senior Deduction is in addition to both the standard deduction and the existing enhanced standard deduction from individual age 65 and older. The existing enhanced senior deduction for 2025 is $2,000 for single filers and head of household, and $1,600 per qualifying individual for married couples filing jointly or separately.

If both spouses are age 65 or older, they both qualify for the $6,000 Senior Deduction ($12,000 combined).

This deduction can result in significant tax savings, especially for retirees living on fixed incomes who may not qualify for other tax credits or deductions.

Income Phase-Out Rules

The deduction is not available to all seniors—there’s an income cap. The new deduction begins to phase out at moderate income levels:

How the Phase-Out Works

However, the deduction is gradually reduced—potentially to $0—if your Modified Adjusted Gross Income (MAGI) exceeds the applicable threshold. Once past that line:

The deduction is reduced by six cents for every $1 over the threshold.

At $175,000 MAGI for singles or $250,000 for joint filers, the deduction is fully phased out.

Example:

Let’s say you’re single and your MAGI is $100,000 in 2025:

That’s $25,000 over the $75,000 threshold.

Multiply that by $0.06:

$25,000 × $0.06 = $1,500 reductionResult:

$6,000 deduction − $1,500 = $4,500 allowable deduction

The reduction applies dollar-for-dollar across the entire overage range. The closer your MAGI is to the top of the phase-out range, the smaller your deduction becomes.

Planning Tip:

If you’re near the phaseout limit, consider deferring income (like IRA withdrawals or capital gains) or increasing deductions (such as HSA contributions or qualified charitable distributions) to stay under the threshold and preserve the full deduction.

When Does It Start (and End)?

This is a temporary provision of the tax code.

Effective Date: January 1, 2025

Expiration Date: December 31, 2028

That means taxpayers will be able to claim the deduction for four tax years (2025 through 2028), unless future legislation extends or makes the benefit permanent.

You Don’t Need to Itemize

One of the biggest benefits of this deduction is its accessibility. Unlike many tax breaks that require itemizing, the $6,000 senior deduction can be claimed even if you take the standard deduction—which most retirees already do.

This makes the deduction especially useful for seniors with:

Modest income from Social Security and pensions

Minimal mortgage interest or medical deductions

No longer itemizing after downsizing or paying off a home

Final Thoughts

The $6,000 senior deduction is a meaningful win for retirees—especially those living on fixed incomes who don’t itemize and have limited ways to reduce taxable income. When combined with the standard deduction and age-based additions, older taxpayers will be able to shelter a larger portion of their income from federal taxes for the 2025–2028 window.

As with any temporary tax benefit, timing and planning are key. Whether you're managing RMDs, structuring retirement income, or simply looking for ways to reduce your tax burden, this new deduction should be part of your strategy in the coming years.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What is the new $6,000 senior tax deduction?

Starting in 2025, taxpayers aged 65 and older can claim a new $6,000 federal tax deduction. It reduces taxable income in addition to the standard deduction and the existing age-based deduction. Married couples where both spouses are age 65 or older can claim $12,000 combined.

How does the new senior deduction interact with existing deductions?

The new deduction stacks on top of both the regular standard deduction. This layering can provide meaningful tax relief for retirees who do not itemize.

Who qualifies for the $6,000 senior deduction?

Any taxpayer who is age 65 or older by the end of the tax year qualifies. The deduction applies to all filing statuses but begins to phase out for higher-income individuals.

What are the income phaseout thresholds for the deduction?

The deduction begins to phase out at $75,000 of Modified Adjusted Gross Income (MAGI) for single filers and $125,000 for joint filers. It is reduced by six cents for every $1 of income above these levels and fully phases out at $175,000 for singles and $250,000 for joint filers.

Do you need to itemize to claim the senior deduction?

No. The $6,000 senior deduction is available even if you take the standard deduction. This makes it particularly beneficial for retirees with modest incomes or limited itemized deductions.

When does the new senior tax deduction take effect—and when does it end?

The deduction applies beginning January 1, 2025, and is set to expire after December 31, 2028, unless Congress extends or makes it permanent. Retirees will have four tax years (2025–2028) to take advantage of it.

