The Hidden Tax Problem in the FIRE Movement (and How to Fix It)

Many FIRE investors overuse tax-deferred accounts without realizing the long-term consequences. Learn how to avoid this common tax trap and build a more flexible early retirement strategy.

The Financial Independence, Retire Early (FIRE) movement has inspired countless professionals to save aggressively, invest efficiently, and exit the workforce decades ahead of schedule. But there’s one tax mistake many FIRE followers don’t recognize until it’s too late: overloading their savings in tax-deferred accounts.

By focusing too heavily on 401(k)s and traditional IRAs, early retirees often create a tax trap that limits flexibility before age 59½ and exposes them to higher tax bills later in life. Here’s what that mistake looks like—and how strategic balance can prevent it.

How the FIRE Tax Trap Happens

The FIRE community is built on discipline: save 50–70% of income, invest consistently, and let compounding do the rest. The problem is where those savings go. Many early retirees direct most of their contributions into pre-tax accounts to minimize taxes today—but that strategy can backfire once they stop working.

Here’s why:

Withdrawals from traditional 401(k)s and IRAs are fully taxable as ordinary income.

You generally can’t access these funds before age 59½ without penalties (unless you use special exceptions).

After reaching age 73, you must start taking required minimum distributions (RMDs), which can trigger higher brackets and Medicare surcharges later.

As a result, someone retiring at 45 may find most of their wealth locked inside accounts they can’t touch for 15 years—unless they want to pay a 10% early withdrawal penalty.

At Greenbush Financial Group, we have seen FIRE followers realize this only after leaving the workforce—when their living expenses suddenly need to come from taxable or penalty-free sources they don’t have.

The Hidden Cost of Being “Too Tax-Deferred”

In the early accumulation years, it feels great to lower your tax bill with pre-tax contributions. But down the road, the strategy flips. You may have built a seven-figure retirement account, yet each withdrawal comes out as taxable income.

Example:

Imagine a 45-year-old who retires with $1.5 million, all in a traditional 401(k). They need $60,000 per year to live on. Every dollar they withdraw is taxed as ordinary income. Even at a modest 22% bracket, that’s over $13,000 in annual federal taxes—without counting state taxes or future rate increases.

The bigger the pre-tax balance, the larger the future tax burden becomes. What feels like “saving on taxes” during the accumulation phase often becomes deferring a much larger tax bill into your 50s, 60s, and 70s.

What You Should Do Instead

The key is diversification—not just by asset class, but by tax treatment.

Here’s how FIRE investors can fix or prevent the mistake:

Build a Roth bucket early.

Contribute to Roth IRAs or make Roth 401(k) contributions if your income allows. Qualified Roth withdrawals are tax-free in retirement.Create a taxable bridge account.

Invest in a regular brokerage account for flexibility. Long-term capital gains and qualified dividends are taxed at lower rates—and you can access this money anytime.Plan Roth conversions strategically.

After leaving work but before Social Security or RMDs begin, your income may temporarily drop. That’s an ideal time to convert pre-tax assets to Roth at lower brackets.Use the 72(t) rule cautiously.

The IRS allows early withdrawals from IRAs using Substantially Equal Periodic Payments (SEPPs), but they’re inflexible and complex. We usually recommend using this only as a last resort.Think long-term tax balance.

The goal is to retire with assets spread across three types of accounts—pre-tax, Roth, and taxable—so you can manage your income (and taxes) in any given year.

Our analysis at Greenbush Financial Group shows that households with this “three-bucket” approach could save hundreds of thousands in lifetime taxes compared to those with all assets tied up in pre-tax accounts.

What to Watch Out For

Even within the FIRE community, not all withdrawal strategies are equal. Watch for these pitfalls:

Underestimating future tax brackets – Low brackets today don’t guarantee low brackets later. Once RMDs and Social Security start, taxable income can spike.

Neglecting ACA subsidies – For those buying health insurance through the Affordable Care Act, high pre-tax withdrawals can disqualify you from premium tax credits.

Ignoring Roth conversion windows – The best time to convert is usually the first few years after leaving work, before other income streams begin.

The Bottom Line

Reaching financial independence takes planning, discipline, and sacrifice—but staying financially independent requires thoughtful tax strategy. The biggest mistake FIRE followers make is deferring too much for too long, only to face tax inflexibility later.

By intentionally building a mix of pre-tax, Roth, and taxable assets, you can control when and how you pay taxes, keeping more of your hard-earned savings over a lifetime of early retirement.

If you’re pursuing financial independence or considering an early retirement, our advisors at Greenbush Financial Group can help you run detailed tax projections and withdrawal strategies to help your FIRE plan burn bright without burning through your savings.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

FAQs: FIRE Movement Tax Planning

-

Why is relying only on a traditional 401(k) risky for early retirees?Because you can't access most of those funds without penalties until 59 1/2, and every withdrawal is taxable as income.

-

How can I access retirement savings early without penalty?Use taxable brokerage accounts, Roth contributions (not earnings), or the 72(t) rule for limited access.

-

Are Roth IRAs better for early retirement (pre-59 1/2)?Yes. Withdrawals are tax-free, and contributions can be withdrawn anytime, offering flexibility.

-

What's a good account mix for FIRE planning?A balanced approach-roughly one-third pre-tax, one-third Roth, one-third taxable-provides strong tax diversification.

-

Can Roth conversions help early retirees?Absolutely. Converting pre-tax funds during low-income years can reduce lifetime taxes and future RMDs.

