What Happens to an HSA Account When Someone Passes Away?

Health Savings Accounts offer powerful tax benefits, but those benefits can change significantly after death. This article explains how HSAs are treated when inherited by a spouse, non-spouse, or estate. Learn key tax rules, planning strategies, and how to reduce the tax burden on beneficiaries. Proper beneficiary designation is critical to maximizing HSA value.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Health Savings Accounts (HSAs) are one of the most tax-advantaged accounts available, but many people don’t realize that what happens to an HSA after death depends entirely on who the beneficiary is. The tax consequences can be very different depending on whether the beneficiary is a spouse, a non-spouse, or if no beneficiary is named at all.

In this article, we’ll cover:

What happens if a spouse is the beneficiary

What happens if a non-spouse is the beneficiary

What happens if no beneficiary is named

Strategies to reduce taxes on inherited HSAs

Why beneficiary designations are so important

Scenario 1: Spouse Is the Beneficiary

If a spouse is listed as the beneficiary of an HSA, the outcome is very favorable.

When the account owner passes away:

The spouse can assume ownership of the HSA

The transfer of ownership is not taxable

The spouse can continue using the HSA tax-free for qualified medical expenses

If the spouse already has their own HSA, they can roll the inherited HSA into their own HSA

This is the best-case scenario from a tax perspective because the account simply continues as an HSA with all the same tax benefits:

Pre-tax contributions

Tax-deferred growth

Tax-free withdrawals for medical expenses

In other words, the surviving spouse steps into the shoes of the original account owner.

Scenario 2: Non-Spouse Is the Beneficiary

If the beneficiary is not a spouse (for example, a child, grandchild, or friend), the rules change significantly.

When a non-spouse inherits an HSA:

The account ceases to be an HSA as of the date of death

The beneficiary cannot continue the HSA

The beneficiary cannot roll it into their own HSA

The fair market value of the HSA becomes taxable income to the beneficiary in the year of death

This means inheriting an HSA as a non-spouse can create a large immediate tax bill.

How to Reduce the Tax Impact

There is one strategy that can reduce the tax burden:

If the deceased had unpaid medical expenses at the time of death, the HSA can be used to pay those expenses. Any amount used to pay the decedent’s qualified medical expenses reduces the taxable amount that passes to the beneficiary.

Example:

HSA value at death: $50,000

Unpaid medical bills: $10,000

Taxable amount to beneficiary: $40,000

This can make a meaningful difference in the taxes owed.

Scenario 3: No Beneficiary Is Named

If no beneficiary is listed on the HSA:

The HSA becomes part of the deceased person’s estate

The fair market value of the HSA becomes taxable income on the final tax return

The account terminates as an HSA

This is usually the least favorable outcome, which is why it is very important to make sure beneficiaries are properly listed on your HSA account.

Planning Strategy: Should You Spend Your HSA If Your Beneficiaries Are Non-Spouse?

Because HSAs are not very tax-efficient to leave to non-spouse beneficiaries, it may make sense to use the HSA during your lifetime especially if:

You are single, or

Your beneficiaries are children or other non-spouse individuals

Remember, when you use HSA money for medical expenses, those dollars come out tax-free. But if a non-spouse inherits the account, the entire account can become taxable immediately.

After Age 65: Your HSA Works Like a Traditional IRA

Another important rule:

After age 65, you can take money out of an HSA for non-medical expenses and:

You will not pay a penalty

But you will pay ordinary income tax

It works similar to a traditional IRA

This creates a planning opportunity.

If it looks like:

You may not use all your HSA for medical expenses, and

You are in a lower tax bracket

It may make sense to intentionally withdraw money from the HSA and pay the tax at your lower tax rate, instead of leaving the entire account to a non-spouse beneficiary who may have to recognize the entire balance as income in a single year.

This strategy can help reduce the overall family tax bill.

Final Thoughts

HSAs are excellent savings vehicles, but they are not great assets to leave to non-spouse beneficiaries due to the immediate tax consequences.

That’s why good HSA planning includes:

Naming the correct beneficiaries

Using the HSA strategically during your lifetime

Coordinating HSA withdrawals with your tax bracket in retirement

When used properly, an HSA can be a powerful tool for retirement healthcare planning — but like all financial accounts, beneficiary planning matters.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

-

Does an HSA avoid probate?Yes, if a beneficiary is named, the HSA typically passes directly to the beneficiary.

-

Can my spouse continue my HSA after I die?Yes, a spouse can assume ownership of the HSA and continue using it as their own.

-

Do non-spouse beneficiaries pay taxes on inherited HSAs?Yes, the full value of the HSA is taxable income to the beneficiary in the year of death.

-

Can a child roll an inherited HSA into their own HSA?No, non-spouse beneficiaries cannot continue or roll over the HSA.

-

Can HSA funds be used to pay medical bills after death?Yes, HSA funds can be used to pay the deceased person's qualified medical expenses, which reduces the taxable amount to beneficiaries.

-

What happens if I forgot to name a beneficiary?The HSA becomes part of your estate and the value becomes taxable on your final tax return.

-

After age 65, can I use my HSA for non-medical expenses?Yes, you can withdraw funds penalty-free, but you will pay ordinary income tax.

-

Is an HSA a good account to leave to children?Generally, no. Because the account becomes fully taxable to them immediately.

-

Who should be the beneficiary of my HSA?In many cases, naming your spouse as beneficiary is the most tax-efficient option.