How can retirees maximize this deduction before it phases out?

Seniors close to the income threshold can use tax planning strategies—such as deferring income, reducing Roth conversions or distributions from pre-tax retirement acounts, or using Qualified Charitable Distributions—to keep MAGI below the phaseout range and preserve the full deduction.

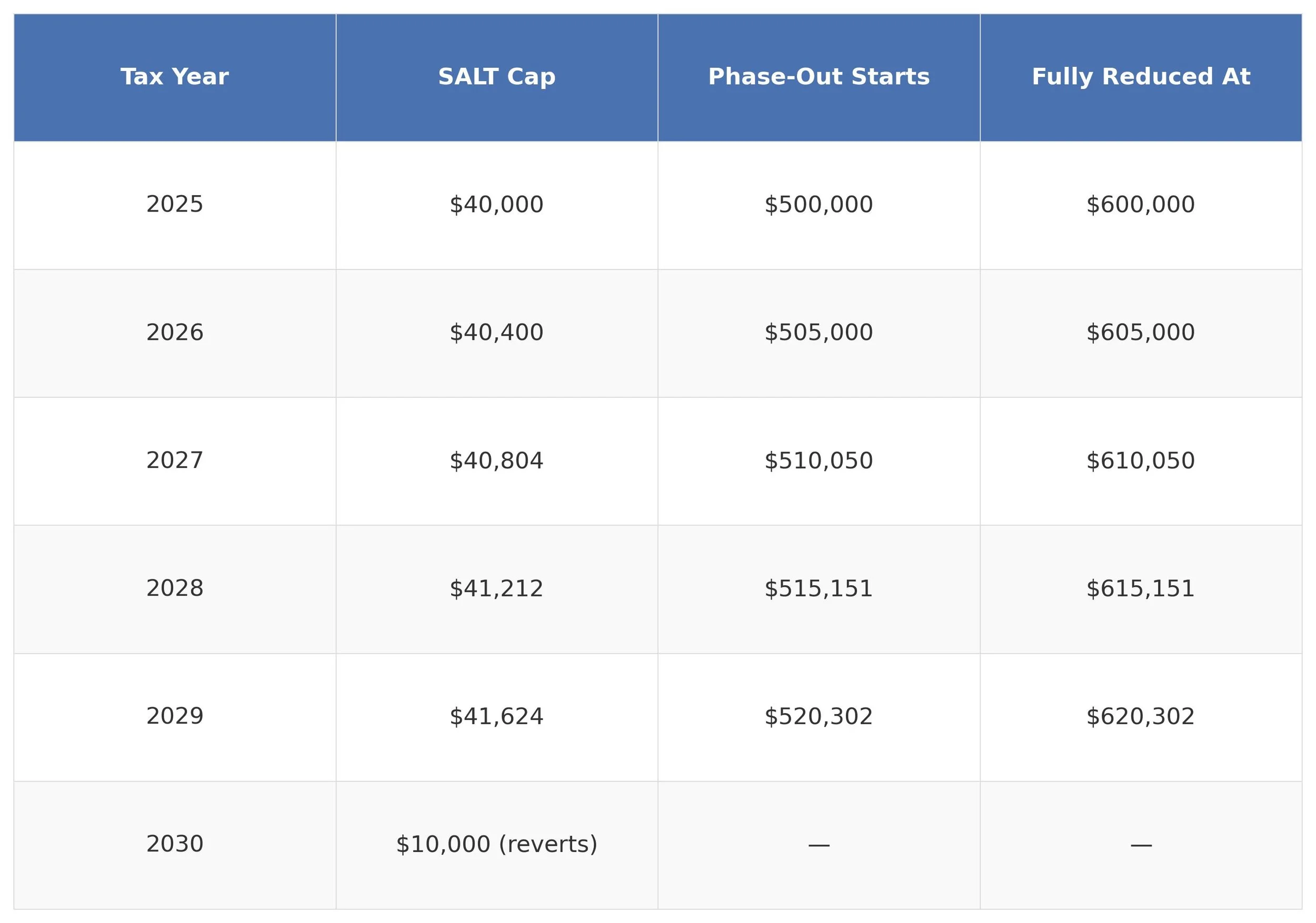

The New $40,000 SALT Cap: What It Means for Taxpayers After the Big Beautiful Tax Bill

