2026 Tax-Efficient Retirement Withdrawals: How to Keep More of Your Money

A tax-efficient retirement withdrawal strategy focuses on minimizing taxes while creating consistent income throughout retirement. The order in which you withdraw from taxable, tax-deferred, and Roth accounts can significantly impact how long your money lasts. At Greenbush Financial Group, our analysis shows that strategic withdrawals can reduce lifetime taxes and increase net retirement income.

A tax-efficient retirement withdrawal strategy focuses on minimizing taxes while creating consistent income throughout retirement. The order in which you withdraw from taxable, tax-deferred, and Roth accounts can significantly impact how long your money lasts. At Greenbush Financial Group, our analysis shows that strategic withdrawals can reduce lifetime taxes and increase net retirement income.

Understanding the Three Types of Retirement Accounts

Before building a withdrawal strategy, it is important to understand how different accounts are taxed.

1. Taxable Accounts (Brokerage Accounts)

Capital gains taxes apply when investments are sold

Long-term capital gains rates are often lower than income tax rates

Dividends may also be taxed annually

2. Tax-Deferred Accounts (Traditional IRA, 401(k))

Withdrawals are taxed as ordinary income

Required Minimum Distributions (RMDs) apply starting in your 70s

3. Tax-Free Accounts (Roth IRA, Roth 401(k))

Qualified withdrawals are tax-free

No RMDs for Roth IRAs

Provides flexibility for tax planning

At Greenbush Financial Group, we view these three “buckets” as the foundation of any tax-efficient withdrawal plan.

The Traditional Withdrawal Order Strategy

A common approach is to withdraw funds in a specific sequence to manage taxes over time.

Standard Withdrawal Order

Taxable accounts first

Tax-deferred accounts second

Roth accounts last

Why This Strategy Works

Allows tax-deferred accounts to continue growing

Delays ordinary income taxes

Preserves Roth accounts for later years or legacy planning

However, this strategy is not always optimal in every situation.

Why a Blended Withdrawal Strategy May Be Better

Strictly following the traditional order can sometimes lead to higher taxes later in retirement.

The Problem

If you delay withdrawals from tax-deferred accounts too long:

RMDs can become large

You may be pushed into higher tax brackets

Social Security may become more taxable

Medicare premiums (IRMAA) may increase

A More Strategic Approach

At Greenbush Financial Group, we often recommend a blended withdrawal strategy:

Withdraw from taxable accounts

Supplement with partial IRA withdrawals

Use Roth accounts strategically when needed

This helps smooth out taxable income over time rather than creating spikes later.

Roth Conversions: A Key Tax Planning Tool

One of the most powerful strategies in retirement is converting pre-tax money into Roth accounts.

How It Works

Move funds from a Traditional IRA to a Roth IRA

Pay taxes now at current rates

Future growth and withdrawals are tax-free

When It Makes Sense

Years with lower income (early retirement before Social Security)

Before RMDs begin

When tax rates are temporarily lower

Example

Convert $50,000 from IRA to Roth

Pay tax today at a lower rate

Reduce future RMDs and taxes

At Greenbush Financial Group, Roth conversion strategies are often a cornerstone of long-term tax planning.

Managing Your Tax Bracket Each Year

Instead of focusing only on which account to withdraw from, it is often more effective to focus on your tax bracket.

Strategy

Fill up lower tax brackets intentionally

Avoid jumping into higher brackets

Coordinate withdrawals with Social Security timing

Example

If the 12% tax bracket ends at a certain income level:

Withdraw just enough from IRA to stay within that bracket

Use Roth or taxable accounts for additional income needs

This approach allows for more control over lifetime taxes.

How Social Security Impacts Your Tax Strategy

Social Security income can change how your withdrawals are taxed.

Key Considerations

Up to 85% of Social Security benefits can be taxable

Additional income from IRA withdrawals can increase taxation

Timing Social Security can impact your tax plan

Planning Insight

Delaying Social Security while using IRA withdrawals or Roth conversions early in retirement can sometimes lead to better long-term outcomes.

Avoiding Common Retirement Tax Mistakes

Many retirees unintentionally increase their tax burden.

Common Mistakes

Waiting too long to withdraw from tax-deferred accounts

Ignoring Roth conversion opportunities

Triggering higher Medicare premiums (IRMAA)

Not coordinating withdrawals with tax brackets

Over-withdrawing in a single year

At Greenbush Financial Group, we often see that small adjustments can lead to significant tax savings over time.

A Simple Example of a Tax-Efficient Withdrawal Plan

Scenario

Age 62, retired

$1,000,000 in savings

$400,000 IRA

$300,000 Roth IRA

$300,000 brokerage

Strategy

Withdraw from brokerage for living expenses

Convert $30,000–$50,000 annually from IRA to Roth

Delay Social Security until later years

Use Roth funds strategically after RMD age

Result

Lower lifetime taxes

Reduced RMD impact

Greater flexibility in retirement

Final Thoughts

A tax-efficient withdrawal strategy is not about following a fixed rule. It is about coordinating income sources, tax brackets, and long-term planning.

At Greenbush Financial Group, our analysis shows that retirees who proactively manage taxes throughout retirement often keep significantly more of their income and reduce the risk of large tax surprises later in life.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

- What is the best order to withdraw retirement funds?Typically taxable accounts first, then tax-deferred, then Roth, but a blended strategy is often more effective.

- Are Roth withdrawals always tax-free?Yes, if the account meets the qualified distribution rules.

- What is a Roth conversion?It is when you move money from a pre-tax account to a Roth account and pay taxes now to avoid taxes later.

- How can I reduce taxes on retirement income?By managing tax brackets, using Roth conversions, and coordinating withdrawals across account types.

- Do Required Minimum Distributions increase taxes?Yes, RMDs are taxable and can push you into higher tax brackets if not planned for

Is $1 Million Enough to Retire? A Practical Income and Longevity Analysis

Pre-retirees can take actionable steps now to strengthen their financial future. Learn essential retirement planning strategies and avoid costly mistakes.