-

Should I spend down my HSA before I die?If your beneficiaries are non-spouse beneficiaries, it may make sense to use the HSA during your lifetime to avoid leaving them a large taxable account.

Tax Rules for Selling Your House to a Family Member

Selling a home to a family member involves more than just agreeing on a price. This guide explains tax implications, gift rules, cost basis considerations, and seller financing strategies. Learn how fair market value, the primary residence exclusion, and the Applicable Federal Rate impact your decision. Understand how to structure the transaction to avoid unintended tax consequences. Ideal for parents helping children navigate today’s housing market.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

This article was inspired by a conversation with a client who is considering selling their primary residence to their child. One of the biggest challenges in today’s housing market is affordability for first-time homebuyers. With housing prices and interest rates rising dramatically over the past five years, many parents who were already planning to downsize, relocate, or move into a more retirement-friendly home are now considering selling their home directly to their children to help them afford their first house.

While this can be a great strategy, there are a number of tax rules, gift rules, and financing considerations that need to be understood before entering into an intrafamily real estate transaction. In this article, we’re going to walk through the key areas families should consider before moving forward.

Discounting the Price of the House

One of the most common questions we get from clients is whether they should sell the house to their child at full market value or discount the price.

For example, if a house is worth $600,000, can you sell it to your child for $400,000?

The answer is yes, you can sell your house for whatever price you want. However, if you sell the home significantly below fair market value, the difference between the market value and the sale price may be considered a gift.

So if:

Market value = $600,000

Sale price = $400,000

Difference = $200,000

That $200,000 could be treated as a gift to the child.

For most families, this does not mean you will owe gift tax. However, you may need to file a gift tax return because the gift exceeds the annual gift exclusion. The amount above the annual exclusion simply reduces your lifetime gift exemption, which is currently $15 million per person at the federal level.

Why Selling at Fair Market Value May Be Better

From a tax standpoint, it may actually make more sense to sell the home at full market value rather than at a discount, because of the primary residence capital gain exclusion.

Single filer: Can exclude $250,000 of gain

Married filing jointly: Can exclude $500,000 of gain

Example

Purchase price: $200,000

Current value: $600,000

Gain: $400,000

If the parents are married, the $400,000 gain is below the $500,000 exclusion, meaning they would owe no capital gains tax even if they sell the home for full market value.

But the bigger planning opportunity is actually for the child’s future taxes.

If the child buys the home for $600,000, that becomes their cost basis. If they later sell the home for $1,000,000, their gain is $400,000, which may be fully covered by the primary residence exclusion.

However, if the parents sold the home for $400,000, the child’s cost basis is $400,000. If they later sell for $1,000,000, the gain is $600,000, and $100,000 could become taxable.

So in many situations, a better strategy may be:

Sell the home at fair market value and gift money for the down payment, instead of discounting the purchase price.

This can create a better long-term tax outcome.

Do the Parents Hold the Mortgage?

The next big question is how the child will finance the purchase. There are two main options:

Option 1: Traditional Mortgage

The child gets a mortgage through a bank, and the parents receive cash from the sale.

Option 2: Parents Hold the Mortgage (Seller Financing)

If the parents do not need the cash from the sale, they can hold the mortgage and essentially act as the bank. The child makes mortgage payments directly to the parents.

This is commonly called seller financing or an intrafamily mortgage.

Minimum Interest Rate (AFR)

If parents hold the mortgage, they must charge a minimum interest rate called the Applicable Federal Rate (AFR) to satisfy IRS rules. For a long-term loan such as a mortgage, the long-term AFR applies.

As of March 2026, the long-term AFR is approximately 4.6%.

So the process typically looks like this:

Determine purchase price

Determine down payment

Remaining balance becomes the mortgage

Mortgage must charge at least the AFR rate

Child makes monthly payments to the parents

Tax Treatment of Payments

As the child makes mortgage payments:

The Principal portion is not taxable to the parents

The Interest portion of each payment is taxable income to the parents

Forgiving the Mortgage

Another question that comes up with intrafamily mortgages is:

“Can we forgive payments or forgive the loan later?”

The answer is yes, but this brings us back to the gift rules.

Forgiving Monthly Payments

Let’s say the child’s mortgage payment is $3,000 per month and the parents decide to waive the payments for a year.

That would equal:

$3,000 × 12 = $36,000 per year

If the parents are married, they can gift up to the annual gift exclusion amount each year without filing a gift tax return (for example, $38,000 combined in 2026). If the forgiven amount is below the annual exclusion, no gift tax return is required.

If the forgiven amount exceeds the annual exclusion, then a gift tax return must be filed, but again, no gift tax is owed unless the parents exceed their lifetime exemption.

Forgiving the Entire Mortgage

If the parents decide at some point to forgive the remaining balance of the mortgage, that is considered a gift of the remaining loan balance, and a gift tax return would need to be filed for that year.

This shows that there is actually a lot of flexibility when families use intrafamily mortgages. Payments can be structured, forgiven, or adjusted over time, but the gift rules must be tracked.

Summary

If parents are in the fortunate position where they can sell their home to their child, we are seeing this strategy more and more due to the challenges first-time homebuyers face in today’s housing market.

However, it’s important to understand the key planning areas:

Should you sell at fair market value or discount the price?

Should the child get a traditional mortgage or should the parents hold the mortgage?

What are the Applicable Federal Rate (AFR) rules?

How do the gift tax rules apply if you discount the house or forgive payments?

How does this affect the child’s future cost basis?

How does this fit into the parents’ estate plan?

