A Financial Checklist for Surviving Spouses

Losing a spouse is overwhelming, and financial matters can add to the stress. Greenbush Financial Group provides a gentle, step-by-step checklist to help surviving spouses address immediate needs, manage estate matters, and plan for the future with confidence.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Losing a spouse is one of life’s most difficult experiences. During this time of grief, handling financial matters can feel overwhelming. It’s important to remember that you don’t need to do everything at once. In fact, we often advise clients not to make any major financial decisions for 6 to 12 months after the loss of a loved one, if it can be avoided.

This guide is designed to provide a gentle checklist of financial steps to consider, along with reassurance that you don’t need to navigate this alone.

Step 1: Take Care of Immediate Needs

In the first weeks, focus only on what must be handled right away:

Ensure bills and accounts are being paid—utilities, mortgage, and insurance premiums—so nothing important lapses. If additional cash is needed to cover these expenses or funeral costs, you may want to contact your investment advisor to request a distribution from your brokerage or retirement account.

Gather key documents such as the death certificate, Social Security card, and marriage certificate. You will need several certified copies of the death certificate.

Notify Social Security to stop benefits if your spouse was receiving them, and inquire about survivor benefits.

Contact your spouse’s employer (if applicable) to ask about any final pay, life insurance, or retirement benefits.

Inventory assets and debts: Create a list of accounts, loans, credit cards, and other financial items.

At this stage, just focus on stabilization. Bigger decisions can wait.

Step 2: Meet With Your Estate Attorney

An estate attorney can be one of the most important resources for a surviving spouse. They will help guide you through the legal aspects of settling your spouse’s estate and make sure everything is handled properly. Some of the areas they may assist with include:

Reviewing your spouse’s will or trust to ensure assets are distributed according to their wishes.

Probate guidance if the estate needs to go through the court process.

Updating property titles and deeds (such as the home, vehicles, or other jointly owned assets).

Retitling accounts that were in your spouse’s name alone.

Confirming beneficiary designations on retirement accounts, life insurance, and other policies.

Handling debts and obligations—making sure outstanding bills or loans are addressed properly.

Advising on estate tax issues and helping file any required estate or inheritance tax returns.

Updating your own estate plan to reflect changes in beneficiaries, powers of attorney, and trusts.

Meeting with an estate attorney early ensures that the legal and financial transition is handled with care, giving you peace of mind during a difficult time.

Step 3: Understand Insurance and Benefits

Life insurance: If your spouse had life insurance, begin the claims process. Take your time deciding how to use any proceeds.

Employer benefits: You may be eligible for continued health coverage, pension payments, or survivor retirement benefits.

Government benefits: Social Security survivor benefits may be available, depending on age and circumstances.

Step 4: Review Bank and Investment Accounts

After the first three steps, begin to look at household finances more closely.

Confirm joint accounts: In many cases, joint bank accounts automatically transfer to the surviving spouse.

Update beneficiary designations: Retirement accounts, life insurance, and transfer-on-death accounts should be reviewed.

Check for automatic payments: Make sure you know which accounts are connected to bills or subscriptions.

Begin retitling accounts per the direction of your estate attorney or investment advisor.

This helps establish a clear picture of where things stand.

Step 5: Avoid Major Financial Decisions for 6–12 Months

Grief can cloud judgment. If possible, hold off on large changes such as:

Selling the family home

Making major investment decisions

Gifting or lending large sums of money

Instead, focus on maintaining stability and keeping everything in order until you feel emotionally and financially ready.

Step 6: Seek Guidance from Financial Professionals

You don’t need to carry this burden alone. Financial professionals can provide both guidance and peace of mind:

Accountants can help navigate tax considerations, including filing final returns for your spouse.

Financial planners can help you prioritize needs and create a roadmap for the months and years ahead.

Investment advisors can review your portfolio and suggest adjustments to fit your new circumstances.

Having trusted professionals at your side means you don’t have to make every decision yourself. They can help simplify the process and give you confidence that nothing is being overlooked.

Step 7: Begin Planning for the Future—When You’re Ready

When you feel ready, start thinking about the long-term picture:

Update your own will, trust, and estate plan.

Revisit beneficiaries on accounts and insurance policies.

Adjust your budget and income sources for your new household situation.

Consider whether your investment and retirement plans need rebalancing.

Take these steps one at a time, at a pace that feels manageable.

Final Thoughts

The loss of a spouse is deeply personal, and the financial responsibilities that follow can feel heavy. Remember: you do not need to have all the answers right away, and you don’t need to do this alone.

By leaning on a checklist like this—and enlisting the support of accountants, planners, and advisors—you can move forward step by step. Over time, clarity will return, and you’ll feel more confident about the financial decisions that lie ahead.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

What financial steps should I take immediately after losing a spouse?

Focus first on essential needs—keeping bills current, gathering key documents, and notifying Social Security and your spouse’s employer. Avoid making major financial changes right away; the priority is maintaining stability during the initial weeks.

Why is meeting with an estate attorney so important after a spouse’s death?

An estate attorney helps ensure your spouse’s will, trusts, and beneficiary designations are properly executed. They can guide you through probate, retitle assets, settle debts, and help update your own estate plan to reflect your new situation.

What types of benefits should a surviving spouse review?

Survivors should check for life insurance proceeds, employer benefits such as pensions or continued health coverage, and Social Security survivor benefits. Each of these may provide valuable financial support during the transition.

When should I start making major financial decisions after a loss?

It’s best to wait six to twelve months before making large financial moves, such as selling property or changing investments. This allows time for emotions to settle and for you to make decisions with clarity.

How can financial professionals help after the loss of a spouse?

Accountants can manage tax filings and estate issues, while financial planners and investment advisors can help organize accounts, adjust your financial plan, and guide long-term decisions with care and objectivity.

What long-term financial updates should I make as a surviving spouse?

When ready, update your own will, trust, and beneficiary designations. Review your budget, income sources, and investment strategy to ensure they align with your new circumstances and future goals.

