How to Minimize Taxes on Social Security

Many retirees are surprised to find that up to 85% of their Social Security benefits could be taxable. But with the right planning, it's possible to reduce or even eliminate those taxes.

The IRS determines how much of your Social Security is taxable using your provisional income, which includes:

Your adjusted gross income (AGI)

Plus any tax-exempt interest (such as from municipal bonds)

Plus 50% of your annual Social Security benefit

Example:

If your AGI is $20,000, you receive $5,000 in municipal bond interest, and your annual Social Security benefit is $30,000, your provisional income would be $40,000 — putting you in the 50% taxable range if you file your taxes married filing joint.

Based on this calculation, here are the income thresholds that determine how much of your benefit is taxable:

Single filers

$25,000 to $34,000 in provisional income: up to 50% of benefits may be taxable

Over $34,000: up to 85% may be taxable

Married filing jointly

$32,000 to $44,000 in provisional income: up to 50% of benefits may be taxable

Over $44,000: up to 85% may be taxable

Note: This doesn’t mean your benefits are taxed at 85%. Rather, it means up to 85% of your benefit amount is included in your taxable income and taxed at your ordinary income tax rate.

Strategies to Reduce or Eliminate Social Security Taxes

1. Delay Taking Social Security

Delaying benefits until age 70 not only increases your monthly payout, but also creates an income “gap window” where you can take advantage of other planning opportunities — such as Roth conversions — before your benefit starts impacting your tax return.

2. Draw Down Pre-Tax Assets Before Claiming

In the early years of retirement, before beginning Social Security, consider withdrawing from traditional IRAs or 401(k)s. These distributions are taxable now, but doing so may reduce your future required minimum distributions (RMDs), which in turn lowers taxable income once you begin collecting Social Security.

3. Consider Roth Conversions

Similar to item 2, Roth conversions allow you to shift money from a traditional IRA to a Roth IRA, paying tax now in order to avoid higher taxes later. By shifting money from a Traditioanl IRA to a Roth IRA prior to starting your social security benefit, it may keep you in lower tax brackets in future years especially when RMDs (requirement minimum distribution) begin at age 73 or 75. Also, once in a Roth IRA, future withdrawals are tax-free and do not count toward provisional income — helping keep more of your Social Security sheltered from taxation.

Note: Keep in mind that conversions count as income in the year they’re done — and can impact provisional income temporarily.

4. Use Qualified Charitable Distributions (QCDs)

QCDs allow individuals age 70½ or older to donate up to $100,000 per year directly from an IRA to a qualified charity. These donations count toward your RMD but are excluded from taxable income.

Clarification: The $100,000 QCD limit applies per individual IRA owner — so a married couple could potentially exclude up to $200,000 in charitable distributions if each spouse qualifies.

This is another way to reduce the size of a pre-tax retirement account balance which counts toward the RMD calculation. Also since the QCD counts toward the RMD amount it can reduce your taxable income, potentially making less of your Social Security benefit subject to taxation at the federal level.

Example: Sue is 78 and is required to take RMD from her traditional IRA of $10,000. Sue decides to process a QCD from her IRA sending $10,000 to her church. She has met the RMD requirement but the $10,000 does not represent taxable income to Sue. Sue’s provision income as a single filer is $30,000 making her Social Security benefit 50% taxable. If she did not process the QCD, that would have raised her provisional income to $40,000 making 85% of her social security benefit subject to taxation.

5. Be Cautious With Tax-Free Interest

Although interest from municipal bonds is federally tax-exempt and potentially state income tax, it is included in the provisional income calculation. If your portfolio includes significant tax-free bond income, it could unintentionally push you into the 50% or 85% taxable Social Security range.

Final Thoughts

Social Security is a cornerstone of retirement income, but managing how it’s taxed is just as important as deciding when to claim. The key to minimizing Social Security taxes is planning around when you claim benefits and where your income is coming from. Strategies like Roth conversions, QCDs, and pre-Social Security IRA withdrawals can all work together to help you keep more of your benefits.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

How does the IRS determine how much of my Social Security is taxable?

The IRS uses your “provisional income” to determine taxation, which includes your adjusted gross income (AGI), tax-exempt interest, and 50% of your annual Social Security benefits. Depending on your filing status and total provisional income, up to 50% or 85% of your Social Security benefits may be taxable.

What are the income thresholds for Social Security taxation?

For single filers, provisional income between $25,000 and $34,000 makes up to 50% of benefits taxable, and income above $34,000 makes up to 85% taxable. For married couples filing jointly, the 50% range applies between $32,000 and $44,000, with anything above $44,000 potentially making up to 85% taxable.

Does “85% taxable” mean I pay 85% tax on my benefits?

No. It means that up to 85% of your Social Security benefit is included in your taxable income and taxed at your ordinary income tax rate. You’re not taxed at 85%; rather, that portion is subject to your regular tax bracket.

How can I reduce or avoid taxes on my Social Security benefits?

You can lower taxable income by delaying Social Security, making Roth conversions before claiming benefits, or drawing down pre-tax accounts early in retirement. Using qualified charitable distributions (QCDs) from IRAs after age 70½ can also reduce taxable income and lower how much of your benefit is taxed.

How do Qualified Charitable Distributions (QCDs) affect Social Security taxation?

QCDs let you donate up to $100,000 per year directly from an IRA to a charity, satisfying required minimum distributions (RMDs) without increasing taxable income. By lowering your income, QCDs can reduce the portion of your Social Security benefits subject to tax.

Does tax-free interest from municipal bonds affect Social Security taxation?

Yes. Although municipal bond interest is exempt from federal income tax, it is included in the provisional income formula. Large amounts of tax-free interest can unintentionally increase the taxable portion of your Social Security benefits.

Does Changing Your State of Domicile Allow You To Avoid Paying Capital Gains Tax?

As individuals approach retirement, they often ask the tax question, “If I were to move to a state that has no state income tax in retirement, would it allow me to avoid having to pay capital gains tax on the sale of my investments or a rental property?” The answer depends on a few variables.

As individuals approach retirement, they will often ask the tax question, “If I were to move to a state that has no state income tax in retirement, would it allow me to avoid having to pay capital gains tax on the sale of my investments or a rental property?”. The answer depends on the following variables:

What type of asset did you sell?

When did you sell it?

What are the requirements to change domicile to another state?

Selling A Rental Property

We will start off by looking at the Rental Property sale scenario. If someone owns an investment property in New York and they plan to move to Florida the following year, would it be better to wait to sell the property until after they have officially changed their domicile to Florida to potentially avoid having to pay state income tax on the gain to New York? Or would they have to pay tax to New York either way?

