Strategies to Save for Retirement with No Company Retirement Plan

The question, “How much do I need to retire?” has become a concern across generations rather than something that only those approaching retirement focus on. We wrote the article, How Much Money Do I Need To Save To Retire?, to help individuals answer this question. This article is meant to help create a strategy to reach that number. More

The question, “How much do I need to retire?” has become a concern across generations rather than something that only those approaching retirement focus on. But what if you, or in the case of married couples, your spouse, are not covered by an employer-sponsored retirement plan? In this article we are going to cover retirement savings strategies for individuals that may not be covered by an employer-sponsored retirement plan.

Married Filing Jointly - One Spouse Covered by Employer Sponsored Plan and is Not Maxing Out

A common strategy we use for clients when a covered spouse is not maxing out their deferrals is to increase the deferrals in the retirement plan and supplement income with the non-covered spouse’s salary. The limits for 401(k) deferrals in 2025 is $23,500 for individuals under 50, $31,000 for individuals 50-59 and 64+ and $34,750 for individuals 60-63. For example, if I am covered and only contribute $8,000 per year to my account and my spouse is not covered but has additional money to save for retirement, I could increase my deferrals up to the plan limits using the amount of additional money we have to save. This strategy is helpful as it allows for easier tracking of retirement accounts and the money is automatically deducted from payroll. Also, if you are contributing pre-tax dollars, this will decrease your tax liability.

Note: Payroll deferrals must be withheld from payroll by 12/31. If you owe money when you file your taxes in April, you would not be able to go back and increase your deferrals in your company plan for that tax year.

Married Filing Jointly - One Spouse Covered by Employer Sponsored Plan and is Maxing Out

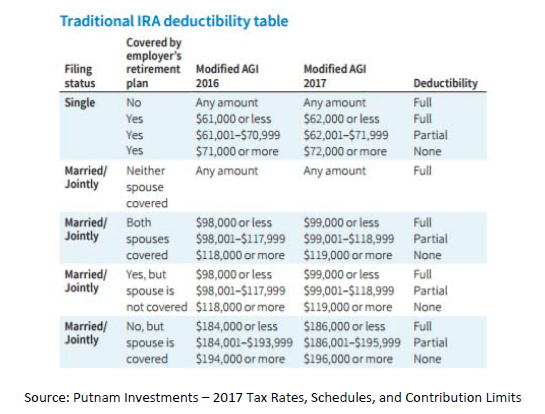

If the covered spouse is maxing out at the high limits already, you may be able to save additional pre-tax dollars depending on your Adjusted Gross Income (AGI).

Below is the Traditional IRA Deductibility Table for 2025. This table shows how much individuals or married couples can earn and still deduct IRA contributions from their taxable income.

As shown in the chart, if you are married filing jointly and one spouse is covered, the couple can fully deduct IRA contributions to an account in the covered spouses name if AGI is less than $126,000 and can fully deduct IRA contributions to an account in the non-covered spouses name if AGI is less than $236,000. The Traditional IRA limits for 2025 are $7,000 if under 50 and $8,000 if 50+. These lower limits and income thresholds make contributing to company sponsor plans more attractive in most cases.

Single or Married Filing Jointly and Neither Spouse is Covered

If you (and your spouse if married filing joint) are not covered by an employer sponsored plan, you do not have an income threshold for contributing pre-tax dollars to a Traditional IRA. The only limitations you have relate to the amount you can contribute. These contribution limits for both Traditional and Roth IRA’s are $7,000 if under 50 and $8,000 if 50+. If married filing joint, each spouse can contribute up to these limits.

Unlike employer sponsored plans, your contributions to IRA’s can be made after 12/31 of that tax year as long as the contributions are in before you file your tax return.

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally , professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, pleas feel free to join in on the discussion or contact me directly.

The Process Of Buying A House

Buying a house can be a fun and exciting experience but it’s also one of the most important financial decisions that you are going to make during your lifetime. This article is designed to help home buyer’s understand:

Buying a house can be a fun and exciting experience but it’s also one of the most important financial decisions that you are going to make during your lifetime. This article is designed to help home buyer’s understand:

The home buying process from start to finish

The parties involved in the process (real estate agent, attorney, bank, etc.)

Common pitfalls to avoid

What to expect when applying for a mortgage

How to calculate the amount of your down payment

Owning Versus Renting

You first have to determine if owning a house is the right financial decision for you. Society wires us to think that owning a house is automatically better than renting but that is not necessarily true in all situations. From a pure dollar and cents standpoint, it may make sense to keep renting given your personal situation. We typically tell clients if there is a fair chance that they may need to sell their house within the next 5 years, in many cases it may make sense to keep renting as opposed to buying a house given all of the upfront costs associated with purchasing a house. It takes a while to recoup closing costs and when you go to sell your house you will most like have to pay your real estate agent 5% - 6% of the selling price.

Determine How Much You Can Afford

Before you even start looking at houses you have to determine two things:

The down payment and closing costs

The amount of the monthly mortgage payment that fits into your budget

There is no point in looking at $300,000 houses if you cannot afford the down payment or the monthly mortgage payment so the initial step involves determining what you can afford.

Calculating Your Closing Costs

Closing costs are in addition to your required “down payment”. First time home buyers often make the mistake of just using the 5% down or 10% down as a rule of thumb for their total upfront cost for buying a house. They often forget about closing costs which can add an additional 2% - 5% of the purchase price of the house to the amount due at closing. Closing costs include:

Discount Points: An up-front fee that you can choose to pay if you want to reduce the interest rate on your loan.

Origination Charge: Fee for processing your mortgage application, pulling credit reports, verifying financial information, and creating the loan

Rate-lock Fee: If you choose to lock in your interest rate beyond a certain period of time

Other Lender Fees: Document preparation fee, processing fee, application fee, and underwriting fees

Appraisal & Inspection Fees: Fees for the lender to inspect and appraise the value of the house

Title Services: Fee charged by the title agent to determine the rightful ownership of the house you are buying and some lenders require title insurance.