Advantages of Using A Bond Ladder Instead of ETFs or Mutual Funds

Bond ladders can provide investors with predictable income, interest rate protection, and more control compared to bond ETFs or mutual funds. Greenbush Financial Group breaks down how they work, the different ladder strategies, and why some investors prefer this approach.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

When it comes to investing, one of the biggest challenges is dealing with interest rate uncertainty. Rates go up, rates go down, and bond prices fluctuate with those changes. For investors who want predictable income and a way to smooth out the risks of rising and falling interest rates, a bond ladder can be a powerful strategy.

In this article, we’ll walk through:

What a bond ladder is and how it works

How a bond ladder helps hedge against interest rate fluctuations

The different types of bond ladders (equal-weighted, barbell, middle-loaded)

Why some investors prefer an individual bond ladder over bond mutual funds or ETFs

What Is a Bond Ladder?

A bond ladder is a portfolio of individual bonds with staggered maturity dates. For example, you might buy bonds maturing in 1 year, 2 years, 3 years, 4 years, and 5 years. When the 1-year bond matures, you reinvest the proceeds into a new 5-year bond, keeping the “ladder” in place.

This structure offers two key benefits:

Hedging Interest Rate Risk: Since a portion of your ladder matures every year (or at regular intervals), you always have an opportunity to reinvest at the prevailing interest rate—whether rates go up or down.

Consistent Income and Liquidity: The maturing bonds provide cash flow that can be reinvested or used for spending needs.

In short, a bond ladder helps smooth out the effects of interest rate fluctuations while still generating steady income.

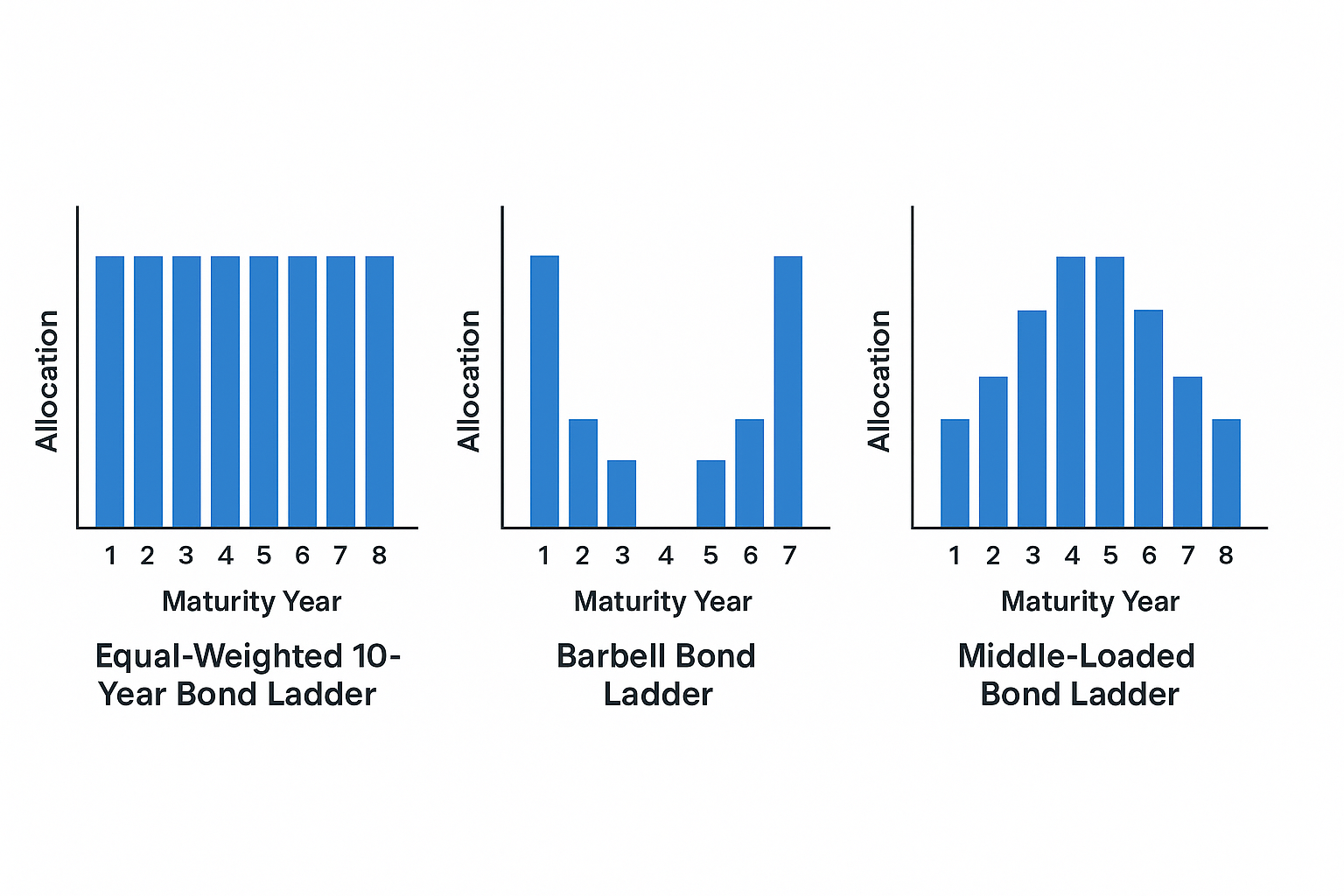

Types of Bond Ladders and How They Work

There isn’t just one way to build a bond ladder. The structure you choose depends on your investment goals, risk tolerance, and views on interest rates. Here are three common approaches:

1. Equal-Weighted Bond Ladder

How it works: Bonds are spread evenly across maturity dates (e.g., equal amounts in 1, 2, 3, 4, and 5-year maturities).

Why use it: This is the most straightforward approach. It balances risk and return by spreading exposure across time horizons, making it a good fit for investors who want predictability.

2. Barbell Strategy

How it works: Bonds are concentrated at the short and long ends of the maturity spectrum, with little or nothing in the middle. For example, you might own 1-year and 10-year bonds, but nothing in between.

Why use it: Short-term bonds provide liquidity and flexibility, while long-term bonds lock in higher yields. This strategy can be appealing when you expect interest rates to change significantly in the future.

