2023 RMDs Waived for Non-spouse Beneficiaries Subject To The 10-Year Rule

There has been a lot of confusion surrounding the required minimum distribution (RMD) rules for non-spouse, beneficiaries that inherited IRAs and 401(k) accounts subject to the new 10 Year Rule. This has left many non-spouse beneficiaries questioning whether or not they are required to take an RMD from their inherited retirement account prior to December 31, 2023. Here is the timeline of events leading up to that answer

There has been a lot of confusion surrounding the required minimum distribution (RMD) rules for non-spouse beneficiaries who inherited IRAs and 401(k) accounts subject to the new 10-Year Rule. This has left many non-spouse beneficiaries questioning whether or not they are required to take an RMD from their inherited retirement account prior to December 31, 2023. Here is the timeline of events leading up to that answer:

December 2019: Secure Act 1.0

In December 2019, Congress passed the Secure Act 1.0 into law, which contained a major shift in the distribution options for non-spouse beneficiaries of retirement accounts. Prior to the passing of Secure Act 1.0, non-spouse beneficiaries were allowed to move these inherited retirement accounts into an inherited IRA in their name, and then take small, annual distributions over their lifetime. This was referred to as the “stretch option” since beneficiaries could keep the retirement account intact and stretch those small required minimum distributions over their lifetime.

Secure Act 1.0 eliminated the stretch option for non-spouse beneficiaries who inherited retirement accounts for anyone who passed away after December 31, 2019. The stretch option was replaced with a much less favorable 10-year distribution rule. This new 10-year rule required non-spouse beneficiaries to fully deplete the inherited retirement account 10 years following the original account owner’s death. However, it was originally interpreted as an extension of the existing 5-year rule, which would not require the non-spouse beneficiary to take annual RMD, but rather, the account balance just had to be fully distributed by the end of that 10-year period.

2022: The IRS Adds RMDs to the 10-Year Rule

In February 2022, the Treasury Department issued proposed regulations changing the interpretation of the 10-year rule. In the proposed regulations the IRS clarified that RMDs would be required for select non-spouse beneficiaries subject to the 10-year rule, depending on the decedent’s age when they passed away. Making some non-spouse beneficiaries subject to the 10-year rule with no RMDs and others subject to the 10-year rule with annual RMDs.

Why the change? The IRS has a rule within the current tax law that states that once required minimum distributions have begun for an owner of a retirement account the account must be depleted, at least as rapidly as a decedent would have, if they were still alive. The 10-year rule with no RMD requirement would then violate that current tax law because an account owner could be 80 years old, subject to annual RMDs, then they pass away, their non-spouse beneficiary inherits the account, and the beneficiary could voluntarily decide not to take any RMDs, and fully deplete the account in year 10 in accordance with the new 10-year rule. So, technically, stopping the RMDs would be a violation of the current tax law despite the account having to be fully depleted within 10 years.

In the proposed guidance, the IRS clarified, that if the account owner had already reached their “Required Beginning Date” (RBD) for required minimum distributions (RMD) while they were still alive, if a non-spouse beneficiary, inherits that retirement account, they would be subject to both the 10-year rule and the annual RMD requirement.

However, if the original owner of the IRA or 401k passes away prior to their Required Beginning Date for RMDs since the RMDs never began if a non-spouse beneficiary inherits the account, they would still be required to deplete the account within 10 years but would not be required to take annual RMDs from the account.

Let’s look at some examples. Jim is age 80 and has $400,000 in a traditional IRA, and his son Jason is the 100% primary beneficiary of the account. Jim passed away in May 2023. Since Jason is a non-spouse beneficiary, he would be subject to the 10-year rule, meaning he would have to fully deplete the account by year 10 following the year of Jim’s death. Since Jim was age 80, he would have already reached his RMD start date, requiring him to take an RMD each year while he was still alive, this in turn would then require Jason to continue those annual RMDs during that 10-year period. Jason’s first RMD from the inherited IRA account would need to be taken in 2024 which is the year following Jim’s death.

Now, let’s keep everything the same except for Jim’s age when he passes away. In this example, Jim passes away at age 63, which is prior to his RMD required beginning date. Now Jason inherits the IRA, he is still subject to the 10-year rule, but he is no longer required to take RMDs during that 10-year period since Jim had not reached his RMD required beginning date at the time that he passed.

As you can see in these examples, the determination as to whether or not a non-spouse beneficiary is subject to the mandatory RMD requirement during the 10-year period is the age of the decedent when they pass away.

No Final IRS Regs Until 2024

The scenario that I just described is in the proposed regulations from the IRS but “proposed regulations” do not become law until the IRS issues final regulations. This is why we advised our clients to wait for the IRS to issue final regulations before applying this new RMD requirement to inherited retirement accounts subject to the 10-year rule.

The IRS initially said they anticipated issuing final regulations in the first half of 2023. Not only did that not happen, but they officially came out on July 14, 2023, and stated that they would not issue final regulations until at least 2024, which means non-spouse beneficiaries of retirement accounts subject to the 10-year rule will not face a penalty for not taking an RMD for 2023, regardless of when the decedent passed away.

Heading into 2024 we will once again have to wait and see if the IRS comes forward with the final regulations to implement the new RMDs rules outlined in their proposed regs.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Requesting FICA Tax Refunds For W2 Employees With Multiple Employers

If you are a W2 employee who makes over $160,200 per year and you have multiple employers or you switched jobs during the year, or you have both a W2 job and a self-employment gig, your employer(s) may be withholding too much FICA tax from your wages and you may be due a refund of those FICA tax overpayments. Requesting a FICA tax refund requires action on your part and an understanding of how the FICA tax is calculated.

If you are a W2 employee who makes over $176,100 per year in 2025 and you have multiple employers or you switched jobs during the year, or you have both a W2 job and a self-employment gig, your employer(s) may be withholding too much FICA tax from your wages and you may be due a refund of those FICA tax overpayments. Requesting a FICA tax refund requires action on your part and an understanding of how the FICA tax is calculated.

How is FICA Tax Calculated

If you are a W2 employee, you will see a FICA deduction on your paychecks, which stands for Federal Insurance Contributions Act. The FICA tax is the funding vehicle for the Medicare and Social Security programs in the U.S. The 7.65% FICA tax consists of 6.2% for Social Security and 1.45% for Medicare, but the 6.2% allocated to Social Security has a cap, which means the government only assesses the 6.2% tax up to a specified wage limit each year. That wage limit is called the “taxable wage base,” and for 2025, the taxable wage base is $176,100. Any income up to the $176,100 taxable wage base is assessed the full 7.65% FICA tax, and any amounts over the taxable wage base are just assessed the 1.45% for Medicare since the Medicare tax does not have a cap.

Note: The IRS taxable wage base usually increases each year.

Employees with Multiple Employers During The Same Tax Year

For employees who work for more than one company during the year and whose total wages are over the $176,100 taxable wage base, this can cause an over-withholding of FICA tax from their wages.

Example: Sue is a doctor employed by XYZ Hospital and earns $150,000 between January and August, then Sue accepts a new position with ABC Hospital and earns $100,000 between September and December. Both XYZ Hospital and ABC Hospital will withhold the full 7.65% in FICA tax from Sue’s paycheck because she was below the taxable wage base of $176,100 with each employer. But Sue is only required to pay the 6.2% Social Security portion of the FICA tax up to $176,100 in wages, so she has too much paid into FICA for the year.

XYZ Hospital SS 6.2% x $150,000 = $9,300

ABC Hospital SS 6.2% x $100,000 = $6,200

Total SS FICA Actually Withheld: $15,500

Annual Limit: SS 6.2% x Taxable Wage Base $176,100 = $10,918.20

Sue’s FICA tax was over-withheld by $4,581.80 for the year. So, how does she get that money back from the IRS?

