Behind Closed Doors: How the Fed Makes Interest Rate Decisions - Voting and Non Voting Members

On September 17, 2025, the Federal Reserve cut interest rates for the first time in years. Here’s how the FOMC voting process works, who gets a say, and why these decisions matter for the economy.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

On September 17, 2025, the Federal Reserve voted to lower its benchmark interest rate by 0.25%—the first rate cut in quite some time. The move brought the federal funds target range down to 4.00%–4.25% and sent a signal to markets that the Fed is beginning to ease monetary policy after a long pause.

This decision raises an important question: how exactly does the Fed decide whether to cut rates, raise them, or leave them the same?

In this post, we’ll break down:

How voting works within the Federal Reserve

The roles of Jerome Powell, the Board of Governors, and the regional Fed presidents

Why independence from politics is so critical to the Fed’s mission

Why rate cuts matter so much to the economy

Current changes happening inside the Fed leadership

Who Actually Votes on Interest Rates?

When the Fed meets to set interest rates, the decision is made by the Federal Open Market Committee (FOMC). The FOMC includes:

The seven members of the Federal Reserve Board of Governors in Washington, D.C.

The President of the New York Federal Reserve Bank, who always has a vote.

Four of the remaining 11 Reserve Bank presidents, who rotate into voting seats each year.

All 19 leaders—the seven governors plus the 12 Reserve Bank presidents—attend FOMC meetings and share their views on the economy. But only 12 get to cast a vote at each meeting.

This structure balances national perspectives from the Board of Governors with regional insights from across the country. For example, the president of the Dallas Fed might emphasize conditions in the oil industry, while the president of the Chicago Fed may highlight trends in agriculture and manufacturing.

The Role of Jerome Powell

Jerome Powell, as Chair of the Federal Reserve, gets most of the headlines. He leads meetings, frames the discussion, and communicates decisions to the public. But in terms of raw power, his vote carries the same weight as every other voting member. He doesn’t have veto authority and can’t unilaterally set policy.

What makes the Chair influential is his ability to guide consensus. Powell works with Fed staff to prepare proposals, sets the tone in deliberations, and—perhaps most importantly—speaks for the Fed in press conferences after decisions are made. His leadership matters, but ultimately he must secure a majority of votes to enact policy.

How the Voting Works at Each Meeting

At each of the Fed’s eight scheduled meetings per year, the process unfolds in a fairly structured way. The first day is devoted to reviewing economic data and forecasts. All members, both voting and non-voting, weigh in with their perspectives.

On the second day, a policy proposal is put on the table—whether to cut, hike, or hold interest rates steady. The voting members then cast their votes, and the majority carries the decision.

In the September 2025 meeting, most members supported a 0.25% rate cut. But not everyone agreed. Newly appointed Governor Stephen Miran dissented, preferring a larger half-point cut. The rest of the committee sided with the smaller step, showing how debates within the Fed can shape outcomes.

Why Rate Cuts Matter

Lowering interest rates is one of the most powerful tools the Fed has to influence the economy. A cut makes borrowing cheaper—whether it’s a family taking out a mortgage, a business financing new equipment, or a consumer using a credit card. This tends to spur spending and investment, which can help keep the economy growing and support job creation.

On the flip side, keeping rates too high for too long can slow growth and risk tipping the economy into recession. That’s why the September cut was seen as so significant: it marked a shift in strategy, signaling the Fed is now more concerned about supporting growth than restraining inflation.

The Fed’s Political Independence—Will It Last?

One of the most important principles of the Federal Reserve is that it is meant to operate independently of politics. Congress gave the Fed a dual mandate: to promote stable prices and maximum employment. To achieve that, Fed leaders serve long terms and can’t be removed simply because the president or Congress doesn’t like their decisions.

This independence is crucial. Without it, presidents might pressure the Fed to cut rates before elections to juice the economy, or raise rates to influence market sentiment—moves that could create long-term economic instability.

Recently, however, that independence of the Fed has been called into question. The Trump administration has openly criticized the Fed for not cutting rates sooner. A new Fed governor, Stephen Miran, joined the Board after also serving in the White House, raising questions about conflicts of interest. Also, the Trump administration is attempting to remove Governor Lisa Cook from the Board, blocked by federal courts so far, highlighting the political pressures the Fed faces today. Governor Cook’s removal would mean the President could select another member to take her place and that person, similar to Governor Miran, could greatly favor larger interest rate cuts per the President’s request.

Looking ahead, Jerome Powell’s term as Chair ends in May 2026. Whoever the president nominates to replace him—and whether the Senate confirms that nominee—will shape the direction of monetary policy for years to come. While Powell’s term as a Governor extends into 2028, his leadership role will change once a new Chair is selected.

Takeaway

The Fed’s decision to cut rates this September highlights not just the power of monetary policy, but also the complex process behind it. Rate decisions aren’t made by one person in Washington—they’re the result of debate, data analysis, and ultimately, a vote among 12 members of the FOMC.

Jerome Powell may be the face of the Fed, but he’s only one voice at the table. And while the Fed is designed to stand apart from partisan politics, the recent events within the current Fed members demonstrate just how difficult it can be to maintain that independence.

For investors, business owners, and households, understanding how these decisions are made is critical—because what happens in those FOMC meetings shapes the borrowing costs, job market, and investment opportunities that affect us all.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

Who decides when the Federal Reserve raises or lowers interest rates?

Interest rate decisions are made by the Federal Open Market Committee (FOMC), which includes the seven members of the Board of Governors, the president of the New York Fed, and four rotating regional Fed presidents. While all 19 leaders participate in discussions, only 12 vote on policy at each meeting.

What role does Jerome Powell play in the Fed’s decision-making process?

As Chair of the Federal Reserve, Jerome Powell leads meetings, shapes discussion topics, and communicates decisions publicly. However, his vote carries the same weight as every other voting member, and policy changes require a majority of the committee’s support.

How does the Federal Reserve vote on interest rate changes?

