The Real Cost of Buying a Home: Expenses First-Time Buyers Often Miss

The true cost of buying a home extends far beyond the mortgage payment. First-time home buyers should plan for closing costs, maintenance, property taxes, homeowners insurance, utilities, HOA fees, and emergency repairs. Understanding these expenses can help avoid cash flow surprises and improve long-term affordability. Greenbush Financial Group explains how thoughtful budgeting and financial preparation can make homeownership more sustainable and less stressful.

Many first-time home buyers focus almost entirely on the down payment and monthly mortgage. But the real cost of homeownership often includes additional expenses that can strain cash flow if they are not planned for ahead of time. Closing costs, maintenance, property taxes, insurance, utilities, and unexpected repairs can all affect affordability. At Greenbush Financial Group, we often find that buyers feel more confident when they understand the full financial picture before purchasing a home.

Buying a Home Costs More Than Most First-Time Buyers Expect

For many people, buying a first home feels like reaching a major financial milestone.

But one of the biggest surprises for first-time buyers is realizing that the monthly mortgage payment is only part of the total cost.

Many buyers spend years saving for:

The down payment

Moving expenses

Furniture

Mortgage qualification

Yet still feel financially stretched after moving in because they underestimated the ongoing costs of homeownership.

The goal is not avoiding homeownership.

The goal is understanding the full financial commitment before signing the paperwork.

Because the hidden costs are often what create stress later.

The Mortgage Payment Is Only the Starting Point

When buyers estimate affordability, they often focus only on:

Principal

Interest

But homeownership usually includes several additional recurring expenses.

Monthly Housing Costs May Include:

Property taxes

Homeowners insurance

HOA fees

Maintenance costs

Utilities

Lawn care

Pest control

Repairs

Internet and security systems

In many cases, the true monthly cost of owning a home can be significantly higher than the mortgage itself.

Hidden Cost #1: Closing Costs

Many first-time buyers are surprised to learn that the down payment is not the only upfront expense.

Closing costs can often range from:

2%–5% of the purchase price

These costs may include:

Loan origination fees

Appraisal fees

Title insurance

Attorney fees

Escrow funding

Recording fees

Inspection costs

Prepaid taxes and insurance

Example

A buyer purchasing a $400,000 home may face:

$8,000–$20,000 in closing costs

In addition to the down payment.

That can create a major cash-flow surprise if buyers are not prepared.

Hidden Cost #2: Maintenance and Repairs

One of the biggest lifestyle adjustments for renters is realizing that homeowners become responsible for everything.

When something breaks, there is no landlord to call.

Common Expenses Include:

Roof repairs

HVAC replacement

Water heaters

Plumbing issues

Appliance replacement

Landscaping

Gutter cleaning

Electrical repairs

A Common Rule of Thumb

Many homeowners should expect to budget roughly:

1%–2% of the home’s value annually for maintenance

That does not mean every year will be expensive.

But large repairs tend to arrive eventually.

Hidden Cost #3: Property Taxes Often Increase

Many buyers underestimate how property taxes may change over time.

Taxes can increase because of:

Rising home values

Local tax reassessments

School district changes

Municipal budget increases

In some areas, property taxes may rise significantly faster than buyers expect.

Important Note

Some online mortgage calculators underestimate future tax increases because they rely on previous owner assessments.

That can create affordability surprises later.

Hidden Cost #4: Homeowners Insurance

Insurance costs have become a growing issue in many parts of the country.

Premiums may rise because of:

Weather risks

Inflation

Construction costs

Claims history

Regional insurance market changes

Many first-time buyers focus heavily on mortgage rates while underestimating how much insurance may affect monthly costs.

Hidden Cost #5: Utilities Can Change Dramatically

Renters sometimes underestimate how utility costs change with larger spaces.

A new home may involve:

Higher electric bills

Water costs

Trash service

Gas bills

Internet upgrades

Older homes may also be less energy efficient than expected.

Hidden Cost #6: Furniture and Home Purchases

Many first-time homeowners spend heavily immediately after moving in.

Common purchases include:

Furniture

Appliances

Window treatments

Tools

Lawn equipment

Decor

Home office setup

Individually, these purchases may seem manageable.

Together, they can significantly strain savings during the first year.

Hidden Cost #7: HOA Fees and Special Assessments

Homeowners Association fees are often overlooked during budgeting.

Monthly HOA dues may cover:

Landscaping

Community maintenance

Amenities

Exterior upkeep

But HOAs can also issue special assessments for unexpected repairs or large projects.

That can create sudden expenses homeowners did not anticipate.

Hidden Cost #8: Emergency Cash Reserves

Many buyers use most of their savings for the down payment and closing costs.

That can leave very little flexibility afterward.

This becomes risky because homeownership often involves unexpected expenses shortly after moving in.

Examples include:

Appliance failure

Water leaks

HVAC repairs

Moving-related costs

Insurance deductibles

Maintaining emergency savings after the purchase is extremely important.

The Emotional Side of Buying a First Home

First-time buyers often feel pressure to:

Stretch their budget

Buy quickly

Win bidding wars

Maximize house size

Compete with peers

That emotional pressure can lead buyers to underestimate ongoing affordability concerns.

Important Question

The better question is often not:

“What is the maximum home I can qualify for?”

Instead ask:

“What home can I comfortably maintain while still saving for future goals?”

A Real-World Example

Sarah and Michael purchase their first home for:

$450,000

They budget carefully for:

Their down payment

Mortgage payment

But after moving in, they encounter:

$11,000 in closing costs

Higher-than-expected property taxes

A leaking water heater

Increased utility bills

Furniture purchases

HOA dues they underestimated

Within the first year, they spend far more than expected beyond the mortgage payment itself.

The issue was not buying the home.

The issue was underestimating total ownership costs.

How First-Time Buyers Can Prepare Financially

1. Stress-Test the Monthly Budget

Estimate housing costs using:

Mortgage

Taxes

Insurance

Maintenance

Utilities

HOA fees

Not just principal and interest.

2. Keep Cash Reserves After Closing

Avoid draining every dollar of savings for the purchase itself.

Many homeowners feel far more comfortable with emergency reserves intact.

3. Plan for Maintenance Early

Repairs are not “if” expenses.

They are “when” expenses.

Building maintenance savings into the budget can reduce future stress.

4. Avoid Furnishing the Entire House Immediately

Many buyers overspend during the first year trying to complete every room immediately.

Gradual upgrades often create less financial pressure.

5. Understand Long-Term Affordability

Ask whether the home still feels affordable if:

Property taxes rise

Insurance increases

One spouse changes jobs

Interest rates remain elevated

Maintenance costs increase

Homeownership should create stability, not constant financial pressure.

Common First-Time Buyer Mistakes

1. Spending All Savings on the Down Payment

This leaves little flexibility for repairs and emergencies.

2. Underestimating Maintenance Costs

Homeownership almost always includes ongoing repairs.

3. Focusing Only on the Mortgage Payment

Taxes, insurance, utilities, and maintenance matter too.

4. Buying Based on Loan Approval Instead of Comfort

Qualification amounts do not always reflect sustainable budgeting.

5. Ignoring Future Lifestyle Changes

Buyers should consider future:

Children

Job changes

Commutes

Healthcare costs

Income changes

Final Thoughts

Buying your first home can be exciting and financially meaningful.

But homeownership costs are often broader than many buyers initially expect.

At Greenbush Financial Group, we often find that financially successful homeowners are not necessarily the ones who buy the largest house. They are often the ones who prepare thoughtfully for both the expected and unexpected costs of ownership.

