Special Rules for S-Corps with Employer-Sponsored Retirement Plans

Missing a Required Minimum Distribution can feel overwhelming, but the rules have changed under SECURE Act 2.0. In this article, we explain how to correct a missed RMD, reduce IRS penalties, and file the right tax forms to stay compliant.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

S-Corporations can be an excellent structure for small business owners, especially from a tax perspective. But when it comes to retirement plans—such as 401(k)s and profit-sharing plans—S-Corps play by a slightly different set of rules compared to other business entities. Understanding these differences is critical for maximizing retirement savings and avoiding unpleasant surprises.

In this article, we’ll cover:

How compensation is defined for S-Corp owners in a retirement plan

Why relying too heavily on distributions can limit retirement savings

The impact of employer contributions for S-Corp owners with staff

Timing considerations for employee deferrals in S-Corps versus pass-through entities

A practical example that shows how these rules work in real life

W-2 Wages Drive Retirement Contributions for S-Corp Owners

Here’s the key difference:

Partnerships and sole proprietorships – Contributions are based on total pass-through earnings from the business.

S-Corporations – Contributions are based only on W-2 wages paid to the owner.

This matters because many S-Corp owners try to minimize their W-2 salary and take more of their income in shareholder distributions. Distributions avoid payroll taxes, which can be a big tax advantage. But retirement plans only look at W-2 wages when calculating contribution limits.

Example: High Income, Low W-2

Suppose an S-Corp owner earns $500,000 total income, but only pays themselves $100,000 in W-2 wages.

Maximum employer contribution = 25% of W-2 wages = $25,000

Add employee salary deferral = up to $23,500 (2025 limit, or $31,000 if age 50+)

Total = roughly $48,500 (or $56,000 with catch-up)

That’s far below the 2025 annual addition limit of $70,000 ($77,500 with catch-up). By keeping W-2 wages artificially low, the owner unintentionally caps their retirement contributions.

The Ripple Effect on Employees

If the owner sets their employer contribution at 25% of W-2 compensation, that percentage generally applies to eligible employees as well.

In our example, if the owner receives a 25% contribution on $100,000 ($25,000), employees may also need to receive a large employer contribution for the plan to pass testing.

For a company with multiple employees, this can become a very expensive retirement plan design.

Timing of Deferrals: Another S-Corp Quirk

Another important difference involves the timing of employee salary deferrals:

S-Corp owners are on payroll, so any employee deferrals must be processed through payroll no later than the final paycheck in December. If you wait until after year-end, it’s too late to make employee deferrals for that tax year.

Partnership or sole proprietor owners may have more flexibility, since contributions can often be made up to the tax filing deadline (with extensions) and still count toward the prior year.

Translation: If you’re an S-Corp owner, don’t wait until tax season to think about retirement contributions. Deferrals need to be in place before December 31st.

Key Takeaways for S-Corp Owners

Only W-2 wages count toward retirement contributions, not shareholder distributions.

Keeping W-2 wages too low may limit your ability to maximize contributions.

Large employer contributions for the owner can trigger equally large contributions for employees.

Employee salary deferrals must run through payroll and be completed by the last December paycheck.

Careful planning throughout the year—not just at tax time—is essential.

If you’re an S-Corp owner considering a retirement plan, make sure your payroll and compensation strategy aligns with your retirement savings goals. The right plan design can help you strike a balance between tax efficiency today and meaningful retirement wealth in the future.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

How do retirement plan contributions work for S-Corporation owners?

For S-Corp owners, retirement contributions are based only on W-2 wages—not total business income or shareholder distributions. This makes salary decisions especially important for maximizing 401(k) or profit-sharing plan contributions.

Why can keeping W-2 wages low hurt retirement savings for S-Corp owners?

While taking more income as shareholder distributions can reduce payroll taxes, it also limits how much you can contribute to a retirement plan. Employer contributions are capped at 25% of W-2 wages, so a lower salary means smaller allowable contributions.

How do employer contributions for owners affect employees in an S-Corp retirement plan?

If an owner contributes a high percentage of their W-2 income (such as 25%), nondiscrimination testing may require giving the same percentage to eligible employees. This can significantly increase plan costs for businesses with multiple staff members.

When must S-Corp owners make 401(k) salary deferrals?

Employee deferrals must be processed through payroll no later than the final paycheck of the year. Unlike partnerships or sole proprietors, S-Corp owners cannot make deferrals after December 31 for the prior tax year.

Can S-Corp owners include distributions when calculating 401(k) contributions?

No. Only W-2 wages qualify for retirement plan contribution calculations. Distributions from the S-Corp are not considered “earned income” for 401(k) or profit-sharing purposes.

What steps should S-Corp owners take to maximize retirement contributions?

Plan ahead by setting a reasonable W-2 salary that supports both tax efficiency and contribution goals. Coordinate payroll timing, plan design, and employee testing requirements with your tax advisor and retirement plan administrator early in the year.

How to Correct Missed Required Minimum Distributions (RMDs)

Missing a Required Minimum Distribution can feel overwhelming, but the rules have changed under SECURE Act 2.0. In this article, we explain how to correct a missed RMD, reduce IRS penalties, and file the right tax forms to stay compliant.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Missing a Required Minimum Distribution (RMD) can cause a lot of stress, especially when you hear the words IRS excise tax. Fortunately, the rules around missed RMDs were updated under the SECURE Act 2.0, which provides some relief compared to the old law. In this article, we’ll break down:

What happens if you miss an RMD and how to correct it

The updated excise tax penalties under SECURE Act 2.0

The “first year” April 1st rule and why you may need to take two RMDs in one year