These transactions involve tax planning, estate planning, and financial planning, so we strongly recommend working with a tax professional and financial advisor when considering an intrafamily real estate transaction.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions

-

Can I sell my house to my child for less than market value?Yes, but the difference may be considered a gift.

-

Do I have to pay gift tax if I sell the house at a discount?Usually no, but you may need to file a gift tax return.

-

Do I pay capital gains tax if I sell to my child?You may qualify for the primary residence capital gain exclusion.

-

Is it better to sell at market value and gift the down payment?In many cases, yes, for long-term tax planning reasons.

-

Can I be the bank for my child’s mortgage?Yes, this is called seller financing.

-

What interest rate do I have to charge?At least the IRS Applicable Federal Rate (AFR).

-

Is the interest my child pays me taxable?Yes, interest is taxable income to the parents.

-

Can I forgive mortgage payments?Yes, but the forgiven amount may be considered a gift.

-

What happens if I forgive the entire loan?It is treated as a gift of the remaining balance.

-

Should we work with a professional for this type of transaction?Yes, you should coordinate with a CPA, financial advisor, and real estate attorney.

In Retirement, What Healthcare Costs Can Be Paid from an HSA Account?

Health Savings Accounts offer tax-free withdrawals for qualified medical expenses in retirement, but understanding eligibility rules is critical. This guide explains which expenses qualify, including Medicare premiums, dental, vision, and out-of-pocket costs. It also covers non-eligible expenses and key withdrawal rules before and after age 65. Use this resource to avoid costly HSA mistakes and maximize your retirement healthcare strategy.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

As people approach retirement, or enter retirement, healthcare costs often become one of the largest expenses in a financial plan. The good news is that Health Savings Accounts (HSAs) can be a powerful tool to help cover many of these costs using tax-free dollars. However, not every healthcare expense qualifies, so it’s important to understand both what can and cannot be paid from an HSA in retirement.

In this article, we’ll cover:

Which Medicare premiums are HSA-eligible

Whether COBRA premiums qualify

Dental, vision, and hearing expenses

Out-of-pocket medical costs

Medical equipment and prescriptions

Expenses that are not HSA-eligible

HSA withdrawal rules before and after age 65

Frequently asked HSA questions in retirement

Medicare Premiums

One of the most common uses for HSA funds in retirement is paying for Medicare premiums. HSA distributions can be used tax-free for:

Medicare Part B premiums

Medicare Part D premiums

Medicare Advantage (Part C) premiums

However, Medigap (Medicare Supplement) premiums are not considered a qualified HSA expense, even though Medicare Advantage plans are. This is a commonly misunderstood rule and an important one for retirees to be aware of when planning healthcare costs.

COBRA Coverage

If you retire before age 65 or leave an employer and elect COBRA coverage, those health insurance premiums can be paid from an HSA. This can be especially helpful for early retirees who need to bridge the gap before Medicare begins.

Dental, Vision, and Hearing Expenses

Dental, vision, and hearing costs are some of the most common out-of-pocket healthcare expenses in retirement — especially since many retirees no longer have employer coverage for these services.

HSA-eligible expenses include:

Dental cleanings, fillings, crowns, dentures, braces, and X-rays

Vision exams, eyeglasses, contact lenses, and LASIK surgery

Hearing aids and hearing aid batteries

Hearing aids alone can cost several thousand dollars, making the HSA a valuable tax-free resource for these expenses.

Out-of-Pocket Medical Expenses

Many routine healthcare costs in retirement are HSA-eligible, including:

Doctor visits

Specialist visits

Hospital services

Co-pays

Deductibles

Coinsurance

Surgery costs

Lab work and imaging

These are often the “everyday” medical expenses retirees experience each year.

Medical Equipment

If medical equipment is needed later in retirement, many of these expenses qualify for HSA distributions, including:

Walkers

Wheelchairs

Blood pressure monitors

Crutches

CPAP machines

Glucose monitors

Prescription Medications

Prescription drugs that are prescribed by a doctor are qualified HSA expenses.

However, over-the-counter medications typically do NOT qualify unless they are prescribed by a physician.

Expenses That Are NOT HSA-Eligible

Some healthcare-related expenses are not considered qualified medical expenses. These typically include:

Gym memberships

Nutritional supplements

Cosmetic procedures

Teeth whitening

General health items not prescribed by a doctor

Even though these may improve health, they are not considered qualified medical expenses under HSA rules.

Why HSAs Are So Powerful for Retirement

HSAs are one of the most tax-advantaged accounts available because they offer:

Tax-deductible contributions

Tax-free growth

Tax-free withdrawals for qualified medical expenses

Because healthcare costs are often highest in retirement, many individuals choose to pay for medical expenses out-of-pocket during their working years and allow their HSA to grow, using it later in retirement when healthcare costs increase.

HSA Withdrawal Rules: Before and After Age 65

It’s also important to understand the rules around HSA withdrawals:

Before age 65

Non-qualified withdrawals = taxable income + 20% penalty

After age 65

Non-qualified withdrawals = taxable income only (no penalty)

Works similar to a Traditional IRA if not used for healthcare

This provides additional flexibility later in retirement.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

-

Can HSA funds be used for Medicare premiums?Yes, for Medicare Part B, Part D, and Medicare Advantage premiums.

-

Can HSA funds be used for Medigap premiums?No, Medigap premiums are not considered a qualified expense.

-

Can I use my HSA for dental expenses in retirement?Yes, most dental expenses qualify.