The goal is not avoiding homeownership.

It is understanding the full financial picture before making one of the largest purchases of your life.

Confidence usually comes from preparation, not stretching every dollar to the limit.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

-

What hidden costs do first-time home buyers often miss?

Common overlooked expenses include closing costs, maintenance, repairs, property taxes, insurance, HOA fees, and utility increases. -

How much should buyers budget for maintenance?

Many homeowners budget roughly 1%-2% of the home's value annually for maintenance and repairs. -

Are closing costs separate from the down payment?

Yes. Closing costs are additional expenses typically ranging from 2%-5% of the purchase price. -

Why do property taxes sometimes increase after purchase?

Taxes may rise because of reassessments, home value increases, or local government changes. -

How much emergency savings should homeowners keep?

Many financial professionals recommend maintaining emergency reserves even after paying the down payment and closing costs. -

Are HOA fees included in mortgage payments?

Sometimes HOA fees are separate from the mortgage payment and must be budgeted independently. -

Should buyers use all available savings for a down payment?

Usually not. Maintaining liquidity for emergencies and repairs is often important after moving into a home. -

What is the biggest mistake first-time home buyers make?

One of the biggest mistakes is focusing only on the mortgage payment while underestimating the full ongoing cost of homeownership.

Retirement Income Planning: How to Pay Yourself Without a Job

Creating retirement income requires more than simply withdrawing money from investment accounts. This guide explains how retirees can coordinate Social Security benefits, investment withdrawals, and cash reserves to build a reliable retirement paycheck while managing taxes, sequence-of-returns risk, and market volatility. Learn practical withdrawal strategies that help improve long-term portfolio sustainability and increase retirement confidence. Discover why organized income planning often matters more than chasing investment returns alone.

The hardest part of retirement is not saving money. It is turning your savings into a paycheck that can last for decades. A strong retirement income strategy combines Social Security, investments, and cash reserves in a way that helps retirees manage taxes, market downturns, and long-term spending needs. At Greenbush Financial Group, we often find that retirees feel more confident once they move from random withdrawals to a structured retirement paycheck plan.

The Hardest Part of Retirement Is Not Saving. It’s Replacing Your Paycheck.

For most of your working life, income was automatic.

You worked, your paycheck arrived, taxes were withheld, and bills were paid.

Retirement changes that system overnight.

Now your income may need to come from:

Social Security

Investment accounts

IRAs

Roth IRAs

Cash savings

Brokerage accounts

Maybe a pension

That transition can feel uncomfortable even for financially responsible retirees.

Many people spend decades learning how to save for retirement but very little time learning how to withdraw from retirement.

That is why one of the biggest retirement questions becomes:

“How do I actually turn my savings into reliable monthly income?”

The answer is usually not:

Living only on dividends

Using the 4% rule blindly

Pulling money randomly from accounts

Staying fully invested with no cash reserves

A retirement paycheck works best when it is intentional, flexible, tax-aware, and designed to handle both good markets and bad ones.

What a Retirement Paycheck Actually Looks Like

A retirement paycheck is usually built from three primary sources:

Guaranteed income

Investment withdrawals

Cash reserves

Each source plays a different role.

The goal is not maximizing investment returns.

The goal is creating sustainable monthly income while reducing unnecessary financial stress.

The 3 Buckets of Retirement Income

Bucket #1: Guaranteed Income

This includes predictable income sources such as:

Social Security

Pensions

Certain annuities

For many retirees, this income helps cover core living expenses like:

Housing

Utilities

Groceries

Insurance

Basic healthcare costs

Guaranteed income creates stability.

The more predictable income a retiree has, the less pressure there may be on investment withdrawals during difficult markets.

Bucket #2: Investment Withdrawals

This is where retirees often generate additional income beyond Social Security.

Withdrawals may come from:

Traditional IRAs

401(k)s

Taxable brokerage accounts

Roth IRAs

This is also where many costly mistakes happen.

Without a strategy, retirees may:

Withdraw too much

Trigger unnecessary taxes

Increase Medicare premiums

Sell investments during downturns

Deplete the wrong accounts too early

The order of withdrawals matters.

Bucket #3: Cash Reserves

Cash reserves are one of the most overlooked parts of retirement income planning.

Cash reserves may include:

Savings accounts

Money market funds

CDs

Treasury bills

Short-term bond holdings

The purpose of cash is not maximizing returns.

Its purpose is flexibility.

Cash reserves help retirees avoid selling investments during bad markets when emotions are elevated and portfolio values are temporarily down.

How Retirement Income Is Structured Month to Month

Retirement income planning usually starts with one simple question:

“How much do you actually need each month?”

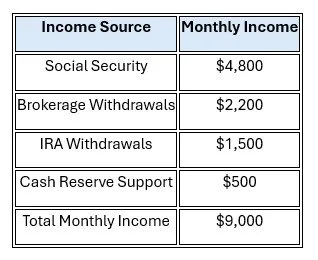

Step 1: Identify Monthly Spending Needs

Example:

John and Linda retire at age 66.

They estimate they need:

$8,000/month after taxes

That includes:

Property taxes

Insurance

Healthcare

Travel

Utilities

Food

Entertainment

Home maintenance

Step 2: Subtract Guaranteed Income

They receive:

$4,500/month combined from Social Security

That leaves:

$3,500/month that must come from investments and savings

This is called the income gap.

Step 3: Build a Withdrawal Strategy

Their assets include:

$950,000 in IRAs

$300,000 in brokerage accounts

$150,000 in cash reserves

$200,000 in Roth IRAs

Instead of taking income randomly, they decide to:

Use brokerage assets first for flexibility

Maintain 18 months of cash reserves

Delay larger IRA withdrawals strategically

Refill cash reserves during stronger market periods

Keep Roth assets growing longer for future flexibility

Now their retirement income becomes organized and repeatable rather than reactive.

Why Random Withdrawals Can Create Long-Term Problems

Many retirees withdraw from whichever account feels easiest at the time.

That can create ripple effects.

Example

Suppose a retiree withdraws $80,000 entirely from an IRA for spending and home renovations.

That withdrawal may:

Push income into higher tax brackets

Increase taxation of Social Security

Trigger Medicare IRMAA surcharges

Reduce future Roth conversion opportunities

A different withdrawal strategy may have created a better long-term outcome.

Retirement income planning is not just about generating cash.

It is about generating cash efficiently.

Why Cash Reserves Matter So Much in Retirement

Many retirees underestimate how emotionally different investing feels after paychecks stop.

During working years, market declines may feel temporary because new paychecks continue arriving.

Retirement changes that dynamic.

Now withdrawals may be happening while investments are falling.

That creates what planners call sequence-of-returns risk.

What Is Sequence Risk?

Sequence risk occurs when poor market returns happen early in retirement while withdrawals are occurring simultaneously.

This combination can permanently reduce long-term portfolio sustainability.

Example

Two retirees start with identical portfolios and identical spending.

One is forced to sell investments during a major downturn to fund living expenses.

The other uses cash reserves temporarily while allowing investments time to recover.

The long-term outcomes can look dramatically different.

How Much Cash Should Retirees Keep?

There is no perfect answer.

But many retirees feel more comfortable keeping:

12–24 months of planned withdrawals in cash or short-term reserves

The appropriate amount depends on:

Risk tolerance

Market exposure

Spending flexibility

Healthcare concerns

Pension income

Comfort during volatility

Important Note

Too little cash may force investment sales during downturns.

