Social Security Filing Strategies

Making the right decision of when to turn on your social security benefit is critical. The wrong decision could cost you tens of thousands of dollars over the long run. Given all the variables surrounding this decision, what might be the right decision for one person may be the wrong decision for another. This article will cover some of the key factors to

Making the right decision of when to turn on your social security benefit is critical. The wrong decision could cost you tens of thousands of dollars over the long run. Given all the variables surrounding this decision, what might be the right decision for one person may be the wrong decision for another. This article will cover some of the key factors to consider:

Normal Retirement Age

First, you have to determine your "Normal Retirement Age" (NRA). This is listed on your social security statement in the "Your Estimated Benefits" section. If you were born between 1955 – 1960, your NRA is between age 66 – 67. If you were born 1960 or later, your NRA is age 67. You can obtain a copy of your statement via the social security website.

Before Normal Retirement Age

You have the option to turn on social security prior to your normal retirement age. The earliest you can turn on social security is age 62. However, they reduce your social security benefit by approximately 7% per year for each year prior to your normal retirement age. See the chart below which illustrates an individual with a normal retirement age of 67. If they turn on their social security benefit at age 62, they would only receive 70% of their full benefit. This reduction is a permanent reduction. It does not increase at a later date, outside of the small cost of living increases.

taking social security early

Taking Social Security Early

The big questions is: “If I start taking it age 62, at what age is the breakeven point?” Remember, if I turn on social security at 62 and my normal retirement age is 67, I have received 5 years of payments from social security. So at what age would I be kicking myself wishing that I had waited until normal retirement age to turn on my benefit. There are a few different ways to calculate this accounting for taxes, the rates of return on other retirement assets, inflations, etc. but in general it’s sometime between the ages of 78 and 82.

Since the breakeven point may be in your early 80’s, depending on your health, and the longevity in your family history, it may or may not make sense to turn on your benefit early. If we have a client that is in ok health but not great health and both of their parents passed way prior to age 85, then it may make sense to for them to turn on their social security benefit early. We also have clients that have pensions and turning on their social security benefit early makes the difference between retiring now or have to work for 5+ more years. As long as the long-term projections work out ok, we may recommend that they turn on their social security benefit early so they can retire sooner.

Are You Still Working?

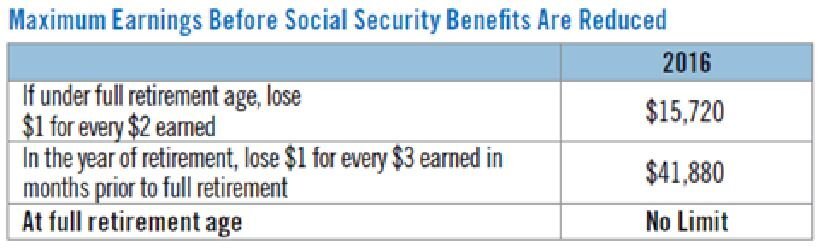

This is a critical question for anyone that is considering turning on their social security benefits early. Why? If you turn on your social security benefit prior to reaching normal retirement age, there is an “earned income” penalty if you earn over the threshold set by the IRS for that year. See the table listed below:

In 2025, for every $2 that you earned over the $23,400 threshold, your social security was reduced by $1. For example, let’s say I’m entitled to $1,000 per month ($12,000 per year) from social security at age 62 and in 2025 I had $25,000 in W2 income. That is $1,600 over the $23,400 threshold for 2025 so they would reduce my annual benefit by $800. Not only did I reduce my social security benefit permanently by taking my social security benefit prior to normal retirement age but now my $12,000 in annual social security payments they are going to reduce that by another $800 due to the earned income penalty. Ouch!!!

Once you reach your normal retirement age, this earned income penalty no longer applies and you can make as much as you want and they will not reduce your social security benefit.

Because of this, the general rule of thumb is if you are still working and your income is above the IRS earned income threshold for the year, you should hold off on turning on your social security benefits until you either reach your normal retirement age or your income drops below the threshold.

Should I Delay May Benefit Past Normal Retirement Age

As was illustrated in first table, if you delay your social security benefit past your normal retirement age, your benefit will increase by approximately 8% per year until you reach age 70. At age 70, your social security benefit is capped and you should elect to turn on your benefits.

So when does it make sense to wait? The most common situation is the one where you plan to continue working past your normal retirement age. It’s becoming more common that people are working until age 70. Not because they necessarily have too but because they want something to keep them busy and to keep their mind fresh. If you have enough income from employment to cover you expenses, in many cases, it does make sense to wait. Based on the current formula, your social security benefit will increase by 8% per year for each year you delay your benefit past normal retirement age. It’s almost like having an investment that is guaranteed to go up by 8% per year which does not exist.

Also, for high-income earners, a majority of their social security benefit will be taxable income. Why would you want to add more income to the picture during your highest tax years? It may very well make sense to delay the benefit and allow the social security benefit to increase.