Requesting a FICA Tax Refund (Multiple Employers)

A refund of the excess FICA tax does not automatically occur. In the example above, if Sue identifies the FICA over withholding prior to filing her taxes for the year, she can recapture the excess withholding when she prepares her tax return (1040) for that tax year. The excess FICA withholding is applied as if it were excess federal income tax withholding.

If Sue does not identify the FICA excess withholding until after she has filed her taxes for the year, she could file IRS Form 843 to recover the excess FICA withholding. Thankfully, it’s a very easy tax form to complete. Timing-wise, it may take the IRS 3 to 4 months to review and process your FICA tax refund.

Requesting A FICA Tax Refund (Single Employer)

The FICA tax refund process is slightly different for individuals who have only one employer. Payroll mistakes will sometimes happen, causing an employer to over-withhold FICA taxes from an employee’s wages. In these cases, the IRS requires you first to try to resolve the FICA excess withholding with your employer before submitting Form 843. If resolving the FICA excess withholding is unsuccessful with your employer, you can file Form 843.

Self-Employed FICA Tax Refund

For individuals who have both a W2 job and are also self-employed they can also experience these FICA overpayment situations. Self-employed individuals pay both the employee portion of the FICA 7.65% and the employer portion of FICA 7.65%, for a total of 15.3% on their self-employment income up to the taxable wage base.

For self-employed individuals who are either sole proprietors or partners in a partnership or LLC, they typically do not have wages, so there is no direct FICA withholding as there is with W2 employees. Self-employed individuals make estimated tax payments four times a year to cover both their estimated FICA and income tax liability. If these individuals end up in a FICA overpayment situation due to W2 wages outside of their self-employment income, the overpayment can be applied toward their tax liability for the year or result in a refund from their self-employment income. They typically do not need to file IRS Form 843.

Note: S-Corp owners do have W2 wages

Requesting A Reduction In FICA Withholding

For employees that are in this two-employer situation, and they know they are going to have W2 wages over the taxable wage base, in a perfect world, they would be allowed to submit a request to one of their employers to either reduce or eliminate the social security portion of their FICA withholding to avoid the over withholding during the tax year. However, this is not allowed. Each employer is responsible for withholding the full 7.65% in FICA tax from the employee’s pay up to the taxable wage base, and this approach makes sense because each individual employer has no way of knowing what you earned in W2 wages at your other employers during the year.

3-Year Status of Limitations

If you are reading this article now, but you realize you have had excess FICA withholding for the past few years without requesting a refund, the IRS allows you to go back 3 years to request a refund of those excess FICA withholdings. Anything over 3 years back and you are out of luck, the U.S. government thanks you for your additional donations to Social Security and Medicare trusts.

The Employer Does Not Get A Refund

FICA tax is paid by both the employee and the employer:

Employee Social Security: 6.2%

Employer Social Security: 6.2%

Employee Medicare: 1.45%

Employer Medicare: 1.45%

Total FICA EE & ER: 15.3%

So if the employee works for 2 different companies, they have combined wages over the $176,100 taxable wage base, making them eligible for a FICA refund for the 6.2% of social security tax on wages paid over the wage base, does the EMPLOYER also get a refund for those excess FICA withholdings?

The answer, unfortunately, is “No”.

If an employee works for 10 different companies and makes $100,000 in W2 wages with each company, each of those 10 employers would withhold the full FICA tax from that employee’s $100,000 in W2 wages, but since the employee had $1,000,000 in combined wages, they would be due a $51,081.80 refund in FICA wages ($1M - $176,100 x 6.2%). However, the government keeps that full 6.2% that was paid in by each of the 10 employers with no refund due to any of the companies.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What is the FICA tax and how is it calculated?

FICA stands for the Federal Insurance Contributions Act and funds Social Security and Medicare. Employees pay 7.65% of their wages—6.2% for Social Security (up to the annual wage base limit of $176,100 for 2025) and 1.45% for Medicare, which has no wage cap.

Why might someone have excess FICA tax withheld?

Over-withholding often happens when a person works for multiple employers in the same year or switches jobs. Since each employer must withhold FICA up to the wage base limit independently, total Social Security tax paid across employers may exceed the annual maximum.

How can you request a refund for excess FICA tax?

If you have multiple employers and your total wages exceed the Social Security wage base, you can claim the excess FICA withheld as a credit on your tax return (Form 1040). If the overpayment is discovered after filing, you can request a refund by submitting IRS Form 843.

What if the over-withholding happened with only one employer?

When a single employer over-withholds FICA tax, you must first request reimbursement directly from that employer. If the issue is not resolved, you can then file IRS Form 843 to request a refund from the IRS.

How does FICA apply to self-employed individuals?

Self-employed individuals pay both the employee and employer portions of FICA—15.3% total—on net self-employment income up to the taxable wage base. If they also earn W2 wages that cause FICA overpayment, the excess can be credited or refunded when filing their tax return without using Form 843.

Can you ask an employer to stop withholding Social Security tax once you reach the wage limit?

No. Each employer is required by law to withhold FICA taxes on wages up to the annual wage base, even if you exceed the limit when combining income from multiple employers. Any overpayment can only be refunded through the tax filing process.

How far back can you request a FICA refund?

You can claim a refund for FICA overpayments made within the last three years. Refund claims for tax years older than three years are no longer eligible.

Do employers receive a refund for overpaid FICA taxes?

No. The FICA refund applies only to the employee’s portion of Social Security tax. Employers cannot recover their share of FICA contributions, even if an employee earns more than the wage base across multiple jobs.

Fewer 401(k) Plans Will Require A 5500 Audit Starting in 2023

401(K) plans with over 100 eligible plan participants are considered “large plans” in the eyes of DOL and require an audit to be completed each year with the filing of their 5500. These audits can be costly, often ranging from $8,000 - $30,000 per year.

Starting in 2023, there is very good news for an estimated 20,000 401(k) plans that were previously subject to the 5500 audit requirement. Due to a recent change in the way that the DOL counts the number of plan participants for purposes of assessing a large plan filer status, many plans that were previously subject to a 401(k) audit, will no longer require a 5500 audit for plan year 2023 and beyond.

401(K) plans with over 100 eligible plan participants are considered “large plans” in the eyes of DOL and require an audit to be completed each year with the filing of their 5500. These audits can be costly, often ranging from $8,000 - $30,000 per year.

Starting in 2023, there is very good news for an estimated 20,000 401(k) plans that were previously subject to the 5500 audit requirement. Due to a recent change in the way that the DOL counts the number of plan participants for purposes of assessing a large plan filer status, many plans that were previously subject to a 401(k) audit, will no longer require a 5500 audit for plan year 2023 and beyond.

401(K) 5500 Audit Requirement

A little background first on the audit rule: if a company sponsors a 401K plan and they have 100 or more participants at the beginning of the year, that plan is now considered a “large plan”, and the plan is required to submit an audit report with their annual 5500 filings.

For plans that are just above the 100 plan participant threshold, the DOL provides some relief in the “80 – 120 rule”, which basically states that if the plan was a “small plan” filer in the previous year, the plan can remain a small plan filer until the plan participant count reaches 121.