Congress just passed the “Big Beautiful Tax Bill,” and one of the biggest changes is a major update to the SALT (State and Local Tax) deduction cap. Instead of being limited to $10,000, some taxpayers will now be eligible for a $40,000 SALT deduction — but only temporarily and only if certain income limits are met.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

After months of negotiation and political tug-of-war, Congress has officially passed what’s being dubbed the “Big Beautiful Tax Bill.” While the legislation covers a broad range of tax reforms, one of the most talked-about provisions is the dramatic change to the SALT (State and Local Tax) deduction cap—raising it from the current $10,000 to a new maximum of $40,000 for some taxpayers. If you’ve felt handcuffed by the old SALT limits, this update could provide much-needed relief—but the details matter.

In this article we will cover:

The effective date of the new $40,000 SALT Cap

Income limitations for single and joint filers

The SALT phaseout calculation

Who benefits the most from the higher SALT Cap?

Do you have to itemize to capture the new SALT Cap?

When the new $40,000 SALT Cap expires

Quick Refresher: What Is the SALT Deduction?

The SALT deduction allows taxpayers who itemize to deduct certain state and local taxes from their federal taxable income. This typically includes:

State and local income taxes

Property taxes paid on real estate

Under the 2017 Tax Cuts and Jobs Act (TCJA), this deduction was capped at $10,000, which hit high-tax states like New York, New Jersey, California, and Massachusetts especially hard. Many taxpayers in those states were no longer able to deduct their full property and income tax payments, resulting in higher federal tax bills.

What’s in the New Bill?

The Big Beautiful Tax Bill raises the SALT cap from $10,000 to $40,000, but with a few catches:

Income limitations apply

The increase applies only to tax years 2025 through 2029.

Starting in 2030, the cap reverts back to $10,000 (unless future legislation says otherwise).

You have to itemize to capture the SALT deduction

So, this is a temporary reprieve—but for many, a meaningful one.

Who Benefits Most?

This new SALT cap will be most beneficial to:

Homeowners in high-tax states (especially those with large property tax bills)

High-income earners who pay significant state income taxes

Taxpayers who itemize deductions (rather than taking the standard deduction)

If you're someone who was paying $25,000–$40,000 in combined state income and property taxes, this change could mean an additional $15,000–$30,000 in deductions, depending on your filing status.

That’s real money back in your pocket—especially if you're in a higher federal tax bracket.

Income Phase‑Outs: Who Gets How Much

While the new SALT cap jump to $40,000 is significant, its benefit isn't universal. There are income limitations for taxpayers based on their modified adjusted gross income.

For tax year 2025, the full SALT cap applies to filers with Modified AGI less than $500,000

MAGI between $500,000 and $600,000: The cap is reduced by 30% of the income over $500,000.

Above MAGI $600,000, the cap is back down to $10,000—the same as the old limit.

Starting in 2026, both the cap and phase-out threshold rise 1% per year, with the reductions continuing until 2029. The $10,000 ceiling returns permanently in 2030

How the Phase‑Out Plays Out

Note: The deduction cannot be reduced below the old $10,000

Does Your Tax Filing Status Matter

The MAGI income thresholds are based on “household income” so both single filers and married filing joint filers have the same income limitations and phaseout range for the new $40,000 SALT Cap. However, for taxpayers who file married filing separately, the new max SALT Cap is $20,000.

Tax Planning Opportunities

If you fall into the group of taxpayers who stand to benefit, here are some strategies to consider:

1. Bunching Deductions

With the cap going up temporarily, it may make sense to accelerate state tax payments or property tax prepayments into the eligible years (2025–2029) to maximize the benefit.

2. Reevaluating Itemized vs. Standard Deduction

Many filers defaulted to the standard deduction under TCJA because of the $10,000 SALT cap. But with the cap raised, it’s time to revisit whether itemizing now produces a better tax result.