Government Recording Charges: Every home buyer must pay these charges for the state and local agencies to record the loans and title documents

Transfer Taxes: Depending on where you live, your state, county or city may charge a tax when the ownership of a home is transferred

Escrow Deposit: At the closing of your home loan, if you decide to escrow or if an escrow is required, there will be an initial deposit in your escrow account to pay for future recurring charges associated with your home, such as property taxes, school taxes, and insurance. You will typically need to pay for the first year of your homeowner’s insurance in full before your home loan closes.

Daily Interest Rate Charge: This charge covers the amount of interest that you will owe on your home loan from the time your loan closes to the first day of your regular mortgage billing cycle.

Flood Insurance: This is a form of hazard insurance that is required by lenders to cover properties in flood zones.

Attorney Fees: Fees typically vary from $300 - $1,000. Most individuals will work with a real estate attorney to review and negotiate the purchase agreement on their behalf. These fees are sometimes paid to the attorney prior to the closing.

As you can see there are a number of fees that you have to be prepared to pay in addition to the down payment required by the lender. Lenders are required by law to give you a “good faith estimate” (GFE) of what the closing costs on your home will be within three days of when you apply for a loan. However, these are just estimates and many of the fees listing on the GFE can legally change by up to 10%, potentially adding thousands of dollars to your final closing cost bill. A day before your closing the lender should provide you with a copy of your HUD-1 settlement statement, which outlines all of the closing fees.

Calculating Your Down Payment

The amount of your down payment will vary based on the type of loan that you received to purchase your house. The three main types of home loans are:

FHA Loan

Conventional Mortgage

VA Loan (Veterans Affairs)

FHA Loan: FHA stands for Federal Housing Administration. The loans are made by banks but they are guaranteed by the FHA which added additional protection for the lender. FHA loans come with a minimum down payment of 3.5% which make them very popular. With these loans borrowers pay PMI (private mortgage insurance) premiums both upfront and each year until the loan is paid down to a specified level. Loan limits vary by housing type and county. These loans tend to favor low to middle income borrowers who do not have a means to make the traditional 10% - 20% down payment at closing.

Conventional Mortgage: Minimum down payment varies from 5% - 20%. Borrowers that put down less than 20% will have to pay PMI (private mortgage insurance). Conventional mortgages typically require a higher FICO score than FHA loans. These loans tend to favor borrowers with higher credit scores and have enough cash on hand to make a sizable down payment.

VA Loan: VA loans are available only to veterans. The greatest benefit of these loans is they require no down payment and they allow qualified borrowers to purchase a home without the need for mortgage insurance. VA loans also tend to have more flexible and forgiving requirements. The VA charges a mandatory Fund Fee of 2.15% for regular military and 2.40% for Reserve/Guard on purchase loans.Let’s bring it all together in an example. If you anticipate on buying a house for $200,000 and you plan on taking an FHA loan, the amount that you will need to save for the closing will be in the range of $11,000 - $17,000 (3.5% for the down payment and 2% - 5% for the closing costs). This calculation will obviously vary based on the type of loan you plan on taking to purchase your house.

Determine what your monthly mortgage payment

After you have determined how much you need to save to meet the upfront cost of purchasing a house, the next step is to determine the monthly mortgage payment that fits into your budget.

Step 1: Establish your current monthly and annual budget. There is no way to determine what you can afford if you have no idea where you are now from an income and expense standpoint. Tip: Be brutally honest with yourself when listing your expenses. The last thing you want to do is underestimate your expenses, buy a house you cannot afford, and then go through a foreclosure. You will also have to factor in additional expenses into your budget as if you owned the house today such as lawn care, snow removal, appliances, and maintenance expense. As a renter you may not have any of these expenses now but as soon as you own a house, now when something breaks you have to pay to fix it. Homeownership is often times more expensive than most individuals anticipate.

Step 2: Based on your current monthly income and expenses, how much is left over to satisfy a monthly mortgage payment? The general rule is your monthly mortgage payment (including property taxes, PMI, and association fees) should not exceed 32% of your monthly gross income. Tip: Leave some extra room in your budget for life’s unexpected surprises. For example, furnace need to be replaced, dishwasher brakes, spouse loses a job, plumbing issues, etc.

Step 3: Use an online mortgage calculator to determine the loan amount that meets your estimated monthly mortgage payment. Do not forget to take into account property taxes, school taxes, association fees, PMI, and homeowners insurance when reaching your estimated monthly payment.

The parties involved in the home buying process

There are a lot of different professionals that you will interact with during the process of purchasing your house. It’s important to understand who is involved, what their role is in the process, and how they are compensated.

Buyer & Seller: This is pretty self-explanatory. Most buyers and sellers work through realtors and attorneys to complete the real estate transaction so there is typically little or no direct interaction between the buyer and the seller. However, in a “for sale by owner”, the buyer or the buyer’s realtor/attorney will be in direct communication with the seller since there is no real estate agent on the sellers side.

Real Estate Agent (Realtor): Real estate agents are important partners when you are buying a house. They can provide you with helpful information on homes and neighborhoods that isn’t easily accessible to the public. Their knowledge of the home buying process, negotiation skills, and familiarity with the area you want to live in can be very valuable. In most cases, as the buyer, it does not typically cost you anything to use a realtor because they are compensated from the commission paid by the seller of the house.

Real Estate Attorney: Remember, buying a home is a legally binding transaction. A real estate attorney can help you avoid some common pitfalls when purchasing your home. The home buying process eventually results in a formal purchase agreement between the buyer and seller. The purchase agreement is the single most important document in the transaction. Although standard printed forms may be used, a lawyer can explain the forms and make changes and additions to reflect the buyer’s wishes. Examples are:

What are the legal consequences if the closing does not take place?

What happens if the inspection reveals termites, radon, or lead based paint?

Will money be held in escrow from the seller’s proceeds to replace certain items?