The SECURE Act 10-Year Rule Explained: Higher Taxes for Kids Who Inherit IRAs

The SECURE Act 10-year rule forces heirs to withdraw inherited retirement accounts faster, often increasing taxes. Learn how it works and strategies to reduce the impact on your family.

When Congress passed the SECURE Act, one of the most significant changes for families came from the new 10-year rule for inherited IRAs. The rule eliminated the ability for most non-spouse beneficiaries, especially adult children, to stretch required distributions over their lifetime. Now, they must empty the account within 10 years of inheriting it.

While this might sound simple, the tax impact can be severe. Compressed distribution windows often push heirs into higher brackets, accelerating income tax on decades of savings. Here is what the rule actually requires and how strategic planning can reduce the hit.

What the SECURE Act’s 10-Year Rule Says

Under the SECURE Act, when a child or other non-spouse inherits an IRA or 401(k), they must withdraw all funds by December 31 of the 10th year following the account owner’s death.

Before 2020, many beneficiaries could stretch required minimum distributions over their own life expectancy, sometimes 30 years or more, allowing continued tax-deferred growth. The SECURE Act ended that option for most heirs.

The result is that your kids will likely pay taxes on inherited retirement funds faster, and at potentially higher marginal rates, than they would have under the old rules.

Who the Rule Applies To

The 10-year rule applies to most non-spouse beneficiaries, but there are exceptions.

The rule applies to:

• Adult children or grandchildren

• Siblings, nieces, nephews, or other non-spouse heirs

• Trusts named as beneficiaries unless they qualify as see-through trusts

The rule does not apply to:

• Surviving spouses

• Minor children until they reach age 21, when the 10-year clock starts

• Disabled or chronically ill beneficiaries

• Beneficiaries less than 10 years younger than the account owner

The Hidden Tax Trap

For many families, the problem is not just the loss of tax deferral. It is the timing of the withdrawals. Most heirs inherit these accounts in their 40s or 50s, right in their peak earning years. Adding large inherited IRA distributions on top of salary and bonuses can easily push them into higher tax brackets.

Example:

If your child earns $120,000 per year and inherits a $1 million traditional IRA, they have just 10 years to withdraw it. Even spreading it evenly means an extra $100,000 in taxable income per year, enough to move them into a much higher bracket and increase Medicare or Net Investment Income taxes if applicable.

Our analysis at Greenbush Financial Group shows that this compression effect often results in 5 to 10 percent higher effective tax rates on inherited IRA dollars compared to pre-SECURE Act rules.

Planning Strategies to Reduce the Impact

There are several ways to mitigate the 10-year rule’s tax impact:

Roth conversions during your lifetime

Converting pre-tax IRAs to Roths allows your children to inherit tax-free assets. They will still follow the 10-year withdrawal rule, but distributions will be tax-free.Strategic beneficiary designations

Leave portions of retirement assets to lower-income heirs or to charitable remainder trusts.Staggered inheritances

Use taxable accounts, life insurance, or non-retirement assets to balance out future income for your kids.Pre-death withdrawals

Taking larger distributions during your own lower-income retirement years can smooth taxes across generations.Trust planning

Review existing conduit trusts. Many written before 2020 no longer operate as intended under the 10-year rule.

At Greenbush Financial Group, we often run multi-scenario tax projections showing how different withdrawal schedules, Roth conversions, or charitable strategies affect heirs’ long-term tax burdens.

Why This Matters for Your Estate Plan

The 10-year rule changed how retirement wealth passes between generations. What used to be a slow, tax-efficient transfer can now create a rapid, high-tax inheritance event.

Updating your beneficiary designations, estate documents, and withdrawal strategy is critical if you want your children to keep more of what you have saved. Even a modest Roth conversion plan or trust revision can reduce total taxes by hundreds of thousands of dollars over time.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

FAQs: SECURE Act 10-Year Rule

-

Do my kids have to take money out every year?Maybe. Annual required minimum distributions may be required if the decedent was of RMD age at passing. The RMD amount is likely less than one tenth of the account. The beneficiaries must still empty the inherited IRA by the end of year 10, so creating a strategy to reduce the overall tax burden is recommended.

-

Does the 10-year rule apply to Roth IRAs?Yes, but Roth withdrawals are tax-free. Heirs still need to empty the account within 10 years.

-

How does this affect trusts as IRA beneficiaries?Many conduit trusts written before 2020 now force the entire balance out in year 10, losing the intended protection and control. These should be reviewed.

-

Can I avoid the 10-year rule for my kids?Not directly, unless your child qualifies as an eligible beneficiary such as a minor or disabled dependent. Strategic Roth conversions or life insurance can help achieve similar goals.

-

Should I change my IRA beneficiaries now?Possibly. If your current structure assumed lifetime stretch distributions, it is time to review it under the new law.

Borrowing from Your 401(k)? One Wrong Move Could Trigger a Massive Tax Bill

Borrowing from your 401(k) may seem simple, but one mistake, like leaving your job, can trigger taxes, penalties, and long-term damage to your retirement savings. Understanding the rules before you borrow is critical.

Borrowing from your 401(k) might seem like an easy way to access cash, no credit check, low interest, and you’re paying yourself back. But one wrong move can trigger immediate taxes, penalties, and a permanent hit to your retirement savings. The IRS has strict rules on how 401(k) loans must be repaid and what happens if you leave your job before it’s paid off. Understanding those rules before you borrow can help you avoid costly surprises.