Old Plan Participant Count Method

Not all employees count toward the 100 or 121 audit threshold. Under the old rules, the company only had to count employees who were:

Eligible to participate in the plan; and

Terminated employees with a balance still in the plan

But under the older rules, ALL plan-eligible employees had to be counted whether or not they had a balance in the plan. For example, if a landscaping company had:

150 employees

95 employees are eligible to participate in the plan

Of the 95 eligible employees, 27 employees have balances in the 401(K) plan

35 terminated employees with a balance still in the plan

Under the 2022 audit rules, this plan would be subject to the 5500 audit requirement because they had 95 eligible plan participants PLUS 35 terminated employees with balances, bringing the plan participant audit count to 130, making them a “large plan” filer. A local accounting firm might charge $10,000 for the plan audit each year.

New Plan Participant Count Method

Starting in 2023, the way that the DOL counts plan participants to determine “large plan” filer status changed. Now, instead of counting all eligible plan participants whether or not they have a balance in the plan, starting in 2023, the DOL will only count:

Eligible employees that HAVE A BALANCE in the plan

Terminated employees with balances still in the plan

Looking at the same landscaping company in the previous example:

150 employees

95 employees are eligible to participate in the plan

Of the 95 eligible employees, 27 employees have balances in the 401(K) plan

35 terminated employees still have balances in the plan

Under the new DOL rules, this 401(K) plan would no longer require a 5500 audit because they only have to count the 27 eligible employees WITH BALANCES in the plan and the 35 terminated employees with balances, bringing the total employee audit count to 62. The plan would be allowed to file as a “small plan” starting in 2023 and would no longer have to incur the $10,000 cost for the 5500 audit each year.

20,000 Fewer 401(k) Plans Requiring An Audit

The DOL expects this change to eliminate the 5500 audit required for approximately 20,000 401(k) plans. The primary purpose of this change is to encourage more companies that do not already offer a 401(k) plan to their employees to adopt one and to lower the annual cost for many companies that would otherwise be subject to a 5500 audit requirement.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What triggers a 401(k) audit requirement?

A 401(k) plan is required to undergo an annual audit if it has 100 or more participants at the beginning of the plan year. This audit, submitted with Form 5500, verifies the accuracy of plan financials and compliance with Department of Labor (DOL) rules.

What is the “80–120 rule” for 401(k) plans?

The DOL’s 80–120 rule allows a plan that filed as a “small plan” in the prior year to continue filing as a small plan until the participant count reaches 121. This provides flexibility and prevents plans hovering around 100 participants from needing frequent audit changes.

How did the DOL change the participant counting method in 2023?

Before 2023, all employees eligible to participate in the 401(k) plan were counted toward the 100-participant threshold, even if they had no account balance. Beginning in 2023, only employees with a balance in the plan—either active or terminated—are counted.

How does the new rule affect which plans need an audit?

Under the new counting method, many plans with numerous eligible but non-participating employees will now fall below the 100-participant threshold. This change means fewer employers will need to complete costly annual audits.

How much can companies save due to the new participant count rule?

A 401(k) audit typically costs between $8,000 and $30,000 per year. By no longer requiring audits for certain plans, the DOL estimates that about 20,000 employers will save these expenses annually.

Why did the DOL change the audit threshold calculation?

The change aims to reduce administrative costs and encourage more small and mid-sized employers to establish 401(k) plans. Lowering the financial burden of compliance helps increase access to workplace retirement savings programs.

So Where Is The Recession?

Toward the end of 2022 and for the first half of this year, many economics and market analysts were warning investors of a recession starting within the first 6 months of 2023. Despite those widespread warnings, the S&P 500 Index is up 16% YTD as of July 3, 2023, notching one of the strongest 6-month starts to a year in history. So why have so many people been wrong about their prediction and off by so much?

Toward the end of 2022 and for the first half of this year, many economists and market analysts were warning investors of a recession starting within the first 6 months of 2023. Despite those widespread warnings, the S&P 500 Index is up 16% YTD as of July 3, 2023, notching one of the strongest 6-month starts to a year in history. So why have so many people been wrong about their prediction and off by so much?

The primary reason is that the U.S. economy and the U.S. stock market are telling us two different stories. The U.S. stock market seems to be telling the story that the worst is behind us, inflation is coming down, and we are at the beginning of a renewed economic growth cycle fueled by the new A.I. technology. But the U.S. economy is telling a very different story. The economic data suggests that the economy is slowing down quickly, higher interest rates are taking their toll on bank lending, the consumer, commercial real estate, and many of the economic indicators that have successfully forecasted a recession in the past are not only flashing red but have become progressively more negative over the past 6 months despite the rally in the stock market.

So are the economists that predicted a recession this year wrong or just early? In this article, we will review both sides of the argument to determine where the stock market may be heading in the second half of 2023.

The Bull Case

Let’s start off by looking at the bull case making the argument that the worst is behind us and the stock market will continue to rally from here.

Strong Labor Markets

The bulls will point to the strength of the U.S. labor market. Due to the shortage of workers in the labor market, companies are still desperate to find employees to hire, and even companies that have experienced a slowdown within the last 6 months are reluctant to layoff employees for fear that they will not be able to hire them back if either a recession is avoided or if it’s just a mild recession.

I agree that the labor market environment is different than previous market cycles, as a business owner myself, I cannot remember the last time it was this difficult to find qualified employees to hire. From the research that we have completed, the main catalyst of this issue stems from a demographic issue within the U.S. labor force. It’s the simple fact that there are a lot more people in the U.S. ages 50 to 70 than there are people ages 20 – 40. You have people retiring in droves, dropping out of the workforce, and there are just not enough people to replace them.

The bulls are making the case that because of this labor shortage, the unemployment rate will remain low, the consumer will retain their spending power, and a recession will be avoided.

Inflation is Dropping Fast

The main risk to the economy over the past 18 months has been the rapid rise in inflation. The bulls will highlight that not only has the inflation dropped but it has dropped quickly. Inflation peaked in June 2022 at around 9% and as of May 2023, the inflation rate has dropped all of the way down to 4% with the Fed’s target at 2% - 3%. The inflation battle is close to being won. As a result of the rapid drop in inflation, the Fed made the decision to pause as opposed to raising the Fed Fund Rate at their last meeting, which is also welcomed news for bullish investors since avoiding additional interest rate hikes and shifting the discussion to Fed Fund rate cuts could eliminate some of the risks of a Fed-induced recession.

The Market Has Already Priced In The Recession

Some bulls will argue that the stock market has already priced in a mild recession which is the reason why the S&P 500 Index was down 19% in 2022, so even if we end up in a recession, the October 2022 market lows will not be retested. Also, since the market was down in 2022, historically it’s a rare occurrence that the market is down two years in a row.

The Bear Case

Now let’s shift gears over to the bear case that would argue that while a recession has not surfaced yet, there are numerous economic indicators that would suggest that there is a very high probability that the U.S. economy will enter a recession within the next 12 months. Full disclosure, we are in this camp and we have been in this camp since December 2021. Admittedly, I am surprised at the “magnitude” of the rally this year but not necessarily surprised at the rally itself.

Bear Market Rallies Are Common

Rarely does the stock market fire a warning shot and then proceed to enter a recession. Historically, it is more common that the stock market experiences what we call a “false rally”, right before the stock market wakes up to the fact that the economy is headed for a recession, followed by a steep selloff but there is always a bull market case that exists that investors want to believe.

The last real recession that we had was the 2008 housing crisis and while investors remember how painful that recession was for their investment accounts, they typically don’t remember what was happening prior to the recession beginning. Leading into the 2008/2009 recession, the S&P 500 Index had rallied 12%, the housing market issues were beginning to surface, but there was still a strong case for a soft landing as the Fed paused interest rate hikes, and began decreasing the Fed Funds Rate at the beginning of 2008, but as we know today the Great Recession occurred anyways.