-

Are vision expenses HSA-eligible?Yes, including exams, glasses, contacts, and LASIK.

-

Are hearing aids covered by an HSA?Yes, including hearing aid batteries.

-

Can I use my HSA for COBRA premiums?Yes, COBRA premiums are a qualified expense.

-

Are prescription drugs HSA-eligible?Yes, if prescribed by a doctor.

-

Are over-the-counter medications HSA-eligible?Typically no, unless prescribed by a physician.

-

What happens if I use HSA money for non-medical expenses before 65?You will owe income tax and a 20% penalty.

-

What happens if I use HSA money for non-medical expenses after 65?You will owe income tax, but no penalty.

Can Anyone Open an HSA Account?

Health Savings Accounts offer powerful tax advantages, but strict eligibility rules apply. This guide explains who can contribute to an HSA in 2026, including HDHP requirements, contribution limits, and Medicare restrictions. Learn how to avoid costly mistakes, especially as you approach age 65. A must-read for retirement-focused healthcare planning.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Health Savings Accounts (HSAs) are one of the most tax-advantaged accounts available and can be a powerful tool for paying healthcare costs in retirement. Contributions are made with pre-tax dollars, the account grows tax-deferred, and distributions are tax-free when used for qualified medical expenses. However, not everyone is eligible to contribute to an HSA, and understanding the eligibility rules is critical.

In this article, we’ll cover:

Who is eligible to contribute to an HSA

What qualifies as a High Deductible Health Plan (HDHP)

2026 HSA contribution limits

Special rules when approaching age 65 and Medicare

Frequently asked questions about HSA eligibility

Who Is Eligible to Contribute to an HSA?

To contribute to an HSA, you must meet all of the following requirements:

You must be enrolled in a High Deductible Health Plan (HDHP)

You cannot be covered by any other non-HDHP health insurance

You cannot be enrolled in Medicare

You cannot be claimed as a dependent on someone else’s tax return

The most common way people become eligible for an HSA is through their employer-sponsored high deductible health insurance plan. If your employer’s health insurance plan is not classified as a high deductible plan, then you are not eligible to contribute to an HSA.

What Qualifies as a High Deductible Health Plan in 2026?

Each year, the IRS defines what qualifies as a High Deductible Health Plan. For 2026, a plan must meet the following minimum deductible and maximum out-of-pocket limits:

If your health insurance plan does not meet these thresholds, it is not considered HSA-eligible, and you cannot contribute to an HSA.

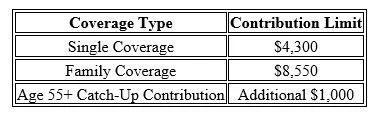

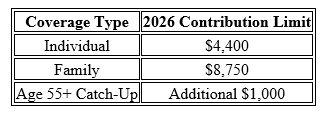

HSA Contribution Limits for 2026

The IRS also sets contribution limits each year. For 2026, the HSA contribution limits are:

These limits include both employee and employer contributions combined. So if your employer contributes to your HSA, that amount counts toward the total annual limit.

Because these limits are indexed for inflation, they typically increase slightly each year.

Be Careful as You Approach Age 65 (Medicare Rule)

There is a very important rule regarding HSAs and Medicare that many people are not aware of:

Once you enroll in Medicare, you can no longer contribute to an HSA.

However, there is an additional rule that affects individuals who work past age 65 and delay Medicare.

The 6-Month Medicare Retroactive Rule

When someone enrolls in Medicare Part A after age 65, Medicare coverage is retroactive for 6 months (but not earlier than age 65).

Because of this:

You must stop HSA contributions 6 months before applying for Medicare

Otherwise, those contributions become excess contributions

Excess contributions can result in tax penalties if not corrected

Example

Let’s say someone is 67, still working, and contributing to an HSA.

If they plan to enroll in Medicare in December, they should stop HSA contributions by June of that year.

If they do not, they may need to withdraw excess contributions and potentially pay penalties.

Important Exception

If you enroll in Medicare right at age 65, you do not need to stop contributions 6 months early because Medicare cannot retroactively start before age 65.

Why HSAs Can Be So Valuable

HSAs are often used as a retirement healthcare savings account because:

Contributions are pre-tax

Growth is tax-deferred

Withdrawals are tax-free for medical expenses

After age 65, withdrawals for non-medical expenses are penalty-free (taxable only)

Because healthcare is often one of the largest expenses in retirement, many individuals choose to save their HSA funds during their working years and use them later in retirement.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

-

Can anyone open an HSA account?No. You must be enrolled in a qualified High Deductible Health Plan.

-

Can I contribute to an HSA if I am self-employed?Yes, as long as you have an HSA-eligible high deductible health insurance plan.

-

Can I contribute to an HSA if I am on Medicare?No. Once enrolled in Medicare, you can no longer contribute.

-

Can my employer contribute to my HSA?Yes, and employer contributions count toward the annual limit.

-

What happens if I contribute to an HSA while on Medicare?Those contributions are considered excess contributions and may be subject to penalties.

-

Can both spouses contribute to an HSA?Yes, if both spouses are eligible and covered by an HSA-qualified plan.

-

Do HSA contribution limits change each year?Yes, they are typically adjusted annually for inflation.

-

What is the catch-up contribution for people over age 55?An additional $1,000 per year.

-

Can I still use my HSA after I go on Medicare?Yes, you just cannot contribute anymore.