Too much cash may reduce long-term purchasing power because inflation slowly erodes cash value.

The goal is balance.

Should Retirees Live Off Dividends Only?

Many retirees like the idea of “never touching principal” and living entirely off dividends.

While dividend income can help, retirement income planning is usually more nuanced than that.

Dividend-only strategies can create problems such as:

Concentrated portfolios

Reduced diversification

Lower flexibility

Chasing yield

Tax inefficiencies

What matters most is not whether income comes from dividends or withdrawals.

What matters is:

Total return

Sustainability

Tax efficiency

Risk management

Flexibility during market declines

A well-designed retirement paycheck should focus on the overall income strategy, not just one type of investment income.

How Social Security Fits Into a Retirement Paycheck

Social Security is often the foundation of retirement income.

The timing decision affects:

Monthly income

Portfolio withdrawals

Survivor income

Longevity protection

Taxes

Claiming at 62

Taking benefits early provides income sooner but permanently reduces monthly payments.

This may reduce portfolio withdrawals initially.

But it also lowers guaranteed lifetime income.

Claiming at Full Retirement Age

Waiting until full retirement age increases monthly benefits and avoids early claiming reductions.

For many retirees, this creates a balance between income needs and future benefit growth.

Delaying Until Age 70

Benefits increase each year benefits are delayed beyond full retirement age.

For healthy retirees, delayed Social Security can act as additional protection against longevity risk later in retirement.

Especially for married couples, this can significantly affect survivor income.

How Retirees Avoid Selling Investments During Market Declines

A strong retirement paycheck strategy is designed before market volatility happens.

That strategy often includes:

Cash reserves

Diversification

Flexible withdrawals

Annual tax reviews

Periodic rebalancing

Spending flexibility

Example Strategy

A retiree may:

Hold 18 months of withdrawals in cash

Use Social Security for core expenses

Withdraw from brokerage accounts during stable markets

Reduce discretionary spending during downturns

Refill cash reserves after stronger market periods

This creates options during stressful periods instead of forcing emotional decisions.

How Often Should Retirement Income Plans Be Reviewed?

Retirement income planning is not a one-time event.

Most retirees should review their strategy annually.

Areas worth reviewing include:

Withdrawal rates

Tax brackets

Roth conversion opportunities

Medicare IRMAA exposure

Cash reserve levels

Investment allocation

Spending changes

Inflation adjustments

The goal is not constantly changing the plan.

The goal is making thoughtful adjustments as retirement evolves.

A Real-World Retirement Paycheck Example

Susan and Mark retire at ages 65 and 63.

They need:

$9,000/month after taxes

Their income plan looks like this:

Their Strategy

They maintain:

18 months of cash reserves

Moderate stock exposure for long-term growth

Diversification across account types

Annual withdrawal reviews

Flexible discretionary spending

During strong markets, they replenish cash reserves.

During weaker markets, they temporarily rely more heavily on cash rather than aggressively selling investments.

This approach helps reduce emotional pressure during volatility.

Common Retirement Paycheck Mistakes

1. Withdrawing Randomly From Accounts

Random withdrawals often create tax inefficiencies and unnecessary portfolio stress.

2. Keeping Too Little Cash

Without adequate reserves, retirees may be forced to sell investments during downturns.

3. Keeping Too Much Cash

Excessive cash can reduce long-term purchasing power because of inflation.

4. Ignoring Taxes

Taxes affect:

IRA withdrawals

Social Security taxation

Medicare premiums

Roth conversion opportunities

Retirement income should be coordinated at the household level.

5. Assuming the Same Strategy Works Forever

Retirement income plans should evolve over time as:

Spending changes

Healthcare costs rise

Markets fluctuate

RMDs begin

Tax laws change

Flexibility matters.

What Retirees Often Discover

Many retirees initially focus almost entirely on investment performance.

But over time, confidence often comes more from:

Organized cash flow

Predictable income

Tax coordination

Flexibility during downturns

Understanding where each dollar comes from

A retirement paycheck is not about finding a perfect strategy.

It is about building a system that feels sustainable and manageable over time.

Final Thoughts

The hardest part of retirement is usually not building wealth.

It is learning how to turn decades of savings into reliable monthly income.

A thoughtful retirement paycheck strategy can help retirees:

Reduce financial stress

Improve tax efficiency

Navigate market downturns

Protect long-term portfolio sustainability

Feel more confident about spending decisions

At Greenbush Financial Group, we often find that retirees gain confidence when they stop thinking about retirement income as random withdrawals and start viewing it as a coordinated household paycheck strategy.

The goal is not predicting every market movement perfectly.

The goal is creating a flexible income system that can support retirement through both strong markets and difficult ones.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

FAQ

-

How do retirees create a monthly paycheck from investments?Most retirees combine Social Security, investment withdrawals, and cash reserves to create consistent monthly income. Withdrawals are typically coordinated across different account types to improve tax efficiency and manage market risk.

-

How much cash should retirees keep?Many retirees benefit from holding 12-24 months of planned withdrawals in cash or short-term reserves, especially during the early retirement years.

-

What accounts should retirees withdraw from first?The answer depends on taxes, age, income needs, and long-term planning goals. Many retirees use a combination of taxable accounts, IRAs, and Roth accounts strategically rather than withdrawing from only one source.

-

What is sequence-of-returns risk?Sequence risk occurs when poor market returns happen early in retirement while withdrawals are being taken. This can permanently reduce long-term portfolio sustainability.

-

Should retirees rely only on dividends for income?Not necessarily. While dividends can help, most retirement income plans work better when they focus on total return, diversification, flexibility, and tax efficiency rather than dividends alone.

-

How does Social Security fit into a retirement paycheck?Social Security often acts as the foundation of retirement income by covering a portion of essential expenses and reducing pressure on investment withdrawals.

-

How often should retirement income plans be reviewed?Most retirees should review income strategies annually to evaluate taxes, spending, investment allocation, withdrawal rates, and healthcare costs.

-

What is the biggest retirement income mistake?One of the biggest mistakes is withdrawing money randomly from investment accounts without coordinating taxes, cash reserves, and long-term income sustainability.

The First Year of Retirement: 7 Financial Moves to Make…and 5 to Avoid

The first year of retirement is one of the most important financial transition periods retirees face. This article explains how to build a retirement withdrawal strategy, evaluate Social Security timing, manage Roth conversion opportunities, avoid Medicare IRMAA surprises, and adjust investment risk after leaving work. Learn the financial mistakes many retirees make during year one and how thoughtful planning can improve long-term retirement income sustainability. Greenbush Financial Group outlines practical retirement planning strategies designed to help retirees build confidence and flexibility during the transition into retirement.

The first year of retirement is one of the most important financial transition periods you’ll ever experience. Decisions around withdrawals, Social Security, taxes, investments, and healthcare can affect your retirement income for decades. Many retirees focus on enjoying newfound freedom but overlook key planning opportunities that exist before year-end and before required distributions begin. At Greenbush Financial Group, we often see that the retirees who build confidence early are the ones who slow down and make intentional first-year decisions.

The First Year of Retirement Is a Transition Year, Not Just a Celebration Year

Retirement changes more than your schedule. It changes how your household generates income, pays taxes, handles market volatility, and manages financial decisions.

For decades, most people operated under a simple formula:

Work

Receive paycheck

Save for retirement

Repeat

Then retirement arrives, and suddenly everything reverses.

Now your investments may need to generate income. Tax planning becomes more flexible but also more important. Healthcare costs become more visible. Market declines can feel more emotional once paychecks stop.