A $1 million retirement portfolio can generate meaningful income, but whether it is enough depends on your spending, longevity, and withdrawal strategy. In many cases, a balanced approach suggests withdrawing around 3% to 4% annually, which translates to $30,000 to $40,000 per year before taxes. At Greenbush Financial Group, our analysis shows that $1 million is often a solid foundation, but rarely a complete solution without additional income sources like Social Security.

How Much Income Can $1 Million Generate in Retirement?

The most common starting point is the safe withdrawal rate, which estimates how much you can withdraw annually without running out of money.

Typical Withdrawal Guidelines

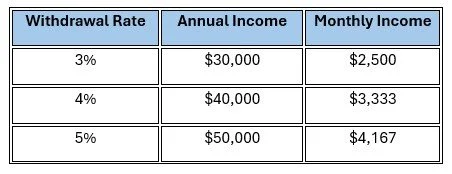

3% withdrawal rate = $30,000 per year

4% withdrawal rate = $40,000 per year

5% withdrawal rate = $50,000 per year (higher risk of depletion)

What This Means in Practice

How Social Security Changes the Equation

For most retirees, Social Security becomes a critical piece of the income plan.

Example Scenario

Portfolio withdrawal (4%) = $40,000

Social Security benefit = $25,000

Total annual income = $65,000

This is where $1 million becomes much more realistic.

Key Insight

Without Social Security, $1 million alone often supports a moderate lifestyle. With Social Security, it can support a comfortable retirement for many households, depending on spending habits.

Inflation: The Silent Risk to Your Retirement Plan

One of the biggest risks retirees face is rising costs over time.

Example

Year 1 expenses = $60,000

20 years later at 3% inflation ≈ $108,000

This is why simply matching your current expenses is not enough. Your income needs to grow over time, which will usually require keeping a portion of your portfolio invested.

At Greenbush Financial Group, we emphasize maintaining a growth component even in retirement portfolios to help offset inflation risk.

How Long Will $1 Million Last?

The longevity of your portfolio depends heavily on:

Withdrawal rate

Investment returns

Market volatility

Lifespan

General Guidelines

3% withdrawal → Often sustainable for 30+ years

4% withdrawal → Historically sustainable, but not guaranteed

5%+ withdrawal → Increased risk of running out of money

Sequence of Returns Risk

Early market downturns in retirement can significantly impact how long your money lasts. This is known as sequence of returns risk, and it is one of the most important planning factors.

What Lifestyle Does $1 Million Support?

The answer varies widely depending on location, spending, and lifestyle expectations.

Likely Scenarios

Modest Lifestyle

Lower cost-of-living area

Limited travel

Paid-off home

Income need: $40,000–$60,000

Moderate Lifestyle

Some travel and discretionary spending

Healthcare costs rising over time

Income need: $60,000–$90,000

High-Spending Lifestyle

Frequent travel, luxury expenses

Higher healthcare and insurance costs

Income need: $100,000+

In many cases, $1 million alone may fall short for higher spending lifestyles without additional income sources.

Tax Considerations on Retirement Income

Not all $40,000 of income is actually spendable.

Key Tax Factors

Traditional IRA/401(k) withdrawals are taxed as ordinary income

Roth IRA withdrawals may be tax-free

Social Security may be partially taxable

Required Minimum Distributions (RMDs) begin in your 70s

At Greenbush Financial Group, tax-efficient withdrawal strategies are often the difference between a plan that works and one that struggles.

Strategies to Make $1 Million Last Longer

There are several ways to improve the sustainability of a $1 million portfolio.

Planning Strategies

Delay Social Security to increase guaranteed income

Use Roth conversions to reduce future taxes

Adjust withdrawals based on market performance

Maintain a diversified portfolio with growth exposure

Reduce fixed expenses before retirement

Real-World Insight

We often see that retirees who remain flexible with spending and withdrawals tend to have significantly better outcomes than those who follow a rigid income plan.

When $1 Million May Not Be Enough

There are specific situations where $1 million may fall short:

Early retirement (before age 62 or 65)

High healthcare costs before Medicare

Significant debt or mortgage payments

High inflation environments

Supporting family members financially

Market downturns and investment mismanagement

In these cases, additional planning becomes critical.

Final Thoughts

A $1 million portfolio can absolutely support retirement, but it is not a one-size-fits-all solution. At Greenbush Financial Group, our analysis shows that success depends on how income is generated, how taxes are managed, and how flexible the retiree is with spending.

For many households, $1 million works best when combined with Social Security and a well-structured withdrawal strategy.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

- Can you retire comfortably with $1 million?Yes, but it depends on your spending level, location, and whether you have additional income like Social Security.

- How much monthly income does $1 million generate?At a 4% withdrawal rate, about $3,300 per month before taxes.

- Is the 4% rule still safe in 2026?It is a useful guideline, but many financial planners now recommend closer to 3% to 4% depending on market conditions.

- What is the safest withdrawal rate for retirement?Around 3% is generally considered more conservative for long retirements.

- How long will $1 million last in retirement?It can last 25 to 30+ years depending on withdrawal rate, investment returns, and market conditions.

5 Questions Every Business Owner Should Answer Before Starting a Business

Starting a business requires more than excitement and a great concept. This article covers five essential questions every business owner should answer before launching, including business planning, client acquisition, startup costs, break-even timelines, and knowing when to walk away. By addressing these issues early, business owners can make smarter financial decisions and reduce the risk of costly mistakes. This is a practical guide for entrepreneurs who want to start a business with a clear plan and realistic expectations.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

After working with business owners for many years as a financial planner, I’ve seen firsthand that while many new businesses struggle, the ones that succeed usually have something in common: they answered a handful of very important questions before they ever opened their doors.

There’s a well-known statistic that a large percentage of new businesses don’t survive long-term. But the businesses that do succeed usually didn’t just have a good idea — they had a plan, a target market, and a clear understanding of the financial side of running a business.

In this article, we’ll cover five important questions every business owner should be able to answer before starting a business:

What is your business plan?

How will you obtain clients?

What are the costs of starting the business?

What is your timeline to break even?

When do you close the business?