Unfortunately, it is the latter of the two. If you own real estate in a state that has income tax and your property has gone up in value, you’ll have to pay tax on the gain to that state when you sell it—regardless of where you live. When someone pays tax to a state other than their state of domicile, they normally receive a credit for the tax paid to offset any tax owed to their state of domicile and avoid double taxation. But that raises the obvious question: What if the state of domicile has no income tax? What happens to the credit? Answer: it’s lost. In the example of someone domiciled in Florida—a state with no income tax—who sells a property in New York, which does have a state income tax, they would owe tax to New York on the gain. However, because Florida has no income tax, there would be nothing to offset, and the credit for taxes paid to New York is effectively lost.

Selling A Primary Residence

While selling a primary residence follows the real estate rules that we just covered, the one main difference is that there is a large gain exclusion when someone sells their primary residence, that does not apply to investment properties. The gain exclusion amounts are as follows:

Single Filer: $250,000

Married Filing Joint: $500,000

Based on these exclusion amounts, someone filing a joint tax return would have to realize a gain greater than $500,000 before they would owe any tax to the federal or state government when they sell their primary residence. Remember, it’s the gain, not the sales price. If someone purchased a house for $300,000 and sells it for $700,000, there is a $400,000 gain in the property. If they file a joint tax return, the full $400,000 is sheltered from taxation by the primary residence exclusion.

Once the gain exceeds $250,000 for a single filer or $500,000 for a joint filer, then the owner of the house would have to pay tax to the state the house is located in, regardless of their state of domicile at the time of the sale.

Selling Stocks or Investments

If someone has a large unrealized gain in their taxable brokerage account and they are considering moving to a state that has no income tax, they will ask, “If I wait to sell my stock until after I have officially changed my state of domicile, will I avoid having to pay state income tax on the realized gain?” The answer here is “Yes”. This is one of the advantages that investment holdings like stocks, bonds, ETFs, and mutual funds have over real estate investments.

For example, Jen lives in New York and purchased shares of Nvidia a few years back for $10,000, which are now worth $200,000. If she sold the shares now, she would have to pay a flat 15% long-term capital gain at the federal level, and approximately 6% ($11,400) to New York State. However, if Jen plans to move to Florida and waits to sell the Nvidia stock until after she has officially domiciled in Florida, she would still have to pay the 15% long-term capital gains tax to the Feds, but she would completely avoid having to pay tax on the gain to New York State, saving her $11,400 in taxes.

The Timing of The Sale of Stock is Key

When someone changes their state of domicile mid-year, which is most, a line in the sand is drawn from a tax standpoint. For example, if Jen moved from New York to Florida on May 15th, all investment activity between January 1st – May 14th would be taxed in New York, and all investment activity May 15th – December 31st would be taxed (essentially not taxed) in Florida. It’s for this reason that individuals who have taxable investment accounts and are planning to move to a more tax-favorable state within the next few years may be influenced as to when they decide to sell certain investments at a gain within their taxable investment portfolio.

IRA Distribution Taxation

Traditional IRA distributions are taxed at ordinary income tax rates, but the same timing principle applies; any distribution processed prior to the change in domicile would be taxed in their current state, and distributions processed after the change of domicile are taxed or, in some cases, not taxed, in their new state. If Roth conversions in retirement are part of your tax strategy, this is also one of the reasons why individuals will wait until they have become domiciled in the new state before actually processing Roth conversions.

What Are The Requirements To Change Your State of Domicile

The rules for changing your state of domicile are more complex than most people think. It’s not just “I have to be in that state for more than 6 months out of the year.” That may be one of the requirements, but there are many others. So many that we had to write a whole separate article on this topic, which can be found here:

Article: How To Change Your Residency To Another State for Tax Purposes

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

Can moving to a state with no income tax help me avoid paying capital gains tax?

It depends on your income picture and the type of assets that you own. If you live in a state now that has income tax but you pay very little state income tax, moving to a state that has no income tax will have a minimal impact. However, if you specific sources of income, such as investment income or taxable income from Roth conversions, moving from a state that has income tax to a state with no income tax can have a meaningful impact.

Do I still owe state tax on the sale of a rental property after moving?

Yes. If you sell a rental property located in a state that imposes income tax, you must pay tax to that state on the gain, regardless of where you live at the time of sale. You receive a credit on the state tax paid to apply against any state tax due in your current state, but if there is no state income tax in your current state of domicile, the credit goes unused.

How is the sale of a primary residence taxed when moving to another state?

You can exclude up to $250,000 in gains if single or $500,000 if married filing jointly when selling your primary residence, provided you meet ownership and use requirements. Any gain above these thresholds is taxable to the state where the property is located, even if you’ve moved to a no-tax state.

Can I avoid state taxes on stock sales by moving before I sell?

Yes. If you wait to sell appreciated investments such as stocks, ETFs, or mutual funds until after establishing domicile in a no-income-tax state, you can avoid state tax on the capital gains. The timing of your move and the sale determines which state has taxing authority.

How does the timing of domicile change affect investment taxation?

When you change residency mid-year, income earned before the move is taxed by your former state, while income earned after is taxed under the new state’s rules. For example, investment gains realized before moving from New York to Florida would be taxed in New York, but gains realized afterward would not be.

Are IRA withdrawals and Roth conversions affected by state residency changes?

Yes. Distributions from traditional IRAs or Roth conversions made before changing residency are taxed in your former state, while those made afterward follow the tax rules of your new domicile. This timing can be strategically used to reduce state income taxes in retirement.

What are the main requirements to change your state of domicile for tax purposes?

Changing domicile involves more than just spending six months in another state. You must establish clear intent and presence — such as changing your driver’s license, voter registration, mailing address, and location of key assets — to prove your new primary residence for tax purposes.