The new IRS guidance for beneficiaries who inherit retirement accounts

What tax forms need to be filed if you miss an RMD

A quick before-and-after look at the old rules versus SECURE Act 2.0

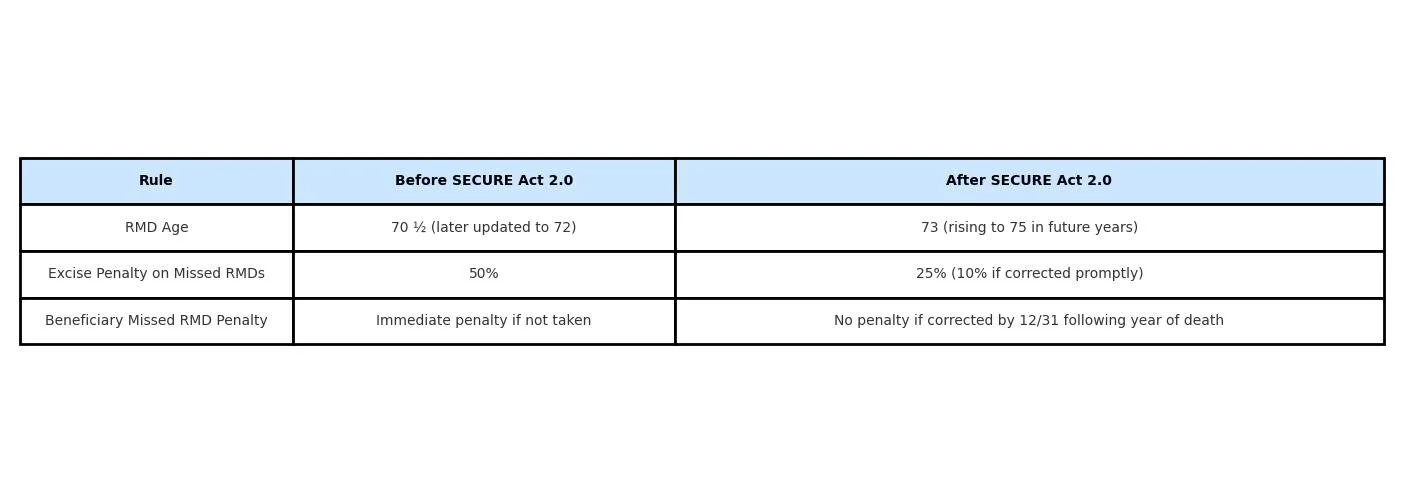

What Happens if You Miss an RMD?

If you forget to take an RMD, the IRS assesses an excise tax penalty on the amount you should have withdrawn. Under the old law, that penalty was steep—50% of the missed RMD.

Under SECURE Act 2.0, the penalty was reduced to a much more manageable amount:

25% penalty on the missed distribution.

If corrected quickly (by taking the missed RMD and filing the proper paperwork), the penalty may be further reduced to 10%.

Example: If you missed a $10,000 RMD:

Old rule: You owed $5,000 in penalties.

New rule: You may owe only $1,000 (if corrected promptly).

The First-Year April 1st Rule

When you reach RMD age (currently age 73 under SECURE Act 2.0), your very first required distribution doesn’t have to be taken in that calendar year. Instead, you can delay it until April 1st of the following year.

But here’s the catch: if you delay your first RMD, you’ll still need to take two RMDs in that next year—the delayed one (by April 1st) plus the regular one (by December 31st).

Example:

Jane turns 73 in 2025.

She can delay her first RMD until April 1, 2026.

If she does, she must also take her 2026 RMD by December 31, 2026—meaning two taxable distributions in one year.

IRS Relief for Inherited Accounts (New Guidance)

For beneficiaries of inherited IRAs or retirement accounts, the IRS just issued new guidance under SECURE Act 2.0.

If a decedent had an RMD due in the year of their death and it wasn’t taken, the beneficiary must still withdraw it. However, the IRS has clarified that as long as the missed RMD is taken by December 31st of the year following the decedent’s death, no excise penalty will be assessed.

This is a significant update and provides more flexibility for beneficiaries who may be navigating a difficult time.

Before SECURE Act 2.0 vs. After

Filing Tax Forms for Missed RMDs

If you missed an RMD, you need to do two things:

Take the missed distribution as soon as possible.

File Form 5329 with your federal tax return to report the missed RMD and calculate the excise penalty.

If you qualify for the reduced 10% penalty, you’ll indicate this on Form 5329.

The actual RMD amount you withdraw will be reported on your Form 1099-R and included in your taxable income for the year you take it.

In some cases, the IRS has historically waived penalties if you can show “reasonable cause” for missing the RMD and that you’ve corrected the mistake. While SECURE Act 2.0 made the penalties less severe, requesting a waiver may still be an option worth considering with your tax professional.

Key Takeaways

SECURE Act 2.0 lowered the penalty for missed RMDs from 50% down to 25% (or 10% if fixed promptly).

The first-year April 1st rule gives you some flexibility but may cause two RMDs in one year.

Beneficiaries now have until December 31st of the year following the decedent’s death to take missed RMDs without penalty.

File Form 5329 to report missed RMDs and claim reduced penalties.

Missing an RMD isn’t ideal, but it’s not the end of the world—especially under the updated SECURE Act 2.0 rules. The most important step is to correct it quickly and make sure you file the proper paperwork with your tax return.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

What happens if you miss a Required Minimum Distribution (RMD)?

If you miss an RMD, the IRS may assess an excise tax penalty on the amount that should have been withdrawn. Under SECURE Act 2.0, the penalty is now 25% of the missed amount, reduced to 10% if you correct the mistake promptly by taking the distribution and filing the appropriate tax form.

How did SECURE Act 2.0 change the penalties for missed RMDs?

Previously, missing an RMD triggered a 50% penalty on the shortfall. SECURE Act 2.0 lowered this to 25%, with a further reduction to 10% if the missed distribution is corrected in a timely manner. This change provides much-needed relief for retirees who make honest errors.

What is the April 1st rule for first-year RMDs?

When you first reach RMD age (currently 73), you can delay your initial withdrawal until April 1st of the following year. However, doing so means you must take two RMDs that year—the delayed one and the new year’s required amount—potentially increasing your taxable income.

What are the new IRS rules for inherited IRAs and missed RMDs?

If a deceased account owner had an RMD due in the year of death, the beneficiary must still take that distribution. Under new guidance, if the missed RMD is taken by December 31st of the year following the death, no excise penalty will apply.

What should you do if you missed an RMD?

Take the missed distribution as soon as possible and file IRS Form 5329 with your tax return to report the oversight and calculate any applicable penalty. Your financial or tax advisor can help determine if you qualify for the reduced 10% penalty or a possible waiver.

Can the IRS waive the RMD penalty entirely?

Yes. The IRS may waive the penalty if you can demonstrate reasonable cause for missing the RMD and show that you corrected the issue promptly. While SECURE Act 2.0 reduced the penalties, requesting a waiver may still be worthwhile in some cases.

Should You Withhold Taxes from Your Social Security Benefit?

Social Security benefits can be taxable at the federal level—and in some states. Should you withhold taxes directly from your benefit or make quarterly estimated payments? This guide explains your options, deadlines, and strategies to avoid IRS penalties.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

For many retirees, Social Security is a cornerstone of their retirement income. But what sometimes comes as a surprise is that Social Security benefits can be subject to federal income tax—and in a few cases, state income tax as well. This raises an important planning question: should you withhold taxes directly from your Social Security benefit, or handle them another way?

Let’s walk through the key considerations.