The Fed Has Never Delivered A Soft Landing

While there is talk of a soft landing with no recession, if you look back in history, anytime the Fed has had to reduce the inflation rate by more than 2%, the Fed rate hike cycle has been followed by a recession every single time. As I mentioned above, the inflation rate peaked at 9% and their target is 2% - 3% so they have to bring down the inflation rate by much more than 2%. If they pull off a soft landing with no recession, it would be the first time that has ever happened.

The Market Bottom

For the bulls that argue that the market is expecting a mild recession and has already priced that in, that would also be the first time that has ever happened. If you look back at the past 9 recessions, how many times in the past 9 recessions did the market bottom PRIOR to the recession beginning? Answer: Zero. In each of the past 9 recessions, the market bottomed at some point during the recession but not before it.

Also, the historical P/E ratio of the S&P 500 Index is a 17. P/E ratios are a wildly used metric to determine whether an investment or index is undervalued, fairly valued, or overvalued. As I write this article on July 3, 2023, the forward P/E of the S&P 500 Index is 22 so the stock market is already arguably overvalued or as others might describe it as “priced to perfection”. So not only is the stock market priced for no recession, it’s priced for significant earnings growth from the companies that are represented within the S&P 500 Index.

A Rally Fueled by 6 Tech Companies

The S&P 500 Index, the stock market, is comprised of 500 of the largest publicly traded companies in the U.S. The S&P Index is a “cap-weighted index” which means the larger the company, the larger the impact on the direction of the index. Why does this matter? In 2023, many of the big tech companies in the U.S. have rallied substantially on the back of the artificial intelligence boom.

As of June 2, 2023, the S&P 500 Index was up 11.4% YTD, and at that time Nvidia one of the top ten largest companies in the S&P 500 was up 171%, Amazon up 49%, Google up 41%. If instead you ignored the size of the companies in the S&P 500 Index and gave equal weight to each of the 500 companies that make up the stock index, the S&P 500 Index would have only been up 1.2% YTD as of June 2, 2023. So this has not been what we consider a broad rally where most of the companies are moving higher. (Data Source for this section: Reuters)

Why is this important? In a truly sustainable growth environment, we tend to see a broad market rally where a large number of companies within the index see a meaningful amount of appreciation and just doesn’t seem to be the case with the stock market rally this year.

2 Predictors of Coming Recessions

There are two economic indicators that have historically been very good at predicting recessions; the yield curve and the Leading Economic Indicators Index. Both started the year flashing red warning signals and despite the stock market rally so far this year, both indicators have moved even more negative within the first 6 months of 2023.

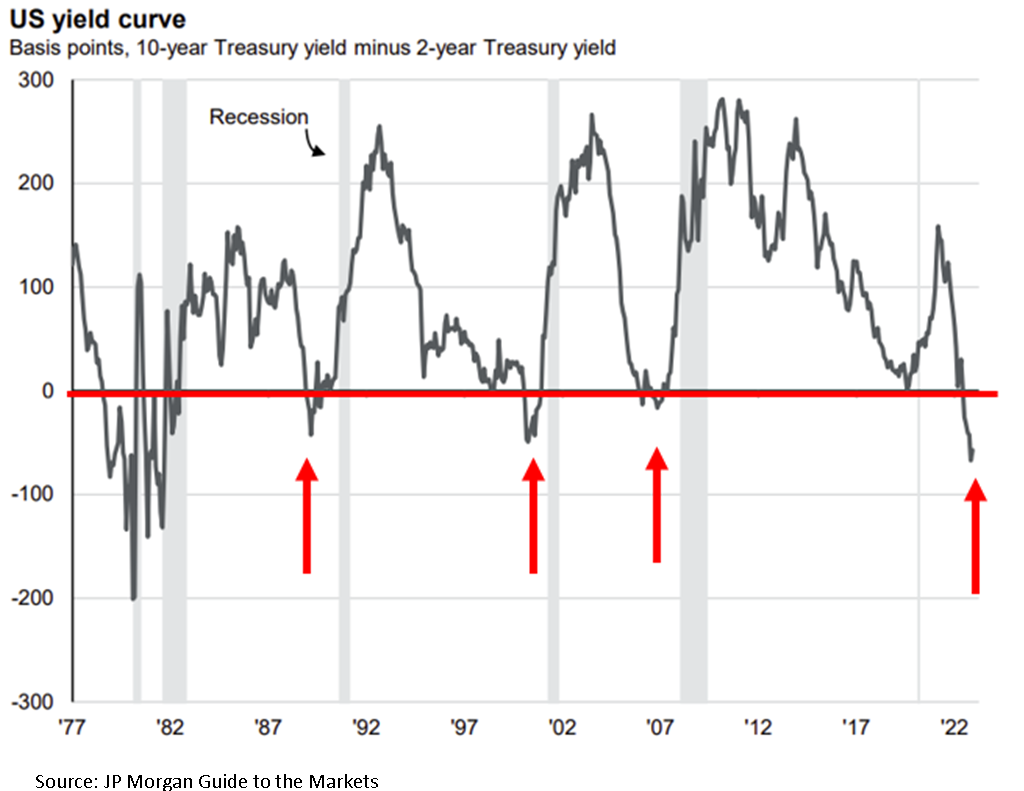

Inverted Yield Curve

The yield curve right now is inverted which historically is a very accurate predictor of a coming recession. Below is a chart of the yield curve going back to 1977, anytime the grey line moved below the red line in the chart, the yield curve is inverted. As you can see, each time the yield curve inverts it’s followed by a recession which are the grey shaded areas within the graph. On the far right side of the chart is where we are now, heavily inverted. If we don’t get a recession within the next 12 months, it would be the first time ever that the yield curve was this inverted and a recession did not occur.

The duration of the inversion is also something to take note of. As of July 2, 2023 the yield curve has been inverted for 159 trading days, since 1962 the longest streak that the yield curve was inverted was 209 trading days ending May 2008 (the beginning of the Great Recession). If the current yield curve stays inverted until mid-September, which is likely, it will break that record.

Leading Economic Indicators Index (LEI Index)

The Leading Economic Indicators index is the second very accurate predictor of a coming recession because as the name suggests the index is comprised of forward-looking economic data including but not limited to manufacturing hours works, building permits, yield curve, consumer confidence, and weekly unemployment claims. The yield curve is a warning from the bond market and the LEI index is a warning from the U.S. economy.

In the chart below, when the blue drops below the red line (where the red arrows are) the LEI index has turned negative, indicating that the forward-looking economic indicators in the U.S. economy are slowing down. The light grey areas are the recessions. As you can see in the chart, shortly after the LEI index goes negative, historically a recession appears shortly after. If you look at where are now on the righthand side of the chart, not only are we negative on the LEI, but we have never been this negative without already being in a recession. Again, if we don’t get a recession within the next 12 months, it would be the first time ever that this indicator did not accurately predict a recession at its current level.

“Well…..This Time It’s Different”

A common phrase that you will hear from the bulls right now is “well…..this time is different” followed by a list of all the reasons why the yield curve, LEI index, and other indicators that are flashing red are no longer a creditable predictor of a coming recession. After being in the investment industry for over 20 years and experiencing the tech bubble bust, housing crisis, Eurozone crisis, and Covid, from my experience, it’s rarely different which is why these predictors of recessions have been so accurate over time. Yes, the market environment is not exactly the same in each time period, sometimes there is a house crisis, other times an energy crisis, or maybe a pandemic, but the impact that monetary policy and fiscal policy have on the economy tend to remain constant over longer periods of time.