Death Benefit

The social security death benefit also comes into play as well when trying to determine which strategy is the right one for you. For a married couple, when their spouse passes away they do not continue to receive both benefits. Instead, when the first spouse passes away, the surviving spouse will receive the “higher of the two” social security benefits for the rest of their life. Here is an example:

Spouse 1 SS Benefit: $2,000

Spouse 2 SS Benefit: $1,000

If Spouse 1 passes away first, Spouse 2 would bump up to the $2,000 monthly benefit and their $1,000 monthly benefit would end. Now let’s switch that around, let’s say Spouse 2 passes away first, Spouse 1 will continue to receive their $2,000 per month and the $1,000 benefit will end.

If social security is a large percentage of the income picture for a married couple, losing one of the social security payments could be detrimental to the surviving spouse. Due to this situation, it may make sense to have the spouse with the higher benefit delay receiving social security past normal retirement to further increase their permanent monthly benefit which in turn increases the death benefit for the surviving spouse.

Spousal Benefit

The “spousal benefit” can be a powerful filing strategy. If you are married, you have the option of turning on your benefit based on your earnings history or you are entitled to half of your spouse’s benefit, whichever benefit is higher. This situation is common when one spouse has a much higher income than the other spouse.

Here is an important note. To be eligible for the spousal benefit, you personally must have earned 40 social security “credits”. You receive 1 credit for each calendar quarter that you earn a specific amount. In 2025, the figure was $1,810. You can earn up to 4 credits each calendar year.

Another important note, under the new rules, you cannot elect your spousal benefit until your spouse has started receiving social security payments.

Here is where the timing of the social security benefits come into play. You can turn on your spousal benefit as early as 62 but similar to the benefit based on your own earnings history it will be reduce by approximately 7% per year for each year you start the benefit prior to normal retirement age. At your normal retirement age, you are entitled to receive your full spousal benefit.

What happens if you delay your spousal benefit past normal retirement age? Here is where the benefit calculation deviates from the norm. Typically when you delay benefits, you receive that 8% annual increase in the benefits up until age 70. The spousal benefit is based exclusively on the benefit amount due to your spouse at their normal retirement age. Even if your spouse delays their social security benefit past their normal retirement age, it does not increase the 50% spousal benefit.

Here is the strategy. If it’s determined that the spousal benefit will be elected as part of a married couple’s filing strategy, since delaying the start date of the benefits past normal retirement age will only increase the social security benefit for the higher income earning spouse and not the spousal benefit, in many cases, it does not make sense to delay the start date of the benefits past normal retirement age.

Divorce

For divorced couples, if you were married for at least 10 years, you can still elect the spousal benefit even though you are no longer married. But you must wait until your ex-spouse begins receiving their benefits before you can elect the spousal benefit.

Also, if you were married for at least 10 years, you are also entitled to the death benefit as their ex-spouse. When your ex-spouse passes away, you can notify the social security office, elect the death benefit, and you will receive their full social security benefit amount for the rest of your life instead of just 50% of their benefit resulting from the “spousal benefit” calculation.

Whether or not your ex-spouse remarries has no impact on your ability to elect the spousal benefit or death benefit based on their earnings history.

Consult A Financial Planner

Given all of the variables in the mix and the importance of this decision, we strongly recommend that you consult with a Certified Financial Planner® before making your social security benefit elections. While the interaction with a fee-based CFP® may cost you a few hundred dollars, making the wrong decision regarding your social security benefits could cost you thousands of dollars over your lifetime. You can also download a Financial Planner Budget Worksheet to give you that extra help when sorting out your finances and monthly budgeting.

About Michael.........

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Equifax Data Breach: How To Protect Yourself

Equifax, a credit agency, had a data breach that resulted in an estimated 143 million people having their personal information compromised. Surprisingly enough, the greatest risk is right not now but rather a few months down the road. After your data is stolen, your information is sold on the black market, and then the bad guys figure out how they

Equifax, a credit agency, had a data breach that resulted in an estimated 143 million people having their personal information compromised. Surprisingly enough, the greatest risk is right not now but rather a few months down the road. After your data is stolen, your information is sold on the black market, and then the bad guys figure out how they are going to use your personal information to maximize their financial gain. So there is delay between the time that your information is stolen and when the fraudulent activity using your data begins.

In this article we are going to discuss the top ways to protect your credit from fraudulent activity. Here are the main steps

Monitor your financial activity closely

Run a free credit report

Consider "Freezing" your credit

Step 1: Monitor Your Financial Activity Closely

Make sure you keep a close eye on each transaction running through your checking account and credit card. This is often the first place that signs of fraudulent activity surfaces. If for some reason you cannot identify a charge to your card or bank account, make sure you contact your financial institution immediately.

Use Credit Cards, Not Debit Cards

Along these lines we strongly recommend that you use a credit card instead of a debit card and just payoff the balance of the credit card each month. If your debit card information is compromised and the "bad guys" charge $1,000 to the card, the $1,000 is actually pulled out of your checking account. You now have to report the fraudulent activity and get your money back. Instead, if your credit card is compromised and they make the $1,000 fraudulent transaction, you notify the credit card company but you are not out the $1,000. They just remove the charge from the bill and the credit card tracks down the bad guys. You should only be using your debit card for ATM withdrawals.