The first year of retirement is often what we call an “adjustment year.” The decisions made during this period can shape:

Future tax brackets

Medicare premiums

Portfolio longevity

Social Security income

Roth conversion opportunities

Spending habits

Confidence during market volatility

The goal is not perfection.

The goal is avoiding expensive mistakes while building a sustainable retirement income strategy.

7 Smart Financial Moves to Make During Your First Year of Retirement

1. Build a Retirement Paycheck Plan Before Taking Withdrawals

One of the biggest mistakes new retirees make is randomly pulling money from accounts as expenses arise.

Retirement income should be coordinated intentionally.

Before taking withdrawals, determine:

How much monthly income you actually need

Which accounts will fund that income

How taxes will affect withdrawals

Which accounts should remain invested longer

How cash reserves will be handled

Many retirees discover their actual spending differs from what they expected.

The first year is often more expensive because of:

Travel

Home projects

Healthcare changes

Helping family

Celebration spending

A paycheck-style withdrawal strategy can create structure and reduce emotional decision-making.

Example

A retired couple needs $7,000 per month after taxes.

They have:

$1.2 million invested

$700,000 in IRAs

$300,000 in taxable accounts

$200,000 in Roth IRAs

No Social Security yet

Instead of withdrawing entirely from their IRA, they may benefit from:

Using taxable savings first

Realizing lower capital gains

Keeping taxable income lower

Preserving future Roth growth opportunities

The order of withdrawals matters more than many retirees realize.

2. Reevaluate Whether to Claim Social Security Immediately

Many retirees automatically claim Social Security as soon as work ends.

That decision can permanently reduce lifetime income.

For healthy retirees with adequate assets, delaying benefits can sometimes improve long-term retirement security.

Key factors include:

Health and longevity expectations

Spousal benefits

Survivor income planning

Tax brackets

Portfolio withdrawal needs

Other income sources

Important Note

Claiming early is not always wrong.

But the first year of retirement is the time to evaluate the decision carefully rather than defaulting to “I stopped working, so I should claim now.”

Example

A retiree eligible for $2,200/month at age 62 may receive roughly $3,900/month if delaying until age 70.

For married couples, this can significantly affect survivor income later.

3. Review Roth Conversion Opportunities Before Year-End

The years between retirement and Required Minimum Distributions (RMDs) can create unusually low-income tax years.

Those years may offer valuable Roth conversion opportunities.

This is one of the most overlooked planning opportunities in retirement.

Converting portions of a traditional IRA to a Roth IRA during lower-income years may help:

Reduce future RMDs

Lower future tax exposure

Create tax-free income later

Reduce widow’s tax risk

Improve long-term tax flexibility

Example

A couple retires at 64 and delays Social Security until 67.

For several years, their taxable income may be significantly lower than during their working years.

They may intentionally convert enough IRA assets annually to “fill up” a lower tax bracket before:

RMDs begin

Social Security increases taxable income

Medicare IRMAA thresholds become an issue

Key Insight

The first retirement year is often more valuable for tax planning than people realize because income may temporarily drop before other retirement income sources begin.

4. Review Medicare IRMAA Exposure Early

Many retirees are surprised when Medicare premiums increase because of prior-year income.

IRMAA stands for Income-Related Monthly Adjustment Amount.

Higher-income retirees can pay significantly more for Medicare Part B and Part D premiums.

Common triggers include:

Large IRA withdrawals

Roth conversions

Capital gains

Selling property

Large bonuses during retirement year

Why This Matters in Year One

The retirement transition often creates unusual tax years.

Without planning, retirees can accidentally trigger higher Medicare premiums two years later.

Important Note

Sometimes triggering IRMAA still makes sense.

For example, a strategic Roth conversion today may still save substantial taxes later.

The key is understanding the tradeoff before making the move.

5. Keep a Larger Cash Reserve Than You Think You Need

The first few years of retirement are emotionally different from the accumulation years.

Market volatility can feel more stressful when paychecks stop.

A properly structured cash reserve can help retirees avoid selling investments during market declines.

This reserve may cover:

12–24 months of spending needs

Major healthcare expenses

Home repairs

Unexpected family support

Market downturns

What Many Retirees Get Wrong

Some retirees stay fully invested because they fear missing returns.

Others hold too much cash and reduce long-term growth potential.

The goal is balance.

A thoughtful reserve strategy can improve both flexibility and emotional confidence.

6. Recheck Your Investment Risk Now That You’re Retired

Many investors discover they were comfortable with risk only while employed.

Once retirement begins, market declines feel different.

This does not mean retirees should abandon growth investments entirely.

But it does mean portfolios should reflect:

Withdrawal needs

Time horizon

Income stability

Emotional tolerance for volatility

Sequence-of-returns risk

What Is Sequence Risk?

Poor market returns early in retirement can create lasting damage when withdrawals are occurring simultaneously.

This is why investment structure matters more after retirement begins.

Common First-Year Mistake

Making aggressive investment changes during a market drop.

Some retirees panic after their first retirement correction and move heavily to cash after losses already occurred.

That can permanently damage long-term retirement sustainability.

7. Review Estate Documents and Beneficiaries

Retirement is a major life transition and an ideal time to revisit estate planning.

Review:

Wills

Trusts

Powers of attorney

Healthcare directives

IRA beneficiaries

Life insurance beneficiaries

Common Issue

Beneficiary designations often override wills.

We regularly see outdated beneficiaries remain unchanged for decades.

Also Important

Review how retirement accounts align with tax planning and legacy goals.

For some households, Roth accounts may be more attractive legacy assets than traditional IRAs because of future tax implications for heirs.

5 Financial Moves to Avoid During Your First Year of Retirement

1. Avoid Major Lifestyle Purchases Too Quickly

Many retirees make large purchases immediately after retiring:

Vacation homes

RVs

Boats

Major renovations

Large gifts to children

The issue is not the purchase itself.

The issue is making irreversible financial decisions before understanding your long-term retirement spending pattern.

Better Approach

Give yourself time to observe:

Actual spending

Healthcare costs

Tax changes

Lifestyle adjustments

Market conditions

Your first-year spending may not reflect your long-term retirement reality.

2. Avoid Claiming Social Security Without Running the Numbers

Social Security timing is often permanent.

Many retirees underestimate:

Survivor implications

Inflation protection

Longevity risk

Tax coordination opportunities

Even delaying benefits by a few years can substantially improve long-term retirement income in some situations.

3. Avoid Taking Large IRA Withdrawals Without Tax Planning

Large withdrawals can create ripple effects:

Higher tax brackets

Increased Medicare premiums

Taxation of Social Security

Reduced Roth conversion opportunities

Example

A retiree withdraws $150,000 from an IRA for home renovations and gifting.

That single decision could:

Push income into higher brackets

Trigger IRMAA surcharges

Increase future tax exposure

Coordinating withdrawals over multiple years may create a better outcome.

4. Avoid Panic Decisions During Market Declines

The first market downturn after retirement can feel emotionally different.

This is often when retirees second-guess their entire plan.

Selling after declines can lock in losses and reduce future recovery potential.

Better Approach

Build a plan before volatility happens:

Maintain cash reserves

Diversify appropriately

Understand withdrawal flexibility

Revisit spending priorities

The goal is not eliminating volatility.

The goal is reducing the need for emotional decisions during volatility.

5. Avoid Treating Retirement Like a Permanent Vacation

Many retirees spend aggressively during the first year before understanding what sustainable retirement spending actually looks like.

This does not mean retirement should be restrictive.