Market Timing

It’s very difficult to time the market. I would love to be able to know exactly when the market was peaking and bottoming in each market cycle but the stock market itself throws off so many false readings that become traps for investors. While we rely more heavily on the economic indicators because they have a better track record of predicting market outcomes over the long term, the timing is never spot on but what I have learned over time is that if you are able to sidestep the recessions, and avoid the big 25%+ downturns in an investment portfolio, it often leads to greater outperformance over the long term. Remember, mathematically, if your portfolio drops by 50%, you have to earn a 100% rate of return to get back to breakeven. But it takes discipline to watch these market rallies happen and not feel like you are missing out.

The Consumer’s Uphill Battle

Consumer spending is the number one driver of the U.S. economy and the consumer is going to face multiple headwinds in the second half of 2023. First, student loan payments are set to restart in October. Due to the Covid relief, many individuals with student loans have not been required to make a payment for the past three years and the $10,000 student loan debt cancellation that many people were banking on was recently struck down by the Supreme Court.

Second, while inflation has dropped, the interest rates on mortgages, car loans, and credit cards have not. The inflation rate dropped from 9% in June 2022 to 4% in May 2023 but the 30-year fixed mortgage rate peaked in November at around 7% and as of July 2023 still remains around 6.8%, virtually unchanged, so not a lot of relief for individuals that are trying to buy a house.

This is largely attributed to the third headwind for consumers which is that banks are tightening their lending practices. The banks see the same charts of the economy that we do and when the economy begins slowing down banks begin to tighten their lending standards making it more difficult for consumers and businesses to obtain loans. Even though the stock market has rallied in 2023, banks have continued to tighten their lending standards over the past 6 months and with more limited access to credit, that could put pressure on the economy in the second half of 2023.

Consumer spending has been stronger than expected in 2023 which has helped fuel the stock market rally this year but we can see in the data that a lot of this spending has been done using credit cards and default rates on credit cards and auto loans are rising quickly. So now many consumers have not only spent through their savings but by the end of the year they could have large credit card payments, car payments, higher mortgage/rent payments, and student loan payments.

Reasons for Recession Delay

With all of these clear headwinds for the market, why has the recession not begun yet as so many economists had forecasted at the beginning of 2023? In my opinion, the primary reason for the delay is that it typically takes 9 to 12 months for each Fed rate hike to impact the economy. When the Fed is raising rates, they are intentionally trying to slow down the economy to curb inflation. The Fed just paused for the first time in June 2023 but all of the rate hikes that were implemented in the first half of 2023 have yet to work their way into the economy. This is why you see yet another very consist historically pattern with the Fed Funds Rate. A pattern that I call the “Fed Table Top”. Here is a chart showing the last three Fed rate hike cycles going back to 2000:

You will see the same pattern over time, the Fed raises interest rates to fight inflation which are the moves higher in the chart, they pause at the top of their rate hike cycle which is the “Table Top”, and then a recession appears as a result of their tightening cycle, and they begin dropping interest rates. Once the Fed has reached its pause status or “table top”, some of those pauses last over a year, while other pauses only last a few months. The pause makes sense because again it takes time for all of those rate hikes to impact the economy so it’s never just a straight up and then a straight down in interest rates.

So then that raises the question, how long will this pause be? Honestly, I have no idea, and this is the tricky part again about timing but the pattern has repeated itself time and time again. However, as you can also see in the Fed chart above when you compare the current Fed rate hike cycle to those of the previous 3 cycles, the Fed just raised rates by more than the previous three cycles in a much shorter period of time, that would lead me to believe that this Fed Table Top could be shorter because the 9-month lag of the interest rate hikes on the economy will happen at a greater magnitude compared to the Fed rating rates at 0.25% - 0.50% per meeting as they did in the previous two Fed rate hike cycles.

Bulls or the Bears?

Only time will tell if the economic patterns of the past will remain true and a recession will emerge within the next 12 months or if this time it is truly different, and a recession will be avoided. For investors that have chosen the path of the bull, they will have to remain on their toes, because historically when the turn comes, it comes fast, and with very little warning.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Big FAFSA Calculation & Application Changes Starting in 2023

Parents that are used to completing the FAFSA application for their children are in for a few big surprises starting in 2023. Not only is the FAFSA application being completely revamped but the FAFSA calculation itself is being changed which could result in substantially lower financial aid awards for many college-bound students.

Parents that are used to completing the FAFSA application for their children are in for a big surprise for FAFSA Application years 2023+. Not only is the FAFSA application being completely revamped but the FAFSA calculation itself is being changed which could result in substantially lower financial aid awards for many college-bound students.

A Simplified FAFSA Application

Completing the FAFSA application can be a very frustrating process; tons of questions, unclear wording as to what information FAFSA is actually asking parents to report, and you have to spend a lot of time collecting all of your personal financial documents that are needed to enter the information on the FAFSA application.

Fortunately, in 2020, Congress passed the FAFSA Simplification Act which greatly simplified the FAFSA application in 2023 and years going forward. The old FAFSA application contained 108 questions, the new FAFSA application is only expected to contain 36 questions. In addition to cutting the questions in half, the wording of many of the questions were amended to make it easier to understand how to report your financial assets. Two very welcome changes to the application.

EFC (Expected Family Contribution) Calculation Removed

In the past, completing the FAFSA application has resulted in an Expected Family Contribution (EFC) amount which is meant to provide a ballpark amount that a family may have to pay out of pocket before need-based financial aid is awarded to a student. The term EFC can be misleading because it’s not necessarily the hard dollar amount that parents will be required to pay out of pocket but rather it’s the family’s financial need relative to other applicants.

To remove this confusion, EFC is now be replaced by SAI (Student Aid Index), so now after parents complete the FAFSA application, it will result in an SAI amount.

Financial Aid Awards Reduced For Multiple Children

Parents that have multiple children in college at the same time may be in for an unfortunate surprise when they see the results of the new SAI calculation. In the past, if a parent completed the FAFSA application and it resulted in an EFC of $30,000, but they had two children in college at the same time, FAFSA would split the $30,000 between the two children, $15,000 each, which would potentially make each student eligible for a higher financial aid award.

Starting the 2024 – 2025 school year, FAFSA no longer provides this EFC (SAI) split for multiple children in college. If the FAFSA calculation results in a $30,000 SAI, that $30,000 will now apply to EACH student, instead of being split equally between each child, which could result in lower need-based financial aid awards going forward.

Divorced Parents FAFSA Calculation Change

When parents are divorced, and they have a child attending college, the custodial parent is the parent that submits the FAFSA application based on their income and assets. Historically, the FAFSA definition of the “custodial parent” was the parent that the child lived with for the majority of the 12-month period ending on the day the FAFSA application is filed. This often times created a very favorable financial aid award if the child was living for a majority of the year with the parent that had lower income and assets.

This will change for years 2023 and going forward. The new FAFSA rules require the parent who provided the most financial support in the “prior-prior” tax year to complete the FAFSA application instead of the custodial parent. Prior-prior refers to the tax year 2 years ago from the beginning of the college semester. For the 2025 – 2026 award year, FAFSA will look at the 2023 tax year for this determination.

For example, Joe and Sue got divorced 5 years ago, and their daughter Mary is currently a sophomore in college. Sue is a homemaker, Mary lives with her mother for the majority of the year, Joe makes $300,000 per year, and pays Sue $25,000 per year in child support and $40,000 per year in alimony. For the 2023 – 2024, under the old FAFSA calculation, Sue was considered the custodial parent, and completed the FAFSA form using her annual income and assets. Since Joe is not the custodial parent, Joe’s income and assets are ignored for purposes of FAFSA.