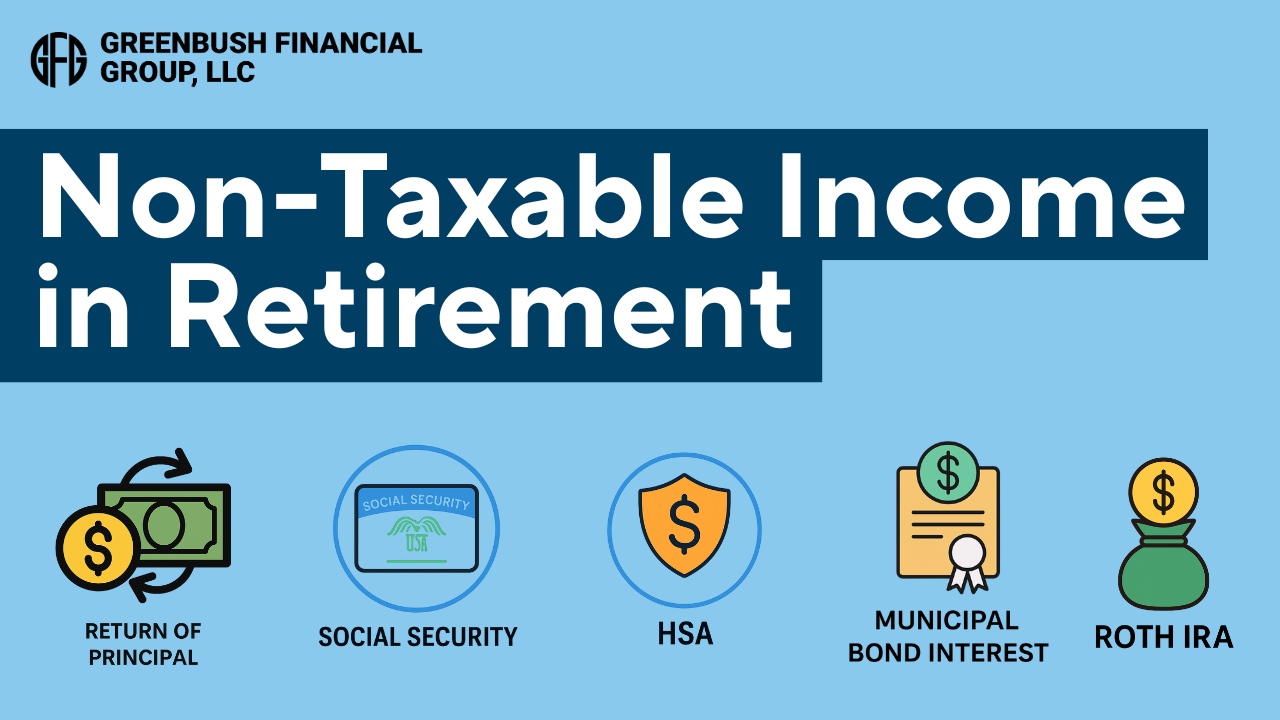

Non-Taxable Income in Retirement: 5 Sources You Should Know About

When it comes to retirement income, not all dollars are created equal. Some income sources are fully taxable, others partially — but a select few can be completely tax-free. And understanding the difference could mean thousands of dollars in savings each year.

When it comes to retirement income, not all dollars are treated equally. Some are fully taxable, others partially taxable, and a select few are entirely tax-free. Understanding the difference is critical to building a retirement income plan that protects your nest egg from unnecessary taxation, especially in a high-inflation, high-cost-of-living environment.

In this article, we break down five sources of non-taxable income in retirement, how they work, and how to strategically use them to lower your tax bill and preserve long-term wealth.

1. Roth IRA Withdrawals

A Roth IRA offers one of the most powerful tax benefits available to retirees — tax-free growth and qualified tax-free withdrawals.

To qualify, withdrawals must occur after age 59½ and at least five years after your first contribution or Roth conversion. If both conditions are met, all distributions (contributions and growth) are 100% tax-free.

Why it matters:

Withdrawals from pre-tax retirement accounts like Traditional IRAs and 401(k)s are taxed as ordinary income, which can push you into a higher tax bracket, increase Medicare premiums, and reduce the portion of your Social Security benefits that are tax-free. With Roth IRAs, none of those problems exist.

Planning strategy:

Many retirees choose to complete Roth conversions during low-income years (such as early retirement) to move pre-tax funds into a Roth IRA while controlling their tax rate. This allows them to create a future pool of tax-free income while reducing Required Minimum Distributions (RMDs) down the line.

2. Health Savings Account (HSA) Distributions for Medical Expenses

HSAs are the only account type that offers triple tax advantages:

Contributions are tax-deductible

Growth is tax-deferred

Withdrawals are tax-free if used for qualified medical expenses

Qualified expenses include Medicare premiums, prescriptions, dental and vision care, long-term care insurance premiums (subject to limits), and more.

Why it matters:

Healthcare is often one of the largest expenses in retirement, and using HSA funds tax-free for these costs allows retirees to preserve their other taxable accounts.

Planning strategy:

For clients who are still working and enrolled in a high-deductible health plan, the strategy may be to contribute the maximum amount to an HSA and pay current medical expenses out-of-pocket. This allows the HSA to grow and be used as a supplemental retirement account for tax-free medical reimbursements later in life.

3. Social Security (Partially Non-Taxable)

Up to 85% of Social Security benefits can be taxable at the federal level, depending on your provisional income (which includes half of your Social Security benefits, taxable income, and tax-exempt interest).

However, if a retiree has very little income other than their social security, it’s possible that they may not pay any tax on their social security benefits.

Why it matters:

Retirees who rely heavily on Roth IRA withdrawals or return of principal from brokerage accounts may be able to keep their provisional income low enough to shield some or all of their Social Security benefits from taxation.

Planning strategy:

By building a tax-efficient distribution plan in retirement, retirees can often reduce the amount of tax paid on their Social Security benefits and improve net income in retirement.

4. Municipal Bond Interest

Interest from municipal bonds is generally exempt from federal income tax. If you reside in the state where the bond was issued, that interest may also be exempt from state and local taxes.

Why it matters:

For retirees in high tax brackets, municipal bonds can provide steady, tax-advantaged income without adding to provisional income or triggering taxes on Social Security.

Planning strategy:

Retirees in high-income tax brackets may hold municipal bonds in taxable brokerage accounts, while keeping higher-yield taxable bonds inside IRAs or 401(k)s where the interest won’t be taxed annually.

5. Return of Principal from Non-Retirement Accounts

Withdrawals from taxable brokerage accounts can be structured to return your cost basis first, which is not subject to tax. Only the gains portion of a sale is subject to capital gains tax — and long-term capital gains may be taxed at 0% if your taxable income is below certain thresholds.

Why it matters:

This allows retirees to tap into their investments in a low-tax or no-tax manner — especially when drawing from principal rather than interest, dividends, or gains.

Planning strategy:

Coordinate asset sales to manage taxable gains, and consider drawing from principal early in retirement to reduce future RMDs or pay the tax liability generated by Roth conversions in lower-income years.

Final Thoughts: Build a Tax-Efficient Retirement Income Plan

Most retirees understand the importance of investment performance, but few give the same attention to tax efficiency, even though taxes can quietly erode thousands of dollars in retirement income each year.

By blending these non-taxable income sources into your withdrawal strategy, you can:

Reduce your tax liability

Lower Medicare surcharges

Improve portfolio longevity

Increase the amount of inheritance passed to the next generation

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What types of retirement income are tax-free?

Common sources of tax-free retirement income include qualified Roth IRA withdrawals, Health Savings Account (HSA) distributions for medical expenses, a portion of Social Security benefits, municipal bond interest, and the return of principal from non-retirement investments. These sources can help retirees reduce overall taxable income and extend portfolio longevity.

Why are Roth IRA withdrawals tax-free in retirement?

Roth IRA withdrawals are tax-free if you’re over age 59½ and the account has been open for at least five years. Because Roth withdrawals don’t count toward taxable income, they won’t increase your tax bracket, affect Medicare premiums, or reduce the tax-free portion of your Social Security benefits.

How can a Health Savings Account (HSA) provide tax-free income in retirement?