How much does a real estate attorney cost? It varies, but expect to pay somewhere in the range of $350 - $1,000. Often times you have to pay the attorney a retainer or pay them in advance of the closing. The amount an attorney charges is usually dependent on the level of services that they are provided to you. Some attorneys may just be preparing the deed while other attorney’s may provide you with a more complete package which can include deed preparation, title examination, purchase agreement review, and lender work. Make sure you fully understand how the attorney’s fee structure works and it often helps to ask your professional network or friends for attorney’s that they have worked with and would recommend.

Bank / Credit Union: Most home buyers need a mortgage to finance the purchase of their house. It is recommended that you contact a few banks and credit unions in your area to compare interest rates, closing costs, and fees associated with the issuance of your mortgage. Similar to selecting a real estate attorney we strongly recommend asking your professional network (accountant, investment advisor) for lenders that they recommend working with. You will have a lot of interaction with the lender throughout the home buying process and working with a lender that makes the underwriting process as smooth as possible will make the overall home buying experience much more enjoyable.

Home Inspector: After your offer has been accepted by the seller you will need to hire a home inspector to visit the house. Your real estate agent will most likely recommend a home inspector to use. The job of the home inspector is to visit the property to make sure there are no issues with the house that may not be apparent to the untrained eye. They look for termite damage, structural issues, mold, condition of the roof, electric, plumbing, drainage, septic, radon levels, etc. A few days after their visit they will provide you with a formal report of their inspection. You typically pay them at the time they conduct the inspection. The cost of a home inspection typically ranges from $250 - $600.

Insurance Broker: You will need to obtain a homeowners insurance policy prior to the closing date. Since you are adding a house to your insurance coverage, often times this is a good opportunity to look at your insurance coverage as a whole because insurance companies will usually offer discounts on “bundling” your insurance coverage. Meaning that a single provider covers your house, cars, and personal umbrella policy. The annual cost of your homeowners insurance will vary greatly depending on the value of your house and where the house is located. For homeowners that have an escrow account associated with their mortgage, the homeowners insurance premium is typically baked into your total monthly mortgage payment , the insurance company issues the invoice directly to the bank, and the bank pays your homeowners insurance directly out of your escrow account.

Timeline: The home buying process from start to finish

Now that we have explained how to determine what you can afford and the parties involved in the home buying process it’s time to put it all together so you know what to expect step by step through the process of purchasing your new home.

Step 1: Get prequalified for a mortgage. You may think you can qualify for a $250,000 mortgage but you really do not know until you actually apply. In the preapproval process you will provide some information to the bank that will be issuing your mortgage such as tax returns, statements showing investment and savings accounts, and they will usually run a credit report. The more intense financial due diligence happens after an offer has been accepted on your house and they are actually preparing to provide you with the loan.

Step 2: Begin looking at houses. Most individuals at this point will hire a real estate agent to help them find and look at houses.

Step 3: Make an offer. Once you find the house that you want, you will have your real estate agent present the seller with your offer. This is where the negotiation process begins. If the seller is listing the house for $200,000, you can make an offer for whatever amount you choose. Once an offer is presented to the seller, three things can happen:

The seller can accept it

The seller can reject it

The seller will counter offer

Your real estate agent can really help you in this process to determine what may be a reasonable offer. It is usually dependent upon how long the house has been on the market, where is the property located, is there a situation that requires selling the house quickly, and what have other similar houses sold for in the area. After making the offer you will typically receive a response within 48 hours. The seller will sometimes give their real estate agent a range saying that they will accept less than the asking price but only to a specific threshold. In most situations the buyer and the seller meet somewhere in the middle. If the house is listed for $200K, the buyer may put in an offer for $180K and after some back and forth they eventually meet somewhere around $190K. But that is not always the case. If there are multiple offers on the house you could end up in a “bidding war”. Offers are “blind bids” meaning that you and your real estate agent have no way of knowing what other people are offering the seller for the house. Buyers are essentially making their “best guess” that their offer will win. You may make an offer for full price only for another buyer to come in two hours later and offer $10,000 over their asking price. You really have to lean on your real estate agent to give you some guidance based on their knowledge of the market.

Step 4: Offer accepted……now what? Typically, purchase offers are contingent on a home inspection of the property. Your real estate agent will usually help you arrange to have a home inspection conducted within a few days of your offer being accepted. There are usually contingencies in your offer agreement that provides you with the chance to renegotiate your offer or withdraw it without penalty if the inspection reveals significant material damage. If the inspector discovers issues with the house you will have to make the decision if you want to ask the seller to fix the issue prior to the closing date. Prior to the close you will have a walk-through of the house, which gives you a chance to confirm that any agreed-upon repairs have been made.

Step 5: Apply for a mortgage. Now that your offer has been accepted the mortgage underwriting process will kick into high gear. The bank will assign you a “loan officer” or “mortgage broker” to serve as the direct contact at the bank throughout the mortgage approval process. You will provide them with the information on the house that you intend to purchase, they will send you the mortgage application with all of financial documents that they will need to formally approve you for the mortgage. The bank will also arrange for an appraiser to visit the house and provide an independent estimate of the value of the house. After all if they are giving you a loan for $200,000, they want to make sure that house is worth at least $200,000 in case you were to stop paying the mortgage then essentially the bank would own the house and have to sell it. You will receive a “commitment letter” from your bank once your mortgage has been formally approved.

You will need to show the bank documentation of the account that is currently holding the cash that will be used for your down payment and closing costs. If someone gifts you money to buy your house, the person that made the gift will most likely have to sign a letter stating that it was an outright gift and not a loan.

Step 5½ : You will simultaneous engage a real estate attorney to begin working with at this time. Your attorney will review the purchase agreement, initiate a title search and review the results, begin prepping the deed, and communicate directly with the seller’s attorney if changes or additions need to be made to the purchasing agreement.