At each of the eight scheduled meetings per year, members review economic data and forecasts before voting on whether to raise, cut, or hold rates steady. The majority vote determines the outcome, and dissenting opinions are noted in official meeting records.

Why does the Fed lower interest rates?

The Fed cuts rates to make borrowing cheaper, which can stimulate consumer spending, business investment, and overall economic growth. Lower rates are often used when inflation is under control but the economy shows signs of slowing.

Why is the Federal Reserve’s independence from politics so important?

Independence allows the Fed to make decisions based on economic data rather than political pressure. Without it, policymakers could be influenced to manipulate interest rates for short-term political gains, potentially creating long-term economic instability.

What changes in Fed leadership could impact future monetary policy?

Jerome Powell’s term as Chair ends in May 2026, and whoever is appointed next will significantly influence the direction of monetary policy. Ongoing political tensions and leadership shifts could affect how aggressively the Fed adjusts rates in the coming years.

What’s a Target Date Fund and Should I Invest in It?

Target date funds adjust automatically as you approach retirement, offering a simple “set it and forget it” investment strategy. They can be a smart option for early savers, but investors with complex financial situations may need more customized solutions.

If you've logged into your 401(k) or IRA recently, there's a good chance you've seen investment options labeled something like “2050 Target Date Fund” or “2065 Retirement Fund.” But what exactly is a target date fund, and is it the right choice for your retirement savings?

This article breaks down how target date funds work, their pros and cons, and when they make sense within a broader financial plan.

What Is a Target Date Fund?

A target date fund is a type of investment fund that automatically adjusts its asset allocation based on your expected retirement year—your target date.

For example, a “2060 Target Date Fund” is designed for someone retiring around the year 2060. The fund starts out heavily invested in stocks to maximize growth. Over time, it gradually becomes more conservative, shifting toward bonds and cash equivalents as the retirement year approaches. This automatic reallocation is called the glide path.

Target date funds are often considered a “set-it-and-forget-it” option for retirement investors but understanding how they work may help determine whether they are a suitable option for your savings.

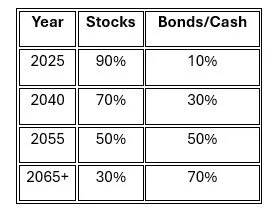

How the Glide Path Works

The glide path is the fund’s built-in schedule for reducing investment risk over time. Here's a simplified example of how the asset allocation might shift as retirement nears:

This gradual transition helps reduce the impact of market volatility as you get closer to drawing income from the portfolio. The example above may be a glide path associated with a “2065 Target Date Fund”.

Benefits of Target Date Funds

Simplicity: Target date funds are professionally managed, removing the need to select and monitor individual investments.

Diversification: These funds typically include a mix of U.S. and international stocks, bonds, and sometimes alternative investments, offering broad market exposure.

Automatic rebalancing: The fund rebalances its portfolio over time, keeping it aligned with its risk-reduction strategy without requiring action from the investor.

Good default option: Many 401(k) plans use target date funds as the default investment for participants who don’t actively choose their own allocation.

Potential Drawbacks to Consider

One-size-fits-all: These funds assume that all investors retiring in the same year have similar goals and risk tolerances, which isn’t always the case.

Higher fees: Some target date funds—especially those with actively managed components—can carry higher expense ratios compared to index-based options.

Misaligned risk profile: Some glide paths become too conservative too early, while others remain aggressive longer than ideal. The right fit depends on your personal retirement income plan.

Tax inefficiency in taxable accounts: Frequent rebalancing may create taxable events when held in non-retirement accounts. They are generally best suited for IRAs or 401(k)s.

When Target Date Funds Make Sense

Target date funds can be a solid choice if you:

Are early in your career and want a simple, broadly diversified investment

Don’t want to actively manage your retirement portfolio

Prefer to avoid emotional or reactive investment decisions

Are not yet working with a financial advisor

They are especially useful as a default option when you’re getting started or want to automate long-term investing with minimal oversight.

When to Consider Alternatives

You may want to explore other investment options if you:

Have substantial assets and want a more customized portfolio

Are implementing tax planning strategies like Roth conversions or asset location

Have other income sources in retirement that affect your risk tolerance

Want more control over your asset mix and withdrawal strategy

Have a lower risk tolerance than where the target date fund would allocate your investments

In these cases, building a personalized portfolio may better align with your goals and offer more flexibility.

Final Thoughts

Target date funds can offer convenience, professional management, and a clear path toward a retirement-ready portfolio. For many investors—especially those early in their careers—they can be a smart, efficient way to begin building long-term wealth.

However, as your financial picture grows more complex, it may be worth reevaluating whether a one-size-fits-all fund still fits your personal strategy. A custom portfolio tailored to your income needs, tax situation, and risk tolerance may offer more precise control over your retirement outcome.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

Frequently Asked Questions (FAQs)

What is a target date fund?

A target date fund is a diversified investment designed to automatically adjust its mix of stocks, bonds, and other assets as you approach a specific retirement year. It aims to provide growth in the early years and gradually reduce risk as the target date gets closer.

How does a target date fund’s glide path work?

The glide path is the fund’s schedule for shifting from aggressive investments, like stocks, to more conservative holdings, such as bonds and cash equivalents. This gradual transition helps reduce volatility as you near retirement while still pursuing growth early on.

How do I choose the right target date fund?

Most investors select the fund closest to their expected retirement year. However, personal factors such as risk tolerance, savings rate, and income goals should also be considered when choosing a fund.

What are the main benefits of target date funds?

Target date funds offer automatic diversification and rebalancing, making them a convenient “set-it-and-forget-it” option. They can simplify retirement investing for those who prefer not to manage asset allocation themselves.

What are the potential drawbacks of target date funds?

One downside is that investors have little control over the fund’s specific holdings or risk adjustments. Glide paths also vary by provider, meaning some funds may remain more aggressive or conservative than expected.

Are target date funds a good choice for everyone?

They can be a strong fit for investors who want a hands-off approach, but those with complex financial goals or multiple investment accounts may benefit from a more customized strategy. Reviewing the fund’s allocation and costs before investing is essential.