These questions may not be the most exciting part of starting a business, but they can dramatically increase your chances of success.

1. What Is Your Business Plan?

There are a million great ideas for businesses. But a business idea is not a business plan.

A solid business plan should outline:

What product or service are you offering?

How does the business make money?

What is your pricing structure?

Who are your ideal clients?

How will you onboard new clients?

What does it cost to produce your product or deliver your service?

How much do you need to sell to be profitable?

Who is responsible for what within the company?

How much money do you need to start the business?

What is the realistic timeline to profitability?

Without a plan, you’re not running a business — you’re making an educated guess.

That doesn’t mean your plan won’t change. In fact, it almost certainly will. But having a plan gives you something incredibly important: a starting point and something to adjust when things don’t go as expected.

It’s also incredibly valuable to:

Talk to other business owners in your industry

Study competitors in your area

Study competitors outside your area

Do market research before launching

One thing almost every business owner learns quickly: starting and running a business is harder than it looks from the outside. Expect challenges and be ready to adjust.

2. How Am I Going to Obtain Clients?

This is one of the most important questions a business owner can answer.

Many new business owners make the mistake of trying to sell to everyone. In reality, businesses tend to be more successful when they clearly define their ideal client.

You need to be able to answer two key questions about your potential clients:

Do they want what I’m selling?

Can they afford what I’m selling?

If the answer to either question is no, the business may struggle.

For example:

If people want your product but can’t afford it → You have a pricing problem.

If people can afford it but don’t want it → You have a marketing or product problem.

If people both want it and can afford it → Now you have a business opportunity.

One of the best things you can do before starting a business is talk to potential customers. Survey them. Ask questions. Have real conversations.

Many business owners are surprised to learn that what they thought people wanted is not actually what people needed or were willing to pay for.

3. What Are the Costs of Starting the Business?

Business owners almost always underestimate how much it costs to start a business.

Costs may include:

Inventory or materials

Software and technology

Website development

Marketing and advertising

Rent or office space

Build-out and equipment

Insurance

Accountant and tax preparation fees

Legal fees

Payroll or contractor costs

Licenses and permits

It’s usually wise to overestimate costs and underestimate revenue early on. That creates a financial cushion and helps prevent cash flow problems.

It’s also very helpful to talk with a tax professional or accountant early, because there are many financial and tax-related items new business owners may not be aware of.

4. What Is the Timeline to Break Even?

This question ties directly into the cost of starting the business.

Most businesses do not become profitable immediately. It takes time to:

Find clients

Deliver the product or service

Get paid

Build consistent revenue

Meanwhile, the business has ongoing expenses.

You should be able to estimate:

How many clients do I need to break even?

How long will it realistically take to get that many clients?

Can I financially survive until that point?

Simple Example:

If your business expenses are $5,000 per month and you make $100 per client, you need 50 clients per month just to break even.

But how long will it take to get those 50 clients?

3 months?

12 months?

24 months?

This is a critical planning question because many businesses fail not because the idea was bad, but because they ran out of money before they reached profitability.

5. When Do You Close the Business?

This is the hardest question on the list, but it may be one of the most important.

Starting a business is exciting. Business owners are proud of what they’re building. They tell friends and family. They invest time, money, and energy into making it work.

But sometimes, despite best efforts, a business simply isn’t going to work long-term.

The danger is when business owners:

Rack up credit card debt

Take out personal loans

Refinance their home

Drain retirement accounts

Continue pouring money into a business that isn’t sustainable

I’ve seen situations where business owners didn’t just end up closing the business — they ended up in a much worse financial position than before they started.

That’s why it’s important to define ahead of time:

How much money are you willing to invest?

How long are you willing to try?

What financial metrics need to be met to continue?

At what point do you walk away?

Closing a business is not a personal failure. Sometimes it’s a financial decision, and making that decision at the right time can prevent long-term financial damage.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

How Does Depreciation Work for Rental Properties?

Rental property depreciation allows investors to reduce taxable income by spreading the cost of a property over 27.5 years. This article explains how depreciation works, how it offsets rental income, and how improvements are treated. It also covers what happens when a property is fully depreciated and how depreciation recapture impacts taxes when selling. Understanding these rules can help investors maximize tax efficiency and avoid costly surprises.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Depreciation is one of the most important tax benefits of owning rental property. It allows property owners to offset part of the cost of owning the property against the rental income they receive, which can significantly reduce taxes in the early years of ownership.

In this article, we’ll cover:

What depreciation is and how it works

The 27.5-year depreciation rule for rental properties

How depreciation can offset rental income

How improvements are depreciated

What happens when depreciation runs out

What depreciation recapture is when you sell the property

What Is Depreciation?

Depreciation is a tax deduction that allows rental property owners to recover the cost of a property over time. Even though real estate often increases in value, the IRS allows you to treat the property as if it is wearing out over time and deduct a portion of its value each year.

This deduction can be used to offset rental income, which may reduce how much tax you owe on the income the property generates.

The 27.5-Year Depreciation Rule

Residential rental properties are typically depreciated over 27.5 years.

This means you take the purchase price of the property (excluding land value) and divide it by 27.5 to determine your annual depreciation deduction.

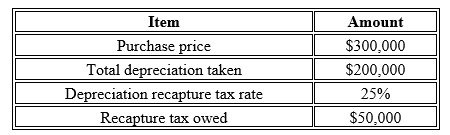

Example:

So, if you purchased a rental property for $300,000, you can depreciate roughly $11,000 per year.

How Depreciation Offsets Rental Income

Depreciation is considered a non-cash expense, meaning you don’t actually write a check for it, but you still get the tax deduction.

Example Scenario:

Rental income: $11,000 per year

Depreciation: $11,000 per year

In this example, the depreciation deduction offsets the rental income, which may result in little to no taxable rental income for that year.

This is one of the reasons rental real estate can be a very tax-efficient investment.

Depreciation on Improvements

Many rental property owners make improvements to their property, such as:

New roof

New furnace or heating system

Kitchen renovation

Bathroom remodel

Flooring

Additions

These are called capital improvements, and each improvement typically has its own depreciation schedule separate from the original property purchase.