Starting in the 2024 – 2025 school year, under the new rules, that has now changed. Since Joe is providing a majority of the financial support via child support and alimony payments, Joe would now be the parent required to submit the FAFSA application based on his income and assets. Since Joe’s income is substantially higher than Sue’s, it could result in a much lower college financial aid award.

There has been some initial guidance, that if there is a “tie” as to which parent provided the majority of the financial support, the ties are broken based on whichever parent has the higher adjusted gross income.

Changes to Pell Grants

One of the largest sources of need-based financial aid from the federal government is awarded via Pell Grants. Starting in the 2024 – 2025 school year, the maximum Pell Grant amount was increased but they have changed how the Pell Grant is calculated. The Pell Grant takes into account both the SAI result (new EFC) and the applicant’s adjusted gross income. Since the calculation of the SAI has changed, for reasons that we have already discussed, it could impact the amount of the Pell Grants awarded to students.

As a new benefit, parents will now be able to determine if their child will be eligible for a Pell Grant award based on income and family size before they even complete the FAFSA form.

Grandparent 529 Penalty Removed

A positive change that they made was eliminating the restriction associated with distributing money from a 529 account owned by a grandparent for the benefit of the grandchild. Previously, if distributions were made from a grandparent owned 529 accounts, those distributions were considered “income of the student” in the FAFSA calculation, which could dramatically reduce the financial aid awards in future years. The new legislation removed this restriction and made grandparent owned 529 accounts even more valuable than they were prior to this change.

Income Protection Allowance Increased

The FAFSA calculation has income thresholds that exclude specific amounts of income of both the parents and the child in the calculation of the Student Aid Index. Those income exclusion allowances were increased starting in 2024. The income protection allowance for parents was increased by about 20%.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What is changing with the FAFSA application starting in 2023?

Beginning with the 2023–2024 academic year, the FAFSA is being redesigned under the FAFSA Simplification Act. The number of questions has been reduced from 108 to about 36, and the language has been simplified to make it easier for families to understand and complete the form.

What is the difference between EFC and SAI?

The Expected Family Contribution (EFC) has been replaced with the Student Aid Index (SAI). While both estimate a family’s financial ability to contribute toward college costs, the new SAI formula is designed to simplify the process and remove confusion surrounding the term “expected contribution.”

How will the new FAFSA rules affect families with multiple children in college?

Under the old FAFSA calculation, the EFC was divided among multiple students in college, potentially increasing need-based aid for each child. Starting with the 2024–2025 school year, that split no longer applies—each student will have the same SAI, which may reduce financial aid eligibility for families with multiple college students.

How are FAFSA rules changing for divorced or separated parents?

Previously, the “custodial parent”—the one the student lived with most—was responsible for filing FAFSA. Beginning in 2024–2025, the parent who provided the most financial support during the “prior-prior” tax year must complete the application. This change may increase the reported household income for some families, reducing aid eligibility.

What are the new rules for Pell Grants?

Starting in 2024–2025, Pell Grant eligibility will be determined based on the new SAI formula and household adjusted gross income. While the maximum Pell Grant amount is increasing, the new calculation could alter eligibility for some students. Families will also be able to check Pell Grant eligibility before completing the FAFSA form.

How do the new rules affect 529 plans owned by grandparents?

Distributions from grandparent-owned 529 plans will no longer be counted as student income in the FAFSA formula. This change removes a previous penalty that reduced financial aid eligibility, making grandparent-owned 529 plans more advantageous.

What is the Income Protection Allowance and how is it changing?

The Income Protection Allowance excludes a portion of a family’s income from the aid calculation to protect funds for basic living expenses. Starting in 2024, these thresholds are increasing by roughly 20%, allowing more income to be shielded from the FAFSA formula and potentially increasing aid eligibility.

Social Security: Suspending Payments vs. Withdraw of Benefits Election

It’s not an uncommon occurrence when a retiree turns on their social security benefits, but then all of a sudden take on either part-time or full-time employment, begin making more income than they expected, and they start searching for options to suspend their social security benefits until a later date.

The good news is there are “do-over” options for your social security benefit that exist depending on your age and how long it’s been since you started receiving your social security benefits. The are two different strategies:

If you have started receiving your social security benefits but you now want to suspend receiving your social security payments going forward, you have two options available to you. You can either:

Suspending Your Social Security Benefit

Withdrawing Your Social Security Benefit

They seem like the same thing, but they are two completely different strategies. One option requires you to pay back the social security benefits already received; the other does not. One option has an age restriction; the other does not.

Some of the most common reasons why retirees elect to either suspend or withdraw their social security benefits are:

Retirees either take on either part-time or full-time employment or receives an inheritance, they no longer need their social security benefit to supplement their income, and they would prefer to allow their social security benefit to keep growing by 6% - 8% per year.

A retiree turns on their social security prior to Full Retirement Age, begins making income over the allowable social security threshold, and is now faced with the social security earned income penalty

Since social security benefits are taxable income to many retirees, by suspending their social security payments, it opens up valuable tax and wealth accumulation strategies. We will cover a number of those strategies in this article.

Social Security: Withdraw of Benefits

The Withdraw of Benefits option is ONLY available if you started receiving your social security benefits within the past 12 months. If you are reading this article and you started receiving your social security benefits more than a year ago, you are not eligible for the withdraw of benefits strategy (however, you may still be eligible for a suspension of benefits covered later).

You can withdraw your benefits at any age: 62, 64, 68, etc. We find that the Withdrawal of Benefits strategy is the most common for retirees that retired before their Social Security Full Retirement Age (FRA), turned on their SS benefits early, began working again, and make more income than they expected. They realize very quickly that this scenario can have the following negative impacts on their social security benefits:

They may incur an Earning Income Penalty which claws back some of the social security benefits that they received.

A larger percentage of their social security benefit may be subject to taxation

They may have to pay a higher tax rate on their social security benefits

By turning on their social security early, they permanently reduced the amount of their social security benefit. Had they known they would earn this extra income, they would have waited and allowed their social security benefit to continue to grow.

You Must Repay The Social Security Benefits That You Received

Since the Withdrawal of Benefits option is the truest “Do-Over” option, you, unfortunately, must return to social security all of the benefit payments you received within the last 12 months. If you received $1,000 per month for the past 10 months and you file a Form SSA-521, you will be required to return the $10,000 that you received to social security. However, in addition to returning the social security benefits that you received, you also have to return the following:

Payments made to your spouse under the 50% spousal benefit

Payments to your children made under the dependent benefit

Voluntary federal and state taxes that were withheld from your social security payments

Medicare premiums that were withheld from your social security payments

This is why this option is the purest “do-over.” Once you have filed the Withdraw of Benefits and repaid social security the required amount, it’s like it never happened.

One Lifetime Withdrawal

To prevent abuse, you are only allowed one “Withdraw of Benefits” application during your lifetime.

How To Apply For A Social Security Withdraw of Benefits

You can apply to withdraw your benefits by mailing or hand-delivering form SSA-521 to your local social security office. Once Social Security has approved your withdrawal application, you have 60 days to change your mind.

Suspending Your Social Security Benefits

Now let’s shift gears to the second strategy, which involves voluntarily suspending your social security benefits. Why is a “Suspension” different than a “Withdrawal of Benefits”?

You are only allowed to “suspend” your social security benefits AFTER you have reached Full Retirement Age (FRA). For anyone born 1960 or later, that would be age 67. Suspending your benefit is not an option if you have not yet reached your social security full retirement age.

You do not have to repay the social security benefits you already received.

By suspending your benefits, the monthly payments cease as of the suspension date, and from that date forward, your social security benefit continues to grow at a rate of 8% per year until the maximum social security age of 70.