3. Rethinking Income Timing

If you have control over how and when you recognize income (e.g., through bonuses, deferred comp, self-employment, or retirement distributions), you might explore ways to align higher-income years with the higher SALT cap window.

4. AMT Considerations

While not as widespread as in the past, the Alternative Minimum Tax (AMT) can still limit your ability to take advantage of certain deductions—including SALT. Make sure your tax preparer checks how the new cap interacts with AMT exposure.

Final Thoughts

The new $40,000 SALT cap is a welcome change for many taxpayers who have felt the squeeze over the past few years. But it’s a temporary window of opportunity, and one that requires careful planning to take full advantage of.

If you live in a high-tax state, this change could have a significant impact on your tax strategy moving forward. As always, consult with your financial planner or tax advisor to determine how these changes fit into your overall financial picture.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What is the new $40,000 SALT deduction cap?

Under the Big Beautiful Tax Bill, the State and Local Tax (SALT) deduction cap increases from $10,000 to $40,000 for eligible taxpayers beginning in 2025. The expanded cap applies to combined state income and property taxes but is temporary—set to expire after 2029.

Who benefits most from the higher SALT cap?

The change primarily benefits homeowners and high-income earners in high-tax states such as New York, New Jersey, California, and Massachusetts. Those who pay substantial property and state income taxes and who itemize deductions stand to gain the most.

When does the new $40,000 SALT cap take effect—and when does it expire?

The increased cap is effective for tax years 2025 through 2029. Beginning in 2030, the cap reverts to the previous $10,000 limit unless new legislation extends it.

Are there income limits for the new SALT deduction?

Yes. The full $40,000 cap applies to taxpayers with Modified Adjusted Gross Income (MAGI) under $500,000. Between $500,000 and $600,000, the cap is reduced by 30% of the income over $500,000. Above $600,000 MAGI, the deduction returns to the old $10,000 limit.

Do you need to itemize to use the $40,000 SALT deduction?

Yes. The SALT deduction is only available to taxpayers who itemize deductions on their federal tax return. If you claim the standard deduction, you cannot take advantage of the higher SALT cap.

What tax strategies can help maximize the new SALT deduction?

Taxpayers can “bunch” property or state tax payments into the eligible years (2025–2029), reevaluate whether to itemize, and time income recognition to align with the higher cap window. Consulting a tax professional can help optimize these strategies within IRS guidelines.

Will the Alternative Minimum Tax (AMT) affect the SALT deduction?

It might. The AMT can limit or disallow SALT deductions, depending on your income level and deductions. Taxpayers subject to AMT should review how the new cap interacts with their overall tax situation.

PTET Survives: Why This Pass-Through Entity Tax Loophole Still Matters After Passing of the Big Beautiful Tax Bill

There was a lot of buzz surrounding the “Big Beautiful Tax Bill” recently signed into law, and while most headlines focused on the new $40,000 SALT deduction cap, a quieter but equally important victory came in the form of what didn’t make it into the final bill for the business owners of pass-through entities.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

There was a lot of buzz surrounding the “Big Beautiful Tax Bill” recently signed into law, and while most headlines focused on the new $40,000 SALT deduction cap, a quieter but equally important victory came in the form of what didn’t make it into the final bill for the business owners of pass-through entities.

One major provision originally tucked into the House version of the bill would have eliminated the PTET (Pass-Through Entity Tax) workaround—a popular strategy business owners have been using to bypass the federal $10,000 SALT deduction cap. Thankfully, the Senate stripped that provision from the final legislation, meaning PTET is here to stay—at least for now.

This article will walk through what PTET is, why it still matters (even with a $40,000 cap), and how business owners should think about it in light of the latest tax reform.

What Is PTET?

The Pass-Through Entity Tax (PTET) is a state-level workaround created in response to the federal $10,000 SALT deduction cap introduced under the 2017 Tax Cuts and Jobs Act. Since pass-through entities like S corporations and partnerships don’t pay federal income tax directly, owners report their share of the business income on their personal returns—and thus, their state taxes on that income were limited by the $10,000 SALT cap.