How 401(k) Loans Work

Most employer-sponsored 401(k) plans allow participants to borrow up to the lesser of $50,000 or 50% of their vested balance. Loans typically have to be repaid within five years through automatic payroll deductions, and the interest you pay goes back into your account.

On paper, it looks simple. You’re borrowing from yourself and putting the money back over time. But the biggest risk comes if your employment status, or repayment schedule, changes.

The Costly Mistake: Leaving Your Job Before Repayment

If you leave your employer, voluntarily or otherwise, with an outstanding 401(k) loan, the clock starts ticking. Under IRS rules, you must repay the entire remaining balance by the tax-filing deadline of the following year.

If you don’t repay it in time, the IRS classifies the unpaid balance as a “deemed distribution.” That means:

The outstanding amount is treated as taxable income in that year.

If you’re under age 59½, you’ll also face a 10% early withdrawal penalty.

Example:

If you owe $20,000 on a 401(k) loan when you change jobs and don’t repay it, that $20,000 becomes taxable income. Assuming a 22% federal bracket, you’ll owe $4,400 in federal tax, plus a $2,000 early withdrawal penalty—a total of $6,400 lost instantly.

Our analysis at Greenbush Financial Group shows that many borrowers underestimate this risk, particularly if they expect to switch jobs or retire early.

Why the Real Cost Is Even Higher

Taxes and penalties are only part of the loss. When you default on a 401(k) loan:

You lose future growth on the money permanently removed from your retirement plan.

You can’t simply “rollover” the unpaid balance into an IRA—it’s treated as distributed cash.

In long-term projections, a $20,000 distribution today can mean over $60,000 less in retirement savings 20 years from now, assuming a 7% annual return.

Smart Ways to Borrow Without Derailing Your Retirement

If you’re considering a 401(k) loan, these steps can help minimize the risk:

Understand your plan’s terms. Confirm repayment rules, interest rates, and whether you can continue contributing while repaying the loan.

Have a backup plan. Keep cash reserves or other assets available in case you leave your job unexpectedly.

Avoid borrowing for depreciating expenses. Using retirement funds for short-term needs like vacations or vehicles can compound long-term losses.

Check your employment stability. If you expect to change jobs soon, it’s better to wait or use other financing options.

Compare alternatives. A home equity line of credit (HELOC) or personal loan may cost less in taxes and missed growth over time.

At Greenbush Financial Group, we often help clients run side-by-side projections showing the real long-term cost of borrowing from their 401(k) compared to other options. In most cases, the total impact of lost compounding far outweighs the short-term benefit of easy access to funds.

The Bottom Line

A 401(k) loan can make sense in limited cases, such as paying off high-interest debt or covering an emergency expense when other options are exhausted. But understanding the repayment rules—and the risk of job loss—is critical. One mistake, like leaving your employer before repaying the loan, can trigger thousands in taxes and permanently shrink your retirement balance.

Before taking out a loan, it’s worth modeling different scenarios with a financial planner to ensure your short-term decision doesn’t create a long-term setback.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

FAQs: 401(k) Loan Rules and Risks

-

What’s the maximum I can borrow from my 401(k)?Generally, up to $50,000 or 50% of your vested balance, whichever is less.

-

How long do I have to repay a 401(k) loan?Most plans require repayment within five years, except when borrowing to purchase a primary residence.

-

What happens if I default on my loan?The unpaid balance is treated as a taxable distribution and may incur a 10% early withdrawal penalty if you’re under age 59½.

-

Can I roll my 401(k) loan into an IRA or new employer plan?No, loans cannot be rolled over. The balance must be repaid directly to avoid taxes.

-

Should I ever take a 401(k) loan?Only if the need is critical and you’re confident you’ll remain employed through the repayment period.

Is the Market About To Stage A Huge Rally?

The recent stock market pullback has been driven by rising oil prices, inflation concerns, and geopolitical tension involving Iran. As oil surged and uncertainty increased, markets reacted with increased volatility.

However, history shows that declines tied to geopolitical events are often temporary. This raises a key question for investors: is this a warning sign, or a setup for a potential market rally?

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

If the recent market volatility has made you uneasy, you’re not alone. Over the last few weeks, markets have reacted to rising oil prices, inflation concerns, and geopolitical tension in Iran. When volatility returns after a relatively calm period, it can feel like something is seriously wrong, but history tells us this is a normal part of investing, and specifically in this case, the market could be poised to rally in the coming weeks.

In this article, we’ll cover:

Forces at work in the market that have created the recent selloff

Whether the market may be near a bottom

What assets classes are performing well YTD in 2026

Charts to guide us as to where the market could go from here

What’s Causing the Market Sell-Off?

The recent market pullback hasn’t been caused by just one issue, but rather a combination of global events and economic pressures.

The biggest driver has been the conflict involving Iran, which has pushed oil prices significantly higher. At the start of the year, oil was around $57 per barrel, and as of March 23, 2026, oil has risen to roughly $90 per barrel. When oil prices rise that quickly:

The cost of transporting goods increases

The cost of producing goods increases

Inflation fears begin to rise

The Federal Reserve becomes less likely to cut interest rates

This is why markets have reacted negatively in the short term.

However, based on analyst expectations, there is a high probability that the Iran conflict will be resolved in the reasonably near future. If that happens, oil prices could fall, transportation costs could decline, and inflation fears could ease, which could put the Federal Reserve back on a path toward lowering interest rates.

And that combination has historically been very positive for markets.