Social Security Withholding Options

The Social Security Administration (SSA) allows you to elect to have federal income taxes withheld directly from your monthly benefit. Unlike wages, where you can set a specific withholding percentage, Social Security offers fixed percentage options:

7%

10%

12%

22%

These percentages are applied to your total monthly benefit, and the withheld amount is sent directly to the IRS. This system is called voluntary withholding, and it can be a convenient way to avoid unexpected tax bills at the end of the year.

How Social Security Is Taxed at the Federal Level

Whether or not your Social Security benefit is taxable depends on your provisional income, which includes:

Your adjusted gross income (AGI), plus

Any tax-exempt interest, plus

50% of your Social Security benefits

Depending on your filing status and income level:

Single filers: If provisional income is between $25,000 and $34,000, up to 50% of your Social Security is taxable. Above $34,000, up to 85% of benefits may be taxable.

Married filing jointly: If provisional income is between $32,000 and $44,000, up to 50% of benefits are taxable. Above $44,000, up to 85% of benefits may be taxable.

It’s important to note that no one pays tax on more than 85% of their Social Security benefit.

State Taxation of Social Security

Most states do not tax Social Security benefits. However, as of now, 12 states do tax Social Security in some form:

Colorado

Connecticut

Kansas

Minnesota

Montana

Nebraska

New Mexico

Rhode Island

Utah

Vermont

West Virginia

Wisconsin

Each state has its own rules, income thresholds, and exemptions, so the actual impact can vary significantly.

What If You Don’t Withhold? Estimated Tax Payments

If you choose not to have taxes withheld from your Social Security benefits, you may need to make quarterly estimated tax payments to the IRS. These payments cover your expected federal tax liability and prevent penalties.

The deadlines for estimated tax payments are:

April 15 – for income earned January 1 through March 31

June 15 – for income earned April 1 through May 31

September 15 – for income earned June 1 through August 31

January 15 (of the following year) – for income earned September 1 through December 31

How to Elect Withholding from Your Social Security Benefit

You can elect to have taxes withheld from your Social Security in two ways:

Online – Log into your my Social Security account and update your withholding preferences electronically.

Paper Form – Complete IRS Form W-4V (Voluntary Withholding Request) and mail it to your local Social Security office.

Once processed, your elected withholding percentage will be applied to each monthly benefit.

IRS Penalties for Not Withholding or Paying Estimated Taxes

If you fail to withhold taxes or make sufficient estimated tax payments, the IRS may assess underpayment penalties. These penalties are essentially interest charges, calculated on the unpaid balance for each quarter you were short.

The penalty is based on:

The amount underpaid, and

The length of time the payment was late

The interest rate is tied to the federal short-term interest rate plus 3% and is adjusted quarterly.

For retirees living on fixed income, these penalties can feel like an unnecessary burden. Electing withholding or staying current with estimated payments can help avoid these surprises.

Final Thoughts

For many retirees, setting up withholding directly from Social Security benefits is the easiest way to stay on top of taxes. It provides peace of mind, ensures compliance, and avoids the hassle of quarterly estimated payments.

However, every situation is unique. The decision should factor in your other sources of income, state tax laws, and overall tax bracket.

Working with a financial planner or tax professional can help determine whether withholding, estimated payments, or a combination of both makes the most sense for you.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

Are Social Security benefits taxable?

Depending on your total income, up to 85% of your Social Security benefits may be subject to federal income tax. The amount taxed is based on your provisional income—which includes your adjusted gross income, tax-exempt interest, and half of your Social Security benefits.

How can I have taxes withheld from my Social Security benefits?

You can elect voluntary withholding through the Social Security Administration. Fixed percentages of 7%, 10%, 12%, or 22% can be withheld from each monthly payment and sent directly to the IRS to cover your federal tax liability.

How do I request tax withholding from my Social Security payments?

You can make the election online through your my Social Security account or by filing IRS Form W-4V (Voluntary Withholding Request) with your local Social Security office. Once processed, the withholding percentage applies automatically to future payments.

Which states tax Social Security benefits?

Most states do not tax Social Security, but a handful—including Colorado, Kansas, Minnesota, Montana, Nebraska, New Mexico, Rhode Island, Utah, Vermont, West Virginia, Wisconsin, and Connecticut—do in some form. Rules and exemptions vary by state.

What happens if I don’t withhold taxes from my Social Security income?

If you choose not to withhold, you may need to make quarterly estimated tax payments to the IRS. Missing these payments or paying too little can result in underpayment penalties and interest charges.

When are quarterly estimated tax payments due?

Estimated payments are typically due on April 15, June 15, September 15, and January 15 of the following year. These payments cover taxes owed on income not subject to withholding, including Social Security, pensions, and investment income.

How can retirees avoid IRS underpayment penalties?

Setting up withholding directly from Social Security benefits is often the easiest option. Alternatively, retirees can work with a tax professional to estimate their annual tax liability and adjust quarterly payments accordingly to avoid penalties.

Understanding Self-Employment Tax: A Guide for the Newly Self-Employed

Self-employment taxes can catch new business owners off guard. Our step-by-step guide explains the 15.3% tax rate, quarterly deadlines, and strategies to avoid costly mistakes.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Becoming self-employed can be one of the most rewarding career moves you’ll ever make. It comes with flexibility, independence, and the ability to control your own destiny. But it also comes with new responsibilities—particularly when it comes to taxes. One of the first financial hurdles new business owners encounter is understanding self-employment tax and how to keep up with their tax obligations throughout the year.

For business owners learning these rules for the first time, here is the step-by-step breakdown of what you need to know.

What Is Self-Employment Tax?

When you work as an employee and receive a W-2, your employer withholds Social Security and Medicare taxes from your paycheck. What many don’t realize is that your employer is paying half of those taxes on your behalf.

When you’re self-employed, however, you are both the employer and the employee. That means you’re responsible for the full 15.3% self-employment tax (12.4% for Social Security and 2.9% for Medicare) on your net earnings. If your income is above certain thresholds, an additional 0.9% Medicare surtax may apply.

This tax is in addition to federal and state income taxes, which makes planning ahead critical.

Estimated Tax Payments and Deadlines

Unlike W-2 employees, there’s no paycheck system automatically sending taxes to the government for you. The IRS expects you to make quarterly estimated tax payments. These payments cover both your income tax liability and your self-employment tax.

The deadlines for estimated tax payments are:

April 15 – for income earned January 1 through March 31

June 15 – for income earned April 1 through May 31

September 15 – for income earned June 1 through August 31

January 15 (of the following year) – for income earned September 1 through December 31

If the due date falls on a weekend or holiday, the deadline shifts to the next business day.