States like New York, New Jersey, California, and over 30 others adopted PTET programs, allowing these businesses to elect to pay state income tax at the entity level. Because entity-level taxes are fully deductible at the federal level, this approach effectively restores the lost deduction for many business owners.

PTET has become one of the most powerful tools for state tax planning, and in many cases, saves owners thousands—or even tens of thousands—of dollars in federal tax liability.

What the House Tried to Do—and What the Senate Undid

In the original House version of the Big Beautiful Tax Bill, lawmakers proposed to eliminate the PTET workaround starting in 2025, citing the new $40,000 SALT cap as sufficient relief. The rationale was that, with a higher cap on SALT deductions, there was no longer a need for a workaround like PTET.

But here’s the catch: the new $40,000 SALT cap is temporary and has income limitations

It only lasts from 2025 through 2029

It phases out for high-income taxpayers (starting at $500,000 AGI and fully phased out at $600,000)

It reverts to $10,000 in 2030, unless Congress intervenes again

Fortunately, the Senate recognized the long-term value and flexibility of PTET, especially for business owners whose income levels could exceed the new cap thresholds. In the final bill, the PTET elimination was removed, preserving the deduction strategy.

Why PTET Still Matters—Even With a $40,000 Cap

Even with the temporary SALT cap increase, PTET remains a valuable planning strategy for three reasons:

1. Not Everyone Qualifies for the Full $40,000 Cap

If your income exceeds $500,000, your benefit from the new SALT cap begins to phase out. At $600,000 or more, it drops back to $10,000—and PTET becomes your best tool for reclaiming that lost deduction.

2. PTET Applies at the Entity Level

Unlike the SALT cap, which applies at the individual level, PTET deductions occur above the line at the business level. That means the full amount paid as state tax by the business is deductible federally, regardless of your personal AGI.

3. Taxpayers May Benefit from BOTH

It’s possible for an owner of a pass-through entity to benefit from both the preservation of the PTET deduction as well as the increased $40,000 SALT Cap, especially for business owners that have high property taxes.

Planning Considerations Moving Forward

If you’re a business owner in a state with an active PTET program, here’s what you should be thinking about:

Continue electing into PTET where beneficial: The deduction is still fully valid under federal law and can provide meaningful savings for those with large state tax liabilities.

Coordinate with your SALT cap usage: While the new $40,000 cap opens opportunities, use both PTET and the SALT cap strategically based on your AGI and other deductions.

Review PTET election timing and payments: Some states require estimated payments or year-end elections. Make sure you're aligned with state-specific rules to lock in the deduction.

And remember—just because the PTET survived this round doesn't mean it's immune to future legislative changes. It’s wise to work with your tax professional to maximize the benefit while it lasts.

Final Thoughts

The survival of the PTET deduction is a major win for business owners who rely on this strategy to manage their federal tax exposure. While the expanded SALT cap helps in the short term, PTET offers a more durable and targeted solution—especially for high earners and pass-through business owners in high-tax states.

As always, tax planning is about playing the long game. The Big Beautiful Tax Bill gave us some new tools—but it also confirmed that tried-and-true strategies like PTET still have a place in the modern tax toolkit.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What is the Pass-Through Entity Tax (PTET)?

The PTET is a state-level workaround that allows S corporations, partnerships, and other pass-through entities to pay state income tax at the business level rather than at the individual level. Because entity-level taxes are fully deductible federally, PTET helps business owners bypass the federal $10,000 SALT deduction cap.

Did the Big Beautiful Tax Bill eliminate PTET?

No. While the House version of the bill originally proposed eliminating PTET starting in 2025, the Senate removed that provision from the final legislation. As a result, PTET remains fully intact under current federal law.

Why does PTET still matter even with the new $40,000 SALT cap?

The new $40,000 SALT cap is temporary (2025–2029) and phases out for taxpayers with income above $500,000. PTET, on the other hand, applies at the entity level, offering a potentially unlimited deduction regardless of the owner’s income. This makes PTET particularly valuable for high earners in high-tax states.

Can business owners use both PTET and the new $40,000 SALT cap?