But retirees benefit from observing:

Real monthly expenses

Healthcare changes

Inflation effects

Travel patterns

Long-term lifestyle costs

The first year should help establish sustainable habits and confidence.

A Real-World First-Year Retirement Scenario

John and Susan retire at 64.

They have:

$1.2 million invested

$80,000 in cash

A paid-off home

No pension

Estimated spending needs of $7,000/month after taxes

Their first instinct is:

Claim Social Security immediately

Withdraw additional income entirely from IRAs

Renovate the home

Increase stock exposure after hearing “retirees need growth”

Instead, after planning carefully, they decide to:

Delay Social Security until age 67

Use taxable savings for part of their income

Complete partial Roth conversions annually

Maintain 18 months of cash reserves

Reduce portfolio volatility modestly

Delay large home projects for one year

The Result

They create:

Lower projected lifetime taxes

Higher future guaranteed income

Better Medicare premium management

Greater flexibility during market declines

More confidence about long-term sustainability

None of the decisions were dramatic.

But together, they improved the odds of long-term retirement success.

Questions to Review Before December 31 of Your First Retirement Year

Your first retirement year may create unique tax planning opportunities before year-end.

Questions worth reviewing include:

Should you do a Roth conversion this year?

Are capital gains unusually low this year?

Should you harvest gains before Social Security begins?

Are Medicare IRMAA thresholds an issue?

Are you withholding enough taxes from withdrawals?

Should you rebalance investments?

Are charitable giving strategies appropriate?

Have beneficiaries been updated?

These decisions are often easier and more valuable before future retirement income sources begin.

Common First-Year Retirement Mistakes

Here are several patterns we frequently see:

Spending before building a withdrawal strategy

Claiming Social Security too quickly

Ignoring Roth conversion windows

Taking unnecessary taxable withdrawals

Underestimating healthcare costs

Overreacting to market volatility

Maintaining outdated investment allocations

Forgetting beneficiary reviews

Making emotional investment changes

The first year of retirement often sets the tone for future decision-making.

Final Thoughts

Your first year of retirement is not just about leaving work. It is about transitioning from accumulation to distribution, from saving to creating sustainable income.

The retirees who navigate this transition best are usually not the ones making dramatic moves.

They are the ones slowing down, reviewing tax opportunities carefully, building intentional withdrawal strategies, and avoiding irreversible mistakes too early.

At Greenbush Financial Group, we often find that the most successful retirement transitions come from thoughtful planning rather than reacting emotionally to headlines, market volatility, or uncertainty.

The goal of year one is not perfection.

It is building confidence, flexibility, and a financial foundation that can support the next several decades.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

FAQ

-

What is the biggest financial mistake retirees make in their first year?One of the biggest mistakes is withdrawing money from retirement accounts without a coordinated tax and income strategy. Poor withdrawal sequencing can increase taxes, Medicare premiums, and long-term portfolio stress.

-

Should I take Social Security as soon as I retire?Not necessarily. Many retirees benefit from delaying benefits, especially if they expect longer life expectancy or want to maximize survivor income for a spouse.

-

Should retirees use cash first before withdrawing from investments?In many cases, maintaining a cash reserve for near-term spending can reduce the need to sell investments during market declines. The right approach depends on taxes, market conditions, and withdrawal needs.

-

Why are Roth conversions often valuable early in retirement?Early retirement years may temporarily lower taxable income before RMDs and Social Security begin. This can create opportunities to convert IRA assets at lower tax rates.

-

How much cash should retirees keep during the first year?Many retirees benefit from holding 12-24 months of spending needs in cash or short-term reserves, especially during the retirement transition period.

-

Can retirement withdrawals increase Medicare premiums?Yes. Large IRA withdrawals, Roth conversions, and capital gains can increase income enough to trigger IRMAA surcharges for Medicare Part B and Part D.

-

Should retirees change investments immediately after retiring?Not automatically. However, retirement is a good time to reassess whether your portfolio still aligns with your income needs, risk tolerance, and withdrawal strategy.

-

What should retirees review before the end of their first retirement year?Retirees should review taxes, Roth conversions, Medicare income thresholds, investment allocations, withdrawal strategies, and beneficiary designations before December 31.

Do I Really Need Disability Insurance? What Working Adults Should Understand

Disability insurance helps replace income if illness or injury prevents you from working. This article explains the difference between short-term and long-term disability insurance, how employer-sponsored disability plans work, and why many professionals may have hidden coverage gaps. Learn the difference between own occupation and any occupation coverage, common disability insurance mistakes, and how income protection fits into retirement planning. Greenbush Financial Group outlines the key financial planning considerations working adults should understand before relying solely on employer benefits.

Many people insure their home, car, and life but overlook the income that supports all of those expenses. Disability insurance is designed to replace part of your income if illness or injury prevents you from working. Understanding the different types of disability coverage, how employer plans work, and where financial gaps may exist can help protect long-term financial stability. At Greenbush Financial Group, we often find that income protection becomes more important as careers, family responsibilities, and retirement savings grow.

Most People Protect Their Property Before Protecting Their Income

Many households insure:

Their home

Their car

Their health

Their life

But far fewer spend time thinking about what would happen if they suddenly could not work for months or years.

For most working adults, future earning power is one of their largest financial assets.

That income supports:

Mortgage payments

Retirement savings

Healthcare costs

Family expenses

College savings

Everyday living expenses

Disability insurance exists to help protect that income if illness or injury interrupts the ability to work.

The goal is not expecting the worst.

The goal is understanding how financial stability would be affected if paychecks unexpectedly stopped.

What Is Disability Insurance?

Disability insurance helps replace a portion of income if a person becomes unable to work because of:

Illness

Injury

Medical conditions

Certain disabilities

Coverage typically pays monthly benefits for a defined period depending on the policy structure.

Unlike health insurance, disability insurance does not primarily cover medical bills.

It helps replace lost income.

Why Disability Insurance Matters More Than Many People Realize

Many people associate disability with catastrophic accidents.

But long-term disabilities are often caused by:

Cancer

Back injuries

Chronic illness

Neurological disorders

Mental health conditions

Heart disease

Surgery recovery complications

In many cases, disabilities are medical events rather than dramatic accidents.

The financial impact can become significant because expenses usually continue even when income slows or stops.

The Two Main Types of Disability Insurance

Short-Term Disability Insurance

Short-term disability coverage typically provides income replacement for temporary situations.

Coverage periods often range from:

A few weeks

To several months

Common Uses

Short-term disability may help during:

Surgery recovery

Pregnancy and childbirth

Temporary illnesses

Injuries requiring recovery time

Benefits often begin quickly after a waiting period of:

A few days

Or a couple of weeks

Long-Term Disability Insurance

Long-term disability insurance is designed for more serious or extended work interruptions.

Coverage may last:

Several years

Until retirement age

Or for a specific policy duration

Long-term disability becomes especially important for protecting:

Retirement savings

Family cash flow

Long-term financial plans

Because prolonged income loss can significantly affect future financial security.

Employer Disability Insurance vs. Individual Coverage

Many employees already have some disability insurance through work.

But there are important details people often overlook.

Employer Coverage May:

Replace only part of income

Have benefit caps

End if employment changes

Be taxable

Offer limited portability

Some plans replace:

50%–60% of salary

Which may sound reasonable until households compare it against actual expenses.

Example

Suppose someone earns:

$140,000 annually

Employer disability coverage replaces:

60% of salary

But benefits are taxable.

Actual take-home replacement income may be significantly lower than expected while expenses remain largely unchanged.