3. Middle-Loaded Ladder

How it works: Bonds are concentrated in intermediate maturities (e.g., 3–7 years).

Why use it: Provides a balance between short-term reinvestment risk and long-term interest rate exposure. This can be attractive if you think the current yield curve makes mid-range maturities the “sweet spot” for returns.

Bond ladders can also vary by duration. Some investors create 5-year ladders, 10-year ladders, or 20-year ladders.

Why Build a Bond Ladder Instead of Using a Mutual Fund or ETF?

You might wonder: why not just buy a bond fund and let the professionals handle it? There are several reasons why individual investors prefer building their own bond ladders:

Predictable Cash Flow: With a ladder, you know exactly when each bond will mature and what it will pay. Bond funds and ETFs fluctuate daily, and there are no set maturity dates.

Control Over Holdings: You decide the maturity schedule, the credit quality, and the exact bonds in your ladder. In a fund, you’re subject to the manager’s decisions.

Reduced Interest Rate Risk: In a bond ladder, if you hold bonds to maturity, you get your principal back regardless of market fluctuations. Bond funds never truly “mature,” so you’re always exposed to price swings.

Potentially Lower Costs: By buying individual bonds and holding them, you avoid ongoing expense ratios charged by mutual funds and ETFs.

In short, a bond ladder offers clarity, predictability, and control that pooled investment vehicles can’t always match.

Why You Need Significant Capital for a Bond Ladder

While bond ladders offer many advantages, they aren’t practical for every investor. Building a well-diversified ladder requires a substantial amount of money for a few reasons:

Minimum Purchase Amounts: Many individual bonds trade in $1,000 or $5,000 increments. To build a ladder with multiple rungs across different maturities, you need enough capital to meet those minimums. When investing in short-term U.S. treasuries, sometimes the purchase minimum is $250,000.

Diversification Needs: A proper ladder spreads risk across multiple issuers and maturities. Doing this with small amounts of money is difficult, leaving you concentrated in just a few bonds.

Transaction Costs: Buying and selling individual bonds often involves markups or commissions, which can eat into returns if the investment amount is too small.

Income Needs: If you’re using the ladder to generate income, small investments may not produce meaningful cash flow compared to what’s achievable with funds or ETFs.

For these reasons, investors with smaller portfolios often turn to bond mutual funds or ETFs. These vehicles pool money from many investors, allowing even modest contributions to achieve diversification, professional management, and steady income without the large upfront commitment required by a ladder

Final Thoughts

A bond ladder can be an excellent strategy for investors looking to hedge interest rate risk, generate predictable income, and maintain flexibility. Whether you choose an equal-weighted ladder for balance, a barbell strategy for flexibility and yield, or a middle-loaded approach to target the sweet spot of the curve, the right structure depends on your unique goals.

And while bond mutual funds and ETFs may be convenient, an individual bond ladder provides unmatched control, transparency, and reliability.

If you’re considering adding a bond ladder to your portfolio, the key is aligning it with your financial objectives, income needs, and risk tolerance. Done correctly, it’s a time-tested way to bring stability and consistency to your investment plan.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

What is a bond ladder and how does it work?

A bond ladder is a portfolio of individual bonds with staggered maturity dates, such as 1-, 2-, 3-, 4-, and 5-year terms. As each bond matures, the proceeds are reinvested into a new long-term bond, creating a cycle that provides steady income and helps manage interest rate risk.

How does a bond ladder help protect against interest rate changes?

Because bonds mature at regular intervals, you continually reinvest at current market rates. This means when interest rates rise, maturing bonds can be rolled into higher-yielding ones; when rates fall, the longer-term bonds in the ladder continue to earn higher fixed rates.

What are the different types of bond ladders?

Common structures include equal-weighted ladders (evenly spread maturities), barbell strategies (short- and long-term maturities), and middle-loaded ladders (focused on intermediate terms). Each structure balances risk, return, and flexibility differently.

Why might investors choose a bond ladder over a bond mutual fund or ETF?

An individual bond ladder offers predictable maturity dates, control over holdings, and stable cash flow if bonds are held to maturity. In contrast, bond funds and ETFs fluctuate in value and have no set maturity, which can expose investors to ongoing price volatility.

Who is a bond ladder best suited for?

Bond ladders typically work best for investors with larger portfolios who want predictable income and can meet minimum bond purchase requirements. Smaller investors may prefer bond funds or ETFs for diversification and lower entry costs. We advise consulting with your personal investment advisor.

What are the key advantages of using a bond ladder in a portfolio?

A bond ladder provides consistent income, reduces interest rate risk, and enhances liquidity through regular maturities. It also allows investors to match cash flow needs with future expenses while maintaining control over credit quality and investment duration.

5 Must-Read Financial Books to Build Wealth and Success at Any Stage of Life

Looking to build wealth and sharpen your money skills? Greenbush Financial Group highlights 5 must-read financial books that cover debt, investing, business strategy, and long-term success. Perfect for every stage of life.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Knowledge is power—especially when it comes to money. The earlier you learn the fundamentals of personal finance and business, the faster you can avoid mistakes and build wealth compared to your peers. But whether you’re just starting out in your career, navigating mid-life financial challenges, or planning for retirement, the right financial knowledge can create opportunities and help you achieve greater freedom.

As the Managing Partner of Greenbush Financial Group, I often recommend books as a way to jump-start that education. The right book can provide not only financial strategies but also the mindset shifts needed to succeed both personally and professionally. Below are five must-read books that cover everything from managing debt to investing to starting a business:

The Total Money Makeover by Dave Ramsey

How to Win Friends and Influence People by Dale Carnegie

Rich Dad Poor Dad by Robert Kiyosaki

Blue Ocean Strategy by W. Chan Kim and Renée Mauborgne

One Up on Wall Street by Peter Lynch

1. The Total Money Makeover by Dave Ramsey

For individuals who find themselves weighed down by student loans, credit card balances, or car payments, this book is the perfect starting point. Ramsey lays out a proven system—his famous “baby steps”—to help readers eliminate debt, build an emergency fund, and begin saving for the future. His approach is straightforward, no-nonsense, and centered on living a debt-free lifestyle.