Yes. It’s possible to benefit from both. Business owners can use PTET to deduct state income taxes paid at the entity level while still itemizing and using the higher $40,000 SALT cap for property taxes or other eligible personal state taxes.

Which states have PTET programs?

More than 30 states—including New York, New Jersey, California, and Illinois—currently offer PTET elections. Rules vary by state, so business owners should review eligibility, election deadlines, and payment timing requirements with their tax professional.

When does the new $40,000 SALT cap expire?

The expanded SALT cap is available for tax years 2025 through 2029 and is scheduled to revert to $10,000 in 2030 unless Congress extends it. PTET remains in effect beyond that date unless future legislation changes it.

What should business owners do next?

Business owners should continue electing PTET where available, coordinate its use with the new SALT cap for optimal tax benefit, and monitor future tax legislation for potential changes. Working closely with a CPA or tax advisor ensures compliance with both federal and state-level PTET rules.

Only Minor Changes to HSA Accounts Following The Passing of the Big Beautiful Tax Bill

The Big Beautiful Tax Bill made waves with several high-profile tax changes, but surprisingly, very few changes were made to Health Savings Accounts (HSAs). Below we outline what made it into the final bill, what got removed, and what retirees—especially those on Medicare—need to know going forward.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

The Big Beautiful Tax Bill made waves with several high-profile tax changes, but surprisingly, very few changes were made to Health Savings Accounts (HSAs).

The original House version of the bill proposed several generous HSA reforms, but many of those provisions did not survive final negotiations in the Senate. What passed into law is far more limited in scope—but still important for HSA participants and high-deductible health plan (HDHP) users to understand.

Below we outline what made it into the final bill, what got removed, and what retirees—especially those on Medicare—need to know going forward.

What Changed for HSAs (Final Bill Provisions)

While many headline HSA changes were removed, a few modest but helpful updates did make it into the final version of the Big Beautiful Tax Bill. Starting in 2026, these changes will apply:

1. Modest Increase in Contribution Limits

HSA contribution limits will still increase, though not as dramatically as proposed in the original House bill. The finalized increases will be indexed annually, but will remain tethered to the HDHP inflation formula.

Projected (not confirmed) 2026 limits:

These are normal annual adjustments, not the doubling of limits that was originally proposed in the House version.

2. Expanded Eligible Expenses (Still Intact)

The final bill does include modest expansion of what HSA funds can be used for without penalty:

Fitness and wellness programs (with physician sign-off)

Some home health monitoring equipment

Nutritional counseling and weight loss programs (medically prescribed)

Telehealth and other remote care services before meeting the deductible (effective 2025)

While not a massive overhaul, this creates more flexibility for proactive health management and out-of-pocket wellness spending.

What Got Removed From the Final Bill

The Senate stripped out several big-ticket HSA reforms that many taxpayers were hoping for. These proposed changes did not make it into law:

No HSA Contributions for Medicare Enrollees

One of the biggest disappointments was the Senate’s removal of the provision that would have allowed retirees on Medicare Part A to continue contributing to HSAs.

As it stands under current law—and unchanged by the new bill—if you are enrolled in any part of Medicare, including just Part A (hospital insurance), you are prohibited from making HSA contributions, even if you're still working and covered by an employer’s HDHP.

For more information, read our article:

“The HSA 6-Month Rule: What Happens When You Enroll In Medicare at Age 65”

No Doubling of Contribution Limits

The House bill proposed doubling the annual HSA contribution limits but the Senate eliminated this enhancement during reconciliation. For now, standard annual inflation adjustments will continue to dictate contribution caps.

No Catch-Up Coordination for Married Couples

Another House provision that would have allowed spousal catch-up contributions into a single HSA was removed. Currently, each spouse must open their own HSA to make the age 55+ catch-up contribution. That rule remains unchanged.

Planning Implications for Retirees on Medicare

The final bill leaves the existing HSA-Medicare rule intact, which means:

If you’re age 65 or older and enrolled in Medicare, even just Part A, you cannot contribute to an HSA

You can still spend previously accumulated HSA funds tax-free on qualified medical expenses, including:

Medicare premiums (Parts B, D, and Medicare Advantage)

Long-term care insurance premiums (subject to limits)

Dental, vision, hearing, and copays

This reinforces the strategy of front-loading HSA contributions before Medicare enrollment, while you’re still eligible.