Will Social Security Be There When You Retire?

Social Security is projected to face a funding shortfall in 2034, leading many Americans to wonder if it will still be there when they retire. While the system won’t go bankrupt, benefits could be reduced by about 20% unless Congress acts. Our analysis at Greenbush Financial Group explores what 2034 really means, why lawmakers are likely to intervene, and how to plan your retirement with Social Security uncertainty in mind.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

If you’ve looked at your Social Security statement recently, you may have noticed a troubling note: beginning in 2034, the system will no longer have enough funding to pay out full promised benefits. For many Americans, this raises a big question: Will Social Security even be there when I retire?

In this article, we’ll break down:

How Social Security is currently funded and why it faces challenges

What the 2034 date really means (hint: it’s not “bankruptcy”)

Why Congress is likely to act before major benefit cuts happen

Practical solutions that could shore up the system for future retirees

Why meaningful reform may not happen until the last minute

How Social Security Works Today

Social Security is funded primarily through FICA payroll taxes. Workers and employers each pay 6.2% of wages (12.4% total) into the system, which goes toward funding retirement benefits for current retirees.

Here’s the key point: the money doesn’t accumulate in a large “savings account” for future benefits. Instead, today’s payroll taxes go right back out the door to pay today’s beneficiaries. This setup worked well when there were many workers for each retiree, but demographic trends are changing the math.

Baby Boomers are retiring in large numbers.

People are living longer, so they collect benefits for more years.

Birth rates are low, meaning fewer workers are paying into the system.

This imbalance is the root of Social Security’s funding challenge.

What Happens in 2034?

Many people think 2034 is the year Social Security “goes bankrupt.” That’s not the full story.

According to the Social Security Trustees’ report, if Congress does nothing, the system’s trust funds will be depleted by 2034. At that point, incoming payroll taxes would still be enough to pay about 80% of promised benefits.

In practical terms, this would mean an immediate 20% cut in benefits for all recipients. While Social Security wouldn’t disappear, such a cut would have a huge impact on retirees who rely on it as their primary source of income.

Why We Believe Congress Will Act

It’s our opinion that Congress will not allow benefits to be cut so dramatically. Here’s why:

For a large portion of Americans over age 65, Social Security is the primary source of retirement income.

Cutting benefits by 20% would potentially impoverish millions of retirees.

Retirees also represent a powerful voting population, making it politically unlikely that lawmakers would let the system fail without intervention.

That doesn’t mean changes won’t come—but it does make drastic benefit cuts less likely.

Possible Solutions to Fix Social Security

The challenge is real, but there are several practical options available. The earlier these changes are made, the smaller the adjustments need to be. If lawmakers wait until 2034, the fixes may be more drastic. Some of the most common proposals include:

1. Increasing the Taxable Wage Base

Right now, Social Security taxes only apply to wages up to $176,100 (2025 limit). Someone earning $400,000 pays Social Security tax on less than half of their income.

Raising or eliminating the cap would bring more revenue into the system.

While no one likes higher taxes, it may be less painful than the economic impact of the sudden cut in Social Security Benefits starting in 2034

2. Extending the Full Retirement Age

Currently, full retirement age is 67. But Social Security hasn’t been properly indexed for life expectancy. Studies suggest that if it were, the full retirement age could be in the early 70s.

Extending retirement age would reduce how long people collect benefits.

This adjustment reflects the fact that Americans are living longer and the Social Security system was not originally designed to make payments to retirees for 15+ years

3. Limiting Early Filing Options

Right now, many people file early at 62, locking in a reduced benefit.

One proposal is to require younger workers (e.g., those 50 and under) to wait until full retirement age to claim.

This would preserve more assets in the trust over the long term.

Why Reform May Be Delayed

Unfortunately, even though the math is clear, we don’t expect Congress to make many changes before 2034. Why? Because fixing Social Security is a politically unfriendly topic.

To save the system, lawmakers must either raise taxes or cut benefits.

Neither of those options wins votes, which makes reform easy to push off.

This likely means the situation will get more tense as we approach 2034. If reforms aren’t passed in time, one possibility is a government bailout of the Social Security Trust, with additional money created to keep it solvent. While this could buy time, it doesn’t address the underlying funding imbalance—and could carry broader economic consequences.

How We Plan Around Social Security Uncertainty

For our clients, we don’t take a “wait and see” approach. Since we don’t know the exact fate of Social Security, for clients under a specific age, we build retirement plans that assume a reduction in benefits.

If Social Security benefits are reduced in the future, our clients’ plans are already designed to account for the cut, meaning their retirement income won’t be derailed.

If, on the other hand, Congress keeps Social Security fully intact, that’s fantastic—it simply means more income than we initially projected.

This conservative approach provides peace of mind and ensures that retirement strategies remain flexible no matter what happens in Washington.

The Bottom Line

Social Security faces real funding challenges, but it’s highly unlikely to disappear. Instead, it will probably undergo adjustments to ensure long-term solvency.

For retirees and pre-retirees, the key takeaway is this: don’t panic, but don’t ignore it either. Build your retirement plan with the assumption that Social Security may look different in the future. A fee-based financial planner can help you model different scenarios and build a strategy that works no matter how Congress acts.

If you’d like to explore how Social Security fits into your retirement plan, learn more about our financial planning services here.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

What Should I Do With My 401(k) From My Old Company?

When you leave a job, your old 401(k) doesn’t automatically follow you. You can leave it in the plan, roll it to your new employer’s 401(k), move it to an IRA, or cash it out. Each choice has different tax, investment, and planning implications.

Changing jobs often means leaving more than just your old desk behind. If you participated in your former employer’s 401(k) plan, you’re now faced with a decision: what should you do with that account?

It’s an important question—one that affects how you manage your retirement savings, your investment options, and potentially your tax situation. In this article, we’ll walk through the four main options for handling an old 401(k), along with the pros, cons, and planning considerations for each.