Step 2: Run A Free Credit Report

You should get in the habit of running a credit report on yourself once a year. These credit reports list all of your current creditors: car loans, mortgage, credit cards, store charge accounts, credit lines, etc. If you see a creditor on the list that you cannot identify that is a big red flag. If your data is compromised, the bad guys may use your data to apply for a credit card without your knowledge. The only way that you would find out that the fraudulent account existed is by running a credit report on yourself. Running your credit report once a year does not hurt your credit score. It's only if you are running your credit report more frequently that it could impact your credit score. Frequent credit runs can give the impression that you are eagerly searching for more credit and it can lower your credit score.

You can run a free credit report at www.annualcreditreport.com or you can request one from your bank or credit union.

Step 3: Consider Freezing Your Credit

One of the best ways to protect yourself is to freeze your credit with the 3 credit bureaus. There 3 credit bureaus are:

Equifax

Experian

TransUnion

A credit freeze means if someone tries to access your credit to establish a credit card, car loan, whatever it is, the request for the credit report will reject. When you set up the credit freeze each of the bureaus will you with a login or a pin number that allows you to "unfreeze" your credit for a selected period of time. If you have implemented a credit freeze and you apply for a car loan, you would follow the steps below:

Ask the dealership which credit bureau they run their reports through

Login to your account at that credit bureau

Unfreeze your credit report for a selected period of time

Notify the dealership of the limited time window to request the credit report

The window will automatically close and your credit will "re-freeze"

The credit freeze is simple to implement and it can be implemented by visiting the website of each credit bureau. You can also implement the freeze by calling the credit bureau but the on hold wait time is so long that we recommend to our clients implement the freeze via the web.Below is great video that walks you though what the online freezing process looks like:

Don't Use Public Wifi

One last tip to protect your information, do not use public wifi networks. It's tempting if you are at a coffee shop, hotel, or airport to access their free wifi network but it's the wrong move. There are individuals that have special programs that hack into the wireless network and see everything that you are looking at on your laptop or mobile device. If you are going to use a wireless network, make sure it is secure.

About Michael.........

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

How Does A Simple IRA Plan Work?

Not every company with employees should have a 401(k) plan. In many cases, a Simple IRA plan may be the best fit for a small business. These plans carry the following benefits

Not every company with employees should have a 401(k) plan. In many cases, a Simple IRA plan may be the best fit for a small business. These plans carry the following benefits

No TPA fees

Easy to setup & operate

Employee attraction and retention tool

Pre-tax contributions for the owners to lower their tax liability

Your company

To be eligible to sponsor a Simple IRA, your company must have less than 100 employees. The contribution limits to these plans are about half that of a 401(k) plan but it still may be the right fit for you company. Here are some of the most common statements that we hear from the owners of the business that would lead you to considering a Simple IRA plan over a 401(k) plan:

"I want to put a retirement plans in place for my employees that has very low fees and is easy to operate."

"We are a start-up, we don't have a lot of money to contribute to the plan as the owners, but we want to put a plan in place to attract and retain employees."

"I plan on contributing $15,000 per year to the plan, even if I sponsored a plan that allowed me to contribute more I wouldn't because I'm socking all of the profits back into the business"

"I have a SEP IRA now but I just hired my first employee. I need to setup a different type of plan since SEP IRA's are 100% employer funded"

Establishment Deadline

The deadline to establish a Simple IRA plan is October 1st. Once you have cross over that date, you would have to wait until the following calendar year to set the plan.

Eligibility

The eligibility requirements for a Simple IRA are different than a SEP IRA or 401(k) plans. Unlike these other plan "1 Year of Service" = $5,000 of compensation earned in a calendar year. If you want to only cover "full-time" employees with your retirement plan, you may need to consider a 401(k) plan which has the 1 year and 1000 hours requirement to obtain a year of service. The most restrictive "wait time" that you can put into place is 2 years. Meaning an employee must obtain 2 years of service before they are eligible to start contributing to the plan. You can also be more lenient that 2 years, such as immediate entry or a 1-year wait, but 2 years is the most restrictive it can be.

Types of Contributions

Like a 401(k) plan, Simple IRA have both employee deferral contributions and employer contributions.

Employee Deferrals

Eligible employees are allowed to make pre-tax contributions to their Simple IRA accounts. The contribution limits are less than a traditional 401(k). Below is a tale comparing the 2021 contribution limits of a Simple IRA vs a 401(k) Plan:

There are not Roth deferrals allows in Simple IRA plans.

Employer Contributions

Unlike other employer sponsored retirement plans, employer contributions are mandatory each year to a Simple IRA plan. The company must choose between two pre-set employer contribution formulas:

2% Non-elective

3$ Matching contribution

With the 2% non-elective contribution, the company must contribute 2% of each eligible employee’s compensation to the plan whether they contribute to the plan or not.

For the 3% matching contribution, it’s a dollar for dollar match up to 3% of compensation that they employee contributes to the plan. The match formula is more popular than the 2% non-elective contribution because the company only must contribute if the employee contributes.