Step 6: Set a closing date. The closing date is the date that you will sign a huge pile of papers and the house officially becomes yours. There is typically an “estimated closing date” set in the purchase agreement but a firm date needs to be set by the buyer, seller, attorneys, and the bank. The seller’s real estate agent, the buyer’s real estate agent, your mortgage broker, and the attorneys on both sides will typically communicate with each other to establish the closing date. A special note……..a lot can happen during a real estate transaction that can delay the closing date. Issues can arise on the seller’s side or the mortgage process could take longer than expected. In other words, even though you have a “final closing date” be prepared for the closing date to change. If you are renting right now and have a lease, if your closing date is May 1st it’s usually recommended that you have your current lease run until May 30th or June 30th in case the closing date gets pushed back. Real estate transactions have a lot of moving parts and a lot of unexpected things that are out of your control can happen.

Step 7: Contact your insurance broker to establish a homeowner’s policy. Your bank will require you to have homeowners insurance on the property. You must pay for the policy and have it at closing. You are free to select your own insurance carrier but the lender will typically require the insurance company issuing the policy to be a specific rating or higher.

Your insurance broker may also help you with your title insurance policy. Many lenders will require you to have a title insurance policy at closing. As part of the home buying process a title search should be conducted which results in a report that shows who owns the property and if there are any liens against the property. Title insurance protects you and the lender up to the full value of the property if fraud, a lien, or faulty title is discovered after your closing.

Step 8: The day BEFORE the closing. It is recommended that you send a reminder email to your real estate agent, attorney, and mortgage broker to confirm that everything is a “go” for the closing the next day. You and your real estate agent should make a final inspection of the property within 24 hours prior to the closing. In many cases, the lender will make a similar inspection before closing. The bank that is issuing you the loan should also be able to provide you with a copy of your HUD-1, which is a long, one page document that details all of the financial activity associated with the purchase of your house. You should review this document with your mortgage broker and/or attorney prior to the closing to make sure everything is accurate.

You will also need to confirm with your attorney/mortgage broker the amount of the certified check that you will need to bring to the closing. A certified check is a special type of check issued by a bank that guarantees that the funds to back that check are guaranteed by the bank issuing the check.

Step 9: The date of your closing. You made it!!!!!! Today is the day your new house officially becomes yours. There are two primary things that you need to bring with you to the closing:

Certified check

Homeowners policy and proof of payment

The actual closing is conducted by a “closing agent” who may be an employee of the lender or title company, or it may be an attorney representing you or the lender. The lender and seller, or their representatives, and the real estate agents may or may not be at the actual closing. It is not unusual for the parties to the transaction to complete their roles without ever meeting face to face.

For the most part, your role at closing is to review and sign the numerous documents associated with a mortgage loan. The closing agent should explain the nature and purpose of each one and give you and your attorney an opportunity to check them before signing.

At the conclusion of the meeting you receive the keys to the house and you are officially a new homeowner.

Step 10: Begin making your monthly mortgage payments. One of the top questions that we get is “What is an escrow account?” You will hear that term a lot when you are going through the mortgage process. Think of an escrow account as a separate savings account that is attached to your mortgage. When you make a monthly mortgage payment, it is made up of a few components:

Principal & Interest Payments: Amount applied against your actual loan

PMI (if applicable): Mortgage insurance

Escrow: Cash reserve to pay taxes and homeowners insurance

If my monthly mortgage payment is $2,000, only $1,100 of that amount may actually be applied against the loan. The other $900 may be used to pay my monthly PMI and the remainder is deposited to my escrow account.

When your property taxes and school taxes are due, the county that you live in will typically send those tax bills directly to the bank holding your mortgage and then the bank in turn pays those bills out of your escrow account. The bank will typically mail the homeowners a receipt that the tax bill has been paid. It’s basically a forced monthly savings account for your anticipated tax bills. The same thing is true for your homeowner insurance premium payments. The bank that is holding your mortgage forecasts how much your taxes and homeowner insurance is going to be for the next 12 months and then builds those amounts into your monthly mortgage payments. The bank does not want you to lose your house because you were unable to pay your property or school taxes. The property and school tax bills show up once a year and depending on where you live those bills can be for thousands of dollars.

If there is additional money left in your escrow account after the taxes and homeowner insurance has been paid, the bank is usually required to send a portion of that additional cash reserve to the homeowner in the form of a check. Those are fun checks to get in the mail.

Michael Ruger

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

How Much Money Do I Need To Save To Retire?

This is by far the most popular question that we come across as financial planners. You may have heard some of the "rules of thumb" like “80% of your current take-home pay” or “1 million dollars”. In reality, the answer varies greatly on an individual by individual basis. This article will outline the procedures that we follow as financial planners to help

poc

This is by far the most popular question that we come across as financial planners. You may have heard some of the "rules of thumb" like “80% of your current take-home pay” or “1 million dollars”. In reality, the answer varies greatly on an individual by individual basis. This article will outline the procedures that we follow as financial planners to help individuals answer this very important question.

Step 1: Estimate Your Annual Expenses In Retirement

The first step is to get a ballpark idea of what your annual expenses might look like in retirement. The best place to start is to list your current monthly and annual expenses. Then create a separate column labeled “expenses in retirement”. Whether you are 2 years, 10 years, or 20 years away from retirement the idea is to pretend as if you were retiring tomorrow and determining what your annual expenses might look like. Some of your expenses in retirement will be lower, others may be higher, but most people find that a lot of their current expenses will carry over at the same level into the retirement years. This is because most people have become accustom to a certain standards of living and they intend to maintain that standard of living in retirement. Here are a few important questions that you should ask yourself when forecasting your retirement expenses:

How much should I budget for health insurance?

Will I have a mortgage or debt when I retire?

Do I plan to move when I retire?

Since I will not be working, should I budget additional expenses for vacations and hobbies?

Will I need to keep my life insurance policies after I retire?

Step 2: Adjust Your Retirement Expenses For Inflation

Now that you have a ballpark number of your annual expenses in retirement, you will need to adjust those expenses for inflation. Inflation is just a fancy word for “the price of everything that we buy today will gradually go up in price over time”. If the price of a gallon of milk today is $2 then most likely 20 years from now that same gallon of milk will cost $3.51. A 75% increase!! Historically inflation has grown at a rate of about 3% per year. There are periods of time when the rate of inflation grows faster or slower but on average it grows at 3% per year.