Individual Disability Insurance

Individual policies are purchased privately and may offer:

More customized coverage

Portable benefits

Stronger definitions of disability

Higher income protection flexibility

Professionals with specialized careers often explore individual policies because their income may be difficult to replace.

Understanding “Own Occupation” vs. “Any Occupation”

This is one of the most important disability insurance concepts.

Own Occupation Coverage

This coverage generally pays benefits if you cannot perform the duties of your specific profession.

Example:

A surgeon unable to operate because of hand injuries may still technically be able to work elsewhere, but not within their specialized occupation.

Own occupation policies may still provide benefits.

Any Occupation Coverage

This standard is stricter.

Benefits may only apply if the person cannot reasonably work in almost any occupation.

This distinction can dramatically affect how coverage functions during a claim.

How Much Disability Coverage Do People Typically Need?

The answer depends on factors such as:

Income level

Savings

Family obligations

Debt

Career specialization

Retirement readiness

Questions worth considering include:

How long could savings support expenses?

Would a spouse’s income be enough?

Would retirement contributions stop?

Could mortgage payments continue comfortably?

Disability insurance is often less about replacing every dollar and more about protecting financial stability during a difficult period.

Who Often Benefits Most From Disability Insurance?

Coverage tends to become more important when people have:

High incomes

Dependents

Mortgage obligations

Specialized careers

Limited liquid savings

Long working years ahead

Especially for younger professionals, future earning power may greatly exceed current investment assets.

People Who May Need Less Disability Coverage

Not everyone needs the same level of protection.

Some people may need less coverage if they have:

Significant investment income

Pension income

Substantial liquid assets

Minimal debt

Financial independence already achieved

The key is evaluating how dependent the household remains on earned income.

A Real-World Example

Mark is 42 years old and earns:

$180,000 annually

He and his spouse have:

Young children

A mortgage

Ongoing retirement savings goals

Initially, Mark assumes his employer coverage is sufficient.

But after reviewing the details, he discovers:

Benefits are taxable

Coverage replaces less income than expected

Bonuses are excluded

Coverage would not fully support household expenses

He eventually supplements employer coverage with an individual long-term disability policy.

The decision was not based on fear.

It was based on recognizing how dependent the household remained on his future earnings.

Common Disability Insurance Mistakes

1. Assuming Employer Coverage Is Enough

Many people never review:

Benefit percentages

Tax treatment

Coverage limits

Waiting periods

2. Waiting Until Health Changes Occur

Coverage availability and pricing may change significantly after medical diagnoses.

3. Focusing Only on Accidents

Many disabilities stem from illness, not catastrophic injuries.

4. Ignoring Household Cash Flow Needs

Disability planning should evaluate:

Fixed expenses

Debt obligations

Family support needs

Long-term savings goals

5. Overinsuring or Underinsuring

Coverage should fit actual financial exposure and long-term needs.

Questions to Ask Before Buying Disability Insurance

Important questions include:

How much income would actually need replacement?

What coverage already exists through work?

Are benefits taxable?

How long could emergency savings last?

Does the policy use own occupation or any occupation definitions?

How long do benefits last?

What waiting period applies?

Would my spouse or family remain financially stable?

The answers often reveal whether meaningful protection gaps exist.

The Retirement Planning Connection

Disability insurance is often overlooked in retirement planning conversations.

But a major disability during working years can affect:

Retirement savings

Social Security timing

Investment growth

Debt repayment

College funding

Long-term financial independence

Protecting income during working years may help protect retirement goals later.

Final Thoughts

Disability insurance is not always the most exciting financial topic.

But for many working households, protecting future income may be just as important as protecting investments or property.

At Greenbush Financial Group, we often encourage clients to evaluate disability coverage not from a fear perspective, but from a financial planning perspective.

The question is not:

“What is the worst-case scenario?”

The better question is:

“How would the household function financially if earned income unexpectedly stopped for an extended period?”

For some people, the answer may reveal meaningful protection gaps.

For others, existing assets and flexibility may already provide enough security.

The key is understanding the tradeoffs before a health event forces the conversation unexpectedly.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

FAQ

-

What is disability insurance?Disability insurance helps replace part of your income if illness or injury prevents you from working.

-

What is the difference between short-term and long-term disability insurance?Short-term disability usually covers temporary situations lasting weeks or months, while long-term disability covers extended work interruptions that may last years.

-

Is disability insurance worth it?For many working adults, especially those dependent on earned income, disability insurance may help protect financial stability and long-term goals.

-

Does employer disability insurance provide enough coverage?Sometimes, but many employer plans replace only part of income and may include taxable benefits or coverage limits.

-

What does "own occupation" disability insurance mean?Own occupation coverage generally pays benefits if you cannot perform your specific profession, even if you could work elsewhere.

-

Are disability insurance benefits taxable?It depends on how premiums are paid. Employer-paid benefits are often taxable, while individually funded policies may provide tax-free benefits.

-

Who benefits most from disability insurance?High earners, professionals, families with dependents, and households heavily dependent on employment income often benefit most from coverage.

-

What is the biggest mistake people make with disability insurance?One of the biggest mistakes is assuming employer coverage fully protects household income without reviewing the actual policy details.

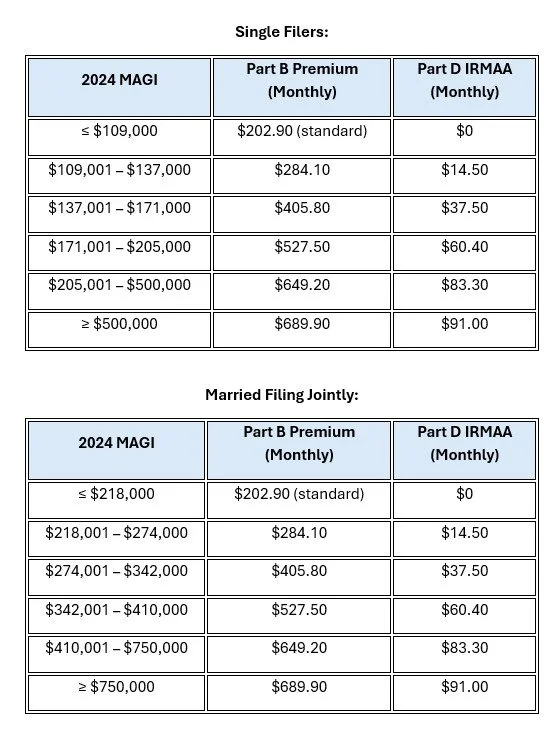

2026 Medicare IRMAA Brackets: What Triggers Higher Premiums and How to Avoid

Medicare IRMAA increases Part B and Part D premiums when your income exceeds specific thresholds based on your MAGI from two years prior. In 2026, managing income through strategies like Roth conversions, withdrawal timing, and tax planning can help reduce or avoid these surcharges. Even small income increases can trigger higher premiums, making proactive planning essential. Greenbush Financial Group helps retirees minimize IRMAA and control long-term healthcare costs.

Medicare IRMAA (Income-Related Monthly Adjustment Amount) is a surcharge added to Medicare Part B and Part D premiums when your income exceeds certain thresholds. These surcharges are based on your Modified Adjusted Gross Income (MAGI) from two years prior. At Greenbush Financial Group, our analysis shows that proactive tax and withdrawal planning can help retirees avoid or minimize IRMAA and significantly reduce long-term healthcare costs.

What Is Medicare IRMAA and How Does It Work?

IRMAA is an additional premium Medicare beneficiaries pay if their income exceeds specific limits.