Final Thoughts

The final version of the Big Beautiful Tax Bill made far fewer changes to HSAs than originally proposed. While modest improvements to eligible expenses were included, the most exciting enhancements—especially for higher-income workers and retirees—were removed.

That said, HSAs remain one of the most tax-advantaged accounts available:

Tax-deductible contributions

Tax-free growth

Tax-free withdrawals for qualified expenses

For now, the existing HSA rules remain in place, and careful planning before Medicare enrollment is still essential for maximizing long-term tax benefits.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What HSA changes were included in the Big Beautiful Tax Bill?

The final bill made only modest updates to Health Savings Accounts (HSAs), including a small inflation-based increase in contribution limits beginning in 2026 and expanded eligibility for certain health-related expenses such as fitness programs, home health monitoring devices, and nutritional counseling.

Did the Big Beautiful Tax Bill double HSA contribution limits?

No. The Senate removed the House’s proposed doubling of annual HSA contribution limits. Instead, contribution limits will continue to rise modestly based on standard inflation adjustments tied to high-deductible health plan (HDHP) thresholds.

Can retirees on Medicare still contribute to an HSA?

No. The new law did not change the rule preventing Medicare enrollees—including those enrolled only in Part A—from contributing to an HSA. Once you enroll in Medicare, you can no longer make new contributions, though you can continue using existing funds for qualified medical expenses.

What expenses can HSAs now cover under the new law?

Beginning in 2026, HSAs can be used for a slightly broader range of qualified expenses, including physician-approved fitness and wellness programs, telehealth services before meeting the deductible, certain home monitoring devices, and medically prescribed nutritional counseling or weight loss programs.

What HSA reforms were removed from the final bill?

The following proposals from the House version were cut by the Senate:

Allowing Medicare enrollees to continue contributing to HSAs

Doubling annual HSA contribution limits

Allowing married couples to make both catch-up contributions into one HSA

What should retirees know about HSAs and Medicare under current law?

If you are 65 or older and enrolled in any part of Medicare, you cannot contribute new funds to an HSA. However, you may still withdraw from your HSA tax-free to pay for qualified medical expenses, including Medicare premiums, long-term care insurance (within IRS limits), and out-of-pocket healthcare costs.

Are HSAs still valuable after the Big Beautiful Tax Bill?

Yes. Even with limited reform, HSAs remain a “triple-tax-advantaged” account: contributions are tax-deductible, growth is tax-free, and withdrawals for qualified expenses are tax-free. Pre-retirees should maximize contributions while eligible to take full advantage of these benefits.

EV Tax Credit Eliminated By The Big Beautiful Tax Bill: What You Need to Know Before the Clock Runs Out

The recently passed “Big Beautiful Tax Bill” includes sweeping changes to the tax code, but one provision that caught many by surprise is the elimination of the Electric Vehicle (EV) tax credit—a popular incentive for buyers of new, used, and commercial EVs.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

The recently passed “Big Beautiful Tax Bill” includes sweeping changes to the tax code, but one provision that caught many by surprise is the elimination of the Electric Vehicle (EV) tax credit—a popular incentive for buyers of new, used, and commercial EVs.

If you’ve been eyeing a new Tesla, Rivian, or Chevy Bolt and planning on that federal tax credit to sweeten the deal, the window is now closing faster than you might expect. Let’s break down what’s changing, when it changes, and what smart tax planning looks like from here.

What’s Changing: EV Credit Ends September 30, 2025

The new tax legislation repeals the federal EV tax credit for all categories of eligible vehicles—new, used, and commercial EVs—effective September 30, 2025.

Here are the key points:

Credits remain available through 9/30/2025 for qualifying vehicles that meet the current rules (including final assembly and battery sourcing requirements).

Starting October 1, 2025, no EV tax credits will be available—regardless of the manufacturer, price point, or battery configuration.