Another way to look at inflation is $20,000 in today’s dollars will not buy the same amount of goods and services 10 years from now because inflation erodes the purchasing power of your $20,000. If I did my annual expense planner and it tells me that I need $50,000 per year in retirement to meet all of my estimated expenses, let’s look at what adjusting that $50,000 for inflation does over different periods of time assuming a 3% rate of inflation:

Today’s Dollars 5 Years From Now 10 Years From Now 20 Years From Now

$50,000 $56,275 $65,238 $87,675

In the above example, if I am retiring in 10 years, and my estimated annual expenses in retirement will be $50,000 in today’s dollars, by the time I retire 10 years from now my annual expenses will increase to $65,238 per year just to stay in the same place that I am in today. Also, inflation does not stop when you retire, it continues into the retirement years. If I am 50 today and plan to live until 90, I have to apply this inflation adjustment for 40 years. It’s clear to see how inflation can have a significant impact on the amount that you may need to withdrawal for your account to meet you estimated expenses at a future date.

Step 3: Gather The Information On Your Current Assets

Once you know your expenses, you now need to gather all of the information on your retirement accounts and pension plans. You should collect the most recent statement for all of your investment accounts (401K, 403B, IRA’s, brokerage accounts, stocks, etc.), pension statements (if applicable), obtain your most recent social security statement, and gather information on the other sources of income and/or assets that may be available when you retire. Such as:

Sale of a business

Downsizing the primary residence

Rental income

Part-time employment

Step 4: Project The Growth Of Your Retirement Assets

There are three main categories to consider when calculating the growth rate of your retirement assets:

Annual contributions

Withdrawals

Investment rate of return

For annual contributions, it’s determining which accounts you plan on making deposits too each year and how much? For most individuals, their employer sponsored retirement plan is the main source of new contributions to their retirement nest egg. If your employer makes regular employer contributions to your retirement plan, you should factor those in as well. For example, if I am contributing 8% of my pay into the plan and my employer is providing me with a 4% matching contributions, I would reasonably assume that I’m adding 12% of my pay to my 401(k) plan each year.

The most popular question that we get in this category is “how much should I be contributing each year to my retirement account with my employer?” We advise employees that they should have a goal of contributing 10% of their pay each year to their retirement accounts. This is an aggregate total between your personal contributions and the employer contributions. Even if you cannot reach that level right now, 10%+ is the target.

Let’s move onto the next category…….withdrawals. Pre-retirement withdrawals from retirement accounts have become much more common in recent years due largely to the rising cost of college education. Parents will take loans from their 401K/403B plans or take early withdrawals from IRA accounts to fulfill the need for additional income during the years that their children are in college. If part of your overall financial plan is to use your retirement accounts to pay for one-time expenses such as college, you will need to factor that into your projections.

The third variable to consider when determining the growth of your assets is the assumed annual rate of return on your investments. There are many items to consider when determining a reasonable annual rate of return for your accounts. Some of those considerations include:

Time horizon to retirement

Allocation of your portfolio (stocks vs bonds)

Concentrated holdings (10%+ of your portfolio allocated to a single investment)

Accumulation phase versus distribution phase

The answer to the question: “what rate of return should I expect from my retirement accounts?”, can really only be determine on a case by case basis. Using an unreasonable rate of return assumption can create a significant disconnect between your retirement projections versus what is likely to actually occur within your investment accounts. Be careful with this step.

Step 5: Factor In Taxes

Don’t forget about the lovely IRS. All assets are not treated equally from a tax standpoint. For most individuals, the majority of their retirement savings will be in pre-tax retirement vehicles such as 401(k), 403(b), and Traditional IRA’s. That means when you take distributions from those accounts, you will realize earned income, and have to pay tax. For example, if you have $400,000 in your 401K account and you are in the 25% tax bracket, $100,000 of that $400,000 will be lost to taxes as withdrawals are made from the account.

If you have after tax investment accounts, it’s possible that you may owe little to no taxes on withdrawals. However, if there are unrealized investment gains built up in your after tax investment accounts then you may owe capital gains tax when liquidating positons.

Also note, you may have to pay taxes on a portion of your social security benefit. The amount of your social security benefit that is taxable varies based on your level of income.

Step 6: Spend Down Your Assets

In the final step, you should run long term projections to illustrate the spend down of your assets in retirement. Here are the steps:Example

Start with your annual after tax expense number $60,000

Subtract social security less taxes: ($20,000)

Subtract pension payments less taxes (if applicable): ($10,000)

Annual Expenses Net SS and Pensions: $30,000

In the example above, this individual would need an additional $30,000 after-tax to meet their anticipated annual expenses in Year 1 of retirement. I stress “after-tax” because if all of the retirement assets are in a pre-tax retirement account then they would need to gross up their distributions for taxes to get to the $30,000 after tax. If it is assumed that $40,000 has to be withdrawn from an IRA each year, the 3% inflation rate is applied to the annual expenses, and the life expectancy of this individual is 20 years from the date that they retire, this individual would need to withdrawal $1,074,814 out of their retirement accounts over the next 20 years to meet their income needs.

Step 7: Identify Multiple Solutions

There are often times multiple roads to reach a destination and the same is true when planning for retirement. If you find that you assets are falling short of the amount that is needed to sustain your expenses in retirement, you should work with a knowledgeable financial planner to identify alternative solutions. It may help you to answer questions like:

If I decided to work part-time in retirement how much would I have to earn?

If I downsize my primary residence in retirement how does this impact the overall picture?

If I can’t retire at age 63, what age can I comfortably retire at?

What are the pros and cons of taking social security benefits prior to normal retirement age

I also encourage clients to spend time looking at their annual expenses. If you find that your are cutting it close on income versus expenses in retirement, it's usually easier to cut expenses than it is to create more income in the retirement year.