It’s also important to remember that we’ve seen this movie before. Recent geopolitical events involving Greenland and Venezuela caused short-term market drops, but the markets recovered very quickly once those situations stabilized. Geopolitical events tend to create temporary volatility, not permanent declines.

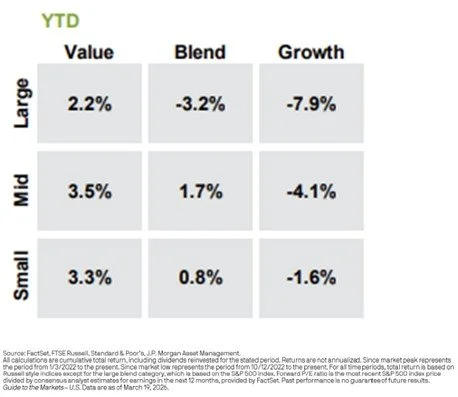

An Interesting Trend in 2026: Value vs. Growth

One of the most interesting trends this year has been the difference between large cap growth and large cap value.

As of last week:

Large cap growth is down about 7.9% year-to-date

Large cap value is up about 2.2% year-to-date

This shouldn’t be a huge surprise. Large cap value includes sectors like energy, which have performed very well due to rising oil prices. Meanwhile, many large cap growth and technology companies, including several of the “Magnificent Seven” stocks, have pulled back this year.

This is a great real-world reminder of why diversification matters.

When one part of the market struggles, another part of the market may be doing well. A properly diversified portfolio helps smooth out the ride when unexpected events occur.

Remember: Volatility Is Normal

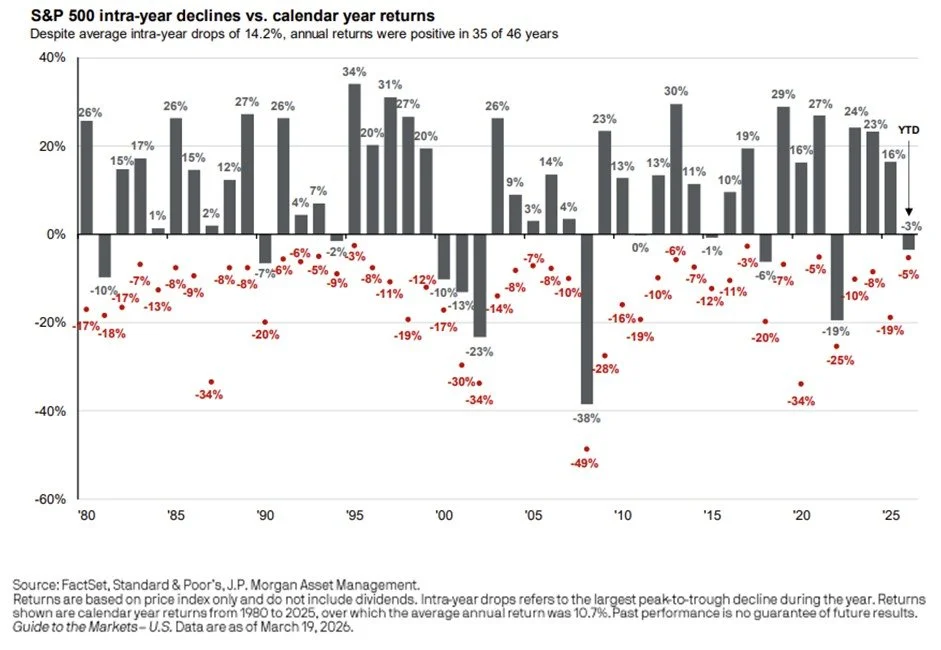

The chart below is a great reminder that selloffs and market volatility are normal even during good years for the stock market.

The chart shows two things going back to 1980:

The gray bars show the S&P 500 return for the full year

The red dots show the largest drop that occurred at some point during that year

For example:

In 2025, the market finished up 16%, but at one point during the year, it dropped by 19%

In 2024, the market finished up 23%, but had an 8% correction during the year

When you look at the last 45 years, a clear pattern emerges:

Most years the market finishes positive, but most years also have a signification correction at some point during the year.

This is the price of admission for investing. You don’t get the long-term returns of the market without experiencing volatility along the way.

Emotions and Panic Are the Enemy of Good Investment Decisions

The media and the markets will give investors something to worry about every single day.

Some of those concerns are legitimate. Many are not. The key is determining whether a current event represents a temporary disruption or a permanent change to the global economy.

Right now, the concern is Iran, oil prices, and inflation. A few months from now, it will likely be something else. That has always been the case, and it will continue to be the case.

One thing investors cannot forget is that we are currently in a massive wave of innovation and growth driven by artificial intelligence, automation, and robotics. These trends will likely have a much larger long-term impact on markets than most short-term geopolitical events.

This doesn’t mean markets won’t fall. They will.

It doesn’t mean volatility won’t happen. It will.

It doesn’t mean corrections won’t occur. They will.

But it does mean that panic-driven decisions are often the biggest mistake investors make.

Is the Market Close to the Bottom?

No one can consistently predict the exact bottom of a market correction. However, market declines driven by geopolitical events and oil shocks have historically recovered relatively quickly once the situation stabilizes. The Iran conflict is not likely be to any different.

If the Iran conflict cools down, and:

Oil prices fall

Transportation costs fall

Inflation fears ease

Then the current market pullback could reverse faster than many investors expect.