For example:

Appliances: Often 5-year depreciation

Carpeting: Often 5–7 years

Roof: Often 27.5 years

HVAC systems: Often 15–27.5 years depending on classification

There are also situations where bonus depreciation or Section 179 may allow you to deduct a larger portion of the improvement cost upfront.

This is an area where working with a knowledgeable tax professional is very important, because depreciation schedules vary depending on the type of improvement.

What Happens When a Property Is Fully Depreciated?

After 27.5 years, the property is considered fully depreciated.

This means:

You no longer receive the annual depreciation deduction

More of your rental income becomes taxable

Your tax liability on rental income may increase

However, you still own the property and still collect rental income — you just don’t get the depreciation tax benefit anymore.

What Is Depreciation Recapture?

Depreciation is a great tax benefit while you own the property, but when you sell the property, the IRS requires something called depreciation recapture.

When you sell a rental property:

You pay capital gains tax on the profit from the sale

You also pay tax on all the depreciation you took over the years

Depreciation recapture is taxed at a flat 25% federal tax rate

Example:

So in this example, when the property is sold, the owner would owe:

Capital gains tax on the profit plus

$50,000 in depreciation recapture tax

This surprises many real estate investors if they are not prepared for it.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

-

How long do you depreciate a rental property?Residential rental property is depreciated over 27.5 years.

-

What happens if I don't take depreciation?The IRS assumes you took it anyway, and you may still have to pay depreciation recapture when you sell.

-

Can I depreciate renovations on my rental property?Yes, but renovations and improvements typically have their own depreciation schedules.

-

What is bonus depreciation?Bonus depreciation allows you to deduct a large portion of certain improvements upfront instead of spreading the deduction over many years.

-

Do I have to pay depreciation back when I sell the property?When you sell the property, you may be subject to depreciation recapture, which taxes the total depreciation amount taken by 25%.

-

What happens after 27.5 years of depreciation?The property is fully depreciated and you no longer receive the annual depreciation deduction.

-

Does depreciation reduce my capital gains when I sell?No. Depreciation actually lowers your cost basis, which can increase your taxable gain and trigger depreciation recapture.

-

Can depreciation create a loss on paper?Yes. Depreciation can sometimes create a taxable loss even if the property is producing positive cash flow.

-

Should I work with a CPA if I own rental property?It's highly recommended. Depreciation, improvements, and recapture rules are complex, and a knowledgeable CPA can help you maximize tax benefits and avoid costly mistakes.

Understanding the Social Security 50% Spousal Benefit

The Social Security 50% spousal benefit allows married or divorced individuals to receive up to half of their spouse’s full retirement age benefit. This guide explains eligibility rules, timing strategies, and why delaying benefits may not always maximize household income. Learn how filing decisions affect both spouses and how to coordinate benefits for optimal retirement income. Understanding these rules is essential for building an efficient Social Security strategy.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

When married couples are deciding when to file for Social Security, there are several strategies to consider. One of the most important — and often misunderstood — is the 50% spousal benefit. This rule can have a major impact on when each spouse should file and how to maximize total household Social Security income over retirement.

In this article, we’ll walk through:

What the 50% spousal benefit is

Special filing rules to qualify

Why “file and suspend” is no longer allowed

Why delaying to age 70 may not always make sense

Special rules for divorced spouses

Other factors to consider when choosing a filing strategy

What Is the 50% Spousal Benefit?

When you are married and eligible for Social Security, you have the option to receive:

100% of your own Social Security benefit, or

50% of your spouse’s benefit, whichever is higher.

You do not get both — Social Security will essentially give you the higher of the two amounts.

Example

Let’s look at an example:

Paul’s Full Retirement Age (FRA) benefit: $3,600 per month

Sharon’s FRA benefit: $800 per month

When Sharon files at her full retirement age (67), she can choose:

Her own benefit: $800/month

50% of Paul’s benefit: $1,800/month

Since $1,800 is higher than $800, she would elect the 50% spousal benefit.

This filing strategy is extremely important in situations where one spouse earned significantly more than the other.

Special Filing Rules

One of the most important rules for the 50% spousal benefit is this:

The higher-earning spouse must be receiving their Social Security benefit in order for the lower-earning spouse to claim the 50% spousal benefit.

Using Paul and Sharon again:

Both are age 67

Paul’s FRA benefit = $3,600

Sharon’s FRA benefit = $800

If Paul decides to delay his Social Security until age 70, Sharon cannot collect the spousal benefit until Paul actually turns his benefit on.

So Sharon would:

Take her own benefit of $800 at 67

Elect the 50% spousal benefit when Paul turn on at age 70 increasing to $1,800

This rule alone often drives a lot of the Social Security filing decision for married couples.

File and Suspend Is No Longer Allowed

Years ago, there was a strategy called “file and suspend.”

This allowed the higher-earning spouse to:

File for Social Security

Immediately suspend their benefit

Allow their benefit to continue growing until age 70

Meanwhile, the lower-earning spouse could collect the 50% spousal benefit

This strategy was very powerful, but the Social Security Administration eliminated the file and suspend strategy. Now, the higher-earning spouse must actually be receiving benefits for the spouse to receive the spousal benefit.

Delaying Until Age 70 May Not Always Make Sense

Many people know that if you delay Social Security past full retirement age, your benefit increases by approximately 8% per year until age 70.

From an individual standpoint, delaying can make a lot of sense. However, for married couples, the spousal benefit changes the math.

Here’s the key rule:

The 50% spousal benefit is based on 50% of the higher earner’s Full Retirement Age benefit, not their age 70 benefit.

Example

Let’s go back to Paul and Sharon:

Paul’s FRA benefit: $3,600/month

Paul’s age 70 benefit: about $4,500/month

Sharon’s own benefit: $800/month

Sharon’s spousal benefit: $1,800/month (50% of $3,600)

If Paul delays until age 70:

Sharon cannot collect the spousal benefit for 3 years

Her spousal benefit does not increase — it stays at $1,800

So the couple must evaluate:

Is the increase in Paul’s benefit worth Sharon not receiving the addition $1,000/month for three years? ($1,800 spousal benefit less Sharon’s $800 FRA benefit)

In situations where the spousal benefit is a large increase for the lower-earning spouse, it may make sense for the higher earner to file earlier, even if that means giving up the delayed credits.