-

What happens if I exceed the HSA contribution limit?You may have to withdraw the excess contribution and could owe penalties if not corrected.

4 Reasons Why You Would Not Delay Social Security Benefits to Age 70

The Social Security 50% spousal benefit allows married or divorced individuals to receive up to half of their spouse’s full retirement age benefit. This guide explains eligibility rules, timing strategies, and why delaying benefits may not always maximize household income. Learn how filing decisions affect both spouses and how to coordinate benefits for optimal retirement income. Understanding these rules is essential for building an efficient Social Security strategy.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Many people have heard that the optimal strategy is to delay Social Security benefits until age 70 so that you receive the maximum possible benefit. While that can be true in some situations, there are many scenarios where filing before age 70 may actually make more sense from a financial planning standpoint.

In this article, we’re going to walk through five reasons why you may not want to delay Social Security benefits to age 70, and why the decision should be based on your personal financial situation, health, and retirement goals.

1. Health Concerns and Life Expectancy

The decision to file early or delay Social Security is largely based on longevity. If there are health concerns or a shorter life expectancy, it may make more sense to file earlier rather than later.

While Social Security benefits increase over time, if you delay too long and pass away earlier than expected, you may never make up the years of missed payments.

Example

Let’s say someone is entitled to receive:

$3,000 per month at age 67

If they file at age 62, their benefit is reduced by about 30% to $2,100 per month

By filing at age 62 instead of 67, they would receive:

$2,100 × 12 = $25,200 per year

Over 5 years = $126,000 received before age 67

The question becomes: how long do you have to live for waiting to pay off?

The break-even point is typically somewhere between age 80 and 82.

If you live past 82, delaying often results in more lifetime income

If you pass away before 82, taking benefits earlier often results in more total dollars received

So when there are health concerns or reduced life expectancy, filing earlier can make financial sense.

2. The 50% Spousal Benefit

For married couples, the 50% spousal benefit can significantly impact when the higher-earning spouse should file.

Remember:

The lower-earning spouse can receive their own benefit or 50% of their spouse’s benefit, whichever is higher.

However, the lower-earning spouse cannot receive the spousal benefit until the higher-earning spouse files.

Example

Ken and Tracy:

Ken’s Full Retirement Age benefit: $3,000/month

Tracy’s FRA benefit: $1,000/month

Tracy’s 50% spousal benefit: $1,500/month

If Ken files at 67:

Ken receives $3,000

Tracy receives $1,500

Total household benefit = $4,500/month

If Ken delays until 70:

Tracy can only collect her own $1,000 until Ken files

She must wait 3 years before increasing to $1,500

The spousal benefit does not increase based on Ken waiting until 70

So when there is a large gap between the lower-earning spouse’s benefit and the spousal benefit, it can often make sense for the higher-earning spouse to file before age 70 to unlock the spousal benefit earlier.

3. You Need the Income to Retire

Sometimes the decision is simple: you need the income to retire.

Many individuals plan to retire at 62, 65, or 67, and Social Security is a key part of their retirement income plan along with pensions, investments, or other income sources.

If delaying Social Security to age 70 means:

You have to continue working longer than you want, or

You have to withdraw heavily from retirement accounts early,

Then filing earlier may be the better decision because it allows you to retire when you want while maintaining your lifestyle.

In other words, Social Security is not always about maximizing the monthly benefit — sometimes it’s about making retirement possible.

4. Delaying Withdrawals from Investment Accounts

Another reason someone may file earlier is to preserve their investment accounts.

Here’s the math:

Social Security increases about 6% per year before full retirement age

Social Security increases about 8% per year from full retirement age to age 70

If someone has investment accounts that are earning more than 6–8% per year, it may make sense to:

Turn on Social Security earlier

Use Social Security income

Allow investment accounts to continue growing

However, this is not a perfect apples-to-apples comparison because:

Social Security increases are guaranteed

Investment returns are not guaranteed and require market risk

But in strong market environments or for aggressive investors, this strategy can sometimes make sense.

Summary

While delaying Social Security until age 70 can increase your monthly benefit, it is not always the best financial decision. The right decision depends on:

Health and life expectancy

Spousal benefits

Retirement income needs

Investment returns

Estate planning goals

Social Security decisions should be made as part of a full retirement income plan, not in isolation.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions

-

Is age 70 always the best age to take Social Security?No. Age 70 provides the highest monthly benefit, but not always the highest lifetime benefit.

-

What is the Social Security break-even age?Typically between age 80 and 82.

-

When should I take Social Security if I have health issues?Filing earlier may make sense if life expectancy is shorter.

-

How does the spousal benefit affect when we should file?The higher-earning spouse filing earlier may allow the lower-earning spouse to collect a larger spousal benefit sooner.

-

Does Social Security increase every year I wait?Yes, roughly 6% per year before full retirement age and 8% per year after full retirement age until age 70.

-

Should I take Social Security early to preserve my investments?In some cases, yes - especially if your investments are growing faster than the Social Security increase.

-

What happens to my Social Security when I die?Your spouse may be eligible for a survivor benefit equal to your benefit.

-

Can I work and still collect Social Security?Yes, but if you collect before full retirement age, there may be an earnings limit.

-

Is Social Security taxable?Yes, depending on your total income, up to 85% of your Social Security may be taxable at the Federal level.

-

Should I talk to a financial advisor before filing for Social Security?Yes. The timing decision can impact hundreds of thousands of dollars over your lifetime.