Option 1: Leave It Where It Is

Most employers allow former employees to leave their 401(k) accounts in the plan, provided the balance exceeds a minimum threshold (usually $7,000).

Pros

No immediate action required

Maintains investment options

Any growth in the account will continue to be tax-deferred

Cons

Potentially limited investment options compared to IRAs

Plan fees may be higher than alternatives

Harder to manage if you accumulate multiple old accounts

When It Makes Sense

If the old plan has strong investment options and low fees—or if you’re not ready to make a rollover decision—this can be a suitable temporary solution.

Option 2: Roll It Over to Your New Employer’s 401(k)

If your new employer offers a 401(k), you may be able to consolidate your old account into the new one.

Pros

Simplifies your retirement accounts

Keeps funds in a tax-advantaged account

May offer access to institutional fund pricing

Allows loans (if the new plan permits)

Cons

New plan may also have limited investment choices

Rollovers can take time and paperwork

Not all plans accept incoming rollovers

When It Makes Sense: If your new plan is well-managed and offers solid investment options and service, this can be a good way to consolidate and simplify your financial life.

Option 3: Roll It Over to an IRA

This is often the most flexible option for those who want greater control over their investments and potentially lower overall fees.

Pros

Broad range of investment choices

Can consolidate multiple old accounts into one

Often lower fees than 401(k) plans

More flexibility with withdrawal and Roth conversion strategies

Cons

Cannot take a loan from an IRA

Creditor protections may be weaker than in a 401(k), depending on your state

When It Makes Sense: If you’re comfortable managing your investments or working with a financial advisor, rolling into an IRA allows for more customization and control—especially when building a tax-efficient retirement income plan.

Option 4: Cash It Out

You always have the option to take the money and run—but doing so comes at a steep cost.

Pros

Provides immediate access to funds

Simple and final

Cons

Subject to income taxes

10% early withdrawal penalty if under age 59½

Permanently reduces your retirement savings

When It Makes Sense: Rarely. This is generally a last resort option, appropriate only in cases of financial emergency or if the balance is very small.

Additional Considerations

Check for Roth balances

Some plans allow Roth 401(k) contributions. If you have both pre-tax and Roth dollars, each portion must be rolled over correctly—to a Traditional IRA and Roth IRA respectively.

Watch for employer stock

If your 401(k) includes company stock, you may be eligible for Net Unrealized Appreciation (NUA) treatment, a tax strategy worth exploring with a professional.

Don’t miss the deadline

If you request a check and don’t complete a rollover within 60 days, it’s considered a distribution and taxed accordingly.

Final Thoughts

If you’ve left a job and have an old 401(k) sitting idle, now is the time to make a plan. Whether you leave it where it is, roll it over to your new plan or IRA, or—less ideally—cash it out, the decision should align with your long-term retirement goals, risk tolerance, and tax strategy.

In many cases, rolling the balance into an IRA offers the most flexibility, especially for those interested in managing taxes, investment choices, and future retirement withdrawals. If you're unsure which route is best, a financial advisor can help evaluate your options based on your full financial picture.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

What Happens If You Die Without a Will?

Dying without a will means state laws decide who inherits your assets, not you. It also creates longer, more expensive probate and leaves guardianship decisions for your children up to a judge. This article explores the risks of dying intestate and how a simple will can protect your family.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

No one likes to think about their own death, but estate planning is one of the most important financial steps you can take to protect your family and loved ones. One of the simplest — yet most critical — estate planning tools is a will.

Unfortunately, many people pass away without one. According to surveys, more than half of Americans don’t have a will in place. But what really happens if you die without a will?

State laws decide who gets your assets — not you.

The probate process becomes longer, more expensive, and more stressful for your family.

Guardians for minor children are chosen by a judge, not by you.

Children can inherit large sums at age 18 with no safeguards, which can sometimes hurt more than help.

Simple solutions exist — a basic will can often be set up for a minimal cost.

Let’s walk through what happens if you don’t have a will, why that can create complications, and what you can do to avoid these pitfalls.

State Laws Take Over

If you die without a will, you die “intestate.” This means your estate will be distributed according to your state’s intestacy laws. These laws vary by state, but most follow a general pattern:

If you’re married, your assets may be split between your spouse and children.

If you’re single with children, everything generally goes to your kids in equal shares.

If you have no spouse or children, assets may pass to your parents, siblings, nieces, nephews, or more distant relatives.

The problem? State law or a judge, who doesn’t know you or your family dynamics will decide how your estate is distributed. You lose the ability to decide who receives what, when they receive it, or under what conditions.

A Longer, More Expensive Probate Process

With a valid will, your executor follows your instructions and distributes assets relatively quickly. Without a will, the court must:

Appoint an executor (which may take time and spark disagreements).

Require appraisals of property, attorney involvement, and court oversight.

Follow state intestacy laws to distribute assets.

This makes the probate process longer, more complicated, and often more expensive. Beneficiaries can wait months — even years — before assets are fully distributed.

For families already grieving a loss, this added complexity can be emotionally draining.

The Stakes Are Higher With Minor Children

If you have children under 18, the consequences of dying without a will become even more serious.

Guardianship: A judge will appoint a guardian for your children, without knowing who you would have chosen.

Inheritance access: At age 18, children may receive their full inheritance outright.

That means a teenager could suddenly inherit hundreds of thousands of dollars from life insurance, retirement accounts, or the sale of your home. Without safeguards in place, that money may not be used wisely and could dramatically affect your child’s life path.

A properly drafted will (or even better, a trust) can set rules, such as delaying inheritance until your children reach a more mature age or providing funds gradually over time.

Probate Isn’t the Only Issue

Estate planning attorneys often recommend going one step further than a will to avoid probate altogether. Common strategies include:

Revocable living trust: Assets in a trust bypass probate and are distributed privately according to your instructions.

Transfer on Death (TOD) accounts: Bank and brokerage accounts with TOD designations pass directly to beneficiaries without probate.