However, if the spousal benefit is only slightly higher than the lower earner’s own benefit, delaying may still make sense.

This is why Social Security filing decisions should always be looked at from a household strategy, not just an individual strategy.

Divorced Couples: Special Consideration

Many people don’t realize that divorced spouses may still be eligible for the spousal benefit.

You may qualify for a 50% spousal benefit on an ex-spouse’s record if:

The marriage lasted at least 10 years

You are currently unmarried

Your own Social Security benefit is less than 50% of your ex-spouse’s benefit

Your ex-spouse is eligible for Social Security (they do not have to be collecting yet if divorced more than 2 years)

Even if your ex-spouse has remarried, you may still be eligible for the spousal benefit based on their record.

Importantly:

Your ex-spouse collecting a spousal benefit does NOT reduce their benefit and does not impact their current spouse.

Other Factors to Consider When Filing for Social Security

The 50% spousal benefit is just one piece of the Social Security planning puzzle. When building a filing strategy, we also consider:

Survivor benefits

Life expectancy of both spouses

Taxation of Social Security

Other retirement income sources

Roth conversion strategy

Required Minimum Distributions (RMDs)

The difference between each spouse’s benefit

The survivor benefit is especially important — when one spouse passes away, the surviving spouse keeps the higher of the two Social Security benefits, which is another reason why delaying the higher earner’s benefit can sometimes make sense.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions About the Social Security 50% Spousal Benefit

- What is the Social Security spousal benefit?The spousal benefit allows a married spouse to receive up to 50% of their spouse's full retirement age Social Security benefit if that amount is higher than their own benefit.

- Do I get my own benefit plus 50% of my spouse's benefit?No. You receive either your own benefit or the spousal benefit - whichever is higher - but not both.

- When can I claim the spousal benefit?You can claim the spousal benefit as early as age 62, but the benefit will be reduced if taken before your full retirement age.

- Does my spouse have to file before I can receive the spousal benefit?Yes. The higher-earning spouse must be actively receiving Social Security benefits before the lower-earning spouse can claim the 50% spousal benefit.

- Is the spousal benefit based on my spouse's age 70 benefit?No. The spousal benefit is based on 50% of your spouse's full retirement age benefit, not their age 70 benefit.

- If my spouse delays until age 70, does my spousal benefit increase?No. Your spousal benefit does not increase if your spouse delays past full retirement age. However, you must wait until they file to receive it.

- Can a divorced spouse collect a spousal benefit?Yes, if the marriage lasted at least 10 years and the individual is currently unmarried, they may be eligible for a spousal benefit based on their ex-spouse's record.

- Does my ex-spouse need to be collecting for me to claim a spousal benefit?If you have been divorced for more than two years, you may be able to claim a spousal benefit even if your ex-spouse has not filed yet, as long as they are eligible.

- What happens to the spousal benefit if my spouse passes away?The spousal benefit is replaced by a survivor benefit, which allows the surviving spouse to receive up to 100% of the deceased spouse's benefit.

- How do we know when we should file for Social Security?The optimal time to file depends on several factors including life expectancy, income needs, taxes, and the difference between each spouse's benefit. This decision should be evaluated as part of a full retirement income plan.

Rules for Inheriting a Retirement Account from a Sibling

When inheriting an IRA or 401(k) from a sibling, the rules depend heavily on age difference and IRS guidelines under the SECURE Act. This article explains the 10-year rule, Eligible Designated Beneficiary exception, and Required Minimum Distribution requirements. It also outlines tax-efficient withdrawal strategies for both pre-tax and Roth accounts. Understanding these rules can help reduce taxes and maximize long-term value.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

When you inherit a retirement account , whether it’s a 401(k), Traditional IRA, or Roth IRA, the rules depend heavily on who you inherited the account from. The rules for inheriting a retirement account from a sibling are very different from inheriting from a spouse, parent, or grandparent, and the distribution rules can have major tax consequences if not handled properly.

In this article, we’re going to walk through the key rules and planning strategies, including:

The 10-year rule for inherited retirement accounts

The age exception for siblings within 10 years

Required Minimum Distribution (RMD) rules

Tax strategies for inherited IRAs and 401(k)s

The 10-Year Rule

The IRS changed the rules for inherited retirement accounts starting in 2020 under the SECURE Act. For most non-spouse beneficiaries, inherited retirement accounts are now subject to the 10-year rule, which means the account must be fully depleted by the end of the 10th year following the year of death.

However, there is an important exception that often applies to siblings.

The Age Exception for Siblings

If you inherit a retirement account from a sibling and you are within 10 years of their age, you may qualify for the Eligible Designated Beneficiary exception. This allows you to use the old stretch IRA rules, instead of the 10-year rule.

This means:

You are not required to empty the account within 10 years

You are required to take annual RMDs based on your life expectancy

The account can continue to grow tax-deferred over your lifetime

Example

Let’s say:

Sue is age 50

Brian is her brother, age 45

Brian inherits Sue’s IRA

Because Brian is within 10 years of Sue’s age, he qualifies for the exception and can stretch distributions over his lifetime instead of following the 10-year rule.

He must begin taking Required Minimum Distributions (RMDs) starting the year after Sue passes away, but he is not forced to liquidate the entire account within 10 years.

Confusion With RMD Rules

This is one of the biggest areas of confusion for sibling beneficiaries.

There are two different sets of rules depending on whether the sibling qualifies for the within 10 year of age rule or not.

Situation 1: Sibling Within 10 Years of Age (Stretch Rules Apply)

If the sibling beneficiary is within 10 years of the person who passed away:

They are using the stretch IRA rules

They must take RMDs every year

RMDs begin the year after death

RMDs are calculated using the IRS Single Life Expectancy Table

They are not required to empty the account within 10 years

This is true regardless of whether the person who died had started RMDs or not.