HSAs offer triple tax advantages: contributions are tax-deductible, growth is tax-deferred, and withdrawals are tax-free for qualified medical expenses. Retirees can use HSA funds to pay for Medicare premiums, prescriptions, and other healthcare costs without generating taxable income.

Are Social Security benefits always taxable?

No. Depending on your provisional income, up to 85% of Social Security benefits may be taxable, but some retirees owe no tax on their benefits. Keeping taxable income low through Roth withdrawals or return of principal from brokerage accounts can help reduce or eliminate Social Security taxation.

How are municipal bond earnings taxed?

Interest earned from municipal bonds is typically exempt from federal income tax and, if the bonds are issued by your home state, may also be exempt from state and local taxes. This makes municipal bonds a valuable source of tax-advantaged income for retirees in higher tax brackets.

What does “return of principal” mean for taxable accounts?

When you sell investments in a taxable brokerage account, the portion representing your original cost basis is considered a return of principal and isn’t taxed. Only the gains portion is subject to capital gains tax, which may be as low as 0% for retirees in lower income brackets.

How can retirees use non-taxable income to improve their financial plan?

Strategically blending tax-free and taxable income sources can lower your overall tax burden, reduce Medicare surcharges, and improve long-term portfolio sustainability. This approach helps preserve wealth and increase the amount that can ultimately be passed to heirs.

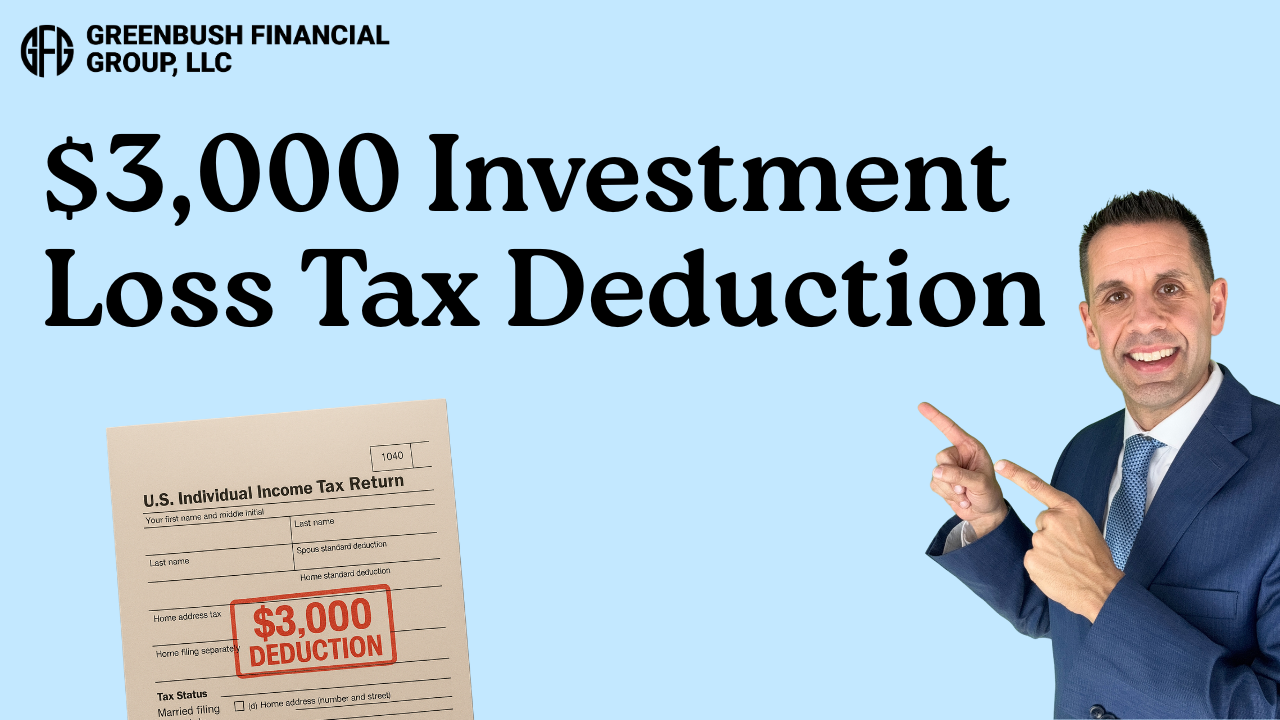

Understanding the $3,000 Investment Loss Annual Tax Deduction

Each year, the IRS allows a tax deduction for investment losses that can be used to offset earned income. However, it’s a use-it-or-lose-it tax deduction, meaning if you fail to realize losses in your investment accounts by December 31st, you could forfeit a valuable tax deduction.

Each year, the IRS allows a tax deduction for investment losses that can be used to offset earned income. However, it’s a use-it-or-lose-it tax deduction, meaning if you fail to realize losses in your investment accounts by December 31st, you could forfeit a valuable tax deduction. In this article, we are going to cover:

Investment loss deduction limit

Single filer versus Joint filer

Short-term vs Long-term losses offset

Carryforward loss rules

Wash sale rules

$3,000 Investment Loss Deduction

Each year, the IRS allows both single filers and joint filers to deduct $3,000 worth of investment losses against their ordinary income. Usually, this is not allowed because investment gains and losses are considered “passive income”, while W-2 income or self-employment income is considered “earned income.” In most cases, gains and losses on the passive side of the fence do not normally offset income on the earned side of the fence. This $3,000 annual deduction for investment losses is the exception to the rule.

Realized Losses In Investment Accounts

To capture the tax deduction for the investment losses, the losses have to be “realized losses,” meaning you actually sold the investment at a loss, which turned the loss from an “unrealized” loss into a “realized loss” by December 31st. In addition, the realized loss has to take place in a taxable investment account like an individual account, a joint account, or a revocable trust account. Accounts such as an IRA, 401(k), or SEP IRA are tax-deferred accounts, so they do not generate realized gains or losses.

Long-term versus Short-term Losses

The realized losses can be either short-term or long-term, or a combination of both, leading up to the $3,000 annual loss limit. But if you have the option, it’s often more beneficial from a pure tax standpoint to realize a long-term loss, and I’ll explain why.

In the investment world, short-term gains are taxed as ordinary income and long-term gains are taxed at preferential long-term capital gains rates that range from 0% - 23.8% (including the Medicare surcharge). But when you realize investment losses, long-term losses cannot offset short-term gains. Only short-term losses can offset short-term gains.

By realizing $3,000 in long-term capital losses, you can use that amount to offset $3,000 of earned income—taxed at higher ordinary income rates—rather than just offsetting long-term capital gains, which are already taxed at lower preferential rates. Potentially saving you more tax dollars.