Beneficiary designations: Retirement accounts and life insurance policies allow you to name beneficiaries directly, which supersedes a will.

These strategies not only streamline the distribution process but can also protect your family from unnecessary legal fees and court delays.

A Will Doesn’t Have to Be Expensive

One of the biggest misconceptions is that creating a will is time-consuming or costly. In reality, establishing a will can be very inexpensive:

Online services like LegalZoom.com or Rocket Lawyer can help you set up a simple will for a minimal fee.

While these are good starting points, we recommend working with an estate attorney if your situation is more complex — especially if you have children, significant assets, or unique wishes.

Think of a will as one of the most affordable forms of “insurance” you can buy. For a small upfront cost, you can save your family thousands of dollars, countless hours, and significant emotional stress later.

Final Thoughts

If you die without a will, the state — not you — decides how your assets are distributed and who cares for your children. The probate process becomes more costly, more time-consuming, and much more stressful for your loved ones.

The good news is that creating a will is relatively easy and inexpensive. Whether through a simple online service or a consultation with an estate attorney, taking this step ensures you stay in control and your family is protected.

At the end of the day, a will is about more than just money — it’s about peace of mind.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

What happens if you die without a will?

If you die without a will, your estate is distributed according to your state’s intestacy laws. This means a court decides who receives your assets and when, which can lead to outcomes you may not have intended.

How does dying without a will affect the probate process?

Without a will, the probate process is usually longer, more expensive, and more complicated. The court must appoint an executor, oversee asset distribution, and may require appraisals or attorney involvement—all of which add time and cost.

What happens to minor children if a parent dies without a will?

If you have minor children and no will, a judge will decide who becomes their guardian. In addition, any inheritance they receive becomes theirs outright at age 18, without safeguards to ensure it’s managed responsibly.

Can you avoid probate without a will?

Yes. Using tools like revocable living trusts, Transfer on Death (TOD) accounts, and beneficiary designations can help assets pass directly to heirs without going through probate. These strategies can save time and reduce legal expenses.

Is creating a will expensive or time-consuming?

Creating a basic will is typically affordable and straightforward. Online services can help for a low cost, while more complex situations may benefit from an estate attorney’s guidance.

Why is having a will so important?

A will ensures your wishes are honored, your loved ones are protected, and your estate is distributed efficiently. It also provides peace of mind knowing your family won’t face unnecessary legal or financial burdens during an already difficult time.

If You Retire With $1 Million, How Long Will It Last?

Is $1 million enough to retire? The answer depends on withdrawal rates, inflation, investment returns, and taxes. This article walks through different scenarios to show how long $1 million can last and what retirees should consider in their planning.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Retirement planning often circles around one big question: If I save $1 million, how long will it last once I stop working? The answer isn’t one-size-fits-all. It depends on a handful of key factors, including:

Your annual withdrawal rate

Inflation (the rising cost of goods and services over time)

Your assumed investment rate of return

Taxes (especially if most of your money is in pre-tax retirement accounts)

In this article, we’ll walk through each of these factors and then run the numbers on a few different scenarios. By the end, you’ll have a much clearer idea of how far $1 million can take you in retirement.

Step 1: Determining Your Withdrawal Rate

Your withdrawal rate is simply the amount of money you’ll need to take from your retirement accounts each year to cover living expenses. Everyone’s number looks different:

Some retirees might only need $60,000 per year after tax.

Others might need $90,000 per year after tax.

The key is to determine your annual expenses first. Then consider:

Other income sources (Social Security, pensions, part-time work, rental income, etc.)

Tax impact (if pulling from pre-tax accounts, you’ll need to withdraw more than your net spending need to cover taxes).

For example, if you need $70,000 in after-tax spending money, you might need to withdraw closer to $75,000–$90,000 per year from your 401(k) or IRA to account for taxes.

Step 2: Don’t Forget About Inflation

Inflation is the silent eroder of retirement plans. Even if you’re comfortable living on $70,000 today, that number won’t stay static. If we assume a 3% inflation rate, here’s how that changes over time:

At age 65: $70,000

At age 80: $109,000

At age 90: $147,000

Expenses like healthcare, insurance, and groceries tend to rise faster than other categories, so it’s critical to build inflation adjustments into your plan.

Step 3: The Assumed Rate of Return

Once you retire, you move from accumulation mode (saving and investing) to distribution mode (spending down your assets). This shift raises important questions about asset allocation.

During accumulation years, you weren’t withdrawing, so market dips didn’t permanently hurt your portfolio.

In retirement, selling investments during downturns locks in losses, making it harder for your account to recover.

That’s why most retirees take at least one or two “step-downs” in portfolio risk when they stop working.

For most clients, a reasonable retirement assumption is 4%–6% annual returns, depending on risk tolerance.

Step 4: The Impact of Taxes

Taxes can make a significant difference in how long your retirement savings last.

If most of your money is in pre-tax accounts (401k, traditional IRA), you’ll need to gross up withdrawals to cover taxes.

Example: If you need $80,000 after tax, and your tax bill is $10,000, you’ll really need to withdraw $90,000 from your retirement accounts.

Now, if you have Social Security income or other sources, that reduces how much you need to pull from your investments.

Example:

Annual after-tax expenses: $80,000

Grossed-up for taxes: $90,000

Social Security provides: $30,000

Net needed from retirement accounts: $60,000 (indexed annually for inflation)

Scenarios: How Long Does $1 Million Last?

Now let’s put the numbers into action. Below are four scenarios that show how long a $1 million retirement portfolio lasts under different withdrawal rates. Each assumes:

Retirement age: 65

Beginning balance: $1,000,000

Inflation: 3% annually

Investment return: 5% annually

Scenario 1: Withdrawal Rate $40,000 Per Year

Assumptions:

Annual withdrawal: $40,000 (indexed for 3% inflation)

Rate of return: 5%

Result: Portfolio lasts 36 years (until age 100).

Why not forever? Because inflation steadily raises the withdrawal amount. At age 80, withdrawals rise to $62,000/year. By age 90, they reach $83,000/year.