This is where many people get confused. Under the old stretch rules, RMDs were always required for inherited IRAs, unless the beneficiary was a spouse.

Situation 2: Sibling More Than 10 Years Younger or Older (10-Year Rule Applies)

If the sibling is more than 10 years apart in age, they do not qualify for the exception and are subject to the 10-year rule.

Example:

Tim is age 55

His sister Jen is age 42

Jen inherits Tim’s IRA

Because the age difference is greater than 10 years, Jen must fully deplete the account within 10 years.

Now here’s where RMD rules depend on the age of the person who passed away:

If the person who passed away was not RMD age (under age 73) → No annual RMDs required, but account must be emptied by year 10.

If the person who passed away was already taking RMDs → The beneficiary must continue taking annual RMDs during the 10-year period.

Tax Strategies for Siblings Inheriting Retirement Accounts

This is where planning becomes very important, especially for siblings subject to the 10-year rule.

Strategy for Inherited Pre-Tax IRA or 401(k)

Distributions from inherited pre-tax retirement accounts are taxable income.

If you wait until year 10 and withdraw the entire account at once, that could push you into a very high tax bracket.

So in many cases, it may make sense to:

Take distributions gradually over the 10 years

Spread the tax liability over multiple years

Coordinate withdrawals with lower-income years

Take more in years where income is lower (retirement, job change, etc.)

Strategy for Inherited Roth IRA

If a sibling inherits a Roth IRA and is subject to the 10-year rule:

The account grows tax-free

Withdrawals are tax-free

The strategy is often to wait until year 10 and withdraw the account at the last possible moment to maximize tax-free growth

So the strategy is often:

Pre-tax account → Spread withdrawals out

Roth account → Wait as long as possible

Advanced Tax Strategy: The “Tax Bracket Wash” Strategy

There is also a more advanced strategy for individuals who are still working and inheriting a pre-tax retirement account.

If someone:

Takes a distribution from an inherited IRA (taxable)

Then increases their pre-tax contributions to their employer retirement plan (401(k), 403(b), etc.)

They may be able to offset the taxable income from the inherited IRA distribution with the tax deduction from increasing their pre-tax contributions.

In simple terms, they are:

Taking money out with one hand and putting money back into a retirement account with the other hand, while potentially neutralizing the tax impact.

This can be a very effective strategy for high-income earners who are not already maxing out their employer retirement plans.

Summary

When inheriting a retirement account from a sibling, the most important factor is the age difference between the siblings.

There are two main categories:

If Siblings Are Within 10 Years of Age:

Eligible Designated Beneficiary

Can use the stretch IRA rules

Must take annual RMDs

Do not have to empty the account within 10 years

If Siblings Are More Than 10 Years Apart:

Subject to the 10-year rule

Must empty the account within 10 years

May or may not have to take annual RMDs depending on the age of the sibling who passed away

Because inherited retirement accounts can have significant tax consequences, beneficiaries should strongly consider working with a financial advisor and tax professional to determine the best withdrawal strategy.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions

-

Do siblings have to follow the 10-year rule when inheriting an IRA?Only if they are more than 10 years apart in age.

-

What happens if siblings are within 10 years of age?They can stretch distributions over their lifetime and take RMDs each year.

-

When do RMDs start for stretch rule inherited IRAs?Typically starting the year after the original owner passes away.

-

Do I have to take RMDs if I'm subject to the 10-year rule?It depends on whether the person who passed away had started RMDs.

-

Are inherited IRA distributions taxable?Yes, if it is a pre-tax IRA or 401(k).

-

Are inherited Roth IRA distributions taxable?No, Roth IRA distributions are typically tax-free.

-

Should I take money out each year or wait until year 10?It depends on your tax bracket and whether the account is pre-tax or Roth.

-

What is the stretch IRA rule?It allows beneficiaries to take RMDs over their lifetime instead of emptying the account in 10 years.

-

Can I reduce taxes from an inherited IRA?Yes, by spreading distributions over multiple years, waiting until lower income years to process distributions, or coordinating with retirement plan contributions.

-

Should I talk to a financial advisor about inherited retirement accounts?Yes, because the withdrawal strategy can significantly impact how much tax you pay.

Self-Employment Side Hustle? Benefits of a Solo 401(k) Plan

A Solo 401(k) offers business owners and side hustlers a powerful way to reduce taxable income and accelerate retirement savings. This guide explains contribution limits, tax strategies, and how to choose between pre-tax and Roth contributions in 2026. Learn how to build a tax-efficient retirement plan and potentially eliminate income taxes on self-employment income. Discover why Solo 401(k) plans can outperform SEP IRAs in many cases.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Today, more and more individuals have side hustles in addition to their main W-2 jobs. Others may be full-time business owners but only generate a modest amount of self-employment income. In both cases, one of the most powerful retirement and tax planning tools available is the Solo 401(k) plan.

In this article, we’re going to walk through some of the tax strategies and wealth accumulation strategies we use with clients who have self-employment income and may benefit from a Solo 401(k). Specifically, we’ll cover:

What a Solo 401(k) plan is

How a Solo 401(k) can reduce tax liability

How to use a Solo 401(k) to build a larger Roth bucket

How to decide between pre-tax vs. Roth contributions

What happens when the Solo 401(k) is terminated

What Is a Solo 401(k) Plan?

A Solo(k) plan, also called an Individual(k), is a retirement plan designed for owner-only businesses. This means the business cannot have any full-time employees working more than 1,000 hours per year, other than the owner and possibly their spouse.

Because these plans only cover the business owner, they are typically simple to administer, often have little to no administrative costs, and still provide the full benefits of a traditional 401(k) plan.

Solo 401(k) plans include:

Pre-tax employee deferrals

Roth employee deferrals

Employer contributions

Potential 401(k) loan provisions

Contribution Limits (2026)

Solo 401(k) plans allow for relatively high contribution limits. For 2026:

Employee deferral limit: $24,500 (under age 50)

Age 50+ catch-up: $32,500 total deferral

Employer contribution: Up to 20% of net self-employment income (sole proprietor/partnership)

S-Corp employer contribution: Up to 25% of W-2 wages

Example

Let’s say a sole proprietor generates $40,000 in net self-employment income and is under age 50.