Loss Carryforward Rules

But what if your realized losses are more than $3,000 for the year? No worries, both short-term and long-term losses are eligible for “carryforward” which means you can keep carrying forward those losses into future tax years until you have additional realized investment gains to eat up the loss, or you can continue to take the $3,000 per year investment loss deduction until your carryforward loss has been used up.

Single Filer versus Joint Filer

Whether you are a single filer or a joint filer, the total annual investment losses deduction is $3,000. It does not double because you file married filing jointly - even though technically each spouse could have their own individual brokerage account with $3,000 in realized losses. However, if you file “married filing separately,” the annual deduction is limited to $1,500.

Wash Sale Rule

When you intentionally sell investments for purposes of capturing this $3,000 annual loss deduction, you have to be careful of the 30-Day Wash Sale Rule, which states that if you sell an investment at a loss and then buy that same investment or a “substantially identical security” back within 30 days of the sale, it prevents the investor from taking deduction for the realized loss.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What is the IRS investment loss deduction limit?

The IRS allows taxpayers to deduct up to $3,000 of realized investment losses ($1,500 if married filing separately) against ordinary income each year. This deduction applies only to losses in taxable investment accounts and must be realized by December 31st to count for that tax year.

What counts as a “realized” investment loss?

A loss is realized when you sell an investment for less than its purchase price. Unrealized losses—investments that have declined in value but haven’t been sold—do not qualify for the deduction. Losses must occur in taxable accounts, not tax-deferred ones like IRAs or 401(k)s.

How do short-term and long-term losses differ for tax purposes?

Short-term losses offset short-term gains, while long-term losses offset long-term gains. However, up to $3,000 of net long-term losses can also offset ordinary income, which is taxed at higher rates. This can provide a greater tax benefit than simply offsetting lower-taxed long-term gains.

What happens if I have more than $3,000 in investment losses?

Losses that exceed the $3,000 annual limit can be carried forward indefinitely to future tax years. These carryforward losses can offset future investment gains or continue to reduce ordinary income by up to $3,000 each year until they are fully used.

Does the $3,000 investment loss deduction double for married couples?

No. The deduction limit is $3,000 per tax return, whether you file as single or married filing jointly. For those filing separately, the limit is reduced to $1,500 per person.

What is the wash sale rule and how does it affect loss deductions?

The IRS wash sale rule disallows a deduction if you sell an investment at a loss and repurchase the same or a substantially identical security within 30 days before or after the sale. To preserve the deduction, you must wait at least 31 days before buying the same investment again.

Why is it important to realize losses before year-end?

The investment loss deduction follows a “use it or lose it” rule — losses must be realized before December 31st to count for that year’s tax filing. Missing the deadline means forfeiting the potential $3,000 deduction for that tax year.

401(k) Catch-Up Contribution FAQs: Your Top Questions Answered (2025 Rules)

Got questions about 401(k) catch-up contributions? You’re not alone. With updated 2025 limits and new Roth rules on the horizon, this article answers the most common questions about who qualifies, how much you can contribute, and what strategic moves to consider in your 50s and early 60s.

As retirement gets closer, many individuals start to wonder how they can supercharge their savings and make up for lost time. For those age 50 and older, catch-up contributions offer a powerful opportunity to contribute more to retirement accounts beyond the standard annual limits. Below, I’ve addressed some of the most common questions I get from clients about catch-up contributions, especially with the updated 2025 rules in play.

Can I make catch-up contributions if I’m working part-time in retirement?

Yes, as long as you have earned income from a job, and you have met the plan’s eligibility requirements. So, even if you’ve scaled back your hours or semi-retired, you may still be eligible to make additional contributions.

For example, if you're age 65 and working part-time and eligible for your company’s 401(k) plan, you can contribute up to $23,500, plus an extra $7,500 in catch-up contributions for a total of $31,000 in 2025, assuming you have at least $31,000 in W2 compensation.

If you have less than $31,000 in W2 comp, you will be capped by the lesser of the annual contribution limit or 100% of your W2 compensation.

Are Roth catch-up contributions allowed?

Yes. If your employer plan offers a Roth option, you can choose to make your catch-up contributions as Roth dollars. This means you contribute after-tax money now and take qualified distributions tax-free in retirement.

This option is popular for individuals who are in the same tax bracket now as they plan to be in retirement. The Roth source also avoids required minimum distributions (RMDs) starting at age 73 or 75.

How do catch-up contributions impact required minimum distributions (RMDs)?

Catch-up contributions themselves don’t change the timing or calculation of RMDs. However, where you put the catch-up dollars can affect your future RMDs. If you contribute catch-up dollars to a Roth 401(k) and then roll over the balance to a Roth IRA prior to the RMD start age, RMDs are not required.

Adding more to the pre-tax employee deferral source within the plan may increase your future RMD requirement since pre-tax retirement accounts are subject to the annual RMD requirement once you reach age 73 (for those born 1951–1959) or 75 (for those born 1960 or later).

Should I prioritize catch-up contributions or pay down my mortgage?

This depends on your interest rate, your retirement timeline, tax bracket, and your overall financial goals. Generally, if your mortgage interest rate is below 4% and you’re behind on retirement savings, catch-up contributions may be a better use of your idle cash, especially if your investments are growing tax-deferred (pre-tax) or tax-free (roth).

However, if you’re already on track for retirement and the psychological benefit of being debt-free is important to you, putting extra cash toward your mortgage can make sense. It’s all about balancing the right financial decision with your personal preferences.

What happens if I forget to update my payroll deferrals after turning 50?

Unfortunately, you won’t automatically get the benefit since your employer’s payroll system won’t adjust your contributions just because you had a birthday. You need to take action and manually increase your deferrals to take advantage of the higher limits.

For example, if you turn 50 this year and forget to bump your 401(k) deferrals, you may miss out on contributing an additional $7,500. Worse yet, once the calendar year closes, you can't go back and make up for it.

Are there additional tax benefits associated with making catch-up contributions?

It’s common that the years leading up to retirement are often the highest income years for an individual. The additional pre-tax contributions associated with the catch-up contribution allow employees to take more of their income off the table during the peak income years and shift it into the retirement years, when ideally they are in a lower tax bracket.

What is the new age 60 – 63 catch-up contribution?

Starting in 2025, there is a new enhanced catch-up contribution available to employees covered by 401(k) and 403(b) plans who are aged 60 to 63. Instead of being limited to just the regular $7,500 catch-up contribution, in 2025, employees age 60 – 63 will be allowed to make a catch-up contribution equal to $11,250.

What is the Mandatory Roth catch-up for high income earners?

Starting in 2026, and for the following years, if an employee makes more than $145,000 in W2 compensation (indexed for inflation) with the same employer in the previous year, that employee will no longer be allowed to make pre-tax catch-up contributions. If they make a catch-up contribution, it will be required to be a Roth catch-up contribution.