Health Savings Account Distribution Tax and Penalty Rules

Health Savings Account (HSA) withdrawals have different tax and penalty rules depending on age and how funds are used. This guide explains the four distribution scenarios, tax treatment before and after age 65, and advanced strategies to maximize tax-free benefits. Learn how HSAs can serve as a powerful retirement healthcare tool and how to avoid common withdrawal mistakes. Ideal for pre-retirees planning tax-efficient income strategies.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Health Savings Accounts (HSAs) are one of the most tax-advantaged accounts available, but the tax treatment of distributions depends on how the money is used and the age of the account owner. There are essentially four different distribution scenarios that HSA owners can run into, and each scenario has different tax and penalty rules that are important to understand.

In this article, we’ll cover:

The four HSA distribution scenarios

Tax treatment before age 65

Tax treatment after age 65

Why HSAs are so valuable for retirement planning

Advanced HSA distribution strategies

Common HSA distribution mistakes to avoid

Frequently asked questions about HSA distributions

Why HSA Accounts Are So Valuable

Health Savings Accounts are unique because they offer a rare triple tax advantage:

Contributions are made pre-tax

The account grows tax-deferred

Distributions are tax-free if used for qualified medical expenses

Very few accounts receive this type of tax treatment. Traditional retirement accounts are tax-deferred, and Roth accounts are tax-free on the way out, but HSAs can be tax-free on both the contribution and distribution side when used correctly.

Because of this, many financial planners recommend not spending HSA funds during working years if possible, and instead allowing the account to grow and using it later in retirement when healthcare costs are typically much higher.

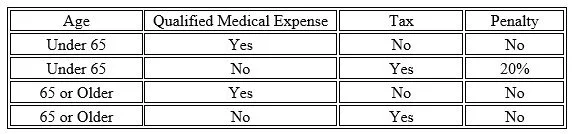

The Four HSA Distribution Scenarios

There are four main distribution scenarios that determine whether you owe taxes and/or penalties on HSA withdrawals:

Let’s walk through each scenario.

Distributions Prior to Age 65 (Qualified Medical Expenses)

If you take a distribution from an HSA before age 65 and use the money for a qualified medical expense, the distribution is:

Tax-free

Penalty-free

This is the ideal use of an HSA. Qualified expenses can include:

Doctor visits

Deductibles and coinsurance

Dental and vision care

Hearing aids

Prescription medications

Medicare premiums (after age 65)

Medical equipment

In these cases, the HSA functions exactly as intended — a tax-free healthcare account.

Distributions Prior to Age 65 (Non-Qualified Expenses)

If you take a distribution before age 65 and the expense is not qualified, the distribution is:

Subject to ordinary income tax

Subject to a 20% penalty

For example, if someone is in a 30% tax bracket and takes a non-qualified distribution:

30% tax

20% penalty

Total loss = 50% of the distribution

This is why it is usually recommended to preserve HSA funds for medical expenses whenever possible.

Distributions Age 65 or Older (Qualified Medical Expenses)

This scenario works the same as before age 65.

If the distribution is used for qualified medical expenses, the withdrawal is:

Tax-free

Penalty-free

This is why HSAs are often used as a retirement healthcare fund.

Common qualified expenses in retirement include:

Medicare Part B premiums

Medicare Part D premiums

Medicare Advantage premiums

Out-of-pocket medical expenses

Deductibles and coinsurance

Dental and vision care

Hearing aids

Medical equipment

Distributions Age 65 or Older (Non-Qualified Expenses)

This is where the rules change.

After age 65, if you take money from an HSA for non-qualified expenses:

You pay ordinary income tax

No 20% penalty

At this point, the HSA starts to function similarly to a Traditional IRA. The money can be used for anything, but it becomes taxable income if not used for medical expenses.

This provides flexibility in retirement in case the funds are needed for non-medical expenses.

Important Rule: Reimbursed Expenses Do NOT Qualify

One important rule that retirees need to be aware of:

If a medical expense is reimbursed by insurance or a former employer, you cannot also take a tax-free HSA distribution for that same expense.

For example:

Some retirees have employer retiree health plans that reimburse Medicare premiums.

If the retiree is reimbursed for Medicare Part B or Part D, those expenses cannot also be reimbursed from the HSA tax-free.

This would be considered a non-qualified distribution, and taxes would apply.

Advanced HSA Distribution Strategies

There are several advanced strategies that can make HSAs even more powerful:

1. Save Receipts and Reimburse Yourself Later

There is no time limit on when you reimburse yourself from an HSA for a qualified expense, as long as:

The expense occurred after the HSA was established

You kept the receipt

This means someone could:

Pay medical expenses out-of-pocket during working years

Allow the HSA to grow

Reimburse themselves years later tax-free

This effectively turns the HSA into a tax-free retirement account.

2. Use HSA for Medicare Premiums

HSA funds can be used tax-free for:

Medicare Part B

Medicare Part D

Medicare Advantage

(This becomes a built-in retirement healthcare fund.)

3. Treat HSA Like a Backup Traditional IRA

After age 65, if needed, HSA funds can be withdrawn for non-medical expenses and simply taxed as income, with no penalty.

Common HSA Distribution Mistakes

Some of the most common mistakes include:

Using HSA funds for non-qualified expenses before 65

Losing receipts for reimbursement

Using HSA funds for reimbursed expenses

Spending HSA funds during working years instead of investing them

Not investing HSA funds for long-term growth

Forgetting that non-qualified withdrawals before 65 have a 20% penalty

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

-

Do I pay taxes on HSA distributions?Only if the distribution is used for a non-qualified expense.