They could contribute:

$24,500 as an employee deferral

$8,000 as an employer contribution (20% of $40,000)

That’s a total of $32,500 going into a retirement account from just $40,000 of side hustle income.

That’s a powerful savings and tax planning opportunity.

Reducing Tax Liability

One of the primary reasons business owners establish Solo 401(k) plans is to reduce their overall tax liability.

If someone has:

W-2 income: $200,000

Self-employment income: $40,000

That self-employment income gets stacked on top of their W-2 income and may be taxed at a high marginal tax rate.

However, if that business owner contributes $30,000 of that $40,000 into a Solo 401(k) using pre-tax contributions, they may only pay income tax on $10,000 instead of the full $40,000.

That can result in significant tax savings.

Solo(K) Plans Can Potentially Eliminate Federal & State Income Taxes

If a business owner has less than the annual employee deferral limit in net income, they may be able to defer 100% of their self-employment income into the Solo 401(k).

Example:

Net self-employment income: $20,000

Employee deferral limit: $24,500

Since the income is lower than the limit, they could defer the entire $20,000 pre-tax, avoiding federal and state income tax on that income.

Note: They still must pay self-employment tax, but they can avoid income tax on that portion.

Building a Larger Roth Bucket

Another major benefit of a Solo 401(k) is the ability to build Roth retirement assets, which can be extremely valuable long-term.

Roth contributions are made after-tax, but:

The money grows tax-deferred

Withdrawals after age 59½ are tax-free

One major advantage of a Roth Solo 401(k) is:

There are no income limits for Roth 401(k) contributions.

This is very important because many high-income earners are phased out of Roth IRA contributions, but they can still contribute to a Roth Solo 401(k).

Example

Imagine a 29-year-old business owner with a side hustle contributing $24,500 per year to a Roth Solo 401(k). The money grows tax-deferred for 30 years and then all of the earning in the account can be withdrawn tax free after age 59½.

We also see this strategy used for retirees who do consulting work. If someone is 65+ and earning self-employment income but doesn’t need the income, they can contribute to a Roth Solo 401(k) and move that money into a tax-free growth bucket instead of a taxable brokerage account.

This can be a powerful long-term tax strategy regardless of age of the business owner.

To Roth or Not to Roth?

Remember, there are two types of contributions to a Solo 401(k):

1. Employee Deferral → Can be Pre-Tax or Roth

2. Employer Contribution → Typically Pre-Tax

For sole proprietors and partnerships:

Employer contribution = 20% of net earned income

For S-Corps:

Employer contribution = 25% of W-2 wages

Important: Only W-2 wages count — not S-Corp distributions

While SECURE Act 2.0 opened the door for Roth employer contributions, we are still waiting on full IRS guidance for this to be widely implemented in Solo 401(k) plans. So for now, employer contributions are generally still pre-tax, while employee deferrals can be Roth or pre-tax.

General Rule of Thumb

You might consider:

Pre-tax contributions if you are in a high tax bracket today

Roth contributions if you are in a lower tax bracket today or want tax-free income later

This is where tax planning and coordination with a financial advisor and CPA becomes very important.

What Happens When the Solo 401(k) Is Terminated?

Eventually, the self-employment income may stop. When that happens, the Solo 401(k) is typically terminated, and the assets are rolled into IRAs.

Typically:

Pre-tax Solo 401(k) money → Traditional IRA

Roth Solo 401(k) money → Roth IRA

The money can then continue growing in those IRA accounts, and the Solo 401(k) plan is closed.

Working With an Advisor Who Understands Solo 401(k) Plans

Solo 401(k) plans are extremely powerful, but there are important rules and nuances business owners must be aware of.

For example:

If you hire employees, you may have to discontinue the plan

Plan documents must be set up properly

Once plan assets exceed $250,000, you must file Form 5500 annually

There are coordination issues between your CPA and financial advisor

You must choose between pre-tax vs. Roth strategies

You must compare Solo 401(k) vs. SEP IRA vs. SIMPLE IRA

Because of these moving parts, it’s important to work with an advisor who understands how to design and manage Solo 401(k) plans properly as part of an overall financial and tax strategy.

Our firm offers free consultations for business owners and individuals with side hustle income who want to evaluate whether a Solo 401(k) plan makes sense for their situation. If you’d like help determining whether this strategy is right for you, we’d be happy to help you build a plan around your specific goals. Feel free to schedule your complementary consult via our website.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions About Solo 401(k) Plans

-

Who qualifies for a Solo 401(k)?Business owners with no full-time employees working more than 1,000 hours per year.

-

Can I have a W-2 job and a Solo 401(k)?Yes. As long as you have self-employment income, you can open a Solo 401(k) for that income.

-

How much can I contribute to a Solo 401(k)?In 2026, employee deferrals are $24,500 (under 50), plus employer contributions up to 20% of income (or 25% of W-2 wages for S-Corps).

-

Can I contribute 100% of my side hustle income?Yes, if your income is below the employee deferral limit, you may be able to defer the entire amount.

-

Do Solo 401(k) contributions reduce taxes?Yes, pre-tax contributions reduce your taxable income.

-

Can I make Roth contributions to a Solo 401(k)?Yes, employee deferrals can be Roth, with no income limits.

-

What happens when I stop my side hustle?The Solo 401(k) is typically rolled into a Traditional IRA and/or Roth IRA.

-

Is a Solo 401(k) better than a SEP IRA?In many cases, yes, because it allows Roth contributions and higher contributions at lower income levels.

-

Do I have to file anything for a Solo 401(k)?Once the account exceeds $250,000, you must file Form 5500 annually.

-

Can I take a loan from a Solo 401(k)?Some Solo 401(k) plans allow participant loans, similar to traditional employer 401(k) plans.

What Causes the Price of Gold to Go Up and Down?