Special 1% Rule

With the employer matching contribution there is also a special rule. In 2 out of any 5 consecutive years, the company can lower the employer match to as low as 1% of pay. We will often see start-up company's take advantage of this rule by putting a 1% employer match in place for the first 2 years of the plan to minimize costs and then they are committed to making the 3% match for years 3, 4, and 5.

100% Vesting

All employer contributions to Simple IRA plans are 100% vested. The company is not allowed to attach a "vesting schedule" to the contributions.

Important Compliance Requirements

Make sure you have a 5304 Simple Form in your files for each year you sponsor the Simple IRA plan. If you are audited by the IRS or DOL, they will ask for these forms. You need to distribute this form to all of your employee each year between Nov 1st and Dec 1st for the upcoming plan year. The documents notifies your employees that:

A retirement plan exists

Plan eligibility requirement

Employer contribution formula

Who they submit their deferral elections to within the company

If you do not have this form on file, the IRS will assume that you have immediate eligibility for your Simple IRA plan, meaning that all of your employees are due employer contributions since day one of employment. Even employee that used to work for you and have since terminated employment. It’s an ugly situation.

Make sure the company is timely when submitting the employee deferrals to the Simple IRA plan. Since you are withholding money from employees pay for the salary deferrals the IRS want you to send that money to their Simple IRA accounts “as soon as administratively feasible”. The suggested time phrase is within a week of the deduction in payroll. But you must be consistent with the timing of your remittances to your Simple IRA plan. If you typically submit contributions to your Simple IRA provider 5 days after a payroll run but one week you randomly submit it 2 days after the payroll run, 2 days just became the rule and all of the other deferral remittances are “late”. The company will be assessed penalties for all of the late deferral remittances. So be consistent.

Cannot Terminate Mid-Year

Unlike other retirement plans, you cannot terminate a Simple IRA plan mid-year. Simple IRA plan termination are most common when a company started with a Simple IRA, has grown in employee head count, and now wishes to put a 401(k) plan in place. You must wait until after December 31st to terminate the Simple IRA plan and implement the new 401(k) plan.

Special 2 Year Rule

If you replace your Simple IRA with a 401(k) plan, the balances in the Simple IRA can usually be rolled over into the new 401(k) if the employee elects to do so. However, be very careful of the special Simple IRA 2 Year Distribution Rule. If you process any type of distribution from a Simple IRA, within a two-year period of the employee depositing their first dollar to the account, and the employee is under 59½, they are hit with a 25% IRS penalty. THIS ALSO APPLIES TO DIRECT ROLLOVERS. Normally when you process a direct rollover from one retirement plan to another, no taxes or penalties are assessed. That is not the case in Simple IRA plan so be care of this rule. If you decide to switch from a Simple IRA to a 401(k), make sure you run a list of all the employees that maintain a balance in the Simple IRA plan to determine which employees are subject to the 2-year withdrawal restriction.

About Michael.........

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Watch These Two Market Indicators

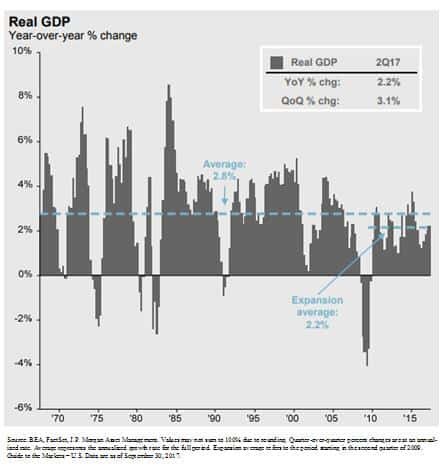

While a roaring economy typically rewards equity investors, the GDP growth rate in the U.S. has continued to grow at that same 2.2% pace that we have seen since the recovery began in March 2009. When you compare that to the GDP growth rates of past economic expansions, some may classify the current growth rate as “sub par”. As in the tale of the

While a roaring economy typically rewards equity investors, the GDP growth rate in the U.S. has continued to grow at that same 2.2% pace that we have seen since the recovery began in March 2009. When you compare that to the GDP growth rates of past economic expansions, some may classify the current growth rate as “sub par”. As in the tale of the tortoise and the hare, sometimes slow and steady wins the race.

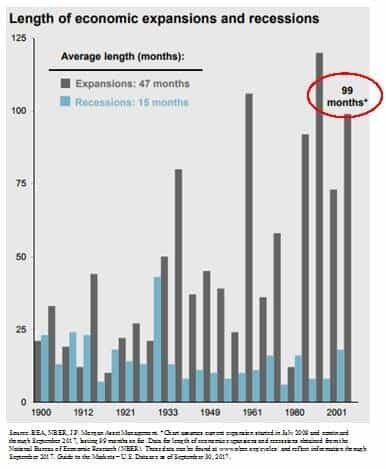

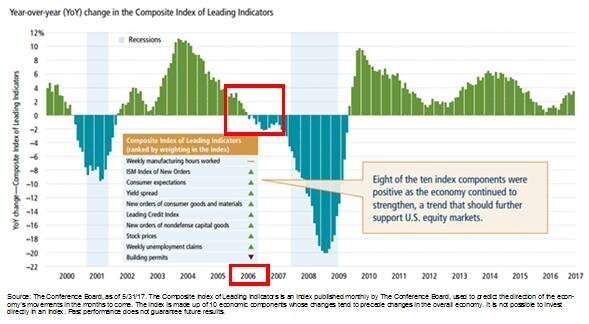

The number one questions on investor’s minds: “It’s been a great rally but are we close to the end?” Referencing the chart below, if you look at the length of the current economic expansion, going back to 1900 we are now witnessing the 3rd longest economic expansion on record which is making investors nervous because as we all know that markets work in cycles.