Key Lessons:

Start with a written budget and tell every dollar where to go.

Attack debt with the “debt snowball” method—paying off the smallest balances first.

Build an emergency fund to protect against unexpected expenses.

Avoid credit cards and debt as a lifestyle—cash is freedom.

Live below your means to create margin for saving and investing.

2. How to Win Friends and Influence People by Dale Carnegie

Originally published in 1936, this timeless classic focuses on building strong relationships—a skill just as valuable in business as it is in everyday life. Carnegie teaches that success often depends more on how you treat people than on technical expertise. For anyone looking to grow their career, improve leadership skills, or strengthen communication, this book remains one of the best guides available.

Key Lessons:

Don’t criticize, condemn, or complain—lead with kindness.

Give honest and sincere appreciation—people thrive on recognition.

Become genuinely interested in others, and remember their names.

Avoid arguments—approach conversations with warmth and curiosity.

Let others feel ownership of ideas—collaboration builds stronger outcomes.

3. Rich Dad Poor Dad by Robert Kiyosaki

This book reshapes the way many people think about money. Through the contrast of his “rich dad” and “poor dad,” Kiyosaki explains why building assets and investing are essential, while relying solely on a paycheck can limit financial growth. The book highlights the benefits of owning a business or investing in income-producing assets versus being stuck in the cycle of working for money.

Key Lessons:

Assets put money in your pocket, liabilities take it out—know the difference.

Don’t work only for money—learn how money works and put it to work for you.

Entrepreneurship and investing create wealth faster than wages.

Financial education is more important than formal education.

Take calculated risks instead of seeking complete security.

4. Blue Ocean Strategy by W. Chan Kim and Renée Mauborgne

For those who aspire to start their own business, this book is essential. The authors explain how companies can break away from crowded, competitive “red oceans” and instead create innovative products or services in uncontested “blue oceans.” This strategy allows entrepreneurs to differentiate themselves, grow faster, and avoid the race-to-the-bottom competition.

Key Lessons:

Don’t compete in crowded markets—create new market space.

Focus on differentiation and value innovation, not price wars.

Eliminate what doesn’t add value, and elevate what customers truly care about.

Small, creative ideas can disrupt entire industries.

Long-term success comes from standing apart, not blending in.

5. One Up on Wall Street by Peter Lynch

Originally published in 1989, this classic investment book remains one of the most practical guides for everyday investors. Lynch, one of the most successful mutual fund managers of all time, explains how average people can use their everyday knowledge—like the products they buy and the companies they interact with—to make smart investment decisions. While the markets have evolved since the book’s release, the core principles remain timeless.

Key Lessons:

Invest in what you know—your everyday life can reveal great companies.

Do your own research before following Wall Street trends.

Long-term investing beats short-term speculation.

A simple, understandable company is often a better investment than a complex one.

Patience and discipline are critical—ignore market noise.

Final Thoughts

Each of these books delivers valuable lessons that can change the way you approach money, career, and business. From getting out of debt, to building stronger relationships, to launching innovative companies, these resources provide a roadmap to success.

No matter your stage of life or career, pick the book that speaks most to your current situation and commit to applying what you learn. Over time, the habits and strategies you gain will compound, setting you apart and positioning you for long-term wealth.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

Why is financial education so important?

Financial knowledge helps individuals make informed decisions about saving, investing, and managing debt. The earlier you learn core principles, the more effectively you can avoid mistakes, build wealth, and create financial independence over time.

What are the best books to start learning about personal finance?

Books like The Total Money Makeover by Dave Ramsey, Rich Dad Poor Dad by Robert Kiyosaki, and One Up on Wall Street by Peter Lynch offer practical guidance on budgeting, investing, and building long-term wealth. Each provides actionable strategies for different stages of life.

How can The Total Money Makeover help with debt management?

Dave Ramsey’s book focuses on eliminating debt through a structured “baby steps” plan. It teaches readers to live on a budget, build an emergency fund, and use the “debt snowball” method to gain momentum toward financial freedom.

What’s the main takeaway from Rich Dad Poor Dad?

The book emphasizes that wealth comes from owning assets and understanding how money works, not just earning a paycheck. It encourages entrepreneurship, investing, and financial education as the keys to long-term success.

Why is How to Win Friends and Influence People valuable for financial success?

Success in business and personal finance often depends on relationships and communication. Dale Carnegie’s classic teaches principles of empathy, influence, and connection that are vital for leadership, networking, and negotiation.

Who should read Blue Ocean Strategy?

Aspiring entrepreneurs and business leaders can benefit from this book’s insights on creating new markets instead of competing in saturated ones. It provides a framework for innovation, differentiation, and long-term growth.

What investing lessons does One Up on Wall Street teach?

Peter Lynch shows that everyday investors can identify great opportunities by observing products and companies they already know. His approach focuses on patience, research, and long-term investing rather than short-term speculation.

Understanding Per Stirpes Beneficiary Designations

“Per stirpes” is a common estate planning term that determines how assets pass to descendants if a beneficiary dies before you. Greenbush Financial Group explains how per stirpes works, compares it to non–per stirpes designations, and outlines why updating your beneficiary forms is critical for ensuring your wishes are honored.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

When you fill out a beneficiary form for a retirement account, life insurance policy, or investment account, you may come across the term “per stirpes.” It’s a Latin phrase, but don’t let that intimidate you. Choosing per stirpes for your beneficiaries simply determines what happens if one of your named beneficiaries passes away before you do.

In this article, we’ll cover:

What per stirpes means and how it works

A simple comparison of per stirpes vs. non–per stirpes designations

Why keeping beneficiaries up to date is so important

Special considerations when children or minors are involved

What Does Per Stirpes Mean?

Per stirpes means “by branch” or “by the bloodline.” With this designation, if one of your named beneficiaries passes away before you, their share of the inheritance automatically passes down to their descendants.

If you don’t select per stirpes, your beneficiary designation is considered non–per stirpes, which means that if a beneficiary predeceases you, their share is generally redistributed among the remaining named beneficiaries.