Market pullbacks often create opportunities that weren’t available when markets were at all-time highs just a few months ago.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

What Happens to an HSA Account When Someone Passes Away?

Health Savings Accounts offer powerful tax benefits, but those benefits can change significantly after death. This article explains how HSAs are treated when inherited by a spouse, non-spouse, or estate. Learn key tax rules, planning strategies, and how to reduce the tax burden on beneficiaries. Proper beneficiary designation is critical to maximizing HSA value.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Health Savings Accounts (HSAs) are one of the most tax-advantaged accounts available, but many people don’t realize that what happens to an HSA after death depends entirely on who the beneficiary is. The tax consequences can be very different depending on whether the beneficiary is a spouse, a non-spouse, or if no beneficiary is named at all.

In this article, we’ll cover:

What happens if a spouse is the beneficiary

What happens if a non-spouse is the beneficiary

What happens if no beneficiary is named

Strategies to reduce taxes on inherited HSAs

Why beneficiary designations are so important

Scenario 1: Spouse Is the Beneficiary

If a spouse is listed as the beneficiary of an HSA, the outcome is very favorable.

When the account owner passes away:

The spouse can assume ownership of the HSA

The transfer of ownership is not taxable

The spouse can continue using the HSA tax-free for qualified medical expenses

If the spouse already has their own HSA, they can roll the inherited HSA into their own HSA

This is the best-case scenario from a tax perspective because the account simply continues as an HSA with all the same tax benefits:

Pre-tax contributions

Tax-deferred growth

Tax-free withdrawals for medical expenses

In other words, the surviving spouse steps into the shoes of the original account owner.

Scenario 2: Non-Spouse Is the Beneficiary

If the beneficiary is not a spouse (for example, a child, grandchild, or friend), the rules change significantly.

When a non-spouse inherits an HSA:

The account ceases to be an HSA as of the date of death

The beneficiary cannot continue the HSA

The beneficiary cannot roll it into their own HSA

The fair market value of the HSA becomes taxable income to the beneficiary in the year of death

This means inheriting an HSA as a non-spouse can create a large immediate tax bill.

How to Reduce the Tax Impact

There is one strategy that can reduce the tax burden:

If the deceased had unpaid medical expenses at the time of death, the HSA can be used to pay those expenses. Any amount used to pay the decedent’s qualified medical expenses reduces the taxable amount that passes to the beneficiary.

Example:

HSA value at death: $50,000

Unpaid medical bills: $10,000

Taxable amount to beneficiary: $40,000

This can make a meaningful difference in the taxes owed.

Scenario 3: No Beneficiary Is Named

If no beneficiary is listed on the HSA:

The HSA becomes part of the deceased person’s estate

The fair market value of the HSA becomes taxable income on the final tax return

The account terminates as an HSA

This is usually the least favorable outcome, which is why it is very important to make sure beneficiaries are properly listed on your HSA account.

Planning Strategy: Should You Spend Your HSA If Your Beneficiaries Are Non-Spouse?

Because HSAs are not very tax-efficient to leave to non-spouse beneficiaries, it may make sense to use the HSA during your lifetime especially if:

You are single, or

Your beneficiaries are children or other non-spouse individuals

Remember, when you use HSA money for medical expenses, those dollars come out tax-free. But if a non-spouse inherits the account, the entire account can become taxable immediately.

After Age 65: Your HSA Works Like a Traditional IRA

Another important rule:

After age 65, you can take money out of an HSA for non-medical expenses and:

You will not pay a penalty

But you will pay ordinary income tax

It works similar to a traditional IRA

This creates a planning opportunity.

If it looks like:

You may not use all your HSA for medical expenses, and

You are in a lower tax bracket

It may make sense to intentionally withdraw money from the HSA and pay the tax at your lower tax rate, instead of leaving the entire account to a non-spouse beneficiary who may have to recognize the entire balance as income in a single year.

This strategy can help reduce the overall family tax bill.

Final Thoughts

HSAs are excellent savings vehicles, but they are not great assets to leave to non-spouse beneficiaries due to the immediate tax consequences.

That’s why good HSA planning includes:

Naming the correct beneficiaries

Using the HSA strategically during your lifetime

Coordinating HSA withdrawals with your tax bracket in retirement

When used properly, an HSA can be a powerful tool for retirement healthcare planning — but like all financial accounts, beneficiary planning matters.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

-

Does an HSA avoid probate?Yes, if a beneficiary is named, the HSA typically passes directly to the beneficiary.

-

Can my spouse continue my HSA after I die?Yes, a spouse can assume ownership of the HSA and continue using it as their own.

-

Do non-spouse beneficiaries pay taxes on inherited HSAs?Yes, the full value of the HSA is taxable income to the beneficiary in the year of death.

-

Can a child roll an inherited HSA into their own HSA?No, non-spouse beneficiaries cannot continue or roll over the HSA.

-

Can HSA funds be used to pay medical bills after death?Yes, HSA funds can be used to pay the deceased person's qualified medical expenses, which reduces the taxable amount to beneficiaries.

-

What happens if I forgot to name a beneficiary?The HSA becomes part of your estate and the value becomes taxable on your final tax return.

-

After age 65, can I use my HSA for non-medical expenses?Yes, you can withdraw funds penalty-free, but you will pay ordinary income tax.

-

Is an HSA a good account to leave to children?Generally, no. Because the account becomes fully taxable to them immediately.

-

Who should be the beneficiary of my HSA?In many cases, naming your spouse as beneficiary is the most tax-efficient option.