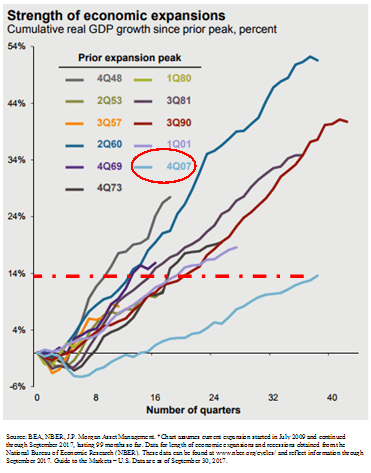

However, if you ignore the “length” of the rally for a moment and look at the “magnitude” of the rally it would seem that total GDP growth of the current economic expansion has been relatively tame compared to some of the economic recoveries in the past. See the chart below. The chart shows evidence that there have been economic rallies in the past that were shorter in duration but greater in magnitude. This may indicate that we still have further to go in the current economic expansion.

What causes big rallies to end?

Looking back at strong economic rallies in the past, the rallies did not die of old age but rather there was an event that triggered the next recession. So we have to be able identify trends within the economic data that would suggest that the economic expansion has ended and it will lead to the next recession.

Watch these two indicators

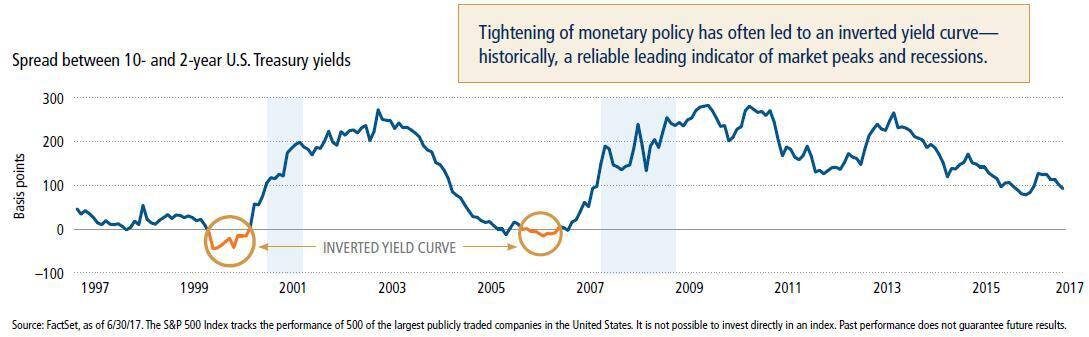

Two of the main indicators that we monitor to determine where we are in the current economic cycle are the Leading Indicators Index and the Yield Curve. History rarely repeats itself but it does rhyme. Look at the chart of the leading indicators index below. The leading indicators index is comprised of multiple economic indicators that are considered “forward looking”, like housing permits. If there are a lot of housing permits being issues, then demand for housing must be strong, and a strong housing market could lead to further economic growth. Look specifically at 2006. The leading indicators went negative in 2006, over a year before the stock market peaked in 2007. This indicator was telling us there was a problem before a majority of investors realized that we were on the doorstep of the recession.

Let’s look at the second key indicator, the yield curve. You will hear a lot about the “slope of the yield curve” in the media. In a healthy economy, long term interest rates are typically higher than short term rates which results in a “positively slopped” yield curve. In other words, when you go to the bank and you have the choice of buying a 2 year CD or a 10 year CD, you would expect to receive a higher interest rate on the 10 year CD because they are locking up your money for 10 years instead of 2.

There are periods of time where the interest rate on a 10 year government bond will drop below the interest rate on a 2 year government bond which is considered an “inverted yield curve”. Why does this happen and why would investors by that 10 year bond that is yielding less than the 2 year bond? This happens because bond investors are predicting an economic slowdown in the foreseeable future. They want to lock in the current 10 year interest rate knowing that if the economy goes into a recession that the Fed may begin to lower the Fed Funds Rate which has a more rapid impact on short term rates. It’s a bet that the 2 year bond rate will drop below the 10 year bond rate within the next few years.

If you look at the historical chart of the yield curve above, the yield curve inverted prior to the recession in the early 2000’s and prior to the 2008 recession.

Looking at where we sit today, within the last 6 months the leading indicators index has not only been positive but it’s accelerating and the yield curve is still positively sloped. While we realize that there is not a single indicator that accurately predicts the end of a market cycle, these particular economic indicators have historically been helpful in predicting danger ahead.