There is no phaseout, no new tiered system—it’s just gone.

This change has huge implications not just for consumers, but for dealers, automakers, and fleet operators who had integrated the credit into pricing, marketing, and adoption strategies.

Reminder: It’s a One-and-Done Tax Credit

One of the most misunderstood parts of the EV tax credit is how it actually works on your tax return. This isn’t a rebate or a refund check from the government—it’s a non-refundable tax credit, which means:

It can only be used once per taxpayer (for a qualifying new or used EV).

You only receive the portion of the credit that offsets your federal tax liability.

If your total tax due is less than the credit amount (e.g., $5,000 tax liability with a $7,500 credit), the excess is lost—you don’t get a refund or carryforward.

For this reason, tax planning is critical. You want to time the EV purchase in a year where you have enough tax liability to fully absorb the credit.

We break this concept down in greater detail in our dedicated article:

$7,500 EV Tax Credit: Use It or Lose It

What You Should Do Now

If you were planning to purchase an EV and benefit from the tax credit, here are a few action steps to consider:

1. Make Your Purchase Before the Deadline

To qualify, your EV purchase must be completed on or before September 30, 2025. If you’re ordering a vehicle with a long wait time, make sure delivery and documentation are completed by that deadline.

2. Coordinate With Your 2025 Tax Liability

Work with your tax advisor to project your 2025 tax liability. If it's too low to fully use the credit, you may want to consider:

Accelerating income into 2025

Deferring deductions

Selling appreciated assets that create short-term capital gains

IRA distributions or a Roth conversion

Why Is It Being Eliminated?

Supporters of the repeal argue that the EV market has matured, manufacturers have regained pricing power, and incentives are no longer needed to drive adoption. Others see it as a budgetary trade-off in the Big Beautiful Tax Bill designed to extend tax relief elsewhere (like the higher SALT cap and increased estate tax exemption).

Regardless of your view, the elimination is now law—and proactive planning is the only way to ensure you don’t leave money on the table.

Final Thoughts

The repeal of the EV tax credit may not be front-page news, but for taxpayers and businesses considering electric vehicle purchases, it’s a deadline worth tracking. If an EV is on your radar for 2025, your timing and tax planning just became far more important.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

When does the federal EV tax credit end?

The Big Beautiful Tax Bill eliminates the federal electric vehicle (EV) tax credit for new, used, and commercial EVs effective September 30, 2025. Purchases completed before that date may still qualify under current IRS rules.

Does the repeal apply to all types of EVs?

Yes. Beginning October 1, 2025, no EVs—regardless of manufacturer, price, or battery type—will be eligible for a federal tax credit. This repeal applies across the board with no phaseout or grandfathering period.

How does the EV tax credit work before the repeal?

The EV credit is a non-refundable tax credit, not a rebate. It reduces your federal income tax liability dollar-for-dollar, but only up to the amount you owe. Any unused portion is lost—you cannot carry it forward or receive it as a refund.

Can I still claim the EV tax credit in 2025?

Yes, if your qualifying vehicle is purchased and placed in service on or before September 30, 2025. To ensure eligibility, buyers should verify that final assembly, delivery, and paperwork are completed by that date.

Who benefits most from claiming the EV tax credit before it ends?

Taxpayers with sufficient federal tax liability to fully absorb the credit—often those with moderate to high income—benefit the most. Buyers with little or no tax liability may not receive the full $7,500 value.

How can I make sure I get the full EV credit?

Coordinate your purchase with your 2025 tax planning. If your expected tax bill is lower than the credit, consider strategies such as accelerating income, realizing capital gains, or completing a Roth conversion to increase your 2025 taxable income.

Why is the EV tax credit being repealed?

Lawmakers argued that the EV market has matured and that incentives are no longer needed to sustain demand. Others viewed the repeal as a budgetary offset to fund other tax relief measures, including a higher SALT cap and estate tax exemption.

What should EV buyers do now?

If you’re planning to buy an EV, act early to ensure delivery before the September 30, 2025 cutoff. Work with your tax advisor to evaluate your eligibility and confirm that you can maximize the credit before it disappears.