Final Thoughts…

Whether you’re still decades from retirement or just a few years away, catch-up contributions are a crucial part of retirement planning for those age 50 and older. With the 2025 limits now in place and Roth rules continuing to evolve, understanding how these contributions fit into your broader plan can help you save smarter — and avoid costly mistakes.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What are catch-up contributions and who qualifies for them?

Catch-up contributions allow individuals age 50 and older to contribute additional funds to retirement accounts beyond the standard annual limits. For 2025, employees can contribute up to $23,500 to a 401(k) plus an extra $7,500 in catch-up contributions, for a total of $31,000 — provided they have sufficient earned income.

Can part-time workers make catch-up contributions?

Yes. As long as you have earned income and meet your employer plan’s eligibility requirements, you can make catch-up contributions even if you’re working part-time. The total contribution amount cannot exceed 100% of your W-2 compensation.

Are Roth catch-up contributions available?

If your employer plan offers a Roth option, you can make your catch-up contributions as Roth dollars. Roth contributions are made after tax, grow tax-free, and qualified withdrawals are also tax-free, offering flexibility for future tax planning.

How do catch-up contributions affect required minimum distributions (RMDs)?

Catch-up contributions do not change when RMDs begin, but the type of account matters. Pre-tax catch-up dollars increase your future RMDs, while Roth 401(k) contributions can be rolled into a Roth IRA before RMD age to avoid mandatory withdrawals altogether.

Should I prioritize catch-up contributions or pay down my mortgage?

It depends on your financial situation. If your mortgage rate is low (under 4%) and you’re behind on retirement savings, maximizing catch-up contributions may be beneficial. However, paying down your mortgage may make sense if you’re already on track for retirement and value being debt-free or if you have a higher interest rate on your mortgage.

What happens if I forget to increase my deferrals after turning 50?

Your employer’s payroll system won’t automatically adjust contributions, so you must update them manually. Missing the adjustment means forfeiting that year’s extra contribution opportunity — once the year ends, you can’t retroactively make up the difference.

What is the new enhanced age 60–63 catch-up contribution for 2025?

Starting in 2025, employees aged 60 to 63 can make a larger catch-up contribution of up to $11,250 to 401(k) and 403(b) plans, providing an additional savings boost in the final years before retirement.

What is the new rule for high-income earners and Roth catch-ups?

Beginning in 2026, employees earning more than $145,000 (indexed for inflation) in W-2 income with the same employer will be required to make catch-up contributions as Roth contributions — pre-tax catch-ups will no longer be allowed for this group.

401(k) Catch-Up Contributions Explained: Maximize Your Retirement Savings in 2025

Turning 50? It’s time to boost your retirement savings.

This article breaks down the updated 2025 401(k) catch-up contribution limits, new rules for ages 60–63, and whether pre-tax or Roth contributions make the most sense for your situation.

For individuals aged 50 or older, catch-up contributions allow for additional retirement savings during what are often their highest earning years. With updated limits and new provisions taking effect in 2025, this strategy can be especially valuable for those looking to strengthen their financial position ahead of retirement and maximize tax efficiency in what are typically their highest income years leading up to retirement.

Below, I break down the 2025 catch-up contribution limits, rules, and strategic considerations to help you make informed decisions.

What Are Catch-Up Contributions?

Catch-up contributions allow individuals aged 50 or older to contribute above the standard annual limits to retirement accounts. You’re eligible to make catch-up contributions starting in the calendar year you turn 50.

2025 Contribution Limits

Here are the updated 2025 401(k) contribution limits for each plan type:

401(k), 403(b), 457(b):

Standard limit: $23,500

Age 50 – 59 & Age 64+ catch-up: $7,500

Age 60 – 63 catch-up: $11,250

New 401(k) Age 60–63 Catch-Up Limits

Beginning in 2025, a new tier of higher catch-up limits will apply to individuals between ages 60 and 63. Under the SECURE 2.0 Act, these individuals can contribute an additional amount equal to 50% of the regular catch-up contribution for that plan year. For 2025, this equates to an extra $3,750, bringing the total possible contribution to $34,750 for 401(k), 403(b), and 457(b) plans. This enhanced catch-up contribution is optional for employers, so it's important to confirm with your plan sponsor whether this provision is available in your plan.

To learn more, read our article: New Age 60 – 63 401(k) Enhanced Catch-up Contribution Starting in 2025

Pre-Tax vs. Roth Catch-Up Contributions

Employer-sponsored retirement plans often allow participants to choose whether their catch-up contributions are made on a pre-tax or Roth (after-tax) basis. The best approach depends on income levels, expected tax rates in retirement, and broader financial planning goals.

Pre-tax contributions reduce your taxable income today but are taxed when withdrawn in retirement.

Roth contributions provide no current tax deduction but grow and distribute tax-free in retirement.

When Pre-Tax May Make Sense:

You're in a high tax bracket today (e.g., 24%+)

You expect to be a lower tax bracket during the retirement years

Example:

Tom is age 60, married, and earns $400,000 annually, placing him in the 32% federal tax bracket. In the next 5 years, Tom expects to retire and be in a lower federal tax bracket. By making pre-tax catch-up contributions now, it will allow him to reduce his current taxable income, while potentially taking distributions in a lower tax bracket later.

When Roth May Make Sense:

You expect your current tax rate to be roughly the same in retirement

You already have substantial pre-tax retirement account balances

You expect tax rates to rising in the future

Example:

Susan is age 52, single filer, earns $125,000 per year, and is in the 22% tax bracket. She expects her income to remain steady over time. By choosing Roth catch-up contributions, she pays tax now at a relatively low rate and avoids taxation on future withdrawals.

Mandatory Roth Catch-Up Contributions for High Earners (Effective 2026)

Starting in 2026, individuals earning $145,000 or more (adjusted for inflation) in wages from the same employer in the previous year will be required to make catch-up contributions to their workplace plan on a Roth basis. This rule applies only to employer-sponsored plans (like 401(k)s) and does not impact Simple IRA plans. For 2025, these Roth rules have been delayed, giving high-income earners time to prepare.

To learn about the rules and exceptions for high earners, read our article: Mandatory 401(k) Roth Catch-up Details Confirmed by IRS January 2025

The Big Picture: Why This Strategy Matters Near Retirement

For individuals within five to ten years of retirement, catch-up contributions provide an opportunity to meaningfully increase retirement savings without relying on higher investment returns or making dramatic lifestyle changes. The added contributions also support strategic tax planning by allowing savers to choose between pre-tax and Roth treatment based on their broader income picture.

Catch-up contributions can help:

Maximize tax-advantaged savings when your income is typically at its highest

Take advantage of compound growth on a larger balance

Strategically shift assets into Roth accounts for future tax-free income

Consider the numbers:

A 60-year-old contributing the full $34,750 annual catch-up amount for three consecutive years could accumulate over $111,000 in additional retirement savings, assuming a 7% annual return. If contributed to a Roth 401(k), those funds would grow and be distributed tax-free, offering valuable flexibility in retirement.