-

What is the penalty for non-qualified HSA withdrawals before age 65?A 20% penalty plus ordinary income tax.

-

What happens to the penalty after age 65?The 20% penalty goes away, but distributions are still taxable if not used for medical expenses.

-

Can I use my HSA for Medicare premiums?Yes, for Medicare Part B, Part D, and Medicare Advantage.

-

Can I reimburse myself years later from my HSA?Yes, as long as the expense occurred after the HSA was established and you kept the receipt.

-

Are HSA distributions reported on a tax return?Yes, distributions are reported on IRS Form 8889.

-

Can I use my HSA for my spouse's medical expenses?Yes, even if your spouse is not on your health insurance plan.

-

What happens to my HSA when I turn 65?You can still use it tax-free for medical expenses, and penalty-free for non-medical expenses (taxable).

-

Can I use my HSA for dental and vision expenses?Yes, most dental and vision expenses qualify.

-

Is an HSA better than a 401(k)?For medical expenses, an HSA can be more tax-efficient because it is tax-free on both contributions and qualified distributions.

Should You Spend or Save Your HSA Account?

Health Savings Accounts offer a unique triple tax advantage, making them one of the most powerful retirement planning tools available. This article explains when to spend versus save your HSA, how to invest it for long-term growth, and how it can be used for healthcare costs in retirement. You’ll also learn the 2026 HSA contribution limits and strategies to maximize your account’s value. Understanding how to use your HSA properly can significantly improve retirement income planning and reduce future medical expenses.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Health Savings Accounts (HSAs) are one of the most tax-advantaged accounts available, yet many people still wonder whether they should use the HSA now for medical expenses or save it for retirement. The answer depends on your financial situation, but in many cases, saving your HSA for the future can provide significant long-term benefits.

In this article, you’ll learn:

How HSAs receive triple tax advantages

When it makes sense to spend vs. save your HSA

How HSAs can be used for healthcare expenses in retirement

Why investing your HSA can dramatically increase its value

2026 HSA contribution limits

A real-life example showing long-term HSA growth

A hybrid strategy that works for many households

Understanding the Triple Tax Advantage of an HSA

HSAs are unique because they offer what is often called a triple tax benefit:

Contributions are made pre-tax

The money grows tax-deferred

Withdrawals are tax-free if used for qualified medical expenses

Very few accounts offer this type of tax treatment. Traditional retirement accounts are tax-deferred, Roth accounts are tax-free on withdrawal, but HSAs offer both benefits — which is why many financial planners consider HSAs one of the most powerful long-term savings tools available.

Should You Spend or Save Your HSA?

The original purpose of an HSA was to pay for current medical expenses with pre-tax dollars. However, a larger planning opportunity exists:

If you can afford to pay medical expenses out-of-pocket today, it may make sense to leave your HSA invested and growing for retirement.

Why? Because healthcare costs tend to increase significantly as we age, especially in retirement. Having a dedicated account for healthcare expenses reduces the risk that large medical costs will disrupt your retirement income plan.

What Can HSAs Be Used for in Retirement?

Many people don’t realize how many retirement healthcare expenses can be paid from an HSA, including:

Medicare Part B premiums

Medicare Part D premiums

Medicare Advantage premiums

Dental expenses

Vision expenses

Hearing aids

Long-term care insurance premiums (within limits)

Medical equipment (wheelchairs, walkers, etc.)

Deductibles and copays

Prescription medications

Because these expenses can be paid tax-free from an HSA, it effectively makes those healthcare costs tax deductible in retirement.

2026 HSA Contribution Limits

For 2026, the IRS increased HSA contribution limits:

These limits include both employee and employer contributions combined.

The Power of Investing Your HSA

If you plan to use your HSA more than 5 years in the future, it often makes sense to invest the HSA rather than leaving it in cash or a money market account. The reason is simple: compound interest.

Example:

If you are age 40, contribute $4,000 per year, and earn 8% annually, by age 62 your HSA could grow to approximately:

Total account value: $243,000

Total contributions: $92,000

Investment growth: $151,000

In this example, most of the account value came from investment growth, not contributions. That is the real power of using an HSA as a long-term healthcare investment account.

Not All HSA Providers Allow Investing

Some HSAs only allow cash savings, while others allow full investment access similar to a retirement account. Some popular HSA providers that offer investment options include:

Fidelity Investments

Charles Schwab

HealthEquity

If your HSA is through your employer, it often makes sense to:

Contribute through payroll to capture tax benefits

Then periodically transfer funds to an HSA provider with investment options

This strategy allows you to get the best of both worlds — tax savings and investment growth.

A Hybrid Strategy May Work Best

Not everyone can afford to pay medical expenses out-of-pocket. That’s where a hybrid strategy can work well:

Use your HSA for large medical expenses

Pay smaller expenses out-of-pocket when possible

Try to preserve and invest as much of the HSA as possible for retirement

This approach balances current needs with long-term planning.

Final Thoughts

Healthcare is one of the largest expenses in retirement. Having a dedicated, tax-free account to pay for those costs can significantly improve retirement security. For many individuals, the HSA becomes less of a short-term spending account and more of a long-term healthcare retirement account.

If used strategically, an HSA can become a healthcare safety net, helping reduce the financial risk of rising medical costs later in life.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

-

Should I max out my HSA every year?If you can afford to, many financial planners recommend maxing out your HSA due to the triple tax advantage.