Example: 50/50 Beneficiaries

Let’s walk through a clear example.

Case 1: Non–Per Stirpes (default in many plans)

You name your two children, Anna and Ben, as 50/50 beneficiaries.

Anna passes away before you.

Result: Ben inherits 100% of the account. Anna’s children (your grandchildren) do not receive anything unless you’ve updated the beneficiary form to include them.

Case 2: Per Stirpes

You name your two children, Anna and Ben, as 50/50 beneficiaries per stirpes.

Anna passes away before you, leaving two children of her own.

Result: Ben still receives his 50% share. Anna’s 50% share is split evenly between her two children (25% each).

This is why per stirpes is often called a “fail-safe” designation—it ensures the inheritance follows the family line if a beneficiary dies before you.

Why Keeping Beneficiaries Updated Matters

While per stirpes can act as a backup plan, the best approach is to keep your beneficiary designations current.

If a beneficiary passes away, you can always file a new form naming updated beneficiaries.

If you update promptly, the per stirpes designation never even comes into play.

Regular reviews—especially after major life events like births, deaths, or divorces—can help ensure your assets go exactly where you intend.

Special Considerations for Minors

Per stirpes can create complications if the next in line are minor children. For example, if Anna’s 50% share passes to her 10-year-old child, that minor generally cannot inherit assets outright. Instead, the guardian of the child may have to serve as a custodian to the account until the child reaches the age of majority. However, when the child reaches the age of majority, they gain full control over their inheritance, which may or may not be beneficial.

This raises an important planning question:

Do you want minor children to inherit directly?

Or would it make more sense to create a trust and name the trust as the beneficiary?

Working with an estate planning attorney can help clarify the best approach for your family.

Key Takeaways

Per stirpes means a beneficiary’s share passes down to their descendants if they predecease the account owner.

Non–per stirpes means a predeceased beneficiary’s share is typically divided among the remaining beneficiaries.

Keeping beneficiary forms up to date reduces the need to rely on per stirpes.

If potential per stirpes beneficiaries are minors, additional planning (like a trust) may be necessary.

Beneficiary designations are powerful estate planning tools. A quick review of your forms can make all the difference in ensuring your assets are passed down according to your wishes—without leaving things to chance.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

What does “per stirpes” mean on a beneficiary form?

“Per stirpes” is a Latin term meaning “by branch” or “by bloodline.” It ensures that if a named beneficiary passes away before you, their share automatically goes to their descendants, such as their children or grandchildren.

How does per stirpes differ from non–per stirpes?

With a per stirpes designation, a deceased beneficiary’s share passes down to their heirs. In contrast, a non–per stirpes designation redistributes that share among the remaining living beneficiaries, bypassing the deceased beneficiary’s family line.

Why should I keep my beneficiary designations up to date?

Life events such as marriages, births, deaths, or divorces can change your intentions for who should inherit your assets. Regularly updating your forms ensures your accounts are distributed according to your current wishes rather than relying on default rules or outdated designations.

What happens if a per stirpes beneficiary is a minor?

Minors typically cannot inherit assets outright, so a custodian or guardian may need to manage the funds until the child reaches adulthood. Some families use trusts to control when and how minors receive their inheritance.

When should I consider naming a trust instead of individuals as beneficiaries?

If you want more control over how and when heirs—especially minors—receive their inheritance, naming a trust as the beneficiary can help. A trust allows you to set specific rules for distributions and avoid complications with guardianship or early access to funds.

Is per stirpes the best option for everyone?

Not necessarily. While per stirpes ensures assets follow the family line, some people prefer equal redistribution among surviving beneficiaries. The best choice depends on your family structure, estate goals, and how you want your assets to be passed down.

Retiring Before 65? How to Bridge the Health Insurance Gap Until Medicare

Retiring before age 65 creates a major challenge: how to pay for health insurance until Medicare begins. Greenbush Financial Group outlines options including ACA exchange subsidies, COBRA, spouse employer plans, and HSAs—plus key planning steps to manage income, reduce costs, and avoid gaps in coverage.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

One of the biggest challenges for individuals planning to retire before age 65 is how to pay for health insurance until Medicare kicks in. Unlike employer coverage, which often subsidizes a large portion of the premium, individual coverage can be expensive—and health care costs are a major factor in determining if early retirement is financially feasible.

In this article, we’ll explore:

Health insurance through the Affordable Care Act (ACA) exchange and how subsidies work

COBRA coverage as a temporary option and how rules vary by state

Coverage through a spouse’s employer and how to coordinate benefits when one spouse retires

Using a Health Savings Account (HSA) to fund health care expenses before Medicare

Why income planning is critical when considering exchange subsidies

How “Navigators” can help retirees select the right plan

The importance of planning ahead before you retire

Exchange Policies: Income-Based Subsidies

The ACA exchange (also known as the marketplace) provides health insurance options that may be more affordable than people realize—thanks to premium tax credits and cost-sharing subsidies.

Here’s the key: Subsidies are based on income, not assets.

This means someone could have $1 million in investment / retirement accounts but report relatively low taxable income and still qualify for significant subsidies. For example, if you live primarily off savings or manage withdrawals from retirement accounts strategically, you may qualify for much lower premiums.

Planning Tip: Since subsidies are income-driven, managing taxable income (through Roth conversions, tax-efficient withdrawals, or capital gains planning) is a crucial part of retirement planning before age 65.

COBRA Coverage

Another option to bridge the gap is COBRA coverage from your former employer. COBRA allows you to continue your existing employer plan, typically for 18 months, but in some cases longer depending on state laws.

The downside? Cost. Under COBRA, you generally pay the full premium plus a 2% administrative fee, which can be much higher than what you were used to as an active employee.

Coverage Through a Spouse’s Employer

If your spouse is still working, you may be able to join their employer-sponsored health plan. This option is often less expensive than COBRA or the exchange, and employers usually subsidize a portion of the premium for dependents.

When one spouse retires, it’s important to notify the employer and coordinate the change in coverage. Many plans allow special enrollment when a spouse loses employer-sponsored insurance, so timing the switch correctly is key.