Michael Ruger

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

First Time Homebuyer Tips

Buying your first home is one of life’s milestones that everyone should have the opportunity to experience if they choose. Owning a home gives you a feeling of accomplishment and as you make payments a portion is going to your personal net worth rather than a landlord. The process is exciting but one surefire piece of information that I wish I

home buyer tips

Buying your first home is one of life’s milestones that everyone should have the opportunity to experience if they choose. Owning a home gives you a feeling of accomplishment and as you make payments a portion is going to your personal net worth rather than a landlord. The process is exciting but one surefire piece of information that I wish I knew when buying my first home is that you will come across surprises. Whether it be a delay in closing, an issue with financing, or closing costs being higher than expected, it is important to know that you can do all the preparation possible and still be hit in the face with some setbacks.

This article will not only touch on some of the important considerations when buying your first home but will give examples of possible setbacks and how to avoid them.

Know Your Number

The most important piece of information to have when purchasing your home is how much you can spend. The purchase of your home should not be the only goal to consider. All of your other financial objectives such as paying off debt (i.e. college and unsecured) and saving for retirement must be taken into consideration. Also, it is recommended you have an emergency fund in place that would cover at least 4 months of your fixed expenses in case something happens with your job or some other event occurs. Knowing your number does not only include what you can afford today but how much you can afford monthly moving forward. If your monthly cash flow becomes dangerously low or negative with the addition of a mortgage payment (including mortgage/property taxes/homeowners), the house may be too expensive.

NOTE: Just because you are preapproved for a certain amount does not mean you need to spend that amount.

Choose An Agent You Trust

You will be spending a lot of time with your agent so choose them wisely. It should be someone you get along with and someone you can trust will look out for your best interests. If your agent just cares about receiving a commission, they may push you to purchase a home before looking at all of your options or buying a home you can’t afford. Remember, you are the client and therefore should be treated as such.

NOTE: Just because you never physically cut a check to your real estate agent doesn’t mean you aren’t paying them. In a typical transaction the seller will pay the commissions. An agreed upon percentage will come out of the sales proceeds and go to both real estate agents (the buyer’s and the seller’s) and therefore the cost is built into the price you pay.

Use Your Agent As An Asset

Your agent is likely much more knowledgeable about home buying than you so use that knowledge to your benefit. The agent should be able to help you value homes and determine whether the house is fairly priced. Ask them as many questions as possible throughout the entire process.

On The Fence

If you are on the fence whether or not to buy a home then take your time. If you may relocate because of your job or family don’t jump into purchasing a home. It is not worth paying the closing costs and going through the hassle of home buying if you may move in the near future. We typically use the “5 Year Rule” when making the determination. If you don’t see yourself being in the house for at least 5 years you should consider whether or not you will get your money back when you sell.

Compare Lenders

The banking industry is extremely competitive and it is worth shopping around for the best offer when choosing a mortgage provider. If you aren’t comfortable with numbers, don’t be afraid to ask for help. A difference of 0.10% on a 30 year mortgage could be the difference of thousands of dollars wasted on interest.

Don’t Cheap Out On Homeowners

Don’t choose your homeowners policy based on price. Of course price is one of the considerations but it is not the only one. Make sure your policy is the most comprehensive you can comfortably afford as the cost of increased premiums is likely much less than the cost of coming out of pocket for something not covered. Remember, insurance companies, like banks, are in a competitive industry so shop around.

Down Payment

Most lenders require a 20% down payment of the home value to avoid paying additional costs. This means if the value of the home is $200,000, you will have to pay $40,000 out of pocket! Most lenders offer Federal Housing Administration (FHA) loans that allow you to put down as little as 3.5%. If you choose this type of loan you also have to purchase Private Mortgage Insurance (PMI). This will be a cost added to your mortgage payment until the value of your home is adequate enough to remove the PMI. It is important to factor this in as a cost similar to interest because a 5% interest rate could quickly look like 6-7% if you have to pay PMI.

Closing And Other Additional Costs

There are a lot of out of pocket costs to consider when purchasing a home. Examples of these costs are listed below. An important piece of knowing your number is to consider all the costs that may come up during the process.

Loan Origination Fee

Attorney Fees

Property Taxes

Home Owners Insurance

Appraisal Fee

Inspection Fee

Title Insurance

Recording Fee

Government Recording Charges

Credit Report Fee

Flood Determination Fee

How To Help Avoid Certain Complications

Situation: I bought a house at the top of my budget that I thought was move in ready but needs repairs.

Recommendation: Choose an inspector that has a great reputation and knows the location. There may be issues that are common to the area that one inspector may be more likely to identify. Also, bring a contractor or someone of similar background for a walk through. Repairs can be extremely costly and if you purchased a home at the top end of your budget you may not be able to afford certain fixes. It should be known that all issues cannot be foreseen but taking the necessary steps to diminish these situations will not hurt. Don’t purchase a home that will bankrupt you if repairs need to be done.

Situation: I bought a home I can’t fill.

Recommendation: Closing costs and repairs won’t be the only out of pocket expenses. Complete a summary of items you think you may need to buy after the purchase. This may include furniture, appliances, décor, and fixtures. In these situations it is always better to overestimate.

Situation: My lease is up in a month and I would like to purchase a home.

Recommendation: Purchasing a home is something that requires time and planning. The home will likely be the largest purchase you’ve ever made (depending on the college you choose) so it is not something to rush. If you are thinking of moving after your lease is up or when you relocate jobs, start planning as soon as possible. Feeling forced into purchasing something as important as a home will likely lead to regrets.

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally , professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, pleas feel free to join in on the discussion or contact me directly.