-

Should I spend down my HSA before I die?If your beneficiaries are non-spouse beneficiaries, it may make sense to use the HSA during your lifetime to avoid leaving them a large taxable account.

Tax Rules for Selling Your House to a Family Member

Selling a home to a family member involves more than just agreeing on a price. This guide explains tax implications, gift rules, cost basis considerations, and seller financing strategies. Learn how fair market value, the primary residence exclusion, and the Applicable Federal Rate impact your decision. Understand how to structure the transaction to avoid unintended tax consequences. Ideal for parents helping children navigate today’s housing market.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

This article was inspired by a conversation with a client who is considering selling their primary residence to their child. One of the biggest challenges in today’s housing market is affordability for first-time homebuyers. With housing prices and interest rates rising dramatically over the past five years, many parents who were already planning to downsize, relocate, or move into a more retirement-friendly home are now considering selling their home directly to their children to help them afford their first house.

While this can be a great strategy, there are a number of tax rules, gift rules, and financing considerations that need to be understood before entering into an intrafamily real estate transaction. In this article, we’re going to walk through the key areas families should consider before moving forward.

Discounting the Price of the House

One of the most common questions we get from clients is whether they should sell the house to their child at full market value or discount the price.

For example, if a house is worth $600,000, can you sell it to your child for $400,000?

The answer is yes, you can sell your house for whatever price you want. However, if you sell the home significantly below fair market value, the difference between the market value and the sale price may be considered a gift.

So if:

Market value = $600,000

Sale price = $400,000

Difference = $200,000

That $200,000 could be treated as a gift to the child.

For most families, this does not mean you will owe gift tax. However, you may need to file a gift tax return because the gift exceeds the annual gift exclusion. The amount above the annual exclusion simply reduces your lifetime gift exemption, which is currently $15 million per person at the federal level.

Why Selling at Fair Market Value May Be Better

From a tax standpoint, it may actually make more sense to sell the home at full market value rather than at a discount, because of the primary residence capital gain exclusion.

Single filer: Can exclude $250,000 of gain

Married filing jointly: Can exclude $500,000 of gain

Example

Purchase price: $200,000

Current value: $600,000

Gain: $400,000

If the parents are married, the $400,000 gain is below the $500,000 exclusion, meaning they would owe no capital gains tax even if they sell the home for full market value.

But the bigger planning opportunity is actually for the child’s future taxes.

If the child buys the home for $600,000, that becomes their cost basis. If they later sell the home for $1,000,000, their gain is $400,000, which may be fully covered by the primary residence exclusion.

However, if the parents sold the home for $400,000, the child’s cost basis is $400,000. If they later sell for $1,000,000, the gain is $600,000, and $100,000 could become taxable.

So in many situations, a better strategy may be:

Sell the home at fair market value and gift money for the down payment, instead of discounting the purchase price.

This can create a better long-term tax outcome.

Do the Parents Hold the Mortgage?

The next big question is how the child will finance the purchase. There are two main options:

Option 1: Traditional Mortgage

The child gets a mortgage through a bank, and the parents receive cash from the sale.

Option 2: Parents Hold the Mortgage (Seller Financing)

If the parents do not need the cash from the sale, they can hold the mortgage and essentially act as the bank. The child makes mortgage payments directly to the parents.

This is commonly called seller financing or an intrafamily mortgage.

Minimum Interest Rate (AFR)

If parents hold the mortgage, they must charge a minimum interest rate called the Applicable Federal Rate (AFR) to satisfy IRS rules. For a long-term loan such as a mortgage, the long-term AFR applies.

As of March 2026, the long-term AFR is approximately 4.6%.

So the process typically looks like this:

Determine purchase price

Determine down payment

Remaining balance becomes the mortgage

Mortgage must charge at least the AFR rate

Child makes monthly payments to the parents

Tax Treatment of Payments

As the child makes mortgage payments:

The Principal portion is not taxable to the parents

The Interest portion of each payment is taxable income to the parents

Forgiving the Mortgage

Another question that comes up with intrafamily mortgages is:

“Can we forgive payments or forgive the loan later?”

The answer is yes, but this brings us back to the gift rules.

Forgiving Monthly Payments

Let’s say the child’s mortgage payment is $3,000 per month and the parents decide to waive the payments for a year.

That would equal:

$3,000 × 12 = $36,000 per year

If the parents are married, they can gift up to the annual gift exclusion amount each year without filing a gift tax return (for example, $38,000 combined in 2026). If the forgiven amount is below the annual exclusion, no gift tax return is required.

If the forgiven amount exceeds the annual exclusion, then a gift tax return must be filed, but again, no gift tax is owed unless the parents exceed their lifetime exemption.

Forgiving the Entire Mortgage

If the parents decide at some point to forgive the remaining balance of the mortgage, that is considered a gift of the remaining loan balance, and a gift tax return would need to be filed for that year.

This shows that there is actually a lot of flexibility when families use intrafamily mortgages. Payments can be structured, forgiven, or adjusted over time, but the gift rules must be tracked.

Summary

If parents are in the fortunate position where they can sell their home to their child, we are seeing this strategy more and more due to the challenges first-time homebuyers face in today’s housing market.

However, it’s important to understand the key planning areas:

Should you sell at fair market value or discount the price?

Should the child get a traditional mortgage or should the parents hold the mortgage?

What are the Applicable Federal Rate (AFR) rules?

How do the gift tax rules apply if you discount the house or forgive payments?