-

Is an HSA better than a 401(k)?They serve different purposes, but an HSA often has better tax treatment if used for medical expenses.

-

Can I use my HSA for Medicare premiums?Yes, you can use HSA funds for Medicare Part B, Part D, and Medicare Advantage premiums.

-

Can I invest my HSA?Yes, but only if your HSA provider allows investment options.

-

What happens if I use HSA money for non-medical expenses?Before age 65, you pay income tax plus a 20% penalty. After age 65, you only pay income tax.

-

Do HSA funds expire?No. HSA funds roll over every year and stay with you for life.

-

Can I reimburse myself later for medical expenses?Yes. As long as you kept the receipt, you can reimburse yourself years later.

-

Should I invest my HSA or keep it in cash?If the money won't be used for several years, investing often makes sense due to compound growth.

-

Can I have more than one HSA account?Yes. You can contribute to one and transfer to another.

-

What is the biggest benefit of an HSA?The triple tax advantage: pre-tax contributions, tax-deferred growth, and tax-free withdrawals for medical expenses.

College Savings or Retirement First? How to Decide in 2026

Should you save for your child’s college or your own retirement first? It’s one of the most common questions we hear from families trying to balance competing financial goals. Our analysis at Greenbush Financial Group shows that in most cases, prioritizing retirement creates greater long-term security—while still leaving room to build meaningful college savings over time. This guide explains why the order matters, how 529 plans fit in, and how to create a balanced strategy that protects both your future and your child’s opportunities.

One of the most common financial planning questions we hear at Greenbush Financial Group is whether to prioritize saving for your children’s college or for your own retirement. Both goals are important—but when resources are limited, the right order can make a major difference in your long-term security. In most cases, it makes sense to secure your retirement first, then allocate additional savings toward education goals. Here’s why that order matters and how to balance both effectively.

Why Retirement Comes First

Retirement should almost always take priority for one simple reason: there are no loans for retirement. Your future financial independence depends on your ability to replace your income when you stop working—and that window to save is limited.

Key Reasons to Prioritize Retirement

You can’t borrow for it. Your children can access student loans, grants, or scholarships; you cannot do the same for retirement income.

Compounding works best early. The earlier you contribute to retirement accounts like a 401(k) or IRA, the more time your investments have to grow tax-deferred or tax-free.

Employer matches add free money. If you skip retirement contributions to fund college, you may also miss out on employer matching contributions that could increase your savings rate.

Tax advantages are stronger. Retirement accounts typically offer better tax deferral and protection benefits than education accounts.

The Case for Funding College Early

While retirement usually takes priority, it’s also important to plan for education costs strategically. A balanced approach can help you avoid high student loan debt while still protecting your own future.

Benefits of Starting College Savings Early

Tax-free growth. 529 plans grow tax-free and withdrawals are tax-exempt when used for qualified education expenses.

High contribution limits. You can contribute up to $19,000 per year per parent ($38,000 for married couples) in 2026 without triggering the gift tax, and you can front-load five years’ worth at once.

State tax benefits. Many states offer income tax deductions or credits for 529 plan contributions.

Investment flexibility. Funds can be used for tuition, room and board, and even graduate school.

For families with younger children, consistent 529 contributions—even modest ones—can grow meaningfully over 15–18 years while you continue building your retirement savings.

Balancing Both Goals

It doesn’t have to be all-or-nothing. You can take a blended approach:

Maximize employer match in your 401(k) or SIMPLE IRA first.

Open a 529 plan and set up automatic contributions (even $100 per month makes a difference).

Reevaluate each year—as income rises, you can shift additional funds toward college savings.

Use windfalls wisely. Bonuses, tax refunds, or side-income can go toward education savings without disrupting retirement.

Encourage student participation. Teen jobs, scholarships, or community college for core credits can reduce overall cost.

At Greenbush Financial Group, we often model side-by-side scenarios showing how redirecting amounts from retirement to college savings can alter your future income security.

How Retirement Savings Can Help with College

One overlooked advantage: saving for retirement can indirectly help with college funding.

Lower FAFSA impact: Retirement assets aren’t counted toward federal financial aid formulas, while 529 balances are.

Penalty-free withdrawals: The IRS allows penalty-free (but taxable) withdrawals from IRAs for qualified education expenses if needed later.

Future flexibility: A strong retirement foundation may let parents help pay off loans later without jeopardizing their future.

Action Steps to Get Started

Review your retirement contribution rate and increase it until you reach your employer’s match or target savings goal.

Set up a 529 plan for each child, even if contributions start small.

Reassess annually as college costs and retirement targets evolve.

Meet with a financial planner to model the long-term trade-offs of different savings rates.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

FAQs: College Savings vs. Retirement

-

Should I ever prioritize college savings over retirement?Only if your retirement plan is fully funded or you’re on track with a strong pension. Otherwise, we believe that your future security should come first.

-

Can I use my IRA for college expenses?Yes, you can withdraw IRA funds penalty-free (though taxable) for qualified higher education costs, but this should often be a last resort.

-

How much should I contribute to a 529 plan?Many families aim for about one-third of projected costs; the rest can come from cash flow, aid, or loans. Even small, consistent contributions grow substantially over time.

-

What if I can’t afford both?Focus on retirement first. You could potentially help your child repay loans later, but you can’t finance your own retirement.

-

Are there other college savings options besides 529s?Yes—Coverdell ESAs and custodial UGMA/UTMA accounts can also be used, though they have different tax and financial aid impacts.