How Are Estimated Taxes Calculated?

The IRS gives you two main methods for calculating estimated taxes, sometimes called the “safe harbor” rules:

Prior-Year Method (110% Rule)

If your adjusted gross income was more than $150,000 in the previous year (or $75,000 if single), you can avoid penalties by paying 110% of your prior year’s total tax liability in equal quarterly installments.

If your income was below those thresholds, the requirement is 100% of your prior year’s tax liability.

Current-Year Method

Alternatively, you can calculate your actual expected tax liability for the current year and make payments to cover 90% of that amount.

What Happens If You Don’t Pay Estimated Taxes?

Failing to make estimated tax payments can lead to IRS penalties. These are generally underpayment penalties, calculated based on the amount you should have paid each quarter compared to what you actually paid.

In addition to penalties, you’ll still owe the unpaid taxes at year-end. This often creates a cash flow crisis for new self-employed individuals who didn’t set money aside during the year.

The IRS does offer some relief if:

You owe less than $1,000 in tax after subtracting withholding and credits, or

You paid at least 90% of your current-year tax liability (or 100%/110% of your prior year’s tax liability, depending on income).

Still, the safest strategy is to set aside a portion of each payment you receive for taxes and make your estimated payments on time.

How IRS Penalties Are Calculated?

The IRS calculates underpayment penalties using two key components:

Amount of Underpayment – The penalty is based on how much you should have paid each quarter versus how much you actually paid.

Time Period of Underpayment – The penalty is essentially interest charged on the shortfall, starting from the due date of the missed payment until the date you make it.

The interest rate used is tied to the federal short-term interest rate plus 3%. This rate changes quarterly, so the penalty amount can vary depending on when the shortfall occurred.

For example:

If you owed $4,000 in estimated payments for a quarter but only paid $2,000, the IRS considers the $2,000 shortfall late.

Interest is charged daily on the unpaid portion until you make up the difference or file your return.

While penalties may seem small at first, they add up quickly—especially if you consistently underpay throughout the year.

Why Taxes Become More Complex When You’re Self-Employed

For most W-2 employees, tax filing is relatively straightforward—gather a W-2 or two, maybe add a few deductions, and you’re done. For the self-employed, the process quickly becomes more involved:

Tracking business expenses for deductions (supplies, mileage, home office, etc.).

Paying both sides of Social Security and Medicare taxes.

Dealing with quarterly estimated payments.

Understanding rules around depreciation, retirement plan contributions, and health insurance deductions.

Because of these added layers, we strongly recommend engaging an experienced accounting firm or tax professional, especially in your first few years. This not only ensures compliance but also frees up your time to focus on building your business instead of spending evenings trying to interpret the tax code.

Final Thoughts

Transitioning from employee to self-employed entrepreneur comes with an exciting new level of independence—but it also requires discipline. Understanding self-employment tax, staying on top of quarterly estimated payments, and planning ahead for income tax can help you avoid costly surprises at year-end.

Working with a qualified tax professional or financial planner can help you estimate payments accurately, maximize deductions, and keep your business finances running smoothly.

Remember: as a self-employed individual, you are your own payroll department. Treating taxes like a regular business expense is the best way to stay ahead and protect your financial success.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

What is self-employment tax, and who has to pay it?

Self-employment tax covers both the employee and employer portions of Social Security and Medicare taxes, totaling 15.3%. Anyone earning $400 or more in net self-employment income must generally pay this tax, in addition to regular income taxes.

How often do self-employed individuals have to pay taxes?

The IRS requires quarterly estimated tax payments to cover both income and self-employment taxes. Payments are typically due April 15, June 15, September 15, and January 15 of the following year.

How can I calculate my estimated tax payments?

You can use the “safe harbor” rules: pay 100% of your prior year’s tax liability (110% if your income was over $150,000) or 90% of your current year’s expected tax liability. These methods help avoid IRS underpayment penalties.

What happens if I don’t make estimated tax payments?

Missing payments or underpaying can result in IRS penalties and interest, calculated based on how much you underpaid and for how long. Even if penalties apply, you’ll still owe the unpaid taxes at year-end.

How are IRS penalties for underpayment calculated?

Penalties function like interest, accruing daily on any shortfall from the payment due date until it’s paid. The rate is the federal short-term interest rate plus 3%, adjusted quarterly.

Why is tax planning more complex for self-employed individuals?

Self-employed taxpayers must track deductible expenses, manage quarterly payments, pay both sides of payroll taxes, and navigate complex deductions like home office or retirement contributions. Professional guidance can simplify compliance and help maximize deductions.

What’s the best way to stay on top of taxes when self-employed?

Set aside a portion of every payment you receive for taxes, make quarterly estimated payments on time, and work with a tax professional to stay compliant. Treating taxes as a regular business expense helps prevent surprises at year-end.

Residential Solar Tax Credit Eliminated Under the Big Beautiful Tax Bill: What It Means for Homeowners

The recently passed Big Beautiful Tax Bill made headlines for raising the federal estate tax exemption and increasing the SALT deduction cap, but not all of the provisions were taxpayer-friendly. One particularly significant change that’s flying under the radar is the elimination of the 30% Residential Solar Tax Credit—a program that’s been central to the rise in home solar installations over the past decade.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

The recently passed Big Beautiful Tax Bill made headlines for raising the federal estate tax exemption and increasing the SALT deduction cap, but not all of the provisions were taxpayer-friendly. One particularly significant change that’s flying under the radar is the elimination of the 30% Residential Solar Tax Credit—a program that’s been central to the rise in home solar installations over the past decade.

If you're a homeowner considering solar, you now have a deadline: install by December 31, 2025, or you’ll lose access to this valuable credit entirely. And the ripple effects could go well beyond individual tax savings.

Let’s break down what’s changing, what it means for homeowners and the energy grid, and how the solar industry may be reshaped by this policy shift.

What Is the Residential Solar Tax Credit?

The Residential Clean Energy Credit—commonly referred to as the 30% solar tax credit—allows homeowners to deduct 30% of the cost of installing solar panels, battery storage systems, and other qualifying equipment from their federal tax bill.

For example, if your solar installation costs $30,000, the credit could reduce your federal tax liability by $9,000. This credit has been one of the most effective incentives for encouraging adoption of clean energy at the residential level.

The Credit Is Going Away—Here’s the Timeline

Under the Big Beautiful Tax Bill, the federal solar tax credit is officially repealed for residential homeowners after December 31, 2025. Here’s what you need to know:

Installations must be fully complete and placed in service by December 31, 2025 to qualify for the 30% credit.