Using a Health Savings Account (HSA)

If you’ve been contributing to an HSA during your working years, this account can be a valuable bridge for health care costs before Medicare.

HSAs allow you to withdraw funds tax-free for qualified medical expenses, including insurance premiums for COBRA or Medicare.

Unlike Flexible Spending Accounts (FSAs), unused HSA funds carry over year to year, making them an effective tool for pre-retirement savings.

By banking HSA contributions in your working years, you give yourself more flexibility to cover early-retirement health care costs.

The Financial Planning Perspective

Health care is often the largest expense for retirees before Medicare eligibility. When building your retirement income plan, ask:

How much will insurance cost under COBRA, a spouse’s plan, or the exchange?

How much taxable income do you plan to show in early retirement, and will it affect exchange subsidies?

Do you have HSA funds available to offset these costs?

How long will you need coverage before Medicare (just a few years or more than a decade)?

The answers to these questions directly impact whether early retirement is financially realistic.

Exchange Navigators: Help at No Cost

Not everyone feels comfortable navigating the ACA exchange on their own. Fortunately, each state has navigators—trained professionals who help individuals understand their health coverage options and available subsidies.

These navigators are state-funded, so their services come at no additional cost to you. If you’re considering exchange coverage, speaking with a navigator can help ensure you’re getting the right plan and maximizing subsidies.

Planning Ahead Is Critical

One of the biggest mistakes we see is individuals retiring without a plan for health insurance. Waiting too long to assess the various options can lead to gaps in insurance, higher premiums, or missed opportunities for subsidies.

Planning ahead allows you to:

Time your retirement date with coverage options

Estimate premiums under different income scenarios

Decide between COBRA, a spouse’s plan, or the exchange

Maximize tax strategies to reduce costs

Key Takeaways

Retiring before 65 requires a clear plan for health insurance until Medicare.

The ACA exchange offers income-based subsidies, making taxable income planning essential.

COBRA coverage can provide continuity but is usually expensive

If your spouse is still working, joining their plan may be the most cost-effective bridge.

HSAs are a powerful tool to fund health insurance and medical costs pre-Medicare.

Use navigators for guidance on exchange policies and subsidies.

Start planning health coverage well before your retirement date to avoid costly surprises.

Health care is one of the biggest financial considerations for early retirees. By planning ahead, you can bridge the gap to Medicare while keeping costs manageable—and retire with peace of mind.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

What are the main health insurance options for early retirees before Medicare?

Common options include coverage through the Affordable Care Act (ACA) exchange, COBRA from a former employer, or joining a spouse’s employer-sponsored plan. Each option varies in cost, duration, and flexibility, depending on your income and household situation.

How do ACA exchange subsidies work for retirees?

Premium subsidies under the ACA are based on taxable income, not total assets. Retirees who manage withdrawals from retirement accounts strategically can often qualify for significant premium reductions, even with substantial savings.

Is COBRA a good option for early retirees?

COBRA allows you to stay on your former employer’s plan for up to 18 months (depending on state law), maintaining the same coverage. However, you must pay the full premium plus a small administrative fee, which can make it one of the more expensive options.

Can I use my spouse’s health insurance if I retire early?

Yes. If your spouse continues to work, you may be eligible to join their employer-sponsored plan. This is often more affordable than COBRA or an ACA plan, especially since many employers subsidize dependent coverage.

How can a Health Savings Account (HSA) help cover pre-Medicare costs?

Funds in an HSA can be withdrawn tax-free for qualified medical expenses, including COBRA and Medicare premiums. Building up HSA savings before retirement can provide a valuable source of tax-efficient funds to cover healthcare costs.

Why is income planning so important for ACA subsidies?

Since exchange subsidies are income-based, managing distributions from taxable retirement accounts, or capital gains planning, can dramatically lower your health insurance premiums in early retirement.

What are ACA “navigators,” and how can they help?

Navigators are trained, state-funded professionals who help individuals compare ACA plans and determine eligibility for subsidies. Their services are free and can simplify selecting the most cost-effective coverage for your situation.

Putting Your Child on Payroll: Tax Benefits and Planning Considerations for Business Owners

Hiring your child in your business can reduce family taxes and create powerful retirement savings opportunities. Greenbush Financial Group explains how payroll wages allow Roth IRA contributions, open the door to retirement plan participation, and provide long-term wealth benefits—while highlighting the rules and compliance concerns you need to know.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

For business owners, employing your child in the family business can be both financially and personally rewarding. Not only does it teach children about responsibility and work ethic, but it can also open up meaningful tax and retirement planning opportunities. However, this strategy comes with important rules and limitations that need to be carefully understood before implementation.

In this article, we’ll cover:

Why parents consider putting their children on payroll

The tax benefits of shifting income

How retirement plan contributions can supercharge long-term wealth for kids

Using W-2 wages to fund Roth IRAs

Key limitations and compliance concerns to keep in mind

Shifting Income: The Tax Advantage

One of the primary motivations for hiring your child is income shifting—moving taxable income from a higher-bracket parent to a lower-bracket child.

For example, instead of paying yourself additional compensation taxed at 37%, you could pay your child for legitimate work at their much lower (or even 0%) tax bracket. The wages are deductible for the business, and the child may owe little to no federal income tax, depending on their total earnings.

This strategy can effectively lower the family’s overall tax bill while compensating your child fairly for real work.

Retirement Plan Contributions for Your Child

If your child is legitimately on payroll, they may also become eligible for participation in the company’s retirement plan. With the right plan design, this could allow:

401(k) deferrals (including Roth contributions) up to $23,500 per year in 2025

Employer contributions in addition to employee deferrals, depending on plan rules.

Imagine the power of decades of tax-free Roth 401(k) growth starting in your child’s teenage years. Even modest contributions today could compound into significant wealth by retirement.

Funding a Roth IRA

Even if your child doesn’t earn enough to max out a 401(k) or work enough hour to become eligible for the company’s 401(k) plan, any earned income reported on a W-2 makes them eligible to contribute to a Roth IRA.

The 2025 contribution limit is $7,000 for individuals under age 50.

Contributions must not exceed the child’s earned income for the year.