Math Note: For the duration math, while age 90 minus age 65 would be 35 years. We are also counting the first year age 65 all the way through age 90, which is technically 36 years. (Same for all scenarios below)

Scenario 2: Withdrawal Rate $50,000 Per Year

Assumptions:

Annual withdrawal: $50,000 (indexed for 3% inflation)

Rate of return: 5%

Result: Portfolio lasts 26 years (until age 90).

By age 80, withdrawals grow to $77,000/year. By age 90, they reach $104,000/year.

Scenario 3: Withdrawal Rate $60,000 Per Year

Assumptions:

Annual withdrawal: $60,000 (indexed for 3% inflation)

Rate of return: 5%

Result: Portfolio lasts 21 years (until age 85).

Scenario 4: Withdrawal Rate $80,000 Per Year

Assumptions:

Annual withdrawal: $80,000 (indexed for 3% inflation)

Rate of return: 5%

Result: Portfolio lasts 15 years (until age 79).

Even if you bump the return to 6%, it only extends one more year to age 80. Higher withdrawals create a significant risk of outliving your money.

Final Thoughts

If you retire with $1 million, the answer to “How long will it last?” depends heavily on your withdrawal rate, inflation, taxes, and investment returns. A $40,000 withdrawal rate can potentially last through age 100, while a more aggressive $80,000 withdrawal rate may deplete funds before age 80.

The bottom line: Everyone’s situation is unique. Your lifestyle, income sources, tax situation, and risk tolerance will shape your plan. This is why working with a financial advisor is so important — to stress-test your retirement under different scenarios and give you peace of mind that your money will last as long as you do.

For more information on our fee based financial planning services to run your custom retirement projections, please visit our website.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

What is a safe withdrawal rate in retirement?

A commonly used guideline is the 4% rule, meaning you withdraw 4% of your starting balance each year, adjusted for inflation. However, personal factors—such as market performance, expenses, and longevity—should guide your specific rate.

How does inflation affect retirement spending?

Inflation steadily increases the cost of living, which raises how much you need to withdraw each year. At a 3% inflation rate, an annual $70,000 expense today could grow to over $100,000 within 15 years, reducing how long savings can last.

Why do investment returns matter so much in retirement?

Once you start taking withdrawals, poor market performance can have a lasting impact because you’re selling investments during downturns.

How do taxes impact retirement withdrawals?

Withdrawals from pre-tax accounts like traditional IRAs and 401(k)s are taxable, so you may need to take out more than your net spending needs. For instance, needing $80,000 after tax could require withdrawing around $90,000 or more before tax.

What can help make retirement savings last longer?

Strategies like moderating withdrawal rates, maintaining some stock exposure for growth, and factoring in Social Security or pension income can extend portfolio longevity. Regularly reviewing your plan helps ensure it stays aligned with your goals and spending needs.

The Risk of Outliving Your Retirement Savings

Living longer is a blessing, but it also means your savings must stretch further. Rising costs, inflation, and healthcare expenses can quietly erode your nest egg. This article explains how to stress-test your retirement plan to ensure your money lasts as long as you do.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

When you imagine retirement, perhaps you see time with family, travel, golf, and more time for your hobbies. What many don’t realize is how two forces—longer lifespans and rising costs—can quietly erode your nest egg while you're still enjoying those moments. Living longer is a blessing, but it means your savings must stretch further. And inflation, especially for healthcare and long-term care, can quietly chip away at your financial comfort over the years. Let’s explore how these factors shape your retirement picture—and what you can do about it.

What you’ll learn in this article:

How life expectancy is evolving, and how it’s increasing the need for more retirement savings

The impact of inflation on a retiree's expenses over the long term

How inflation on specific items like healthcare and long-term care are running at much higher rates than the general rate of inflation

How retirees can test their retirement projections to ensure that they are properly accounting for inflation and life expectancy

How pensions can be both a blessing and a curse

1. Living Longer: A Good But Bad Thing

The Social Security life tables estimate that a 65-year-old male in 2025 is expected to live another 21.6 years (reaching about age 86.6), while a 65-year-old female can expect about 24.1 more years, extending to around 89.1 (ssa.gov).

That has consequences:

If a retiree spends $60,000 per year, a male might need 21.6 × $60,000 = $1,296,000 in total

A female might need 24.1 × $60,000 = $1,446,000

These totals—before considering inflation—highlight how long-term retirement can quickly become a multi-million-dollar endeavor.

2. Inflation: The Silent Retirement Thief

Inflation steadily erodes the real value of money. Over the past 20 years, average annual inflation has held near 3%. Let’s model how inflation reshapes $60,000 in annual after-tax expenses for a 65 year-old retiree over time with a 3% annual increase:

At age 80 (15 years after retirement):

$60,000 × (1.03)^15 ≈ $93,068 per yearAt age 90 (25 years after retirement):

$60,000 × (1.03)^25 ≈ $127,278 per year

In just the first 15 years, this retiree’s annual expenses increased by $33,068 per year, a 55% increase.

3. The Hidden Risk of Relying Too Much on Pensions

One of the most common places retirees feel this pinch is with pensions. Most pensions provide a fixed monthly amount that does not rise meaningfully with inflation. That can create a false sense of security in the early years of retirement.

Example:

A married couple has after-tax expenses of 70,000 per year.

They receive $50,000 from pensions and $30,000 from Social Security.

At retirement, their $80,000 of income in enough to meet their $70,000 in after-tax annual expenses.

Here’s the problem:

The $50,000 pension payment will not increase.

Their expenses, however, will rise with inflation. After 15 years at 3% inflation, those same expenses could total about $109,000 per year.

By then, their combined pension and Social Security will fall well short, forcing them to dip heavily into savings—or cut back their lifestyle.

This illustrates why failing to account for inflation often means retirees “feel fine” at first, only to face an unexpected shortfall 10–15 years later.