There is no phaseout—the credit simply ends.

The repeal applies to all residential installations, including solar panels, inverters, and eligible battery storage systems.

This means homeowners considering solar need to act quickly, as installations can take several months from contract to completion.

Higher Utility Bills on the Horizon?

The elimination of the solar credit could also have macro-level consequences. Here's why:

Fewer homeowners are likely to install solar once the credit expires, meaning less distributed generation contributing to local grids.

At the same time, electricity demand is rising sharply:

AI data centers are consuming massive amounts of power

More Americans are charging electric vehicles (EVs) at home

Electrification trends are increasing energy use in heating, cooking, and water systems

With less residential solar feeding energy back into the grid and more demand pulling from it, utility companies may need to invest in expensive infrastructure upgrades—costs that could ultimately be passed on to consumers in the form of higher utility bills.

In other words, the removal of the credit doesn’t just impact those who install solar—it could raise costs for those who don’t.

Solar Installation Industry Faces Uncertainty

The solar industry, which has grown rapidly in recent years, could face significant headwinds after the credit expiration. Many residential solar installers have built their business models around the financial appeal of the 30% tax credit.

Once that incentive disappears:

Residential demand is expected to drop sharply, especially among middle-income homeowners.

Smaller solar installation companies—which rely heavily on residential volume—could experience contraction, layoffs, or closures.

The market may shift focus to commercial-scale solar, battery backup systems, and states with additional local incentives—but that won't be enough to fully offset the change.

Consumers should be prepared for less pricing competition, longer wait times, and fewer installer options if demand falls off and the industry consolidates.

Final Thoughts: Should You Move Forward With Solar Now?

If you’re on the fence about going solar, the window to maximize your benefit is narrowing. Here's what you should consider:

Act soon: Begin the planning process now to ensure you can complete installation before year-end 2025.

Get quotes from multiple installers: With high demand expected before the credit expires, early planning can help avoid cost inflation and scheduling delays.

Run the numbers: Even without the credit, solar can make financial sense depending on your local utility rates, energy usage, and how long you plan to stay in your home. But with the credit? The payback period shortens considerably.

Summary

The 30% residential solar tax credit ends after December 31, 2025.

Homeowners must install and place systems in service before that date to claim the credit.

Fewer installations and higher energy demands could mean higher utility costs for everyone.

The solar installation industry may contract, affecting consumer pricing and service availability.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What is the 30% Residential Solar Tax Credit?

The Residential Clean Energy Credit allows homeowners to deduct 30% of the total cost of installing solar panels, inverters, battery storage, and related equipment from their federal tax bill. For example, a $30,000 system could reduce your tax liability by $9,000.

When does the solar tax credit expire?

Under the Big Beautiful Tax Bill, the federal residential solar tax credit ends after December 31, 2025. To qualify, systems must be fully installed and placed in service before that date. There is no phaseout—the credit simply disappears beginning in 2026.

Does the credit apply to battery storage systems?

Yes. The 30% credit covers qualifying home battery systems that store energy from solar panels or the electric grid. However, these installations must also be completed by the end of 2025 to qualify.

What happens if I install solar after 2025?

After December 31, 2025, there will be no federal tax credit for residential solar installations. Homeowners installing after that date will need to rely solely on any available state or utility-level incentives.

How could this change affect utility bills?

Without the federal incentive, fewer homeowners are expected to install solar panels. Combined with growing electricity demand from electric vehicles, AI data centers, and home electrification, utilities may face higher costs that could ultimately raise rates for all consumers.

How might the solar industry be impacted by the credit’s repeal?

Residential solar demand is expected to decline sharply after 2025. Smaller installation companies could face consolidation or closures, while consumers may see higher prices and longer wait times as the market contracts.

Should homeowners move forward with solar now?

If you’re considering solar, it’s best to act soon. Starting early ensures installation before the 2025 deadline and locks in the 30% tax credit. Even with strong local incentives, the loss of this federal benefit could significantly increase system payback times after 2025.

The New $6,000 Senior Tax Deduction Explained

The Big Beautiful Tax Bill that just passed is reshaping the tax landscape for many Americans, but one provision that stands out for retirees is the introduction of a new $6,000 senior tax deduction. This benefit, aimed at providing additional tax relief for older taxpayers, adds a generous layer of savings on top of the regular standard deduction and the existing age-based deduction.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

The Big Beautiful Tax Bill that just passed is reshaping the tax landscape for many Americans, but one provision that stands out for retirees is the introduction of a new $6,000 senior tax deduction. This benefit, aimed at providing additional tax relief for older taxpayers, adds a generous layer of savings on top of the regular standard deduction and the existing age-based deduction.

This new deduction took the place of the promised “100% tax-free social security benefits,” which was too costly to include in the new tax bill.

But as with many of the bill’s provisions, there are income limitations and expiration dates to be aware of. In this article, we break down how the deduction works, who qualifies, and how to make the most of it before it sunsets in 2028.

What Is the New $6,000 Senior Tax Deduction?

Beginning in 2025, taxpayers aged 65 or older will be eligible for a new $6,000 federal tax deduction. This deduction is designed to reduce taxable income and is stacked on top of the standard deduction and the existing senior (age-based) additional deduction.

In Addition to Existing Age 65 $2,000 Deduction

The new $6,000 Senior Deduction is in addition to both the standard deduction and the existing enhanced standard deduction from individual age 65 and older. The existing enhanced senior deduction for 2025 is $2,000 for single filers and head of household, and $1,600 per qualifying individual for married couples filing jointly or separately.

If both spouses are age 65 or older, they both qualify for the $6,000 Senior Deduction ($12,000 combined).

This deduction can result in significant tax savings, especially for retirees living on fixed incomes who may not qualify for other tax credits or deductions.

Income Phase-Out Rules

The deduction is not available to all seniors—there’s an income cap. The new deduction begins to phase out at moderate income levels:

How the Phase-Out Works

However, the deduction is gradually reduced—potentially to $0—if your Modified Adjusted Gross Income (MAGI) exceeds the applicable threshold. Once past that line:

The deduction is reduced by six cents for every $1 over the threshold.

At $175,000 MAGI for singles or $250,000 for joint filers, the deduction is fully phased out.

Example:

Let’s say you’re single and your MAGI is $100,000 in 2025:

That’s $25,000 over the $75,000 threshold.

Multiply that by $0.06:

$25,000 × $0.06 = $1,500 reductionResult:

$6,000 deduction − $1,500 = $4,500 allowable deduction

The reduction applies dollar-for-dollar across the entire overage range. The closer your MAGI is to the top of the phase-out range, the smaller your deduction becomes.