Backdoor Roth IRA Contribution Strategy

This strategy is for high income earners that make too much to contribute directly to a Roth IRA. In recent years, some of these high income earners have been implementing a “backdoor Roth IRA conversion strategy” to get around the Roth IRA contribution limitations and make contributions to Roth IRA’s via “conversions”. For the 2020 tax year, your

backdoor roth ira strategy

This strategy is for high income earners that make too much to contribute directly to a Roth IRA. In recent years, some of these high income earners have been implementing a “backdoor Roth IRA conversion strategy” to get around the Roth IRA contribution limitations and make contributions to Roth IRA’s via “conversions”. For the 2025 tax year, your ability to make contributions to a Roth IRA begins to phase out at the following AGI thresholds based on your filing status:

Single: $150,000

Married Filing Jointly: $236,000

Married Filing Separately: $0

However, in 2010 the IRS removed the income limits on “IRA Conversions” which open up an opportunity……if executed correctly…….for high income earners to make “backdoor” contributions to a Roth IRA.

Why would a high income earning want to contribute to a Roth IRA? Once high income earners have maxed out their contributions to their employer sponsored retirement plans, they usually begin to fund plain vanilla investment management accounts or whole life insurance policies. When assets accumulate in an investment management account, once liquidated, the account owner typically has to pay either short-term or long term capital gains on the appreciation. For whole life insurance, even though the accumulation is tax deferred, if the policy is surrendered, the policy owner pays ordinary income tax on the gain in the policy.

With a Roth IRA, after tax contributions are made to the account and the gains in the account are withdrawn TAX FREE if the account owner at the time of withdrawal is over the age of 59½ and the Roth IRA has been in existence for 5 years. A huge tax benefit for high income earners who are typically in a medium to higher tax bracket even in retirement.

Here is how the strategy works

Rollover all existing pre-tax IRA’s into your employer sponsored retirement plan

Make a non-deductible contribution to a Traditional IRA

Convert the Traditional IRA to a Roth IRA

Here are the pitfalls in the execution process

Over the years, more and more individuals have become aware of this wealth accumulation strategy. However, there are risks associated with executing this strategy and if not executed correctly could result in adverse tax consequences.

Here are the top pitfalls:

Forget to aggregate Pre-Tax IRA’s

Do not understand that SEP IRA’s and Simple IRA’s are included in the Aggregation Rule

They create a “step transaction”

Pitfall #1: IRS Aggregation Rule

The IRA aggregate rule stipulates that when an individual has multiple IRAs, they will all be treated as one account when determining the tax consequences of any distributions (including a distribution out of the account for a Roth conversion).

This creates a significant challenge for those who wish to do the backdoor Roth strategy, but have other existing IRA accounts already in place (e.g., from prior years’ deductible IRA contributions, or rollovers from prior 401(k) and other employer retirement plans). Because the standard rule for IRA distributions (and Roth conversions) is that any after-tax contributions come out along with any pre-tax assets (whether from contributions or growth) on a pro-rata basis, when all the accounts are aggregated together, it becomes impossible to just convert the non-deductible IRA.

picture

If an individual has pre-tax IRA’s we typically recommend that they rollover those IRA’s into their employer sponsored retirement plans which eliminates all of their pre-tax IRA balance and then open the opportunity to execute this backdoor Roth IRA contribution strategy.

Pitfall #2: SEP IRA & Simple IRA's count

Many smaller companies and self-employed individuals sponsor SEP IRA’s or Simple IRA Plans. Many individuals just assume that these are “employer sponsored retirement plans” not subject to the aggregation rules. Wrong. In the eyes of the IRS these are “pre-tax IRA’s” and are subject to the aggregation rules. If you have a Simple IRA or SEP IRA, make sure you take this common pitfall into account.

Pitfall #3: Beware IRS Step Transaction Rule

This is probably the most common pitfall that we see when executing this strategy. Individuals and investment advisors alike will make deposits to the non-deductible traditional IRA and then the next day process the conversion to the Roth IRA. In doing this, you run the risk of creating a “step transaction”.

There is a very long explanation tied to “step transactions” and how to avoid a “step transactions” but I will provide you with a brief summary of the concept.

Here it is, if you use legal loop holes in the tax system in an obvious effort to side step other IRS limitations (like the Roth IRA income limit) it could be considered a “step transaction” by the IRS and the IRS may disallow the conversion and assess tax penalties.

Disclosure: Backdoor Roth IRA Conversion Strategy

It is highly recommend that you work closely with your financial advisor and tax advisor to determine whether or not this is a viable wealth accumulation strategy based on your personal financial situation.

Michael Ruger

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

How Much Life Insurance Do I Need?

Do you even need life insurance? If you have dependants to protect and you do not have enough savings, you will most likely need life insurance. But the question is how much should I have? Well, your home will be one of your biggest assets, and in some cases the money that it makes from its sale when you have passed away is a significant inheritance

How Much Life Insurance Do I Need?

Do you even need life insurance? If you have dependants to protect and you do not have enough savings, you will most likely need life insurance. But the question is how much should I have? Well, your home will be one of your biggest assets, and in some cases the money that it makes from its sale when you have passed away is a significant inheritance for your children.

If you do not have dependents or you have enough savings to cover the current and future expenses for your dependents there really is no need for life insurance. Life insurance sales professional can be very aggressive with their sales tactics and sometime they mask their services as "financial planning" but all of their solutions lead to you buying an expensive whole life insurance policy.

Remember, life insurance is simply a transfer of risk. When you are younger, have a family, a mortgage, and are just starting to accumulate assets, the amount of life insurance coverage is usually at its greatest. But as your children grow up, they finish college, you pay your mortgage, you have no debt, and you have accumulated a good amount in retirement savings, your need to transfer that risk diminishes because you have essentially become self-insured. Just because you had a $1M dollar life insurance policy issued 10 years ago does not mean that is the amount you need now.

Which kind of insurance should you get?

It's our opinion that for most individuals term insurance makes the most sense. Insurance agents are always very eager to sell whole life, variable life, and universal life policies. Why? They pay big commissions!! When you compare a $1M 30 year term policy and a $1M Whole Life policy side by side, often times the annual premium for whole life insurance is 10 times that amount of the term insurance policy. Insurance agents will tout that the whole life policy has cash value, you can take loans, and that it's a tax deferred savings vehicle. But often time when you compare that to: "If I just bought the cheaper term insurance and did something else with the money I would have spent on the more expensive whole life policy such as additional pre-tax retirement savings, college savings for the kids, paying down the mortgage, or setting up an investment management account, at the end of the day I'm in a much better spot financially."