Key Facts

Applies to Medicare Part B and Part D

Based on income from two years prior

Uses Modified Adjusted Gross Income (MAGI)

Adjusted annually for inflation

Example

Your 2026 Medicare premiums are based on your 2024 income.

This lag creates planning opportunities, especially in early retirement years.

2026 IRMAA Income Limits and Surcharge Brackets

IRMAA is triggered when your income crosses certain thresholds.

2026 Estimated IRMAA Thresholds

At Greenbush Financial Group, we emphasize that even $1 over a threshold can trigger a significantly higher premium.

What Counts as Income for IRMAA (MAGI)?

IRMAA is based on Modified Adjusted Gross Income, which includes more than just wages.

Included Income Sources

IRA and 401(k) withdrawals

Capital gains from investments

Dividends and interest

Rental income

Social Security (partially taxable portion)

Roth conversions

Important Note

Tax-free municipal bond interest is also included in MAGI for IRMAA purposes.

How Much Are IRMAA Surcharges?

IRMAA increases both Part B and Part D premiums.

Example Impact

Standard Part B premium (baseline)

IRMAA can increase premiums by hundreds of dollars per month per person

Part D surcharges are smaller but still meaningful

Key Insight

Over a 10–20 year retirement, IRMAA can add up to tens of thousands of dollars in additional healthcare costs if not managed properly.

Planning Strategies to Reduce or Avoid IRMAA

Strategic income planning is the most effective way to manage IRMAA.

1. Manage Your Taxable Income Each Year

Stay below key IRMAA thresholds when possible

Avoid large one-time income spikes

2. Use Roth Conversions Strategically

Convert funds in lower-income years before Medicare

Reduce future taxable income and RMDs

3. Time Large Withdrawals Carefully

Spread income over multiple years

Avoid triggering IRMAA in a single year

4. Leverage Roth Accounts

Roth withdrawals do not increase MAGI

Provides tax-free income flexibility

5. Consider Capital Gains Timing

Harvest gains in lower-income years

Offset gains with losses when possible

At Greenbush Financial Group, we often build multi-year tax projections to help clients stay below IRMAA thresholds.

IRMAA Planning Before and After Retirement

Before Retirement (Ages 55–63)

Ideal window for Roth conversions

Lower income years create planning opportunities

Reduce future IRMAA exposure

Early Retirement (Before Medicare)

Control income levels carefully

Balance withdrawals across accounts

After Age 65

Monitor RMDs and income levels

Use Roth withdrawals to manage thresholds

Plan ahead for future income spikes

What Happens If Your Income Drops?

You may be able to appeal IRMAA if your income has decreased due to certain life events.

Qualifying Life-Changing Events

Retirement

Marriage or divorce

Death of a spouse

Loss of income-producing property

You can file an appeal with Social Security to request a lower premium.

Common IRMAA Mistakes to Avoid

Ignoring IRMAA when doing Roth conversions

Taking large IRA withdrawals in a single year

Not planning for RMDs

Overlooking capital gains impact

Assuming Medicare premiums are fixed

At Greenbush Financial Group, we often see that IRMAA surprises retirees who focus only on taxes without considering healthcare costs.

Final Thoughts

IRMAA is one of the most overlooked retirement expenses, yet it can significantly increase your Medicare costs. The key is not just minimizing taxes in a single year but managing income over time to avoid crossing key thresholds.

At Greenbush Financial Group, our analysis shows that proactive planning around withdrawals, Roth conversions, and income timing can help reduce IRMAA and improve overall retirement outcomes.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

Frequently Asked Questions

-

What does IRMAA stand for?Income-Related Monthly Adjustment Amount, a surcharge on Medicare premiums based on income.

-

What income is used to calculate IRMAA?Modified Adjusted Gross Income (MAGI) from two years prior.

-

Can Roth withdrawals trigger IRMAA?No, qualified Roth withdrawals do not increase MAGI.

-

Can IRMAA be appealed?Yes, if you have a qualifying life-changing event such as retirement or loss of income.

-

How can I avoid IRMAA surcharges?By managing taxable income, using Roth strategies, and avoiding large income spikes.

2026 Roth IRA Conversions Explained: Smart Timing and Costly Mistakes

Roth IRA conversions allow retirees to move pre-tax assets into tax-free accounts by paying taxes now, but timing is critical. The most effective strategies involve spreading conversions over multiple years, managing tax brackets, and coordinating with Social Security and IRMAA thresholds. Poorly timed conversions can increase taxes and Medicare costs. Greenbush Financial Group helps retirees use Roth conversions to reduce lifetime taxes and improve income flexibility.

Roth conversions can be one of the most powerful tax planning tools in retirement, but they are not always beneficial. A Roth conversion involves moving money from a pre-tax account into a Roth account and paying taxes now to avoid taxes later. At Greenbush Financial Group, our analysis shows that Roth conversions are most effective when done strategically across multiple years, not as a one-time decision.

What Is a Roth Conversion and How Does It Work?

A Roth conversion moves funds from a Traditional IRA or 401(k) into a Roth IRA or 401(k).

Key Mechanics

Converted amount is taxed as ordinary income

No early withdrawal penalty if done correctly

Future growth and withdrawals are tax-free

No Required Minimum Distributions (RMDs) for Roth IRAs

Example

Convert $50,000 from an IRA to a Roth IRA

Pay taxes on $50,000 this year

Future withdrawals are tax-free

At Greenbush Financial Group, we view Roth conversions as a way to “prepay taxes” at potentially lower rates.

When Roth Conversions Make Sense

There are specific scenarios where Roth conversions can significantly improve long-term outcomes.

1. Low-Income Years in Early Retirement

The period between retirement and starting Social Security or RMDs is often ideal.

Lower taxable income

Opportunity to fill lower tax brackets

Reduce future tax burden

2. Before Required Minimum Distributions (RMDs)**

RMDs can force higher taxable income later in retirement.

Converting early reduces future RMDs

Helps avoid higher tax brackets in your 70s

3. Expecting Higher Future Tax Rates

If you believe your future tax rate will be higher:

Paying taxes now may be beneficial

Locks in current tax rates

4. Large Pre-Tax Account Balances

High IRA or 401(k) balances can create tax challenges later.

Large RMDs

Increased IRMAA surcharges

Higher Social Security taxation

5. Leaving Assets to Heirs

Roth accounts can be more tax-efficient for beneficiaries.

Tax-free withdrawals for heirs

No lifetime RMDs for original owner

At Greenbush Financial Group, Roth conversions are often used as part of a broader estate and tax planning strategy.

When Roth Conversions May Not Make Sense

Roth conversions are not always the right move.

1. Already in a High Tax Bracket

If converting pushes you into a higher bracket:

You may pay more tax than necessary

Reduces the benefit of the conversion

2. Short Time Horizon

If you expect to use the money soon:

Limited time for tax-free growth

Less benefit from conversion

3. Paying Taxes From the Conversion Itself

Using IRA funds to pay taxes reduces the amount converted.

Decreases long-term growth potential

Less efficient overall

4. Expecting Lower Future Tax Rates

If your income will decrease later:

You may pay more tax now than necessary

5. Impact on Medicare and Social Security

Conversions increase taxable income.

May trigger IRMAA surcharges

Can increase taxation of Social Security

At Greenbush Financial Group, we often see Roth conversions backfire when these factors are not considered.

The “Tax Bracket Filling” Strategy

One of the most effective ways to approach Roth conversions is by filling up lower tax brackets.