Gold prices are influenced by several key factors, including interest rates, inflation, and the strength of the U.S. dollar. While gold is often viewed as a safe haven, it can be highly volatile and may not perform as well as stocks over the long term. This article explains what causes gold to rise and fall, how it compares to other commodities, and how it can be used for diversification. Understanding these drivers can help investors make more informed decisions about including gold in their portfolio.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Over the last few years, gold has experienced a significant rally, followed by periods of sharp volatility—including some recent price declines that have caught investors’ attention. As a result, we’ve been having more frequent conversations with clients about what actually causes gold prices to rise and fall, and whether a recent dip represents an opportunity or a warning sign.

In this article, we’re going to walk through the same conversations we’ve been having with clients and explain the major variables that impact the price of gold. Specifically, you’ll learn:

Why gold is often viewed as a safe haven

How the value of the U.S. dollar affects gold prices

Why interest rates play a major role in gold movements

Whether gold is a good long-term investment

How gold compares to other commodities like silver, copper, and platinum

How gold can fit into a diversified portfolio

Gold as a Safe Haven

Gold is often referred to as a “safe haven” asset. What that means is when there is volatility in the global economy—or sometimes in the U.S. stock market—investors may sell riskier assets like stocks and move money into gold in an attempt to protect their principal.

In certain periods in history, this strategy has worked well. When markets become unpredictable, gold can hold its value or even increase while stocks are falling.

However, investors need to be careful with the idea of gold as a safe haven. While gold is sometimes viewed as a “safer” asset than stocks, it is still a very volatile asset class. It is not unusual for gold to move more than 10% in a short period of time. That’s a big difference compared to bonds, which are also considered conservative investments but typically experience much smaller price swings over short time periods.

So while gold can sometimes be a successful safe haven during global volatility, investors must remember that gold itself can be volatile. It should be viewed as a portfolio diversifier, not a guaranteed protection strategy.

Inverse Relationship to the Value of the Dollar

Historically, gold has had an inverse relationship with the value of the U.S. dollar.

In simple terms:

When the dollar goes down, gold tends to go up

When the dollar goes up, gold tends to go down

Why does this happen?

If paper currency is losing value (purchasing power), investors often move money into physical assets like gold to preserve wealth. Gold is viewed as a store of value that cannot be printed or created like paper money.

On the flip side, when the dollar is strengthening and purchasing power is increasing, investors may feel less need to hold gold, which can lead to falling gold prices.

So historically speaking, movements in the dollar are one of the biggest drivers of gold prices.

Interest Rate Fluctuations

Interest rates are another major factor that influences gold prices, largely because of their relationship with the value of the dollar.

Typically:

When the Federal Reserve lowers interest rates, the dollar often weakens, and gold may rise

When the Federal Reserve raises interest rates, the dollar often strengthens, and gold may fall

One of the primary reasons attributed to gold's rapid appreciation over the last year was due to interest rates coming down, which weakened the dollar and pushed gold prices higher.

Looking forward, if inflation continues to cool and interest rates decline later into 2026 (outside of the recent Iran events), gold could recover much of what was lost in recent weeks. However, investors must also be aware of long-term inflation risks. If inflation rises again and the Federal Reserve is forced to increase interest rates, that could strengthen the dollar and become a major headwind for gold prices.

In many ways, rising interest rates can be one of the biggest enemies of gold.

Gold as a Long-Term Investment

When we look at long-term annualized returns, gold has not historically been a great long-term investment compared to stocks. Over 20- and 30-year periods, the S&P 500 has outperformed gold.

However, that does not mean gold has no place in a portfolio.

Gold can be useful for:

Diversification

Protection during market volatility

Hedging against a declining dollar

Hedging against certain inflationary environments

Gold tends to have lower correlation to stocks and bonds, which means it doesn’t always move in the same direction as traditional investments. Because of that, gold can be a useful component within a diversified portfolio, but investors should be cautious about allocating too much to gold due to its volatility and lower long-term expected returns compared to equities.

Gold Compared to Other Commodities

Clients will often ask: why gold instead of silver, platinum, or copper?

The main reason is predictability.

Gold is primarily viewed as a store of wealth. Its price is largely influenced by:

The value of the dollar

Interest rates

Inflation

Global uncertainty

Central bank policies

However, other metals like silver, platinum, and copper have significant industrial uses. That means their prices are influenced not just by currency and global events, but also by:

Manufacturing demand

Technology demand

Construction activity

Supply chain issues

More variables typically mean more unpredictable price movements.

There are years when gold performs very well and other metals do not, and there are also years where metals like copper or silver outperform gold. In investment management, we often give extra weight to assets that are easier to analyze and understand.

Special Disclosure

This article is meant to educate investors on the price fluctuations in gold based on our experience in investment management over the past number of years. This is not a recommendation to buy or sell gold or any other commodity. Every investor’s situation is different, and decisions should be made based on your individual financial plan, time horizon, and risk tolerance.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions About Gold

-

Why does gold go up when the market goes down?Gold is often viewed as a safe haven, so investors sometimes move money into gold during stock market volatility.

-

What is the biggest factor that affects gold prices?The value of the U.S. dollar and interest rates are two of the biggest drivers of gold prices.

-

Does gold go up when inflation rises?Often it does, because gold is viewed as a store of value when purchasing power declines.

-

Why does gold fall when interest rates rise?Rising interest rates typically strengthen the dollar, which historically puts downward pressure on gold.

-

Is gold a good long-term investment?Historically, stocks have outperformed gold over long periods, but gold can still be useful for diversification.

-

Is gold safer than stocks?Not necessarily, gold is still a very volatile asset class.

-

Why not invest in silver or copper instead of gold?Those metals have industrial uses, which makes their prices more unpredictable compared to gold.

-

How much gold should be in a portfolio?It depends on the investor, but many diversified portfolios only allocate a small percentage to gold (under 15%).

-

What causes gold to drop quickly?A rising dollar, rising interest rates, or reduced global uncertainty can all cause gold prices to fall.

-

Is a drop in gold a buying opportunity?It depends on the reason for the drop. Investors should look at interest rates, the dollar, and global conditions before making a decision.