This is one of the most effective long-term wealth accumulation strategies available for young workers, given the decades of tax-free growth that a Roth IRA can provide.

Practical Limitations and Compliance Concerns

While the benefits are clear, there are serious rules and restrictions that business owners must respect:

Reasonable work and pay: The job duties and pay must be appropriate for the child’s age and abilities. A 6-year-old making $30,000 a year for “marketing or consulting” is not likely to pass IRS scrutiny.

Labor laws: States impose restrictions on how much and what type of work minors can do. These vary by state, and compliance is essential.

Payroll compliance: Children on payroll must be treated like any other employee—filed on W-2s, subject to FICA taxes (unless an exception applies), and paid at reasonable market rates.

Retirement plan eligibility: Not all plans allow immediate participation. Some require minimum service or age thresholds. Plan design must be reviewed before assuming your child can make contributions.

Audit risk: Employing family members can attract IRS attention. Documentation of actual work performed (e.g., timesheets, job descriptions, projects completed) is important.

Other Considerations

While putting children on payroll can save taxes and accelerate wealth-building, it’s not a one-size-fits-all strategy. Business owners must weigh:

The cost of payroll taxes on the child’s wages

Retirement plan contribution obligations for other employees if the child becomes eligible

Administrative requirements and state-specific child labor rules

The optics of compensation relative to duties performed

Key Takeaways

Hiring your child can shift income into a lower tax bracket and reduce the family’s overall tax bill.

Payroll wages open the door to retirement savings strategies like Roth 401(k) contributions (if the plan allows) and Roth IRAs (up to $7,000 per year).

Plan design, labor laws, and IRS scrutiny mean you must be cautious, document carefully, and ensure the arrangement is reasonable.

This strategy can be powerful for both tax savings today and long-term wealth accumulation for your child—but it must be implemented correctly.

Before putting your child on payroll, consult with both your tax advisor and your retirement plan administrator. Done right, this can be a smart family wealth-building strategy. Done wrong, it can create compliance headaches.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

Why would a business owner put their child on payroll?

Hiring your child allows you to shift income from a higher tax bracket to a lower one, reducing the family’s overall tax liability. It also helps children learn valuable work and financial skills while legitimately earning income.

How does hiring a child create tax benefits?

Wages paid to a child for real work are deductible business expenses, lowering the company’s taxable income. Meanwhile, the child may owe little to no federal income tax if their earnings stay below standard deduction thresholds.

Can my child contribute to a retirement plan if they work for my business?

Yes. If they meet eligibility requirements, children can make 401(k) contributions—including Roth deferrals—through your company’s retirement plan. Even small contributions in their early years can compound significantly over time.

Can my child open a Roth IRA with earned income?

Absolutely. As long as your child earns income reported on a W-2, they can contribute up to $7,000 per year (2025 limit) to a Roth IRA, not exceeding their total earned income. Roth IRAs are especially powerful for young workers due to decades of tax-free growth.

What are the key IRS and labor law rules when employing your child?

The work must be age-appropriate, pay must be reasonable for the duties performed, and proper payroll procedures must be followed. Employers must also comply with state child labor laws and maintain documentation of actual work performed.

Are there any risks or downsides to hiring your child?

Yes. Improper pay, lack of documentation, or failure to follow labor laws can trigger IRS scrutiny. Additionally, adding your child to the company’s payroll may create additional administrative costs or affect retirement plan participation rules.

What should business owners do before putting their child on payroll?

Consult with your tax advisor and retirement plan administrator to ensure the arrangement complies with IRS and labor regulations. Proper planning helps you maximize tax benefits while avoiding compliance issues.

Do Social Security and Pension Payments Automatically Stop After Someone Passes Away?

When a loved one passes away, Social Security and pension payments don’t always stop automatically. Greenbush Financial Group explains how benefits are handled, what survivor benefits may continue, and why notifying the right agencies quickly can prevent overpayments and financial stress.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

When a loved one passes away, the last thing most families want to think about is financial paperwork. But knowing how Social Security and pensions handle payments after death is important to avoid complications—and sometimes even having to pay money back.

In this article, we’ll walk through:

How Social Security gets notified of a death

How pension plans handle benefit changes or survivor benefits

What happens if extra payments are made after someone dies

Steps families can take to make the process smoother

Does Social Security Automatically Get Notified?

Social Security does not always know right away when someone has passed away. Notification usually happens through a few channels:

Funeral homes: Most funeral directors automatically report the death to Social Security if you provide the Social Security number.

Vital records offices: State offices that issue death certificates send reports to Social Security.

Family members: Survivors can call Social Security directly at 1-800-772-1213 to report the death.

It’s generally a good idea for a family member to call Social Security directly, even if the funeral home is handling notification. This avoids delays and prevents overpayments.

What About Pension Payments?

Unlike Social Security, pension payments come from an employer-sponsored retirement plan, and each plan has its own rules.

When a pensioner passes away:

The plan administrator must be notified (usually with a copy of the death certificate).

If the pension had a survivor benefit option, payments may continue to the surviving spouse, but potentially at a reduced amount (for example, 50% or 75% of the original benefit).

If no survivor benefit was elected, payments stop entirely.

Employers and pension administrators typically don’t receive automatic death notifications. It is up to the family or executor to contact the plan.

What Happens if Extra Payments Are Made?

If Social Security or a pension plan issues payments after the recipient’s death, those payments are considered overpayments and must be returned.

Social Security: Payments are typically due back if they were made for the month after the person passed. For example, if someone dies in June, the July payment (received in July for June’s benefit) must be returned. The bank may be required to send it back automatically.

Pensions: If payments continue after the date of death, the plan administrator will usually request repayment once notified.

If funds have already been withdrawn from the account, the surviving family may be responsible for repayment.

Key Takeaways

Social Security is usually notified by funeral homes or state records, but families should still call directly to avoid delays.

Pension plans typically do not get automatic notifications—survivors must contact the plan administrator with a death certificate.

Survivor benefits depend on the pension election made at retirement.

Any overpayments from Social Security or pensions must be returned.