How It Works

Identify your current tax bracket

Convert just enough to stay within that bracket

Avoid jumping into higher brackets

Example

Top of 12% bracket = target income level

Convert enough to reach that limit

Stop before entering the 22% bracket

This strategy spreads conversions over multiple years, reducing overall tax impact.

Roth Conversions and IRMAA Considerations

Roth conversions increase your income for that year, which can affect Medicare premiums.

Key Impact

Higher income can trigger IRMAA surcharges

IRMAA is based on income from two years prior

Planning Tip

Balance Roth conversions with IRMAA thresholds to avoid unnecessary premium increases.

A Multi-Year Roth Conversion Strategy Example

Scenario

Age 62, recently retired

$800,000 in IRA

Low income before Social Security

Strategy

Convert $40,000–$60,000 annually

Stay within a lower tax bracket

Delay Social Security

Outcome

Reduced future RMDs

Lower lifetime taxes

Increased tax-free income later

At Greenbush Financial Group, this type of phased approach is often more effective than a single large conversion.

Common Roth Conversion Mistakes

Converting too much in one year

Ignoring tax bracket thresholds

Overlooking IRMAA impacts

Not coordinating with Social Security timing

Failing to plan conversions over multiple years

Final Thoughts

Roth conversions can be a powerful tool, but only when used strategically. The goal is not simply to convert assets, but to reduce lifetime taxes and create more flexibility in retirement income.

At Greenbush Financial Group, our analysis shows that the most successful strategies involve careful timing, tax bracket management, and long-term planning.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

-

Is it a bad idea to retire in a down market?Not necessarily, but it increases sequence of returns risk and requires careful planning.

-

How much cash and short-term fixed income should I have in retirement?Typically 1 to 3 years of living expenses.

-

Should I stop withdrawals during a downturn?Not entirely, but reducing withdrawals can improve long-term outcomes.

-

Can a market downturn ruin my retirement plan?It can if not managed properly, especially in the early years of retirement.

-

What is the best strategy during a market downturn?Maintain a cash reserve, adjust withdrawals, stay invested, and focus on long-term planning.

2026 Bear Market Retirement Planning: How to Avoid Running Out of Money

Retiring in a down market increases sequence of returns risk, which can reduce how long your savings last. The most effective strategies include maintaining a cash reserve, using a bucket income approach, reducing withdrawals, and delaying Social Security. Tax planning and portfolio rebalancing can also improve long-term outcomes. Greenbush Financial Group emphasizes flexibility and disciplined decision-making to help retirees protect income during market volatility.

Retiring during a market downturn can significantly impact how long your retirement savings last due to sequence of returns risk. When withdrawals begin during a declining market, losses can compound and reduce long-term portfolio sustainability. At Greenbush Financial Group, our analysis shows that implementing the right withdrawal, allocation, and income strategies can help protect your retirement plan even in volatile markets.

Why Retiring in a Down Market Is Risky

The primary concern is not just market losses, but when those losses occur.

Sequence of Returns Risk Explained

Sequence risk refers to the timing of market returns relative to your withdrawals.

Negative returns early in retirement can permanently reduce your portfolio

Withdrawals during downturns lock in losses

Recovery becomes more difficult over time

Example

Two retirees with identical portfolios and average returns can have very different outcomes depending on whether market losses occur early or later in retirement.

At Greenbush Financial Group, this is one of the most important risks we plan for when building retirement income strategies.

Strategy 1: Build a Cash Reserve Before Retirement

One of the most effective ways to protect your portfolio is to avoid selling investments during a downturn.

Recommended Approach

Maintain 1–3 years of living expenses in cash or short-term investments

Use this reserve instead of withdrawing from stocks during market declines

Why It Works

Gives your portfolio time to recover

Reduces the need to sell assets at depressed prices

Provides psychological comfort during volatility

Strategy 2: Use a Bucket Strategy for Income

Segmenting your portfolio into different “buckets” can help manage risk.

Example Structure

Short-Term Bucket (0–3 years)

Cash, money markets, short-term bonds

Used for immediate income needs

Mid-Term Bucket (3–10 years)

Bonds, conservative investments

Provides stability and income

Long-Term Bucket (10+ years)

Stocks and growth assets

Designed to outpace inflation

At Greenbush Financial Group, we often use this framework to align investments with time horizons and reduce sequence risk.

Strategy 3: Reduce Withdrawals During Down Markets

Flexibility is critical when markets are volatile.

Key Adjustments

Temporarily reduce discretionary spending

Delay large purchases

Pause inflation increases on withdrawals

Example

Instead of withdrawing $60,000 during a downturn, reducing withdrawals to $50,000 can significantly improve long-term sustainability.

Strategy 4: Delay Social Security If Possible

Social Security provides a guaranteed, inflation-adjusted income stream.

Why Delaying Helps

Increases your monthly benefit

Reduces reliance on portfolio withdrawals early

Provides more stable income later in retirement

Planning Insight

Using portfolio assets early while delaying Social Security can sometimes improve long-term outcomes.

Strategy 5: Rebalance and Stay Invested

Market downturns can create opportunities to rebalance your portfolio.

Key Principles

Avoid panic selling

Rebalance to maintain target allocation

Take advantage of lower asset prices

At Greenbush Financial Group, maintaining discipline during downturns is often the difference between success and failure in retirement planning.

Strategy 6: Consider Part-Time Income or Flexible Retirement

Even a small amount of income can reduce pressure on your portfolio.

Benefits

Reduces withdrawal rate

Allows more time for investments to recover

Provides flexibility in spending

Example

Earning $10,000–$20,000 per year can significantly extend portfolio longevity.

Strategy 7: Tax Planning During Market Downturns

Down markets can create tax planning opportunities.

Strategies

Harvest capital losses to offset gains

Convert IRA funds to Roth at lower market values

Manage taxable income to stay in lower tax brackets

At Greenbush Financial Group, we often see that downturns can be an ideal time to implement tax-efficient strategies.

Common Mistakes to Avoid

Selling investments out of fear

Maintaining rigid withdrawal strategies

Ignoring tax planning opportunities

Failing to adjust spending

Overreacting to short-term market movements

A Real-World Scenario

Scenario

Retiree with $1,000,000 portfolio

Market declines 20% in first year

Withdraws $50,000 annually

Without Adjustments

Portfolio drops significantly

Recovery becomes difficult

With Strategic Adjustments

Uses cash reserve instead of selling stocks

Reduces withdrawals temporarily

Rebalances portfolio

Delays Social Security

Result

Improved long-term sustainability

Reduced sequence risk impact

Final Thoughts

Retiring during a down market does not mean your plan will fail, but it usually does require adjustments. The key is managing withdrawals, maintaining flexibility, and staying disciplined with your investment strategy.

At Greenbush Financial Group, our analysis shows that retirees who proactively adapt their strategy during downturns are far more likely to preserve their wealth and maintain sustainable income throughout retirement.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

-

Is it a bad idea to retire in a down market?Not necessarily, but it increases sequence of returns risk and requires careful planning.

-

How much cash and short-term fixed income should I have in retirement?Typically 1 to 3 years of living expenses.

-

Should I stop withdrawals during a downturn?Not entirely, but reducing withdrawals can improve long-term outcomes.

-

Can a market downturn ruin my retirement plan?It can if not managed properly, especially in the early years of retirement.

-

What is the best strategy during a market downturn?Maintain a cash reserve, adjust withdrawals, stay invested, and focus on long-term planning.

Claiming Social Security Early or Late: Which Age Is Right for You?