Restarting Your Suspended SS Benefits

If you decide to suspend your social security benefits, you can elect to turn that back on at any time. For example, you retire at age 67 and turn on your social security benefit of $2,000 per month, but then your friend approaches you about a consulting gig that will pay you $40,000 only working 2 days a week. You no longer need your social security benefits to cover your expenses, so you contact your local social security office and request that they suspend your benefits. A year later, the consulting gig ends; you can go back to the social security office, and request that they resume your social security payments which have now increased by 8% and will now be $2,160 per month.

How Do You Suspend Your Social Security Benefits?

You can request a suspension by phone, in writing, or by visiting your local social security office.

Reasons To Consider Suspending Your Social Security Benefit

As financial planners, we work with clients to identify wealth accumulation strategies, some basic and some more advanced. In this section I’m going to share with you some of the situations where we have advised clients to suspend their social security benefits:

Income Not Needed: This one we already cover in the example but if a client finds that they don’t need their social security income to meet their expenses, stopping the benefit, and taking advantage of the 8% guaranteed increase in the benefit every year until age 70 is an attractive option. I’m not aware of any investment options at this time that offers a guaranteed 8% rate of return.

Increasing The Survivor Benefits: By suspending your social security benefit, if your social security benefit is higher than your spouse’s benefit, you are increasing the social security survivor benefit that would be available to your spouse if you pass away first. When one spouse passes away, only one social security payment continues, and it’s the higher of the two.

Reduce Taxable Income: Retirees are often surprised to find out that up to 85% of the social security benefits received could be taxed as ordinary income at the federal level and there are a handful of states that tax social security at the state level. If there is temporary income right now that will sunset, instead of your social security benefit being stacked on top of your other taxable income, making it subject to higher tax rates, it may be beneficial to suspend your social security benefit until a later date.

Roth Conversions: Roth conversions can be a fantastic long-term wealth accumulation strategy in retirement but what makes these conversions work, is after you have retired, most retirees are in a lower tax bracket which allows them to convert pre-tax retirement accounts to a Roth IRA, and realize those conversions at a low tax rate. However, as I just mentioned, social security is taxable income, by suspending your social security benefit, and removing that taxable income from the table, it can open up room for larger Roth conversions.

Reduce Future RMDs: For pre-tax IRAs and 401(k), once you reach either 73 or 75 depending on your date of birth, the IRS forces you to start taking taxable required minimum distributions (RMDs) from those retirement accounts. It’s not uncommon for retirees with pensions to retire, they turn on their pension payment and social security payments, and that is more than enough to meet their retirement income needs. However, often times these retirees also have pre-tax retirement accounts that they do not need to take withdraws from to supplement their income so the plan is to just let them continue to accumulate in value.

The problem becomes, if no distributions are taken from those accounts, the balances continue to grow, making the RMDs larger later on, which could make those distributions subject to higher tax rates. Instead, it may be a better strategy to suspend your social security benefits which would allow you to start taking distribution from your pre-tax retirement accounts now, in an effort to reduce the future RMD amounts.

Life Expectancy Protection: With everyone living longer, there is the risk that a retiree could outlive their personal retirement savings but social security payments last for the rest of your life. By suspending your social security benefit and receiving the 8% per year increase, your social security benefit will support a larger percentage of your annual expenses. Also, unlike IRA accounts, social security receives a COLA (cost of living adjustment) each year which increases your social security benefit for inflation. By delaying the benefit, the COLA is now being applied to a higher social security benefit.

Choosing Between Withdraw or Suspend

If you have already reached FRA and you turned on your social security benefit less than 12 months ago, you have the option to either “Suspend” your benefit or “Withdraw” your benefit.

If you suspend your benefit, you do not have to pay back any of the social security benefits that you already received, and your social security benefit will continue to accumulate at 8% per year until you elect to turn your social security back on.

If instead, you decide to withdraw your benefit, yes, you have to pay back any social security payments that you already received but there is one advantage. Since the withdrawal of benefits is a complete “do-over”, you received credit for the 8% per year increase all the way back to your start date. This is not the case with the suspend strategy. If a client has $20,000 in idle cash and they received $20,000 in social security benefits over the past 11 months, if they use their $20,000 to pay back social security, it’s like you are receiving an 8% return on that $20,000 because your social security will be 8% a year from your start date. Not a bad return on your idle cash.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What is the difference between suspending and withdrawing Social Security benefits?

Suspending and withdrawing Social Security benefits are two distinct strategies. A suspension pauses future payments without repayment and is available only after reaching Full Retirement Age (FRA). A withdrawal, on the other hand, is a complete “do-over” available within 12 months of starting benefits and requires repaying all benefits received.

When can you withdraw your Social Security benefits?

You can withdraw your Social Security benefits within 12 months of first receiving them, regardless of your age. However, you must repay all benefits received—this includes your own payments, spousal or dependent benefits, and any withheld taxes or Medicare premiums. You may only use this option once in your lifetime.

When can you suspend your Social Security benefits?

You can voluntarily suspend your benefits after reaching your Full Retirement Age (currently 67 for those born in 1960 or later). During suspension, no repayments are required, and your benefits will grow by approximately 8% per year until age 70, when you can resume receiving a higher monthly benefit.

Why would someone choose to suspend their Social Security payments?

Common reasons include not needing the income immediately, wanting to increase future or survivor benefits, reducing taxable income, or using the pause to perform Roth conversions. Suspending benefits can also help manage future required minimum distributions (RMDs) and protect against longevity risk.

How do you request to suspend or withdraw your benefits?

To suspend your benefits, contact the Social Security Administration by phone, in writing, or in person. To withdraw your benefits, you must submit Form SSA-521 either by mail or in person at your local Social Security office. Once a withdrawal is approved, you have 60 days to change your mind.

What happens to your benefits when you resume after suspension?

When you restart benefits after a suspension, your monthly payment will include the 8% annual increase earned during the suspension period. Any future cost-of-living adjustments (COLAs) will then apply to this higher amount.

Which is better — suspending or withdrawing Social Security benefits?

It depends on your age and financial situation. If you’re within 12 months of starting benefits and can afford to repay the amount received, a withdrawal offers a full “reset” and restarts your benefit growth from your original start date. If you are past that window, suspension allows your benefits to grow without repayment until you choose to resume.

Gifting Your House with a Life Estate vs. Medicaid Trust

I recently published an article called “Don’t Gift Your House To Your Children” which highlighted the pitfalls of gifting your house to your kids versus setting up a Medicaid Trust to own your house, as an asset protection strategy to manage the risk of a long-care care event taking place in the future. That article prompted a few estate attorneys to reach out to me to present a third option which involves gifting your house to your children with a life estate. While the life estate does solve some of the tax issues of gifting the house to your kids with no life estate, there are still issues that persist even with a life estate that can be solved by setting up a Medicaid trust to own your house.

I recently published an article titled “Don’t Gift Your House To Your Children” which highlighted the pitfalls of gifting your house to your kids versus setting up a Medicaid Trust to own your house, as an asset protection strategy to manage the risk of a long-care care event taking place in the future. That article prompted a few estate attorneys to reach out to me to present a third option which involves gifting your house to your children with a life estate. While the life estate does solve some of the tax issues of gifting the house to your kids with no life estate, there are still issues that persist even with a life estate that can be solved by setting up a Medicaid trust to own your house.

In this article, I will cover the following topics:

What is a life estate?

What is the process of gifting your house with a life estate?

How does the life estate protect your assets from the Medicaid spend-down process?