There will always be uncertainty in the world. Currently it has taken the form of U.S, politics, tax reforms, geopolitical events, and global monetary policy but it would seem that based on the hard economic data here in the U.S. that our economic expansion that began in March 2009 may still have further to go.

About Michael.........

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

How Does A SEP IRA Work?

SEP stands for “Simplified Employee Pension”. The SEP IRA is one of the most common employer sponsored retirement plans used by sole proprietors and small businesses.

What is a SEP?

SEP stands for “Simplified Employee Pension”. The SEP IRA is one of the most common employer sponsored retirement plans used by sole proprietors and small businesses.

Special Establishment Deadline

SEP are one of the few retirement plans that can be established after December 31st which make them a powerful tax tool. For example, it’s March, you are meeting with your accountant and they deliver the bad news that you have a big tax bill that is due. You can setup the SEP IRA any time to your tax filing date PLUS extension, fund it, and capture the tax deduction.

Easy to Setup & Low Plan Fees

The other advantage of SEP IRA’s is they are easy to setup and you do not have a third-party administrator to run the plan, so the costs are a lot lower than a traditional 401(k) plans. These plans can typically be setup with 24 hours.

Contributions limits

SEP IRA contributions are expressed as a percentage of compensation. The maximum contribution is either 20% of the owners “net earned income” or 25% of the owners W2 wages. It all depends on how your business is incorporated. You have the option to contribution any amount less than the maximum contribution.

100% Employer Funded

SEP IRA plans are 100% employer funded meaning there is no employee deferral piece. Which makes them expense plans to sponsor for a company that eligible employees because the employer contribution is uniform for all employees. Meaning if the owner contributes 20% of their compensation to the plan for themselves they must also make a contribution equal to 20% of compensation for each eligible employee. Typically, once employees begin becoming eligible for the plan, a company will terminate the SEP IRA and replace it with either a Simple IRA or 401(k) plans.

Employee Eligibility Requirements

An employee earns a “year of service” for each calendar year that they earn $500 in compensation. You can see how easy it is to earn a “year of service” in these types of plans. This is where a lot of companies make an error because they only look at their “full time employees” as eligible. The good news for business owners is you can keep employees out of the plan for 3 years and then they become eligible in the 4th year of employment. For example, I am a sole proprietor and I hire my first employee, if my plan document is written correctly, I can keep that employee out of the SEP IRA for 3 years and then they will not be eligible for the employer contribution until the 4th year of employment.

Read This……..Very Important…..

There is a plan document called a 5305 SEP form that is required to sponsor a SEP IRA plan. This form can be printed off the IRS website or is sometimes provide by the investment platform for your plan. Remember, SEP IRA plans are “self-administered” meaning that you as the business owner are responsible for keeping the plan in compliance. Do cannot always rely on your investment advisor or accountant to help you with your SEP IRA plan. You should have a 5305 SEP for in your employer files for each year you have sponsored the plan. This form does not get filed with the IRS or DOL but rather is just kept in your employer files in the case of an audit. You are required to give this form to all employees of the company each year. It’s a way of notifying your employees that the plan exists and it lists the eligibility requirements.

Compliance Issues

The main compliance issues to watch out for with these plan is not having that 5305 SEP Form for each year the plan has been sponsored, not accurately identifying eligible employees, and miscalculating your “net earned income” for the max SEP IRA contribution.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

How Do Single(k) Plans Work?

A Single(k) plan is an employer sponsored retirement plan for owner only entities, meaning you have no full-time employees. These owner only entities get the benefits of having a full fledge 401(k) plan without the large administrative costs associated with traditional 401(k) plans.

What is a Single(k) Plan?

A Single(k) plan is an employer-sponsored retirement plan for owner-only entities, meaning you have no full-time employees. These owner-only entities get the benefits of having a full-fledged 401(k) plan without the large administrative costs associated with traditional 401(k) plans.

What is the definition of a “full-time” employee?

Oftentimes, a small company will have some part-time staff. It does not matter whether you consider them “part-time”, the definition of full-time employee is defined by the IRS as working 1000 hours in a 12-month period. If you have a “full-time” employee, you would not be eligible to sponsor a Single(k) plan.

Types of Contributions

There are two types of contributions to these plans. Employee deferral contributions and employer profit sharing contributions. The employee deferral piece works like a 401(k) plan. If you are under the age of 50 you can contribute $23,500, in 2025, in employee deferrals. If you are 50-59 or 64 or older, you get the $7,500 catch up contribution so you can contribute $31,000 in employee deferrals. Beginning in 2025, if you are age 60-63, instead of the $7,500 catch-up, you can contribute an additional $11,250 for a total of $34,750 in employee deferrals.

The reason why these plans are a little different than other employer sponsored plans is the employee deferral piece allows you to put 100% of your compensation into these plans up to those dollar thresholds.

In addition to the employee deferrals, you can also contribute 20% of your net earned income in the form of a profit-sharing contribution. For example, if you make $100,000 in net earned income from self-employment and you are age 53, you could contribute $31,000 in employee deferrals and then you could contribute an additional $20,000 in the form of a profit-sharing contribution. Making your total pre-tax contribution $51,000.