Even if retirement is only a few years away, catch-up contributions can play a significant role in improving retirement readiness and reducing future tax burdens.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What are catch-up contributions and who qualifies for them?

Catch-up contributions allow individuals aged 50 or older to contribute more to retirement accounts than the standard annual limit. Eligibility begins in the calendar year you turn 50, regardless of your income level or how close you are to retirement.

What are the 2025 catch-up contribution limits?

In 2025, employees can contribute up to $23,500 to a 401(k), 403(b), or 457(b) plan. Those aged 50–59 and 64 or older can contribute an additional $7,500, while individuals aged 60–63 can make an enhanced catch-up contribution of $11,250, for a total of $34,750 if allowed by their employer’s plan.

How does the new age 60–63 catch-up rule work?

Starting in 2025, individuals between ages 60 and 63 can make a higher catch-up contribution equal to 150% of the standard catch-up limit. This provision under the SECURE 2.0 Act lets older workers maximize savings during their final working years, but availability depends on whether an employer adopts the rule.

Should I make my catch-up contributions pre-tax or Roth?

The best option depends on your tax situation. Pre-tax contributions reduce taxable income now and are ideal if you expect to be in a lower tax bracket in retirement. Roth contributions are made after-tax but grow tax-free and are advantageous if you expect future tax rates to rise or your income to remain steady.

What is the mandatory Roth catch-up rule for high-income earners?

Beginning in 2026, employees earning $145,000 or more (adjusted for inflation) from the same employer in the previous year must make catch-up contributions on a Roth basis. This means contributions will be made after tax, and future withdrawals will be tax-free.

Why are catch-up contributions especially important near retirement?

Catch-up contributions help individuals nearing retirement boost savings during peak earning years without depending solely on market growth. They also provide tax planning flexibility by letting savers choose between pre-tax and Roth options based on their expected future income and tax rates.

How Transfer on Death (TOD) Accounts Help You Avoid Probate

Confused about transfer-on-death (TOD) accounts? This article answers the most common questions about Transfer on Death designations, how they work, and how they can help you avoid probate.

As an investment firm, we typically encourage clients to add TOD beneficiaries to their individual brokerage accounts to avoid the probate process, should the owner of the account unexpectedly pass away. TOD stands for “Transfer on Death”. When someone passes away, their assets pass to their beneficiaries in one of three ways:

Probate

Contract

Trust

Passing Asset by Contract

When you set up an IRA, 401(K), annuity, or life insurance policy, at some point during the account opening process, the custodian or life insurance company will ask you to list beneficiaries on your account. This is a standard procedure for these types of accounts because when the account owner passes away, they look at the beneficiary form completed by the account owner, and the assets pass “by contract” to the beneficiaries listed on the account. Since these accounts pass by contract, they automatically avoid the headaches of the probate process.

Probate

Non-retirement accounts like brokerage accounts, savings accounts, and checking accounts are often set up in an individual's name without beneficiaries listed on the account. If someone that passes away has one of these accounts, the decedent’s last will and testament determines who will receive the balance in those accounts - but those accounts are required to go through a legal process called “probate”. The probate process is required to transfer the decedent’s assets into their “estate”, and then ultimately distribute the assets of the estate to the estate beneficiaries.

Since the probate process involves the public court system, it can often take months before the assets of the estate are distributed to the beneficiaries of the estate. Depending on the size and complexity of the estate, there could also be expenses associated with the probate process, including but not limited to court filing fees, attorney fees, accountant fees, executor fees, appraiser fees, or valuation experts.

For this reason, many estate plans aim to avoid probate whenever possible.

Transfer On Death Designation

A very easy solution to avoid the probate process for brokerage accounts, checking accounts, and savings accounts, is to add a TOD designation to the account. The process of turning an individual account into a Transfer on Death account is also very easy because it usually only involves completing a Transfer-on-Death form, which lists the name and percentages of the beneficiaries assigned to the account. Once an individual account has been changed into a TOD account, if the account owner were to pass away, that account no longer goes through the probate process; it now passes to the beneficiaries by contract, similar to an IRA.

Frequently Asked Questions About TOD Accounts

After we explain the TOD strategy to clients, there are often several commonly asked questions that follow, so I’ll list them in a question-and-answer format:

Q: Can you change the beneficiaries listed on a TOD account at any time?

A: Yes, the beneficiaries assigned to a TOD account can be changed at any time by completing an updated TOD designation form

Q: If I list TOD beneficiaries on all of my non-retirement accounts, do I still need a will?

A: We strongly recommend that everyone execute a will for assets that are difficult to list TOD beneficiaries, such as a car, jewelry, household items, and for any other assets that don’t pass by contract or by trust.

Q: Can I list TOD beneficiaries on my house?

A: It depends on what state you live in. Currently, 31 states allow TOD deeds for real estate. New York became the newest state added to the list in 2024.

Q: Can my TOD beneficiaries be the same as my will?

A: Yes, you can make the TOD beneficiaries the same as your will. However, since TOD accounts pass by contract and not by your will, you can make beneficiary designations other than what is listed in your will.

Q: Can I list different beneficiaries on each TOD account (brokerage, checking, savings)?

A: Yes

Q: Can I list a trust as the beneficiary of my TOD account?

A: Yes

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What does TOD mean and how does it work?

TOD stands for “Transfer on Death.” It allows you to name beneficiaries on certain financial accounts—such as brokerage, checking, or savings accounts—so that the assets transfer directly to those beneficiaries when you pass away, bypassing the probate process entirely.

How is a TOD account different from probate or a trust?

Assets that pass through probate are distributed under a will and may take months to settle, while assets in a trust or TOD account pass directly to beneficiaries without court involvement. A TOD designation provides a simple, low-cost way to avoid probate for individual accounts.

Can I change the beneficiaries on my TOD account?

Yes. You can update or change your TOD beneficiaries at any time by completing a new Transfer-on-Death designation form with your financial institution. The most recent form on file will determine who receives the assets upon your passing.

Do I still need a will if I have TOD accounts?

Yes. A will is still necessary for assets that cannot have TOD beneficiaries, such as vehicles, personal items, or real estate in states that don’t allow TOD deeds. A will ensures these remaining assets are distributed according to your wishes.

Can I add TOD beneficiaries to my house or real estate?

In many states, yes. As of 2024, 31 states—including New York—allow Transfer-on-Death deeds for real estate. Rules vary by state, so it’s important to confirm eligibility and filing requirements where you live.

Can I name different beneficiaries on each TOD account?

Yes. You can assign unique beneficiaries and percentage allocations for each TOD account, giving you flexibility in how your assets are distributed.

Can I name a trust as the beneficiary of my TOD account?

Yes. You can designate a trust as your TOD beneficiary, which can be beneficial if your estate plan includes specific instructions for how and when assets should be distributed to heirs.