Planning Tip:

If you’re near the phaseout limit, consider deferring income (like IRA withdrawals or capital gains) or increasing deductions (such as HSA contributions or qualified charitable distributions) to stay under the threshold and preserve the full deduction.

When Does It Start (and End)?

This is a temporary provision of the tax code.

Effective Date: January 1, 2025

Expiration Date: December 31, 2028

That means taxpayers will be able to claim the deduction for four tax years (2025 through 2028), unless future legislation extends or makes the benefit permanent.

You Don’t Need to Itemize

One of the biggest benefits of this deduction is its accessibility. Unlike many tax breaks that require itemizing, the $6,000 senior deduction can be claimed even if you take the standard deduction—which most retirees already do.

This makes the deduction especially useful for seniors with:

Modest income from Social Security and pensions

Minimal mortgage interest or medical deductions

No longer itemizing after downsizing or paying off a home

Final Thoughts

The $6,000 senior deduction is a meaningful win for retirees—especially those living on fixed incomes who don’t itemize and have limited ways to reduce taxable income. When combined with the standard deduction and age-based additions, older taxpayers will be able to shelter a larger portion of their income from federal taxes for the 2025–2028 window.

As with any temporary tax benefit, timing and planning are key. Whether you're managing RMDs, structuring retirement income, or simply looking for ways to reduce your tax burden, this new deduction should be part of your strategy in the coming years.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What is the new $6,000 senior tax deduction?

Starting in 2025, taxpayers aged 65 and older can claim a new $6,000 federal tax deduction. It reduces taxable income in addition to the standard deduction and the existing age-based deduction. Married couples where both spouses are age 65 or older can claim $12,000 combined.

How does the new senior deduction interact with existing deductions?

The new deduction stacks on top of both the regular standard deduction. This layering can provide meaningful tax relief for retirees who do not itemize.

Who qualifies for the $6,000 senior deduction?

Any taxpayer who is age 65 or older by the end of the tax year qualifies. The deduction applies to all filing statuses but begins to phase out for higher-income individuals.

What are the income phaseout thresholds for the deduction?

The deduction begins to phase out at $75,000 of Modified Adjusted Gross Income (MAGI) for single filers and $125,000 for joint filers. It is reduced by six cents for every $1 of income above these levels and fully phases out at $175,000 for singles and $250,000 for joint filers.

Do you need to itemize to claim the senior deduction?

No. The $6,000 senior deduction is available even if you take the standard deduction. This makes it particularly beneficial for retirees with modest incomes or limited itemized deductions.

When does the new senior tax deduction take effect—and when does it end?

The deduction applies beginning January 1, 2025, and is set to expire after December 31, 2028, unless Congress extends or makes it permanent. Retirees will have four tax years (2025–2028) to take advantage of it.

How can retirees maximize this deduction before it phases out?

Seniors close to the income threshold can use tax planning strategies—such as deferring income, reducing Roth conversions or distributions from pre-tax retirement acounts, or using Qualified Charitable Distributions—to keep MAGI below the phaseout range and preserve the full deduction.

The New $40,000 SALT Cap: What It Means for Taxpayers After the Big Beautiful Tax Bill

Congress just passed the “Big Beautiful Tax Bill,” and one of the biggest changes is a major update to the SALT (State and Local Tax) deduction cap. Instead of being limited to $10,000, some taxpayers will now be eligible for a $40,000 SALT deduction — but only temporarily and only if certain income limits are met.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

After months of negotiation and political tug-of-war, Congress has officially passed what’s being dubbed the “Big Beautiful Tax Bill.” While the legislation covers a broad range of tax reforms, one of the most talked-about provisions is the dramatic change to the SALT (State and Local Tax) deduction cap—raising it from the current $10,000 to a new maximum of $40,000 for some taxpayers. If you’ve felt handcuffed by the old SALT limits, this update could provide much-needed relief—but the details matter.

In this article we will cover:

The effective date of the new $40,000 SALT Cap

Income limitations for single and joint filers

The SALT phaseout calculation

Who benefits the most from the higher SALT Cap?

Do you have to itemize to capture the new SALT Cap?

When the new $40,000 SALT Cap expires

Quick Refresher: What Is the SALT Deduction?

The SALT deduction allows taxpayers who itemize to deduct certain state and local taxes from their federal taxable income. This typically includes:

State and local income taxes

Property taxes paid on real estate

Under the 2017 Tax Cuts and Jobs Act (TCJA), this deduction was capped at $10,000, which hit high-tax states like New York, New Jersey, California, and Massachusetts especially hard. Many taxpayers in those states were no longer able to deduct their full property and income tax payments, resulting in higher federal tax bills.

What’s in the New Bill?

The Big Beautiful Tax Bill raises the SALT cap from $10,000 to $40,000, but with a few catches:

Income limitations apply

The increase applies only to tax years 2025 through 2029.

Starting in 2030, the cap reverts back to $10,000 (unless future legislation says otherwise).

You have to itemize to capture the SALT deduction

So, this is a temporary reprieve—but for many, a meaningful one.

Who Benefits Most?

This new SALT cap will be most beneficial to:

Homeowners in high-tax states (especially those with large property tax bills)

High-income earners who pay significant state income taxes

Taxpayers who itemize deductions (rather than taking the standard deduction)

If you're someone who was paying $25,000–$40,000 in combined state income and property taxes, this change could mean an additional $15,000–$30,000 in deductions, depending on your filing status.

That’s real money back in your pocket—especially if you're in a higher federal tax bracket.

Income Phase‑Outs: Who Gets How Much

While the new SALT cap jump to $40,000 is significant, its benefit isn't universal. There are income limitations for taxpayers based on their modified adjusted gross income.