How does this affect the child’s future cost basis?

How does this fit into the parents’ estate plan?

These transactions involve tax planning, estate planning, and financial planning, so we strongly recommend working with a tax professional and financial advisor when considering an intrafamily real estate transaction.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions

-

Can I sell my house to my child for less than market value?Yes, but the difference may be considered a gift.

-

Do I have to pay gift tax if I sell the house at a discount?Usually no, but you may need to file a gift tax return.

-

Do I pay capital gains tax if I sell to my child?You may qualify for the primary residence capital gain exclusion.

-

Is it better to sell at market value and gift the down payment?In many cases, yes, for long-term tax planning reasons.

-

Can I be the bank for my child’s mortgage?Yes, this is called seller financing.

-

What interest rate do I have to charge?At least the IRS Applicable Federal Rate (AFR).

-

Is the interest my child pays me taxable?Yes, interest is taxable income to the parents.

-

Can I forgive mortgage payments?Yes, but the forgiven amount may be considered a gift.

-

What happens if I forgive the entire loan?It is treated as a gift of the remaining balance.

-

Should we work with a professional for this type of transaction?Yes, you should coordinate with a CPA, financial advisor, and real estate attorney.

In Retirement, What Healthcare Costs Can Be Paid from an HSA Account?

Health Savings Accounts offer tax-free withdrawals for qualified medical expenses in retirement, but understanding eligibility rules is critical. This guide explains which expenses qualify, including Medicare premiums, dental, vision, and out-of-pocket costs. It also covers non-eligible expenses and key withdrawal rules before and after age 65. Use this resource to avoid costly HSA mistakes and maximize your retirement healthcare strategy.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

As people approach retirement, or enter retirement, healthcare costs often become one of the largest expenses in a financial plan. The good news is that Health Savings Accounts (HSAs) can be a powerful tool to help cover many of these costs using tax-free dollars. However, not every healthcare expense qualifies, so it’s important to understand both what can and cannot be paid from an HSA in retirement.

In this article, we’ll cover:

Which Medicare premiums are HSA-eligible

Whether COBRA premiums qualify

Dental, vision, and hearing expenses

Out-of-pocket medical costs

Medical equipment and prescriptions

Expenses that are not HSA-eligible

HSA withdrawal rules before and after age 65

Frequently asked HSA questions in retirement

Medicare Premiums

One of the most common uses for HSA funds in retirement is paying for Medicare premiums. HSA distributions can be used tax-free for:

Medicare Part B premiums

Medicare Part D premiums

Medicare Advantage (Part C) premiums

However, Medigap (Medicare Supplement) premiums are not considered a qualified HSA expense, even though Medicare Advantage plans are. This is a commonly misunderstood rule and an important one for retirees to be aware of when planning healthcare costs.

COBRA Coverage

If you retire before age 65 or leave an employer and elect COBRA coverage, those health insurance premiums can be paid from an HSA. This can be especially helpful for early retirees who need to bridge the gap before Medicare begins.

Dental, Vision, and Hearing Expenses

Dental, vision, and hearing costs are some of the most common out-of-pocket healthcare expenses in retirement — especially since many retirees no longer have employer coverage for these services.

HSA-eligible expenses include:

Dental cleanings, fillings, crowns, dentures, braces, and X-rays

Vision exams, eyeglasses, contact lenses, and LASIK surgery

Hearing aids and hearing aid batteries

Hearing aids alone can cost several thousand dollars, making the HSA a valuable tax-free resource for these expenses.

Out-of-Pocket Medical Expenses

Many routine healthcare costs in retirement are HSA-eligible, including:

Doctor visits

Specialist visits

Hospital services

Co-pays

Deductibles

Coinsurance

Surgery costs

Lab work and imaging

These are often the “everyday” medical expenses retirees experience each year.

Medical Equipment

If medical equipment is needed later in retirement, many of these expenses qualify for HSA distributions, including:

Walkers

Wheelchairs

Blood pressure monitors

Crutches

CPAP machines

Glucose monitors

Prescription Medications

Prescription drugs that are prescribed by a doctor are qualified HSA expenses.

However, over-the-counter medications typically do NOT qualify unless they are prescribed by a physician.

Expenses That Are NOT HSA-Eligible

Some healthcare-related expenses are not considered qualified medical expenses. These typically include:

Gym memberships

Nutritional supplements

Cosmetic procedures

Teeth whitening

General health items not prescribed by a doctor

Even though these may improve health, they are not considered qualified medical expenses under HSA rules.

Why HSAs Are So Powerful for Retirement

HSAs are one of the most tax-advantaged accounts available because they offer:

Tax-deductible contributions

Tax-free growth

Tax-free withdrawals for qualified medical expenses

Because healthcare costs are often highest in retirement, many individuals choose to pay for medical expenses out-of-pocket during their working years and allow their HSA to grow, using it later in retirement when healthcare costs increase.

HSA Withdrawal Rules: Before and After Age 65

It’s also important to understand the rules around HSA withdrawals:

Before age 65

Non-qualified withdrawals = taxable income + 20% penalty

After age 65

Non-qualified withdrawals = taxable income only (no penalty)

Works similar to a Traditional IRA if not used for healthcare

This provides additional flexibility later in retirement.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

-

Can HSA funds be used for Medicare premiums?Yes, for Medicare Part B, Part D, and Medicare Advantage premiums.

-

Can HSA funds be used for Medigap premiums?No, Medigap premiums are not considered a qualified expense.