How much life insurance do you need?

The most common rule of thumb that I hear is "10 times my annual salary". Please throw that out the window. The amount of insurance you need varies greatly from individual to individual. The calculation to reach the answer is fairly straight forward. Below is the approach we take with our clients:

How much debt do you have? This includes mortgages, car loans, personal loans, credit cards, etc. Your total debt amount is your starting point.

What are your annual expenses? Just create a quick list of your monthly expenses, they do not have to be exact, and our recommendation is to estimate on the high side just to be safe. Then multiply your monthly expense by 12 months to reach your "annual after tax expenses".

How much monthly income do you have to replace? If you are married, we have to look at the income of each spouse. If your monthly expenses are $50,000 per year and the husband earns $30,000 and the wife earns $80,000, we are going to need more insurance on the wife because we have to replace $80,000 per year in income if she were to pass away unexpectedly. Married couples make the mistake of getting the same face value of insurance just because. Look at it from an income replacement standpoint. If you are a single parent or provider, you will just look at the amount of income that is needed to meet the anticipated monthly expenses for your dependents.

Factor in long term savings goals and expenses. Examples of this are the college cost for your children and the annual retirement savings for the surviving spouse.

Example:

Husband: Age 40: Annual Income $70,000

Wife: Age 41: Annual Income $70,000

Children: Age 13 & 10

Total Outstanding Debt with Mortgage: $250,000

Total Annual After Tax Expenses: $90,000

Savings & Investment Accounts: $100,000

Remember there is not a single correct way to calculate your insurance need. This example is meant to help you through the thought process. Let's look at an insurance policy for the husband. We first look at what the duration of the term insurance policy should be. Our top two questions are "when will the mortgage be paid off?" and "when will the kids be done with college?" These are the two most common large expenses that we are insuring against. In this example let's assume they have 20 years left on their mortgage so at a minimum we will be looking at a 20 year term policy since the youngest child will done with their 4 year degree within the next 12 years. So a 20 year term covers both.

Here is how we would calculate the amount. Start with the total amount of debt: $250,000. That is our base amount. Then we need to look at college expense for the kids. Assume $20K per year for each child for a 4 year degree: $160,000. Next we look at how much annual income we need to replace on the husband's life to meet their monthly expense. In this example it will be close to all of it but let's reduce it to $60K per year. It is determined that they will need their current level of income until the mortgage is paid in full so $60,000 x 20 Years = $1,200,000. When you add all of these up they will need a 20 year term policy with a death benefit of $1,610,000. But we also have to take into account that they already have $100,000 in savings and their levels of debt should decrease with each year as time progresses. In this scenario we would most likely recommend a 20 Year Term Policy with a $1.5M death benefit on the husband's life.

The calculation for his wife in this scenario would be similar since they have the same level of income.

Michael Ruger

About Michael.........

Hi, I'm Michael Ruger. I'm the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Paying Down Debt: What is the Best Strategy?

Living with debt is not easy. It can be a constant burden and easily disrupt day-to-day life. Having debt will also ruin your credit score too. The worse your credit score gets, the less likely you will be accepted for any type of loan. One of the fastest ways to get rid of your debt is to pay your debt off in the correct order.

strategies for paying off debt

Living with debt is not easy. It can be a constant burden and easily disrupt day-to-day life. Having debt will also ruin your credit score too. The worse your credit score gets, the less likely you will be accepted for any type of loan. One of the fastest ways to get rid of your debt is to pay your debt off in the correct order.

STEP 1: Create a list of all your current debts

The first step is understanding what you owe. To start, make a master list of all your monthly credit card and loan statements. For each bill, include:

The creditor's name

The total amount you owe on that bill

The minimum required monthly payment

The interest rate (also known as APR)

The payment due date

STEP 2: List all of your monthly expenses

Add up all your monthly expenses: rent, car, food, utilities, health insurance and the minimum payments on your debts; as well as regular spending on things such as entertainment and clothing. Subtract that figure from your monthly after-tax income. The remaining amount is what you could put toward debt repayment each month-though it may make sense for you to save some.

STEP 3: Call your lenders

Call your lenders and explain your situation. They may be willing to lower your interest rate temporarily or waive late fees. You may also be able to lower your interest rate by transferring some high-interest credit card debt onto a new credit card with a lower rate (though that's not a long-term solution).

STEP 4: Payoff high interest rate or small balances first

You can start with the bill carrying the highest interest, or the one with the smallest balance. Prioritizing the highest-rate debt can save you more money: You pay off your most expensive debt sooner. Paying off the smallest debt can eliminate a bill faster, providing a motivating boost. Whichever you choose, make sure to pay at least the minimum on all your debts.

credit card debt

Pay the monthly minimum on each debt. The exception: your target bill. Put more money toward this one to pay it down faster. Once you pay off that bill, choose another to pay down aggressively. Your monthly debt repayment total shouldn't change, even when you eliminate bills. This way you gain momentum as you go, putting more and more money toward each remaining bill.

STEP 5: Get creative

You can use your annual tax refund or holiday bonus to pay down debt. Look for small ways to save money every day, such as riding your bike to work, or eating in instead of dining out. Another way to make a dent quickly is to sell unused or unnecessary belongings-maybe downgrading your car to a more affordable model with lower monthly payments.

STEP 6: Break the cycle

As you start to escape debt, it can be tempting to reward yourself by splurging on a new smartphone or an expensive dinner but just a few purchases can erase all your hard work. Instead, buy things with cash or your debit card, and think long and hard before taking on any new debt.

Read this book

If you want to live a debt free life, I strongly recommend you read the book "Total Money Makeover" by Dave Ramsey. Ramsey's book really paves the way to get out of debt and stay out of debt.

dave ramsey book

Michael Ruger

About Michael.........

Hi, I'm Michael Ruger. I'm the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.