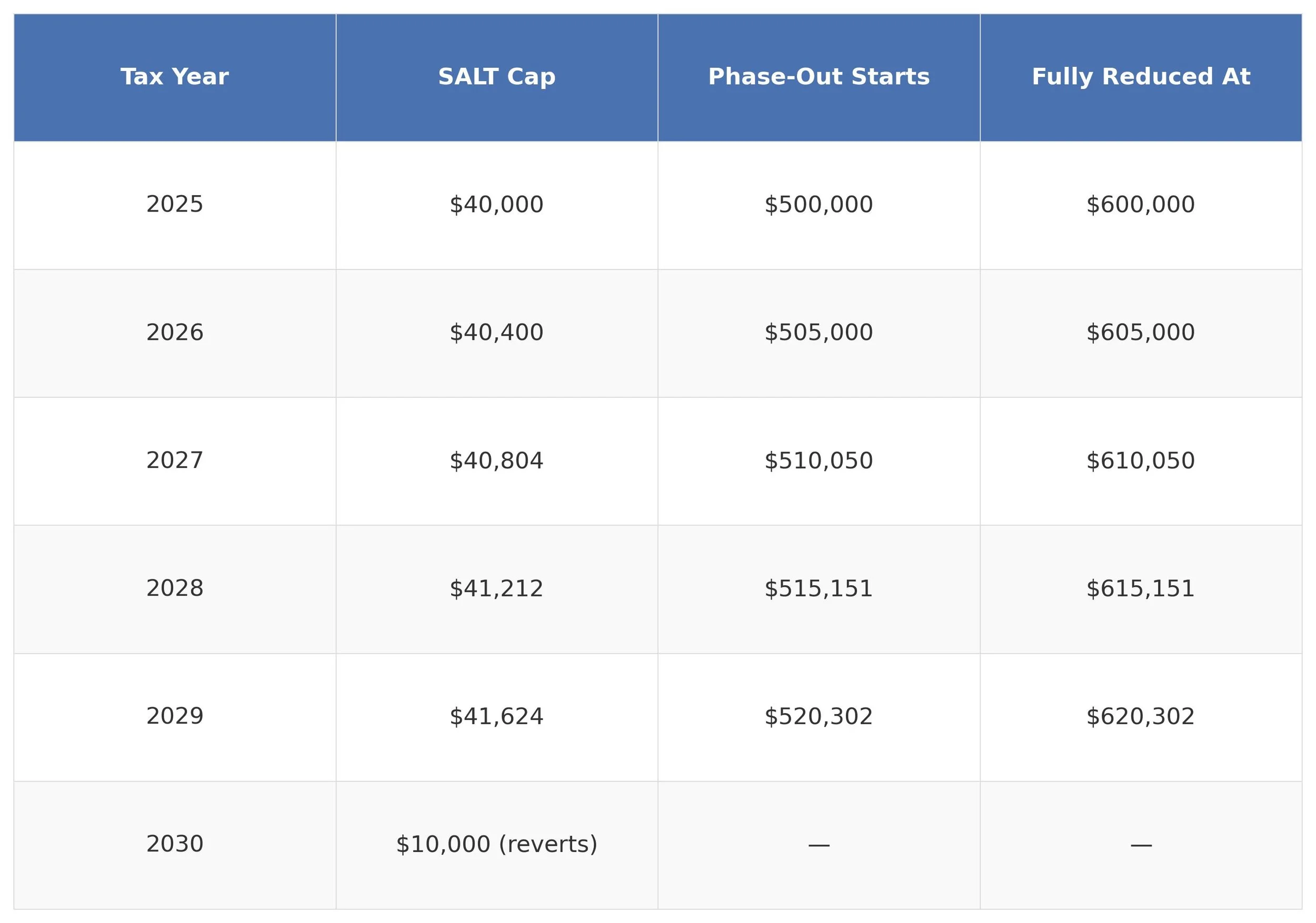

For tax year 2025, the full SALT cap applies to filers with Modified AGI less than $500,000

MAGI between $500,000 and $600,000: The cap is reduced by 30% of the income over $500,000.

Above MAGI $600,000, the cap is back down to $10,000—the same as the old limit.

Starting in 2026, both the cap and phase-out threshold rise 1% per year, with the reductions continuing until 2029. The $10,000 ceiling returns permanently in 2030

How the Phase‑Out Plays Out

Note: The deduction cannot be reduced below the old $10,000

Does Your Tax Filing Status Matter

The MAGI income thresholds are based on “household income” so both single filers and married filing joint filers have the same income limitations and phaseout range for the new $40,000 SALT Cap. However, for taxpayers who file married filing separately, the new max SALT Cap is $20,000.

Tax Planning Opportunities

If you fall into the group of taxpayers who stand to benefit, here are some strategies to consider:

1. Bunching Deductions

With the cap going up temporarily, it may make sense to accelerate state tax payments or property tax prepayments into the eligible years (2025–2029) to maximize the benefit.

2. Reevaluating Itemized vs. Standard Deduction

Many filers defaulted to the standard deduction under TCJA because of the $10,000 SALT cap. But with the cap raised, it’s time to revisit whether itemizing now produces a better tax result.

3. Rethinking Income Timing

If you have control over how and when you recognize income (e.g., through bonuses, deferred comp, self-employment, or retirement distributions), you might explore ways to align higher-income years with the higher SALT cap window.

4. AMT Considerations

While not as widespread as in the past, the Alternative Minimum Tax (AMT) can still limit your ability to take advantage of certain deductions—including SALT. Make sure your tax preparer checks how the new cap interacts with AMT exposure.

Final Thoughts

The new $40,000 SALT cap is a welcome change for many taxpayers who have felt the squeeze over the past few years. But it’s a temporary window of opportunity, and one that requires careful planning to take full advantage of.

If you live in a high-tax state, this change could have a significant impact on your tax strategy moving forward. As always, consult with your financial planner or tax advisor to determine how these changes fit into your overall financial picture.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What is the new $40,000 SALT deduction cap?

Under the Big Beautiful Tax Bill, the State and Local Tax (SALT) deduction cap increases from $10,000 to $40,000 for eligible taxpayers beginning in 2025. The expanded cap applies to combined state income and property taxes but is temporary—set to expire after 2029.

Who benefits most from the higher SALT cap?

The change primarily benefits homeowners and high-income earners in high-tax states such as New York, New Jersey, California, and Massachusetts. Those who pay substantial property and state income taxes and who itemize deductions stand to gain the most.

When does the new $40,000 SALT cap take effect—and when does it expire?

The increased cap is effective for tax years 2025 through 2029. Beginning in 2030, the cap reverts to the previous $10,000 limit unless new legislation extends it.

Are there income limits for the new SALT deduction?

Yes. The full $40,000 cap applies to taxpayers with Modified Adjusted Gross Income (MAGI) under $500,000. Between $500,000 and $600,000, the cap is reduced by 30% of the income over $500,000. Above $600,000 MAGI, the deduction returns to the old $10,000 limit.

Do you need to itemize to use the $40,000 SALT deduction?

Yes. The SALT deduction is only available to taxpayers who itemize deductions on their federal tax return. If you claim the standard deduction, you cannot take advantage of the higher SALT cap.

What tax strategies can help maximize the new SALT deduction?

Taxpayers can “bunch” property or state tax payments into the eligible years (2025–2029), reevaluate whether to itemize, and time income recognition to align with the higher cap window. Consulting a tax professional can help optimize these strategies within IRS guidelines.