-

Can I use my HSA for dental expenses in retirement?Yes, most dental expenses qualify.

-

Are vision expenses HSA-eligible?Yes, including exams, glasses, contacts, and LASIK.

-

Are hearing aids covered by an HSA?Yes, including hearing aid batteries.

-

Can I use my HSA for COBRA premiums?Yes, COBRA premiums are a qualified expense.

-

Are prescription drugs HSA-eligible?Yes, if prescribed by a doctor.

-

Are over-the-counter medications HSA-eligible?Typically no, unless prescribed by a physician.

-

What happens if I use HSA money for non-medical expenses before 65?You will owe income tax and a 20% penalty.

-

What happens if I use HSA money for non-medical expenses after 65?You will owe income tax, but no penalty.

Can Anyone Open an HSA Account?

Health Savings Accounts offer powerful tax advantages, but strict eligibility rules apply. This guide explains who can contribute to an HSA in 2026, including HDHP requirements, contribution limits, and Medicare restrictions. Learn how to avoid costly mistakes, especially as you approach age 65. A must-read for retirement-focused healthcare planning.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Health Savings Accounts (HSAs) are one of the most tax-advantaged accounts available and can be a powerful tool for paying healthcare costs in retirement. Contributions are made with pre-tax dollars, the account grows tax-deferred, and distributions are tax-free when used for qualified medical expenses. However, not everyone is eligible to contribute to an HSA, and understanding the eligibility rules is critical.

In this article, we’ll cover:

Who is eligible to contribute to an HSA

What qualifies as a High Deductible Health Plan (HDHP)

2026 HSA contribution limits

Special rules when approaching age 65 and Medicare

Frequently asked questions about HSA eligibility

Who Is Eligible to Contribute to an HSA?

To contribute to an HSA, you must meet all of the following requirements:

You must be enrolled in a High Deductible Health Plan (HDHP)

You cannot be covered by any other non-HDHP health insurance

You cannot be enrolled in Medicare

You cannot be claimed as a dependent on someone else’s tax return

The most common way people become eligible for an HSA is through their employer-sponsored high deductible health insurance plan. If your employer’s health insurance plan is not classified as a high deductible plan, then you are not eligible to contribute to an HSA.

What Qualifies as a High Deductible Health Plan in 2026?

Each year, the IRS defines what qualifies as a High Deductible Health Plan. For 2026, a plan must meet the following minimum deductible and maximum out-of-pocket limits:

If your health insurance plan does not meet these thresholds, it is not considered HSA-eligible, and you cannot contribute to an HSA.

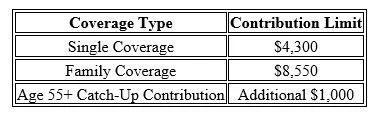

HSA Contribution Limits for 2026

The IRS also sets contribution limits each year. For 2026, the HSA contribution limits are:

These limits include both employee and employer contributions combined. So if your employer contributes to your HSA, that amount counts toward the total annual limit.

Because these limits are indexed for inflation, they typically increase slightly each year.

Be Careful as You Approach Age 65 (Medicare Rule)

There is a very important rule regarding HSAs and Medicare that many people are not aware of:

Once you enroll in Medicare, you can no longer contribute to an HSA.

However, there is an additional rule that affects individuals who work past age 65 and delay Medicare.

The 6-Month Medicare Retroactive Rule

When someone enrolls in Medicare Part A after age 65, Medicare coverage is retroactive for 6 months (but not earlier than age 65).

Because of this:

You must stop HSA contributions 6 months before applying for Medicare

Otherwise, those contributions become excess contributions

Excess contributions can result in tax penalties if not corrected

Example

Let’s say someone is 67, still working, and contributing to an HSA.

If they plan to enroll in Medicare in December, they should stop HSA contributions by June of that year.

If they do not, they may need to withdraw excess contributions and potentially pay penalties.

Important Exception

If you enroll in Medicare right at age 65, you do not need to stop contributions 6 months early because Medicare cannot retroactively start before age 65.

Why HSAs Can Be So Valuable

HSAs are often used as a retirement healthcare savings account because:

Contributions are pre-tax

Growth is tax-deferred

Withdrawals are tax-free for medical expenses

After age 65, withdrawals for non-medical expenses are penalty-free (taxable only)

Because healthcare is often one of the largest expenses in retirement, many individuals choose to save their HSA funds during their working years and use them later in retirement.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

-

Can anyone open an HSA account?No. You must be enrolled in a qualified High Deductible Health Plan.

-

Can I contribute to an HSA if I am self-employed?Yes, as long as you have an HSA-eligible high deductible health insurance plan.

-

Can I contribute to an HSA if I am on Medicare?No. Once enrolled in Medicare, you can no longer contribute.

-

Can my employer contribute to my HSA?Yes, and employer contributions count toward the annual limit.

-

What happens if I contribute to an HSA while on Medicare?Those contributions are considered excess contributions and may be subject to penalties.

-

Can both spouses contribute to an HSA?Yes, if both spouses are eligible and covered by an HSA-qualified plan.

-

Do HSA contribution limits change each year?Yes, they are typically adjusted annually for inflation.

-

What is the catch-up contribution for people over age 55?An additional $1,000 per year.

-

Can I still use my HSA after I go on Medicare?Yes, you just cannot contribute anymore.

-

What happens if I exceed the HSA contribution limit?You may have to withdraw the excess contribution and could owe penalties if not corrected.