How to Avoid the New York State Estate Tax Cliff

When someone passes away in New York, in 2025, there is a $7.16 million estate tax exclusion amount, which is significantly lower than the $13.9M exemption amount available at the federal level. However, in addition to the lower estate tax exemption amount, there are also two estate tax traps specific to New York that residents need to be aware of when completing their estate plan. Those two tax traps are:

1) The $7.5 million Cliff Rule

2) No Portability between spouses

With proper estate planning, these tax traps can potentially be avoided, allowing residents of New York to side-step a significant state tax liability when passing assets onto their heirs.

When someone passes away in New York in 2025, there is a $7.16 million estate tax exclusion amount, which is significantly lower than the $13.9M exemption amount available at the federal level. However, in addition to the lower estate tax exemption amount, there are also two estate tax traps specific to New York that residents need to be aware of when completing their estate plan. Those two tax traps are:

The $7.5 million Cliff Rule

No Portability between spouses

With proper estate planning, these tax traps can potentially be avoided, allowing residents of New York to side-step a significant state tax liability when passing assets onto their heirs.

New York Estate Tax Cliff Rule

When it comes to estate planning, it’s important to understand that estate tax rules at the federal and state levels can vary. Some states adhere to the federal rules, but New York is not one of those states. New York has a very punitive “cliff rule” where once an estate reaches a specific dollar amount, the New York estate tax exemption is eliminated, and the ENTIRE value of the estate is subject to New York state tax.

As mentioned above, the New York estate tax exemption for 2025 is $7,160,000. So, for anyone who lives in New York and passes away with an estate that is valued below that amount, they do not have to pay estate tax at the state or federal level.

For individuals that pass away with an estate valued between $7,160,000 and $7,518,000, they pay estate tax to New York only on the amount that exceeds the $7,160,000 threshold.

But the “cliff” happens at $7,518,000. Once an estate in New York exceeds $7,518,000, the ENTIRE estate is subject to New York Estate Tax, which ranges from 3.06% to 16% depending on the size of the estate.

Non-Portability Between Spouses in New York

Married couples that live in New York must be aware of how the portability rules vary between the federal and state levels. “Portability” is something that happens at the passing of the first spouse, and it refers to how much of the unused estate tax exemption can be transferred or “ported” over to the surviving spouse. The $13.9M federal estate tax exemption is “per person” and “full portable”. Why is this important? It’s common for married couples to own most assets “jointly with rights of survivorship”, so when the first spouse passes away, the surviving spouse assumes full ownership of the asset. However, since the spouse who passed away did not have any assets solely in their name, there is nothing to include in their estate, so the $13.9M federal estate tax exemption at the passing of the first spouse goes unused.

At the federal level that’s not an issue because the federal estate tax exemption for a married couple is portable, which means if the first spouse that passes away does not use their full estate tax exemption, any unused exemption amount is transferred to the surviving spouse. Assuming that the spouse who passes away first does not use any of their estate tax exemption, when the second spouse passes, they would have a $27.8 million federal estate tax exemption ($13.9M x 2).

However, New York does not allow portability, so any unused estate tax exemption at the passing of the first spouse is completely lost. The fact that New York does not allow portability requires more proactive estate tax planning prior to the passing of the first spouse.

Here is a quick example showing how this works: Larry & Kathy are married and have an estate valued at $10M in which most of their assets are titled jointly with rights of survivorship. Since everything is titled jointly, if Larry were to pass away in 2025, the $10M in assets would transfer over to Kathy with no estate taxes due at either the Federal or State level. The problem arises when Kathy passes away 2 years later. Assuming Kathy passes away with the same $10M in her name, there is still no federal estate taxes due because she more than covered by the $27.8M exemption at the federal level, however, because New York’s estate tax exemption is not portable, and her assets are well over the $7.5M cliff, the full $10M would be taxed by the New York level, resulting in close to a $1M tax liability. A tax liability that could have been completely avoided with proper estate planning.

If instead of Larry and Kathy holding all of their assets jointly, they had segregated their assets to $5M owned by Larry and $5M owned by Kathy, when Larry passed away, he would have been able to use his $7.1M New York State estate tax exemption to protect the full $5M. Then, when Kathy passed with her $5M two years later, she would have been able to use her full $7.1M New York State tax exemption, resulting in $0 in taxes paid to New York State — avoiding nearly $1M in unnecessary tax liability.

Setting Up Separate Trusts

A common solution that our clients will use to address both the $7.5M cliff and the non-portability issue in New York is that each spouse will set up their own revocable trust, and then split the non-retirement account assets in a way to maximize the $7.1M New York State exemption amount at the passing of the first spouse.

I will sometimes hear married couples say “Well, we don’t have to worry about this because our total estate is only $6 million.” That would be true today, but if that married couple is only 70 years old, and they are both in good health, what if their assets double in size before the first spouse passes? Now they have a problem.

Special Legal Disclosure: This article is for educational purposes only, and it does not contain any legal advice. For legal advice, please contact an attorney.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQ):

What is the New York estate tax exemption for 2025?

In 2025, New York’s estate tax exclusion amount is $7.16 million per person, which is significantly lower than the federal estate tax exemption of $13.9 million. Estates valued below $7.16 million are not subject to New York or federal estate tax, but larger estates may face substantial state tax liability.

What is the New York “estate tax cliff rule”?

The “cliff rule” means that if an estate exceeds 105% of the exemption amount—$7.518 million in 2025—the entire estate becomes subject to New York estate tax, not just the amount above the threshold. Once an estate crosses the cliff, tax rates ranging from 3.06% to 16% can apply to the entire estate value.

How does New York’s estate tax differ from federal estate tax rules?

Unlike federal law, which allows full portability between spouses and a much higher exemption amount, New York has no portability and a lower threshold. This means any unused exemption at the first spouse’s death is lost unless proactive estate planning is done.

What does “non-portability” between spouses mean in New York?

Non-portability means a surviving spouse cannot use the unused estate tax exemption of their deceased spouse. Without planning, the first spouse’s exemption is forfeited, potentially exposing the surviving spouse’s estate to higher New York taxes later.

How can married couples avoid the New York estate tax cliff and non-portability issue?

Couples can establish separate revocable trusts and divide ownership of assets so that each spouse has enough in their name to fully use their individual New York estate tax exemption. This strategy allows both exemptions to be utilized and avoids unnecessary state taxes at the second spouse’s death.

Why does asset titling matter for estate tax planning in New York?

Jointly held assets automatically transfer to the surviving spouse and bypass the first spouse’s estate, preventing use of that spouse’s exemption. Properly titling assets between spouses or placing them in individual trusts ensures both exemptions can be applied.

When should New York residents start estate tax planning?

It’s wise to plan early—especially for couples whose combined assets approach or exceed $5–6 million. Asset growth, real estate appreciation, and investment performance can easily push estates over the $7.5 million threshold in the future, triggering significant tax liability without planning.