4. Healthcare & Long-term Care Expenses

While the general rise in expenses by 3% per year would seem challenging enough, there are two categories of expenses that have been rising by much more than 3% per year for the past decade: healthcare and long-term care. Since healthcare often becomes a large expense for individuals 65 year of age and older, it’s created additional pressure on the retirement funding gap.

Prescription drugs shot up nearly 40% over the past decade, outpacing overall inflation (~32.5%) (nypost.com).

Overall healthcare spending jumped 7.5% from 2022 to 2023, reaching $4.9 trillion—well above historical averages (healthsystemtracker.org).

In-home long-term care is also hefty—median rates for a home health aide have skyrocketed, with 24-hour care nearing $290,000 annually in some cases (wsj.com).

5. The Solution: Projections That Embrace Uncertainty

When retirement may stretch 20+ years, and inflation isn’t uniform across expense categories, guessing leads to risk. A projection-driven strategy helps you:

Model life expectancy: living until age 85 – 95 (depending on family longevity)

Incorporate general inflation (3%) on your expenses within your retirement projections

Determine if you have enough assets to retire comfortably

Whether your plan shows a wide cushion or flags a potential shortfall, you’ll make confident decisions—about savings, investments, expense reduction, or part-time work—instead of crossing your fingers.

6. Working with a Fee-Based Financial Planner Can Help

Here’s the bottom line: Living longer is wonderful, but it demands more planning in the retirement years as inflation, taxes, life expectancy, and long-term care risks continue to create larger funding gaps for retirees.

A fee-based financial planner can help you run personalized retirement projections, taking these variables into account—so you retire with confidence. And if the real world turns out kinder than your model, that's a bonus. If you would like to learn more about our fee-based retirement planning services, please feel free to visit our website at: Greenbush Financial Group – Financial Planning.

Learn more about our financial planning services here.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

How does longer life expectancy affect retirement planning?

People are living well into their 80s and 90s, meaning retirement savings must cover 20–30 years or more. The longer you live, the more years your portfolio must fund, increasing the importance of conservative withdrawal rates and sustainable planning.

Why is inflation such a big risk for retirees?

Inflation steadily raises the cost of living, reducing the purchasing power of fixed income sources like pensions. Even at a modest 3% inflation rate, living expenses can rise more than 50% over 15 years, requiring larger withdrawals from savings.

How does inflation impact pensions and fixed income sources?

Most pensions don’t increase with inflation, so their purchasing power declines over time. A pension that comfortably covers expenses at retirement may fall short within 10–15 years as costs rise, forcing retirees to draw more from savings.

Why are healthcare and long-term care costs such a concern in retirement?

Healthcare and long-term care expenses have been increasing faster than general inflation. Costs for prescriptions, medical services, and in-home care can grow at 5–7% annually, putting additional strain on retirement savings.

How can retirees plan for inflation and longevity risk?

Running detailed retirement projections that factor in inflation, longer life expectancy, and varying rates of return helps reveal whether savings are sufficient. This approach allows retirees to make informed decisions about spending, investing, and lifestyle adjustments.

When should retirees work with a financial planner?

Consulting a fee-based financial planner early in the retirement planning process can help test different inflation and longevity scenarios. A planner can build customized projections and ensure your plan remains flexible as costs and life circumstances evolve.

How Much Money Will You Need to Retire Comfortably?

Retirement planning isn’t just about hitting a number. From withdrawal rates and inflation to taxes and investment returns, several factors determine if your savings will truly last. This article explores how to test your retirement projections and build a plan for financial security.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

As a Certified Financial Planner who runs retirement projections on a daily basis, one of the most common questions I get is: “How much money do I need to retire?”

The answer may surprise you—because there’s no universal number. The amount you’ll need depends largely on one thing: your expenses.

In this article, we’ll walk through:

Why expenses are the biggest driver of how much you need to retire

How inflation impacts retirement spending

Why the type of account you own matters

The importance of factoring in all your income sources

A quick 60-second way to test your own retirement readiness

Expenses: The Biggest Driver

When you ask, “Can I retire comfortably?”, the first question to answer is: How much do you spend each year?

For example:

If your expenses are $40,000 per year, then $500,000 in retirement savings could potentially be enough—especially if you’re supplementing withdrawals with Social Security or a pension.

But if your expenses are $90,000 per year, that same $500,000 likely won’t stretch nearly as far.

Your retirement lifestyle drives your retirement savings need. Someone with modest expenses may not need millions to retire, while someone with higher spending will require significantly more.

Don’t Forget About Inflation

It’s not just today’s expenses you need to plan for—it’s tomorrow’s too. Inflation quietly eats away at your purchasing power, making your cost of living higher every single year.

Here’s an example:

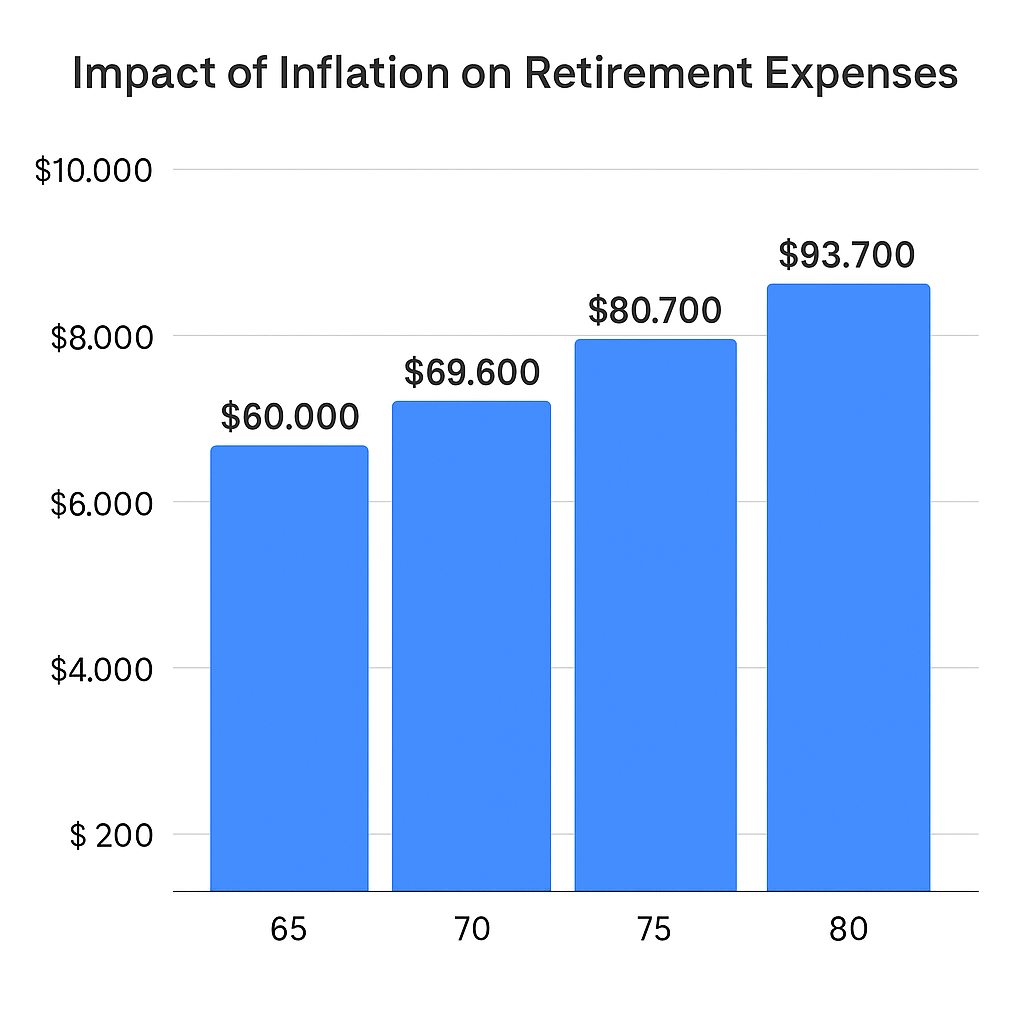

At age 65, your expenses are $60,000 per year.

If expenses rise at 3% annually, by age 80 they’ll be roughly $93,700 per year.

That’s a 50% increase in just 15 years—and you’ll need your retirement assets to keep up.

This is one of the hardest factors for individuals to quantify without financial planning software. Inflation not only increases expenses, but it changes your withdrawal rate from investments, which can impact how long your money lasts.

The Type of Account Matters

Not all retirement accounts are created equal. The type of retirement/investment accounts you own has a big impact on whether you can retire comfortably.

Pre-tax accounts (401k, traditional IRA): Every dollar withdrawn is taxed as ordinary income. A $1,000,000 account might really be worth closer to $700,000 after taxes.

Roth accounts: Withdrawals are tax-free, making these extremely valuable in retirement.

After-tax brokerage accounts: Withdrawals often receive more favorable capital gains treatment, so the tax drag can be lighter compared to pre-tax accounts.

Cash: Offers liquidity but typically earns little return, making it best for short-term expenses.

In short: Roth and after-tax brokerage accounts often provide more after-tax value compared to pre-tax accounts.

Factor in All Your Income Sources

Getting a general idea of your retirement income picture is key. This means adding up:

Social Security benefits

Pensions

Investment income (dividends, interest, etc.)

Part-time income in retirement

Withdrawals from retirement accounts

Once you total these income sources, you’ll need to apply the tax impact. Only then can you compare your after-tax income against your after-tax expenses (adjusted for inflation each year) to see if there’s a gap.

This is exactly how financial planners build retirement projections to determine sustainability.

Find Out If You Can Retire in 60 Seconds

Curious if you’re on track? We’ve built a 60-second retirement check-up that can help you quickly see if you have enough to retire.

Bottom line: There’s no magic retirement number. The amount you need depends on your expenses, inflation, account types, and income sources. By running the numbers—and stress-testing them with a financial planner—you can gain the confidence to know whether you’re truly ready to retire comfortably.

Partner with a Fee-Based Financial Planner to Build Your Retirement Plan

While rules of thumb and calculators can provide a helpful starting point, everyone’s retirement picture looks different. Your income needs, lifestyle goals, and unique financial situation will ultimately determine how much you need to retire comfortably.

Working with a fee-based financial planner can help take the guesswork out of retirement planning. A planner will create a customized strategy that factors in your retirement expenses, investments, Social Security, healthcare, and tax planning—so you know exactly where you stand and what adjustments to make.

If you’d like to explore your own numbers and build a retirement roadmap, we’d love to help. Learn more about our financial planning services here.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

How much money do I need to retire?

There’s no single number that fits everyone—the right amount depends primarily on your annual expenses, lifestyle, and income sources. A retiree spending $40,000 per year will need far less savings than someone spending $90,000.

Why are expenses the most important factor in retirement planning?

Your spending habits determine how much income your portfolio must generate. Knowing your annual expenses helps estimate your withdrawal needs, which directly drives how large your retirement savings must be.

How does inflation affect retirement spending?

Inflation gradually increases the cost of living, reducing the purchasing power of your money. At a 3% inflation rate, $60,000 in annual expenses today could rise to about $94,000 in 15 years, meaning your savings must grow to keep pace.

How does the type of retirement account impact how much you need to save?

Withdrawals from pre-tax accounts like 401(k)s and traditional IRAs are taxable, so you may need to save more to cover taxes. Roth IRAs and brokerage accounts often provide more after-tax value, since withdrawals may be tax-free or taxed at lower rates.

What income sources should I include when estimating retirement readiness?

Include all sources such as Social Security, pensions, dividends, part-time income, and withdrawals from savings. Comparing your total after-tax income against your inflation-adjusted expenses helps reveal whether you’re financially ready to retire.

How can I quickly estimate if I’m on track for retirement?

A simple way is to compare your projected annual expenses (adjusted for inflation) with your expected retirement income. Working with a fee-based financial planner can oftern provide a more comprehensive approach to answering the question “Do I have enough to retire?”