Establishment Deadline

The deadline for establishing a Solo(k) plan varies based on how the business is incorporated. If the business is an S-Corp or multi-member partnership, the business owner(s) must have the Solo(k) plan setup by December 31st. If the business is a sole proprietor or single member LLC, the Solo(k) plan can be setup by the tax filing deadline plus extension.

Loans & Roth Deferrals

Single(k) plans provide all of the benefits to the owner of a full 401(k) plan at a fraction of the cost. You can set up the plan to allow 401(k) loan and Roth deferral contributions.

SEP IRA vs Single(k) Plans

A lot of small business owners find themselves in a position where they are trying to decide between setting up a SEP IRA or a Single(k) plan. One of the big factors, that is often times the deciding factor, is how much the owner intends to contribute to the plan. The SEP IRA limits the business owner to just the 20% of net earned income. Whereas the Single(k) plan allows the 20% of net earned income plus the employee deferral contribution amount. However, if 20% of your net earned income would satisfy your target amount then the SEP IRA may be the right choice.

Advanced Strategy Using A Single(k) Plan

Here is a great tax strategy if you have one spouse that is the primary breadwinner bringing in most of the income and the other has self-employment income for a side business. If the spouse with the self-employment income is over the age of 50 and makes $20,000 in net earned income, they could set up a Single(k) Plan and defer the full $20,000 into their Single(k) plan as employee deferrals. If they had a SEP IRA, the max contribution would have been $4,000.

A huge tax savings for a married couple that is looking to lower their tax liability.

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally , professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, pleas feel free to join in on the discussion or contact me directly.

Can I Negotiate A Car Lease Buyout?

The short answer is "yes", but the approach that you take will most likely determine whether or not you are successful at purchasing your vehicle for a lower price than the amount listed in the lease agreement. When you lease a car, the lease agreement typically includes an amount that you can purchase the car for at the end of the lease. That amount is

The short answer is "yes", but the approach that you take will most likely determine whether or not you are successful at purchasing your vehicle for a lower price than the amount listed in the lease agreement. When you lease a car, the lease agreement typically includes an amount that you can purchase the car for at the end of the lease. That amount is essentially a guess by the bank that is providing the financing for the lease as to what the future value of your vehicle will be at the end of the lease.

Lease Buyout Calculation

Step number one in the negotiation process is to determine what your vehicle is worth. Did the bank guess right or wrong? If the purchase amount in your lease agreement is $25,000 but you find that the vehicle, based on current market conditions, is only worth $18,000, you probably have room to negotiate the purchase price of your vehicle but you have to do your homework. Compare your vehicle's purchase price to the retail value of local auto dealers. If you can show the bank that there is a local auto dealer trying to sell the exact make and model of your leased car with similar mileage, the bank will be more likely to accept a lower purchase price realizing that they guessed wrong.

Deal Directly With The Bank

You may have noticed that I continue to reference the "bank" in the negotiation process and not the "dealer". This is intentional. Some leasing banks allow dealers to increase the cost of the lease buyout to make a profit. Dealers can also charge document fees, which are taxable in most states. It may also be advantageous to line up your own financing for the lease purchase amount before entering into the negotiation process. If the dealer arranges the financing for you, it can sometimes increase your interest rate to make more money on the purchase. By dealing directly with the leasing bank you can cut out these additional costs.

You Make The Offering Price

Start by making an offer to the leasing bank based on your market research. Also make sure you contact the leasing bank well in advance of the lease "turn-in date". The bank may not be able to provide you with an immediate response to your offer so give yourself plenty of time for the negotiation process to work.

About Michael.........

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog. I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Can I Use My 401K or IRA To Buy A House?

The most difficult part of buying a house is coming up with the down payment. This leads to the question, "Can I access cash in my retirement accounts to help toward the down payment on my house?". The short answer is in most cases, "Yes". The next important questions is "Is it a good idea to take a withdrawal from my retirement account for the down

The most difficult part of buying a house is coming up with the down payment. This leads to the question, "Can I access cash in my retirement accounts to help toward the down payment on my house?". The short answer is in most cases, "Yes". The next important questions is "Is it a good idea to take a withdrawal from my retirement account for the down payment given all of the taxes and penalties that I would have to pay?" This article aims to answer both of those questions and provide you with withdrawal strategies to help you avoid big tax consequences and early withdrawal penalties.

401(k) Withdrawal Options Are Not The Same As IRA's

First you have to acknowledge that different types of retirement accounts have different withdrawal options available. The withdrawal options for a down payment on a house from a 401(k) plan are not the same a the withdrawal options from a Traditional IRA. There is also a difference between Traditional IRA's and Roth IRA's.

401(k) Withdrawal Options

There may be loan or withdrawal options available through your employer sponsored retirement plan. I specifically say "may" because each company's retirement plan is different. You may have all or none of the options available to you that will be presented in this article. It all depends on how your company's 401(k) plan is designed. You can obtain information on your withdrawal options from the plan's Summary Plan Description also referred to as the "SPD".