Will the Alternative Minimum Tax (AMT) affect the SALT deduction?

It might. The AMT can limit or disallow SALT deductions, depending on your income level and deductions. Taxpayers subject to AMT should review how the new cap interacts with their overall tax situation.

PTET Survives: Why This Pass-Through Entity Tax Loophole Still Matters After Passing of the Big Beautiful Tax Bill

There was a lot of buzz surrounding the “Big Beautiful Tax Bill” recently signed into law, and while most headlines focused on the new $40,000 SALT deduction cap, a quieter but equally important victory came in the form of what didn’t make it into the final bill for the business owners of pass-through entities.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

There was a lot of buzz surrounding the “Big Beautiful Tax Bill” recently signed into law, and while most headlines focused on the new $40,000 SALT deduction cap, a quieter but equally important victory came in the form of what didn’t make it into the final bill for the business owners of pass-through entities.

One major provision originally tucked into the House version of the bill would have eliminated the PTET (Pass-Through Entity Tax) workaround—a popular strategy business owners have been using to bypass the federal $10,000 SALT deduction cap. Thankfully, the Senate stripped that provision from the final legislation, meaning PTET is here to stay—at least for now.

This article will walk through what PTET is, why it still matters (even with a $40,000 cap), and how business owners should think about it in light of the latest tax reform.

What Is PTET?

The Pass-Through Entity Tax (PTET) is a state-level workaround created in response to the federal $10,000 SALT deduction cap introduced under the 2017 Tax Cuts and Jobs Act. Since pass-through entities like S corporations and partnerships don’t pay federal income tax directly, owners report their share of the business income on their personal returns—and thus, their state taxes on that income were limited by the $10,000 SALT cap.

States like New York, New Jersey, California, and over 30 others adopted PTET programs, allowing these businesses to elect to pay state income tax at the entity level. Because entity-level taxes are fully deductible at the federal level, this approach effectively restores the lost deduction for many business owners.

PTET has become one of the most powerful tools for state tax planning, and in many cases, saves owners thousands—or even tens of thousands—of dollars in federal tax liability.

What the House Tried to Do—and What the Senate Undid

In the original House version of the Big Beautiful Tax Bill, lawmakers proposed to eliminate the PTET workaround starting in 2025, citing the new $40,000 SALT cap as sufficient relief. The rationale was that, with a higher cap on SALT deductions, there was no longer a need for a workaround like PTET.

But here’s the catch: the new $40,000 SALT cap is temporary and has income limitations

It only lasts from 2025 through 2029

It phases out for high-income taxpayers (starting at $500,000 AGI and fully phased out at $600,000)

It reverts to $10,000 in 2030, unless Congress intervenes again

Fortunately, the Senate recognized the long-term value and flexibility of PTET, especially for business owners whose income levels could exceed the new cap thresholds. In the final bill, the PTET elimination was removed, preserving the deduction strategy.

Why PTET Still Matters—Even With a $40,000 Cap

Even with the temporary SALT cap increase, PTET remains a valuable planning strategy for three reasons:

1. Not Everyone Qualifies for the Full $40,000 Cap

If your income exceeds $500,000, your benefit from the new SALT cap begins to phase out. At $600,000 or more, it drops back to $10,000—and PTET becomes your best tool for reclaiming that lost deduction.

2. PTET Applies at the Entity Level

Unlike the SALT cap, which applies at the individual level, PTET deductions occur above the line at the business level. That means the full amount paid as state tax by the business is deductible federally, regardless of your personal AGI.

3. Taxpayers May Benefit from BOTH

It’s possible for an owner of a pass-through entity to benefit from both the preservation of the PTET deduction as well as the increased $40,000 SALT Cap, especially for business owners that have high property taxes.

Planning Considerations Moving Forward

If you’re a business owner in a state with an active PTET program, here’s what you should be thinking about:

Continue electing into PTET where beneficial: The deduction is still fully valid under federal law and can provide meaningful savings for those with large state tax liabilities.

Coordinate with your SALT cap usage: While the new $40,000 cap opens opportunities, use both PTET and the SALT cap strategically based on your AGI and other deductions.

Review PTET election timing and payments: Some states require estimated payments or year-end elections. Make sure you're aligned with state-specific rules to lock in the deduction.

And remember—just because the PTET survived this round doesn't mean it's immune to future legislative changes. It’s wise to work with your tax professional to maximize the benefit while it lasts.

Final Thoughts

The survival of the PTET deduction is a major win for business owners who rely on this strategy to manage their federal tax exposure. While the expanded SALT cap helps in the short term, PTET offers a more durable and targeted solution—especially for high earners and pass-through business owners in high-tax states.

As always, tax planning is about playing the long game. The Big Beautiful Tax Bill gave us some new tools—but it also confirmed that tried-and-true strategies like PTET still have a place in the modern tax toolkit.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What is the Pass-Through Entity Tax (PTET)?

The PTET is a state-level workaround that allows S corporations, partnerships, and other pass-through entities to pay state income tax at the business level rather than at the individual level. Because entity-level taxes are fully deductible federally, PTET helps business owners bypass the federal $10,000 SALT deduction cap.

Did the Big Beautiful Tax Bill eliminate PTET?

No. While the House version of the bill originally proposed eliminating PTET starting in 2025, the Senate removed that provision from the final legislation. As a result, PTET remains fully intact under current federal law.

Why does PTET still matter even with the new $40,000 SALT cap?

The new $40,000 SALT cap is temporary (2025–2029) and phases out for taxpayers with income above $500,000. PTET, on the other hand, applies at the entity level, offering a potentially unlimited deduction regardless of the owner’s income. This makes PTET particularly valuable for high earners in high-tax states.

Can business owners use both PTET and the new $40,000 SALT cap?

Yes. It’s possible to benefit from both. Business owners can use PTET to deduct state income taxes paid at the entity level while still itemizing and using the higher $40,000 SALT cap for property taxes or other eligible personal state taxes.

Which states have PTET programs?

More than 30 states—including New York, New Jersey, California, and Illinois—currently offer PTET elections. Rules vary by state, so business owners should review eligibility, election deadlines, and payment timing requirements with their tax professional.

When does the new $40,000 SALT cap expire?

The expanded SALT cap is available for tax years 2025 through 2029 and is scheduled to revert to $10,000 in 2030 unless Congress extends it. PTET remains in effect beyond that date unless future legislation changes it.

What should business owners do next?

Business owners should continue electing PTET where available, coordinate its use with the new SALT cap for optimal tax benefit, and monitor future tax legislation for potential changes. Working closely with a CPA or tax advisor ensures compliance with both federal and state-level PTET rules.