While it’s an uncomfortable topic, taking quick action to notify Social Security and pension administrators can prevent financial stress later. It’s one of those small but important steps in the estate settlement process.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions:

Does Social Security automatically know when someone dies?

Not always. Funeral homes typically report deaths to Social Security if given the person’s Social Security number, and state vital records offices also send reports. However, families should still call Social Security directly at 1-800-772-1213 to confirm notification and prevent overpayments.

What happens to Social Security payments after death?

Social Security benefits stop the month a person dies. Any payment made for the month after death must be returned. For example, if someone passes in June, the benefit received in July must be sent back.

How are pension payments handled when a retiree passes away?

Pension plans must be notified of the death, usually with a copy of the death certificate. If a survivor benefit was chosen, payments may continue to the spouse—often at a reduced amount (such as 50% or 75%). If no survivor option was selected, pension payments stop entirely.

Who is responsible for reporting a death to the pension plan?

The family, executor, or surviving spouse must contact the pension plan administrator directly. Employers and pension providers do not receive automatic death notifications.

What if Social Security or the pension keeps paying after death?

Any payments made after the date of death are considered overpayments and must be returned. The bank may automatically send back Social Security payments, while pension plans typically contact the family to recover funds.

Special Rules for S-Corps with Employer-Sponsored Retirement Plans

Missing a Required Minimum Distribution can feel overwhelming, but the rules have changed under SECURE Act 2.0. In this article, we explain how to correct a missed RMD, reduce IRS penalties, and file the right tax forms to stay compliant.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

S-Corporations can be an excellent structure for small business owners, especially from a tax perspective. But when it comes to retirement plans—such as 401(k)s and profit-sharing plans—S-Corps play by a slightly different set of rules compared to other business entities. Understanding these differences is critical for maximizing retirement savings and avoiding unpleasant surprises.

In this article, we’ll cover:

How compensation is defined for S-Corp owners in a retirement plan

Why relying too heavily on distributions can limit retirement savings

The impact of employer contributions for S-Corp owners with staff

Timing considerations for employee deferrals in S-Corps versus pass-through entities

A practical example that shows how these rules work in real life

W-2 Wages Drive Retirement Contributions for S-Corp Owners

Here’s the key difference:

Partnerships and sole proprietorships – Contributions are based on total pass-through earnings from the business.

S-Corporations – Contributions are based only on W-2 wages paid to the owner.

This matters because many S-Corp owners try to minimize their W-2 salary and take more of their income in shareholder distributions. Distributions avoid payroll taxes, which can be a big tax advantage. But retirement plans only look at W-2 wages when calculating contribution limits.

Example: High Income, Low W-2

Suppose an S-Corp owner earns $500,000 total income, but only pays themselves $100,000 in W-2 wages.

Maximum employer contribution = 25% of W-2 wages = $25,000

Add employee salary deferral = up to $23,500 (2025 limit, or $31,000 if age 50+)

Total = roughly $48,500 (or $56,000 with catch-up)

That’s far below the 2025 annual addition limit of $70,000 ($77,500 with catch-up). By keeping W-2 wages artificially low, the owner unintentionally caps their retirement contributions.

The Ripple Effect on Employees

If the owner sets their employer contribution at 25% of W-2 compensation, that percentage generally applies to eligible employees as well.

In our example, if the owner receives a 25% contribution on $100,000 ($25,000), employees may also need to receive a large employer contribution for the plan to pass testing.

For a company with multiple employees, this can become a very expensive retirement plan design.

Timing of Deferrals: Another S-Corp Quirk

Another important difference involves the timing of employee salary deferrals:

S-Corp owners are on payroll, so any employee deferrals must be processed through payroll no later than the final paycheck in December. If you wait until after year-end, it’s too late to make employee deferrals for that tax year.

Partnership or sole proprietor owners may have more flexibility, since contributions can often be made up to the tax filing deadline (with extensions) and still count toward the prior year.

Translation: If you’re an S-Corp owner, don’t wait until tax season to think about retirement contributions. Deferrals need to be in place before December 31st.

Key Takeaways for S-Corp Owners

Only W-2 wages count toward retirement contributions, not shareholder distributions.

Keeping W-2 wages too low may limit your ability to maximize contributions.

Large employer contributions for the owner can trigger equally large contributions for employees.

Employee salary deferrals must run through payroll and be completed by the last December paycheck.

Careful planning throughout the year—not just at tax time—is essential.

If you’re an S-Corp owner considering a retirement plan, make sure your payroll and compensation strategy aligns with your retirement savings goals. The right plan design can help you strike a balance between tax efficiency today and meaningful retirement wealth in the future.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

How do retirement plan contributions work for S-Corporation owners?

For S-Corp owners, retirement contributions are based only on W-2 wages—not total business income or shareholder distributions. This makes salary decisions especially important for maximizing 401(k) or profit-sharing plan contributions.

Why can keeping W-2 wages low hurt retirement savings for S-Corp owners?

While taking more income as shareholder distributions can reduce payroll taxes, it also limits how much you can contribute to a retirement plan. Employer contributions are capped at 25% of W-2 wages, so a lower salary means smaller allowable contributions.

How do employer contributions for owners affect employees in an S-Corp retirement plan?

If an owner contributes a high percentage of their W-2 income (such as 25%), nondiscrimination testing may require giving the same percentage to eligible employees. This can significantly increase plan costs for businesses with multiple staff members.

When must S-Corp owners make 401(k) salary deferrals?

Employee deferrals must be processed through payroll no later than the final paycheck of the year. Unlike partnerships or sole proprietors, S-Corp owners cannot make deferrals after December 31 for the prior tax year.

Can S-Corp owners include distributions when calculating 401(k) contributions?

No. Only W-2 wages qualify for retirement plan contribution calculations. Distributions from the S-Corp are not considered “earned income” for 401(k) or profit-sharing purposes.

What steps should S-Corp owners take to maximize retirement contributions?

Plan ahead by setting a reasonable W-2 salary that supports both tax efficiency and contribution goals. Coordinate payroll timing, plan design, and employee testing requirements with your tax advisor and retirement plan administrator early in the year.