Taking a 401(k) loan.............

The first option is a 401(k) loan. Some plans allow you to borrow 50% of your vested balance in the plan up to a maximum of $50,000 in a 12 month period. Taking a loan from your 401(k) does not trigger a taxable event and you are not hit with the 10% early withdrawal penalty for being under the age of 59.5. 401(k) loans, like other loans, change interest but you are paying that interest to your own account so it is essentially an interest free loan. Typically 401(k) loans have a maximum duration of 5 years but if the loan is being used toward the purchase of a primary residence, the duration of the loan amortization schedule can be extended beyond 5 years if the plan's loan specifications allow this feature.

Note of caution, when you take a 401(k) loan, loan payments begin immediately after the loan check is received. As a result, your take home pay will be reduced by the amount of the loan payments. Make sure you are able to afford both the 401(k) loan payment and the new mortgage payment before considering this option.

The other withdrawal option within a 401(k) plan, if the plan allows, is a hardship distribution. As financial planners, we strongly recommend against hardship distributions for purposes of accumulating the cash needed for a down payment on your new house. Even though a hardship distribution gives you access to your 401(k) balance while you are still working, you will get hit with taxes and penalties on the amount withdrawn from the plan. Unlike IRA's which waive the 10% early withdrawal penalty for first time homebuyers, this exception is not available in 401(k) plans. When you total up the tax bill and the 10% early withdrawal penalty, the cost of this withdrawal option far outweighs the benefits.

If You Have A Roth IRA.......Read This.....

Roth IRA's can be one of the most advantageous retirement accounts to access for the down payment on a new house. With Roth IRA's, you make after tax contributions to the account, and as long as the account has been in existence for 5 years and you are over the age of 59� all of the earnings are withdrawn from the account 100% tax free. If you withdraw the investment earnings out of the Roth IRA before meeting this criteria, the earnings are taxed as ordinary income and a 10% early withdrawal penalty is assessed on the earnings portion of the account.

What very few people know is if you are under the age of 59� you have the option to withdraw just your after-tax contributions and leave the earnings in your Roth IRA. By doing so, you are able to access cash without taxation or penalty and the earnings portion of your Roth IRA will continue to grow and can be distributed tax free in retirement.

The $10,000 Exclusion From Traditional IRA's.......

Typically if you withdraw money out of your Traditional IRA prior to age 59� you have to pay ordinary income tax and a 10% early withdrawal penalty on the distribution. There are a few exceptions and one of them is the "first time homebuyer" exception. If you are purchasing your first house, you are allowed to withdrawal up to $10,000 from your Traditional IRA and avoid the 10% early withdrawal penalty. You will still have to pay ordinary income tax on the withdrawal but you will avoid the early withdrawal penalty. The $10,000 limit is an individual limit so if you and your spouse both have a traditional IRA, you could potentially withdrawal up to $20,000 penalty free.

Helping your child to buy a house..........

Here is a little known fact. You do not have to be the homebuyer. You can qualify for the early withdrawal exemption if you are helping your spouse, child, grandchild, or parent to buy their first house.

Be careful of the timing rules..........

There is a very important timing rule associated with this exception. The closing must take place within 120 day of the date that the withdrawal is taken from the IRA. If the closing happens after that 120 day window, the full 10% early withdrawal penalty will be assessed. There is also a special rollover rule for the first time homebuyer exemption which provides you with additional time to undo the withdrawal if need be. Typically with IRA's you are only allowed 60 days to put the money back into the IRA to avoid taxation and penalty on the IRA withdrawal. This is called a "60 Day Rollover". However, if you can prove that the money was distributed from the IRA with the intent to be used for a first time home purchase but a delay or cancellation of the closing brought you beyond the 60 day rollover window, the IRS provides first time homebuyers with a 120 window to complete the rollover to avoid tax and penalties on the withdrawal.

Don't Forget About The 60 Day Rollover Option

Another IRA withdrawal strategy that is used as a “bridge solution” is a “60 Day Rollover”. The 60 Day Rollover option is available to anyone with an IRA that has not completed a 60 day rollover within the past 12 months. If you are under the age of 59.5 and take a withdrawal from your IRA but you put the money back into the IRA within 60 days, it’s like the withdrawal never happened. We call it a “bridge solution” because you have to have the cash to put the money back into your IRA within 60 days to avoid the taxes and penalty. We frequently see this solution used when a client is simultaneously buying and selling a house. It’s often the intent that the seller plans to use the proceeds from the sale of their current house for the down payment on their new house. Unfortunately due to the complexity of the closing process, sometimes the closing on the new house will happen prior to the closing on the current house. This puts the homeowner in a cash strapped position because they don’t have the cash to close on the new house.

As long as the closing date on the house that you are selling happens within the 60 day window, you would be able to take a withdrawal from your IRA, use the cash from the IRA withdrawal for the closing on their new house, and then return the money to your IRA within the 60 day period from the house you sold. Unlike the “first time homebuyer” exemption which carries a $10,000 limit, the 60 day rollover does not have a dollar limit.

About Michael.........

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.