Tax issues associated with a life estate

Control issues associated with a life estate

Comparing the life estate strategy to setting up a Medicaid Trust to own your house

3 Asset Protection Strategies

There are three main asset protection strategies when it comes to protecting your house from the Medicaid spend-down process triggered by a long-term care event:

Gifting your house to your children

Gifting your house to your children with a life estate

Gifting your house to a Medicaid Trust

Gifting Your House To Your Children

Gifting your house outright to your children without a life estate is probably the least advantageous of the three asset protection strategies. While gifting your house to your kids may be a successful strategy for getting the house out of your name to begin the Medicaid 5-Year Lookback Period, it creates a whole host of tax and control issues that can arise both while you are still alive and when your children inherit your house after you pass away.

Note: The primary residence is not usually a countable asset for purposes of Medicaid BUT some counties may place a lien against the property for any payments that Medicaid makes on your behalf for long-term care services. While Medicaid can’t make you sell the house while you are still alive, once you pass away, Medicaid may be waiting to recoup the money they paid, so your house ends up going to Medicaid instead of passing to your children.

Here is a quick list of the issues:

No Control: When you gift your house to your kids, you no longer have any control of that asset, meaning if the kids wanted to, they could sell the house whenever they want without your permission.

Tax Issue If You Sell Your House: If you gift your house to your kids and then you sell your house while you are still alive it creates numerous issues. First, from a tax standpoint, if you sell your house for more than you purchased it for, your children have to pay tax on the gain in the house. Normally, when you sell your primary residence, a single filer can exclude $250,000 of gain and a married filer can exclude $500,000 of gain from taxation. However, since your kids own the house, and it’s not their primary residence, you lose the exclusion, and your kids have to pay tax on the property as if it was an investment property.

No Step-up In Cost Basis: When you gift an asset to your kids while you are still alive, they inherited your cost basis in the property, meaning if you paid $100,000 for your house 30 years ago, their cost basis in your house is $100,000. After you pass away, your children do not receive a step-up in cost basis, which means when they go to sell the house, they have to pay tax on the full gain amount of the property. If your kids sell your house for $500,000 and you purchase it for $100,000, they could incur a $60,000+ tax bill.

Life Estate Option

Now let’s move on to option #2, gifting your house to your kids with a life estate. What is a life estate? A life estate allows you to gift your house to your children but you reserve the right to live in your house for the rest of your life, and your children cannot sell the house while you are still alive without your permission.

Here are the advantages of gifting your house with a life estate versus gifting your house without a life estate:

More Control: The life estate gives the person gifting the house more control because your kids cannot make you sell your house against your will while you are still alive.

Medicaid Protection: Similar to the outright gift your kids, a gift with a life estate, allows you to begin the Medicaid 5-year look back on your primary residence so a lien cannot be placed against the property if a long-term care event occurs.

Step-up in Cost Basis: One of the biggest advantages of the life estate is that the beneficiaries of your estate receive a step-up in costs basis when they inherit your house. If you purchase your house for $100,000 30 years ago but your house is worth $500,000 when you pass away, your children receive a step-up in the cost basis to the $500,000 fair market value when you pass, meaning if they sell the house the next day for $500,000, there are no taxes due on the full $500,000. This is because when you pass away, the life estate expires, and then your house passes through your estate, which allows the step-up in basis to take place.

Lower-Cost Option: Gifting your house to your children with a life estate only requires a simple deed change which may be a lower-cost option compared to the cost of setting up a Medicaid Trust which can range from $1,500 - $5,000.

Disadvantages of Life Estate

However, there are numerous disadvantages associated with life estates:

Control Problems If You Want To Sell Your House: While the life estate allows you to live in the house for the rest of your life, you give up control as to whether or not you can sell your house while you are still alive. If you want to sell your house while you are still alive, you, and ALL of your children that have a life estate, would all have to agree to sell the house. If you have three children and they all share in the life estate, if one of your children will not agree to sell the house, you won’t be able to sell it.

Tax Problem If You Sell It: If you want to sell your house while you are still alive and all of your children with the life estate agree to the sale, it creates a tax issue similar to the outright gift to your kids without a life estate. Since you gifted the house to your kids, they inherited your cost basis in the property and would not be eligible for the primary gain exclusion of $250,000 / $500,000, so they would have to pay tax on the gain.

One slight difference, the life estate that you retained has value when you sell the house, so if you sell your house for $500,000, depending on the life expectancy tables, your life estate may be worth $50,000, so that $50,000 would be returned to you, and your children would receive the remaining $450,000.

Medicaid Eligibility Issue: Building on the house sale example that we just discussed, if you sell your house, and the value of your life estate is paid to you, if you or your spouse are currently receiving Medicaid benefits, it could put you over the asset allowance, and make you or your spouse ineligible for Medicaid.

Even if you are not receiving Medicaid benefits when you sell the house, the cash coming back to you would be a countable asset subject to the Medicaid 5-Year Lookback period, so the proceeds from the house may now become an asset that needs to be spent down if a long-term care event happens within the next 5 years.

Your Child’s Financial Problems Become Your Problem: If you gift your house to your children with a life estate, similar to an outright gift, you run the risk that your child’s financial problems may become your financial problem. Since they have an ownership interest in your house, their ownership interest could be exposed to personal lawsuits, divorce, and/or tax liens.

Your Child Predeceases You: If your child dies before you, their ownership interest in your house could be subject to probate, and their ownership interest could pass to their spouse, kids, or other beneficiaries of their estate which might not have been your original intention.

Medicaid Trust

Setting up a Medicaid Trust to protect your house from a long-term care event solves many of the issues that arise compared to gifting your house to your children with a life estate.

Control: You can include language in your trust documents that would allow you to live in your house for the rest of your life and your trustee would not have the option of selling the house while you are still living.

Protection From Medicaid: If you gift your house to a grantor irrevocable trust, otherwise known as a Medicaid Trust, you will have made a completed gift in the eyes of Medicaid, and it will begin the Medicaid look back period.

Step-up In Cost Basis: Since it’s a grantor trust, when you pass away, your house will go through your estate, and your beneficiaries will receive a step-up in cost basis.

Retain The Primary Residence Tax Exclusion: If you decide to sell your house in the future, since it’s a grantor trust, you preserve the $250,000 / $500,000 capital gain exclusion when you sell your primary residence.

Ability to Choose 1 or 2 Trustees: When you set up your trust, you will have to select at least 1 trustee, the trustee is the person that oversees the assets that are owned by the trust. If you have multiple children, you have the choice to designate one of the children as trustee, so if you want to sell your house in the future, only your child that is trustee would need to authorize the sale of the house. You do not need to receive approval from all of your children like you would with a life estate.

Protected From Your Child’s Financial Problems: It’s common for parents to list their children as beneficiaries of the trust, so after they pass, the house passes to them. But the trust is the owner of the house, not your children, so it protects you from any financial troubles that could arise from your children since they are not currently owners of the house.

Protect House Sale Proceeds from Medicaid: If your trust owns the house and you sell the house while you are still alive, at the house closing, they would make the check payable to your trust, and your trust could either purchase your next house, or you could set up an investment account owned by your trust. The key planning item here is the money never leaves your trust. As soon as the money leaves your trust, it’s no longer protected from Medicaid, and you would have to restart the Medicaid look back period.

A Trust Can Own Other Assets: Trusts can own other assets besides real estate. A trust can own an investment account, savings account, business interest, vehicle, and other assets. The only asset a trust typically cannot own is a retirement account like an IRA or 401(k) account. For individuals that have more than just a house to protect from Medicaid, a trust may be the ideal solution.

Comparing Asset Protection Strategies

When you compare the three Medicaid asset protection options:

Gifting your house to your children

Gifting your house to your children with a life estate

Gifting your house to a Medicaid Trust